Financial Resources and Decisions Report: Clariton Antiques

VerifiedAdded on 2019/12/18

|20

|5117

|173

Report

AI Summary

This report provides a comprehensive analysis of financial resources and decision-making for Clariton Antiques Ltd, an unincorporated business. It begins by exploring internal and external sources of finance, including owner capital, business loans, retained earnings, and equity shares, along with their implications. The report then delves into the costs associated with different financial sources, such as interest, dividends, and taxes, and emphasizes the significance of financial planning, including budgeting and economic forecasting. The information required for effective decision-making by partners, venture capitalists, and finance brokers is detailed. Furthermore, the impact of financial sources on accounting statements is examined, followed by an overview of cash budgeting, unit cost and pricing decisions, and investment decisions using NPV, ARR, and payback period calculations. Finally, the report analyzes the key components of financial statements, financial formats for sole traders and partnerships, and a comparison of financial ratios to assess Clariton's financial performance.

Managing Financial Resources and

Decisions

Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................4

Task 1..........................................................................................................................................................4

1.1 Sources of finance.............................................................................................................................4

1.2 Implications of financial sources........................................................................................................5

1.3 Appropriate source of finance............................................................................................................6

Task 2..........................................................................................................................................................6

2.1 Cost of financial sources....................................................................................................................6

2.2 Financial planning and its significance..............................................................................................7

2.3 Information requires to make effective decision................................................................................8

2.4 Impact of financial sources on accounting statements.......................................................................9

Task 3..........................................................................................................................................................9

3.1 Cash budget.......................................................................................................................................9

3.2 Unit cost and pricing decisions........................................................................................................11

3.3 Investment decisions........................................................................................................................12

Task 4........................................................................................................................................................14

4.1 Key components of financial statements..........................................................................................14

4.2 Financial formats for sole traders and partnership firm...................................................................15

4.3 Comparison of financial ratios.........................................................................................................15

Conclusion.................................................................................................................................................18

References.................................................................................................................................................19

Introduction.................................................................................................................................................4

Task 1..........................................................................................................................................................4

1.1 Sources of finance.............................................................................................................................4

1.2 Implications of financial sources........................................................................................................5

1.3 Appropriate source of finance............................................................................................................6

Task 2..........................................................................................................................................................6

2.1 Cost of financial sources....................................................................................................................6

2.2 Financial planning and its significance..............................................................................................7

2.3 Information requires to make effective decision................................................................................8

2.4 Impact of financial sources on accounting statements.......................................................................9

Task 3..........................................................................................................................................................9

3.1 Cash budget.......................................................................................................................................9

3.2 Unit cost and pricing decisions........................................................................................................11

3.3 Investment decisions........................................................................................................................12

Task 4........................................................................................................................................................14

4.1 Key components of financial statements..........................................................................................14

4.2 Financial formats for sole traders and partnership firm...................................................................15

4.3 Comparison of financial ratios.........................................................................................................15

Conclusion.................................................................................................................................................18

References.................................................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Financial management is the planning and monitoring tool through which an entity can

make effective control over its monitory resources. It support in taking such decisions which

can maximize the value of organizations. Management of economic activities assist in selecting

effective source of finance otherwise entities can expose to higher risk. Current assignment is

based on Clariton Antiques Ltd, it is an unincorporated business which is founded by four

partners. Report will discuss the internal and external sources of finance and their implications

on business (Herzallah, Gutiérrez-Gutiérrez and Munoz Rosas, 2014). Cost of several sources

will be discussed and impact of sources will be illustrated in the study. In addition to this

calculations of NPV, ARR and pay back period will be done for making investment decision. At

the end of report financial performance of Clariton will be analyzed.

Task 1

1.1 Sources of finance

Selection of appropriate source can protect firms from suffering higher risk (Newman, Borgia

and Deng, 2013). Raising money for earning higher profit is difficult task. Sufficient funds can

support in running business smoothly.

a) Unincorporated business

These are commercial enterprises which are ruled by owner of partners. As such type of entities

have not been granted corporate status, so owner is responsible for debts of the company.

Sources of finance for such type of business are as following:

Owner or partner capital: Clariton is the partnership firm, there are four partners in the

organization and all of them are having equal rights in the organization (Infelise, 2014). Cited

firm is aiming to raise its funds for further development for that all partners can invest their

capital in the business. For increasing cash inflow they can introduce one more partner in it. As

new person will also invest own capital in entity that would help in raising funds.

Business loan: It is another available source of finance for unincorporated businesses, they can

take support of financial institutions. Bank charges interest and grand loan to start up firms sot

that they can run their operations well (Huang, Rice and Martin, 2015).

b) Incorporated business

Financial management is the planning and monitoring tool through which an entity can

make effective control over its monitory resources. It support in taking such decisions which

can maximize the value of organizations. Management of economic activities assist in selecting

effective source of finance otherwise entities can expose to higher risk. Current assignment is

based on Clariton Antiques Ltd, it is an unincorporated business which is founded by four

partners. Report will discuss the internal and external sources of finance and their implications

on business (Herzallah, Gutiérrez-Gutiérrez and Munoz Rosas, 2014). Cost of several sources

will be discussed and impact of sources will be illustrated in the study. In addition to this

calculations of NPV, ARR and pay back period will be done for making investment decision. At

the end of report financial performance of Clariton will be analyzed.

Task 1

1.1 Sources of finance

Selection of appropriate source can protect firms from suffering higher risk (Newman, Borgia

and Deng, 2013). Raising money for earning higher profit is difficult task. Sufficient funds can

support in running business smoothly.

a) Unincorporated business

These are commercial enterprises which are ruled by owner of partners. As such type of entities

have not been granted corporate status, so owner is responsible for debts of the company.

Sources of finance for such type of business are as following:

Owner or partner capital: Clariton is the partnership firm, there are four partners in the

organization and all of them are having equal rights in the organization (Infelise, 2014). Cited

firm is aiming to raise its funds for further development for that all partners can invest their

capital in the business. For increasing cash inflow they can introduce one more partner in it. As

new person will also invest own capital in entity that would help in raising funds.

Business loan: It is another available source of finance for unincorporated businesses, they can

take support of financial institutions. Bank charges interest and grand loan to start up firms sot

that they can run their operations well (Huang, Rice and Martin, 2015).

b) Incorporated business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These are those firms which are having corporate status and they are legally registered

companies. Owner has benefit of limited liability as if corporation defaults to earn profit then

owner needs not to use personal assets for repayment of debts. Sources of finance available for

incorporated firms are as below:

Retained Earning: It is the amount of profit which is retained by the business for further

development. Many start up businesses like Clariton believes that it does not have economic

cost so it is effective source of finance (Tsai, 2015). It avoids the situation of loosing controlling

power so most of the organizations opt this source of finance.

Equity share: Corporations can issue equity shares in public for raising funds. It can enhance

brand name of the company. Ownership gets transferred and person becomes equity holder in

the organization (Mancusi and Vezzulli, 2014).

1.2 Implications of financial sources

a) Internal sources

Many times due to heavy costs of external sources, organizations prefer to use internal funds for

development of the company.

Sales of assets: It is one of the common source of finance which can help in raising

capital of the company. Clariton can use this source and sales its tangible assets in

market. This money is not necessary to be paid by the cited firm so no economic

implication is here. But for selling assets they have to follow legal guideline and have to

make a legal contract between purchaser and seller. That is legal implication of sales of

assets (Avdeitchikova and Landström, 2016). No possession cost is associated with it so

controlling remain in the same hands, no need to share it.

Retained Earning: It is retained part of profit of the organization so can be used in the

business operations. No economic, legal and possession cost is associated with this

source of finance. This is own profit so no one will ask for repayment.

b) External sources

Some time due to requirement of large funds, entities collect money from external sources.

Implications of these sources are as below:

Bank loan: It is appropriate financial source and can raise capital of the company. As if

Clariton goes with this source then it will have to make legal contract with bank this

companies. Owner has benefit of limited liability as if corporation defaults to earn profit then

owner needs not to use personal assets for repayment of debts. Sources of finance available for

incorporated firms are as below:

Retained Earning: It is the amount of profit which is retained by the business for further

development. Many start up businesses like Clariton believes that it does not have economic

cost so it is effective source of finance (Tsai, 2015). It avoids the situation of loosing controlling

power so most of the organizations opt this source of finance.

Equity share: Corporations can issue equity shares in public for raising funds. It can enhance

brand name of the company. Ownership gets transferred and person becomes equity holder in

the organization (Mancusi and Vezzulli, 2014).

1.2 Implications of financial sources

a) Internal sources

Many times due to heavy costs of external sources, organizations prefer to use internal funds for

development of the company.

Sales of assets: It is one of the common source of finance which can help in raising

capital of the company. Clariton can use this source and sales its tangible assets in

market. This money is not necessary to be paid by the cited firm so no economic

implication is here. But for selling assets they have to follow legal guideline and have to

make a legal contract between purchaser and seller. That is legal implication of sales of

assets (Avdeitchikova and Landström, 2016). No possession cost is associated with it so

controlling remain in the same hands, no need to share it.

Retained Earning: It is retained part of profit of the organization so can be used in the

business operations. No economic, legal and possession cost is associated with this

source of finance. This is own profit so no one will ask for repayment.

b) External sources

Some time due to requirement of large funds, entities collect money from external sources.

Implications of these sources are as below:

Bank loan: It is appropriate financial source and can raise capital of the company. As if

Clariton goes with this source then it will have to make legal contract with bank this

legal consequences are implications of this source. Interest cost is associated with it that

can increase economic burden of Clariton. But ownership and power need not to be

shared with others (Abascal, Alonso and Pacheco, 2015).

Venture capitalist: Cited firm can make connection with big investors those who invest

large amount in start up entities. As they have to involve them in business decision and

have to give them power so ownership gets diluted. Apart from this dividend cost is

economic implication of this source. Legal agreement form between owner and investor

as both have to follow laws and conditions of the contract.

1.3 Appropriate source of finance

Cariton is new to this industry, for meeting competition and to achieve its objective of

opening new branch, cited firm is required a lots of funds. But it is necessary to calculate cost of

each source then they have to make their decisions. Bank loan can be suggested as most

appropriate financial source, I can fulfill monitory needs of the company easily (Boyer and

Blazy, 2014). Interest rates of business loans are nominal and repayment is also easy. Banks

grants loan to such type of entities quickly by looking upon their growth and market reputation.

Though long term liability can get increased but with the help of this Clartion can easily meet

its objectives.

Retained earning can also be suggested as good source of finance for Clariton Antiques

Ltd. As it does not create financial burden on the firm so it is good and can give higher return to

the cited firm. Partners can take their decisions easily, they need not to involve outsiders like

investors in the business decisions (Hossain and Kauranen, 2016).

Task 2

2.1 Cost of financial sources

For running business smoothly, organizations are required to have sufficient monitory

resources. But their cost has to be beard by the firms. For instance if entity raise money by

investors then possession cost and dividend cost are associated with it. Equity shares are result

oriented tools or source but owner has to share ownership with the equity holders. Same as

Clariton can choose venture capitalist, “We finance limited” has approached to cited firm. But

company is demanding 20%stake that can create financial burden on the organization

can increase economic burden of Clariton. But ownership and power need not to be

shared with others (Abascal, Alonso and Pacheco, 2015).

Venture capitalist: Cited firm can make connection with big investors those who invest

large amount in start up entities. As they have to involve them in business decision and

have to give them power so ownership gets diluted. Apart from this dividend cost is

economic implication of this source. Legal agreement form between owner and investor

as both have to follow laws and conditions of the contract.

1.3 Appropriate source of finance

Cariton is new to this industry, for meeting competition and to achieve its objective of

opening new branch, cited firm is required a lots of funds. But it is necessary to calculate cost of

each source then they have to make their decisions. Bank loan can be suggested as most

appropriate financial source, I can fulfill monitory needs of the company easily (Boyer and

Blazy, 2014). Interest rates of business loans are nominal and repayment is also easy. Banks

grants loan to such type of entities quickly by looking upon their growth and market reputation.

Though long term liability can get increased but with the help of this Clartion can easily meet

its objectives.

Retained earning can also be suggested as good source of finance for Clariton Antiques

Ltd. As it does not create financial burden on the firm so it is good and can give higher return to

the cited firm. Partners can take their decisions easily, they need not to involve outsiders like

investors in the business decisions (Hossain and Kauranen, 2016).

Task 2

2.1 Cost of financial sources

For running business smoothly, organizations are required to have sufficient monitory

resources. But their cost has to be beard by the firms. For instance if entity raise money by

investors then possession cost and dividend cost are associated with it. Equity shares are result

oriented tools or source but owner has to share ownership with the equity holders. Same as

Clariton can choose venture capitalist, “We finance limited” has approached to cited firm. But

company is demanding 20%stake that can create financial burden on the organization

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Jindrichovska, 2013). Finance brokers charge commissions that is another economic cost for

the organization.

a) Dividend:

it is associated with venture capitalist, as Clariton will have to give dividend to the We finance

limited. It increase economic burden of the company to great extent (Rupeika-Apoga, 2014).

b) Interest

Whenever organization borrow money from banks then they charge interest on it. For

instance if annual interest rate of financial institutes is 2% and cited firm has taken loan

of 500000 then cost of interest would be:

=500000*2%+ 1% brokerage

=10000+5000=15000

. This financial cost will have to be faced by the Clariton for longer period.

c) Tax:

Cited firm will have to pay tax on its earned income. Tax rate of government is fixed and

for registered business it is compulsory to pay corporate tax and they have to show tax amount

in income statement (Dutescu, Popa,. and Ponorîca, 2014).

2.2 Financial planning and its significance

Economic forecasting is the mechanism through which organization can forecast future

and can identify upcoming uncertainties. It suggests the projects in which investment can give

higher returns. It is important and gives positive result to the corporations. Budget preparation,

utilization of funds can be done significantly by proper economic planning. It helps to avoid

uncertainties of business and by this way owner can make strategies to making successful to

business (Hsu and et.al, 2014).

a) Budget:

It is the estimated projection of income and expenditures. Economic forecasting is the

tool which assists and guide in making cash and sales budget. By this way owner will be able to

allocate funds in each task and activity. With the help of this evaluation of financial

performance can be done effectively. Cot control can be done by proper budgeting easily that

can enhance revenues of the company (Zheng, X., Xu, Y. and Gu, L., 2013).

the organization.

a) Dividend:

it is associated with venture capitalist, as Clariton will have to give dividend to the We finance

limited. It increase economic burden of the company to great extent (Rupeika-Apoga, 2014).

b) Interest

Whenever organization borrow money from banks then they charge interest on it. For

instance if annual interest rate of financial institutes is 2% and cited firm has taken loan

of 500000 then cost of interest would be:

=500000*2%+ 1% brokerage

=10000+5000=15000

. This financial cost will have to be faced by the Clariton for longer period.

c) Tax:

Cited firm will have to pay tax on its earned income. Tax rate of government is fixed and

for registered business it is compulsory to pay corporate tax and they have to show tax amount

in income statement (Dutescu, Popa,. and Ponorîca, 2014).

2.2 Financial planning and its significance

Economic forecasting is the mechanism through which organization can forecast future

and can identify upcoming uncertainties. It suggests the projects in which investment can give

higher returns. It is important and gives positive result to the corporations. Budget preparation,

utilization of funds can be done significantly by proper economic planning. It helps to avoid

uncertainties of business and by this way owner can make strategies to making successful to

business (Hsu and et.al, 2014).

a) Budget:

It is the estimated projection of income and expenditures. Economic forecasting is the

tool which assists and guide in making cash and sales budget. By this way owner will be able to

allocate funds in each task and activity. With the help of this evaluation of financial

performance can be done effectively. Cot control can be done by proper budgeting easily that

can enhance revenues of the company (Zheng, X., Xu, Y. and Gu, L., 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Implication of failure:

Financial planning is the tool that supports in reducing the circumstances of failure of the

business. Sometimes wrong decisions can revenues of the company. As Clariton is

engaged in selling of antique items so it is essential for the cited firm to purchase right

products and as per the demand. So that operational cost remain in control otherwise it

can create situation of failure for the organization (Dutescu, Popa,. and Ponorîca, 2014)..

c) Overtrading:

It is another importance of financial planning, by looking upon the previous sales records

partners of Clariton can estimate future sale. That would help them in making balance between

demand and supply thus issues related to over trading can be minimized. This will be beneficial

for the organizations as they will be able to make proper control over their expenditures that

will help in accomplishing the objectives of the company (Zheng, X., Xu, Y. and Gu, L., 2013)..

2.3 Information requires to make effective decision

There are many persons those who are involved in the business, all they need verity of

details so that they invest their money in the entity accordingly. If persons invest in wrong

business then it may be possible that individual fails to get its return (Jindrichovska, 2013).

a) The partner: As Clariton is the partnership firm, it has four partners. To raise capital is their

objective and personal saving is one of the best cheaper source of finance through which they

can increase their cash inflows. They need information like solvency ratio, efficiency ratio,

assets value, profit percentage, previous liabilities etc. These details help them in taking

significant investment decisions and they will be able to gain estimated profit on their

investments (Rupeika-Apoga, 2014).

b) Venture Capitalist: We Finance limited is the capitalist which has offered to Clariton for

investment. But before offering cited firm investors look upon the profit history, worth of

products, market position, dividend policy, net profit ratio, assets turnover ratio etc. These

details help them in making good decisions (Hsu and et.al, 2014).

c) Finance broker: Individual is the person who has good connections with financial institutions

and persons can provide loan to start up firms. But broker need information like profit history,

solvency ratio, total current liabilities, repay capacity, credit worthiness of partners etc. These

Financial planning is the tool that supports in reducing the circumstances of failure of the

business. Sometimes wrong decisions can revenues of the company. As Clariton is

engaged in selling of antique items so it is essential for the cited firm to purchase right

products and as per the demand. So that operational cost remain in control otherwise it

can create situation of failure for the organization (Dutescu, Popa,. and Ponorîca, 2014)..

c) Overtrading:

It is another importance of financial planning, by looking upon the previous sales records

partners of Clariton can estimate future sale. That would help them in making balance between

demand and supply thus issues related to over trading can be minimized. This will be beneficial

for the organizations as they will be able to make proper control over their expenditures that

will help in accomplishing the objectives of the company (Zheng, X., Xu, Y. and Gu, L., 2013)..

2.3 Information requires to make effective decision

There are many persons those who are involved in the business, all they need verity of

details so that they invest their money in the entity accordingly. If persons invest in wrong

business then it may be possible that individual fails to get its return (Jindrichovska, 2013).

a) The partner: As Clariton is the partnership firm, it has four partners. To raise capital is their

objective and personal saving is one of the best cheaper source of finance through which they

can increase their cash inflows. They need information like solvency ratio, efficiency ratio,

assets value, profit percentage, previous liabilities etc. These details help them in taking

significant investment decisions and they will be able to gain estimated profit on their

investments (Rupeika-Apoga, 2014).

b) Venture Capitalist: We Finance limited is the capitalist which has offered to Clariton for

investment. But before offering cited firm investors look upon the profit history, worth of

products, market position, dividend policy, net profit ratio, assets turnover ratio etc. These

details help them in making good decisions (Hsu and et.al, 2014).

c) Finance broker: Individual is the person who has good connections with financial institutions

and persons can provide loan to start up firms. But broker need information like profit history,

solvency ratio, total current liabilities, repay capacity, credit worthiness of partners etc. These

details can help banks in giving loan to right persons and banks ensure that their loan amount

will be repaid by borrower easily (Jindrichovska, 2013).

These all information can be gathered by looking upon financial statements of the cited firm.

Income statements gives detail about profit history and expenditures, Balance sheet provides in

depth knowledge about assets and liabilities of the organization. Deep study of these data can

help in taking effective decisions which can give positive results to the enterprise (Tsai, 2015).

2.4 Impact of financial sources on accounting statements

Organizations prepare accounting statements to analyze their performance and to keep

records for future. For raising funds they have to take support of financial sources, these source

have some economic cost which impacts on the financial statements of the company.

a) Venture Capitalist

As We Finance limited is the capitalist and is taking interest regarding investment in the

Clariton. This investment can increase capital of the cited firm and it will reflect in the balance

sheet of the organization. As cash inflow will get increased so it will also impact on the cash

flow statement (Hossain and Kauranen, 2016). On other hand cited firm will have to involve

capitalist in the decision making process and necessary to give dividend to them so it will

defiantly impact on the income statement in expenditure side. By adding dividend in the profit

and loss account, net profit will get calculated.

b) Finance broker:

Broker always charge commission that is economic cost for the Clariton. As 1% brokerage and

2% annual bank interest will reflect in the income statement. That will reduce net profit of the

cited firm. Bank loan also impacts on the capital side of balance sheet. And also it increases

liability as well so reflects in the same financial statement (Tsai, 2015). .

All sources of finance impact on the financial statements either they create liability or

increases capital side.

Task 3

3.1 Cash budget

Objective of preparing cash budget is to estimate income and payments in specific time

period of an organization. It is an accounting tool which shows the income which is expected to

will be repaid by borrower easily (Jindrichovska, 2013).

These all information can be gathered by looking upon financial statements of the cited firm.

Income statements gives detail about profit history and expenditures, Balance sheet provides in

depth knowledge about assets and liabilities of the organization. Deep study of these data can

help in taking effective decisions which can give positive results to the enterprise (Tsai, 2015).

2.4 Impact of financial sources on accounting statements

Organizations prepare accounting statements to analyze their performance and to keep

records for future. For raising funds they have to take support of financial sources, these source

have some economic cost which impacts on the financial statements of the company.

a) Venture Capitalist

As We Finance limited is the capitalist and is taking interest regarding investment in the

Clariton. This investment can increase capital of the cited firm and it will reflect in the balance

sheet of the organization. As cash inflow will get increased so it will also impact on the cash

flow statement (Hossain and Kauranen, 2016). On other hand cited firm will have to involve

capitalist in the decision making process and necessary to give dividend to them so it will

defiantly impact on the income statement in expenditure side. By adding dividend in the profit

and loss account, net profit will get calculated.

b) Finance broker:

Broker always charge commission that is economic cost for the Clariton. As 1% brokerage and

2% annual bank interest will reflect in the income statement. That will reduce net profit of the

cited firm. Bank loan also impacts on the capital side of balance sheet. And also it increases

liability as well so reflects in the same financial statement (Tsai, 2015). .

All sources of finance impact on the financial statements either they create liability or

increases capital side.

Task 3

3.1 Cash budget

Objective of preparing cash budget is to estimate income and payments in specific time

period of an organization. It is an accounting tool which shows the income which is expected to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

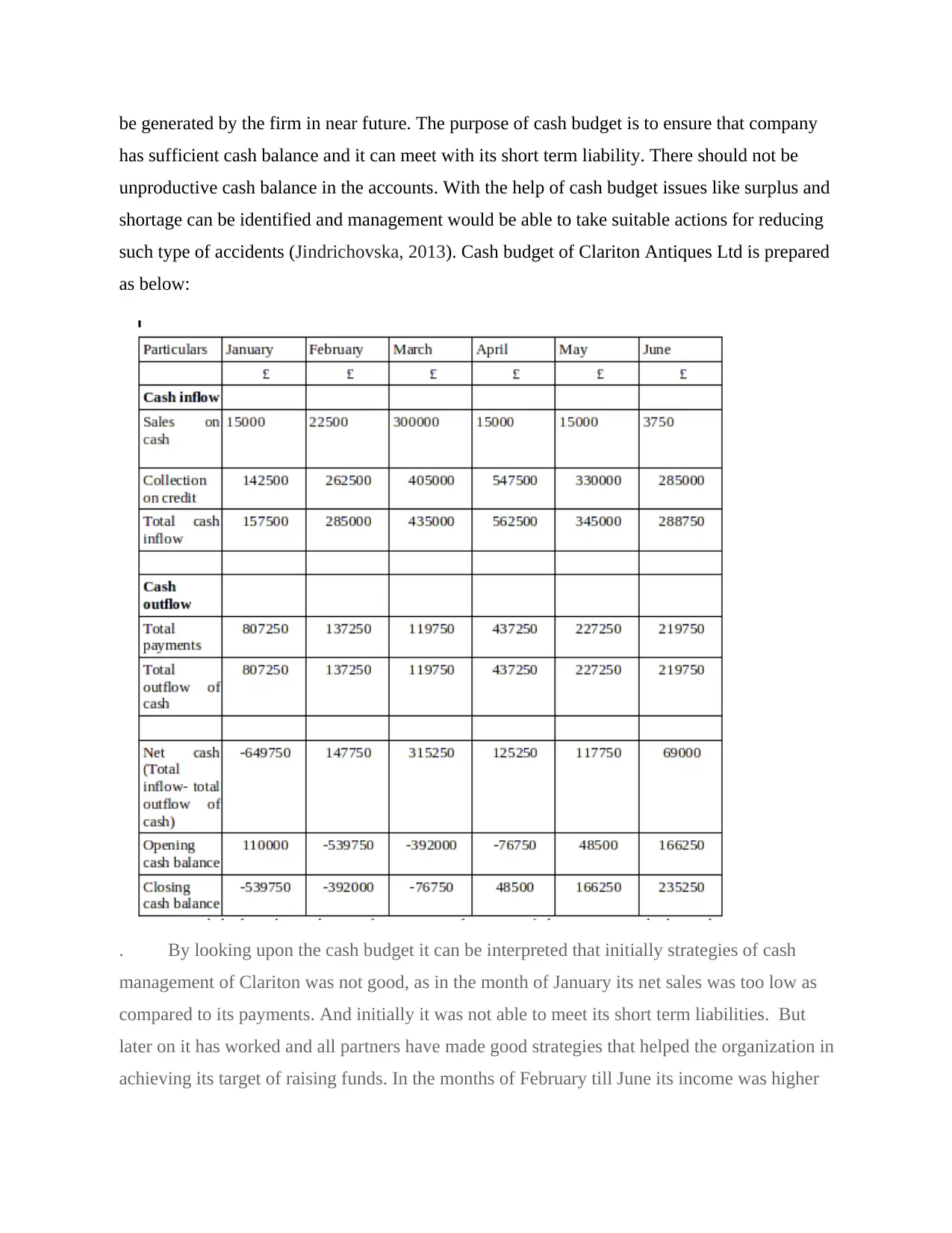

be generated by the firm in near future. The purpose of cash budget is to ensure that company

has sufficient cash balance and it can meet with its short term liability. There should not be

unproductive cash balance in the accounts. With the help of cash budget issues like surplus and

shortage can be identified and management would be able to take suitable actions for reducing

such type of accidents (Jindrichovska, 2013). Cash budget of Clariton Antiques Ltd is prepared

as below:

. By looking upon the cash budget it can be interpreted that initially strategies of cash

management of Clariton was not good, as in the month of January its net sales was too low as

compared to its payments. And initially it was not able to meet its short term liabilities. But

later on it has worked and all partners have made good strategies that helped the organization in

achieving its target of raising funds. In the months of February till June its income was higher

has sufficient cash balance and it can meet with its short term liability. There should not be

unproductive cash balance in the accounts. With the help of cash budget issues like surplus and

shortage can be identified and management would be able to take suitable actions for reducing

such type of accidents (Jindrichovska, 2013). Cash budget of Clariton Antiques Ltd is prepared

as below:

. By looking upon the cash budget it can be interpreted that initially strategies of cash

management of Clariton was not good, as in the month of January its net sales was too low as

compared to its payments. And initially it was not able to meet its short term liabilities. But

later on it has worked and all partners have made good strategies that helped the organization in

achieving its target of raising funds. In the months of February till June its income was higher

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

than payments (Infelise, 2014). That means cash management strategies have been improved by

the partners for the betterment of the cited firm. Initially net cash balance was negative that is

showing poor performance of the company in its early stage. By this way it can be said that cash

budget is very important and can help in making significant strategies which can help in the

development of the entity (Avdeitchikova and Landström, 2016).

3.2 Unit cost and pricing decisions

Unit cost is the cost of the company which has been incurred in producing one unit. Cost

may be of two types; fixed and variables. Fixed expenditures are those spending which are

necessary to do by organizations for running operations well. Such as salaries to employees is

necessary to pay whether business is earning profit or not. It can be calculated by using

formula:

Unit cost= (direct+ indirect cost)/ total produced units

As Clariton does not manufacture goods it just sales antiques items. So fixed cost for the

cited firm can be as salaries, rent etc. whereas indirect expenditure are utility bills etc (Boyer

and Blazy, 2014). By adding all these costs total payments expenditures can be calculated. For

instance cited firm plans to produce 10000 unit, it salary expenses are 25000, rent 20000, utility

bills are 25000 and other spending are 10000 then

Unit cost = 80000/10000

Unit cost = 8 that means per unit cost is 8 in the Clariton. By using this mount pricing decision

can be taken by the organization (Avdeitchikova and Landström, 2016)..

Pricing decision

On the bases of cost per unit, Clariton can take decision of selling price. For instance

cited firm wants to earn profit of 25% then

Selling price = unit cost+ per unit cost* profit percentage

Selling price= 8+8*25%

Selling price =8+2

the partners for the betterment of the cited firm. Initially net cash balance was negative that is

showing poor performance of the company in its early stage. By this way it can be said that cash

budget is very important and can help in making significant strategies which can help in the

development of the entity (Avdeitchikova and Landström, 2016).

3.2 Unit cost and pricing decisions

Unit cost is the cost of the company which has been incurred in producing one unit. Cost

may be of two types; fixed and variables. Fixed expenditures are those spending which are

necessary to do by organizations for running operations well. Such as salaries to employees is

necessary to pay whether business is earning profit or not. It can be calculated by using

formula:

Unit cost= (direct+ indirect cost)/ total produced units

As Clariton does not manufacture goods it just sales antiques items. So fixed cost for the

cited firm can be as salaries, rent etc. whereas indirect expenditure are utility bills etc (Boyer

and Blazy, 2014). By adding all these costs total payments expenditures can be calculated. For

instance cited firm plans to produce 10000 unit, it salary expenses are 25000, rent 20000, utility

bills are 25000 and other spending are 10000 then

Unit cost = 80000/10000

Unit cost = 8 that means per unit cost is 8 in the Clariton. By using this mount pricing decision

can be taken by the organization (Avdeitchikova and Landström, 2016)..

Pricing decision

On the bases of cost per unit, Clariton can take decision of selling price. For instance

cited firm wants to earn profit of 25% then

Selling price = unit cost+ per unit cost* profit percentage

Selling price= 8+8*25%

Selling price =8+2

Selling price = 10

Which means if Clariton takes decision of keeping selling price 10 then it has great

chance to earn profit of 25% soon. By using unit cost well organizations can reduce their cost

and can make effective strategies to increase revenues of the company. It would help them in

accomplishing their goal in an effective manner (Boyer and Blazy, 2014).

3.3 Investment decisions

It is necessary for the growth of entities that they invest their money in right place.

Organization growth and their future depend upon their investment decisions. Investment

appraisal techniques are those accounting tools which assist owner in taking their decisions.

NPV, ARR, PBP etc. are many calculative techniques which support in knowing about the

feasibility of the projects.

Net present Value (NPV):

It is a calculative technique which focuses on the present cash outflow value and compare

it with future income. If it has huge difference which mean project is not viable and can not get

good returns (Boyer and Blazy, 2014). As it is based on assumption such as PV factor is

assumed by the owner, there is chanced that they may get differed. But is focuses on risk factor

that can give positive results to the entity.

From the above calculation it can be said that both projects are viable and are able to

recover amount soon. Less risk is attached with both projects. Clariton was assuming to invest

Which means if Clariton takes decision of keeping selling price 10 then it has great

chance to earn profit of 25% soon. By using unit cost well organizations can reduce their cost

and can make effective strategies to increase revenues of the company. It would help them in

accomplishing their goal in an effective manner (Boyer and Blazy, 2014).

3.3 Investment decisions

It is necessary for the growth of entities that they invest their money in right place.

Organization growth and their future depend upon their investment decisions. Investment

appraisal techniques are those accounting tools which assist owner in taking their decisions.

NPV, ARR, PBP etc. are many calculative techniques which support in knowing about the

feasibility of the projects.

Net present Value (NPV):

It is a calculative technique which focuses on the present cash outflow value and compare

it with future income. If it has huge difference which mean project is not viable and can not get

good returns (Boyer and Blazy, 2014). As it is based on assumption such as PV factor is

assumed by the owner, there is chanced that they may get differed. But is focuses on risk factor

that can give positive results to the entity.

From the above calculation it can be said that both projects are viable and are able to

recover amount soon. Less risk is attached with both projects. Clariton was assuming to invest

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.