Case Study Of Oversea-Chinese Banking Corporation Limited

Added on 2021-09-18

58 Pages16163 Words52 Views

Introduction

Oversea-Chinese Banking Corporation Limited, abbreviated as OCBC Bank. It is a

publicly listed financial services organisation with its head office in Singapore. OCBC Bank

was born out of the Great Depression through the consolidation of three banks in 1932 - the

Chinese Commercial Bank Limited (incorporated in 1912), the Ho Hong Bank Limited

(incorporated in 1917) and the Oversea-Chinese Bank Limited (incorporated in 1919).

Although publicly listed, OCBC Bank's largest shareholder is the Lee Group of

Companies. Lee Kong Chian and his son Lee Seng Wee also served as OCBC chairman in

the 1930s and 1990s respectively. OCBC Bank has assets of more than 224 billion SGD.

Based on Bloomberg, in 2011 OCBC is the number one of the world's strongest $100 billion

assets banks. It is Singapore's oldest local bank.

The "Oversea-Chinese" usage leads many to believe mistakenly that the bank's name is

misspelled, but this is the correct traditional spelling. The bank's global network has grown to

comprise subsidiaries, branches, and representative offices in 18 countries and territories. It

has retail banking subsidiaries in Malaysia, Indonesia, Hong Kong, and China, and branches

in China, Hong Kong, Japan, Australia, the UK and US. OCBC's Indonesia subsidiary, Bank

OCBC NISP, has 630 branches and offices. In this report, we will analyze the OCBC bank

and its financial system.

The study is aimed at banking industry in Malaysia, background of the company, type

of financial institution and reasoning of this categorization, type of bank and reasoning of this

categorization, items on the balance sheet for year 2016, services and products offered, recent

developments in the respective bank, the type of banking regulations being used, very brief

background of the relevant banks, reasons for merger or acquisition, and benefits and losses

after the merger or acquisition.

Oversea-Chinese Banking Corporation Limited, abbreviated as OCBC Bank. It is a

publicly listed financial services organisation with its head office in Singapore. OCBC Bank

was born out of the Great Depression through the consolidation of three banks in 1932 - the

Chinese Commercial Bank Limited (incorporated in 1912), the Ho Hong Bank Limited

(incorporated in 1917) and the Oversea-Chinese Bank Limited (incorporated in 1919).

Although publicly listed, OCBC Bank's largest shareholder is the Lee Group of

Companies. Lee Kong Chian and his son Lee Seng Wee also served as OCBC chairman in

the 1930s and 1990s respectively. OCBC Bank has assets of more than 224 billion SGD.

Based on Bloomberg, in 2011 OCBC is the number one of the world's strongest $100 billion

assets banks. It is Singapore's oldest local bank.

The "Oversea-Chinese" usage leads many to believe mistakenly that the bank's name is

misspelled, but this is the correct traditional spelling. The bank's global network has grown to

comprise subsidiaries, branches, and representative offices in 18 countries and territories. It

has retail banking subsidiaries in Malaysia, Indonesia, Hong Kong, and China, and branches

in China, Hong Kong, Japan, Australia, the UK and US. OCBC's Indonesia subsidiary, Bank

OCBC NISP, has 630 branches and offices. In this report, we will analyze the OCBC bank

and its financial system.

The study is aimed at banking industry in Malaysia, background of the company, type

of financial institution and reasoning of this categorization, type of bank and reasoning of this

categorization, items on the balance sheet for year 2016, services and products offered, recent

developments in the respective bank, the type of banking regulations being used, very brief

background of the relevant banks, reasons for merger or acquisition, and benefits and losses

after the merger or acquisition.

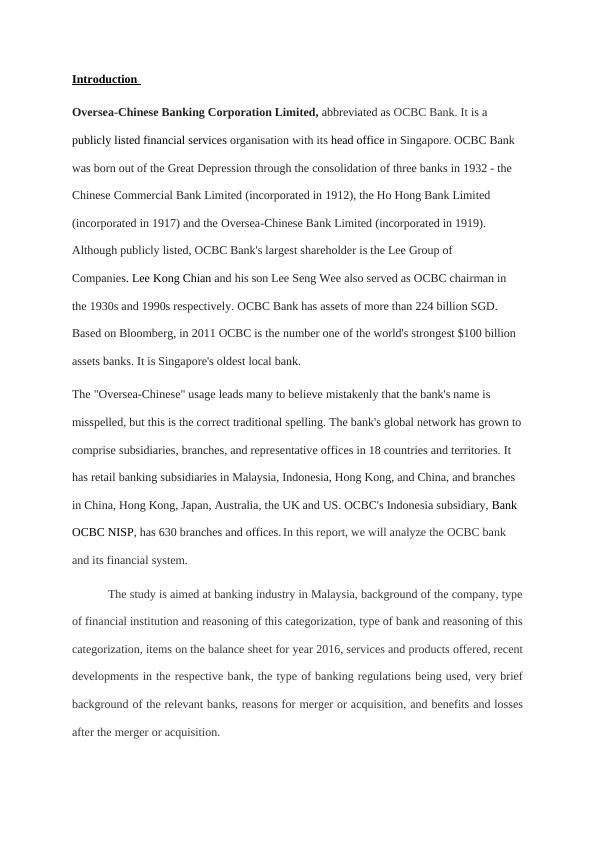

Banking industry in Malaysia

In the research for year 2018, on average, the share price of the local banking players

surged about 17%, with the two banking giants – Malayan Banking Berhad and CIMB Group

Holdings Berhad rising close to 24% and 51% respectively. As the banking industry accounts

for about 32% of weightage in FBMKLCI Index, the sector’s prospect would provide

harbinger of the performance for FBMKLCI Index.

PERFORMANCE OF BANKING SECTOR

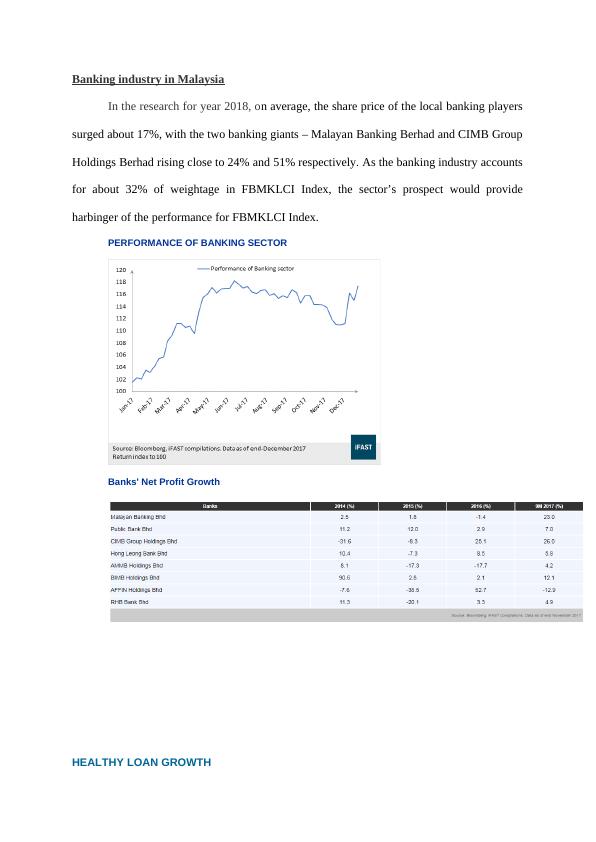

Banks' Net Profit Growth

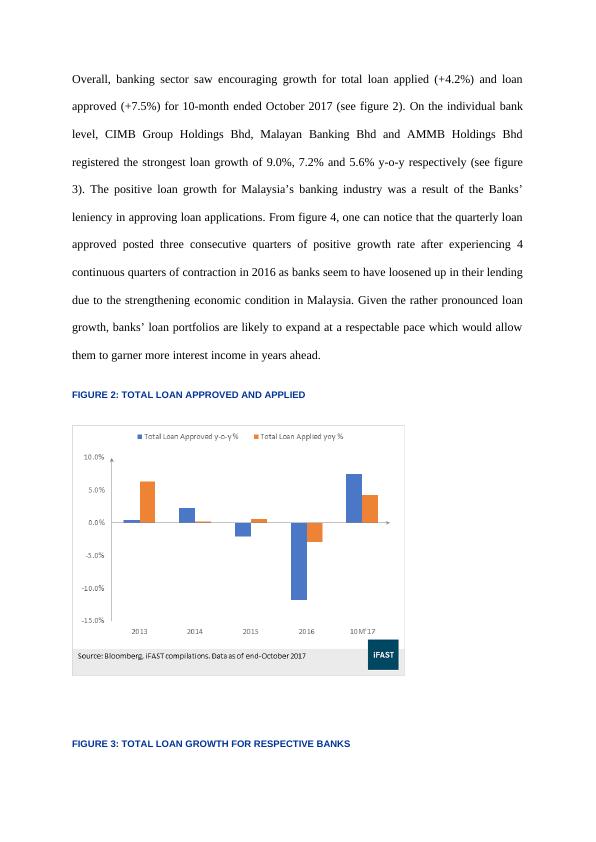

HEALTHY LOAN GROWTH

In the research for year 2018, on average, the share price of the local banking players

surged about 17%, with the two banking giants – Malayan Banking Berhad and CIMB Group

Holdings Berhad rising close to 24% and 51% respectively. As the banking industry accounts

for about 32% of weightage in FBMKLCI Index, the sector’s prospect would provide

harbinger of the performance for FBMKLCI Index.

PERFORMANCE OF BANKING SECTOR

Banks' Net Profit Growth

HEALTHY LOAN GROWTH

Overall, banking sector saw encouraging growth for total loan applied (+4.2%) and loan

approved (+7.5%) for 10-month ended October 2017 (see figure 2). On the individual bank

level, CIMB Group Holdings Bhd, Malayan Banking Bhd and AMMB Holdings Bhd

registered the strongest loan growth of 9.0%, 7.2% and 5.6% y-o-y respectively (see figure

3). The positive loan growth for Malaysia’s banking industry was a result of the Banks’

leniency in approving loan applications. From figure 4, one can notice that the quarterly loan

approved posted three consecutive quarters of positive growth rate after experiencing 4

continuous quarters of contraction in 2016 as banks seem to have loosened up in their lending

due to the strengthening economic condition in Malaysia. Given the rather pronounced loan

growth, banks’ loan portfolios are likely to expand at a respectable pace which would allow

them to garner more interest income in years ahead.

FIGURE 2: TOTAL LOAN APPROVED AND APPLIED

FIGURE 3: TOTAL LOAN GROWTH FOR RESPECTIVE BANKS

approved (+7.5%) for 10-month ended October 2017 (see figure 2). On the individual bank

level, CIMB Group Holdings Bhd, Malayan Banking Bhd and AMMB Holdings Bhd

registered the strongest loan growth of 9.0%, 7.2% and 5.6% y-o-y respectively (see figure

3). The positive loan growth for Malaysia’s banking industry was a result of the Banks’

leniency in approving loan applications. From figure 4, one can notice that the quarterly loan

approved posted three consecutive quarters of positive growth rate after experiencing 4

continuous quarters of contraction in 2016 as banks seem to have loosened up in their lending

due to the strengthening economic condition in Malaysia. Given the rather pronounced loan

growth, banks’ loan portfolios are likely to expand at a respectable pace which would allow

them to garner more interest income in years ahead.

FIGURE 2: TOTAL LOAN APPROVED AND APPLIED

FIGURE 3: TOTAL LOAN GROWTH FOR RESPECTIVE BANKS

FIGURE 4: QUARTERLY LOAN APPROVED

Starting from 1st January 2018, the new accounting standard – MFRS 9 which required

amendments to the following areas such as impairment, hedge accounting, classification and

measurement for financial instruments has kicked into effect. To a certain extent, the

adoption of the new standard is likely to post a greater impact on the banking sector by

increasing the impairment losses provision.

Starting from 1st January 2018, the new accounting standard – MFRS 9 which required

amendments to the following areas such as impairment, hedge accounting, classification and

measurement for financial instruments has kicked into effect. To a certain extent, the

adoption of the new standard is likely to post a greater impact on the banking sector by

increasing the impairment losses provision.

However, at this early stage, no one could determine exactly what are the impacts on banks’

income statement and balance sheet but the increase in impairment losses provision will be

charged to retained earnings, hence it might have a lesser impact on banks’ earnings as

compared to their balance sheet. As such, one should not overly concern about this as most of

the local banks have strong buffers, with the Tier 1 capital ratios well above the minimum

capital ratio (6%) required by the central bank.

BANKS' TIER 1 CAPITAL RATIO

Background of the company

OCBC Bank is the longest established Singapore bank, formed in 1932 from the

merger of three local banks, the oldest of which was founded in 1912. It is now the second-

largest financial services group in Southeast Asia by assets and one of the world’s most

highly-rated banks, with an Aa1 rating from Moody’s. Recognised for its financial strength

and stability, OCBC Bank is consistently ranked among the World’s Top 50 Safest Banks by

income statement and balance sheet but the increase in impairment losses provision will be

charged to retained earnings, hence it might have a lesser impact on banks’ earnings as

compared to their balance sheet. As such, one should not overly concern about this as most of

the local banks have strong buffers, with the Tier 1 capital ratios well above the minimum

capital ratio (6%) required by the central bank.

BANKS' TIER 1 CAPITAL RATIO

Background of the company

OCBC Bank is the longest established Singapore bank, formed in 1932 from the

merger of three local banks, the oldest of which was founded in 1912. It is now the second-

largest financial services group in Southeast Asia by assets and one of the world’s most

highly-rated banks, with an Aa1 rating from Moody’s. Recognised for its financial strength

and stability, OCBC Bank is consistently ranked among the World’s Top 50 Safest Banks by

Global Finance and has been named Best Managed Bank in Singapore and the Asia Pacific

by The Asian Banker.

OCBC Bank and its subsidiaries offer a broad array of specialist financial and wealth

management services, ranging from consumer, corporate, investment, private and transaction

banking to treasury, insurance, asset management and stockbroking services.

OCBC Bank’s key markets are Singapore, Malaysia, Indonesia and Greater China. It

has more than 600 branches and representative offices in 18 countries and regions. These

include over 330 branches and offices in Indonesia under subsidiary Bank OCBC NISP and

over 100 branches and offices in Hong Kong, China and Macao under OCBC Wing Hang.

OCBC Bank’s private banking services are provided by its wholly-owned subsidiary

Bank of Singapore, which operates on a unique open-architecture product platform to source

for the best-in-class products to meet its clients’ goals.

OCBC Bank's insurance subsidiary, Great Eastern Holdings, is the oldest and most

established life insurance group in Singapore and Malaysia. Its asset management subsidiary,

Lion Global Investors, is one of the largest private sector asset management companies in

Southeast Asia.

After being actively involved in offering Islamic banking products and services since

1995, OCBC Bank launched its wholly-owned Islamic banking subsidiary, OCBC Al-Amin

Bank Berhad, on 1 December 2008. OCBC Al-Amin offers products and services which are

developed based on the applicable Shariah contract and with the endorsement of the Shariah

Advisory Committee to meet the requirements of both Muslims and non-Muslims alike.

Features such as fixed financing rates and profit sharing have attracted a growing group of

loyal customers who wish to draw from the Islamic principles of fairness, caring and

accuracy.

by The Asian Banker.

OCBC Bank and its subsidiaries offer a broad array of specialist financial and wealth

management services, ranging from consumer, corporate, investment, private and transaction

banking to treasury, insurance, asset management and stockbroking services.

OCBC Bank’s key markets are Singapore, Malaysia, Indonesia and Greater China. It

has more than 600 branches and representative offices in 18 countries and regions. These

include over 330 branches and offices in Indonesia under subsidiary Bank OCBC NISP and

over 100 branches and offices in Hong Kong, China and Macao under OCBC Wing Hang.

OCBC Bank’s private banking services are provided by its wholly-owned subsidiary

Bank of Singapore, which operates on a unique open-architecture product platform to source

for the best-in-class products to meet its clients’ goals.

OCBC Bank's insurance subsidiary, Great Eastern Holdings, is the oldest and most

established life insurance group in Singapore and Malaysia. Its asset management subsidiary,

Lion Global Investors, is one of the largest private sector asset management companies in

Southeast Asia.

After being actively involved in offering Islamic banking products and services since

1995, OCBC Bank launched its wholly-owned Islamic banking subsidiary, OCBC Al-Amin

Bank Berhad, on 1 December 2008. OCBC Al-Amin offers products and services which are

developed based on the applicable Shariah contract and with the endorsement of the Shariah

Advisory Committee to meet the requirements of both Muslims and non-Muslims alike.

Features such as fixed financing rates and profit sharing have attracted a growing group of

loyal customers who wish to draw from the Islamic principles of fairness, caring and

accuracy.

Type of financial institution and reasoning of this categorization

OCBC Bank is depository and non depository financial institution.

Depository: OCBC Bank accepts deposit from savers.

Non depository: OCBC Bank raise fund by selling security. They are also selling insurance to

their clients.

One further feature that distinguishes monetary financial institutions from other financial

corporation’s lies in the nature of financial contracts:

1. Discretionary: Savers/depositors can make discretionary decisions concerning how

much money they want to hold and for how long the period. Depositors are free to decide the

frequency and amount of their transactions.

2. Contractual: Holding assets from other financial institutions requires a contract

which specifies the amount and frequency of the flow of funds. For example, the monthly

contributions to a pension fund or to an insurance provider are normally fixed at the first

stage of applying.

Type of bank and reasoning of this categorization

Consumer banking, business banking, investment banking, global treasury,

investment management and Islamic banking are the comprehensive service in OCBC Bank.

In addition, the OCBC Group has diverse subsidiaries that are involved in insurance,

financial futures, regional stockbroking, trustee, nominee and custodian services, property

development and hotel management.

Consumer banking is also known as retail banking or personal banking. Consumer

banking offers financial services to consumers usually in small scale nature. These range

from providing convenience in financial transactions and deposits, home loans, credit cards,

OCBC Bank is depository and non depository financial institution.

Depository: OCBC Bank accepts deposit from savers.

Non depository: OCBC Bank raise fund by selling security. They are also selling insurance to

their clients.

One further feature that distinguishes monetary financial institutions from other financial

corporation’s lies in the nature of financial contracts:

1. Discretionary: Savers/depositors can make discretionary decisions concerning how

much money they want to hold and for how long the period. Depositors are free to decide the

frequency and amount of their transactions.

2. Contractual: Holding assets from other financial institutions requires a contract

which specifies the amount and frequency of the flow of funds. For example, the monthly

contributions to a pension fund or to an insurance provider are normally fixed at the first

stage of applying.

Type of bank and reasoning of this categorization

Consumer banking, business banking, investment banking, global treasury,

investment management and Islamic banking are the comprehensive service in OCBC Bank.

In addition, the OCBC Group has diverse subsidiaries that are involved in insurance,

financial futures, regional stockbroking, trustee, nominee and custodian services, property

development and hotel management.

Consumer banking is also known as retail banking or personal banking. Consumer

banking offers financial services to consumers usually in small scale nature. These range

from providing convenience in financial transactions and deposits, home loans, credit cards,

personal overdraft, commercial property loans and premier banking to investment

opportunities and insurance. OCBC Bank also has a leading presence in several segments,

including homes loans and wealth management. A variety of different types of banks offer

personal banking services, these include: commercial banks, saving banks, co-operative

banks, building societies, credit unions, and finance houses.

Business banking is also known as commercial banking and occurs when a bank, or

division of a bank, only deals with business. The business banking of OCBC Bank services

small and medium-sized enterprises (SMEs), large corporates, real estate companies,

government bodies and institutional customers. It offers clients a whole range of products and

services from traditional credit facilities and cash management services to more sophisticated

capital raising arrangements in the public debt market. Note that this distinction is not clear-

cut and some banks do not explicitly distinguish between ‘business banking’ and ‘corporate

banking’.

Investment banking act as the intermediary of between securities issuers and

investors. It works closely with the Business Banking division to develop and customize

products and services to meet customers' specific requirements. An investment bank may also

assist companies involved in mergers and acquisitions (M&A) and provide ancillary services

such as market making, trading of derivatives and equity securities, and FICC services (fixed

income instruments, currencies, and commodities).

Islamic banking based on non-interest principles. Islamic Shariah law prohibits the

payment of riba or interest but does encourage entrepreneurial activity. As such, banks that

wish to offer Islamic banking services have to develop products and services that do not

charge or pay interest. Their solution is to offer various profit-sharing-related products

whereby depositors share in the risk of the bank’s lending. After being actively involved in

offering Islamic banking products and services since 1995, OCBC Bank launched its wholly-

opportunities and insurance. OCBC Bank also has a leading presence in several segments,

including homes loans and wealth management. A variety of different types of banks offer

personal banking services, these include: commercial banks, saving banks, co-operative

banks, building societies, credit unions, and finance houses.

Business banking is also known as commercial banking and occurs when a bank, or

division of a bank, only deals with business. The business banking of OCBC Bank services

small and medium-sized enterprises (SMEs), large corporates, real estate companies,

government bodies and institutional customers. It offers clients a whole range of products and

services from traditional credit facilities and cash management services to more sophisticated

capital raising arrangements in the public debt market. Note that this distinction is not clear-

cut and some banks do not explicitly distinguish between ‘business banking’ and ‘corporate

banking’.

Investment banking act as the intermediary of between securities issuers and

investors. It works closely with the Business Banking division to develop and customize

products and services to meet customers' specific requirements. An investment bank may also

assist companies involved in mergers and acquisitions (M&A) and provide ancillary services

such as market making, trading of derivatives and equity securities, and FICC services (fixed

income instruments, currencies, and commodities).

Islamic banking based on non-interest principles. Islamic Shariah law prohibits the

payment of riba or interest but does encourage entrepreneurial activity. As such, banks that

wish to offer Islamic banking services have to develop products and services that do not

charge or pay interest. Their solution is to offer various profit-sharing-related products

whereby depositors share in the risk of the bank’s lending. After being actively involved in

offering Islamic banking products and services since 1995, OCBC Bank launched its wholly-

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Overview of OCBC Bank and the Banking Industry in Malaysialg...

|58

|16163

|123