Financial Accounting Report: CBA Executive Remuneration Analysis

VerifiedAdded on 2020/06/04

|24

|6383

|54

Report

AI Summary

This report provides a comprehensive analysis of the Commonwealth Bank of Australia's (CBA) executive remuneration, focusing on the accounting issues and financial reporting implications related to money laundering and bonus reductions. The report examines the context of the issue, including the reduction of short-term incentives for senior executives due to money laundering concerns, and details the actual remuneration structure of CBA executives, including fixed and variable components. It explores the financial position of the bank, including the reduction of executive fees and directors' fees, and the adoption of technologies to prevent illegal transactions. The report also delves into the issue of adopting global financial language for better business for SEC regulators, highlighting the major accounting barriers and language issues in international financial reporting. Furthermore, the report discusses the role of the Australian Securities Exchange (ASX), and the importance of understanding different accounting standards. The report concludes with an analysis of the target remuneration set for 2017 and the impact of these changes on the financial position of the entity, while also discussing the importance of GAAP and IFRS in financial reporting.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Question 2........................................................................................................................................7

CONCLUSION..............................................................................................................................13

REFERENCE.................................................................................................................................14

BIBLIOGRAPHY..........................................................................................................................16

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Question 2........................................................................................................................................7

CONCLUSION..............................................................................................................................13

REFERENCE.................................................................................................................................14

BIBLIOGRAPHY..........................................................................................................................16

Illustration Index

Illustration 1: Remuneration to senior executives of CBA..............................................................2

Illustration 2: CBA board.................................................................................................................3

Illustration 3: Target remuneration for 2017...................................................................................4

Illustration 1: Remuneration to senior executives of CBA..............................................................2

Illustration 2: CBA board.................................................................................................................3

Illustration 3: Target remuneration for 2017...................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting is a process of measuring, processing and communicating financial

information of any entity generates ideas for investors, creditors and management of risks.

However, management of entire business operations and decision making on it is possible

through recording and reporting financial transactions. The present report is based on introducing

accounting information article related to remuneration for senior executive for Commonwealth

Bank in Australia. It is financial service provider of the country who made planning policy

regarding article mentioned in Australian Securities Exchange (ASX) today. Including this,

different accounting standard board and theories of regulation regarding public and private

interest for the financial institution. Moreover, accounting standard boards and regulations

mentioned for accountancy will be introduced through this assignment. Likewise, theories used

in accounting and recording of financial transactions can be expressed. Thus, students are able to

understand article related to remuneration for senior executive for CBA as well accounting

theories and concepts deeply through this report.

QUESTION 1

Issues covered in exposure draft

The issue occurred in CBA is related to laundering laws related to money laundering and

according to which senior executive will lose all of their short term variable bonuses. However,

for both short term and long term variable bonuses for the financial year. Similarly, in the

financial year 2016, amount is mentioned for paid operations of banking sector (Noeker and

Juckel, 2017). In this regard, directors served full year will pay 300000 while for directors who

are to serve who fell to just for paid 273000. As such remuneration of executives is to present in

its annual report by which monetary position of the bank can recognise. Further, on the basis of

this issue and financial position of the bank, recording for further years. Thus, article mentioned

in the newspaper regarding financial issue and solving the issue is recorded.

REDUCING SENIOR EXECUTIVES' SHORT TERM INCENTIVE FOR CBA

Due to money laundering issue, CBA is facing issue of economic crises therefore,

planning for reducing short term incentive to create balance and improving financial position

of the organisation. However, it will be able for further implementation and strategies in the

future time period. Thus, bank can achieve effective profit by implementing this strategy and

1

Accounting is a process of measuring, processing and communicating financial

information of any entity generates ideas for investors, creditors and management of risks.

However, management of entire business operations and decision making on it is possible

through recording and reporting financial transactions. The present report is based on introducing

accounting information article related to remuneration for senior executive for Commonwealth

Bank in Australia. It is financial service provider of the country who made planning policy

regarding article mentioned in Australian Securities Exchange (ASX) today. Including this,

different accounting standard board and theories of regulation regarding public and private

interest for the financial institution. Moreover, accounting standard boards and regulations

mentioned for accountancy will be introduced through this assignment. Likewise, theories used

in accounting and recording of financial transactions can be expressed. Thus, students are able to

understand article related to remuneration for senior executive for CBA as well accounting

theories and concepts deeply through this report.

QUESTION 1

Issues covered in exposure draft

The issue occurred in CBA is related to laundering laws related to money laundering and

according to which senior executive will lose all of their short term variable bonuses. However,

for both short term and long term variable bonuses for the financial year. Similarly, in the

financial year 2016, amount is mentioned for paid operations of banking sector (Noeker and

Juckel, 2017). In this regard, directors served full year will pay 300000 while for directors who

are to serve who fell to just for paid 273000. As such remuneration of executives is to present in

its annual report by which monetary position of the bank can recognise. Further, on the basis of

this issue and financial position of the bank, recording for further years. Thus, article mentioned

in the newspaper regarding financial issue and solving the issue is recorded.

REDUCING SENIOR EXECUTIVES' SHORT TERM INCENTIVE FOR CBA

Due to money laundering issue, CBA is facing issue of economic crises therefore,

planning for reducing short term incentive to create balance and improving financial position

of the organisation. However, it will be able for further implementation and strategies in the

future time period. Thus, bank can achieve effective profit by implementing this strategy and

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operating further activities.

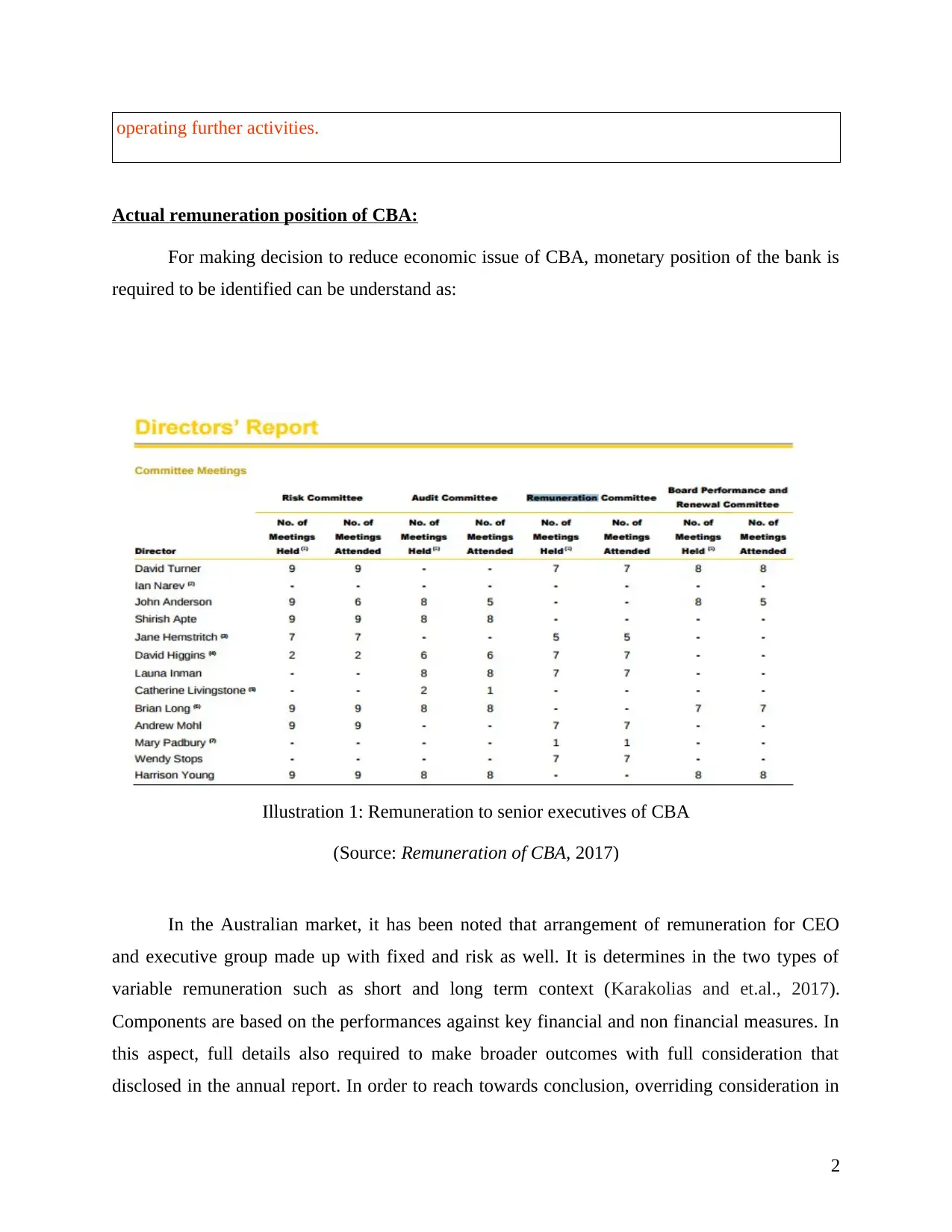

Actual remuneration position of CBA:

For making decision to reduce economic issue of CBA, monetary position of the bank is

required to be identified can be understand as:

In the Australian market, it has been noted that arrangement of remuneration for CEO

and executive group made up with fixed and risk as well. It is determines in the two types of

variable remuneration such as short and long term context (Karakolias and et.al., 2017).

Components are based on the performances against key financial and non financial measures. In

this aspect, full details also required to make broader outcomes with full consideration that

disclosed in the annual report. In order to reach towards conclusion, overriding consideration in

2

Illustration 1: Remuneration to senior executives of CBA

(Source: Remuneration of CBA, 2017)

Actual remuneration position of CBA:

For making decision to reduce economic issue of CBA, monetary position of the bank is

required to be identified can be understand as:

In the Australian market, it has been noted that arrangement of remuneration for CEO

and executive group made up with fixed and risk as well. It is determines in the two types of

variable remuneration such as short and long term context (Karakolias and et.al., 2017).

Components are based on the performances against key financial and non financial measures. In

this aspect, full details also required to make broader outcomes with full consideration that

disclosed in the annual report. In order to reach towards conclusion, overriding consideration in

2

Illustration 1: Remuneration to senior executives of CBA

(Source: Remuneration of CBA, 2017)

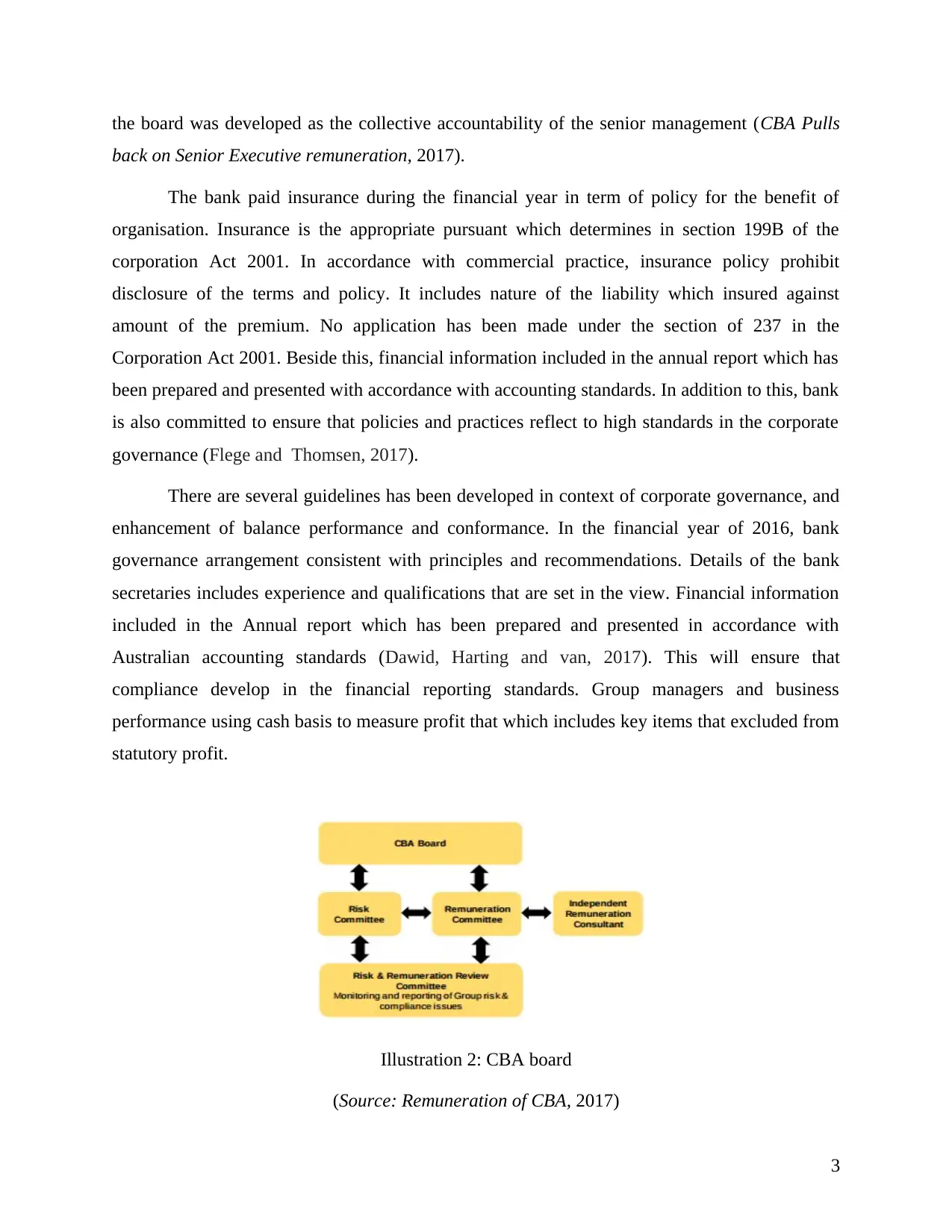

the board was developed as the collective accountability of the senior management (CBA Pulls

back on Senior Executive remuneration, 2017).

The bank paid insurance during the financial year in term of policy for the benefit of

organisation. Insurance is the appropriate pursuant which determines in section 199B of the

corporation Act 2001. In accordance with commercial practice, insurance policy prohibit

disclosure of the terms and policy. It includes nature of the liability which insured against

amount of the premium. No application has been made under the section of 237 in the

Corporation Act 2001. Beside this, financial information included in the annual report which has

been prepared and presented with accordance with accounting standards. In addition to this, bank

is also committed to ensure that policies and practices reflect to high standards in the corporate

governance (Flege and Thomsen, 2017).

There are several guidelines has been developed in context of corporate governance, and

enhancement of balance performance and conformance. In the financial year of 2016, bank

governance arrangement consistent with principles and recommendations. Details of the bank

secretaries includes experience and qualifications that are set in the view. Financial information

included in the Annual report which has been prepared and presented in accordance with

Australian accounting standards (Dawid, Harting and van, 2017). This will ensure that

compliance develop in the financial reporting standards. Group managers and business

performance using cash basis to measure profit that which includes key items that excluded from

statutory profit.

3

Illustration 2: CBA board

(Source: Remuneration of CBA, 2017)

back on Senior Executive remuneration, 2017).

The bank paid insurance during the financial year in term of policy for the benefit of

organisation. Insurance is the appropriate pursuant which determines in section 199B of the

corporation Act 2001. In accordance with commercial practice, insurance policy prohibit

disclosure of the terms and policy. It includes nature of the liability which insured against

amount of the premium. No application has been made under the section of 237 in the

Corporation Act 2001. Beside this, financial information included in the annual report which has

been prepared and presented with accordance with accounting standards. In addition to this, bank

is also committed to ensure that policies and practices reflect to high standards in the corporate

governance (Flege and Thomsen, 2017).

There are several guidelines has been developed in context of corporate governance, and

enhancement of balance performance and conformance. In the financial year of 2016, bank

governance arrangement consistent with principles and recommendations. Details of the bank

secretaries includes experience and qualifications that are set in the view. Financial information

included in the Annual report which has been prepared and presented in accordance with

Australian accounting standards (Dawid, Harting and van, 2017). This will ensure that

compliance develop in the financial reporting standards. Group managers and business

performance using cash basis to measure profit that which includes key items that excluded from

statutory profit.

3

Illustration 2: CBA board

(Source: Remuneration of CBA, 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Common wealth bank of Australia has reduced the pay of senior executive and non

executive directors in order to decrease money laundering activities. Besides reducing the pay

scale of senior executives the financial organisation can reduce short term variable incentive.

There is also decline in non executive directors fees in order to eliminate cyber crime

(Fernández, Arrondo and Pathan, 2017). Technology such as deposit machine can be adopted by

banks in order to facilitate anonymous cheque and cash deposits. This machine will assist

financial institution in preventing illegal transactions, can track criminal conducting illegal

transaction. The use of this machine will help bank in avoiding unnecessary suspicious

transactions. Government can set up an industry to solves various banking industry related

issues. The legal authority can establish an enquiry system to investigate “ culture problems in

the banking sector”.The government can set various limit for various transactions. Due diligence

strategy can be adopted which includes knowing the customer, obtaining information on

intended transaction and verifying above information through certificates and other sources.

Traceability of transactions which can be used by banks for detecting money laundering

activities. This strategy will enable financial organisation to ensure traceability of transaction and

opportunity to identify the origin of transaction (Nadeem, Zaman and Saleem, 2017). Person

who hold special authority to represent a legal entity that deals in financial undertakings

including managing director require verifying of their identity while making transactions.

Questionnaire method can be used in order to get information from customers about intended

transactions, purpose of financial activity, as well as nature of transaction.

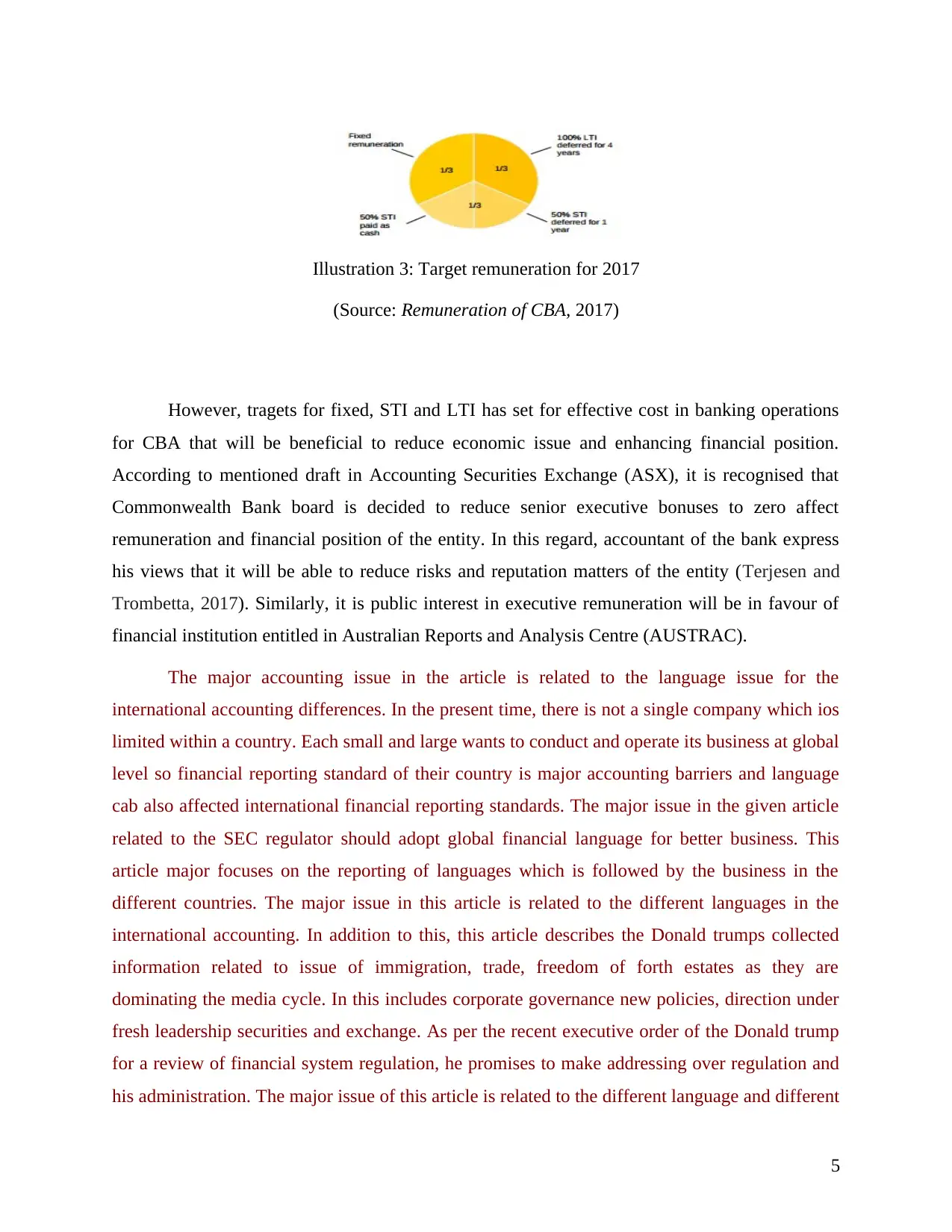

Target remuneration for financial year 2017

On behalf of this data interpretation, it can be recognised that if senior executives of CBA

do not paid short term incentive for financial year 2017 then financial position of the entity.

However, CBA's director also have cut their fees by 20% for economic stability and improving

economic position efficiently (Terjesen and Trombetta, 2017). Therefore, by implementing this

strategy, bank will be able to spend adequate expenditures and increasing its sales revenue.

However, by reducing senior executives' bonuses, financial position of the bank can be improved

effectively. In this regard, following target is set for financial year 2017 overall targeted is to be

presented as:

4

executive directors in order to decrease money laundering activities. Besides reducing the pay

scale of senior executives the financial organisation can reduce short term variable incentive.

There is also decline in non executive directors fees in order to eliminate cyber crime

(Fernández, Arrondo and Pathan, 2017). Technology such as deposit machine can be adopted by

banks in order to facilitate anonymous cheque and cash deposits. This machine will assist

financial institution in preventing illegal transactions, can track criminal conducting illegal

transaction. The use of this machine will help bank in avoiding unnecessary suspicious

transactions. Government can set up an industry to solves various banking industry related

issues. The legal authority can establish an enquiry system to investigate “ culture problems in

the banking sector”.The government can set various limit for various transactions. Due diligence

strategy can be adopted which includes knowing the customer, obtaining information on

intended transaction and verifying above information through certificates and other sources.

Traceability of transactions which can be used by banks for detecting money laundering

activities. This strategy will enable financial organisation to ensure traceability of transaction and

opportunity to identify the origin of transaction (Nadeem, Zaman and Saleem, 2017). Person

who hold special authority to represent a legal entity that deals in financial undertakings

including managing director require verifying of their identity while making transactions.

Questionnaire method can be used in order to get information from customers about intended

transactions, purpose of financial activity, as well as nature of transaction.

Target remuneration for financial year 2017

On behalf of this data interpretation, it can be recognised that if senior executives of CBA

do not paid short term incentive for financial year 2017 then financial position of the entity.

However, CBA's director also have cut their fees by 20% for economic stability and improving

economic position efficiently (Terjesen and Trombetta, 2017). Therefore, by implementing this

strategy, bank will be able to spend adequate expenditures and increasing its sales revenue.

However, by reducing senior executives' bonuses, financial position of the bank can be improved

effectively. In this regard, following target is set for financial year 2017 overall targeted is to be

presented as:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

However, tragets for fixed, STI and LTI has set for effective cost in banking operations

for CBA that will be beneficial to reduce economic issue and enhancing financial position.

According to mentioned draft in Accounting Securities Exchange (ASX), it is recognised that

Commonwealth Bank board is decided to reduce senior executive bonuses to zero affect

remuneration and financial position of the entity. In this regard, accountant of the bank express

his views that it will be able to reduce risks and reputation matters of the entity (Terjesen and

Trombetta, 2017). Similarly, it is public interest in executive remuneration will be in favour of

financial institution entitled in Australian Reports and Analysis Centre (AUSTRAC).

The major accounting issue in the article is related to the language issue for the

international accounting differences. In the present time, there is not a single company which ios

limited within a country. Each small and large wants to conduct and operate its business at global

level so financial reporting standard of their country is major accounting barriers and language

cab also affected international financial reporting standards. The major issue in the given article

related to the SEC regulator should adopt global financial language for better business. This

article major focuses on the reporting of languages which is followed by the business in the

different countries. The major issue in this article is related to the different languages in the

international accounting. In addition to this, this article describes the Donald trumps collected

information related to issue of immigration, trade, freedom of forth estates as they are

dominating the media cycle. In this includes corporate governance new policies, direction under

fresh leadership securities and exchange. As per the recent executive order of the Donald trump

for a review of financial system regulation, he promises to make addressing over regulation and

his administration. The major issue of this article is related to the different language and different

5

Illustration 3: Target remuneration for 2017

(Source: Remuneration of CBA, 2017)

for CBA that will be beneficial to reduce economic issue and enhancing financial position.

According to mentioned draft in Accounting Securities Exchange (ASX), it is recognised that

Commonwealth Bank board is decided to reduce senior executive bonuses to zero affect

remuneration and financial position of the entity. In this regard, accountant of the bank express

his views that it will be able to reduce risks and reputation matters of the entity (Terjesen and

Trombetta, 2017). Similarly, it is public interest in executive remuneration will be in favour of

financial institution entitled in Australian Reports and Analysis Centre (AUSTRAC).

The major accounting issue in the article is related to the language issue for the

international accounting differences. In the present time, there is not a single company which ios

limited within a country. Each small and large wants to conduct and operate its business at global

level so financial reporting standard of their country is major accounting barriers and language

cab also affected international financial reporting standards. The major issue in the given article

related to the SEC regulator should adopt global financial language for better business. This

article major focuses on the reporting of languages which is followed by the business in the

different countries. The major issue in this article is related to the different languages in the

international accounting. In addition to this, this article describes the Donald trumps collected

information related to issue of immigration, trade, freedom of forth estates as they are

dominating the media cycle. In this includes corporate governance new policies, direction under

fresh leadership securities and exchange. As per the recent executive order of the Donald trump

for a review of financial system regulation, he promises to make addressing over regulation and

his administration. The major issue of this article is related to the different language and different

5

Illustration 3: Target remuneration for 2017

(Source: Remuneration of CBA, 2017)

accounting standards in the different country. Thus, organisation have to understand and adopt

different accounting standards. This topic is link with international financial accounting standard

as US is one of the icon in the field of accounting sector which is using GAAP on its financial

report. Other countries like Australia are using the IFRS in its accounting report, so there are

several standards from the IFRS and GAAP which will be the worldwide acceptable reporting

language.

6

different accounting standards. This topic is link with international financial accounting standard

as US is one of the icon in the field of accounting sector which is using GAAP on its financial

report. Other countries like Australia are using the IFRS in its accounting report, so there are

several standards from the IFRS and GAAP which will be the worldwide acceptable reporting

language.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

NEWS LETTER:

ADOPTING GLOBAL FINANCIAL LANGUAGE FOR BETTER BUSINESS FOR SEC

REGULATORS IN AUSTRALIA

The major accounting issue in the article is related to the language issue for the international

accounting differences. In the present time, there is not a single company which is limited

within a country. Each small and large wants to conduct and operate its business at global level

so financial reporting standard of their country is major accounting barriers and language cab

also affected international financial reporting standards.

The given article related to the SEC regulator should adopt global financial language

for better business. This article major focuses on the reporting of languages which is followed

by the business in the different countries. The major issue in this article is related to the

different languages in the international accounting.

This article is related to the different languages in the international accounting. In addition

7

ADOPTING GLOBAL FINANCIAL LANGUAGE FOR BETTER BUSINESS FOR SEC

REGULATORS IN AUSTRALIA

The major accounting issue in the article is related to the language issue for the international

accounting differences. In the present time, there is not a single company which is limited

within a country. Each small and large wants to conduct and operate its business at global level

so financial reporting standard of their country is major accounting barriers and language cab

also affected international financial reporting standards.

The given article related to the SEC regulator should adopt global financial language

for better business. This article major focuses on the reporting of languages which is followed

by the business in the different countries. The major issue in this article is related to the

different languages in the international accounting.

This article is related to the different languages in the international accounting. In addition

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to this, article describes the Donald trumps collected information related to issue of

immigration, trade, freedom of forth estates as they are dominating the media cycle. In this

includes corporate governance new policies, direction under fresh leadership securities and

exchange.

As per the recent executive order of the Donald trump for a review of financial system

regulation, he promises to make addressing over regulation and his administration. The major

issue of this article is related to the different language and different accounting standards in the

different country. Thus, organisation have to understand and adopt different accounting

standards.

However, Other countries like Australia are using the IFRS in its accounting report, so

there are several standards from the IFRS and GAAP which will be the worldwide acceptable

reporting language.

8

immigration, trade, freedom of forth estates as they are dominating the media cycle. In this

includes corporate governance new policies, direction under fresh leadership securities and

exchange.

As per the recent executive order of the Donald trump for a review of financial system

regulation, he promises to make addressing over regulation and his administration. The major

issue of this article is related to the different language and different accounting standards in the

different country. Thus, organisation have to understand and adopt different accounting

standards.

However, Other countries like Australia are using the IFRS in its accounting report, so

there are several standards from the IFRS and GAAP which will be the worldwide acceptable

reporting language.

8

Donald trumps collected information related to issue of immigration, trade, freedom of

forth estates as they are dominating the media cycle. In this includes corporate governance new

policies, direction under fresh leadership securities and exchange.

However, other countries like Australia are using the IFRS in its accounting report,

so there are several standards from the IFRS and GAAP which will be the worldwide acceptable

reporting language.

Draft:

LANGUAGE ISSUES IN ACCOUNTING IN AUSTRALIA

The article is related to understand accounting systems to be followed on in recording financial

transactions of the business enterprise. However, language issues occurred in reporting is useful

for maintaining and reporting. In addition to this, Donald Trump expresses his views that

different language issues occurred in article due to immigration and freedom to forth estate

dominate media cycle. In this regard, importance of GAAP accounting standard has been

described for financial reporting and recording data and administration of organisation

effectively. Similarly, accounting standard and financial reporting for GAAP and IFRS are

determined. In addition to this, accounting standard regarding recording and reporting financial

transactions is described to reduce language issues occurred in accounting process.

Discussion on draft

In this discussion, learners can understand both positive and negative aspects of the

strategy to reduce short term senior executives' bonuses to zero (Cunningham, 2017). In this

regard, its advantages and drawbacks are to be understood as:

9

forth estates as they are dominating the media cycle. In this includes corporate governance new

policies, direction under fresh leadership securities and exchange.

However, other countries like Australia are using the IFRS in its accounting report,

so there are several standards from the IFRS and GAAP which will be the worldwide acceptable

reporting language.

Draft:

LANGUAGE ISSUES IN ACCOUNTING IN AUSTRALIA

The article is related to understand accounting systems to be followed on in recording financial

transactions of the business enterprise. However, language issues occurred in reporting is useful

for maintaining and reporting. In addition to this, Donald Trump expresses his views that

different language issues occurred in article due to immigration and freedom to forth estate

dominate media cycle. In this regard, importance of GAAP accounting standard has been

described for financial reporting and recording data and administration of organisation

effectively. Similarly, accounting standard and financial reporting for GAAP and IFRS are

determined. In addition to this, accounting standard regarding recording and reporting financial

transactions is described to reduce language issues occurred in accounting process.

Discussion on draft

In this discussion, learners can understand both positive and negative aspects of the

strategy to reduce short term senior executives' bonuses to zero (Cunningham, 2017). In this

regard, its advantages and drawbacks are to be understood as:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.