Capital Asset Pricing Model: Theory, Application, and Evaluation

VerifiedAdded on 2021/06/17

|6

|2491

|101

Report

AI Summary

This report offers a comprehensive analysis of the Capital Asset Pricing Model (CAPM), a crucial concept in finance. It begins with an introduction to CAPM, explaining its purpose in assessing risk and expected returns on investments. The report then delves into the workings of the CAPM formula, including its components such as risk-free return, beta, and market return. It explores the benefits of CAPM, such as its simplicity and ability to incorporate systematic risk, while also addressing its drawbacks, including its reliance on assumptions and limitations in real-world application. The report further examines recent developments in CAPM, such as the integration of consumption and the introduction of arbitrage pricing theory. Finally, it concludes by evaluating the overall usefulness of CAPM as a tool for investors, acknowledging both its strengths and weaknesses. The report emphasizes that while CAPM may not provide definitive answers, it offers valuable guidelines for investment decisions.

Introduction

This assignment is about the Capital Asset Pricing Model. A concept which came into use after

the famous noble laureate Mr. William Sharpe introduced it in his book called “Portfolio Theory

of Financial Markets”. Capital Asset Pricing Model is a model that tells an investor about the

risk on particular securities before investing the amount of money. Now whom wont love a

concept or an application that suggests or tells us the rate of risk and the rate of expected return

on the investment that we are going to make, hence capital asset pricing model is the one that

provides good theoretical results which is capable of influencing the decision of the investor in

case of investments (Milton, 2012). If we now talk in simpler words about CAPM then it goes

like this, ‘CAPM is nothing but a theoretical model with a formula that if applied on an

investment plan generates results. Now these results can be in the favor of the investor or against

the investor. It is then the investor who has to decide whether to go with the results or not. In

capital market there are no certainties, you can’t even predict what can happen next, this

uncertain behavior of market restricted many investors to invest their hard earned money.

However the big players of financial markets couldn’t hold this situation and they were looking

for some means of bringing in the investors, so that they can get some money, so what brought in

the confidence of the investors into the financial market was the birth of the capital asset pricing

model. This cannot be said that, ‘it is only CAPM that brought in the confidence of the investors,

long before the birth of CAPM, investors were still investing with big risks, however the birth of

CAPM just brought in the wave of confidence in the investors and even the smallest of the

investors started investing their money (Mizrach, 2014).

What CAPM is all about?

Now here in this section, we are going to discuss about what capital asset pricing model is all

about in very much detail. If we talk about what investors does, then the clear answer would be,

he is a person who invests his or others money into different securities of the market. Now it is

the responsibility of the investor to invest the money in such a way that it gives more returns and

less risk on the investments of the people (Hidek, 2011). However it needs to be understood by

us that more the risk more will be the rate of return and lesser the risk low will be the rate of

return on the investment made by the investor. CAPM capital asset pricing model has played an

significant role in the literature of finance (Giovanis, 2010). The (CAPM) model helps in

understanding the market concept price risk for evaluating the threat for a portfolio. The CAPM

manifest the balance returns rates for the entire menaced portfolio. The theory of CAPM guides

to assimilate the fluctuation of market according to CAPM the market return is not constant.

Moreover the progress of CAPM theory is based on many assumptions (Bejjani, 2009).

Hence in capital market, no matter how hard you try to scatter your investments, there will

always be the scope of risk attached to it (Ang, 2006). Suppose you as an investor have invested

into 20 kinds of different governmental and non-governmental securities and you expect that at-

least 10 out of 20 securities, will give you expected returns with no risk, then it is your mis-

This assignment is about the Capital Asset Pricing Model. A concept which came into use after

the famous noble laureate Mr. William Sharpe introduced it in his book called “Portfolio Theory

of Financial Markets”. Capital Asset Pricing Model is a model that tells an investor about the

risk on particular securities before investing the amount of money. Now whom wont love a

concept or an application that suggests or tells us the rate of risk and the rate of expected return

on the investment that we are going to make, hence capital asset pricing model is the one that

provides good theoretical results which is capable of influencing the decision of the investor in

case of investments (Milton, 2012). If we now talk in simpler words about CAPM then it goes

like this, ‘CAPM is nothing but a theoretical model with a formula that if applied on an

investment plan generates results. Now these results can be in the favor of the investor or against

the investor. It is then the investor who has to decide whether to go with the results or not. In

capital market there are no certainties, you can’t even predict what can happen next, this

uncertain behavior of market restricted many investors to invest their hard earned money.

However the big players of financial markets couldn’t hold this situation and they were looking

for some means of bringing in the investors, so that they can get some money, so what brought in

the confidence of the investors into the financial market was the birth of the capital asset pricing

model. This cannot be said that, ‘it is only CAPM that brought in the confidence of the investors,

long before the birth of CAPM, investors were still investing with big risks, however the birth of

CAPM just brought in the wave of confidence in the investors and even the smallest of the

investors started investing their money (Mizrach, 2014).

What CAPM is all about?

Now here in this section, we are going to discuss about what capital asset pricing model is all

about in very much detail. If we talk about what investors does, then the clear answer would be,

he is a person who invests his or others money into different securities of the market. Now it is

the responsibility of the investor to invest the money in such a way that it gives more returns and

less risk on the investments of the people (Hidek, 2011). However it needs to be understood by

us that more the risk more will be the rate of return and lesser the risk low will be the rate of

return on the investment made by the investor. CAPM capital asset pricing model has played an

significant role in the literature of finance (Giovanis, 2010). The (CAPM) model helps in

understanding the market concept price risk for evaluating the threat for a portfolio. The CAPM

manifest the balance returns rates for the entire menaced portfolio. The theory of CAPM guides

to assimilate the fluctuation of market according to CAPM the market return is not constant.

Moreover the progress of CAPM theory is based on many assumptions (Bejjani, 2009).

Hence in capital market, no matter how hard you try to scatter your investments, there will

always be the scope of risk attached to it (Ang, 2006). Suppose you as an investor have invested

into 20 kinds of different governmental and non-governmental securities and you expect that at-

least 10 out of 20 securities, will give you expected returns with no risk, then it is your mis-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conception only (Banz, 2000). In financial market there is nothing which is risk free. Yes, you

can make investments with government banks in their saving accounts, where you will get a

proper rate of return but it will be quite low, if you compare it with the rate of return of the

financial market. The only benefit you will get on your money with the government bonds or

government banks is that your money is safe and will grow on a very low rate.

Now we are going to discuss, how capital asset pricing model came into existence. As mentioned

in the introduction paragraph, the concept of capital asset pricing model was brought into

existence by the financial economist called “William Sharpe” in the year 1970. He brought this

concept in one of his book. He told that capital asset pricing model will theoretically provide all

the answers to the questions of an investor. In his model of capital asset pricing model, he

mentioned that the expected rate of return, the return which is risk free, the risk and the risk of

the market can be easily find out and on these basis the investor can actually make investments

that yields him more and more returns with lesser risks. However low risk and high returns are

just a myth (Fama, 2012). There is nothing like that in financial market till date. No investor,

economist, financial analyst has found any measure or means to bring the risk to the minimum

and the return to the maximum. Now if we talk about, how capital asset pricing model works,

then first of all we need to understand that the capital asset pricing model is nothing but a

formula that if correctly applied on an investment will give you a close or an accurate result.

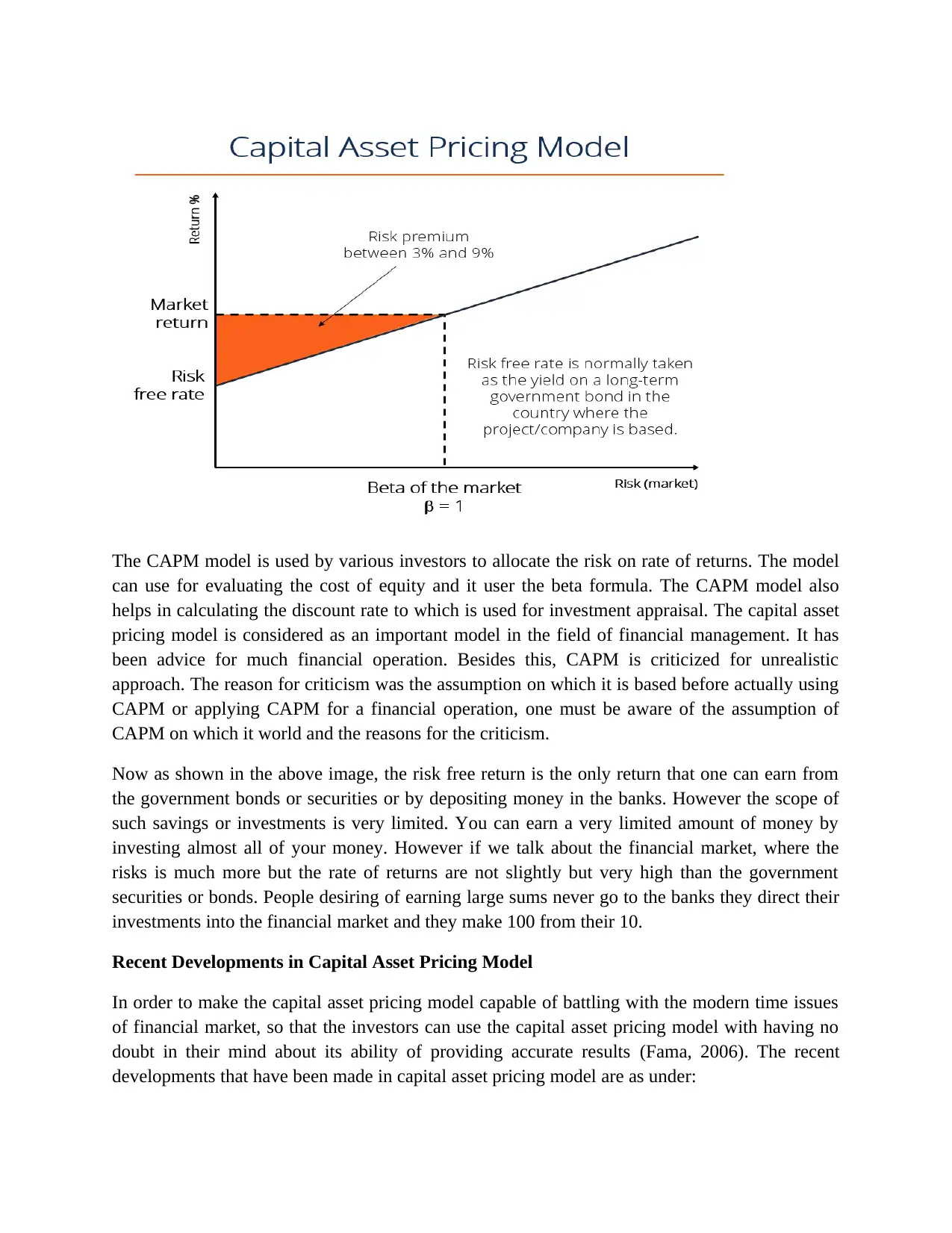

Now this formula with a diagram is as under:

Ra = Rrf + [Ba x (Rm – Rrf)]

Where:

Ra= Stands for the expected return on security

Rrf= Risk Free Return

Ba= Beta of the Security

Rm= Expected return on the security

can make investments with government banks in their saving accounts, where you will get a

proper rate of return but it will be quite low, if you compare it with the rate of return of the

financial market. The only benefit you will get on your money with the government bonds or

government banks is that your money is safe and will grow on a very low rate.

Now we are going to discuss, how capital asset pricing model came into existence. As mentioned

in the introduction paragraph, the concept of capital asset pricing model was brought into

existence by the financial economist called “William Sharpe” in the year 1970. He brought this

concept in one of his book. He told that capital asset pricing model will theoretically provide all

the answers to the questions of an investor. In his model of capital asset pricing model, he

mentioned that the expected rate of return, the return which is risk free, the risk and the risk of

the market can be easily find out and on these basis the investor can actually make investments

that yields him more and more returns with lesser risks. However low risk and high returns are

just a myth (Fama, 2012). There is nothing like that in financial market till date. No investor,

economist, financial analyst has found any measure or means to bring the risk to the minimum

and the return to the maximum. Now if we talk about, how capital asset pricing model works,

then first of all we need to understand that the capital asset pricing model is nothing but a

formula that if correctly applied on an investment will give you a close or an accurate result.

Now this formula with a diagram is as under:

Ra = Rrf + [Ba x (Rm – Rrf)]

Where:

Ra= Stands for the expected return on security

Rrf= Risk Free Return

Ba= Beta of the Security

Rm= Expected return on the security

The CAPM model is used by various investors to allocate the risk on rate of returns. The model

can use for evaluating the cost of equity and it user the beta formula. The CAPM model also

helps in calculating the discount rate to which is used for investment appraisal. The capital asset

pricing model is considered as an important model in the field of financial management. It has

been advice for much financial operation. Besides this, CAPM is criticized for unrealistic

approach. The reason for criticism was the assumption on which it is based before actually using

CAPM or applying CAPM for a financial operation, one must be aware of the assumption of

CAPM on which it world and the reasons for the criticism.

Now as shown in the above image, the risk free return is the only return that one can earn from

the government bonds or securities or by depositing money in the banks. However the scope of

such savings or investments is very limited. You can earn a very limited amount of money by

investing almost all of your money. However if we talk about the financial market, where the

risks is much more but the rate of returns are not slightly but very high than the government

securities or bonds. People desiring of earning large sums never go to the banks they direct their

investments into the financial market and they make 100 from their 10.

Recent Developments in Capital Asset Pricing Model

In order to make the capital asset pricing model capable of battling with the modern time issues

of financial market, so that the investors can use the capital asset pricing model with having no

doubt in their mind about its ability of providing accurate results (Fama, 2006). The recent

developments that have been made in capital asset pricing model are as under:

can use for evaluating the cost of equity and it user the beta formula. The CAPM model also

helps in calculating the discount rate to which is used for investment appraisal. The capital asset

pricing model is considered as an important model in the field of financial management. It has

been advice for much financial operation. Besides this, CAPM is criticized for unrealistic

approach. The reason for criticism was the assumption on which it is based before actually using

CAPM or applying CAPM for a financial operation, one must be aware of the assumption of

CAPM on which it world and the reasons for the criticism.

Now as shown in the above image, the risk free return is the only return that one can earn from

the government bonds or securities or by depositing money in the banks. However the scope of

such savings or investments is very limited. You can earn a very limited amount of money by

investing almost all of your money. However if we talk about the financial market, where the

risks is much more but the rate of returns are not slightly but very high than the government

securities or bonds. People desiring of earning large sums never go to the banks they direct their

investments into the financial market and they make 100 from their 10.

Recent Developments in Capital Asset Pricing Model

In order to make the capital asset pricing model capable of battling with the modern time issues

of financial market, so that the investors can use the capital asset pricing model with having no

doubt in their mind about its ability of providing accurate results (Fama, 2006). The recent

developments that have been made in capital asset pricing model are as under:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The concept of marginal utility or the concept of consumption has been introduced,

which has made the capital asset pricing model, an interesting investment method for

most of the investors in the financial markets.

Arbitrage Pricing Theory is another alternative to the capital asset pricing model and it

won’t be wrong to say that this method has its own importance and it is gaining a wide

acceptance (Fama, 2004).

Dynamic models have been developed as to bring in more evaluation of the investments

portfolios. In the capital asset pricing model only one parameter is required by the CAPM

to access the valuation of the investment but the development or the introduction of

dynamic models has bring in more insights for the assessment that is useful for the

investors. Dynamic models are the one that are now being used for insights information

of the investments.

One of the noticeable developments is the introduction of the high beta shares in the

capital asset pricing model. The high beta shares are the one through which one can get

maximum of the return on his/her shares though high beta shares are considered as the

worst performers still they gives the chance to the investor to double or triples their

money if they wish to.

The capital asset pricing model was initially developed or introduced by “Harry

Markowitz” but his model was not suitable or was not that much investor friendly, many

improvements were done and finally the accepted model was of the Mr. Sharpe. Till date

developments and improvements are being done on this model (Mona., 2016).

Benefits & Drawbacks of Capital Asset Pricing Model

Capital asset pricing model has its own benefits and drawback. First we will discuss about the

disadvantages of CAPM. CAPM has numerous limitation which needs to accessed before

application of the model

Assigning values: Before the application of CAPM value should be assigned to risk free

rate of return the returns from the market when the rate of return is not constant .it

changes on every day basis at that time the investment should be made in short time

investments for less risk. In case of ERP market givens the return which is actually a sum

of capital gains and dividend field for short team period it is not useful it can came crash

in the price of shares so for better returns the long term values should be taken. Beta

values are being calculated regularly because the value of beta is very fluctuating and

keeps on changing time by time.

No taxation: There is on transaction cost ,no divided tax on capital gain tax

Availability of information: All the information is very easily accessible for the

investors.

which has made the capital asset pricing model, an interesting investment method for

most of the investors in the financial markets.

Arbitrage Pricing Theory is another alternative to the capital asset pricing model and it

won’t be wrong to say that this method has its own importance and it is gaining a wide

acceptance (Fama, 2004).

Dynamic models have been developed as to bring in more evaluation of the investments

portfolios. In the capital asset pricing model only one parameter is required by the CAPM

to access the valuation of the investment but the development or the introduction of

dynamic models has bring in more insights for the assessment that is useful for the

investors. Dynamic models are the one that are now being used for insights information

of the investments.

One of the noticeable developments is the introduction of the high beta shares in the

capital asset pricing model. The high beta shares are the one through which one can get

maximum of the return on his/her shares though high beta shares are considered as the

worst performers still they gives the chance to the investor to double or triples their

money if they wish to.

The capital asset pricing model was initially developed or introduced by “Harry

Markowitz” but his model was not suitable or was not that much investor friendly, many

improvements were done and finally the accepted model was of the Mr. Sharpe. Till date

developments and improvements are being done on this model (Mona., 2016).

Benefits & Drawbacks of Capital Asset Pricing Model

Capital asset pricing model has its own benefits and drawback. First we will discuss about the

disadvantages of CAPM. CAPM has numerous limitation which needs to accessed before

application of the model

Assigning values: Before the application of CAPM value should be assigned to risk free

rate of return the returns from the market when the rate of return is not constant .it

changes on every day basis at that time the investment should be made in short time

investments for less risk. In case of ERP market givens the return which is actually a sum

of capital gains and dividend field for short team period it is not useful it can came crash

in the price of shares so for better returns the long term values should be taken. Beta

values are being calculated regularly because the value of beta is very fluctuating and

keeps on changing time by time.

No taxation: There is on transaction cost ,no divided tax on capital gain tax

Availability of information: All the information is very easily accessible for the

investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Based on old theory: The theory was given by William Sharpe in 1964 as factor model.

It should be altered according to the latest requirements.

It is not that the CAPM theory is only based on limitation it has same good benefits as well

Simple and easy: The theory and CAPM is very simple and easy to understand it can be

used by anyone such as investors or financial managers.

Diversified portfolio: Assumption which includes diversified portfolio held by the

investors is very relatable.

Systematic risk: Due to diversified portfolio unsystematic risk has been removed

Reliable method: The CAPM method is reliable. It effectively calculates of the risk.

Conclusion

After going through all the facts and information about the capital asset pricing model, a detailed

conclusion has been provided here. Capital asset pricing model is no doubt earning a good name

amongst the economists or the investors. It is useful too while calculating the expected rate of

returns on riskier investments. The recent developments in the capital asset pricing model shows

that it is now gaining attention and acceptance at a wide scale, however it is still to be loved by

everyone. Early in the year 1980, the capital asset pricing model received much criticism and it

was tested by few economists. The outcome of applying it on the investments didn’t brought out

any noticeable result, which further proved that the capital asset pricing model does not provides

any accurate result. However, here the thing worth mentioning is that most of the economists

find capital asset pricing model as a useful base for investments, though it does not provide any

full proof results but it does provides some guidelines for the investments that proves out to be

useful for the investor. All in all the final conclusion about capital asset pricing model is that,

despite of having much criticism, the capital asset pricing model provides not an accurate but a

better understanding and results about the returns and risk of an investment and it can be used

but keeping certain things in mind.

It should be altered according to the latest requirements.

It is not that the CAPM theory is only based on limitation it has same good benefits as well

Simple and easy: The theory and CAPM is very simple and easy to understand it can be

used by anyone such as investors or financial managers.

Diversified portfolio: Assumption which includes diversified portfolio held by the

investors is very relatable.

Systematic risk: Due to diversified portfolio unsystematic risk has been removed

Reliable method: The CAPM method is reliable. It effectively calculates of the risk.

Conclusion

After going through all the facts and information about the capital asset pricing model, a detailed

conclusion has been provided here. Capital asset pricing model is no doubt earning a good name

amongst the economists or the investors. It is useful too while calculating the expected rate of

returns on riskier investments. The recent developments in the capital asset pricing model shows

that it is now gaining attention and acceptance at a wide scale, however it is still to be loved by

everyone. Early in the year 1980, the capital asset pricing model received much criticism and it

was tested by few economists. The outcome of applying it on the investments didn’t brought out

any noticeable result, which further proved that the capital asset pricing model does not provides

any accurate result. However, here the thing worth mentioning is that most of the economists

find capital asset pricing model as a useful base for investments, though it does not provide any

full proof results but it does provides some guidelines for the investments that proves out to be

useful for the investor. All in all the final conclusion about capital asset pricing model is that,

despite of having much criticism, the capital asset pricing model provides not an accurate but a

better understanding and results about the returns and risk of an investment and it can be used

but keeping certain things in mind.

Bibliography

Ang, A..R.J.H.Y.X.a.X.Z., 2006. The cross section volatility and Expected Returns. The Journal of Finance,

61(1), pp.259 - 299.

Banz, R., 2000. The Relation between Return and Market Values of Common Stock. Journal of Financial

Economics, 9, pp.3-18.

Bejjani, L., 2009. Financial Risk Management: Testing the CAPM of Citigroup Stocks. New York: American

University of Beirut, Department of Economics, 2009.

Fama, E., 2004. The Capital Asset Pricing Model: Theory and Evidence. JOURNAL OF ECONOMIC

PERSPECTIVES, 18(3), pp.25-26.

Fama, E.F.a.K.R.F., 2006. The value premium of CAPM. The Journal of Finance, 61(5), pp.2163 - 2185.

Fama, E.F.a.K.R.F., 2012. Size, Value, and Momentum in International Stock Returns. Journal of Financial

Economics, 105(3), pp., 457 - 472.

Giovanis, E., 2010. Application of Capital Asset Pricing (CAPM) and Arbitrage Pricing. Germany.

Hidek, I.i., 2011. Equilibrium of Asset Pricing Model.

Milton, F., 2012. CAPM Introduction. New York: Cengage Publications.

Mizrach, B., 2014. Testing the CAPM & 25 Portfolios.

Mona., E., 2016. The Capital Asset Pricing Model: An Overview of the Theory. International Journal of

Economics and Finance , 7(1).

Ang, A..R.J.H.Y.X.a.X.Z., 2006. The cross section volatility and Expected Returns. The Journal of Finance,

61(1), pp.259 - 299.

Banz, R., 2000. The Relation between Return and Market Values of Common Stock. Journal of Financial

Economics, 9, pp.3-18.

Bejjani, L., 2009. Financial Risk Management: Testing the CAPM of Citigroup Stocks. New York: American

University of Beirut, Department of Economics, 2009.

Fama, E., 2004. The Capital Asset Pricing Model: Theory and Evidence. JOURNAL OF ECONOMIC

PERSPECTIVES, 18(3), pp.25-26.

Fama, E.F.a.K.R.F., 2006. The value premium of CAPM. The Journal of Finance, 61(5), pp.2163 - 2185.

Fama, E.F.a.K.R.F., 2012. Size, Value, and Momentum in International Stock Returns. Journal of Financial

Economics, 105(3), pp., 457 - 472.

Giovanis, E., 2010. Application of Capital Asset Pricing (CAPM) and Arbitrage Pricing. Germany.

Hidek, I.i., 2011. Equilibrium of Asset Pricing Model.

Milton, F., 2012. CAPM Introduction. New York: Cengage Publications.

Mizrach, B., 2014. Testing the CAPM & 25 Portfolios.

Mona., E., 2016. The Capital Asset Pricing Model: An Overview of the Theory. International Journal of

Economics and Finance , 7(1).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.