Financial Analysis Report: Dexter Plc, Philly Ltd, Sankrust Ltd

VerifiedAdded on 2021/02/22

|17

|4128

|107

Report

AI Summary

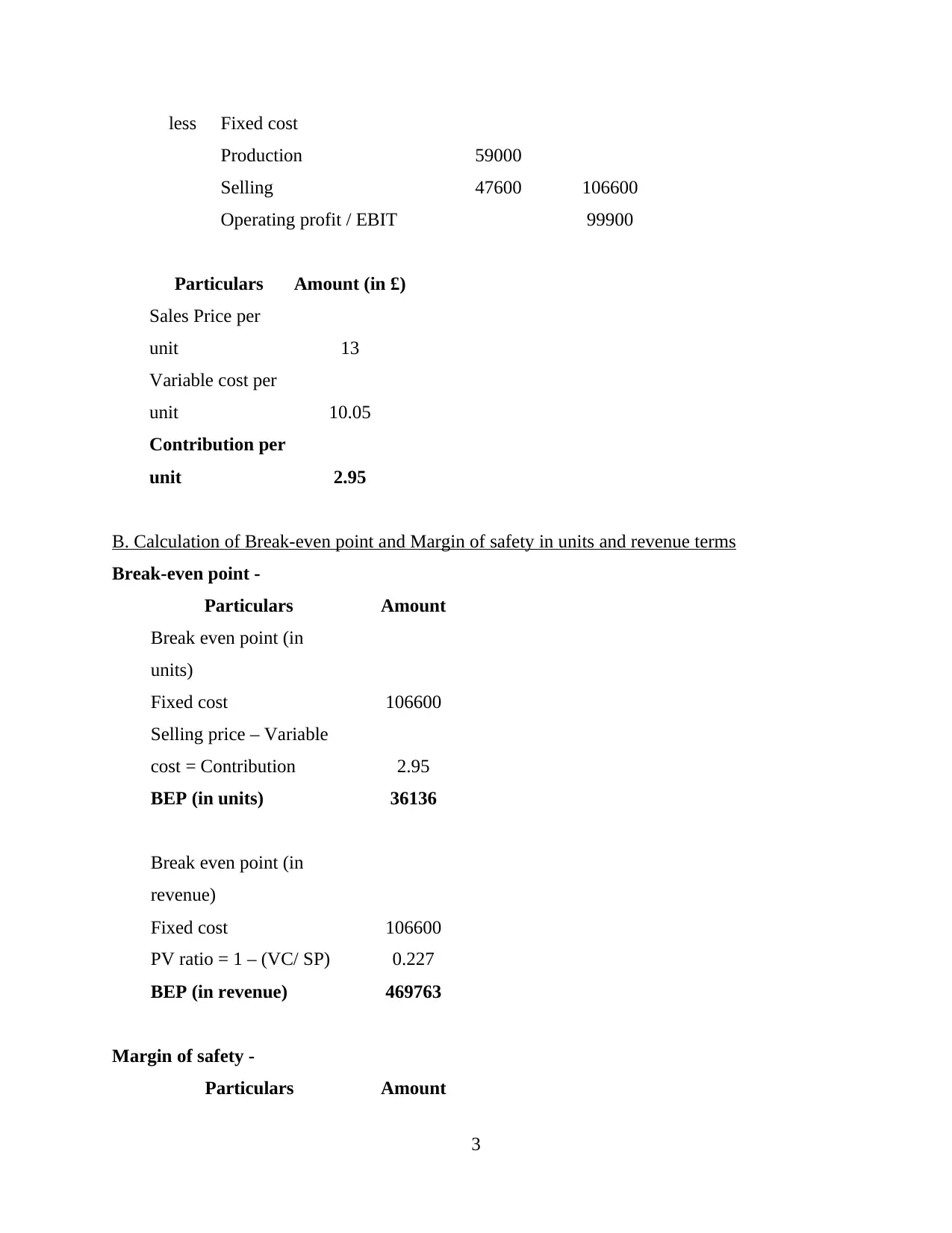

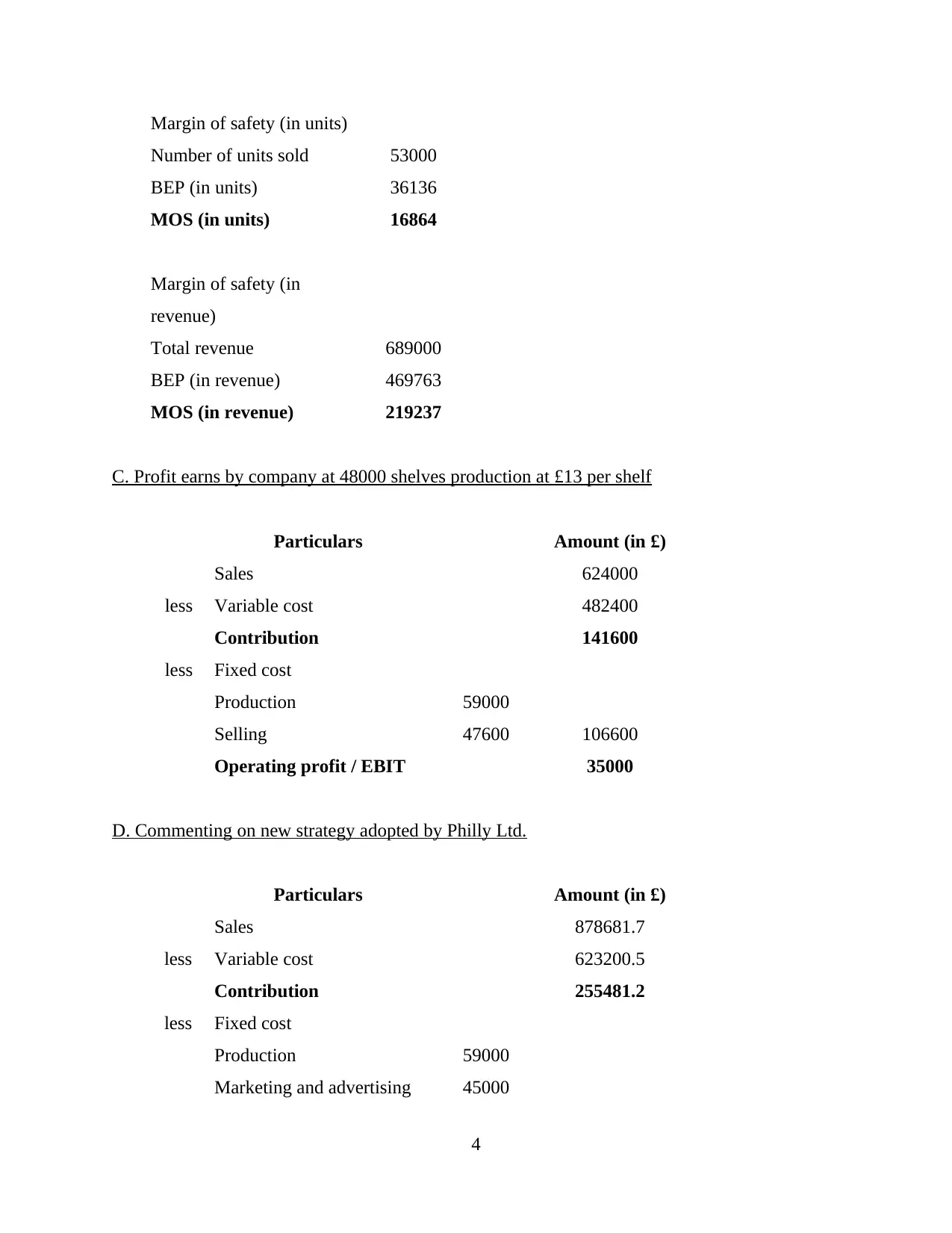

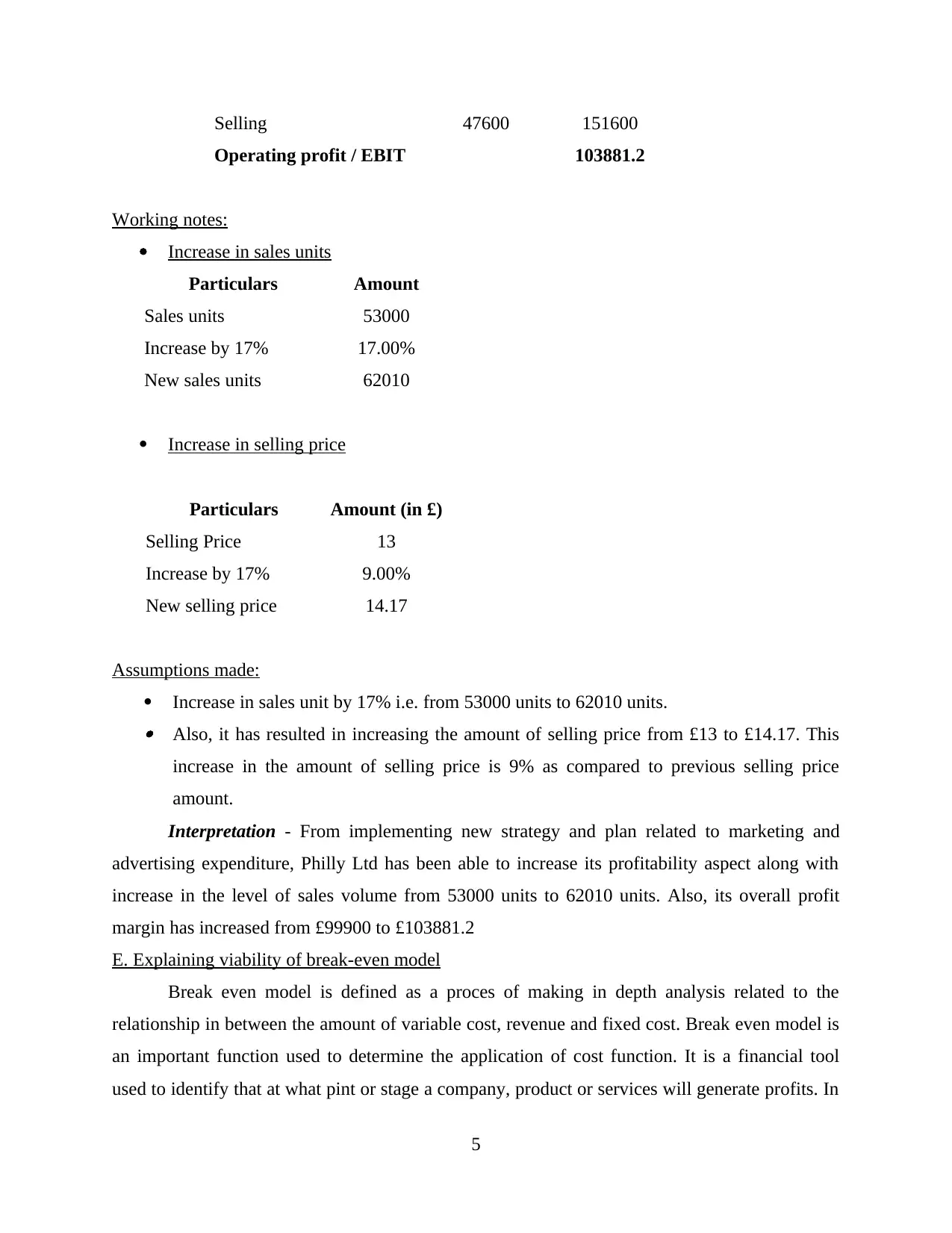

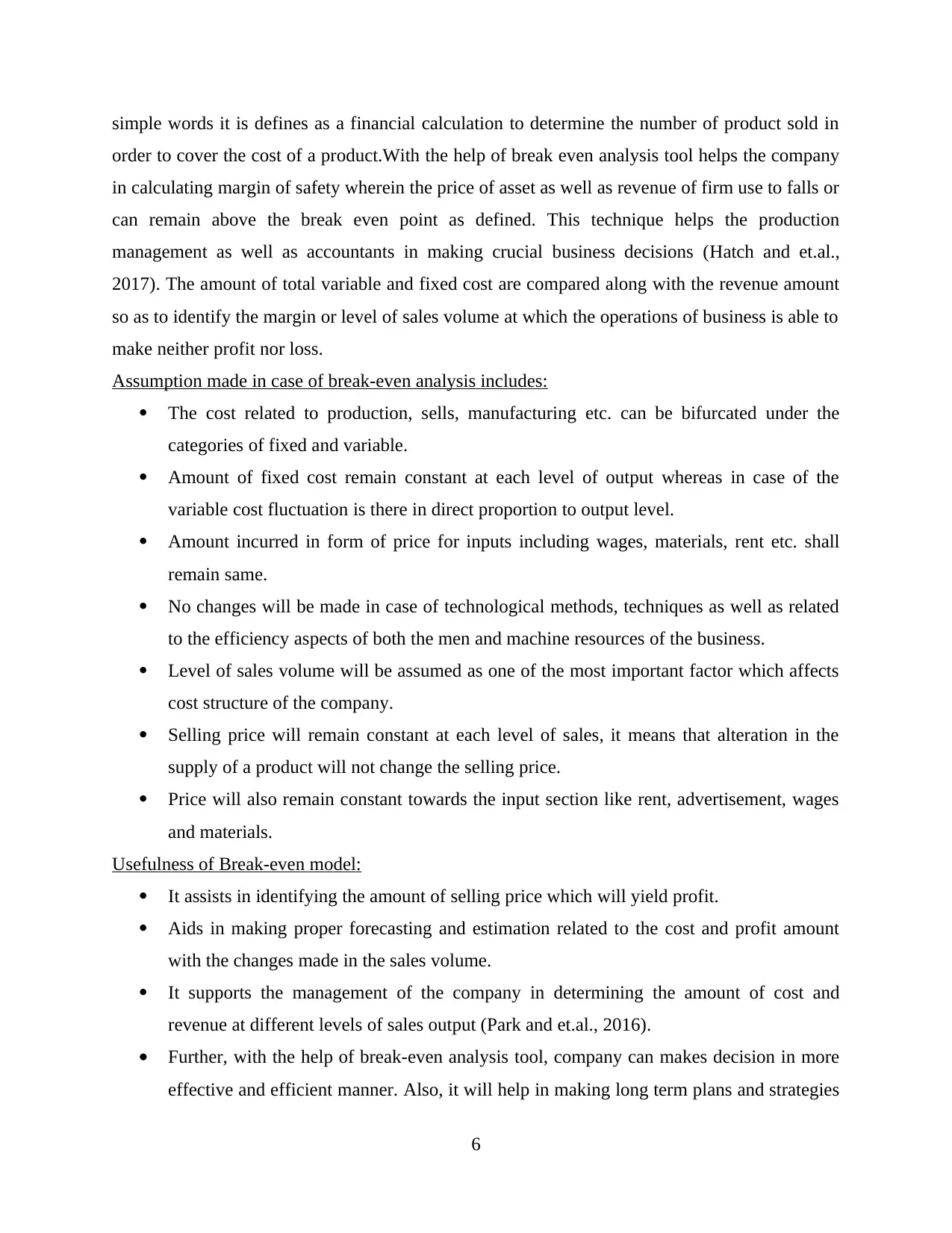

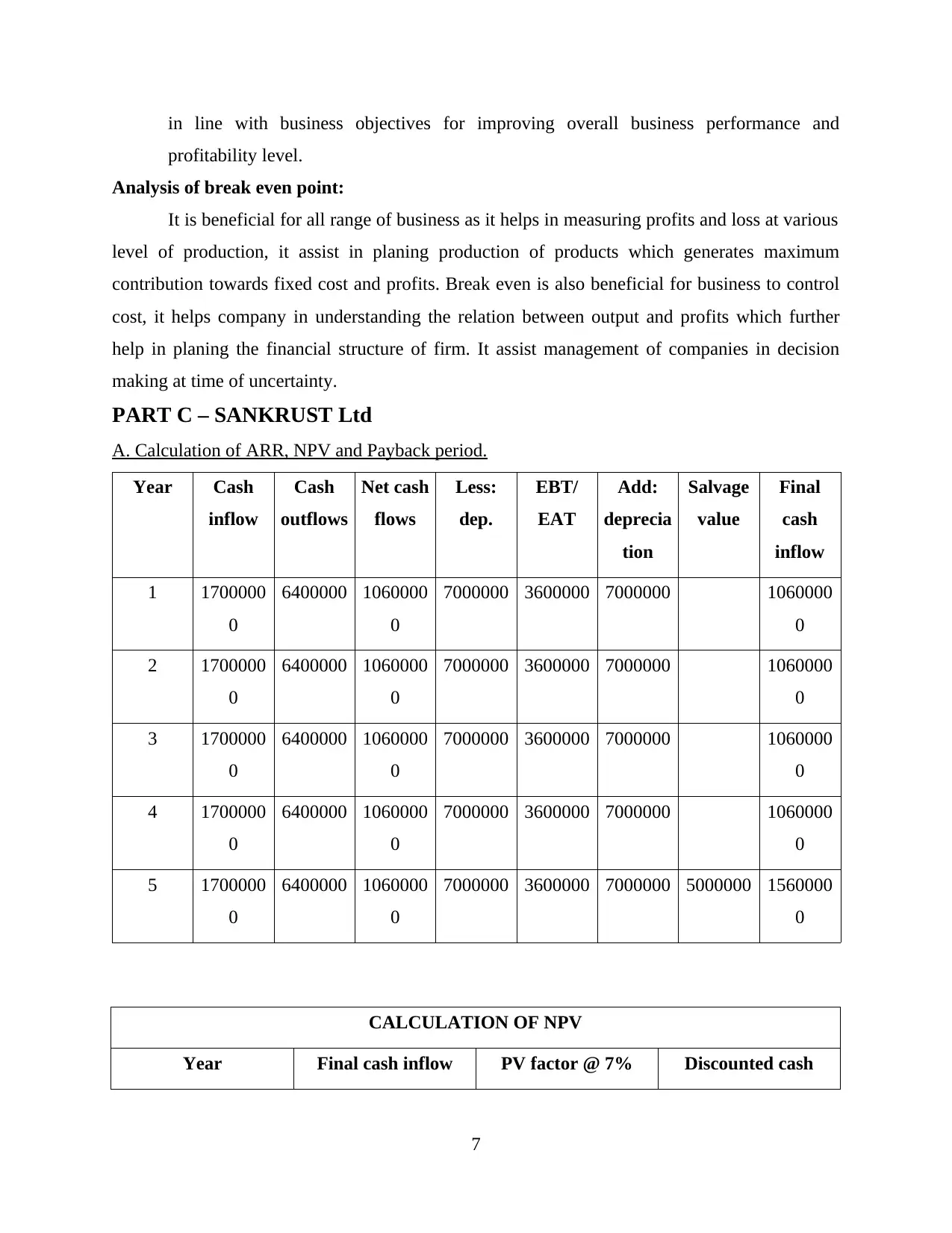

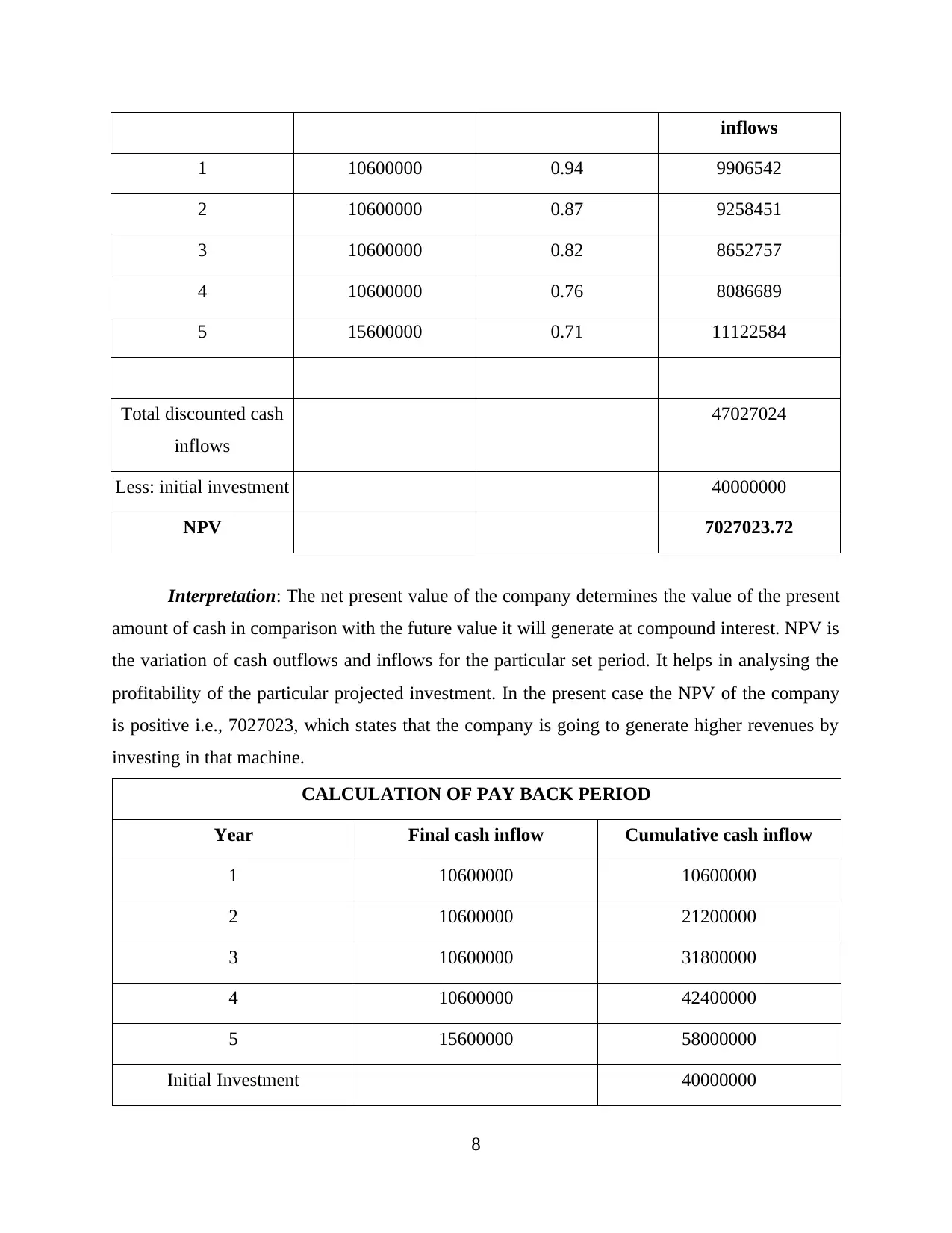

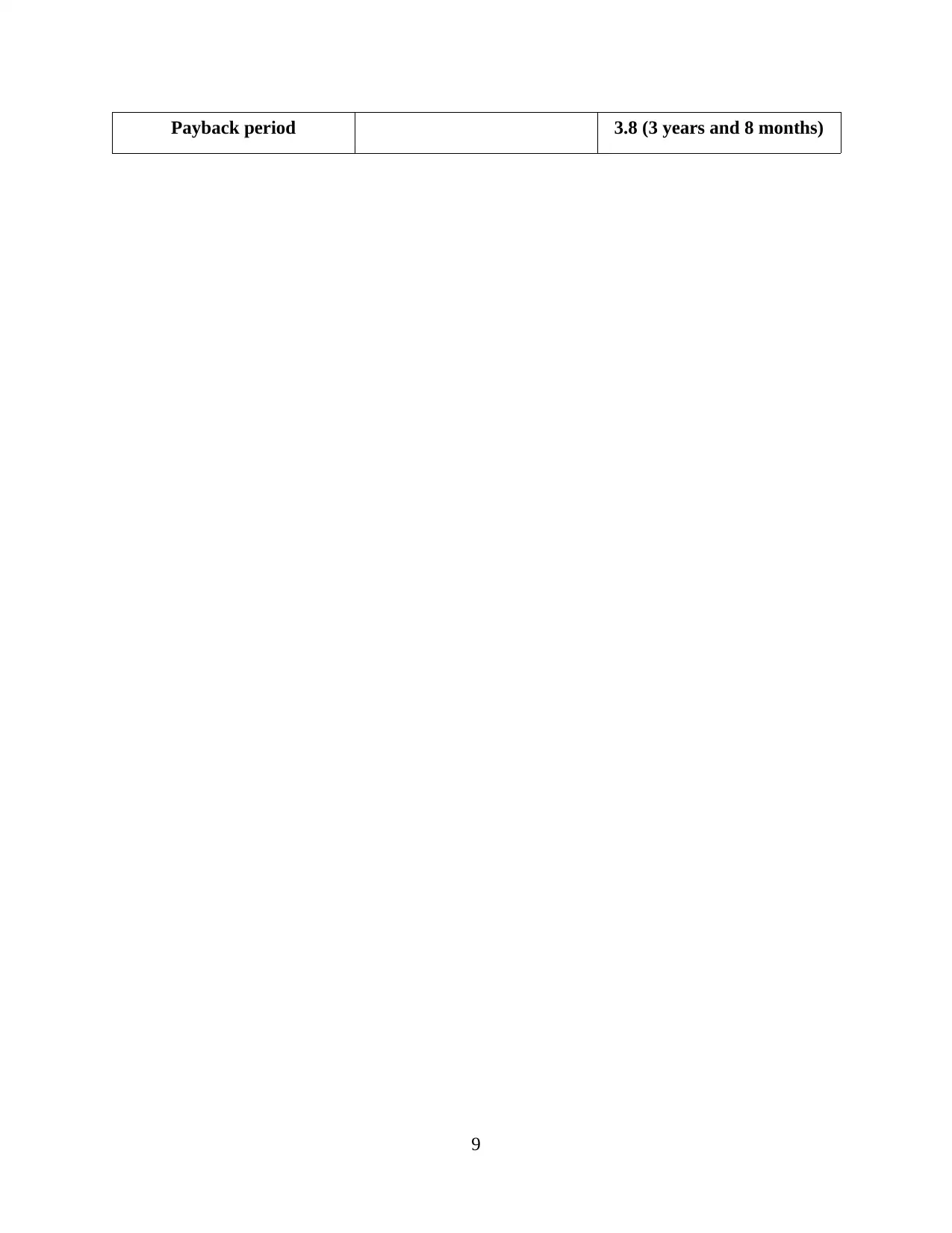

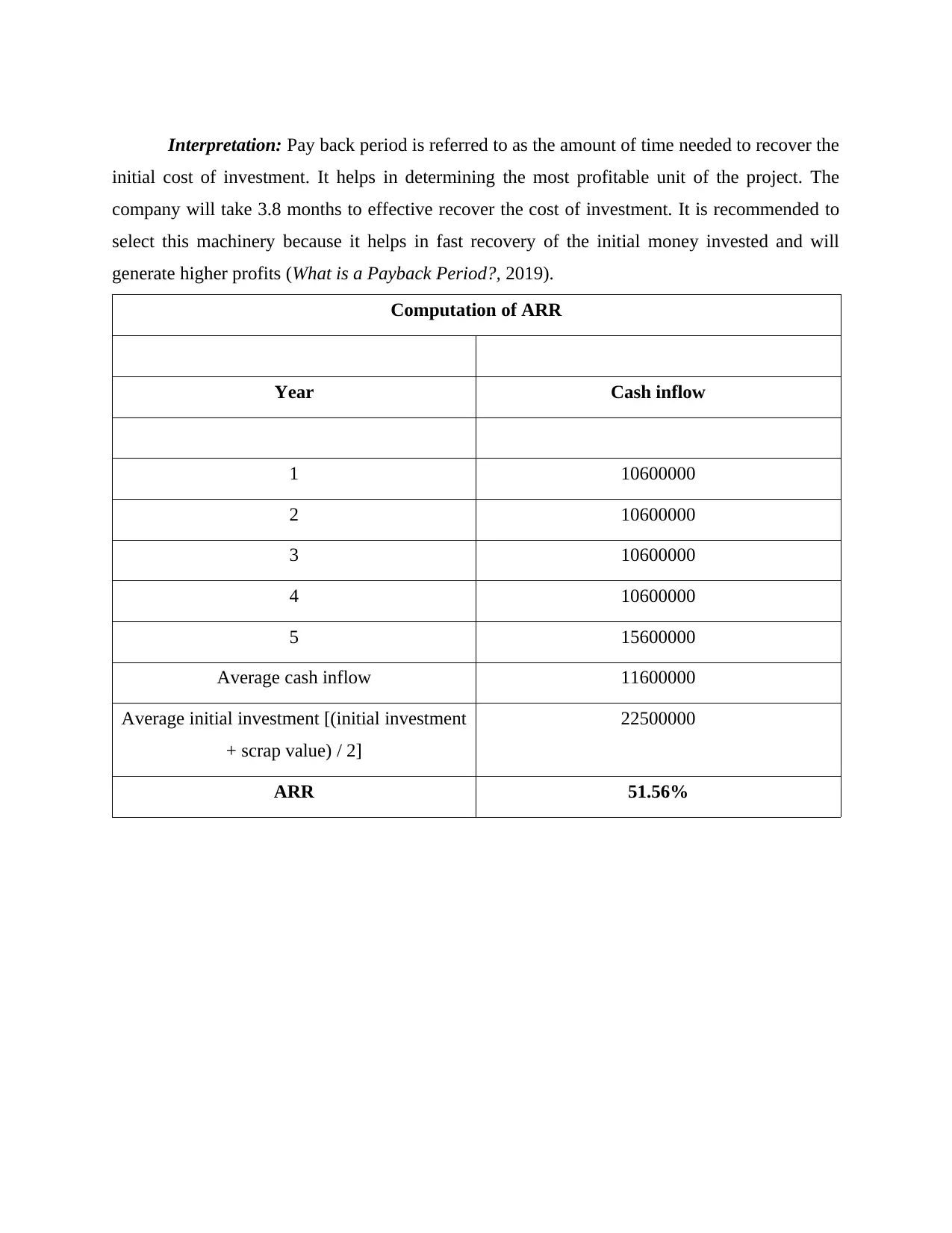

This report presents a financial analysis of three companies: Dexter Plc, Philly Ltd, and Sankrust Ltd. It includes the preparation of income statements and balance sheets for Dexter Plc, as well as calculations of contribution per unit, break-even points, and margin of safety for Philly Ltd. The report also examines the impact of a new marketing strategy on Philly Ltd's profitability and provides an explanation of the break-even model's viability. Furthermore, the report calculates the Average Rate of Return (ARR), Net Present Value (NPV), and payback period for Sankrust Ltd, and discusses the advantages and disadvantages of various investment appraisal techniques and the benefits and limitations of using budgets for strategic planning. The analysis provides insights into the financial performance and strategic considerations for each company, offering a comprehensive overview of their financial positions and investment decisions.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.