Report on Accounting and Finance: Analysis of Three Companies

VerifiedAdded on 2021/02/20

|19

|4303

|74

Report

AI Summary

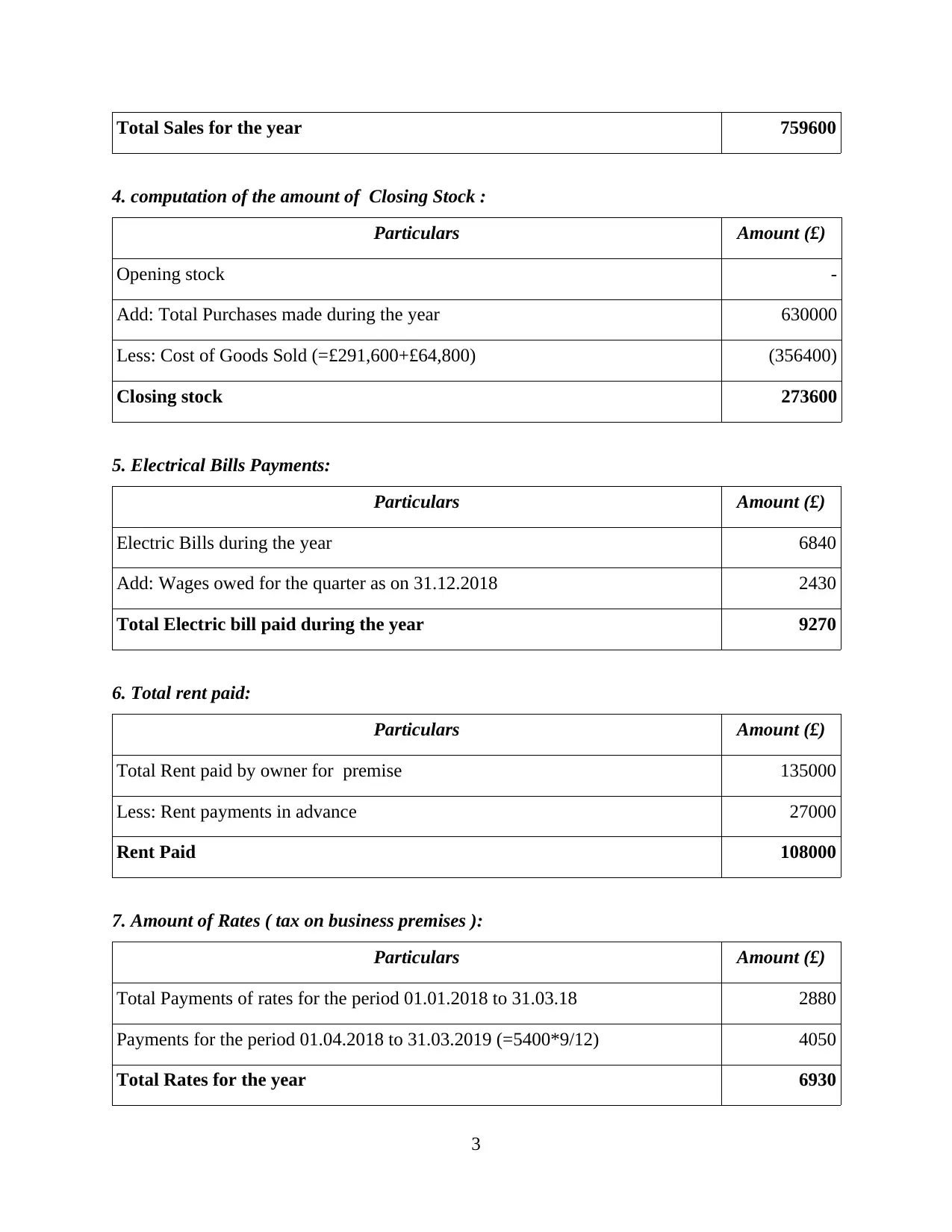

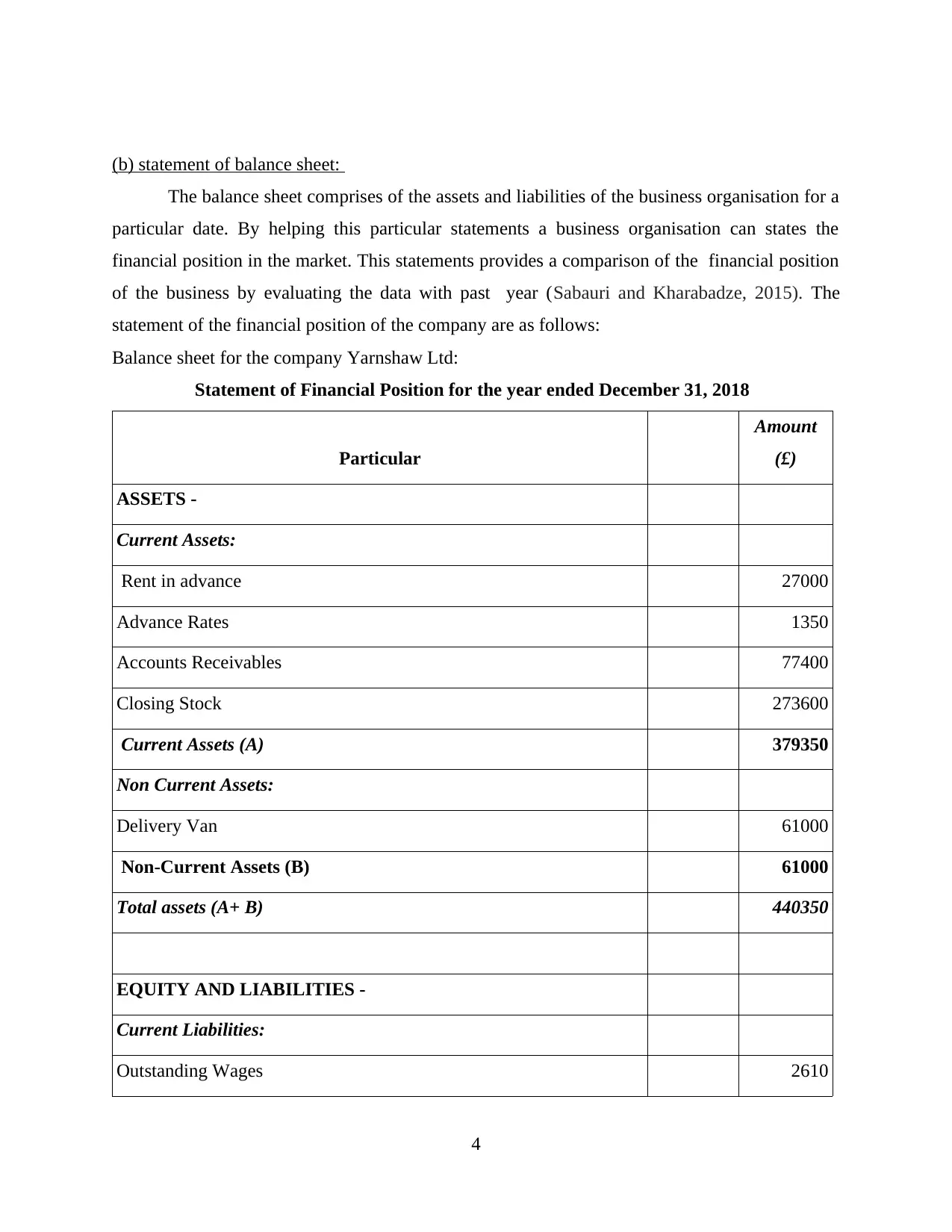

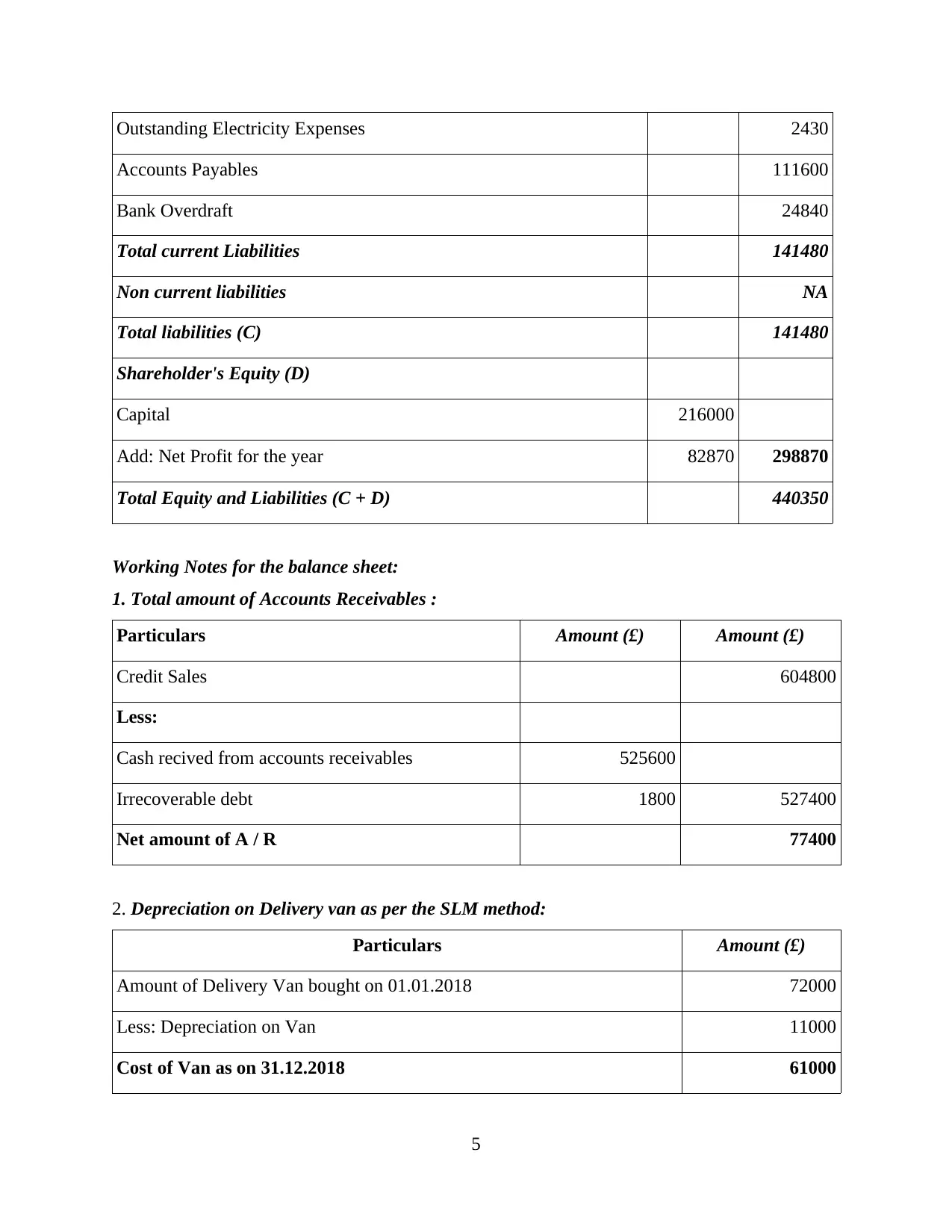

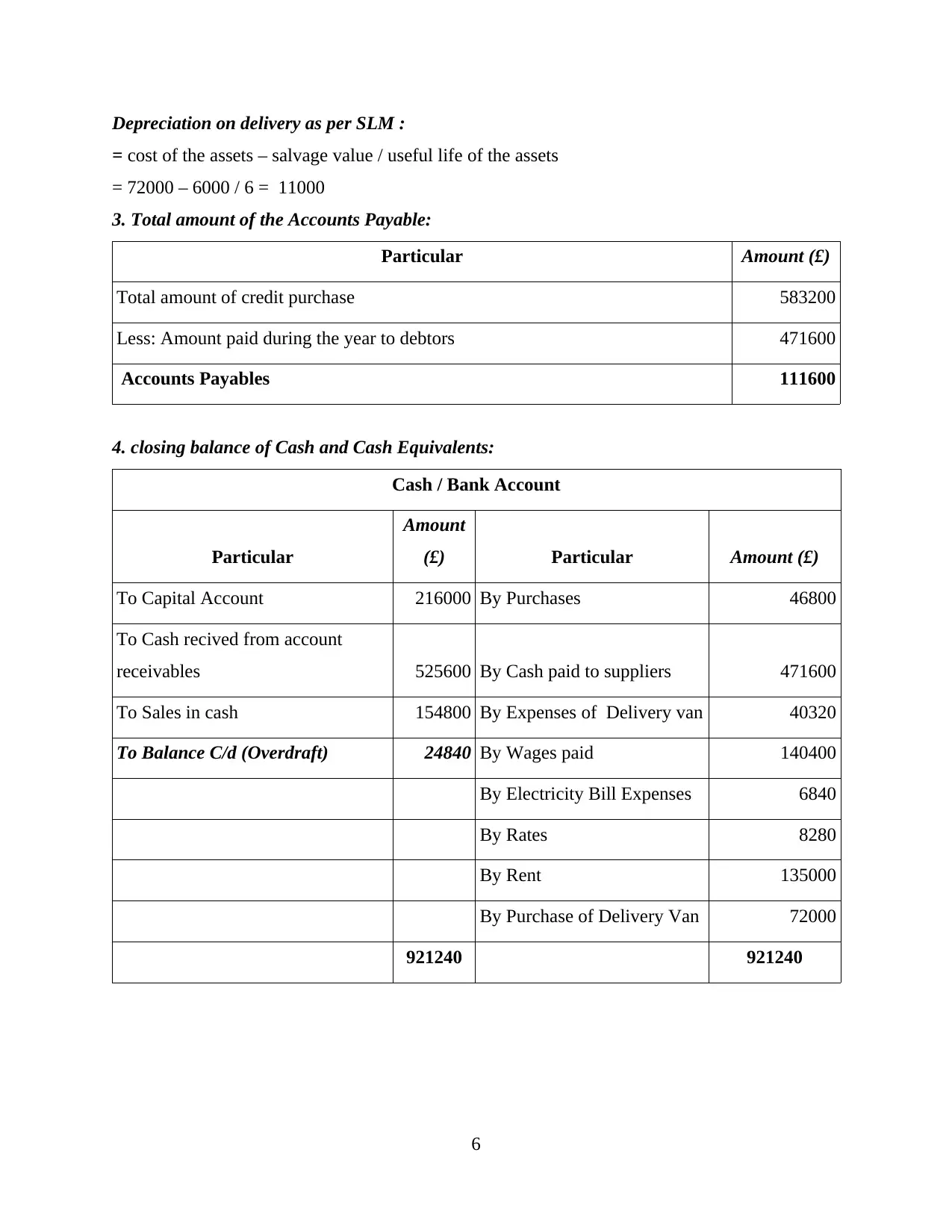

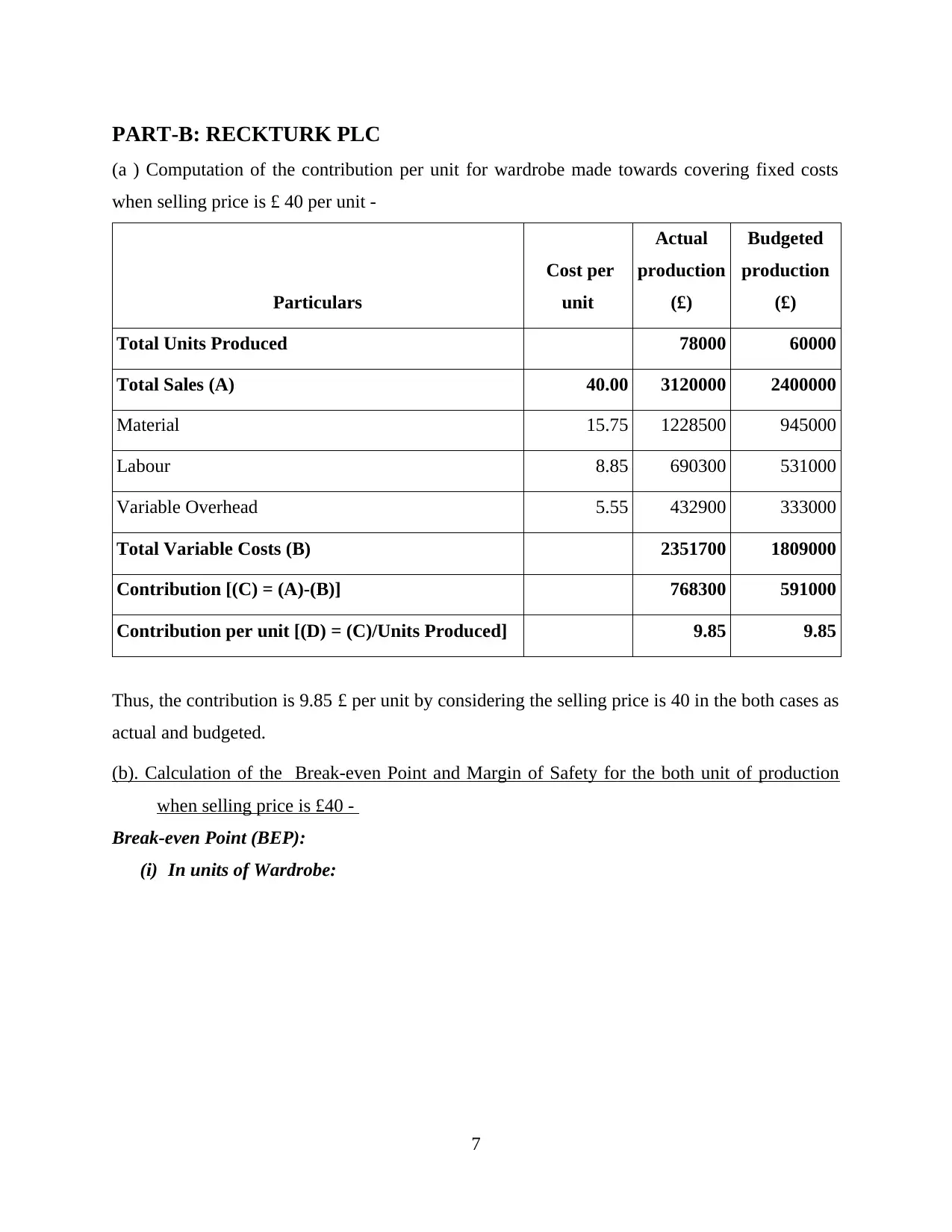

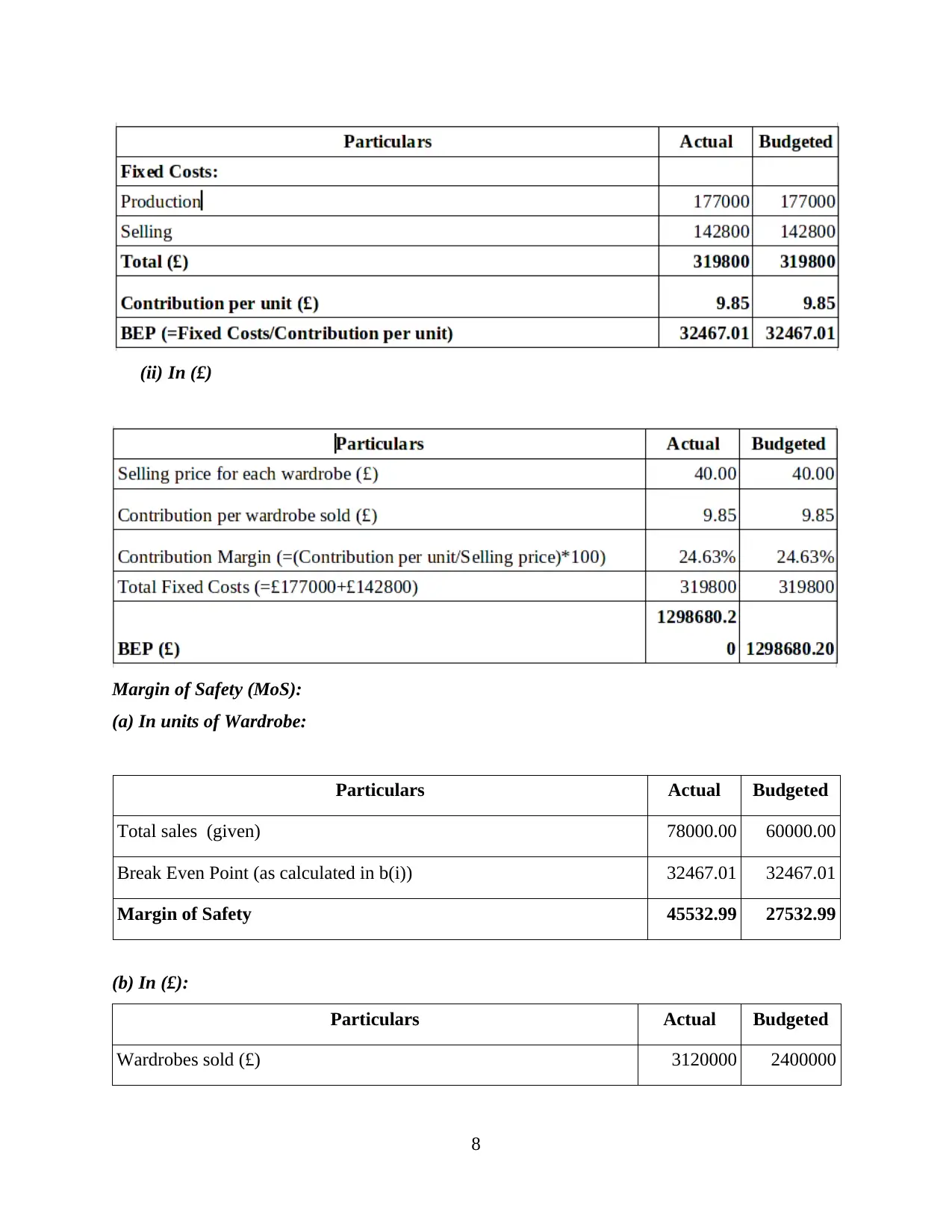

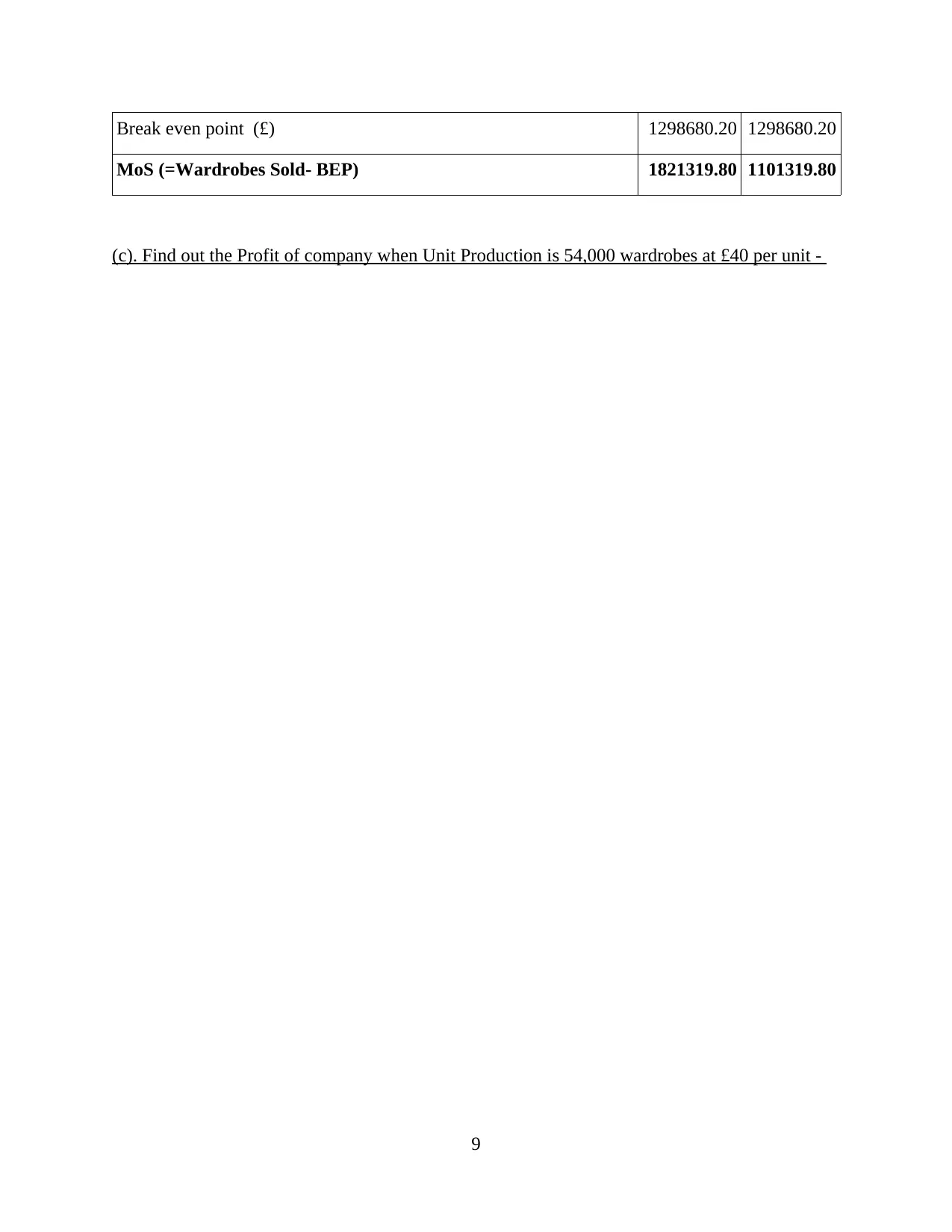

This comprehensive report provides an overview of key concepts in accounting and finance, including financial accounting, financial management, and management accounting. The report is divided into three parts, each focusing on a different company: YARNSHAW LIMITED, RECKTURK PLC, and ROSEVILLE PLC. Part A covers the preparation of a profit and loss statement and balance sheet for YARNSHAW LIMITED, including working notes for calculations. Part B analyzes RECKTURK PLC, calculating the break-even point and margin of safety, and evaluating the impact of marketing expenses on sales and profit. Part C focuses on ROSEVILLE PLC, recommending acceptance or rejection of capital budgeting projects using investment appraisal techniques and discussing the merits and limitations of budgets as a strategic planning tool. The report concludes with a discussion of the assumptions used in break-even analysis and provides relevant references.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.