Accounting and Finance Report: RACCA, RECKTURK, ROCKHAM PLC Analysis

VerifiedAdded on 2023/01/11

Finance Assessment

1

Paraphrase This Document

INTRODUCTION...........................................................................................................................3

PART-A: RACCA LIMITED..........................................................................................................3

a. Profit and Loss Statement...................................................................................................3

b. Statement of Balance Sheet................................................................................................7

PART-B: RECKTURK PLC.........................................................................................................12

a. Determining contribution per electric kettle made towards covering fixed costs when selling

price is £13:..........................................................................................................................12

b. Calculating Break-even Point and Margin of Safety when selling price is £13:..............12

c. Ascertaining Company Profit when Unit Production is 48,000 electric kettles at £13 per

unit........................................................................................................................................13

d. Assessing strategy for Stock stone Ltd Plc.......................................................................13

e. Identification of Underpinning Assumptions in Break-even Model................................14

PART-C: ROCKHAM PLC..........................................................................................................15

a. Recommendation of acceptance or rejection of Capital Budgeting Projects using Investment

Appraisal techniques............................................................................................................15

b. Report on key merits and limitations of various investment appraising techniques........17

c. Report on identification of key merits and demerits of using Budgets as a strategy planning

tool........................................................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

2

Accounting Process and Finance both these concepts are extremely interrelated yet

diverse fields. Concept of accounting is primarily associated with recognizing purchases and can

be assessed monetarily. While the Finance concept involves presentation in form of

different reports to the firm ’s stakeholders. These two components ensure that all the financial

transactions of corporation are properly recorded and communicated effectively to the business's

stakeholders. These allow both the acquisition and distribution of different financial resources

on part of managing personnel who really are accountable for making informed decisions

about same in an acceptable way (Ainsworth and Deines, 2019).

This study seeks to give a comprehensive account of the basic models, principles and

methods used throughout financial accounting as well as management accounting. For this

object, it highlights concept of preparation of company's financial statement such as P&L or

income statements, Statement of financial position, contribution calculation, Margin of

Safety, break-even level as in revenue and units. Further, various investment appraisal methods

used in decisions relating to the capital budgeting are evaluated along with advantages and

drawbacks of budget as strategic planning tool.

PART-A: RACCA LIMITED

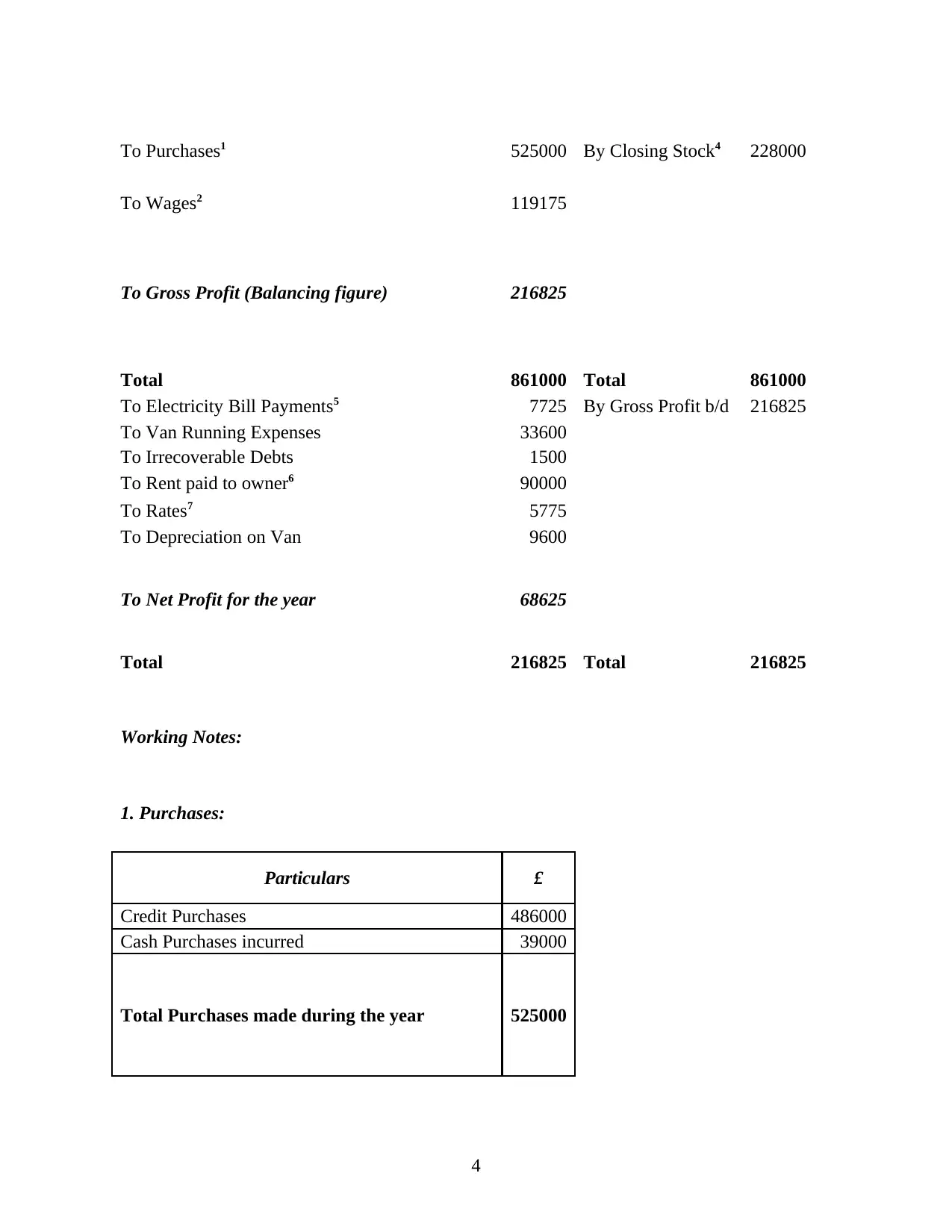

a. Profit and Loss Statement

To assess whether or not entity can expand or step in direction that aligns its goal and targets, an

entity seeks to assess the net profits gained for a particular time-span. An organisation’s Income

Statement is formed for this purpose, as well as aims to report company profits after paying for

taxes, debt, depreciation, as well as other expenditures (Shawver and Miller, 2017). This

gives Management and stakeholders of certain company, like Racca Ltd, a summary of

organisation’s profitability. organisation's profitability. This can be seen as follows:

Statement of Income for the year ended December 31, 2018

Particulars £ Particulars £

To Opening Stock - By Revenue3 633000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To Wages2 119175

To Gross Profit (Balancing figure) 216825

Total 861000 Total 861000

To Electricity Bill Payments5 7725 By Gross Profit b/d 216825

To Van Running Expenses 33600

To Irrecoverable Debts 1500

To Rent paid to owner6 90000

To Rates7 5775

To Depreciation on Van 9600

To Net Profit for the year 68625

Total 216825 Total 216825

Working Notes:

1. Purchases:

Particulars £

Credit Purchases 486000

Cash Purchases incurred 39000

Total Purchases made during the year 525000

4

Paraphrase This Document

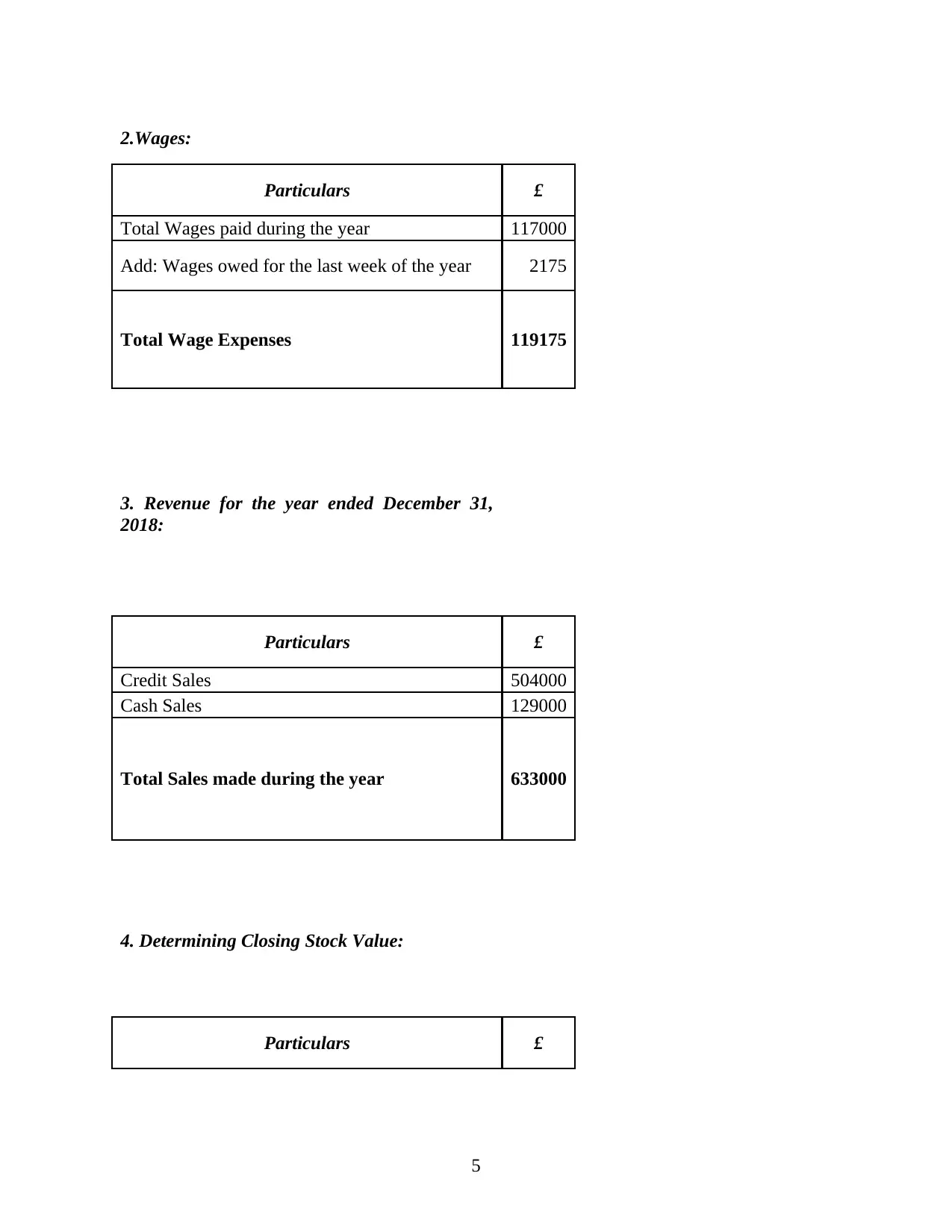

Particulars £

Total Wages paid during the year 117000

Add: Wages owed for the last week of the year 2175

Total Wage Expenses 119175

3. Revenue for the year ended December 31,

2018:

Particulars £

Credit Sales 504000

Cash Sales 129000

Total Sales made during the year 633000

4. Determining Closing Stock Value:

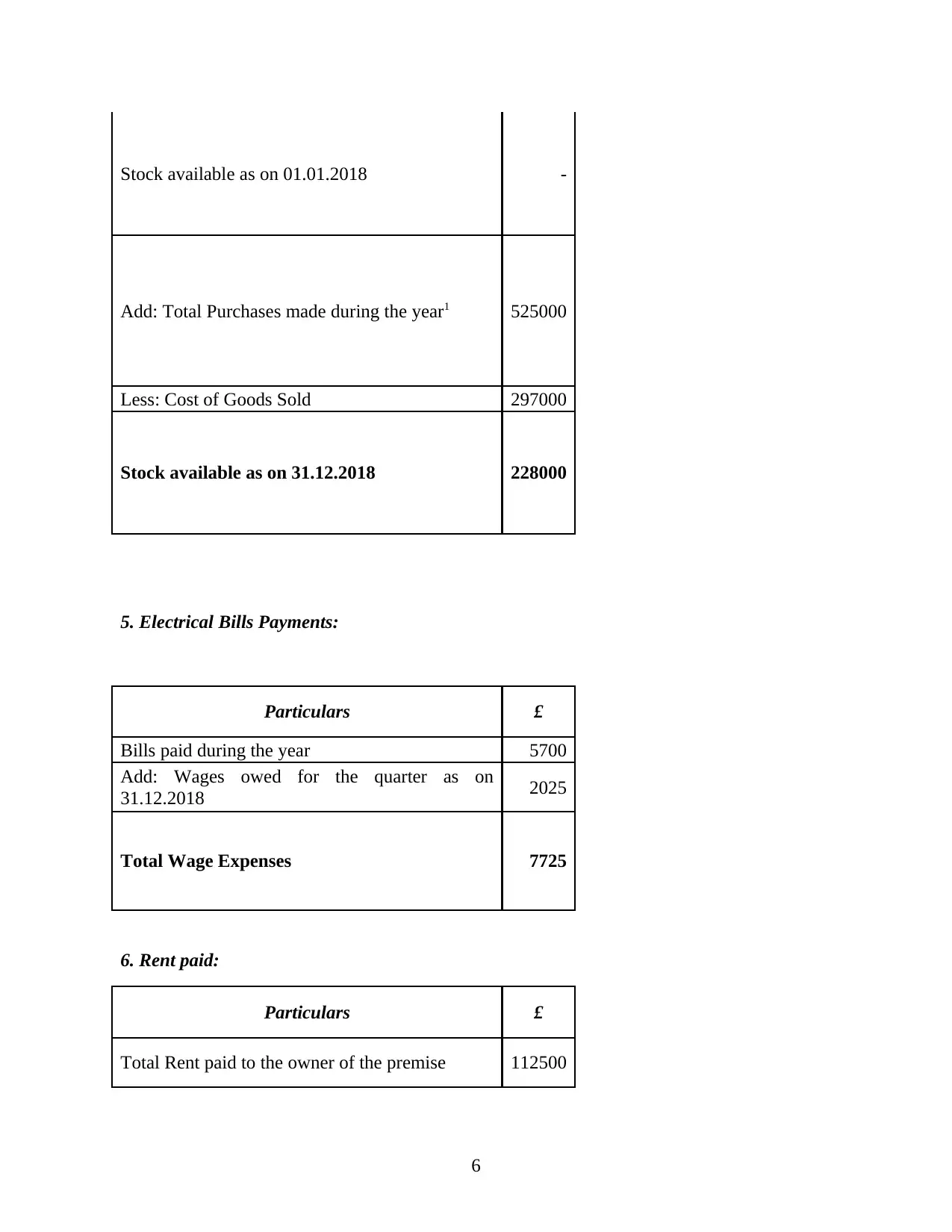

Particulars £

5

Add: Total Purchases made during the year1 525000

Less: Cost of Goods Sold 297000

Stock available as on 31.12.2018 228000

5. Electrical Bills Payments:

Particulars £

Bills paid during the year 5700

Add: Wages owed for the quarter as on

31.12.2018 2025

Total Wage Expenses 7725

6. Rent paid:

Particulars £

Total Rent paid to the owner of the premise 112500

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Rent Paid 90000

7. Rates:

Particulars £

Payments for the period 01.01.2018 to 31.03.18 2400

Payments for the period 01.04.2018 to

31.03.2018 (=5400*9/12) 4500

Total Rates for the year 6900

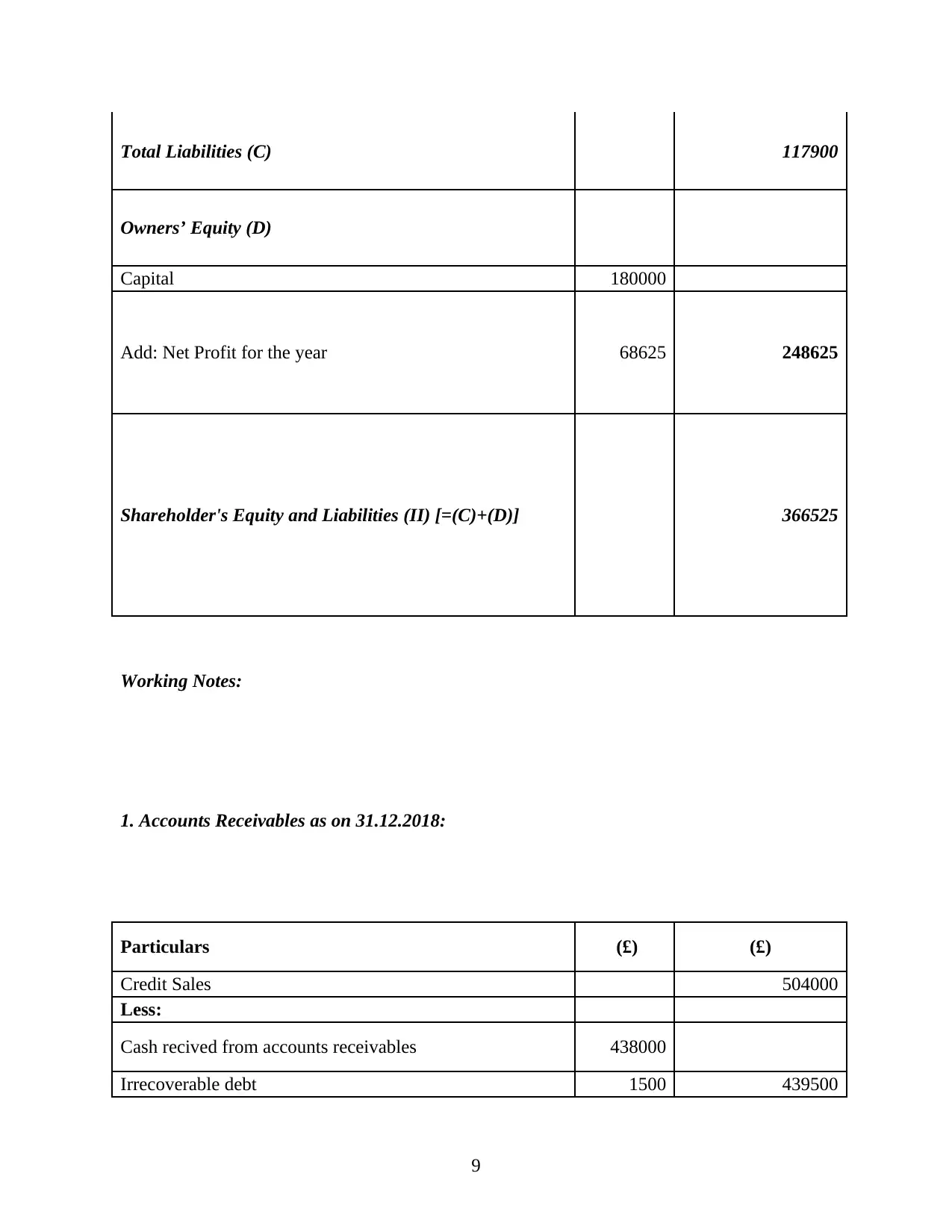

b. Statement of Balance Sheet

An additional element of process of financial reporting that shows financial

position of company at specific given time-frame is statement of Financial Position (Balance-

sheet). This offers comparability to those other organisations working within same sector and the

financial performance of the organization during past years in relative to current year (Webb and

Chaffer, 2016). Overall financial status of Racca Limited is shown in following statement, as

follows:

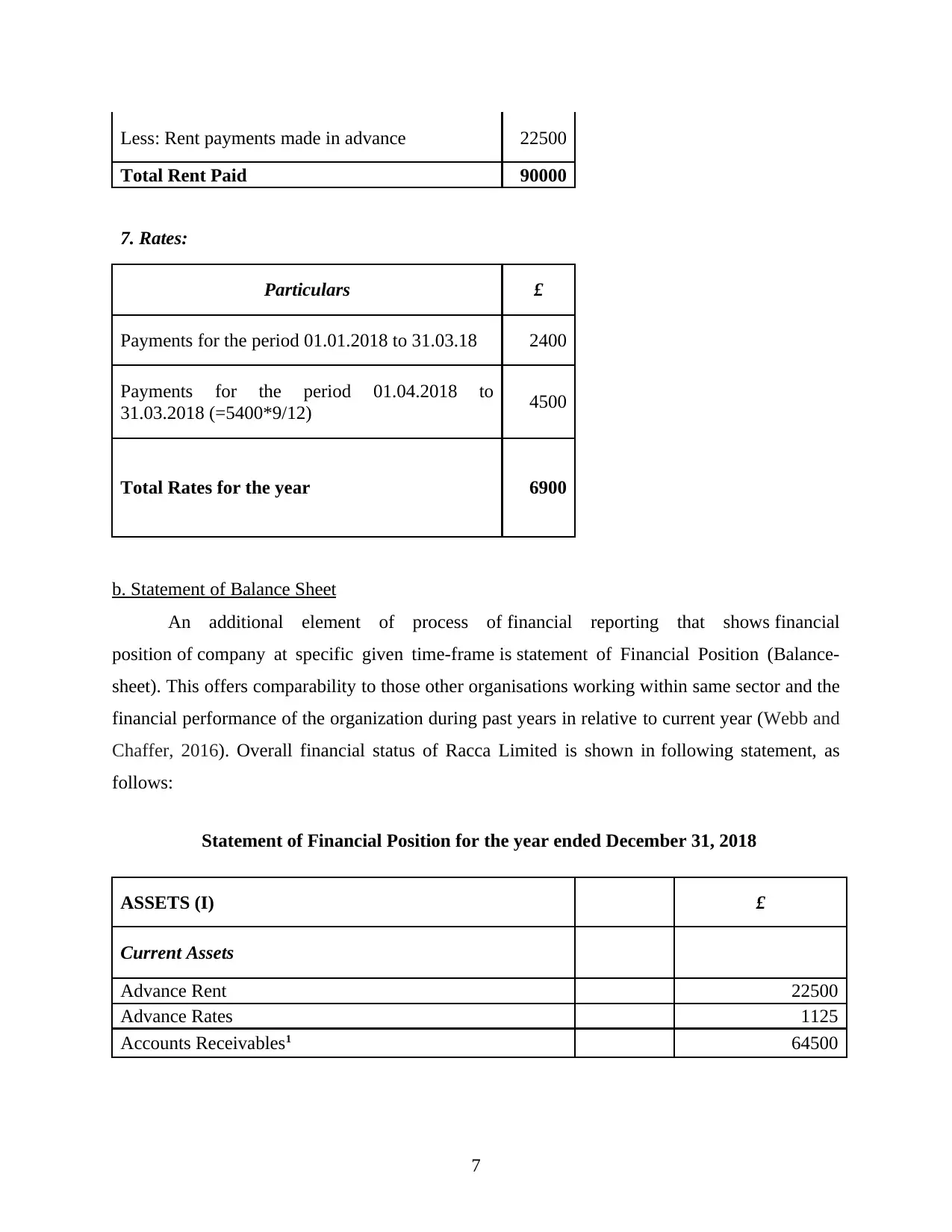

Statement of Financial Position for the year ended December 31, 2018

ASSETS (I) £

Current Assets

Advance Rent 22500

Advance Rates 1125

Accounts Receivables1 64500

7

Paraphrase This Document

Total Current Assets (A) 316125

Non Current Assets

Delivery Van2 50400

Total Non-Current Assets (B) 50400

Assets (I) [= (A) + (B)] 366525

LIABILITIES AND SHAREHOLDER'S EQUITY (II)

Current Liabilities

Owed Wages 2175

Owed Electricity Expenses 2025

Accounts Payables3 93000

Bank Overdraft4 20700

8

Owners’ Equity (D)

Capital 180000

Add: Net Profit for the year 68625 248625

Shareholder's Equity and Liabilities (II) [=(C)+(D)] 366525

Working Notes:

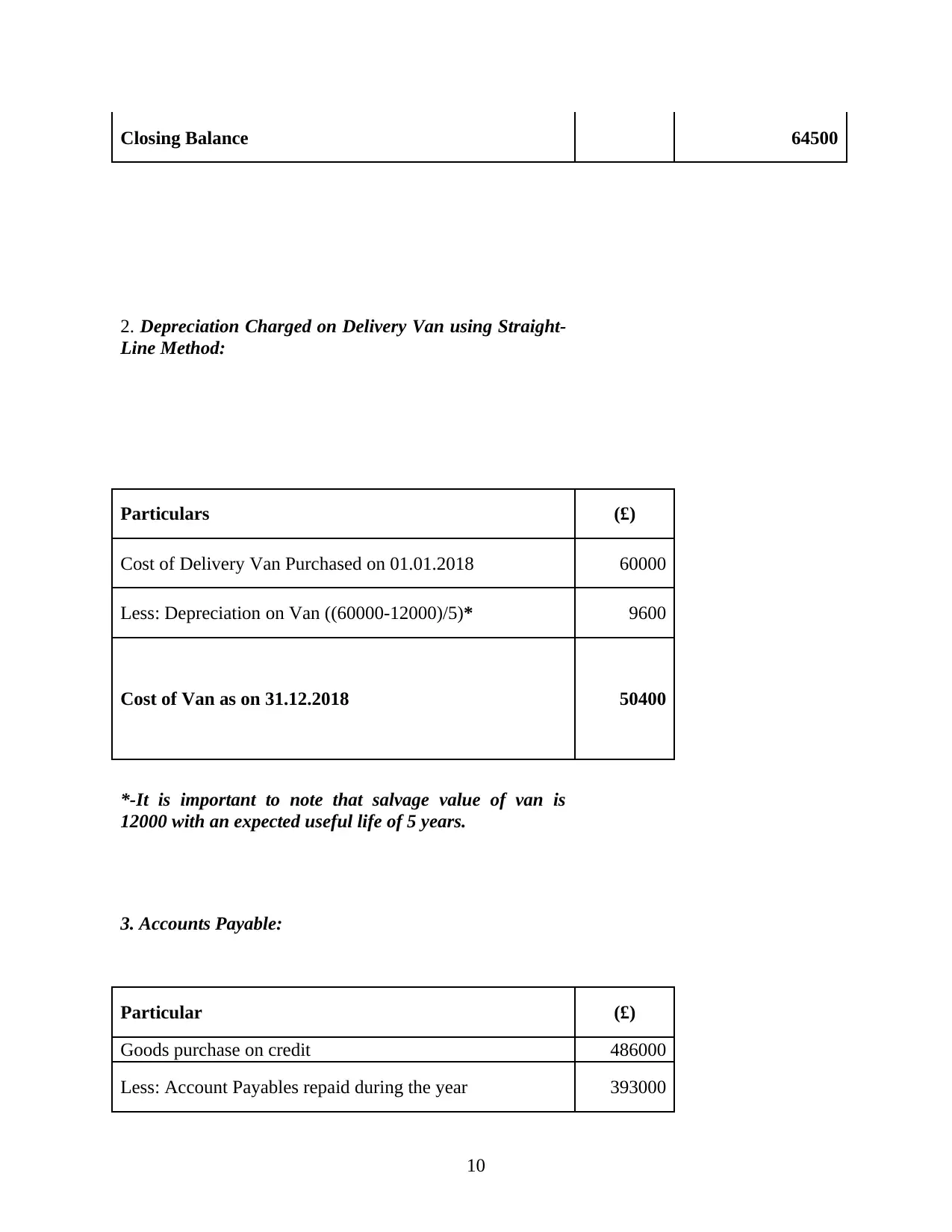

1. Accounts Receivables as on 31.12.2018:

Particulars (£) (£)

Credit Sales 504000

Less:

Cash recived from accounts receivables 438000

Irrecoverable debt 1500 439500

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Depreciation Charged on Delivery Van using Straight-

Line Method:

Particulars (£)

Cost of Delivery Van Purchased on 01.01.2018 60000

Less: Depreciation on Van ((60000-12000)/5)* 9600

Cost of Van as on 31.12.2018 50400

*-It is important to note that salvage value of van is

12000 with an expected useful life of 5 years.

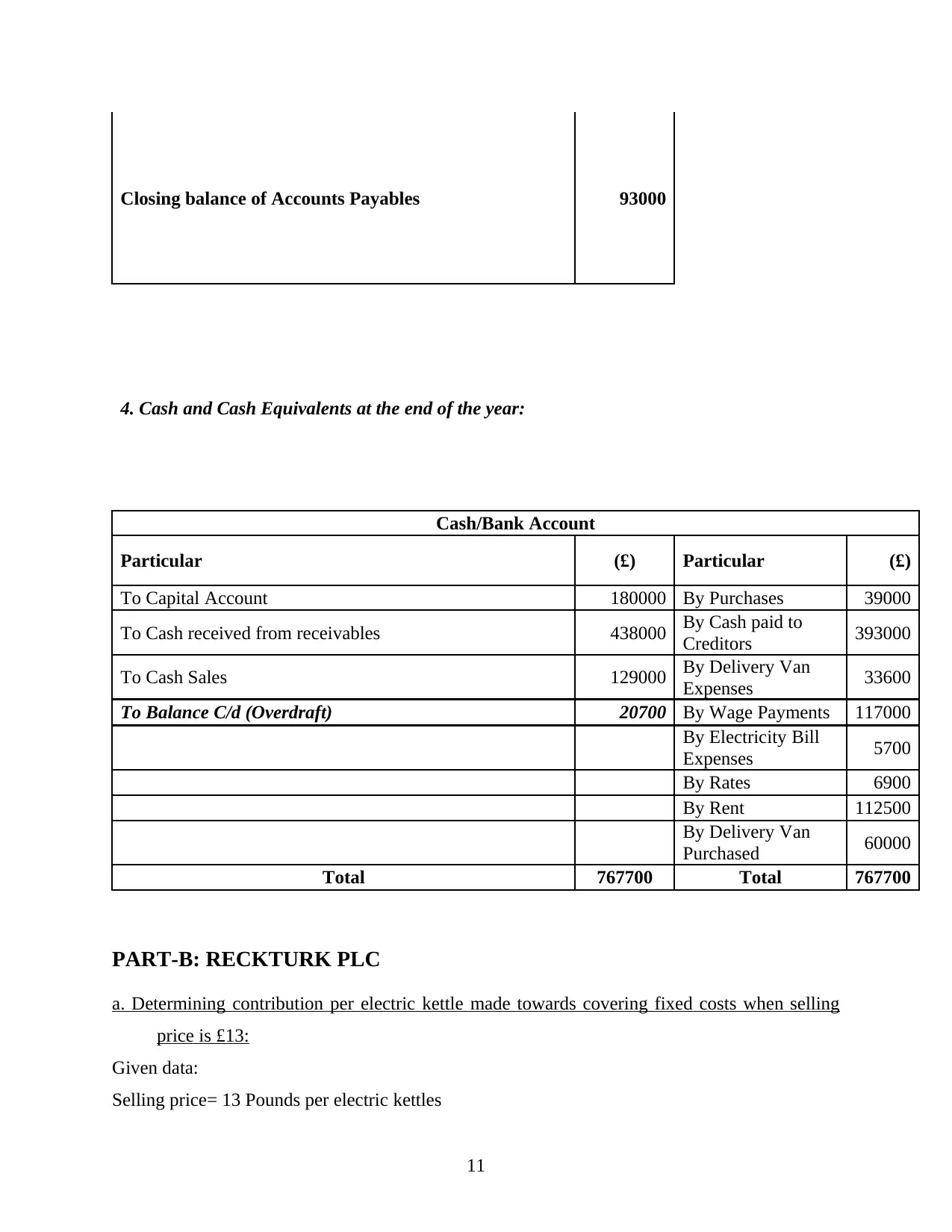

3. Accounts Payable:

Particular (£)

Goods purchase on credit 486000

Less: Account Payables repaid during the year 393000

10

Paraphrase This Document

4. Cash and Cash Equivalents at the end of the year:

Cash/Bank Account

Particular (£) Particular (£)

To Capital Account 180000 By Purchases 39000

To Cash received from receivables 438000 By Cash paid to

Creditors 393000

To Cash Sales 129000 By Delivery Van

Expenses 33600

To Balance C/d (Overdraft) 20700 By Wage Payments 117000

By Electricity Bill

Expenses 5700

By Rates 6900

By Rent 112500

By Delivery Van

Purchased 60000

Total 767700 Total 767700

PART-B: RECKTURK PLC

a. Determining contribution per electric kettle made towards covering fixed costs when selling

price is £13:

Given data:

Selling price= 13 Pounds per electric kettles

11

= £ (5.25+2.95+1.85)

= £10.05

Fixed cost= Production + Selling

= (59000+47600)

= 106600 Pounds

= Contribution = Selling price per unit – variable cost per unit

= 13 – 10.05

= 2.95 per unit

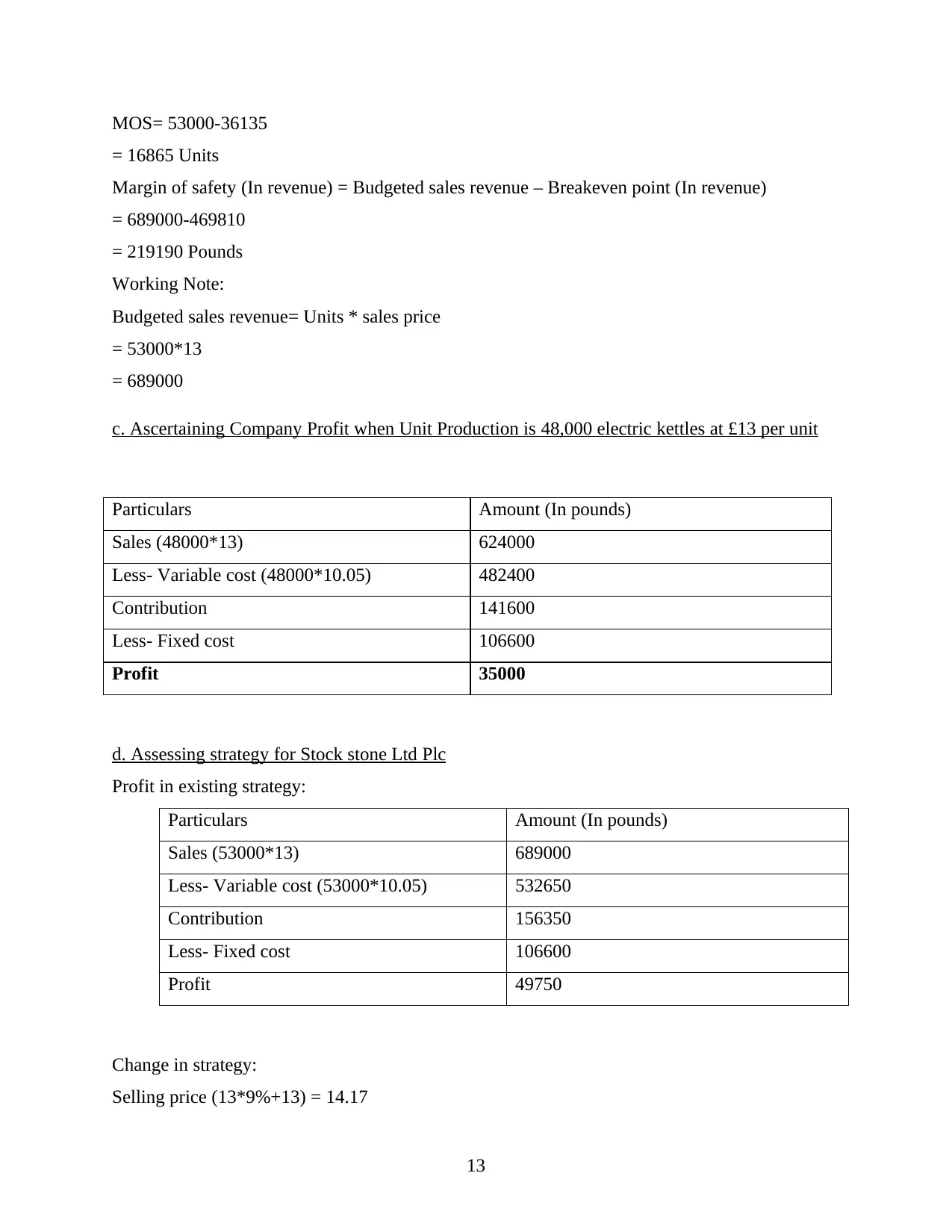

b. Calculating Break-even Point and Margin of Safety when selling price is £13:

Breakeven point (In units) = Fixed cost / contribution per unit

= 106600/2.95

= 36135 Units

Breakeven point (In revenue) = Fixed cost / PV ratio

= 106600 / 22.69%

= 469810 Pounds

Working Note:

PV ratio= Contribution per unit / selling price per unit*100

= 2.95 / 13 * 100

= 22.69%

Margin of safety (In units) = Budgeted sales – Breakeven point (In units)

Budgeted sales= 53000 Units

BEP= 36135

SO,

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 16865 Units

Margin of safety (In revenue) = Budgeted sales revenue – Breakeven point (In revenue)

= 689000-469810

= 219190 Pounds

Working Note:

Budgeted sales revenue= Units * sales price

= 53000*13

= 689000

c. Ascertaining Company Profit when Unit Production is 48,000 electric kettles at £13 per unit

Particulars Amount (In pounds)

Sales (48000*13) 624000

Less- Variable cost (48000*10.05) 482400

Contribution 141600

Less- Fixed cost 106600

Profit 35000

d. Assessing strategy for Stock stone Ltd Plc

Profit in existing strategy:

Particulars Amount (In pounds)

Sales (53000*13) 689000

Less- Variable cost (53000*10.05) 532650

Contribution 156350

Less- Fixed cost 106600

Profit 49750

Change in strategy:

Selling price (13*9%+13) = 14.17

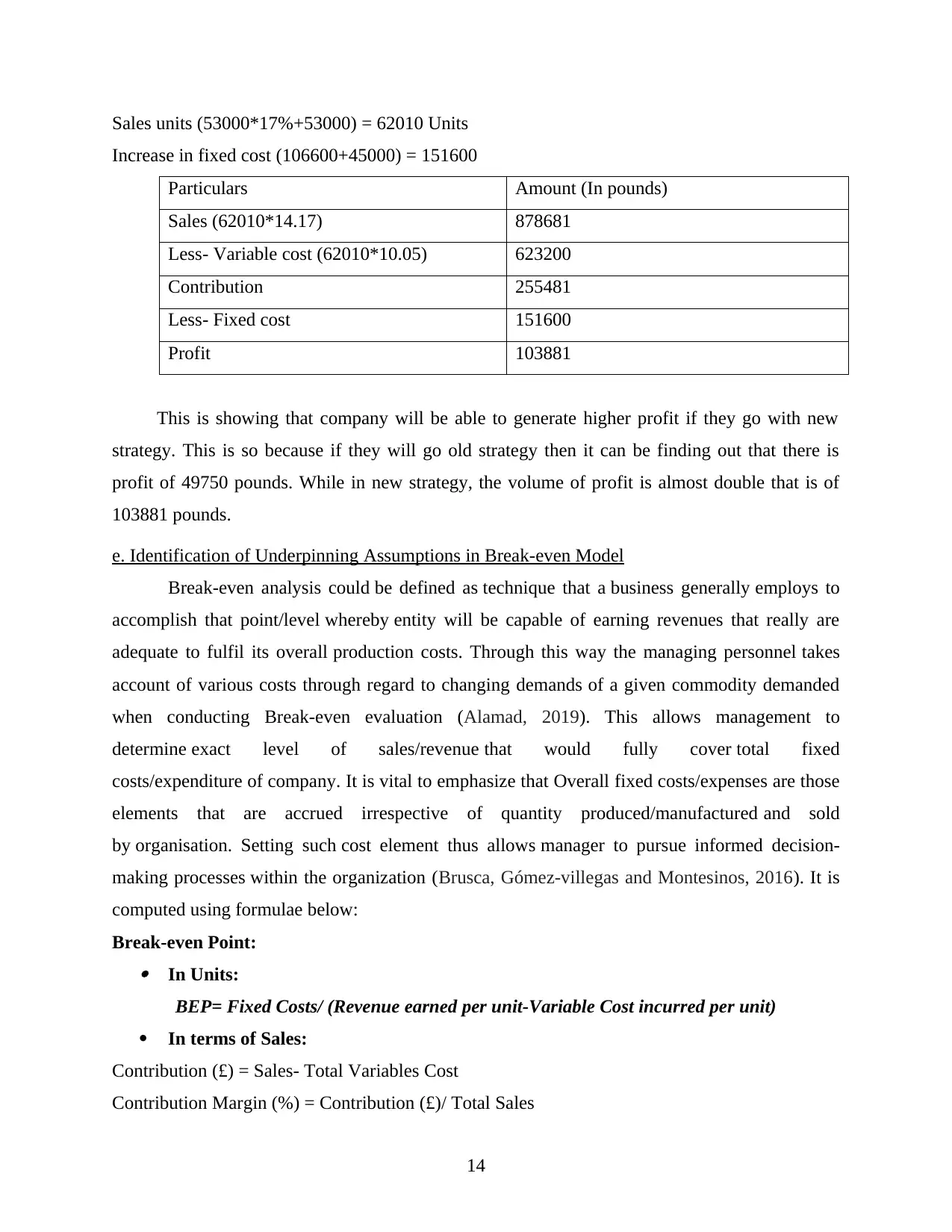

13

Paraphrase This Document

Increase in fixed cost (106600+45000) = 151600

Particulars Amount (In pounds)

Sales (62010*14.17) 878681

Less- Variable cost (62010*10.05) 623200

Contribution 255481

Less- Fixed cost 151600

Profit 103881

This is showing that company will be able to generate higher profit if they go with new

strategy. This is so because if they will go old strategy then it can be finding out that there is

profit of 49750 pounds. While in new strategy, the volume of profit is almost double that is of

103881 pounds.

e. Identification of Underpinning Assumptions in Break-even Model

Break-even analysis could be defined as technique that a business generally employs to

accomplish that point/level whereby entity will be capable of earning revenues that really are

adequate to fulfil its overall production costs. Through this way the managing personnel takes

account of various costs through regard to changing demands of a given commodity demanded

when conducting Break-even evaluation (Alamad, 2019). This allows management to

determine exact level of sales/revenue that would fully cover total fixed

costs/expenditure of company. It is vital to emphasize that Overall fixed costs/expenses are those

elements that are accrued irrespective of quantity produced/manufactured and sold

by organisation. Setting such cost element thus allows manager to pursue informed decision-

making processes within the organization (Brusca, Gómez‐villegas and Montesinos, 2016). It is

computed using formulae below:

Break-even Point: In Units:

BEP= Fixed Costs/ (Revenue earned per unit-Variable Cost incurred per unit)

In terms of Sales:

Contribution (£) = Sales- Total Variables Cost

Contribution Margin (%) = Contribution (£)/ Total Sales

14

Several main assumptions underlying conduct of the Break-even Analysis are being listed

as following:

Overall Cost could be divided into Fixed-costs and Variable Costs. Here, Semi-Variable

costs are not taken into consideration (Kai, Loh and Lian, 2017).

Prices of products are remained unchanged.

Unit Sold (Volume) = Units Actually Produced.

Fixed Costs will remain unchanged regardless of the unit volume manufactured.

Increment rate here is stable in case of Variable Costs.

Factor of improvements in technologies or increases in labour-efficiency are not

considered here.

By evaluating these assumptions, this can be stated that on grounds that promote

similarity, the BEP Analysis technique is theorised. As a consequence, different companies can

pursue such activity regardless of its size, essence and complexity (Kai, Loh and Lian, 2017).

PART-C: ROCKHAM PLC

a. Recommendation of acceptance or rejection of Capital Budgeting Projects using Investment

Appraisal techniques

Payback Period

Initial Investment 40,000,000

Net Annual Cash inflow (17000000 – 6400000) 106,00,000

Cash Flow Net Cash Flow

Year 0 -40,000,000.00 -40,000,000.00

Year 1 10,600,000.00 -29,400,000.00

Year 2 10,600,000.00 -18,800,000.00

Year 3 10,600,000.00 -8,200,000.00

Year 4 10,600,000.00 2,400,000.00

Year 5 10,600,000.00 13,000,000.00

Thus, Payback Period would be: 2 year + (8200000/10600000) = 2.774 years

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

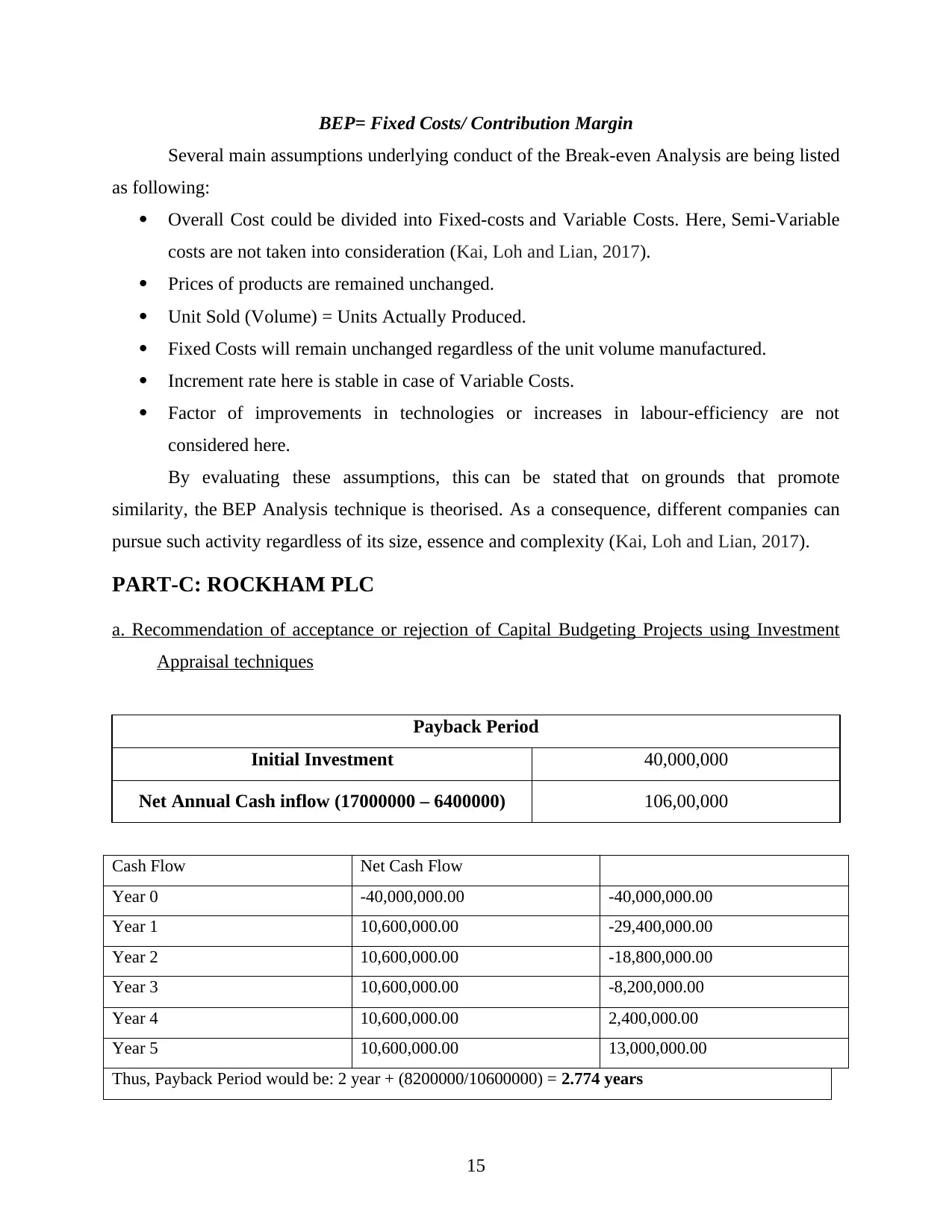

Purchase Cost of New Machine 40000000

Total expected net Cash inflow (17000000 – 6400000) *5 53000000

Depreciation per year [(40000000 – 5000000)/5] 7000000

Accounting Rate of Return 26.50%

Net Present Value

Year Cash Inflow

Cash

Outflow

Net Cash

Inflows

Discounting

Factor

PV of Net Cash

Inflows

1 3400000 1280000 2120000 0.917 1944954.128

2 3400000 1280000 2120000 0.842 1784361.586

3 3400000 1280000 2120000 0.772 1637028.978

4 3400000 1280000 2120000 0.708 1501861.447

5 3400000 1280000 2120000 0.650 1377854.539

Salvage Value 1000000 0.650 649931.386

Sum of PV of Net Cash

Inflows £8,895,992

NPV £895,992

Recommendations:

It has been clear from the above computations that buying new machine of worth

£40,000,000 will be wise decision for the Rockham PLC. This is demonstrated by the

3 investment appraisal techniques that show:

For the specified project payback period is around 2 years and approx. 8 months. This

period is less than usable life of Machinery as it is to be used for five years.

Therefore, make it feasible for company.

The ARR of machine is 26.5 percent. Therefore, this proposal therefore meets the

minimum condition of return on the investment.

The NPV figure is positive, even when taking into consideration both salvage value and

the original investment.

16

Paraphrase This Document

above-mentioned investment evaluation techniques.

17

INVESTMENT APPRAISAL TECHNIQUES

Through corporation carries out those forms of capital budgeting practices to achieve their

goals of increasing and exploiting opportunities which add values to the company in both

present and future time frames of its operational processes. To this end, an organization's

financial managers may conduct certain forms of investment appraisal techniques that can

justifiably support their key decisions (Maas, Schaltegger and Crutzen, 2016). In this

regard, this study dealt with the main advantages and drawbacks of these techniques:

1. Pay-Back Period: This technique helps company's financial manager to calculate the

exact amount of time it will take for given project to retrieve its initial investments. As a

consequence, payback period is time over which project's net cash-inflows are equal

to amount of initial investment incurred thereon. It is computed as below:

PBP = Initial Outlay/ Net Cash Inflows

Merits:

Simple indication of possibilities of blockages of capital in project as longer periods will

prolong recovery of initial investments made.

This method is most appropriate in cases where there has been a great uncertainty about

expected annual cash flows of project or industries/sectors where technological changes

are likely to occur (Renz and Herman, 2016).

Limitations:

It leads to ignore the time values of monies which is crucial component from the

perspective of the capital budgeting.

A shortened PBP, too, doesn't really assure project profitability (Schaltegger and Burritt,

2017).

Accounting Rate of Return: This method is called as financial ratio that is commonly used in

the budgeting capital. It is intended to deliver a payback based on net incomes generated

by proposed project. The ARR is determined according to the following:

ARR= Average Net Profit/ Average Investment

Merits:

Represents the definition of net amount of earnings gained after tax deduction and

depreciation. By giving a good understanding of the feasibility of project.

18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

percentage value.

Limitations:

It overlooks time factor that is important when choosing alternate applications of funds.

Herein cash inflows that form the basis for the accounting profits are not taken into

consideration.

Net Present Value: Net Present Value method is defined as most fevered investment valuation

technique, as value of all potential net cash-inflows which have been here discounted at specific

rate (Maskell, Baggaley, and Grasso, 2017). It is computed as below:

NPV = Σ(Present Value of all future cash flows) – Initial Investment

Merits:

It perceives the time-value of the money, and therefore chronological order

prioritizes cash inflows.

This takes into consideration reinvestment assumption, hence,

following conventionalize.

Limitations:

It's doesn't pursue the sunken cost effect.

Using this approach, it's hard to decide the appropriate discounting rate.

c. Report on identification of key merits and demerits of using Budgets as a strategy

planning tool

BUDGETS: A STRATEGIC PLANNING TOOL

An enterprise is accountable for defining, planning, coordinating, maintaining and regulating

resources in order to preserve its competitiveness and competitive market position without

sacrificing quality and consumer services. A corporate organization seeks to develop budgets

for this purpose. A Budget could be described as process of developing a financial schedule that

includes projections of incomes and expenditures to be received within a specified potential

period (Morris, 2018). Different forms of budgets are being evaluated under this study,

primarily on the grounds of their advantages and pitfalls. These are enumerated as follows:1. Activity Based Budgets: Another form of budget involves preparing a financial

19

Paraphrase This Document

efficacy of organizational activities. Similarly, the budget of the previous year doesn't

form basis for present year.

Merits:

It causes needless practices and, thus, proves to be effective cost saviour.

The issue of the bottlenecks is effectively removed because budget is focused on

activities.

Limitations:

It is much complex process requiring a thorough comprehension

of various business activities.

Activity Based Budgeting focuses mainly on meeting short-term targets that can

be counterproductive to enterprise in long-run.

Zero Based Budgets: This form of budget involving the creation of financial plan for specific

period is primarily based on expenditure for new period and therefore is conjectured on basis of

actual expenditure expected to have been incurred. Therefore, this budget is being prepared

from scratch using zero as basis for each period (Ramiah, Xu and Moosa, 2015).

Merits:

The performance and reliability of companies using this budget as strategic

planning technique is enhanced.

Repetitive tasks are properly identified and efficiently reduced.

Limitations:

This takes a lot of time, because manager has to begin every new cycle from

zero.

The method of planning can be costly for administration.

Incremental Budgets: This form of budget, as name implies, includes making changes

to existing finance plan. Accordingly, it was asserted on basis of details and figures from the

last year (Ramirez, 2015).

Merits:

Implementation is very simple.

Time as well as cost-effectiveness because there are minor adjustments which

need to be incorporated to existing business budget.

20

Lack of creativity will grow because it often contributes to budgetary gap.

Excessive spending can become standard practice owing to simpler budget

accessibility.

CONCLUSION

From the aforementioned study-report, it has been concluded that the accounting and

finance serve a critical role in deciding how business' fiscal resources being used to improve a

specific business' productivity and aggregate organizational performance. Using Costing may

allow management to assess the allocation of capital per unit, and also sales. Also it helps them

to recognize the Break-even Levels which insure that allocating resources doesn't really lead to

degradation of current profits on product sold per-unit. Further, investment evaluation tools and

financial planning enable company to synchronize capital budgeting process and strategic

planning operations with other key aspects. That allows the managers to make important

decisions in informed manner.

21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Books and Journal

Ainsworth, P. and Deines, D., 2019. Introduction to accounting: An integrated approach. Wiley.

Shawver, T. J. and Miller, W. F., 2017. Moral intensity revisited: Measuring the benefit of

accounting ethics interventions. Journal of business ethics. 141(3). pp.587-603.

Webb, J. and Chaffer, C., 2016. The expectation performance gap in accounting education: A

review of generic skills development in UK accounting degrees. Accounting Education.

25(4). pp.349-367.

Alamad, S., 2019. Financial and Accounting Principles in Islamic Finance. Springer.

Brusca, I., Gómez‐villegas, M. and Montesinos, V., 2016. Public financial management reforms:

The role of IPSAS in Latin‐America. Public Administration and Development. 36(1).

pp.51-64.

Kai, C. Y., Loh, U. and Lian, A. N. B., 2017. Accounting education in Singapore. In The

Routledge Handbook of Accounting in Asia (pp. 234-253). Routledge.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136,

pp.237-248.

Renz, D. O. and Herman, R. D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Maskell, B. H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Morris, R., 2018. Early Warning Indicators of Corporate Failure: A critical review of previous

research and further empirical evidence. Routledge.

Ramiah, V., Xu, X. and Moosa, I. A., 2015. Neoclassical finance, behavioral finance and noise

traders: A review and assessment of the literature. International Review of Financial

Analysis. 41. pp.89-100.

Ramirez, J., 2015. Accounting for derivatives: Advanced hedging under IFRS 9. John Wiley &

Sons.

22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.