Introduction to Finance: Inventory, Investment, and Financial Analysis

VerifiedAdded on 2023/01/06

|14

|3845

|37

Homework Assignment

AI Summary

This finance assignment delves into key concepts of financial management. It begins with the calculation of the Economic Order Quantity (EOQ) for inventory management, followed by a critical evaluation of its use. The assignment then explores investment appraisal techniques, including the payback period and accounting rate of return (ARR), providing calculations and evaluations of each. The importance of considering the audience for financial statement analysis is also addressed. Finally, the assignment examines the role of various organizations in the international regulatory framework for accounting and the role of audit committees in corporate governance. The assignment provides detailed calculations, interpretations, and critical evaluations of the financial concepts covered, offering a comprehensive overview of financial analysis and management.

INTRODUCTION TO

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................1

a) Calculate economic order quantity for the hard plastic...........................................................1

b) Total annual cost of the hard plastic........................................................................................1

c) Critical evaluation of the decision of using EOQ model as part approach to management of

the inventories..............................................................................................................................2

d) Advise on cost of handling inventories cost of failing to manage the inventories adequately

and practical implication of inventory management...................................................................3

QUESTION 2..................................................................................................................................3

a) Calculation of payback for Option A and Option B................................................................3

b) Accounting rate of return for option A and option B..............................................................4

c) Critical evaluation of the accounting rate of return.................................................................5

d) Explanations of characteristics of the investment appraisal decisions and advantage and

disadvantages of internal rate of return.......................................................................................6

QUESTION 3..................................................................................................................................6

Calculation of ratios.....................................................................................................................6

Importance of considering audience for financial statement analysis.........................................9

QUESTION 4................................................................................................................................10

Role of different organization in international regulatory framework for accounting..............10

Role of audit committees in corporate governance...................................................................10

REFERENCES..............................................................................................................................12

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................1

a) Calculate economic order quantity for the hard plastic...........................................................1

b) Total annual cost of the hard plastic........................................................................................1

c) Critical evaluation of the decision of using EOQ model as part approach to management of

the inventories..............................................................................................................................2

d) Advise on cost of handling inventories cost of failing to manage the inventories adequately

and practical implication of inventory management...................................................................3

QUESTION 2..................................................................................................................................3

a) Calculation of payback for Option A and Option B................................................................3

b) Accounting rate of return for option A and option B..............................................................4

c) Critical evaluation of the accounting rate of return.................................................................5

d) Explanations of characteristics of the investment appraisal decisions and advantage and

disadvantages of internal rate of return.......................................................................................6

QUESTION 3..................................................................................................................................6

Calculation of ratios.....................................................................................................................6

Importance of considering audience for financial statement analysis.........................................9

QUESTION 4................................................................................................................................10

Role of different organization in international regulatory framework for accounting..............10

Role of audit committees in corporate governance...................................................................10

REFERENCES..............................................................................................................................12

QUESTION 1

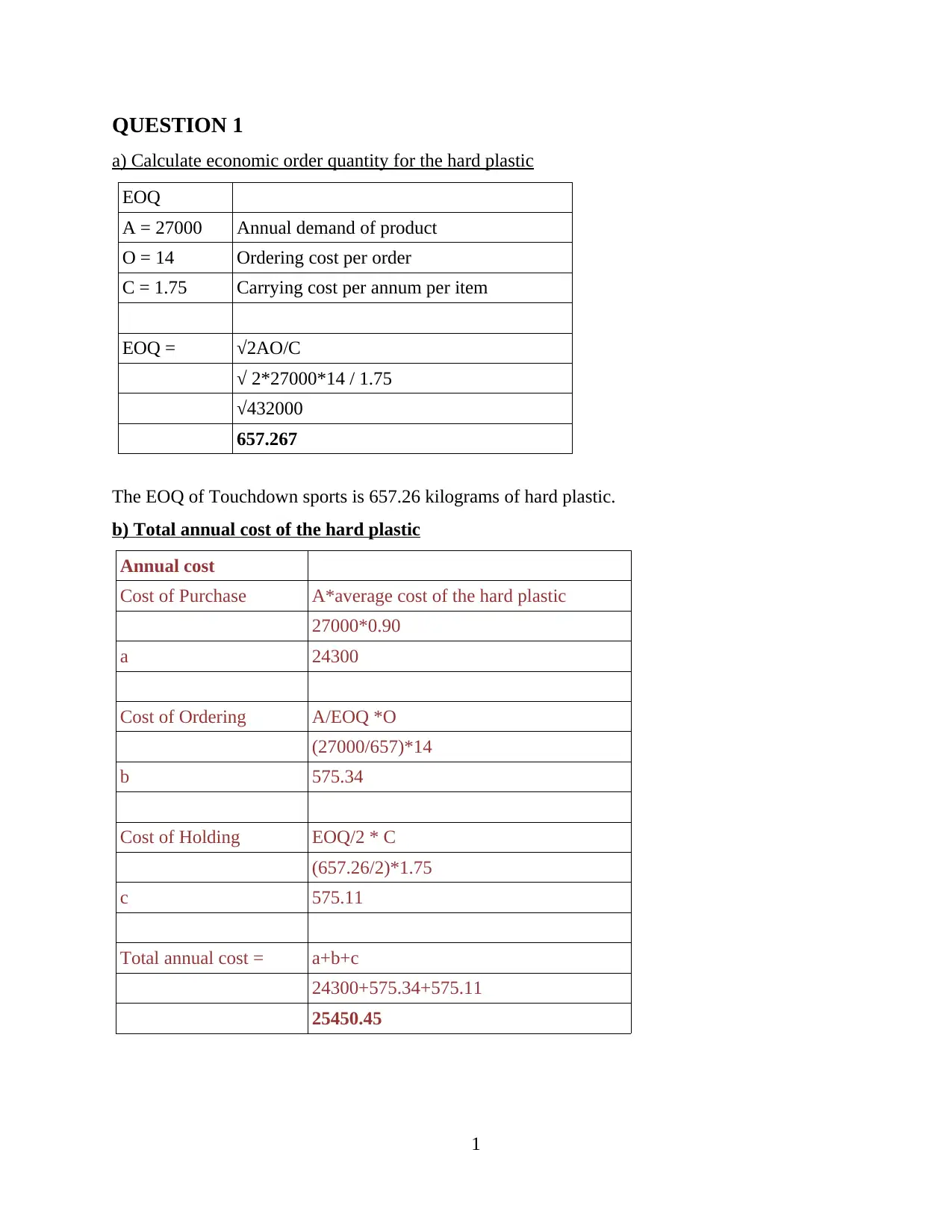

a) Calculate economic order quantity for the hard plastic

EOQ

A = 27000 Annual demand of product

O = 14 Ordering cost per order

C = 1.75 Carrying cost per annum per item

EOQ = √2AO/C

√ 2*27000*14 / 1.75

√432000

657.267

The EOQ of Touchdown sports is 657.26 kilograms of hard plastic.

b) Total annual cost of the hard plastic

Annual cost

Cost of Purchase A*average cost of the hard plastic

27000*0.90

a 24300

Cost of Ordering A/EOQ *O

(27000/657)*14

b 575.34

Cost of Holding EOQ/2 * C

(657.26/2)*1.75

c 575.11

Total annual cost = a+b+c

24300+575.34+575.11

25450.45

1

a) Calculate economic order quantity for the hard plastic

EOQ

A = 27000 Annual demand of product

O = 14 Ordering cost per order

C = 1.75 Carrying cost per annum per item

EOQ = √2AO/C

√ 2*27000*14 / 1.75

√432000

657.267

The EOQ of Touchdown sports is 657.26 kilograms of hard plastic.

b) Total annual cost of the hard plastic

Annual cost

Cost of Purchase A*average cost of the hard plastic

27000*0.90

a 24300

Cost of Ordering A/EOQ *O

(27000/657)*14

b 575.34

Cost of Holding EOQ/2 * C

(657.26/2)*1.75

c 575.11

Total annual cost = a+b+c

24300+575.34+575.11

25450.45

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For calculating the total annual cost of hard plastic first cost of purchase, cost of ordering

and cost of handling are to be calculated. Thereafter, all the costs are added for getting the total

cost of hard plastic per year. Total cost of hard plastic is $25434.

c) Critical evaluation of the decision of using EOQ model as part approach to management of the

inventories

Economic order quantity or EOQ is ideal order quantity company should purchase for

minimising cost of inventory like holding costs, order costs and shortage costs. It is used as the

part of continuous review system where inventory levels are monitored all times and fixed

quantities are ordered every time inventory reaches reorder point (Jiraruttrakul and et.al., 2017).

It provides model for identifying optimum reorder level that ensures instantaneous replenishment

of the inventory without any shortages. It is considered as valuable tool by the organisations and

business that makes decision on inventory level to be kept, how much quantity to order and how

much reorder for incurring lowest possible cost.

The method assumes demand to be constant and also inventory gets depleted at the fix

rate till it reaches zero. As it assumes instantaneous replenishment, there is no shortage of the

inventory or associated cost. Cost of the inventory under EOQ model includes trade-off between

the inventory holding costs and the order cost. Ordering large amount will increase the holding

cost of business at one time but making frequent orders in fewer quantity will be reducing

holding cost but at the same time increasing the order cost (Farhan and Susanto, 2019). EOQ

helps management in identifying quantity which will lower the sum of costs.

The EOQ model for inventory management by Touchdown sport could be effective as it

is having constant demand for the quantity of materials excepts in July and August. This will not

make a major difference. It could use the method for the business as it is having fixed ordering

and carrying cost. It could manage the inventory effectively using the EOQ model for inventory

management. However along with using this approach touchdown sports is required to take

account for other changes in the cost that could affect the inventory order.

d) Advise on cost of handling inventories cost of failing to manage the inventories adequately

and practical implication of inventory management.

2

and cost of handling are to be calculated. Thereafter, all the costs are added for getting the total

cost of hard plastic per year. Total cost of hard plastic is $25434.

c) Critical evaluation of the decision of using EOQ model as part approach to management of the

inventories

Economic order quantity or EOQ is ideal order quantity company should purchase for

minimising cost of inventory like holding costs, order costs and shortage costs. It is used as the

part of continuous review system where inventory levels are monitored all times and fixed

quantities are ordered every time inventory reaches reorder point (Jiraruttrakul and et.al., 2017).

It provides model for identifying optimum reorder level that ensures instantaneous replenishment

of the inventory without any shortages. It is considered as valuable tool by the organisations and

business that makes decision on inventory level to be kept, how much quantity to order and how

much reorder for incurring lowest possible cost.

The method assumes demand to be constant and also inventory gets depleted at the fix

rate till it reaches zero. As it assumes instantaneous replenishment, there is no shortage of the

inventory or associated cost. Cost of the inventory under EOQ model includes trade-off between

the inventory holding costs and the order cost. Ordering large amount will increase the holding

cost of business at one time but making frequent orders in fewer quantity will be reducing

holding cost but at the same time increasing the order cost (Farhan and Susanto, 2019). EOQ

helps management in identifying quantity which will lower the sum of costs.

The EOQ model for inventory management by Touchdown sport could be effective as it

is having constant demand for the quantity of materials excepts in July and August. This will not

make a major difference. It could use the method for the business as it is having fixed ordering

and carrying cost. It could manage the inventory effectively using the EOQ model for inventory

management. However along with using this approach touchdown sports is required to take

account for other changes in the cost that could affect the inventory order.

d) Advise on cost of handling inventories cost of failing to manage the inventories adequately

and practical implication of inventory management.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of holding the inventory are associated with the inventory which remains unsold.

The cost is one of the component of the total inventory cost along with the shortage cosy and

ordering cost. Holding cost includes prices of the goods spoiled or damaged and of storage

space, insurance labour etc.

Cost of failing to manage the inventory could be high. Various analysts and managers are

of the view that organisations having too much of the inventories have high potential of being

destroyed or getting damaged over the time due for reasons beyond the control. Movement of the

inventory is constant activity which requires input from the multiple source throughout supply

chain. If the company fails to manage the manage the inventory it may have to incur increased

storage and carrying cost (Condeixa and et.al., 2020). Increased cost will be reducing the profits

margins of the organisation reducing the return. It will have negative impact over the

organisation and will reflect of inefficiency of management.

Effective inventory management will be improving the accuracy of the inventory orders.

The proper management of inventory helps to find out exactly how much inventory is required. It

will prevent shortages of product and will also allow the organisation to keep enough inventory

without having higher cost of warehouse. Good inventory management will make the production

process productive and efficient to meet the demand of customers. It has to manage the inventory

in manner where all the costs are low.

QUESTION 2

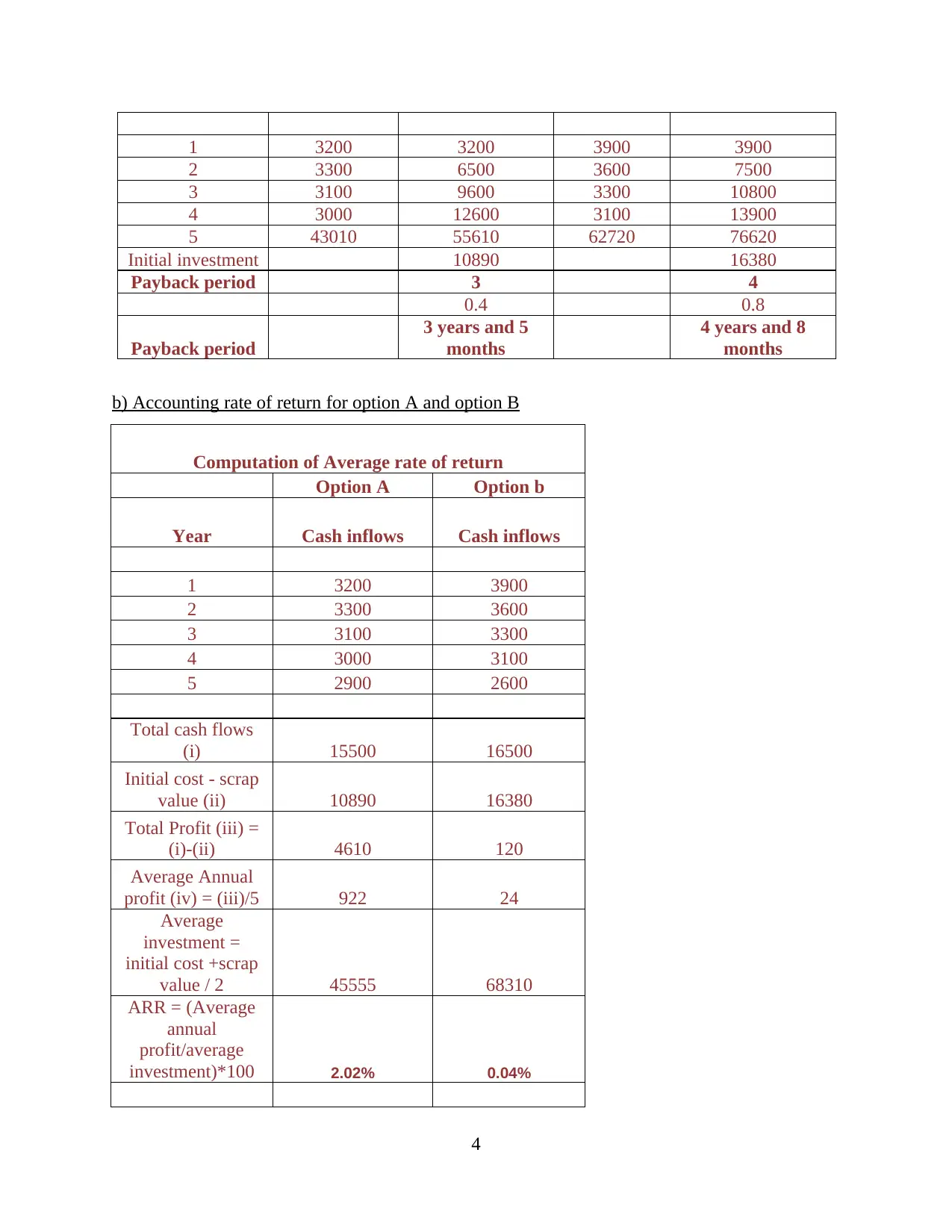

a) Calculation of payback for Option A and Option B

Payback method is an investment appraisal technique that is used by the

management or investors to measure the time taken by the project or investment to

recovers its initial investment costs. The method also helps the management in analysing

the break even point after which it will start earning the returns. The method does not uses

time value of money in calculating the break evens. The method is highly useful for the

management in analysing the viability of investments.

Computation of Payback period

Option A Option B

Year Cash inflows

Cumulative cash

inflows Cash inflows

Cumulative cash

inflows

3

The cost is one of the component of the total inventory cost along with the shortage cosy and

ordering cost. Holding cost includes prices of the goods spoiled or damaged and of storage

space, insurance labour etc.

Cost of failing to manage the inventory could be high. Various analysts and managers are

of the view that organisations having too much of the inventories have high potential of being

destroyed or getting damaged over the time due for reasons beyond the control. Movement of the

inventory is constant activity which requires input from the multiple source throughout supply

chain. If the company fails to manage the manage the inventory it may have to incur increased

storage and carrying cost (Condeixa and et.al., 2020). Increased cost will be reducing the profits

margins of the organisation reducing the return. It will have negative impact over the

organisation and will reflect of inefficiency of management.

Effective inventory management will be improving the accuracy of the inventory orders.

The proper management of inventory helps to find out exactly how much inventory is required. It

will prevent shortages of product and will also allow the organisation to keep enough inventory

without having higher cost of warehouse. Good inventory management will make the production

process productive and efficient to meet the demand of customers. It has to manage the inventory

in manner where all the costs are low.

QUESTION 2

a) Calculation of payback for Option A and Option B

Payback method is an investment appraisal technique that is used by the

management or investors to measure the time taken by the project or investment to

recovers its initial investment costs. The method also helps the management in analysing

the break even point after which it will start earning the returns. The method does not uses

time value of money in calculating the break evens. The method is highly useful for the

management in analysing the viability of investments.

Computation of Payback period

Option A Option B

Year Cash inflows

Cumulative cash

inflows Cash inflows

Cumulative cash

inflows

3

1 3200 3200 3900 3900

2 3300 6500 3600 7500

3 3100 9600 3300 10800

4 3000 12600 3100 13900

5 43010 55610 62720 76620

Initial investment 10890 16380

Payback period 3 4

0.4 0.8

Payback period

3 years and 5

months

4 years and 8

months

b) Accounting rate of return for option A and option B

Computation of Average rate of return

Option A Option b

Year Cash inflows Cash inflows

1 3200 3900

2 3300 3600

3 3100 3300

4 3000 3100

5 2900 2600

Total cash flows

(i) 15500 16500

Initial cost - scrap

value (ii) 10890 16380

Total Profit (iii) =

(i)-(ii) 4610 120

Average Annual

profit (iv) = (iii)/5 922 24

Average

investment =

initial cost +scrap

value / 2 45555 68310

ARR = (Average

annual

profit/average

investment)*100 2.02% 0.04%

4

2 3300 6500 3600 7500

3 3100 9600 3300 10800

4 3000 12600 3100 13900

5 43010 55610 62720 76620

Initial investment 10890 16380

Payback period 3 4

0.4 0.8

Payback period

3 years and 5

months

4 years and 8

months

b) Accounting rate of return for option A and option B

Computation of Average rate of return

Option A Option b

Year Cash inflows Cash inflows

1 3200 3900

2 3300 3600

3 3100 3300

4 3000 3100

5 2900 2600

Total cash flows

(i) 15500 16500

Initial cost - scrap

value (ii) 10890 16380

Total Profit (iii) =

(i)-(ii) 4610 120

Average Annual

profit (iv) = (iii)/5 922 24

Average

investment =

initial cost +scrap

value / 2 45555 68310

ARR = (Average

annual

profit/average

investment)*100 2.02% 0.04%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c) Critical evaluation of the accounting rate of return

ARR could be said as financial ratio that is used in the capital budgeting for assessing the

returns that will be generated under the capital budgeting. The ratio calculates the returns to be

generated by the projects or investments on the basis of accounting profits. This is a method of

investment appraisal which does not uses time value of money. It reflects percentage return on

the investment or the assets compared with initial cost of investment. Formula derives return or

ratio that could be expected over lifetime of project or investment.

Using the method management and investors analyse the profitability of the projects

proposed to be taken. The method is used primarily for comparing the different projects for

determining expected rate of the return over each project for making decisions related to

investments. It factors in any of the possible expenses involving depreciation associated with

project (Egbunike, 2018). Depreciation is accounting convention where cost of the fixed assets

are spread out annually during life of asset. However the drawback of the method is that it could

not be used for investments that are yielding different cash flows over useful life of project.

Though the method is highly used but there are drawbacks of the method which includes

no use of time factor in calculations. When two projects yielding uneven revenues and one is

giving more returns early and other is returning in later years. The method does not assign higher

value to project which return profits sooner that could be invested for earning more money. Also

it only considers accounting profits in measuring the rate of return. However is one of the

important technique used by the investors and management for assessing the viability of

investments.

d) Explanations of characteristics of the investment appraisal decisions and advantage and

disadvantages of internal rate of return

Investment appraisal techniques are used by the management for evaluating the viability

of different investments or projects that company plans. Capital projects of the company involves

huge costs and expenditures therefore they are required to be assessed thoroughly before the

investments are made. Good investment appraisal technique is one that enables the organisation

to evaluate the viability considering all the relevant factors associated with the project.

Internal Rate of Return

It is the method used by the business for estimating profitability of the potential projects

or investments. IRR is said to be a discount rate which makes present value of cash flows equals

5

ARR could be said as financial ratio that is used in the capital budgeting for assessing the

returns that will be generated under the capital budgeting. The ratio calculates the returns to be

generated by the projects or investments on the basis of accounting profits. This is a method of

investment appraisal which does not uses time value of money. It reflects percentage return on

the investment or the assets compared with initial cost of investment. Formula derives return or

ratio that could be expected over lifetime of project or investment.

Using the method management and investors analyse the profitability of the projects

proposed to be taken. The method is used primarily for comparing the different projects for

determining expected rate of the return over each project for making decisions related to

investments. It factors in any of the possible expenses involving depreciation associated with

project (Egbunike, 2018). Depreciation is accounting convention where cost of the fixed assets

are spread out annually during life of asset. However the drawback of the method is that it could

not be used for investments that are yielding different cash flows over useful life of project.

Though the method is highly used but there are drawbacks of the method which includes

no use of time factor in calculations. When two projects yielding uneven revenues and one is

giving more returns early and other is returning in later years. The method does not assign higher

value to project which return profits sooner that could be invested for earning more money. Also

it only considers accounting profits in measuring the rate of return. However is one of the

important technique used by the investors and management for assessing the viability of

investments.

d) Explanations of characteristics of the investment appraisal decisions and advantage and

disadvantages of internal rate of return

Investment appraisal techniques are used by the management for evaluating the viability

of different investments or projects that company plans. Capital projects of the company involves

huge costs and expenditures therefore they are required to be assessed thoroughly before the

investments are made. Good investment appraisal technique is one that enables the organisation

to evaluate the viability considering all the relevant factors associated with the project.

Internal Rate of Return

It is the method used by the business for estimating profitability of the potential projects

or investments. IRR is said to be a discount rate which makes present value of cash flows equals

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to zero in discounted cash flow analysis. It relies over same formula which is used for calculating

NPV of the project (Kengatharan and Clamenthu, 2017). The method is highly useful for

comparing the projects for making accurate investment decisions.

Advantages

The method is useful and draws more reliable conclusions as compared with other

techniques as uses time value of money in the calculations. The method is simple and

understandable. In the method also the required rate or hurdle rate is not required as they are

rough estimates.

Disadvantages

The method ignores the economies of scale associated with the project. It also undertakes

impractical assumptions that returns will be reinvested. The method does not considers other

factors associated with the project or investments.

QUESTION 3

Calculation of ratios

Gross profit

margin Formula 2019

GP/ sales 37.568

GP 1313

Sales 3495

Interpretation- with the above calculation it is clearly visible that gross profit margin is 37.56 %

which indicates the gross profit of company is moderate. The major reason behind this fact is

that when company is operating in business environment then there are many expenses which

company has to bear and for this the profit of company is low. But now company has to manage

and try to increase the profit so that company can manage its performance and profitability.

Asset usage Formula 2019

Sales / total asset 1.206

Sales 3495

Total asset 2898

6

NPV of the project (Kengatharan and Clamenthu, 2017). The method is highly useful for

comparing the projects for making accurate investment decisions.

Advantages

The method is useful and draws more reliable conclusions as compared with other

techniques as uses time value of money in the calculations. The method is simple and

understandable. In the method also the required rate or hurdle rate is not required as they are

rough estimates.

Disadvantages

The method ignores the economies of scale associated with the project. It also undertakes

impractical assumptions that returns will be reinvested. The method does not considers other

factors associated with the project or investments.

QUESTION 3

Calculation of ratios

Gross profit

margin Formula 2019

GP/ sales 37.568

GP 1313

Sales 3495

Interpretation- with the above calculation it is clearly visible that gross profit margin is 37.56 %

which indicates the gross profit of company is moderate. The major reason behind this fact is

that when company is operating in business environment then there are many expenses which

company has to bear and for this the profit of company is low. But now company has to manage

and try to increase the profit so that company can manage its performance and profitability.

Asset usage Formula 2019

Sales / total asset 1.206

Sales 3495

Total asset 2898

6

Interpretation- from the above asset utilization ratio it was evident that ratio for company is

1.206. This ratio indicates that how well the company is able to generate revenue with the help of

the provided assets which company is possessing. This ratio is good but the need to be improved

to the ideal of 2:1 which suggest that for earning 2 company must have at least 1 asset. For this

company need to improve its asset utilization so that they can effectively manage the revenue of

company.

Current ratio Formula 2019

CA/ CL 2.27

CA 1687

CL 744

Interpretation- the analysis of current ratio is very important for company to manage its liquidity.

The major reason for this is that this ratio assist company in managing their liquidity and how

they will manage their day to day operations. The current ratio of company is 2.27 which suggest

that company is having good current ratio. The major reason underlying this fact is that for an

ideal current ratio is need to be 2:1 that is two current assets for every one current liability. For

company they are meeting the ideal criteria as for every liability it is having 2.27 asset for paying

it off.

Acid test Formula 2019

(CA- stock)/ CL 2.06586

CA 1687

CL 744

Inventories 150

Interpretation- with the assistance of acid test ratio it was seen that the ratio is 2.06 and this

measures that how well the company is able to satisfy the short term financial obligation and

liabilities of company. The ideal acid test ratio is 1:1 or higher than this and in present case this

is higher. Thus, this suggest that company has high liquidity and is in a better position to meet

all current obligation with help of the liquid asset.

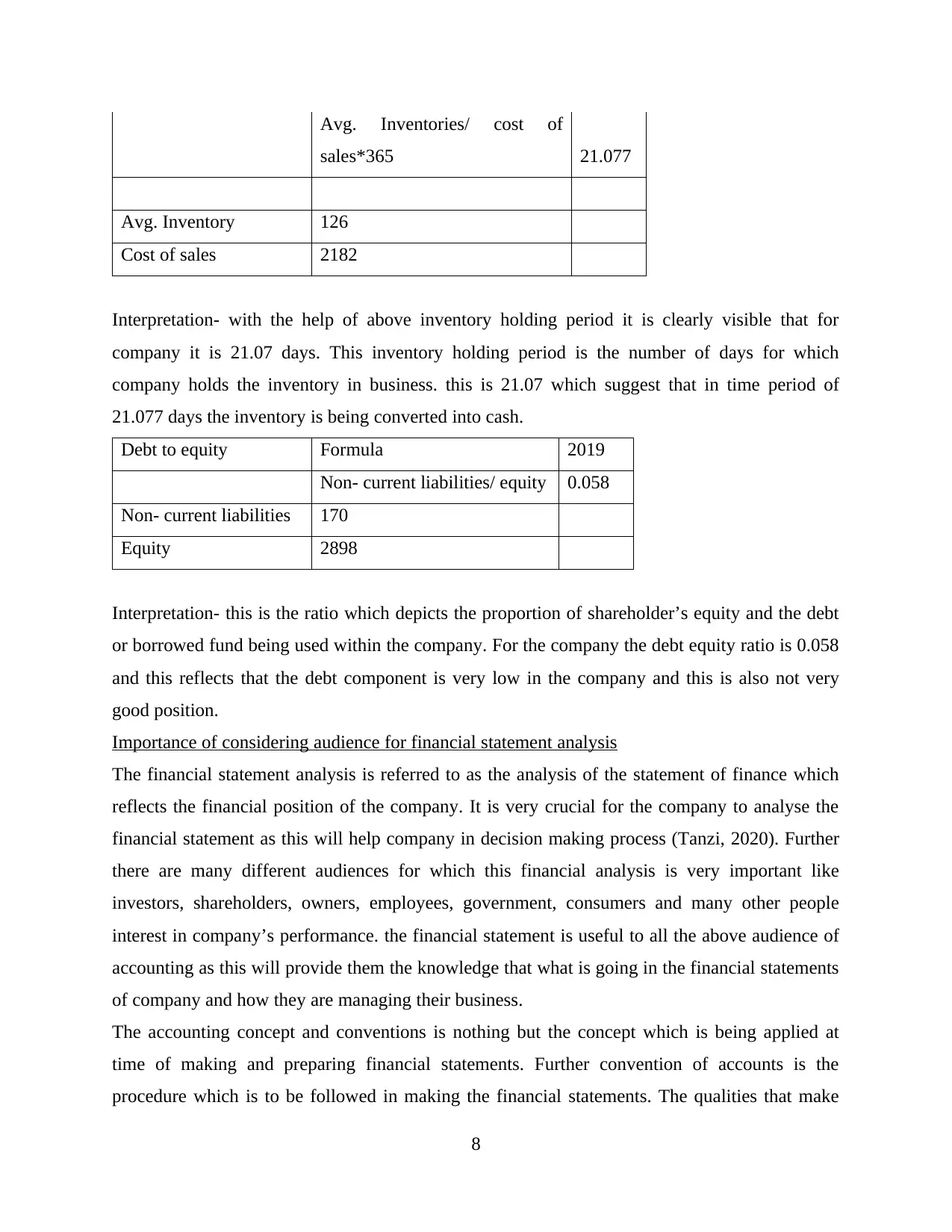

Inventories holding

period Formula 2019

7

1.206. This ratio indicates that how well the company is able to generate revenue with the help of

the provided assets which company is possessing. This ratio is good but the need to be improved

to the ideal of 2:1 which suggest that for earning 2 company must have at least 1 asset. For this

company need to improve its asset utilization so that they can effectively manage the revenue of

company.

Current ratio Formula 2019

CA/ CL 2.27

CA 1687

CL 744

Interpretation- the analysis of current ratio is very important for company to manage its liquidity.

The major reason for this is that this ratio assist company in managing their liquidity and how

they will manage their day to day operations. The current ratio of company is 2.27 which suggest

that company is having good current ratio. The major reason underlying this fact is that for an

ideal current ratio is need to be 2:1 that is two current assets for every one current liability. For

company they are meeting the ideal criteria as for every liability it is having 2.27 asset for paying

it off.

Acid test Formula 2019

(CA- stock)/ CL 2.06586

CA 1687

CL 744

Inventories 150

Interpretation- with the assistance of acid test ratio it was seen that the ratio is 2.06 and this

measures that how well the company is able to satisfy the short term financial obligation and

liabilities of company. The ideal acid test ratio is 1:1 or higher than this and in present case this

is higher. Thus, this suggest that company has high liquidity and is in a better position to meet

all current obligation with help of the liquid asset.

Inventories holding

period Formula 2019

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Avg. Inventories/ cost of

sales*365 21.077

Avg. Inventory 126

Cost of sales 2182

Interpretation- with the help of above inventory holding period it is clearly visible that for

company it is 21.07 days. This inventory holding period is the number of days for which

company holds the inventory in business. this is 21.07 which suggest that in time period of

21.077 days the inventory is being converted into cash.

Debt to equity Formula 2019

Non- current liabilities/ equity 0.058

Non- current liabilities 170

Equity 2898

Interpretation- this is the ratio which depicts the proportion of shareholder’s equity and the debt

or borrowed fund being used within the company. For the company the debt equity ratio is 0.058

and this reflects that the debt component is very low in the company and this is also not very

good position.

Importance of considering audience for financial statement analysis

The financial statement analysis is referred to as the analysis of the statement of finance which

reflects the financial position of the company. It is very crucial for the company to analyse the

financial statement as this will help company in decision making process (Tanzi, 2020). Further

there are many different audiences for which this financial analysis is very important like

investors, shareholders, owners, employees, government, consumers and many other people

interest in company’s performance. the financial statement is useful to all the above audience of

accounting as this will provide them the knowledge that what is going in the financial statements

of company and how they are managing their business.

The accounting concept and conventions is nothing but the concept which is being applied at

time of making and preparing financial statements. Further convention of accounts is the

procedure which is to be followed in making the financial statements. The qualities that make

8

sales*365 21.077

Avg. Inventory 126

Cost of sales 2182

Interpretation- with the help of above inventory holding period it is clearly visible that for

company it is 21.07 days. This inventory holding period is the number of days for which

company holds the inventory in business. this is 21.07 which suggest that in time period of

21.077 days the inventory is being converted into cash.

Debt to equity Formula 2019

Non- current liabilities/ equity 0.058

Non- current liabilities 170

Equity 2898

Interpretation- this is the ratio which depicts the proportion of shareholder’s equity and the debt

or borrowed fund being used within the company. For the company the debt equity ratio is 0.058

and this reflects that the debt component is very low in the company and this is also not very

good position.

Importance of considering audience for financial statement analysis

The financial statement analysis is referred to as the analysis of the statement of finance which

reflects the financial position of the company. It is very crucial for the company to analyse the

financial statement as this will help company in decision making process (Tanzi, 2020). Further

there are many different audiences for which this financial analysis is very important like

investors, shareholders, owners, employees, government, consumers and many other people

interest in company’s performance. the financial statement is useful to all the above audience of

accounting as this will provide them the knowledge that what is going in the financial statements

of company and how they are managing their business.

The accounting concept and conventions is nothing but the concept which is being applied at

time of making and preparing financial statements. Further convention of accounts is the

procedure which is to be followed in making the financial statements. The qualities that make

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting information useful is that this information are relevant, reliable, comparable,

consistent, understandable and material to the audience. Further for financial analysis audience

make use of following methods-

Income statement- the audience with help of income statement try to find the profitability of

company. With help of this statement audience will learn the amount of profit earned or loss

incurred.

Balance sheet- with help of balance sheet the audience of company will try to find the position of

company that is asset and liabilities of company.

Cash flow statement- with assistance of this statement audience is in condition to analyse the net

inflow or outflow of the cash and make necessary changes according to that.

Ratios- this is a financial analysis tool which assist audience to identify the relation of

company’s financial position with different aspect of business (Bernards and Campbell-Verduyn,

2019).

Horizontal analysis- this is used by audience in order to gather information relating to changes in

amount of corresponding financial statement items over a period of time.

Vertical analysis- this is used by audience as this will assist in gaining knowledge that each

particular of financial statement is compared against the base figure.

Trend analysis- this analysis is used by company in order to understand the trend or pattern of

any change and then try to follow it.

QUESTION 4

Role of different organization in international regulatory framework for accounting

IFRS foundation- the role of this organization in accounting framework is to develop and

promote the IFRS standards and bring in efficiency, transparency and accountability within the

financial market all over the globe (Melé, Rosanas and Fontrodona, 2017). The major goal is to

foster trust, growth and financial stability with respect to accounting all over the globe.

IFRS advisory council- the advisory council of IFRS major role is advise the board or decision

makers to take effective decision and to inform the board of the views of organization in setting

standard.

International accounting standards board- the role of IASB is to be responsible for all the matters

including making of IFRS, issuance of drafts, setting up of procedures for the review of

comments and many other matters.

9

consistent, understandable and material to the audience. Further for financial analysis audience

make use of following methods-

Income statement- the audience with help of income statement try to find the profitability of

company. With help of this statement audience will learn the amount of profit earned or loss

incurred.

Balance sheet- with help of balance sheet the audience of company will try to find the position of

company that is asset and liabilities of company.

Cash flow statement- with assistance of this statement audience is in condition to analyse the net

inflow or outflow of the cash and make necessary changes according to that.

Ratios- this is a financial analysis tool which assist audience to identify the relation of

company’s financial position with different aspect of business (Bernards and Campbell-Verduyn,

2019).

Horizontal analysis- this is used by audience in order to gather information relating to changes in

amount of corresponding financial statement items over a period of time.

Vertical analysis- this is used by audience as this will assist in gaining knowledge that each

particular of financial statement is compared against the base figure.

Trend analysis- this analysis is used by company in order to understand the trend or pattern of

any change and then try to follow it.

QUESTION 4

Role of different organization in international regulatory framework for accounting

IFRS foundation- the role of this organization in accounting framework is to develop and

promote the IFRS standards and bring in efficiency, transparency and accountability within the

financial market all over the globe (Melé, Rosanas and Fontrodona, 2017). The major goal is to

foster trust, growth and financial stability with respect to accounting all over the globe.

IFRS advisory council- the advisory council of IFRS major role is advise the board or decision

makers to take effective decision and to inform the board of the views of organization in setting

standard.

International accounting standards board- the role of IASB is to be responsible for all the matters

including making of IFRS, issuance of drafts, setting up of procedures for the review of

comments and many other matters.

9

IFRS interpretation committee- major role of IFRS interpretation committee is to interpret the

application and use of IFRS standards. This role is important as this assist company in

understanding the meaning of the standard and how to comply with it with help of interpretation.

Role of audit committees in corporate governance

The audit committee plays a crucial role in the corporate governance and its management. This is

particularly because of the fact that the main aim of audit committee of company is to give an

insight of whole financial reporting and the process. On the other side corporate governance is

referred to as the following of all rules and regulation and procedures which the company has to

follow in order to manage the business of the company. The major role of audit committee in

managing corporate governance in the company is to manage all the performance of company in

accordance with statutory requirement. This is the major role as when the audit committee of

company includes generally senior managers or employees of company (Rethel and Thurbon,,

2020).

Thus, these people know that how the company is working and what is the major requirement of

company. Thus, the audit committee in this will assist company in managing corporate

governance because of the reason that if corporate governance will not be managed then this will

be the responsibility of audit committee. The major reason underlying this fact audit committee

comprises of people belonging to company itself and if they will not be in condition of managing

the corporate governance then this will affect the working of the company.

In addition to this another major role of audit committee is that they are responsible for

managing corporate governance in company. If audit committee will not be able to manage the

corporate governance, then this will affect the whole working pattern and environment of

company (Nielson, , Parks, and Tierney, 2017). The major reason underlying this fact is that

audit committee creates the environment which includes the effective working according to the

rules and regulations prescribes under corporate governance.

Another major role of audit committee in managing and maintenance of corporate governance is

that it helps in effective application of all accounting policies and procedures. It is the duty of

audit committee to make sure that whether the company is abiding by the auditing procedure or

not and if not then what corrective actions are to be taken. Further another major role of auditing

committee in managing corporate governance is to comply with all the rules and regulation being

applicable over the business. The major reason for this is that when the auditing committee will

10

application and use of IFRS standards. This role is important as this assist company in

understanding the meaning of the standard and how to comply with it with help of interpretation.

Role of audit committees in corporate governance

The audit committee plays a crucial role in the corporate governance and its management. This is

particularly because of the fact that the main aim of audit committee of company is to give an

insight of whole financial reporting and the process. On the other side corporate governance is

referred to as the following of all rules and regulation and procedures which the company has to

follow in order to manage the business of the company. The major role of audit committee in

managing corporate governance in the company is to manage all the performance of company in

accordance with statutory requirement. This is the major role as when the audit committee of

company includes generally senior managers or employees of company (Rethel and Thurbon,,

2020).

Thus, these people know that how the company is working and what is the major requirement of

company. Thus, the audit committee in this will assist company in managing corporate

governance because of the reason that if corporate governance will not be managed then this will

be the responsibility of audit committee. The major reason underlying this fact audit committee

comprises of people belonging to company itself and if they will not be in condition of managing

the corporate governance then this will affect the working of the company.

In addition to this another major role of audit committee is that they are responsible for

managing corporate governance in company. If audit committee will not be able to manage the

corporate governance, then this will affect the whole working pattern and environment of

company (Nielson, , Parks, and Tierney, 2017). The major reason underlying this fact is that

audit committee creates the environment which includes the effective working according to the

rules and regulations prescribes under corporate governance.

Another major role of audit committee in managing and maintenance of corporate governance is

that it helps in effective application of all accounting policies and procedures. It is the duty of

audit committee to make sure that whether the company is abiding by the auditing procedure or

not and if not then what corrective actions are to be taken. Further another major role of auditing

committee in managing corporate governance is to comply with all the rules and regulation being

applicable over the business. The major reason for this is that when the auditing committee will

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.