Introduction to Finance: EOQ, Ratio Analysis, and Investment Decisions

VerifiedAdded on 2023/01/06

|16

|3728

|72

Homework Assignment

AI Summary

This finance assignment delves into key concepts including the Economic Order Quantity (EOQ) model, ratio analysis, and investment appraisal techniques. The solution presents calculations for EOQ, annual costs, and evaluates the decision to use the EOQ model for inventory management. It then an...

Introduction to

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 1....................................................................................................................................3

Question 2........................................................................................................................................5

Question 3..................................................................................................................................10

Question 4..................................................................................................................................12

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 1....................................................................................................................................3

Question 2........................................................................................................................................5

Question 3..................................................................................................................................10

Question 4..................................................................................................................................12

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

INTRODUCTION

Finance is a broad concept that includes practises relating to financial, debt or borrowing,

investing, capital markets, funds and equity. Basically, finance demonstrates the administration

of funds and the process for collecting the requisite funds (Tripathi, 2019). The function of

financing is to ensuring that there are adequate resources to operate and the business is able to

manage and retain the capital. This assessment is based on four distinct types of questions

involving the sources of funding, the estimation of the averages for the measurement of the

financial performance of the company and the use of investment appraisal methods to determine

the feasibility of the various alternatives. In addition, description of the position of a number of

diverse regulatory system entities and address the role of the audit board.

MAIN BODY

Question 1

(a) Measurement of EOQ-

Economic ordering quantity: √2*annual usage*Ordering cost/Carrying or holding cost

Annual usage: 27000 KG

Carrying or holding cost: $1.75 @ per KG of year

Ordering cost: $0.9

Hence,

EOQ: √2*27000*0.9/1.75

= √48600/1.75

= √27771.43

= 166.65 Or 167

(b) Calculation of annual cost-

Finance is a broad concept that includes practises relating to financial, debt or borrowing,

investing, capital markets, funds and equity. Basically, finance demonstrates the administration

of funds and the process for collecting the requisite funds (Tripathi, 2019). The function of

financing is to ensuring that there are adequate resources to operate and the business is able to

manage and retain the capital. This assessment is based on four distinct types of questions

involving the sources of funding, the estimation of the averages for the measurement of the

financial performance of the company and the use of investment appraisal methods to determine

the feasibility of the various alternatives. In addition, description of the position of a number of

diverse regulatory system entities and address the role of the audit board.

MAIN BODY

Question 1

(a) Measurement of EOQ-

Economic ordering quantity: √2*annual usage*Ordering cost/Carrying or holding cost

Annual usage: 27000 KG

Carrying or holding cost: $1.75 @ per KG of year

Ordering cost: $0.9

Hence,

EOQ: √2*27000*0.9/1.75

= √48600/1.75

= √27771.43

= 166.65 Or 167

(b) Calculation of annual cost-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Buying cost: 27000Kg @ 0.90

= $24300

Ordering cost: Annual demand*per unit ordering cost/EOQ

(27000*0.90/167)

= $145.50

Holding cost: Holding Cost per unit*EOQ/2

(1.75*167/2)

= $146

Hence,

Annual cost: $24300+$145.50+$146

= $24591.5

(c) Evaluation of decision to use EOQ model.

In reference to Touchdown Sports Inc, administrators use the EOQ model to define the

optimal order size that significantly reduces total expense or satisfy consumer demand.

EOQ may be about 167 that minimises costs or allows Touchdown Sports Inc. to

increase the profit margin. The Organization’s decision to choose this design is that it

needs to decrease stock or retention costs and determines how much company requires

retaining stock or re-ordering the other volume. This system can also suggest buying a

larger amount with fewer orders to take better advantage of reduced bulk sales and lower

ordering cost. Likewise, they may refer to more and more orders for fewer items to

minimise the operating costs, if they are high and the order volumes are typically low

(Mokhtari and Asadkhani, 2019).

(d) Suggestion to Touchdown plc.

The key aim of inventory control has been proposed to the senior leadership team of

Touchdown Sports Inc. to reduce the total cost of stock and, with the aid of the EOQ

model, executives are able to decrease it by minimising order or retaining expenses that

= $24300

Ordering cost: Annual demand*per unit ordering cost/EOQ

(27000*0.90/167)

= $145.50

Holding cost: Holding Cost per unit*EOQ/2

(1.75*167/2)

= $146

Hence,

Annual cost: $24300+$145.50+$146

= $24591.5

(c) Evaluation of decision to use EOQ model.

In reference to Touchdown Sports Inc, administrators use the EOQ model to define the

optimal order size that significantly reduces total expense or satisfy consumer demand.

EOQ may be about 167 that minimises costs or allows Touchdown Sports Inc. to

increase the profit margin. The Organization’s decision to choose this design is that it

needs to decrease stock or retention costs and determines how much company requires

retaining stock or re-ordering the other volume. This system can also suggest buying a

larger amount with fewer orders to take better advantage of reduced bulk sales and lower

ordering cost. Likewise, they may refer to more and more orders for fewer items to

minimise the operating costs, if they are high and the order volumes are typically low

(Mokhtari and Asadkhani, 2019).

(d) Suggestion to Touchdown plc.

The key aim of inventory control has been proposed to the senior leadership team of

Touchdown Sports Inc. to reduce the total cost of stock and, with the aid of the EOQ

model, executives are able to decrease it by minimising order or retaining expenses that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reduce the cost of the products that either meets consumer demand or fulfils the target of

the organisation to increase their benefit. Keeping costs are all expenses associated with

maintaining inventories that are not available. These costs are also part of the total cost of

product, along with the cost of purchase and the expense of scarcity. The cost of keeping

a company includes the price of missing or damaged objects, as well as storage room,

personnel and insurance. It is also noted that the Just-In-Time approach is more

appropriate when consumer demand is low but, in the event of high demand, the EOQ

model is more fitting. In the background of Touchdown Sports Inc., the largest maker of

safety apparel for sports people. It is very crucial for leaders to successfully apply the

EOQ model in order to reduce the total cost and then define the maximised quantity

needed to order in case of reducing storage and holding situation.

Question 2

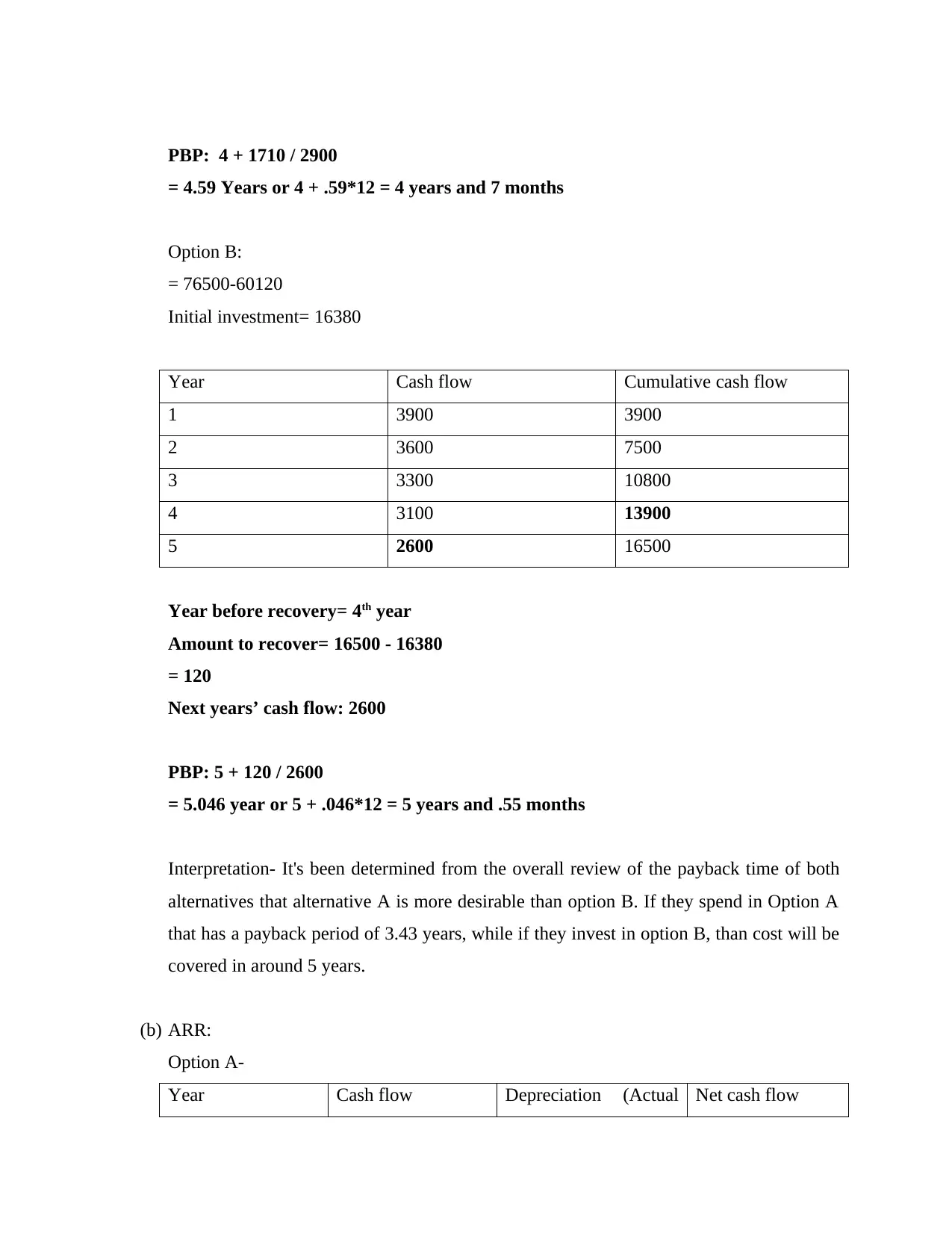

(a) Payback period: Year before recovery + amount to be recover/next years’ cash flow

Investment: Cost-Scrap value

Option A:

= 51000-40110

Initial investment= 10890

Year Cash flow Cumulative cash flow

1 3200 3200

2 3300 6500

3 3100 9600

4 3000 12600

5 2900 15500

Year before recovery= 3rd year

Amount to recover= 12600 – 10890 = 1710

Next years’ cash flow: 2900

the organisation to increase their benefit. Keeping costs are all expenses associated with

maintaining inventories that are not available. These costs are also part of the total cost of

product, along with the cost of purchase and the expense of scarcity. The cost of keeping

a company includes the price of missing or damaged objects, as well as storage room,

personnel and insurance. It is also noted that the Just-In-Time approach is more

appropriate when consumer demand is low but, in the event of high demand, the EOQ

model is more fitting. In the background of Touchdown Sports Inc., the largest maker of

safety apparel for sports people. It is very crucial for leaders to successfully apply the

EOQ model in order to reduce the total cost and then define the maximised quantity

needed to order in case of reducing storage and holding situation.

Question 2

(a) Payback period: Year before recovery + amount to be recover/next years’ cash flow

Investment: Cost-Scrap value

Option A:

= 51000-40110

Initial investment= 10890

Year Cash flow Cumulative cash flow

1 3200 3200

2 3300 6500

3 3100 9600

4 3000 12600

5 2900 15500

Year before recovery= 3rd year

Amount to recover= 12600 – 10890 = 1710

Next years’ cash flow: 2900

PBP: 4 + 1710 / 2900

= 4.59 Years or 4 + .59*12 = 4 years and 7 months

Option B:

= 76500-60120

Initial investment= 16380

Year Cash flow Cumulative cash flow

1 3900 3900

2 3600 7500

3 3300 10800

4 3100 13900

5 2600 16500

Year before recovery= 4th year

Amount to recover= 16500 - 16380

= 120

Next years’ cash flow: 2600

PBP: 5 + 120 / 2600

= 5.046 year or 5 + .046*12 = 5 years and .55 months

Interpretation- It's been determined from the overall review of the payback time of both

alternatives that alternative A is more desirable than option B. If they spend in Option A

that has a payback period of 3.43 years, while if they invest in option B, than cost will be

covered in around 5 years.

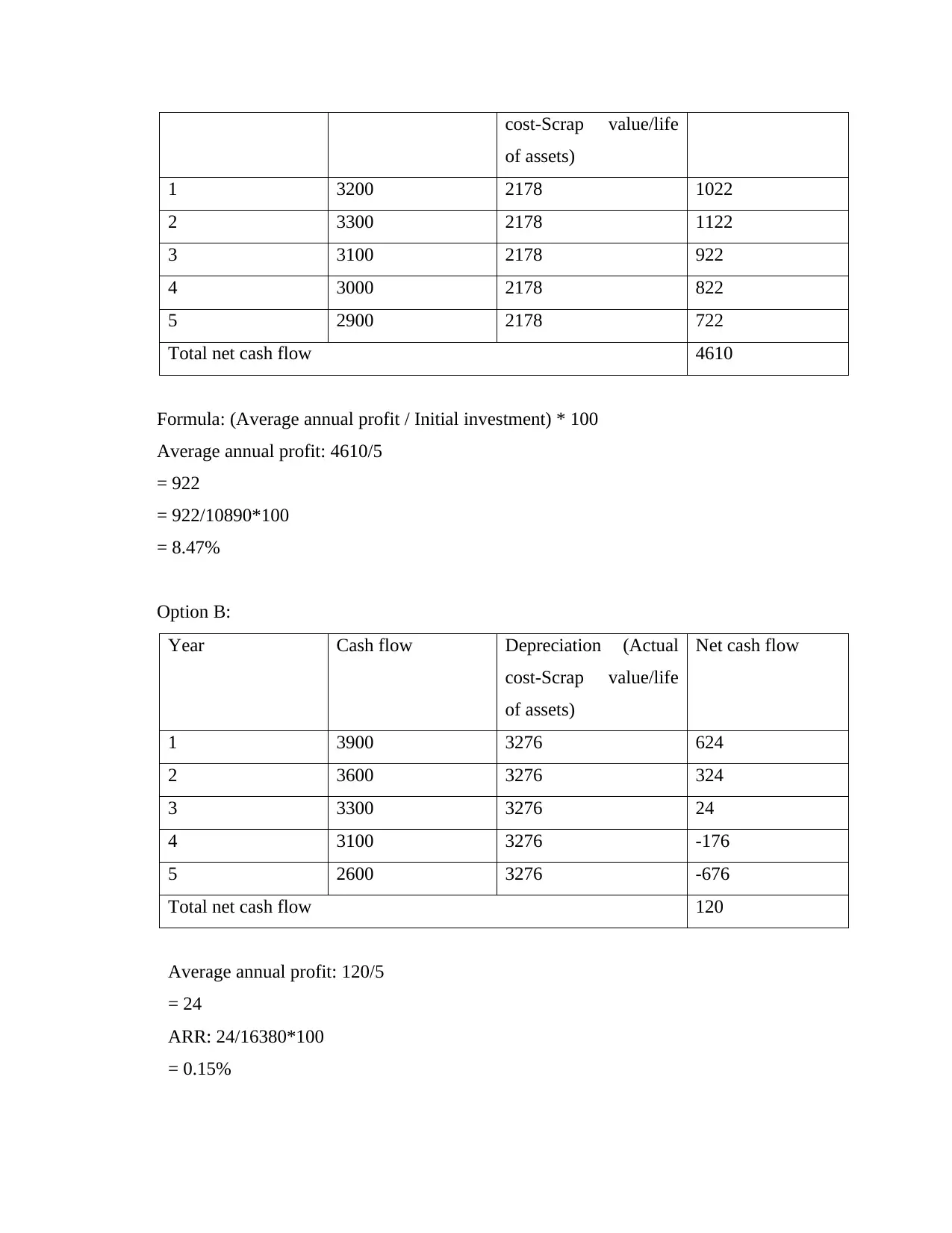

(b) ARR:

Option A-

Year Cash flow Depreciation (Actual Net cash flow

= 4.59 Years or 4 + .59*12 = 4 years and 7 months

Option B:

= 76500-60120

Initial investment= 16380

Year Cash flow Cumulative cash flow

1 3900 3900

2 3600 7500

3 3300 10800

4 3100 13900

5 2600 16500

Year before recovery= 4th year

Amount to recover= 16500 - 16380

= 120

Next years’ cash flow: 2600

PBP: 5 + 120 / 2600

= 5.046 year or 5 + .046*12 = 5 years and .55 months

Interpretation- It's been determined from the overall review of the payback time of both

alternatives that alternative A is more desirable than option B. If they spend in Option A

that has a payback period of 3.43 years, while if they invest in option B, than cost will be

covered in around 5 years.

(b) ARR:

Option A-

Year Cash flow Depreciation (Actual Net cash flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost-Scrap value/life

of assets)

1 3200 2178 1022

2 3300 2178 1122

3 3100 2178 922

4 3000 2178 822

5 2900 2178 722

Total net cash flow 4610

Formula: (Average annual profit / Initial investment) * 100

Average annual profit: 4610/5

= 922

= 922/10890*100

= 8.47%

Option B:

Year Cash flow Depreciation (Actual

cost-Scrap value/life

of assets)

Net cash flow

1 3900 3276 624

2 3600 3276 324

3 3300 3276 24

4 3100 3276 -176

5 2600 3276 -676

Total net cash flow 120

Average annual profit: 120/5

= 24

ARR: 24/16380*100

= 0.15%

of assets)

1 3200 2178 1022

2 3300 2178 1122

3 3100 2178 922

4 3000 2178 822

5 2900 2178 722

Total net cash flow 4610

Formula: (Average annual profit / Initial investment) * 100

Average annual profit: 4610/5

= 922

= 922/10890*100

= 8.47%

Option B:

Year Cash flow Depreciation (Actual

cost-Scrap value/life

of assets)

Net cash flow

1 3900 3276 624

2 3600 3276 324

3 3300 3276 24

4 3100 3276 -176

5 2600 3276 -676

Total net cash flow 120

Average annual profit: 120/5

= 24

ARR: 24/16380*100

= 0.15%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

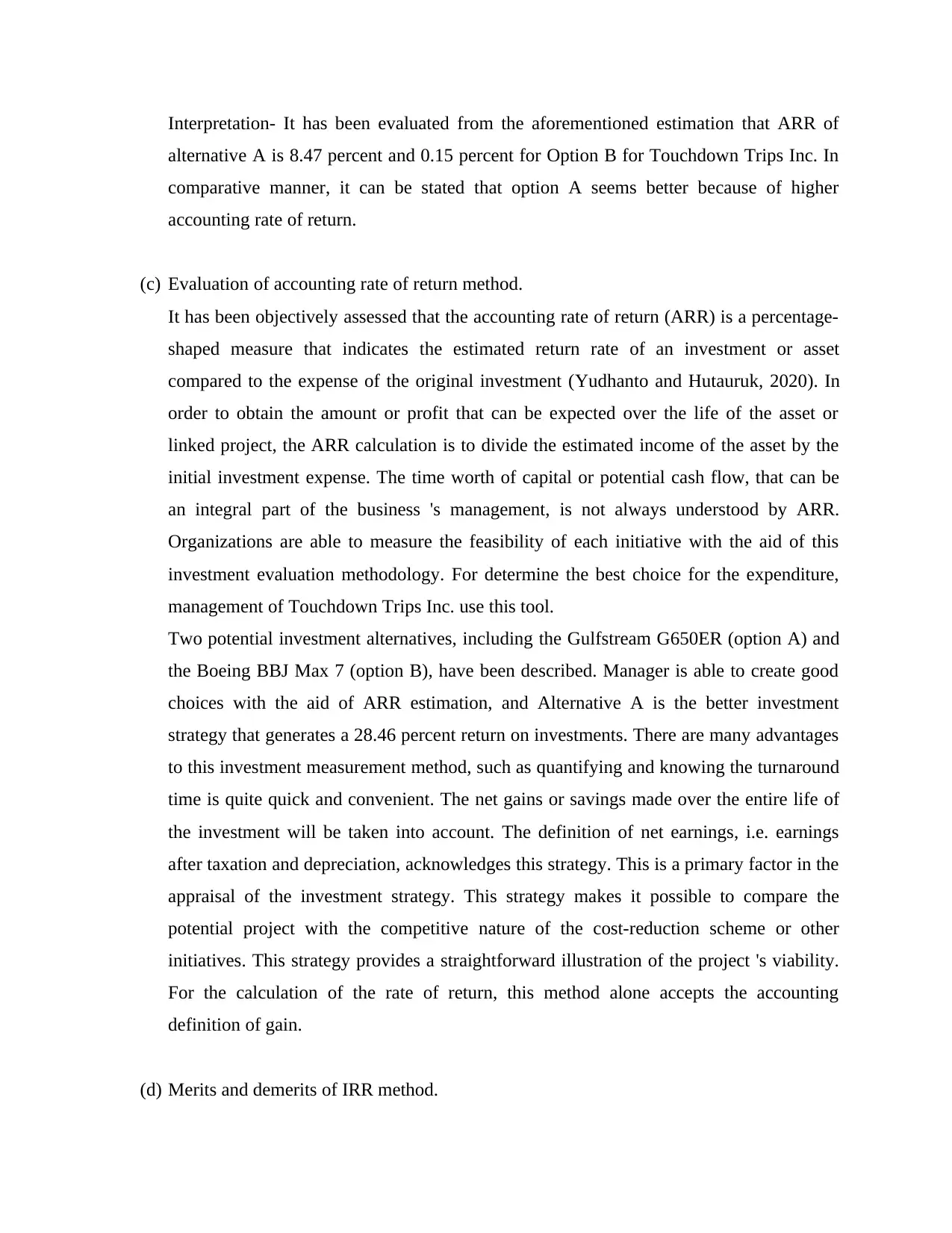

Interpretation- It has been evaluated from the aforementioned estimation that ARR of

alternative A is 8.47 percent and 0.15 percent for Option B for Touchdown Trips Inc. In

comparative manner, it can be stated that option A seems better because of higher

accounting rate of return.

(c) Evaluation of accounting rate of return method.

It has been objectively assessed that the accounting rate of return (ARR) is a percentage-

shaped measure that indicates the estimated return rate of an investment or asset

compared to the expense of the original investment (Yudhanto and Hutauruk, 2020). In

order to obtain the amount or profit that can be expected over the life of the asset or

linked project, the ARR calculation is to divide the estimated income of the asset by the

initial investment expense. The time worth of capital or potential cash flow, that can be

an integral part of the business 's management, is not always understood by ARR.

Organizations are able to measure the feasibility of each initiative with the aid of this

investment evaluation methodology. For determine the best choice for the expenditure,

management of Touchdown Trips Inc. use this tool.

Two potential investment alternatives, including the Gulfstream G650ER (option A) and

the Boeing BBJ Max 7 (option B), have been described. Manager is able to create good

choices with the aid of ARR estimation, and Alternative A is the better investment

strategy that generates a 28.46 percent return on investments. There are many advantages

to this investment measurement method, such as quantifying and knowing the turnaround

time is quite quick and convenient. The net gains or savings made over the entire life of

the investment will be taken into account. The definition of net earnings, i.e. earnings

after taxation and depreciation, acknowledges this strategy. This is a primary factor in the

appraisal of the investment strategy. This strategy makes it possible to compare the

potential project with the competitive nature of the cost-reduction scheme or other

initiatives. This strategy provides a straightforward illustration of the project 's viability.

For the calculation of the rate of return, this method alone accepts the accounting

definition of gain.

(d) Merits and demerits of IRR method.

alternative A is 8.47 percent and 0.15 percent for Option B for Touchdown Trips Inc. In

comparative manner, it can be stated that option A seems better because of higher

accounting rate of return.

(c) Evaluation of accounting rate of return method.

It has been objectively assessed that the accounting rate of return (ARR) is a percentage-

shaped measure that indicates the estimated return rate of an investment or asset

compared to the expense of the original investment (Yudhanto and Hutauruk, 2020). In

order to obtain the amount or profit that can be expected over the life of the asset or

linked project, the ARR calculation is to divide the estimated income of the asset by the

initial investment expense. The time worth of capital or potential cash flow, that can be

an integral part of the business 's management, is not always understood by ARR.

Organizations are able to measure the feasibility of each initiative with the aid of this

investment evaluation methodology. For determine the best choice for the expenditure,

management of Touchdown Trips Inc. use this tool.

Two potential investment alternatives, including the Gulfstream G650ER (option A) and

the Boeing BBJ Max 7 (option B), have been described. Manager is able to create good

choices with the aid of ARR estimation, and Alternative A is the better investment

strategy that generates a 28.46 percent return on investments. There are many advantages

to this investment measurement method, such as quantifying and knowing the turnaround

time is quite quick and convenient. The net gains or savings made over the entire life of

the investment will be taken into account. The definition of net earnings, i.e. earnings

after taxation and depreciation, acknowledges this strategy. This is a primary factor in the

appraisal of the investment strategy. This strategy makes it possible to compare the

potential project with the competitive nature of the cost-reduction scheme or other

initiatives. This strategy provides a straightforward illustration of the project 's viability.

For the calculation of the rate of return, this method alone accepts the accounting

definition of gain.

(d) Merits and demerits of IRR method.

Investment alternative A is chosen on the basis of the aforementioned study, which has a

lower recovery time and a stronger ARR. Moreover, Touchdown Trips Inc.

administrators can make successful judgments with the aid of investment evaluation

methods (Khasikov, 2020). Investment assessment approaches provide some attributes

that have a deeper interpretation and they are as follows:

Assessment of the amount of expected returns earned in comparison to the degree

of investment sustained.

It foresees the potential risks and profits over the project lifecycle.

The group's costs and output can be calculated over the estimated length of the

project while assessing the proposed capital investment.

Usually, this is the projected useful life of a non-current commodity to be

obtained for several years as well.

This assumes that prospective forecasts of costs and rewards call for long-term

projections.

Moreover, the internal rate of return strategy has some benefits and drawbacks. These

are as follows:

Merits:

The first and most important aspect is that when analysing a proposal, the IRR takes the

time value of capital into consideration. This is a significant decline in the ARR, the total

return rate and the duration of payback (Nami and Anvari-Moghaddam, 2020). It is

possible to measure the IRR by calculating rate at which the cash flow PV is equal to the

necessary capital spending.

The most enticing thing about this method, when it has been calculated after IRR, is

really simple to understand. Endorse the project, and otherwise not, until the IRR reaches

the money value. For managers, this is very easy to imagine, which is why it is better that

they do not face sporadic unfinished situations, such as similarly limited services, etc.

Demerits:

This necessarily involves the new investment of positive cash flows for the future into an

IRR for the existing period of the project when assessing a project using IRR method. If

the idea has a lower IRR, a low rate of return is expected for capital investment. If the

lower recovery time and a stronger ARR. Moreover, Touchdown Trips Inc.

administrators can make successful judgments with the aid of investment evaluation

methods (Khasikov, 2020). Investment assessment approaches provide some attributes

that have a deeper interpretation and they are as follows:

Assessment of the amount of expected returns earned in comparison to the degree

of investment sustained.

It foresees the potential risks and profits over the project lifecycle.

The group's costs and output can be calculated over the estimated length of the

project while assessing the proposed capital investment.

Usually, this is the projected useful life of a non-current commodity to be

obtained for several years as well.

This assumes that prospective forecasts of costs and rewards call for long-term

projections.

Moreover, the internal rate of return strategy has some benefits and drawbacks. These

are as follows:

Merits:

The first and most important aspect is that when analysing a proposal, the IRR takes the

time value of capital into consideration. This is a significant decline in the ARR, the total

return rate and the duration of payback (Nami and Anvari-Moghaddam, 2020). It is

possible to measure the IRR by calculating rate at which the cash flow PV is equal to the

necessary capital spending.

The most enticing thing about this method, when it has been calculated after IRR, is

really simple to understand. Endorse the project, and otherwise not, until the IRR reaches

the money value. For managers, this is very easy to imagine, which is why it is better that

they do not face sporadic unfinished situations, such as similarly limited services, etc.

Demerits:

This necessarily involves the new investment of positive cash flows for the future into an

IRR for the existing period of the project when assessing a project using IRR method. If

the idea has a lower IRR, a low rate of return is expected for capital investment. If the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other strategy appears to have a very high IRR, a very high return would be expected for

reinvestment.

The downside of the IRR is that important factors, such as the time cycle of the project,

future costs or the size of the project, are not really taken into consideration by the

process. Except for those considerations, the IRR adequately operates the cash outcomes

of the process at the existing expense of the venture.

Question 3

(a) Measurement of ratios-

Ratio analysis- Through analyzing financial statements including the balance sheet and

income statement, ratio analysis is a quantitative way of gaining visibility into the

sustainability, operating performance, and performance of a company (Kärenlampi,

2020). A foundation of quantitative equity valuation is ratio analysis.

Gross profit margin:

Gross profit margin = Gross profit / Revenue * 100

= 1313 / 3495 * 100

= 37.56%

Assets turnover ratio:

Assets turnover ratio = Net Sales / Total assets

= 3495 / 2898

= 1.20 times

The turnover ratio of assets is greater than 1, and it's always great. Since that ensures that the

company generates sufficient income from assets.

Current ratio:

Current ratio = Current assets / Current liabilities

= 1687 / 744

= 2.26 times

reinvestment.

The downside of the IRR is that important factors, such as the time cycle of the project,

future costs or the size of the project, are not really taken into consideration by the

process. Except for those considerations, the IRR adequately operates the cash outcomes

of the process at the existing expense of the venture.

Question 3

(a) Measurement of ratios-

Ratio analysis- Through analyzing financial statements including the balance sheet and

income statement, ratio analysis is a quantitative way of gaining visibility into the

sustainability, operating performance, and performance of a company (Kärenlampi,

2020). A foundation of quantitative equity valuation is ratio analysis.

Gross profit margin:

Gross profit margin = Gross profit / Revenue * 100

= 1313 / 3495 * 100

= 37.56%

Assets turnover ratio:

Assets turnover ratio = Net Sales / Total assets

= 3495 / 2898

= 1.20 times

The turnover ratio of assets is greater than 1, and it's always great. Since that ensures that the

company generates sufficient income from assets.

Current ratio:

Current ratio = Current assets / Current liabilities

= 1687 / 744

= 2.26 times

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acid test ratio:

Acid test ratio = Quick assets / Current liabilities

= 1537 / 744

= 2.06 times

Working Notes:

Quick assets = Current assets – Inventory

= 1687 – 150

= 1537

Inventories turnover period:

Inventories turnover period = Cost of Goods Sold (COGS) / Average Inventory

= 2182 / 126

= 17.31

Working Notes:

Average inventory = (Opening stock + Closing stock) / 2

= (102 + 150) / 2

= 252 / 2

= 126

Debt to Equity ratio:

Debt to Equity ratio = Total liabilities / Total shareholder’s equity

= 914 / 2898

= 0.31

(b) Role of considering the financial statement analysis.

The review of financial reports can be defined by reviewing the financial details

published, in general the annual and quarterly accounts, as the method of taking care of

the condition and results of an organisation (Michael, 2019). Financial statement analysis

is a predictive assessment instrument for determining a company's historical, current and

future results, and is more applicable to the viewer or investors required for research and

Acid test ratio = Quick assets / Current liabilities

= 1537 / 744

= 2.06 times

Working Notes:

Quick assets = Current assets – Inventory

= 1687 – 150

= 1537

Inventories turnover period:

Inventories turnover period = Cost of Goods Sold (COGS) / Average Inventory

= 2182 / 126

= 17.31

Working Notes:

Average inventory = (Opening stock + Closing stock) / 2

= (102 + 150) / 2

= 252 / 2

= 126

Debt to Equity ratio:

Debt to Equity ratio = Total liabilities / Total shareholder’s equity

= 914 / 2898

= 0.31

(b) Role of considering the financial statement analysis.

The review of financial reports can be defined by reviewing the financial details

published, in general the annual and quarterly accounts, as the method of taking care of

the condition and results of an organisation (Michael, 2019). Financial statement analysis

is a predictive assessment instrument for determining a company's historical, current and

future results, and is more applicable to the viewer or investors required for research and

for making more successful decisions about their interest in a specific entity. The most

critical aspect of the financial reports analysis is that it offers shareholders with the ability

to invest by deciding to focus their funds on a single entity. Another value of the financial

reports analysis is that the organisation can verify that federal agencies such as the IASB

meet with the applicable accounting requirements. In reviewing the taxes owed to the

corporation, the analysis of the financial reports is of benefit to the government officials.

It just makes complete sense to just try to learn how well the company performs

according to a specific litmus test if any person considers spending money in the

company, not the indicators an organisation has designed to make itself look better.

That's when the value for clients in financial reports comes into effect. This also extends

to sources of credit and banks who recommend lending capital to a corporation. In such

situations, a clear perception of how likely persons are to be rewarded in full will need to

be obtained so that they can make savings correctly. The relevance of review and

presentation of financial statements also applies to shareholders.

It is necessary to ensure full disclosure to all properties, liabilities, resource use, revenues

and associated company expenses whether they hold shares in a firm or are an investment

company with a major equity interest. Users would also want to learn that the

organisation does things that they shouldn't have to do.

Question 4

(a)

IFRS Foundation:

The creation, through its best practice body, the IASB, of a popular set of high-

quality, available, binding legal and globally accepted International Financial

Reporting Standards (IFRSs).

Promote the use of such requirements and their rigorous execution

(Karabarbounis and Neiman, 2019).

Take into account the demands of emerging countries and small and medium-

sized companies (SMEs) in the financial report.

critical aspect of the financial reports analysis is that it offers shareholders with the ability

to invest by deciding to focus their funds on a single entity. Another value of the financial

reports analysis is that the organisation can verify that federal agencies such as the IASB

meet with the applicable accounting requirements. In reviewing the taxes owed to the

corporation, the analysis of the financial reports is of benefit to the government officials.

It just makes complete sense to just try to learn how well the company performs

according to a specific litmus test if any person considers spending money in the

company, not the indicators an organisation has designed to make itself look better.

That's when the value for clients in financial reports comes into effect. This also extends

to sources of credit and banks who recommend lending capital to a corporation. In such

situations, a clear perception of how likely persons are to be rewarded in full will need to

be obtained so that they can make savings correctly. The relevance of review and

presentation of financial statements also applies to shareholders.

It is necessary to ensure full disclosure to all properties, liabilities, resource use, revenues

and associated company expenses whether they hold shares in a firm or are an investment

company with a major equity interest. Users would also want to learn that the

organisation does things that they shouldn't have to do.

Question 4

(a)

IFRS Foundation:

The creation, through its best practice body, the IASB, of a popular set of high-

quality, available, binding legal and globally accepted International Financial

Reporting Standards (IFRSs).

Promote the use of such requirements and their rigorous execution

(Karabarbounis and Neiman, 2019).

Take into account the demands of emerging countries and small and medium-

sized companies (SMEs) in the financial report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Develop and promote the organization, through the incorporation of national

accounting standards and IFRSs, of IFRSs, that are recommendations and

descriptions supplied by the IASB.

IFRS Advisory Council

The IFRS advisory group is the official professional advisory panel for the IASB

and the IFRS Foundation Members. This involves a wide number of stakeholders

from the related communities that are active in the application of the IASB.

This contains financial reporting customers, finance analysts and other customers,

as well as auditors, academics, bookkeepers, legislators, accounting consultancy

companies and regular-setters. The Trustees shall nominate the members of the

Advisory Board.

The advisory group normally meets three times a year in London for a total of two

days.

The chairman of the IASB, the Manager of Technological Practices, the Director

of Studies, the Director of Execution actions and the members of the IASB and

the directly affecting for the agenda items of the Consultative Council are

normally expected to engage in the proceedings of the Consultative Council.

International Accounting Standards Board (IASB):

The task of its representatives (presently 16 full-time representatives) is to produce and

release IFRSs, like IFRSs for small and medium-sized businesses, as well as to accept

IFRS Explanations as set up by the International accounting Panel (formerly IFRIC). In

general and on the web, all IASB debates are planned (Warren, Jonick and Schneider,

2020).

The IASB facilitates comprehensive, accessible and usable due process in the execution

of its national standards positions, where even the release of informative materials, such

as consultation papers and recommendations for transparency, is an important aspect of

government opinion.

The IASB works closely with global partners, such as customers, experts, politicians,

business executives, financial reporting agencies and finance companies.

accounting standards and IFRSs, of IFRSs, that are recommendations and

descriptions supplied by the IASB.

IFRS Advisory Council

The IFRS advisory group is the official professional advisory panel for the IASB

and the IFRS Foundation Members. This involves a wide number of stakeholders

from the related communities that are active in the application of the IASB.

This contains financial reporting customers, finance analysts and other customers,

as well as auditors, academics, bookkeepers, legislators, accounting consultancy

companies and regular-setters. The Trustees shall nominate the members of the

Advisory Board.

The advisory group normally meets three times a year in London for a total of two

days.

The chairman of the IASB, the Manager of Technological Practices, the Director

of Studies, the Director of Execution actions and the members of the IASB and

the directly affecting for the agenda items of the Consultative Council are

normally expected to engage in the proceedings of the Consultative Council.

International Accounting Standards Board (IASB):

The task of its representatives (presently 16 full-time representatives) is to produce and

release IFRSs, like IFRSs for small and medium-sized businesses, as well as to accept

IFRS Explanations as set up by the International accounting Panel (formerly IFRIC). In

general and on the web, all IASB debates are planned (Warren, Jonick and Schneider,

2020).

The IASB facilitates comprehensive, accessible and usable due process in the execution

of its national standards positions, where even the release of informative materials, such

as consultation papers and recommendations for transparency, is an important aspect of

government opinion.

The IASB works closely with global partners, such as customers, experts, politicians,

business executives, financial reporting agencies and finance companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IFRS Interpretations Committee:

The conceptual agency of the IASB is the International accounting Commission. The

Interpretation segment comprises of 14 voting members appointed by the Stewards and

picked from a number of degrees of foreign experience.

The task of the Implementation Panel is to review, on a regular basis, critical accounting

problems occurring within the meaning of current IFRSs and to provide remedial steps

(IFRICs) on these problems.

Representatives of the Classification member shall be freely available and webcast. The

Explanation Panel collaborates with relevant national commissions in the formulation of

interpretations and maintains a transparent, comprehensive and usable due procedure.

(b)

At least one individual on the council who is considered to be a financial specialist must be on

the external auditors. This is not necessary for the members of the board to be technical

consultants, but they would be people who are aware about financial challenges or who have a

clear understanding of accounting principles, finance and audit terms and definitions (Kanal, D.

and Kornegay, 2019). In the financial reporting process, senior management and auditors

(independent auditors) play a major part. The manager is also responsible for reviewing the

financial records and for creating the company's financial protection procedures.

Management also has to establish internal procedures to ensure that the method of company audit

is accurate and effective. It is the responsibility of the independent accountant to express an idea

on the efficacy of the firm's earnings accounts, including the company's financial transactions in

terms of operational performance and working capital, and to aid with ensuring that these issues

conform to widely agree financial accounting methods.

The members of the panel will need to evaluate how the government collects and reflects on

inner financial details until the audit committee performs their work (Adams and Hunter, 2019).

Analysis of internal documents has the opportunity of internal auditors to address concerns about

the completeness, accuracy and time management of audit results. Having a clear summary of

the audit results means that the audit committee members are aware of the potential

The conceptual agency of the IASB is the International accounting Commission. The

Interpretation segment comprises of 14 voting members appointed by the Stewards and

picked from a number of degrees of foreign experience.

The task of the Implementation Panel is to review, on a regular basis, critical accounting

problems occurring within the meaning of current IFRSs and to provide remedial steps

(IFRICs) on these problems.

Representatives of the Classification member shall be freely available and webcast. The

Explanation Panel collaborates with relevant national commissions in the formulation of

interpretations and maintains a transparent, comprehensive and usable due procedure.

(b)

At least one individual on the council who is considered to be a financial specialist must be on

the external auditors. This is not necessary for the members of the board to be technical

consultants, but they would be people who are aware about financial challenges or who have a

clear understanding of accounting principles, finance and audit terms and definitions (Kanal, D.

and Kornegay, 2019). In the financial reporting process, senior management and auditors

(independent auditors) play a major part. The manager is also responsible for reviewing the

financial records and for creating the company's financial protection procedures.

Management also has to establish internal procedures to ensure that the method of company audit

is accurate and effective. It is the responsibility of the independent accountant to express an idea

on the efficacy of the firm's earnings accounts, including the company's financial transactions in

terms of operational performance and working capital, and to aid with ensuring that these issues

conform to widely agree financial accounting methods.

The members of the panel will need to evaluate how the government collects and reflects on

inner financial details until the audit committee performs their work (Adams and Hunter, 2019).

Analysis of internal documents has the opportunity of internal auditors to address concerns about

the completeness, accuracy and time management of audit results. Having a clear summary of

the audit results means that the audit committee members are aware of the potential

consequences of the financial statement. Recent policy and organisational changes and updates

should also be up-to - date with all audit committees.

Conclusion

It has been noted from the aforementioned article that financing or financial planning lies

in its capacity to keep a firm running smoothly despite declaring bankruptcy while also drawing

long-term investment funds. Financial ratios allow companies to determine the viability of the

enterprise and management may choose the right investment strategies that are more

advantageous as well as productive with the aid of investment evaluation approaches.

should also be up-to - date with all audit committees.

Conclusion

It has been noted from the aforementioned article that financing or financial planning lies

in its capacity to keep a firm running smoothly despite declaring bankruptcy while also drawing

long-term investment funds. Financial ratios allow companies to determine the viability of the

enterprise and management may choose the right investment strategies that are more

advantageous as well as productive with the aid of investment evaluation approaches.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Tripathi, R.P., 2019. Economic order quantity models for price dependent demand and different

holding cost functions. JORDAN J Math Stat, 12(1), pp.15-33.

Mokhtari, H. and Asadkhani, J., 2019. Economic Order Quantity for Imperfect Quality Items

under Inspection Errors, Batch Replacement and Multiple Sales of Returned

Items. Scientia Iranica.

Yudhanto, N.A. and Hutauruk, P.S., 2020, July. Calculation of EOQ (Economic Order Quantity)

In Optimizing the Inventory Level of Dacron at Mell Toys’ Home Industry. In Journal of

Physics: Conference Series (Vol. 1573, No. 1, p. 012036). IOP Publishing.

Khasikov, S., 2020. Calculation of the Payback Period for Energy-Efficient Building

Envelope. MS&E, 753(4), p.042032.

Nami, H. and Anvari-Moghaddam, A., 2020. Small-scale CCHP systems for waste heat recovery

from cement plants: Thermodynamic, sustainability and economic

implications. Energy, 192, p.116634.

Kärenlampi, P.P., 2020. Net present value of multiannual growth in the absence of periodic

boundary conditions. Agricultural Finance Review.

Michael, A., 2019. The Net Present Value of a Hydraulic Fracture Treatment. Society of

Petroleum Engineers. The Way Ahead.

Karabarbounis, L. and Neiman, B., 2019. Accounting for factorless income. NBER

Macroeconomics Annual, 33(1), pp.167-228.

Kanal, D. and Kornegay, J.T., 2019. Accounting for Household Production in the National

Accounts. Survey of Current Business, 99(6), pp.1-9.

Warren, C., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

Tripathi, R.P., 2019. Economic order quantity models for price dependent demand and different

holding cost functions. JORDAN J Math Stat, 12(1), pp.15-33.

Mokhtari, H. and Asadkhani, J., 2019. Economic Order Quantity for Imperfect Quality Items

under Inspection Errors, Batch Replacement and Multiple Sales of Returned

Items. Scientia Iranica.

Yudhanto, N.A. and Hutauruk, P.S., 2020, July. Calculation of EOQ (Economic Order Quantity)

In Optimizing the Inventory Level of Dacron at Mell Toys’ Home Industry. In Journal of

Physics: Conference Series (Vol. 1573, No. 1, p. 012036). IOP Publishing.

Khasikov, S., 2020. Calculation of the Payback Period for Energy-Efficient Building

Envelope. MS&E, 753(4), p.042032.

Nami, H. and Anvari-Moghaddam, A., 2020. Small-scale CCHP systems for waste heat recovery

from cement plants: Thermodynamic, sustainability and economic

implications. Energy, 192, p.116634.

Kärenlampi, P.P., 2020. Net present value of multiannual growth in the absence of periodic

boundary conditions. Agricultural Finance Review.

Michael, A., 2019. The Net Present Value of a Hydraulic Fracture Treatment. Society of

Petroleum Engineers. The Way Ahead.

Karabarbounis, L. and Neiman, B., 2019. Accounting for factorless income. NBER

Macroeconomics Annual, 33(1), pp.167-228.

Kanal, D. and Kornegay, J.T., 2019. Accounting for Household Production in the National

Accounts. Survey of Current Business, 99(6), pp.1-9.

Warren, C., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.