Finance Report: Financial Ratio Analysis and Investment Appraisal

VerifiedAdded on 2023/06/04

|16

|3493

|148

Report

AI Summary

This finance report provides a comprehensive analysis of various financial aspects. It begins with an introduction to finance and then delves into detailed calculations of financial ratios, including gross profit margin, asset usage ratio, and current ratio, offering interpretations and insights into their significance. The report also covers the importance of considering the audience for financial statement analysis. Furthermore, it includes the preparation of a monthly cash budget, break-even point calculations, and margin of safety analysis. The report then proceeds to investment appraisal techniques, calculating payback period, net present value (NPV), and accounting rate of return (ARR) for different investment options, culminating in recommendations on which projects to undertake and discussions on improving investment appraisal approaches. The report, contributed by a student, is available on Desklib, a platform for AI-based study tools.

Introduction to finance

Contents

Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

a) Calculation of financial ratios............................................................................................3

b) The importance of considering the audience for financial statement analysis...................5

Question 2........................................................................................................................................5

a) Opening statement of financial position.............................................................................5

b ) monthly cash budget for 6 months....................................................................................6

c) Description of additional expenditure................................................................................7

Question 3........................................................................................................................................7

a) Calculation of breakeven point...........................................................................................7

b) Margin of safety ( MOS ) for the year ended 2019 and 2020............................................8

c) Analysis about new strategy formed by Jessica.................................................................9

Question 4........................................................................................................................................9

Calculation of payback period, NPV and ARR......................................................................9

Analysis for the project that should be undertaken..............................................................12

Approaches to investment appraisals and their improvement..............................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

a) Calculation of financial ratios............................................................................................3

b) The importance of considering the audience for financial statement analysis...................5

Question 2........................................................................................................................................5

a) Opening statement of financial position.............................................................................5

b ) monthly cash budget for 6 months....................................................................................6

c) Description of additional expenditure................................................................................7

Question 3........................................................................................................................................7

a) Calculation of breakeven point...........................................................................................7

b) Margin of safety ( MOS ) for the year ended 2019 and 2020............................................8

c) Analysis about new strategy formed by Jessica.................................................................9

Question 4........................................................................................................................................9

Calculation of payback period, NPV and ARR......................................................................9

Analysis for the project that should be undertaken..............................................................12

Approaches to investment appraisals and their improvement..............................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Finance is the understanding and discipline of cash, currencies, and assets. It is associated

to, but not identical with, economics, the education of the manufacture, distribution, and

ingesting of cash, capital assets, goods, and services. Since financial activities take place in the

system of finance in numerous sectors, the sectors can be broadly categorised into personal

finance, corporate finance and public finance. Accounting for financial management is the

maintenance frequently related with CFO and finance branch of the organisation. These type of

services mainly encompass looking into the future by converting a plan for business into a

budget or a financial model and assist an organisation to manage its plan (Atrill and Lindley,

2019). This report contains the calculation of numerous ratios and their analysis, preparing cash

budget, and analysis for NPV.

MAIN BODY

Question 1

a) Calculation of financial ratios

Gross profit margin = ( sales - COGS ) * 100 / sales

= ( 3495 – 2182 ) * 100 / 3495

= ( 1313 / 3495 ) * 100

= 37.57 %

Assets usage ratio = total sales / average total assets

= 3495 / [( 3812 + 2503 ) / 2]

= 3495 / 3157.5

= 1.10 times

Current ratio = current assets / current liabilities

= 1687 / 744

= 2.27 times

Acid test ratio = ( Current asset – stock ) / current liability

= ( 1687 – 150 ) / 744

= 1537 / 744

Finance is the understanding and discipline of cash, currencies, and assets. It is associated

to, but not identical with, economics, the education of the manufacture, distribution, and

ingesting of cash, capital assets, goods, and services. Since financial activities take place in the

system of finance in numerous sectors, the sectors can be broadly categorised into personal

finance, corporate finance and public finance. Accounting for financial management is the

maintenance frequently related with CFO and finance branch of the organisation. These type of

services mainly encompass looking into the future by converting a plan for business into a

budget or a financial model and assist an organisation to manage its plan (Atrill and Lindley,

2019). This report contains the calculation of numerous ratios and their analysis, preparing cash

budget, and analysis for NPV.

MAIN BODY

Question 1

a) Calculation of financial ratios

Gross profit margin = ( sales - COGS ) * 100 / sales

= ( 3495 – 2182 ) * 100 / 3495

= ( 1313 / 3495 ) * 100

= 37.57 %

Assets usage ratio = total sales / average total assets

= 3495 / [( 3812 + 2503 ) / 2]

= 3495 / 3157.5

= 1.10 times

Current ratio = current assets / current liabilities

= 1687 / 744

= 2.27 times

Acid test ratio = ( Current asset – stock ) / current liability

= ( 1687 – 150 ) / 744

= 1537 / 744

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 2.06 times

Inventory holding period = ( average inventory / cost of goods sold ) * 365

= [( 150 + 102 ) / 2 ] / 2182 * 365

= ( 126 / 2182 ) * 365

= 21.08 days

Debt to equity ratio = total debts / total equity

= 170 / 2898

= 0.058 times

Interpretations:

Gross profit margin: It is generally classified as a profitability measure that compares a

company's total profit to its turnover. Given the question, the total profit is 37.57% which is

38%. This means, as a growing company in the industry, only after deducting the cost of these

commodities.

Assets usage ratio: It is categorized as an efficiency ratio that helps an organization generate

turnover from its holdings in terms of monetary value using net income of average total asset

value. This ratio means that the higher the ratio, the more efficient the organization. The ideal

ratio is 2.5 times or more (Baker, Kumar and Pandey, 2020). Given the question, the

organization's asset utilization is 1.10, which is well below ideal. Business need to improve your

ability to generate income and maximize the use of assets in the right way.

Current ratio: This ratio measures a company's ability to meet its short-term obligations in the

short term. Analyze the company's short-term liquidity. The ideal ratio is 2:1, but the specified

company scored 2.27, which is above ideal. This is the most suitable situation for companies

with more working capital.

Acid test ratio: This endurance-test ratio compares an organization's highly liquid assets to

current liabilities. Ideally once. This question gives 2.06 hours. This means a safer, more rational

ability to meet short-term commitments.

Inventory holding period = ( average inventory / cost of goods sold ) * 365

= [( 150 + 102 ) / 2 ] / 2182 * 365

= ( 126 / 2182 ) * 365

= 21.08 days

Debt to equity ratio = total debts / total equity

= 170 / 2898

= 0.058 times

Interpretations:

Gross profit margin: It is generally classified as a profitability measure that compares a

company's total profit to its turnover. Given the question, the total profit is 37.57% which is

38%. This means, as a growing company in the industry, only after deducting the cost of these

commodities.

Assets usage ratio: It is categorized as an efficiency ratio that helps an organization generate

turnover from its holdings in terms of monetary value using net income of average total asset

value. This ratio means that the higher the ratio, the more efficient the organization. The ideal

ratio is 2.5 times or more (Baker, Kumar and Pandey, 2020). Given the question, the

organization's asset utilization is 1.10, which is well below ideal. Business need to improve your

ability to generate income and maximize the use of assets in the right way.

Current ratio: This ratio measures a company's ability to meet its short-term obligations in the

short term. Analyze the company's short-term liquidity. The ideal ratio is 2:1, but the specified

company scored 2.27, which is above ideal. This is the most suitable situation for companies

with more working capital.

Acid test ratio: This endurance-test ratio compares an organization's highly liquid assets to

current liabilities. Ideally once. This question gives 2.06 hours. This means a safer, more rational

ability to meet short-term commitments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory holding period: Inventory holding time is a ratio that represents the number of days a

company holds inventory before selling. Indicates the number of days it takes for inventory to

rotate within the organization.

Debt to equity ratio: If there is high leverage in this ratio, it indicates that the company has more

leverage from the capital markets in its business. Low leverage, on the other hand, indicates that

the asset is being used optimally and is less leveraged outside the market. For this particular

question, 0.058 means less borrowed capital and less risk on hand (Brunstein and Perera, 2019).

b) The importance of considering the audience for financial statement analysis

This is the financial statement for the fiscal year, divided into expenses and income.

Provide opportunities for internal and external stakeholders to make informed decisions related

to investments. It also gives lenders an unbiased view of a company's financial health. This helps

with loan selection. This assessment reviews the trading company's financial statements to gain

insight into its financial functioning. These statements consist of profit statements, stability

sheets, and coin flows. Evaluation of the internal workings is done by workers, authorities,

managers, etc. using accounting information from the trading company. External ratings, on the

other hand, are done by outsiders who have access to the posted account. This includes investors,

credit and government agencies, and creditors. It allows us to make the right and appropriate

choices to improve the company's financial role (Klimczak, 2020).

Question 2

a) Opening statement of financial position

Assets

Non current assets

Tangible assets £ 150,000

Current assets

cash at bank £ 50,000

Total assets £ 200,000

liabilities

Capital £ 200,000

company holds inventory before selling. Indicates the number of days it takes for inventory to

rotate within the organization.

Debt to equity ratio: If there is high leverage in this ratio, it indicates that the company has more

leverage from the capital markets in its business. Low leverage, on the other hand, indicates that

the asset is being used optimally and is less leveraged outside the market. For this particular

question, 0.058 means less borrowed capital and less risk on hand (Brunstein and Perera, 2019).

b) The importance of considering the audience for financial statement analysis

This is the financial statement for the fiscal year, divided into expenses and income.

Provide opportunities for internal and external stakeholders to make informed decisions related

to investments. It also gives lenders an unbiased view of a company's financial health. This helps

with loan selection. This assessment reviews the trading company's financial statements to gain

insight into its financial functioning. These statements consist of profit statements, stability

sheets, and coin flows. Evaluation of the internal workings is done by workers, authorities,

managers, etc. using accounting information from the trading company. External ratings, on the

other hand, are done by outsiders who have access to the posted account. This includes investors,

credit and government agencies, and creditors. It allows us to make the right and appropriate

choices to improve the company's financial role (Klimczak, 2020).

Question 2

a) Opening statement of financial position

Assets

Non current assets

Tangible assets £ 150,000

Current assets

cash at bank £ 50,000

Total assets £ 200,000

liabilities

Capital £ 200,000

Total £ 200,000

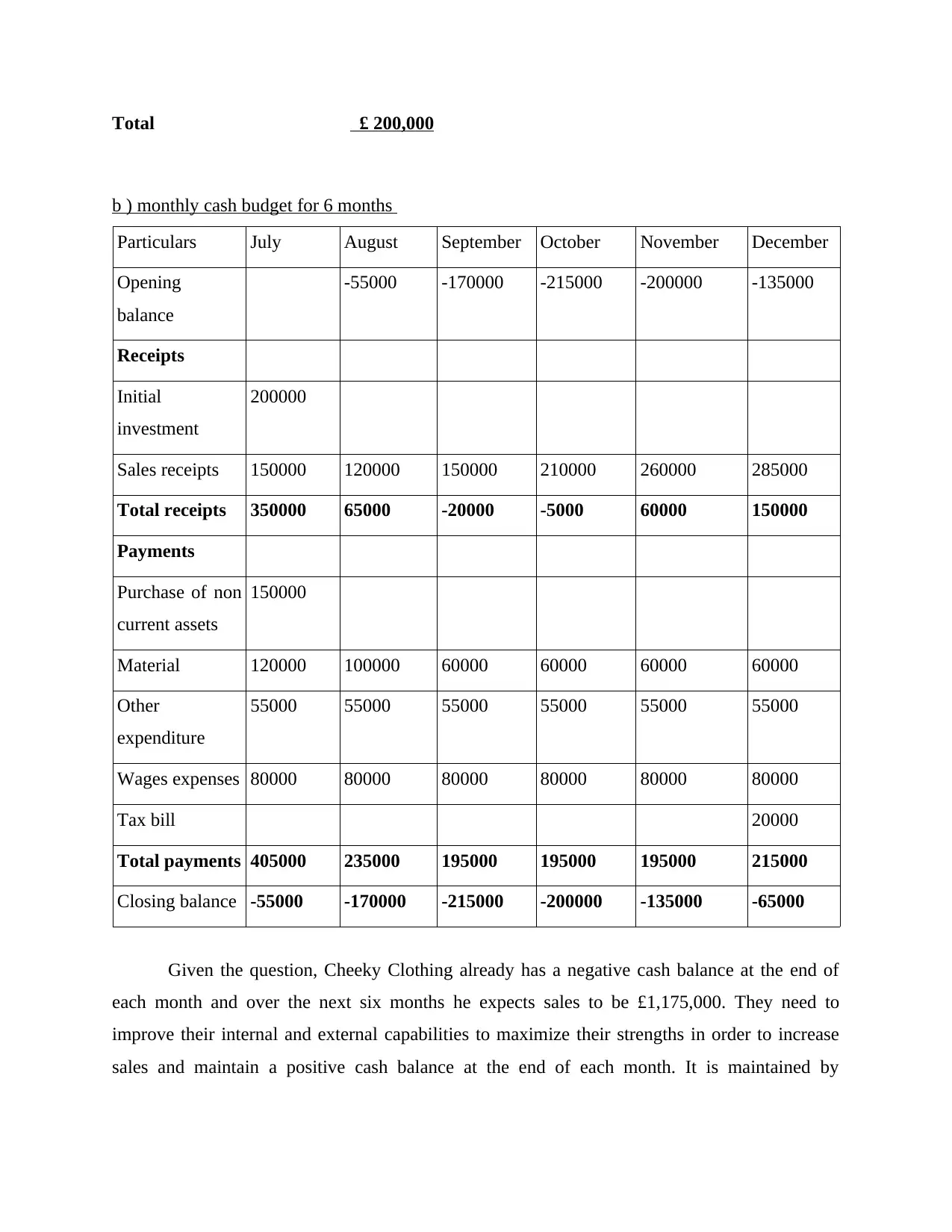

b ) monthly cash budget for 6 months

Particulars July August September October November December

Opening

balance

-55000 -170000 -215000 -200000 -135000

Receipts

Initial

investment

200000

Sales receipts 150000 120000 150000 210000 260000 285000

Total receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of non

current assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages expenses 80000 80000 80000 80000 80000 80000

Tax bill 20000

Total payments 405000 235000 195000 195000 195000 215000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

Given the question, Cheeky Clothing already has a negative cash balance at the end of

each month and over the next six months he expects sales to be £1,175,000. They need to

improve their internal and external capabilities to maximize their strengths in order to increase

sales and maintain a positive cash balance at the end of each month. It is maintained by

b ) monthly cash budget for 6 months

Particulars July August September October November December

Opening

balance

-55000 -170000 -215000 -200000 -135000

Receipts

Initial

investment

200000

Sales receipts 150000 120000 150000 210000 260000 285000

Total receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of non

current assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages expenses 80000 80000 80000 80000 80000 80000

Tax bill 20000

Total payments 405000 235000 195000 195000 195000 215000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

Given the question, Cheeky Clothing already has a negative cash balance at the end of

each month and over the next six months he expects sales to be £1,175,000. They need to

improve their internal and external capabilities to maximize their strengths in order to increase

sales and maintain a positive cash balance at the end of each month. It is maintained by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

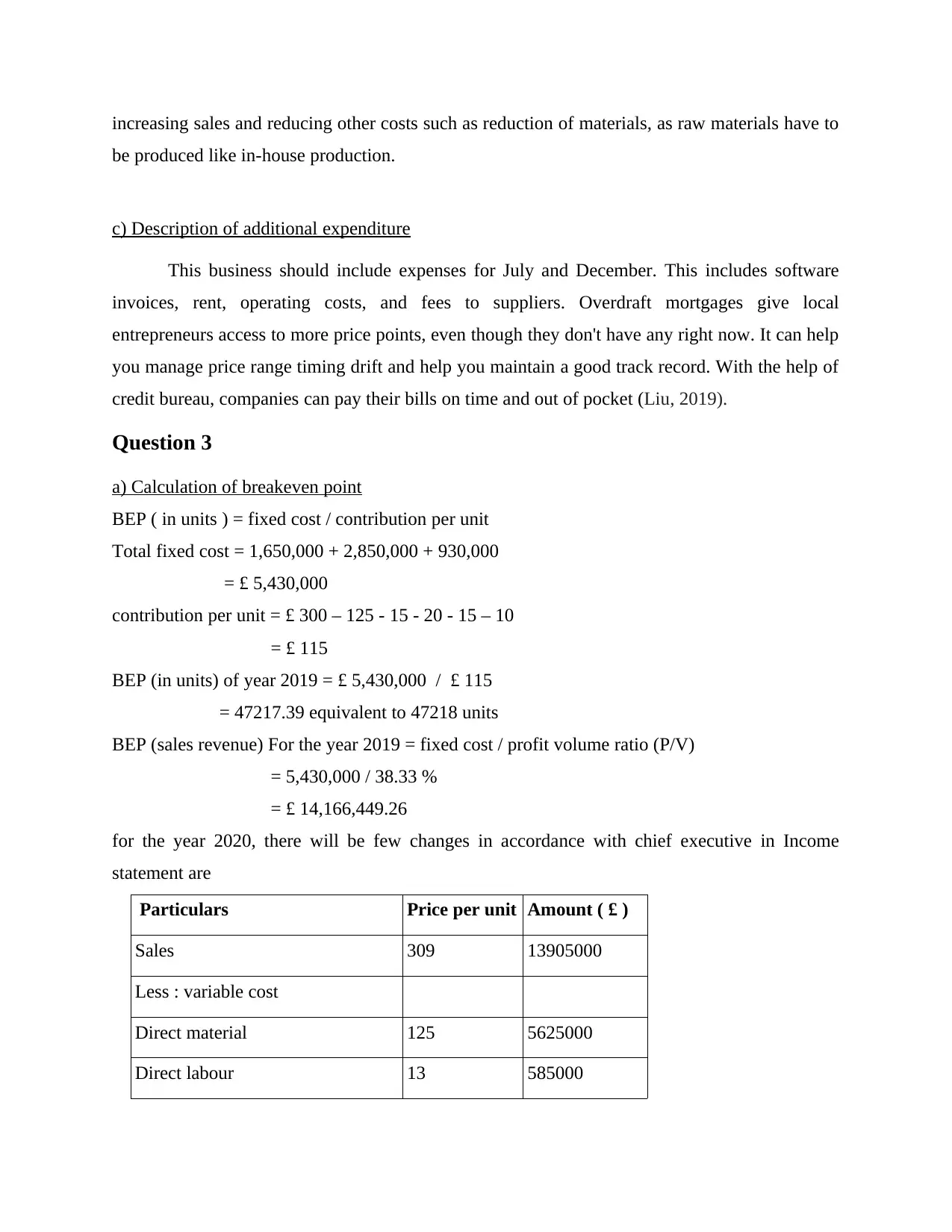

increasing sales and reducing other costs such as reduction of materials, as raw materials have to

be produced like in-house production.

c) Description of additional expenditure

This business should include expenses for July and December. This includes software

invoices, rent, operating costs, and fees to suppliers. Overdraft mortgages give local

entrepreneurs access to more price points, even though they don't have any right now. It can help

you manage price range timing drift and help you maintain a good track record. With the help of

credit bureau, companies can pay their bills on time and out of pocket (Liu, 2019).

Question 3

a) Calculation of breakeven point

BEP ( in units ) = fixed cost / contribution per unit

Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

BEP (in units) of year 2019 = £ 5,430,000 / £ 115

= 47217.39 equivalent to 47218 units

BEP (sales revenue) For the year 2019 = fixed cost / profit volume ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

for the year 2020, there will be few changes in accordance with chief executive in Income

statement are

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

be produced like in-house production.

c) Description of additional expenditure

This business should include expenses for July and December. This includes software

invoices, rent, operating costs, and fees to suppliers. Overdraft mortgages give local

entrepreneurs access to more price points, even though they don't have any right now. It can help

you manage price range timing drift and help you maintain a good track record. With the help of

credit bureau, companies can pay their bills on time and out of pocket (Liu, 2019).

Question 3

a) Calculation of breakeven point

BEP ( in units ) = fixed cost / contribution per unit

Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

BEP (in units) of year 2019 = £ 5,430,000 / £ 115

= 47217.39 equivalent to 47218 units

BEP (sales revenue) For the year 2019 = fixed cost / profit volume ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

for the year 2020, there will be few changes in accordance with chief executive in Income

statement are

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

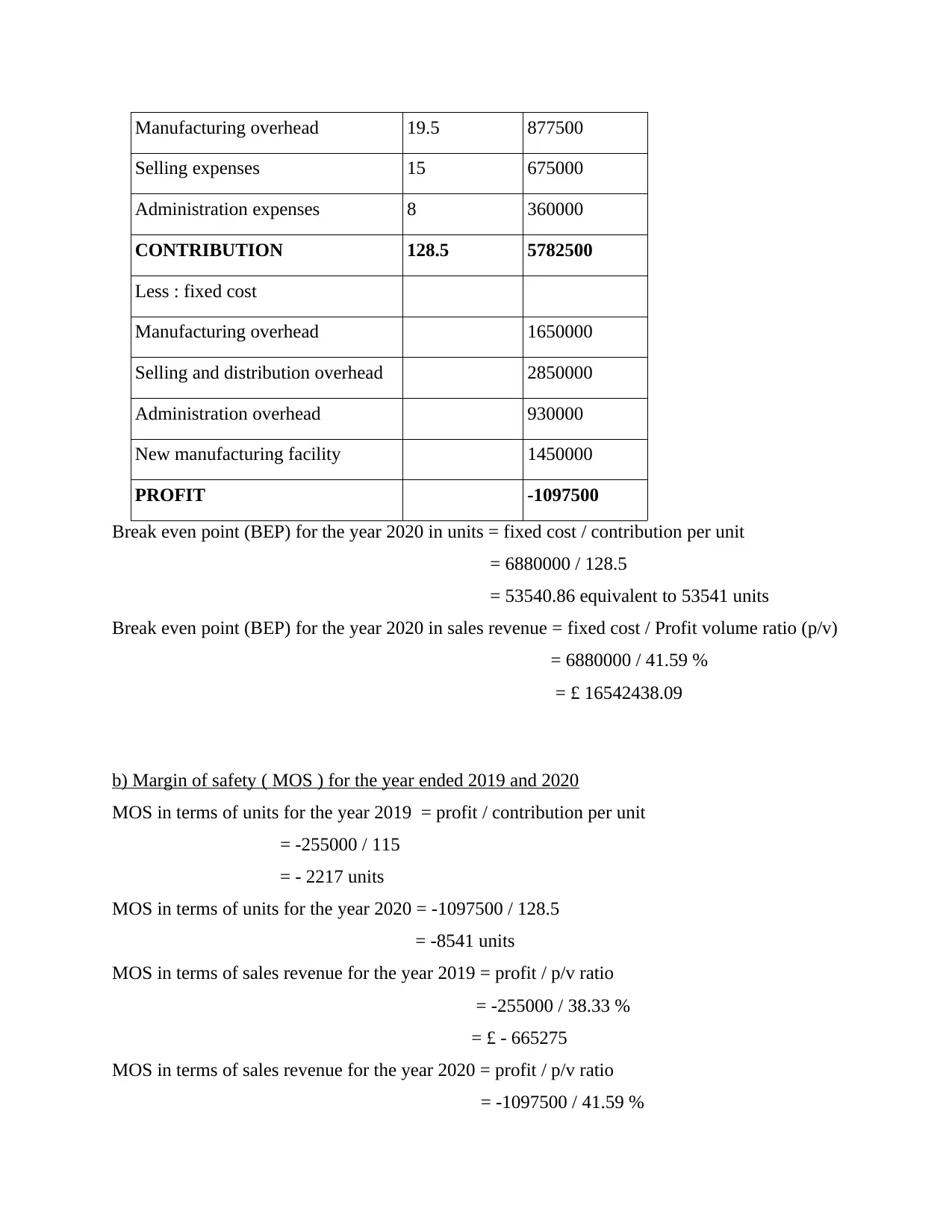

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break even point (BEP) for the year 2020 in units = fixed cost / contribution per unit

= 6880000 / 128.5

= 53540.86 equivalent to 53541 units

Break even point (BEP) for the year 2020 in sales revenue = fixed cost / Profit volume ratio (p/v)

= 6880000 / 41.59 %

= £ 16542438.09

b) Margin of safety ( MOS ) for the year ended 2019 and 2020

MOS in terms of units for the year 2019 = profit / contribution per unit

= -255000 / 115

= - 2217 units

MOS in terms of units for the year 2020 = -1097500 / 128.5

= -8541 units

MOS in terms of sales revenue for the year 2019 = profit / p/v ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of sales revenue for the year 2020 = profit / p/v ratio

= -1097500 / 41.59 %

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break even point (BEP) for the year 2020 in units = fixed cost / contribution per unit

= 6880000 / 128.5

= 53540.86 equivalent to 53541 units

Break even point (BEP) for the year 2020 in sales revenue = fixed cost / Profit volume ratio (p/v)

= 6880000 / 41.59 %

= £ 16542438.09

b) Margin of safety ( MOS ) for the year ended 2019 and 2020

MOS in terms of units for the year 2019 = profit / contribution per unit

= -255000 / 115

= - 2217 units

MOS in terms of units for the year 2020 = -1097500 / 128.5

= -8541 units

MOS in terms of sales revenue for the year 2019 = profit / p/v ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of sales revenue for the year 2020 = profit / p/v ratio

= -1097500 / 41.59 %

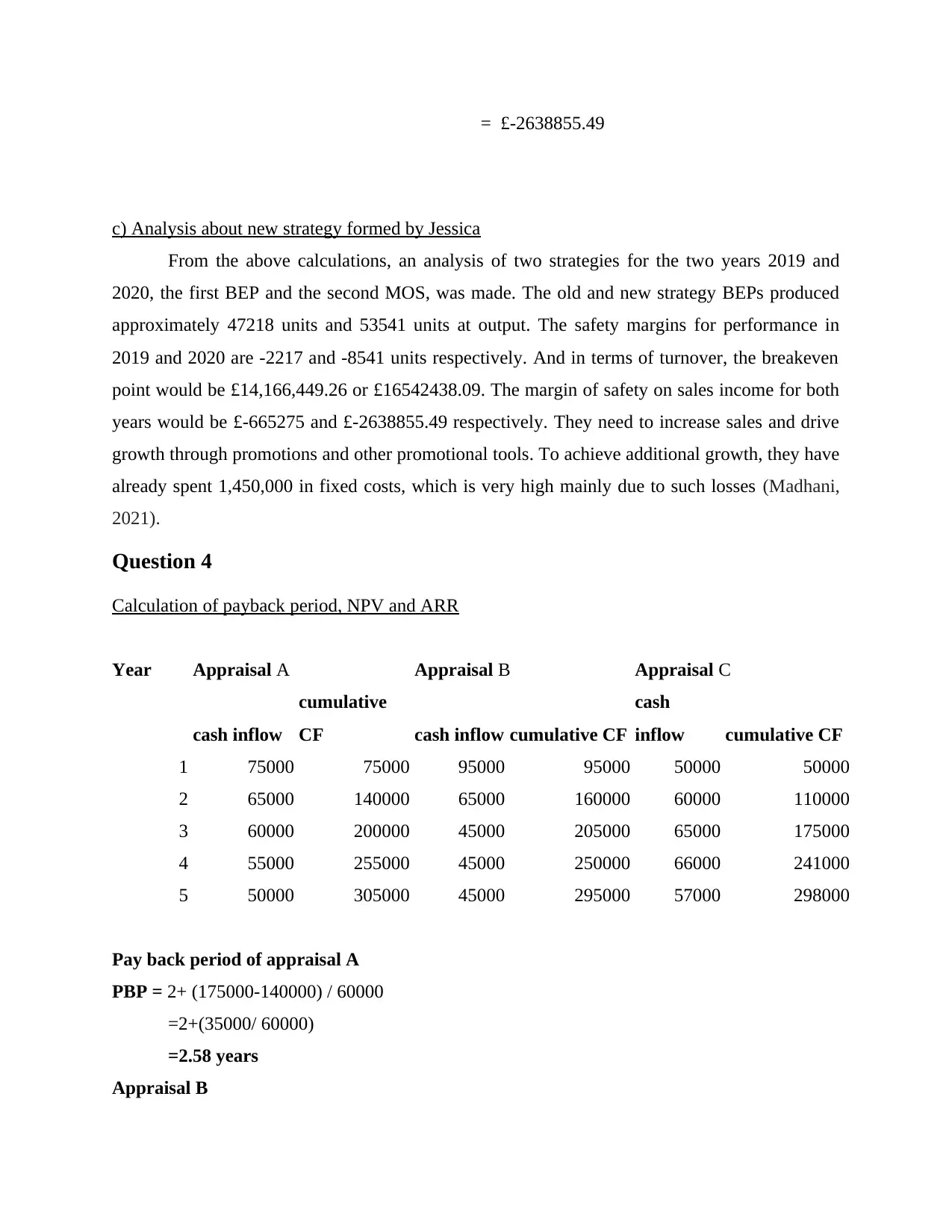

= £-2638855.49

c) Analysis about new strategy formed by Jessica

From the above calculations, an analysis of two strategies for the two years 2019 and

2020, the first BEP and the second MOS, was made. The old and new strategy BEPs produced

approximately 47218 units and 53541 units at output. The safety margins for performance in

2019 and 2020 are -2217 and -8541 units respectively. And in terms of turnover, the breakeven

point would be £14,166,449.26 or £16542438.09. The margin of safety on sales income for both

years would be £-665275 and £-2638855.49 respectively. They need to increase sales and drive

growth through promotions and other promotional tools. To achieve additional growth, they have

already spent 1,450,000 in fixed costs, which is very high mainly due to such losses (Madhani,

2021).

Question 4

Calculation of payback period, NPV and ARR

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF

cash

inflow cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay back period of appraisal A

PBP = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

c) Analysis about new strategy formed by Jessica

From the above calculations, an analysis of two strategies for the two years 2019 and

2020, the first BEP and the second MOS, was made. The old and new strategy BEPs produced

approximately 47218 units and 53541 units at output. The safety margins for performance in

2019 and 2020 are -2217 and -8541 units respectively. And in terms of turnover, the breakeven

point would be £14,166,449.26 or £16542438.09. The margin of safety on sales income for both

years would be £-665275 and £-2638855.49 respectively. They need to increase sales and drive

growth through promotions and other promotional tools. To achieve additional growth, they have

already spent 1,450,000 in fixed costs, which is very high mainly due to such losses (Madhani,

2021).

Question 4

Calculation of payback period, NPV and ARR

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF

cash

inflow cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay back period of appraisal A

PBP = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

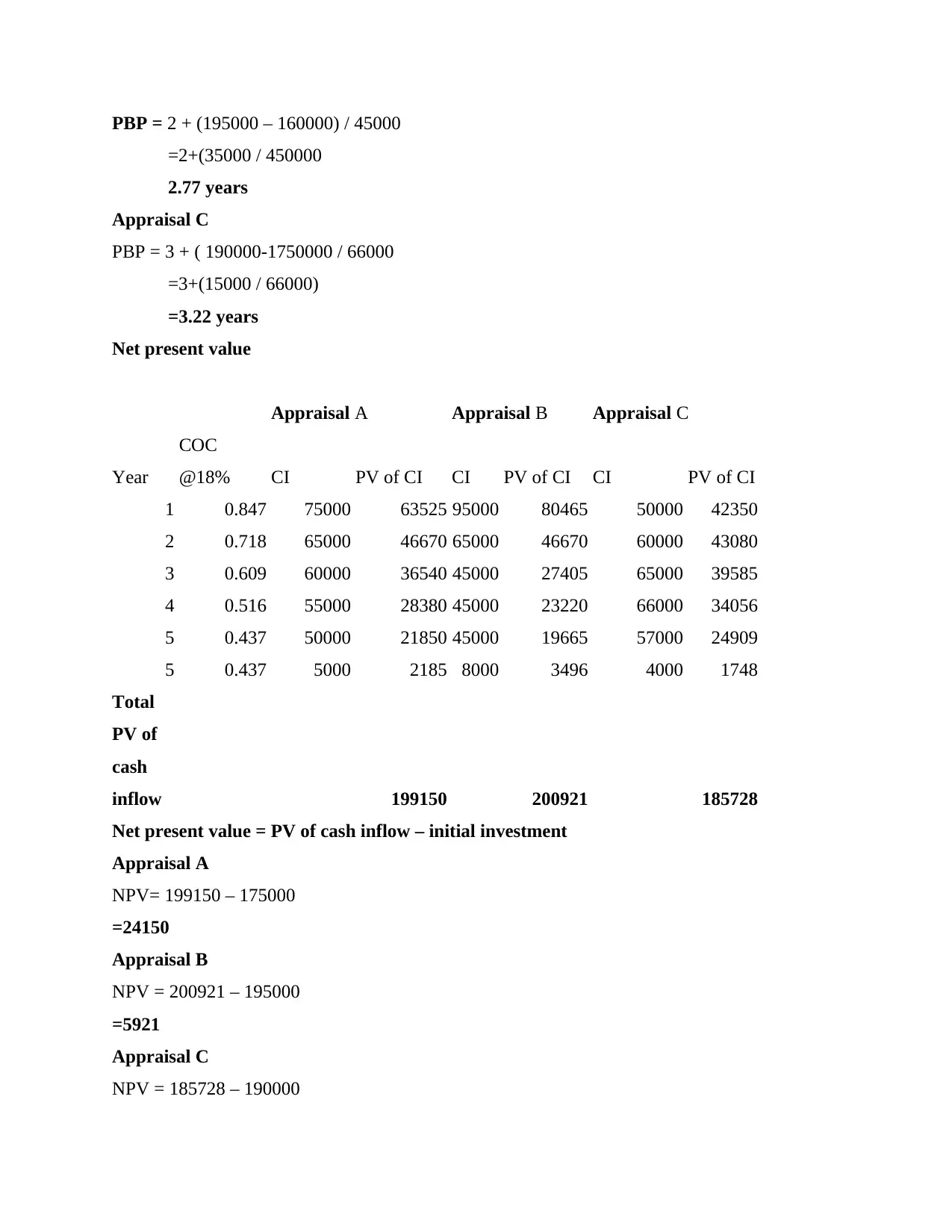

PBP = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

2.77 years

Appraisal C

PBP = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

Net present value = PV of cash inflow – initial investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=2+(35000 / 450000

2.77 years

Appraisal C

PBP = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

Net present value = PV of cash inflow – initial investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

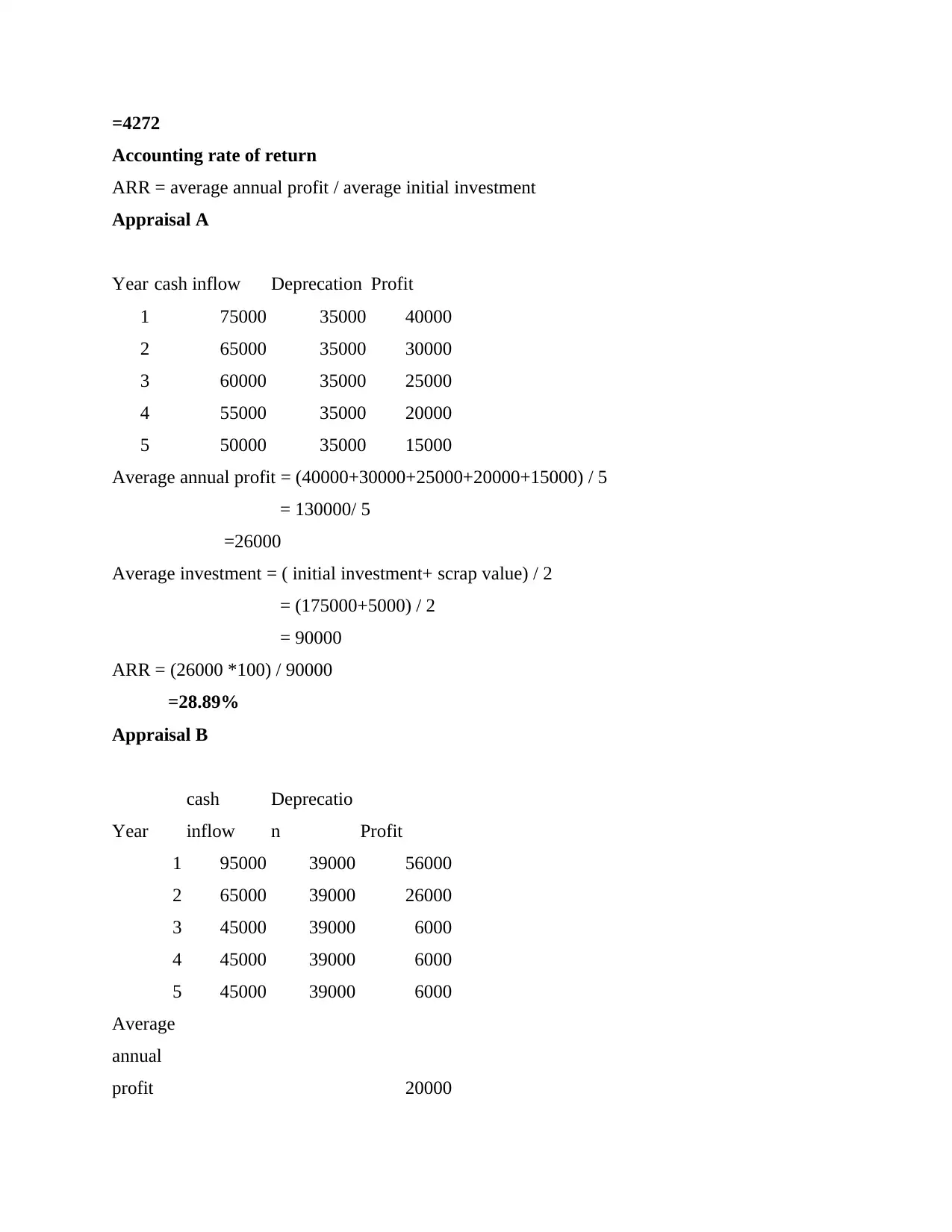

=4272

Accounting rate of return

ARR = average annual profit / average initial investment

Appraisal A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

=26000

Average investment = ( initial investment+ scrap value) / 2

= (175000+5000) / 2

= 90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

Year

cash

inflow

Deprecatio

n Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average

annual

profit 20000

Accounting rate of return

ARR = average annual profit / average initial investment

Appraisal A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

=26000

Average investment = ( initial investment+ scrap value) / 2

= (175000+5000) / 2

= 90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

Year

cash

inflow

Deprecatio

n Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average

annual

profit 20000

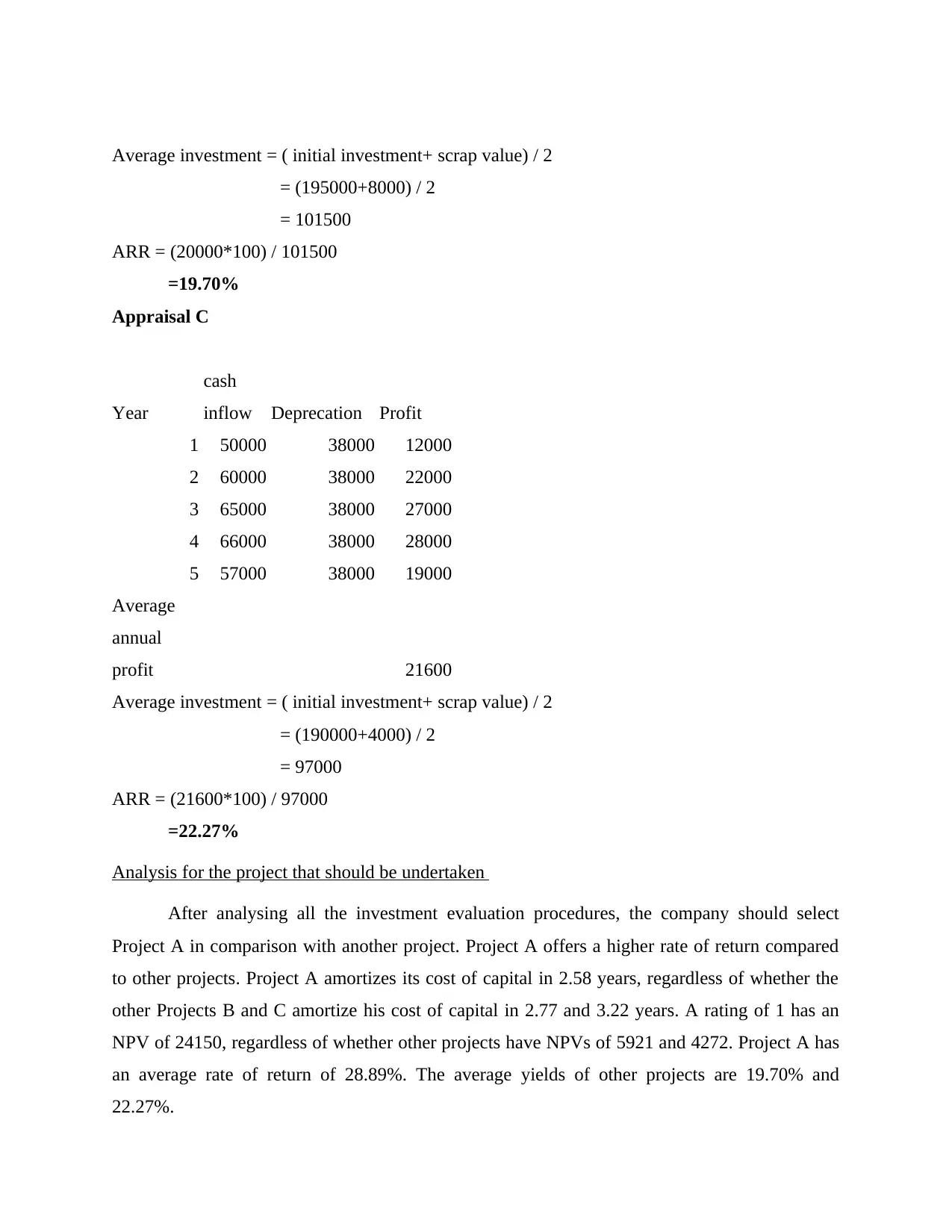

Average investment = ( initial investment+ scrap value) / 2

= (195000+8000) / 2

= 101500

ARR = (20000*100) / 101500

=19.70%

Appraisal C

Year

cash

inflow Deprecation Profit

1 50000 38000 12000

2 60000 38000 22000

3 65000 38000 27000

4 66000 38000 28000

5 57000 38000 19000

Average

annual

profit 21600

Average investment = ( initial investment+ scrap value) / 2

= (190000+4000) / 2

= 97000

ARR = (21600*100) / 97000

=22.27%

Analysis for the project that should be undertaken

After analysing all the investment evaluation procedures, the company should select

Project A in comparison with another project. Project A offers a higher rate of return compared

to other projects. Project A amortizes its cost of capital in 2.58 years, regardless of whether the

other Projects B and C amortize his cost of capital in 2.77 and 3.22 years. A rating of 1 has an

NPV of 24150, regardless of whether other projects have NPVs of 5921 and 4272. Project A has

an average rate of return of 28.89%. The average yields of other projects are 19.70% and

22.27%.

= (195000+8000) / 2

= 101500

ARR = (20000*100) / 101500

=19.70%

Appraisal C

Year

cash

inflow Deprecation Profit

1 50000 38000 12000

2 60000 38000 22000

3 65000 38000 27000

4 66000 38000 28000

5 57000 38000 19000

Average

annual

profit 21600

Average investment = ( initial investment+ scrap value) / 2

= (190000+4000) / 2

= 97000

ARR = (21600*100) / 97000

=22.27%

Analysis for the project that should be undertaken

After analysing all the investment evaluation procedures, the company should select

Project A in comparison with another project. Project A offers a higher rate of return compared

to other projects. Project A amortizes its cost of capital in 2.58 years, regardless of whether the

other Projects B and C amortize his cost of capital in 2.77 and 3.22 years. A rating of 1 has an

NPV of 24150, regardless of whether other projects have NPVs of 5921 and 4272. Project A has

an average rate of return of 28.89%. The average yields of other projects are 19.70% and

22.27%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.