Financial Analysis of Liverton Co.: Ratios, Budgeting, and Investment

VerifiedAdded on 2023/06/04

|16

|3888

|289

Homework Assignment

AI Summary

This finance assignment delves into key aspects of financial analysis, commencing with an introduction to financial statements and their significance. The assignment presents detailed calculations and interpretations of various financial ratios, including gross profit margin, asset usage ratio, current ratio, acid-test ratio, inventory holding period, and debt-equity ratio for Liverton Co. The analysis extends to the preparation of an opening statement of financial position and a monthly cash budget, along with an exploration of break-even points and margins of safety. Furthermore, the assignment encompasses the calculation and comparison of project investment appraisals using the payback period, accounting rate of return, and NPV analysis to aid in project selection. The student also explains the importance of financial statement analysis for making informed decisions regarding investment, assessing the future growth of the firm, and providing meaningful information to shareholders.

Introduction

to

Finance

to

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The dictionary meaning of the term finance has broad aspect which states that something

which deals in monetary terms. In relation to the business, the meaning of finance is the financial

structure of the company such as, debt employed, equity capital employed. In this file, there have

been shown an adequate discussion about the financial statement ratios like gross profit ratio,

assets usage ratio, current ratio, acid test ratio, inventories holding period and debt-equity ratio

and explanation of financial statement analysis (Alshater, Atayah and Hamdan, 2021). There has

also been shown an opening statement of financial position and and cash budget of the

companies and a brief glimpse of the break-even point and margin of safety (Beaumont, 2019).

And lastly there is also shown the calculation of payback period, accounting rate of return and

NPV analysis of the projects and the selection of the projects.

TASK

Question 1 :

(a) Calculations of ratios for the year 2019 and 2018 :

(I) Gross Profit Margin = Gross Profit / Sales * 100

= £1313 / £3495 * 100

= 37.57 %

Interpretation :

Gross profit margin is a profitability ratio based on sales, it represents the relationship

between the gross profit earned and sales made during the year (Ge, Cai and Song, 2022). A high

gross profit margin is a favourable sign of effective management, in the above scenario, Liverton

Co. is earning gross profit at the rate of 37.57 % of the sales, which is quite good.

(II) Assets Usage Ratio = Total Sales / Average Total Assets

= £3495 / £3157.5

= 1.10 times

Interpretation :

Assets usage ratio refers to the relationship between the total sales of the year and

average total assets. This ratio is categorized under efficiency ratio, it measures the efficiency

The dictionary meaning of the term finance has broad aspect which states that something

which deals in monetary terms. In relation to the business, the meaning of finance is the financial

structure of the company such as, debt employed, equity capital employed. In this file, there have

been shown an adequate discussion about the financial statement ratios like gross profit ratio,

assets usage ratio, current ratio, acid test ratio, inventories holding period and debt-equity ratio

and explanation of financial statement analysis (Alshater, Atayah and Hamdan, 2021). There has

also been shown an opening statement of financial position and and cash budget of the

companies and a brief glimpse of the break-even point and margin of safety (Beaumont, 2019).

And lastly there is also shown the calculation of payback period, accounting rate of return and

NPV analysis of the projects and the selection of the projects.

TASK

Question 1 :

(a) Calculations of ratios for the year 2019 and 2018 :

(I) Gross Profit Margin = Gross Profit / Sales * 100

= £1313 / £3495 * 100

= 37.57 %

Interpretation :

Gross profit margin is a profitability ratio based on sales, it represents the relationship

between the gross profit earned and sales made during the year (Ge, Cai and Song, 2022). A high

gross profit margin is a favourable sign of effective management, in the above scenario, Liverton

Co. is earning gross profit at the rate of 37.57 % of the sales, which is quite good.

(II) Assets Usage Ratio = Total Sales / Average Total Assets

= £3495 / £3157.5

= 1.10 times

Interpretation :

Assets usage ratio refers to the relationship between the total sales of the year and

average total assets. This ratio is categorized under efficiency ratio, it measures the efficiency

with which the firm uses its assets. High asset usage ratio depicts the efficient utilisation of the

assets in generating the sales, likewise a lower assets usage ratio indicates that the assets are not

efficiently utilised to generate sales. In the present case, Liverton Co. is making sales by 1.10

times through utilization of its assets .

(III) Current Ratio = Current Assets / Current Liabilities

For year 2019 = £1687 / £744

= 2.267 times

For year 2018 = £418 / £502

= 0.8327 times

Interpretation :

Current ratio is a measure of short term solvency, it shows the relationship between the

current assets and current liabilities. An ideal current ratio is 2:1, however, ratio's satisfactory

depends upon the nature of the business (Hattori and Ishida, 2021). In the year 2018, the current

ratio of liverton co. was 0.8327 times but it has increased to 2.267 times in the year 2019. The

increment is because of the drastic change in short term investment, trade receivables and cash at

bank. The company has made short term investment of £75,000 and trade receivables has also

increased by £695,000 and cash at bank has also been increased by £451,000.

(IV) Acid Test ratio = Current Assets - inventory / Current liabilities

For year 2019 = £1687 – £150 / £744

= 2.066 times

For year 2018 = £418 – £102 / £502

= 0.63 times

Interpretation :

Acid test ratio also known as liquid ratio, it shows the measurement of short term

liquidity of the company (Ji and et.al. 2019). It depicts the relationship between liquid assets and

liquid or current liabilities, an ideal acid-test ratio is 1:1. Liquid assets does not include the

inventory hence the value of inventory is deducted from the current assets. In the present

scenario, the company's acid test ratio was 0.63 times in the year 2018 but in the year 2019 it has

assets in generating the sales, likewise a lower assets usage ratio indicates that the assets are not

efficiently utilised to generate sales. In the present case, Liverton Co. is making sales by 1.10

times through utilization of its assets .

(III) Current Ratio = Current Assets / Current Liabilities

For year 2019 = £1687 / £744

= 2.267 times

For year 2018 = £418 / £502

= 0.8327 times

Interpretation :

Current ratio is a measure of short term solvency, it shows the relationship between the

current assets and current liabilities. An ideal current ratio is 2:1, however, ratio's satisfactory

depends upon the nature of the business (Hattori and Ishida, 2021). In the year 2018, the current

ratio of liverton co. was 0.8327 times but it has increased to 2.267 times in the year 2019. The

increment is because of the drastic change in short term investment, trade receivables and cash at

bank. The company has made short term investment of £75,000 and trade receivables has also

increased by £695,000 and cash at bank has also been increased by £451,000.

(IV) Acid Test ratio = Current Assets - inventory / Current liabilities

For year 2019 = £1687 – £150 / £744

= 2.066 times

For year 2018 = £418 – £102 / £502

= 0.63 times

Interpretation :

Acid test ratio also known as liquid ratio, it shows the measurement of short term

liquidity of the company (Ji and et.al. 2019). It depicts the relationship between liquid assets and

liquid or current liabilities, an ideal acid-test ratio is 1:1. Liquid assets does not include the

inventory hence the value of inventory is deducted from the current assets. In the present

scenario, the company's acid test ratio was 0.63 times in the year 2018 but in the year 2019 it has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

increased to 2.066 times. The base for the increment is major change in trade receivables and

cash at bank and introduction of short term investment.

(V) Inventories = Average Inventory / Cost of goods sold * 365

Holding Period

= (102 + 150 / 2) / 2182 * 365

= 21.08 days

Interpretation :

Inventories holding period presents the number of days for which the company holds the

finished goods stock for making sales, higher the ratio the better it will be. In the above case, the

company holds its inventories for approximately 21 days for making sales, it can be considered

as good period as will help the company to make or purchase the goods, in the lead time for

selling them to the customers.

(VI) Debt-Equity Ratio = Long term debt / Total equity

For year 2019 = 170 / 2898

= .059 times

For year 2018 = 50 / 1951

= .026 times

Interpretation :

Debt-Equity ratio is a measurement of the long term solvency of the organisations, the

higher debt- equity ratio depicts the less protection to the creditors and vice versa (Kong and

Gallagher, 2021). This ratio indicates the relationship of long term debt fund or outside liabilities

with the total equity of the company, it is also an indicator of the financial leverage of the

company. In the present case, the debt equity ratio for the year 2018 was .026 times and for the

year there has been noticed an increment in the ratio of .059 times. Although the company has

noticed the increment, yet it would not have any major impact on the liverton co.'s operations.

cash at bank and introduction of short term investment.

(V) Inventories = Average Inventory / Cost of goods sold * 365

Holding Period

= (102 + 150 / 2) / 2182 * 365

= 21.08 days

Interpretation :

Inventories holding period presents the number of days for which the company holds the

finished goods stock for making sales, higher the ratio the better it will be. In the above case, the

company holds its inventories for approximately 21 days for making sales, it can be considered

as good period as will help the company to make or purchase the goods, in the lead time for

selling them to the customers.

(VI) Debt-Equity Ratio = Long term debt / Total equity

For year 2019 = 170 / 2898

= .059 times

For year 2018 = 50 / 1951

= .026 times

Interpretation :

Debt-Equity ratio is a measurement of the long term solvency of the organisations, the

higher debt- equity ratio depicts the less protection to the creditors and vice versa (Kong and

Gallagher, 2021). This ratio indicates the relationship of long term debt fund or outside liabilities

with the total equity of the company, it is also an indicator of the financial leverage of the

company. In the present case, the debt equity ratio for the year 2018 was .026 times and for the

year there has been noticed an increment in the ratio of .059 times. Although the company has

noticed the increment, yet it would not have any major impact on the liverton co.'s operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Explanation of importance of financial statement analysis :

Financial statement analysis is an identification and analysis of the financial statements of

the company. Financial statement is a structured representation of the historical financial

information of the company, it includes balance sheet, profit and loss account and cash flow

statements. Financial statements analysis is mandatory for the sound decision making regarding

investment, it also helps in assessment of the future growth of the firm. Analysing the financial

statements shows presents the liquidity, efficiency, solvency and profitability of the business.

Financial statement analysis is useful in providing the meaningful information to the

shareholders for making decisions regarding holding the shares of the company (Liermann, Li and

Schaudinnus, 2019). In short, financial statement analysis is the process of evaluation of the

financial condition of the business.

Question 2 :

(a) Opening statement of financial position at the start of July 20X5 :

Particulars Amount in “£”

Equity And Liabilities

Equity Share Capital 200000

Total 200000

Assets :

Non-Current Assets :

Tangible Non Current Assets 150000

Current Assets :

Cash At Bank 50000

Total Assets 200000

Financial statement analysis is an identification and analysis of the financial statements of

the company. Financial statement is a structured representation of the historical financial

information of the company, it includes balance sheet, profit and loss account and cash flow

statements. Financial statements analysis is mandatory for the sound decision making regarding

investment, it also helps in assessment of the future growth of the firm. Analysing the financial

statements shows presents the liquidity, efficiency, solvency and profitability of the business.

Financial statement analysis is useful in providing the meaningful information to the

shareholders for making decisions regarding holding the shares of the company (Liermann, Li and

Schaudinnus, 2019). In short, financial statement analysis is the process of evaluation of the

financial condition of the business.

Question 2 :

(a) Opening statement of financial position at the start of July 20X5 :

Particulars Amount in “£”

Equity And Liabilities

Equity Share Capital 200000

Total 200000

Assets :

Non-Current Assets :

Tangible Non Current Assets 150000

Current Assets :

Cash At Bank 50000

Total Assets 200000

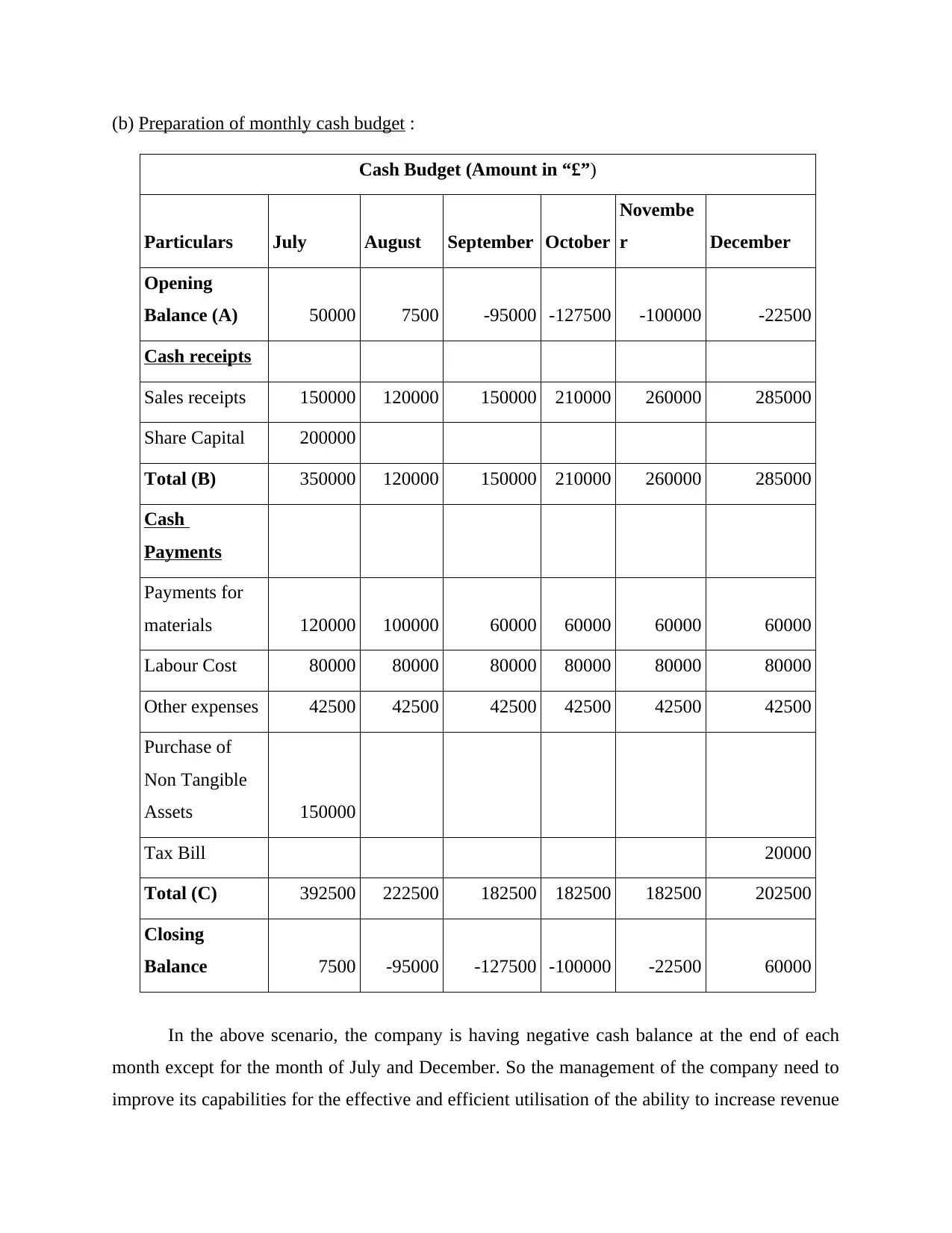

(b) Preparation of monthly cash budget :

Cash Budget (Amount in “£”)

Particulars July August September October

Novembe

r December

Opening

Balance (A) 50000 7500 -95000 -127500 -100000 -22500

Cash receipts

Sales receipts 150000 120000 150000 210000 260000 285000

Share Capital 200000

Total (B) 350000 120000 150000 210000 260000 285000

Cash

Payments

Payments for

materials 120000 100000 60000 60000 60000 60000

Labour Cost 80000 80000 80000 80000 80000 80000

Other expenses 42500 42500 42500 42500 42500 42500

Purchase of

Non Tangible

Assets 150000

Tax Bill 20000

Total (C) 392500 222500 182500 182500 182500 202500

Closing

Balance 7500 -95000 -127500 -100000 -22500 60000

In the above scenario, the company is having negative cash balance at the end of each

month except for the month of July and December. So the management of the company need to

improve its capabilities for the effective and efficient utilisation of the ability to increase revenue

Cash Budget (Amount in “£”)

Particulars July August September October

Novembe

r December

Opening

Balance (A) 50000 7500 -95000 -127500 -100000 -22500

Cash receipts

Sales receipts 150000 120000 150000 210000 260000 285000

Share Capital 200000

Total (B) 350000 120000 150000 210000 260000 285000

Cash

Payments

Payments for

materials 120000 100000 60000 60000 60000 60000

Labour Cost 80000 80000 80000 80000 80000 80000

Other expenses 42500 42500 42500 42500 42500 42500

Purchase of

Non Tangible

Assets 150000

Tax Bill 20000

Total (C) 392500 222500 182500 182500 182500 202500

Closing

Balance 7500 -95000 -127500 -100000 -22500 60000

In the above scenario, the company is having negative cash balance at the end of each

month except for the month of July and December. So the management of the company need to

improve its capabilities for the effective and efficient utilisation of the ability to increase revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to maintain positive cash balances at the end of each month (Piccio and Van Biezen, 2018). It can be

maintained by increasing sales and lowering the expenses related to sales, such as reduction in

raw material purchasing cost, labour cost and other expenses as well.

(c) Explanation of additional expenses which should be taken into consideration :

The overdraft facility is provided to the companies over and above the amount

maintained in the bank account of the company and it allows the company to pay their pending

bills and other liabilities (Ross and Wright, 2022). To avail the facility of overdraft, the company

needs to pay the fee and have to incur other expenditures such as, bank charges, maintenance fee

etc. With the help of overdraft, the organisation is capable of paying the bills and other costs on

time.

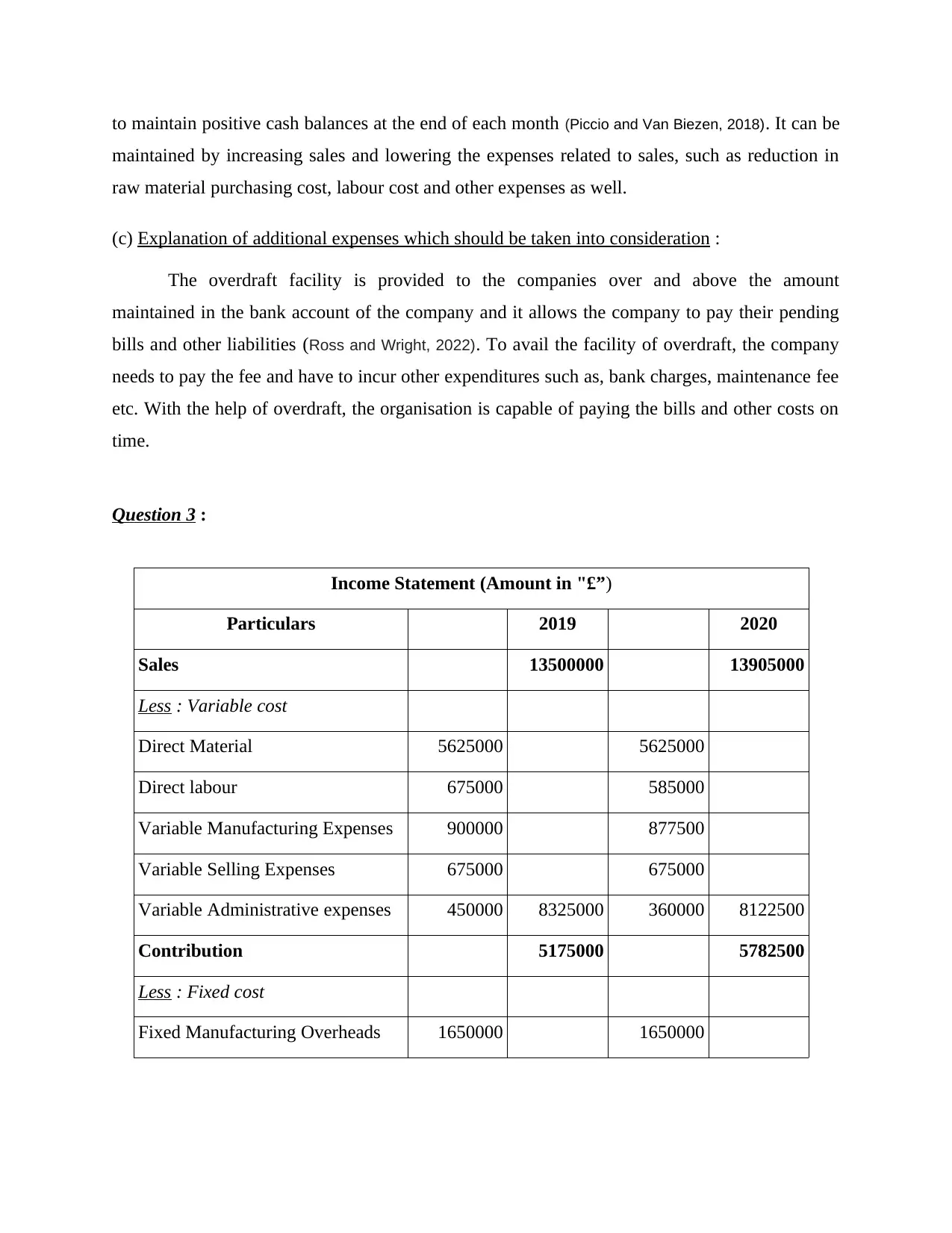

Question 3 :

Income Statement (Amount in "£”)

Particulars 2019 2020

Sales 13500000 13905000

Less : Variable cost

Direct Material 5625000 5625000

Direct labour 675000 585000

Variable Manufacturing Expenses 900000 877500

Variable Selling Expenses 675000 675000

Variable Administrative expenses 450000 8325000 360000 8122500

Contribution 5175000 5782500

Less : Fixed cost

Fixed Manufacturing Overheads 1650000 1650000

maintained by increasing sales and lowering the expenses related to sales, such as reduction in

raw material purchasing cost, labour cost and other expenses as well.

(c) Explanation of additional expenses which should be taken into consideration :

The overdraft facility is provided to the companies over and above the amount

maintained in the bank account of the company and it allows the company to pay their pending

bills and other liabilities (Ross and Wright, 2022). To avail the facility of overdraft, the company

needs to pay the fee and have to incur other expenditures such as, bank charges, maintenance fee

etc. With the help of overdraft, the organisation is capable of paying the bills and other costs on

time.

Question 3 :

Income Statement (Amount in "£”)

Particulars 2019 2020

Sales 13500000 13905000

Less : Variable cost

Direct Material 5625000 5625000

Direct labour 675000 585000

Variable Manufacturing Expenses 900000 877500

Variable Selling Expenses 675000 675000

Variable Administrative expenses 450000 8325000 360000 8122500

Contribution 5175000 5782500

Less : Fixed cost

Fixed Manufacturing Overheads 1650000 1650000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed Selling and Distribution

Overheads 2850000 2850000

Fixed Administrative Overheads 930000 5430000 930000

Other Fixed Cost 1450000 6880000

Profit -255000 -1097500

Profit-Volume Ratio 38.33 41.59

(a) Calculation of the break-even point in units and sales revenue :

(I) Break-Even Point = Fixed Cost / Contribution per unit

(In units)

Year 2019 = £5,430,000 / £115

= 47,217.39 fans

Year 2020 = £6880000 / £128.5

= 53,540.86 fans

(II)Break-Even Sales = Fixed Cost / Profit – Volume Ratio

(In “£”)

Year 2019 = £5,430,000 / 38.33 %

= £14,165,229.71

Year 2020 = £6880000 / 41.59 %

= £16,542,438.09

(b) Calculation of margin of safety in units and sales revenue :

(I) Margin Of Safety = Profit / Contribution Per Unit

(In Units)

Year 2019 = £-255000 / £115

= -2217.40 fans

Year 2020 = £-1097500 / £128.5

= -8540.86 fans

(II) Margin Of Safety = Profit / Profit-Volume Ratio

Overheads 2850000 2850000

Fixed Administrative Overheads 930000 5430000 930000

Other Fixed Cost 1450000 6880000

Profit -255000 -1097500

Profit-Volume Ratio 38.33 41.59

(a) Calculation of the break-even point in units and sales revenue :

(I) Break-Even Point = Fixed Cost / Contribution per unit

(In units)

Year 2019 = £5,430,000 / £115

= 47,217.39 fans

Year 2020 = £6880000 / £128.5

= 53,540.86 fans

(II)Break-Even Sales = Fixed Cost / Profit – Volume Ratio

(In “£”)

Year 2019 = £5,430,000 / 38.33 %

= £14,165,229.71

Year 2020 = £6880000 / 41.59 %

= £16,542,438.09

(b) Calculation of margin of safety in units and sales revenue :

(I) Margin Of Safety = Profit / Contribution Per Unit

(In Units)

Year 2019 = £-255000 / £115

= -2217.40 fans

Year 2020 = £-1097500 / £128.5

= -8540.86 fans

(II) Margin Of Safety = Profit / Profit-Volume Ratio

(In “£”)

Year 2019 = £-255000 / 38.33%

= £-665,223.17

Year 2020 = £-1097500 / 41.59%

= £-2,638,855.49

(c) Discussion about the new strategy :

Break-even point refers to the point where fixed cost equals to the contribution, that

means it is no profit and no loss situation for the company, whereas margin of safety represents

the sales over and above the break even sales (Sarker, Khatun and Alam, 2019). In the current case,

taking lessons from the past, Jessica decides to lower its cost, for this the company has

established a new manufacturing unit in Leicester that has burdened the company with

£1,450,000 as fixed cost. On the basis of above calculations, it has come to notice that

contribution per unit has increased to £128.5 but due to excess fixed cost, the loss has also

increased by £842,500. Thus it can be concluded that Jessica needs opt for reactive approach to

reformulate the strategy to attain the expected results. Apart from all these, the company has

noticed decline in the direct labour cost, variable manufacturing and administrative overheads.

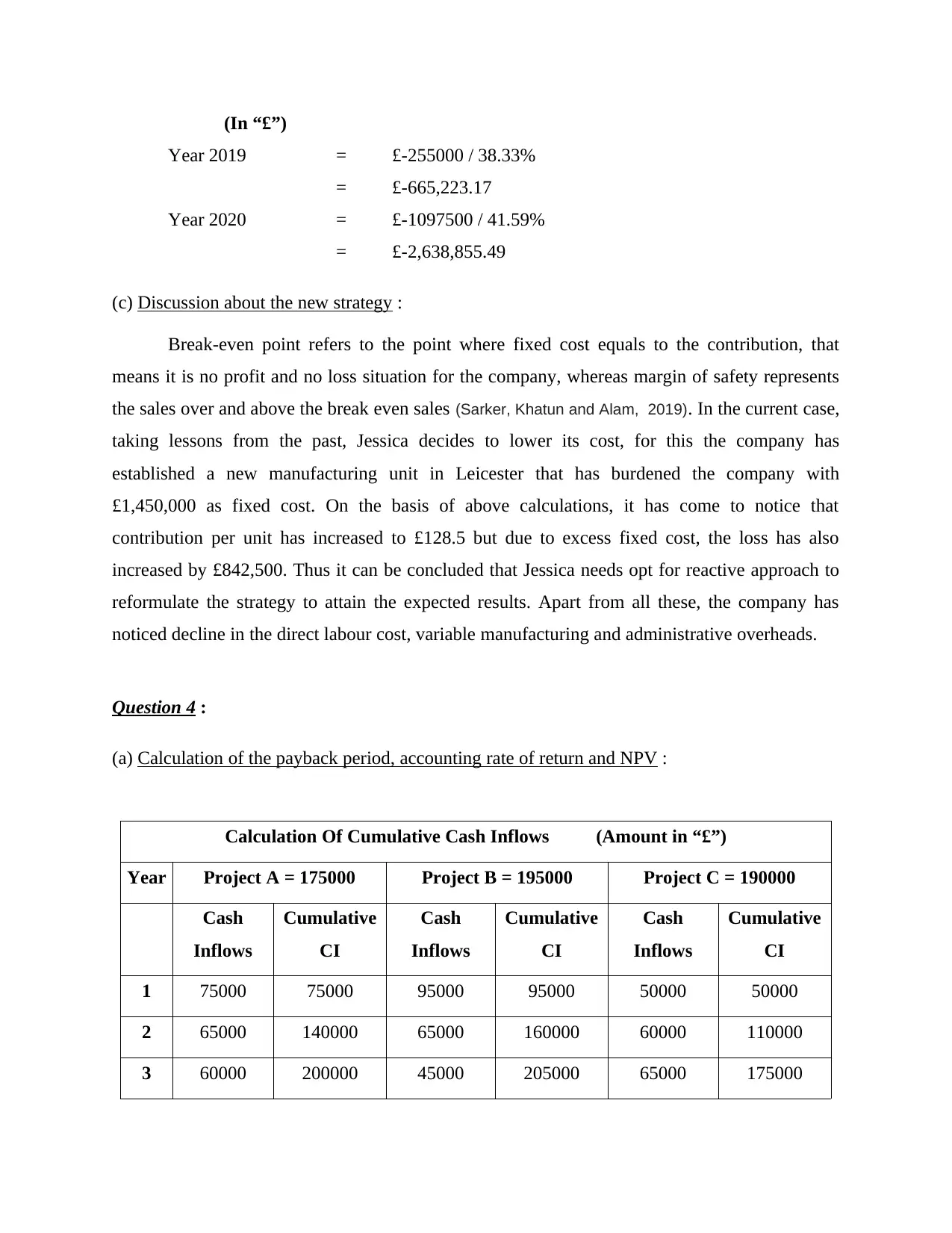

Question 4 :

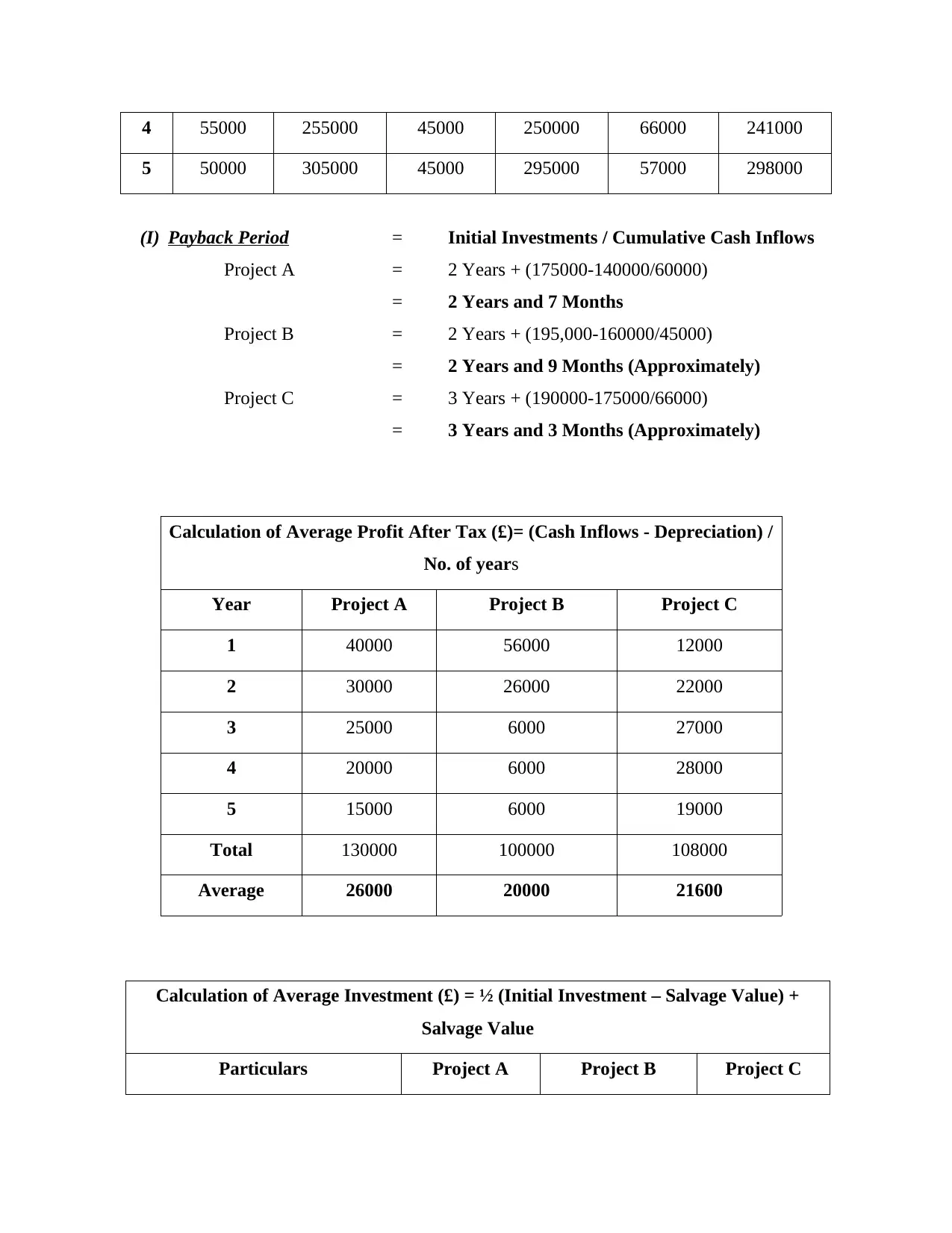

(a) Calculation of the payback period, accounting rate of return and NPV :

Calculation Of Cumulative Cash Inflows (Amount in “£”)

Year Project A = 175000 Project B = 195000 Project C = 190000

Cash

Inflows

Cumulative

CI

Cash

Inflows

Cumulative

CI

Cash

Inflows

Cumulative

CI

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

Year 2019 = £-255000 / 38.33%

= £-665,223.17

Year 2020 = £-1097500 / 41.59%

= £-2,638,855.49

(c) Discussion about the new strategy :

Break-even point refers to the point where fixed cost equals to the contribution, that

means it is no profit and no loss situation for the company, whereas margin of safety represents

the sales over and above the break even sales (Sarker, Khatun and Alam, 2019). In the current case,

taking lessons from the past, Jessica decides to lower its cost, for this the company has

established a new manufacturing unit in Leicester that has burdened the company with

£1,450,000 as fixed cost. On the basis of above calculations, it has come to notice that

contribution per unit has increased to £128.5 but due to excess fixed cost, the loss has also

increased by £842,500. Thus it can be concluded that Jessica needs opt for reactive approach to

reformulate the strategy to attain the expected results. Apart from all these, the company has

noticed decline in the direct labour cost, variable manufacturing and administrative overheads.

Question 4 :

(a) Calculation of the payback period, accounting rate of return and NPV :

Calculation Of Cumulative Cash Inflows (Amount in “£”)

Year Project A = 175000 Project B = 195000 Project C = 190000

Cash

Inflows

Cumulative

CI

Cash

Inflows

Cumulative

CI

Cash

Inflows

Cumulative

CI

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

(I) Payback Period = Initial Investments / Cumulative Cash Inflows

Project A = 2 Years + (175000-140000/60000)

= 2 Years and 7 Months

Project B = 2 Years + (195,000-160000/45000)

= 2 Years and 9 Months (Approximately)

Project C = 3 Years + (190000-175000/66000)

= 3 Years and 3 Months (Approximately)

Calculation of Average Profit After Tax (£)= (Cash Inflows - Depreciation) /

No. of years

Year Project A Project B Project C

1 40000 56000 12000

2 30000 26000 22000

3 25000 6000 27000

4 20000 6000 28000

5 15000 6000 19000

Total 130000 100000 108000

Average 26000 20000 21600

Calculation of Average Investment (£) = ½ (Initial Investment – Salvage Value) +

Salvage Value

Particulars Project A Project B Project C

5 50000 305000 45000 295000 57000 298000

(I) Payback Period = Initial Investments / Cumulative Cash Inflows

Project A = 2 Years + (175000-140000/60000)

= 2 Years and 7 Months

Project B = 2 Years + (195,000-160000/45000)

= 2 Years and 9 Months (Approximately)

Project C = 3 Years + (190000-175000/66000)

= 3 Years and 3 Months (Approximately)

Calculation of Average Profit After Tax (£)= (Cash Inflows - Depreciation) /

No. of years

Year Project A Project B Project C

1 40000 56000 12000

2 30000 26000 22000

3 25000 6000 27000

4 20000 6000 28000

5 15000 6000 19000

Total 130000 100000 108000

Average 26000 20000 21600

Calculation of Average Investment (£) = ½ (Initial Investment – Salvage Value) +

Salvage Value

Particulars Project A Project B Project C

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Initial Investment 175000 195000 190000

Salvage value 5000 8000 4000

Average Investment 90000 101500 97000

(II) Accounting Rate = Average Profit / Average * 100

Of Return After Tax Investment

Project A = £26,000 / £90,000 * 100

= 28.89 %

Project B = £20,000 / £101,500 * 100

= 19.70 %

Project C = £21,600 / £97,000 * 100

= 22.27 %

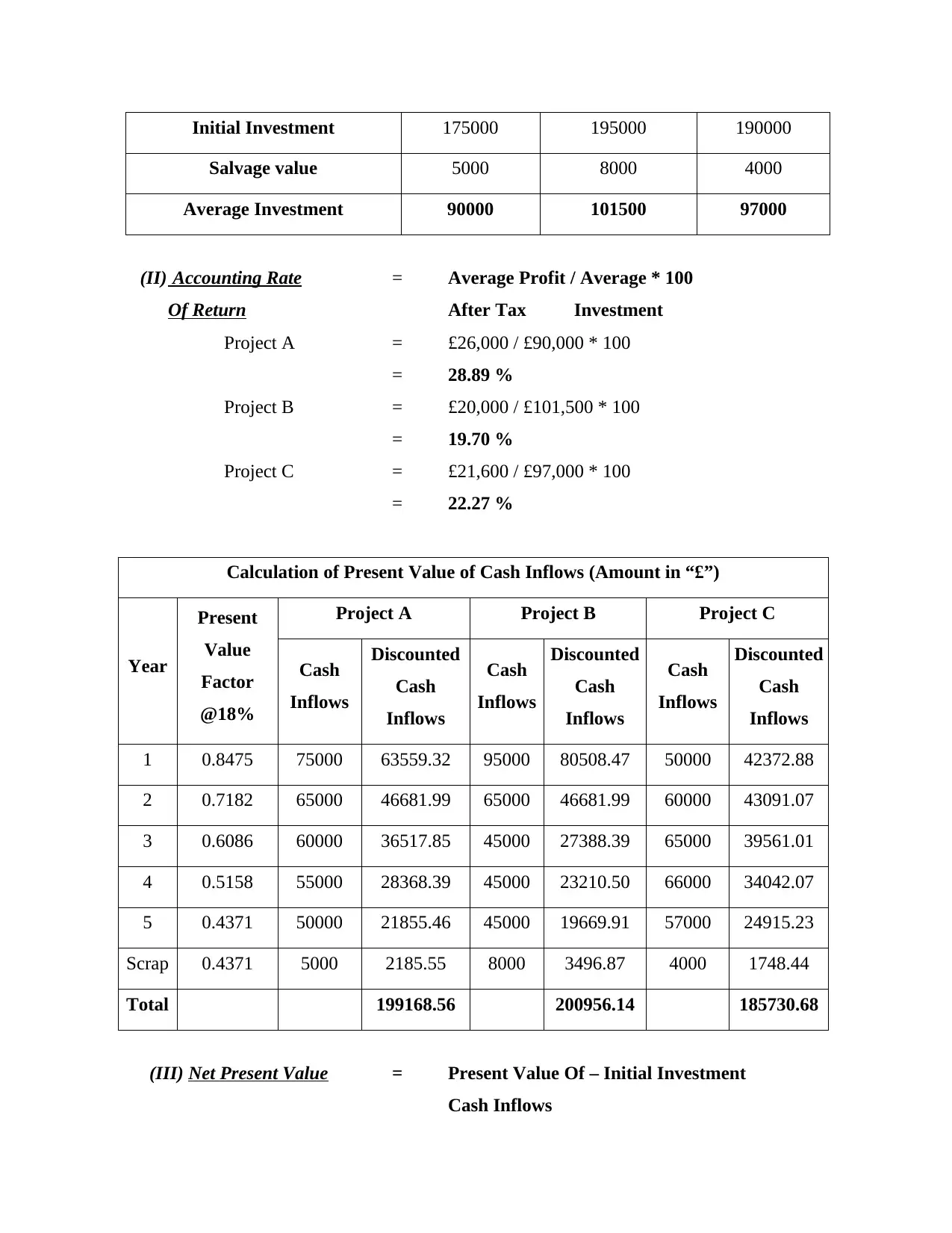

Calculation of Present Value of Cash Inflows (Amount in “£”)

Year

Present

Value

Factor

@18%

Project A Project B Project C

Cash

Inflows

Discounted

Cash

Inflows

Cash

Inflows

Discounted

Cash

Inflows

Cash

Inflows

Discounted

Cash

Inflows

1 0.8475 75000 63559.32 95000 80508.47 50000 42372.88

2 0.7182 65000 46681.99 65000 46681.99 60000 43091.07

3 0.6086 60000 36517.85 45000 27388.39 65000 39561.01

4 0.5158 55000 28368.39 45000 23210.50 66000 34042.07

5 0.4371 50000 21855.46 45000 19669.91 57000 24915.23

Scrap 0.4371 5000 2185.55 8000 3496.87 4000 1748.44

Total 199168.56 200956.14 185730.68

(III) Net Present Value = Present Value Of – Initial Investment

Cash Inflows

Salvage value 5000 8000 4000

Average Investment 90000 101500 97000

(II) Accounting Rate = Average Profit / Average * 100

Of Return After Tax Investment

Project A = £26,000 / £90,000 * 100

= 28.89 %

Project B = £20,000 / £101,500 * 100

= 19.70 %

Project C = £21,600 / £97,000 * 100

= 22.27 %

Calculation of Present Value of Cash Inflows (Amount in “£”)

Year

Present

Value

Factor

@18%

Project A Project B Project C

Cash

Inflows

Discounted

Cash

Inflows

Cash

Inflows

Discounted

Cash

Inflows

Cash

Inflows

Discounted

Cash

Inflows

1 0.8475 75000 63559.32 95000 80508.47 50000 42372.88

2 0.7182 65000 46681.99 65000 46681.99 60000 43091.07

3 0.6086 60000 36517.85 45000 27388.39 65000 39561.01

4 0.5158 55000 28368.39 45000 23210.50 66000 34042.07

5 0.4371 50000 21855.46 45000 19669.91 57000 24915.23

Scrap 0.4371 5000 2185.55 8000 3496.87 4000 1748.44

Total 199168.56 200956.14 185730.68

(III) Net Present Value = Present Value Of – Initial Investment

Cash Inflows

Project A = £199,168.56 – £175,000

= £24,168.56

Project B = £200,956.14 – £195,000

= £5,956.14

Project C = £185,730.68 – £190,000

= £-4,269.32

(b) Evaluation of the above three potential investment to be undertaken :

If the calculations in part (a) are considered, then it can be explained that Project A

should be selected among all three proposals as it would recover its initial cost in least time of all

(Tellier, 2019). If Scrappit plc chooses the project B and C over project A then it would be able

to recover its cost in 2 years and 9 months and 3 years and 3 months respectively. Although

company can think about the project B apart from project A but it should completely ignore the

project C.

If accounting rate of return is considered, then project A should be chosen over all as it

provides the return of 28.27% but if the company is willing to select the project between B and C

then the company should ignore the project B as it has the least rate of return.

On the basis of net present value analysis, the company should opt for the project A as it

gives the company, highest NPV among all the potential investments, and project C provides the

return in negative, so choosing the proposal C would not be beneficial for it.

Therefore, it can be summarised that selecting the project A should be advantageous to

Scrappit Plc as it has least payback period, higher rate of return over investment and the highest

net present value.

(c) Discussion of approaches of investment appraisals :

Payback Period :

Payback period refers to the period of time, in which the company can recover its

project cost, the payback period is derived through dividing the total initial investment by the

annual cash flow after tax if cash inflow is equal throughout the period whereas if cash inflow is

= £24,168.56

Project B = £200,956.14 – £195,000

= £5,956.14

Project C = £185,730.68 – £190,000

= £-4,269.32

(b) Evaluation of the above three potential investment to be undertaken :

If the calculations in part (a) are considered, then it can be explained that Project A

should be selected among all three proposals as it would recover its initial cost in least time of all

(Tellier, 2019). If Scrappit plc chooses the project B and C over project A then it would be able

to recover its cost in 2 years and 9 months and 3 years and 3 months respectively. Although

company can think about the project B apart from project A but it should completely ignore the

project C.

If accounting rate of return is considered, then project A should be chosen over all as it

provides the return of 28.27% but if the company is willing to select the project between B and C

then the company should ignore the project B as it has the least rate of return.

On the basis of net present value analysis, the company should opt for the project A as it

gives the company, highest NPV among all the potential investments, and project C provides the

return in negative, so choosing the proposal C would not be beneficial for it.

Therefore, it can be summarised that selecting the project A should be advantageous to

Scrappit Plc as it has least payback period, higher rate of return over investment and the highest

net present value.

(c) Discussion of approaches of investment appraisals :

Payback Period :

Payback period refers to the period of time, in which the company can recover its

project cost, the payback period is derived through dividing the total initial investment by the

annual cash flow after tax if cash inflow is equal throughout the period whereas if cash inflow is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.