Introduction to Finance: Analysis and Capital Budgeting

VerifiedAdded on 2023/01/16

|11

|1257

|100

Homework Assignment

AI Summary

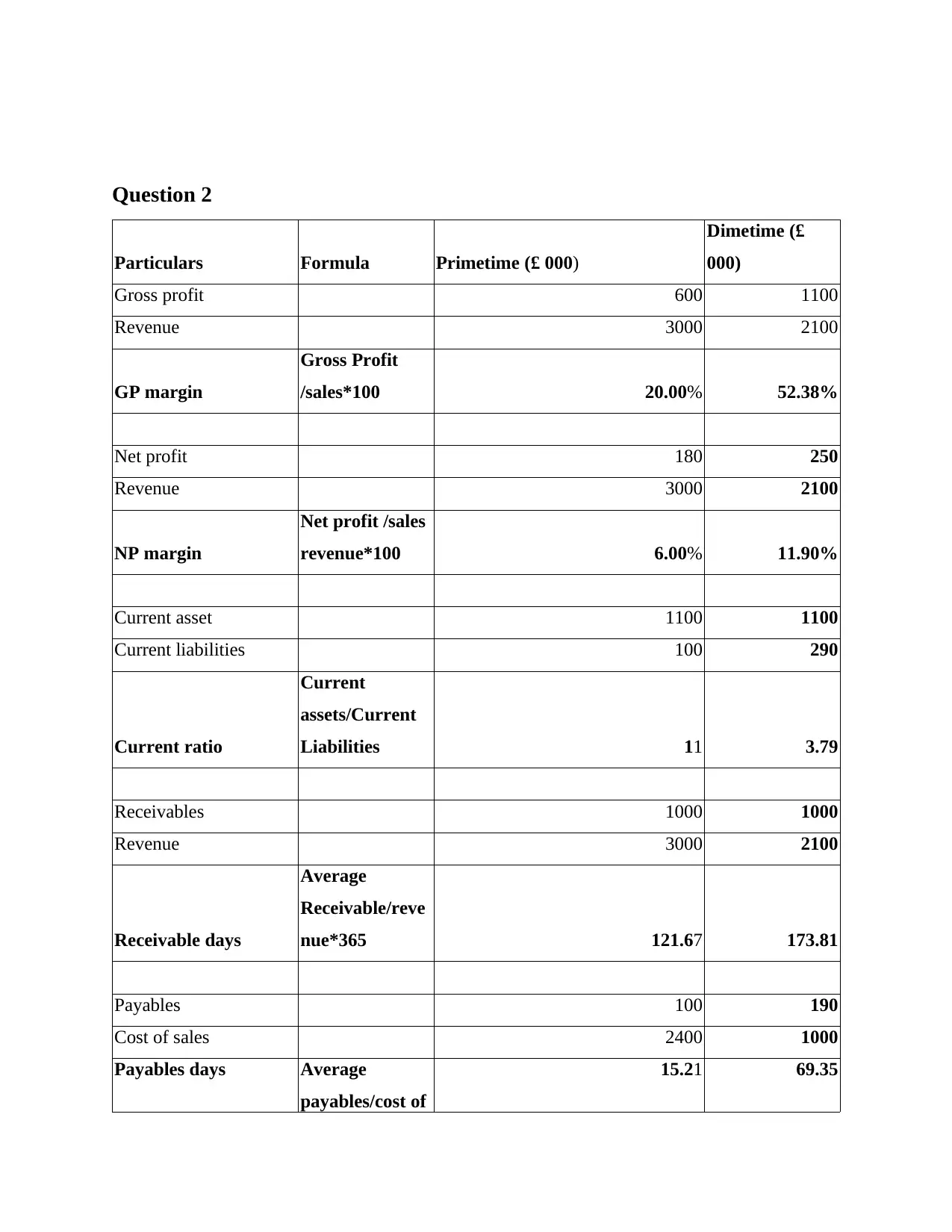

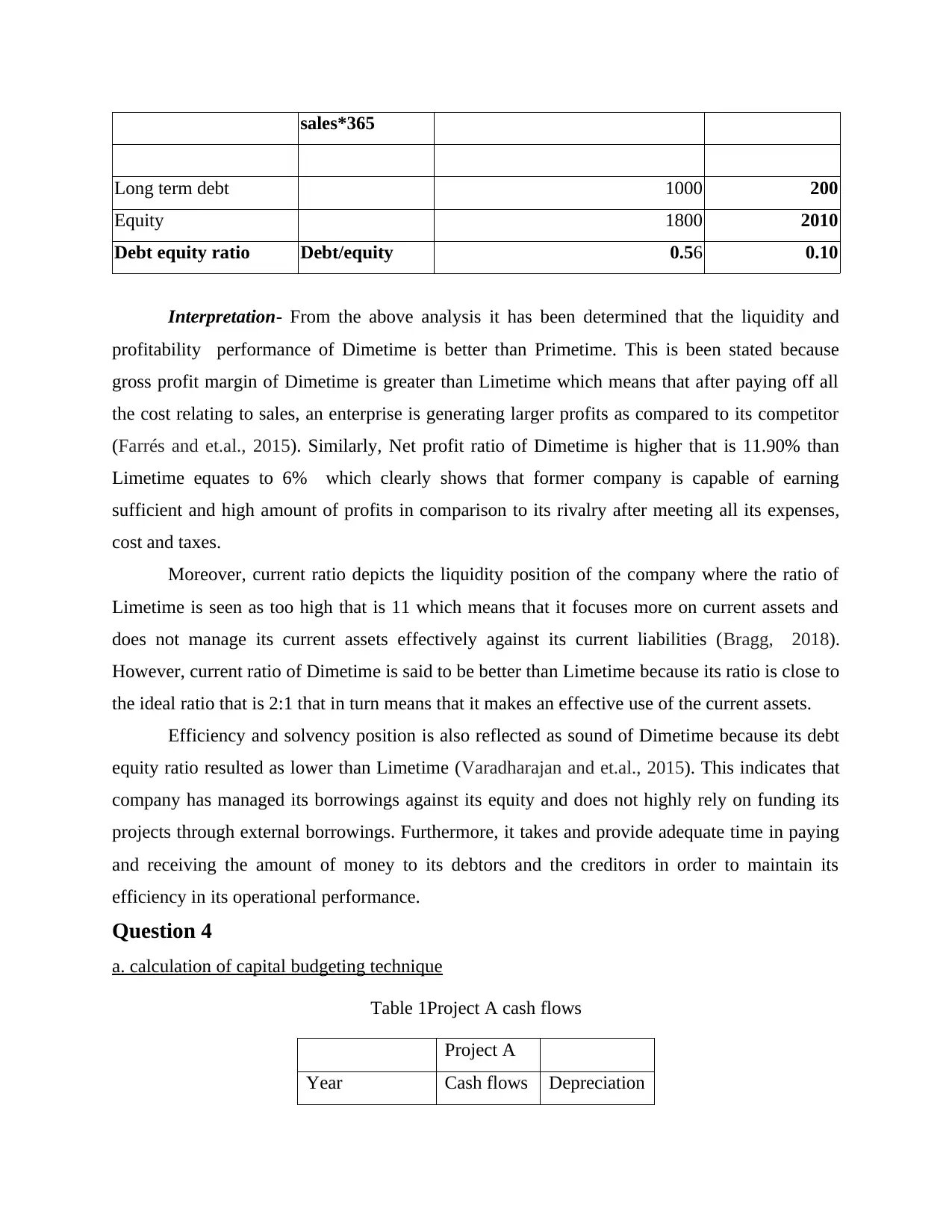

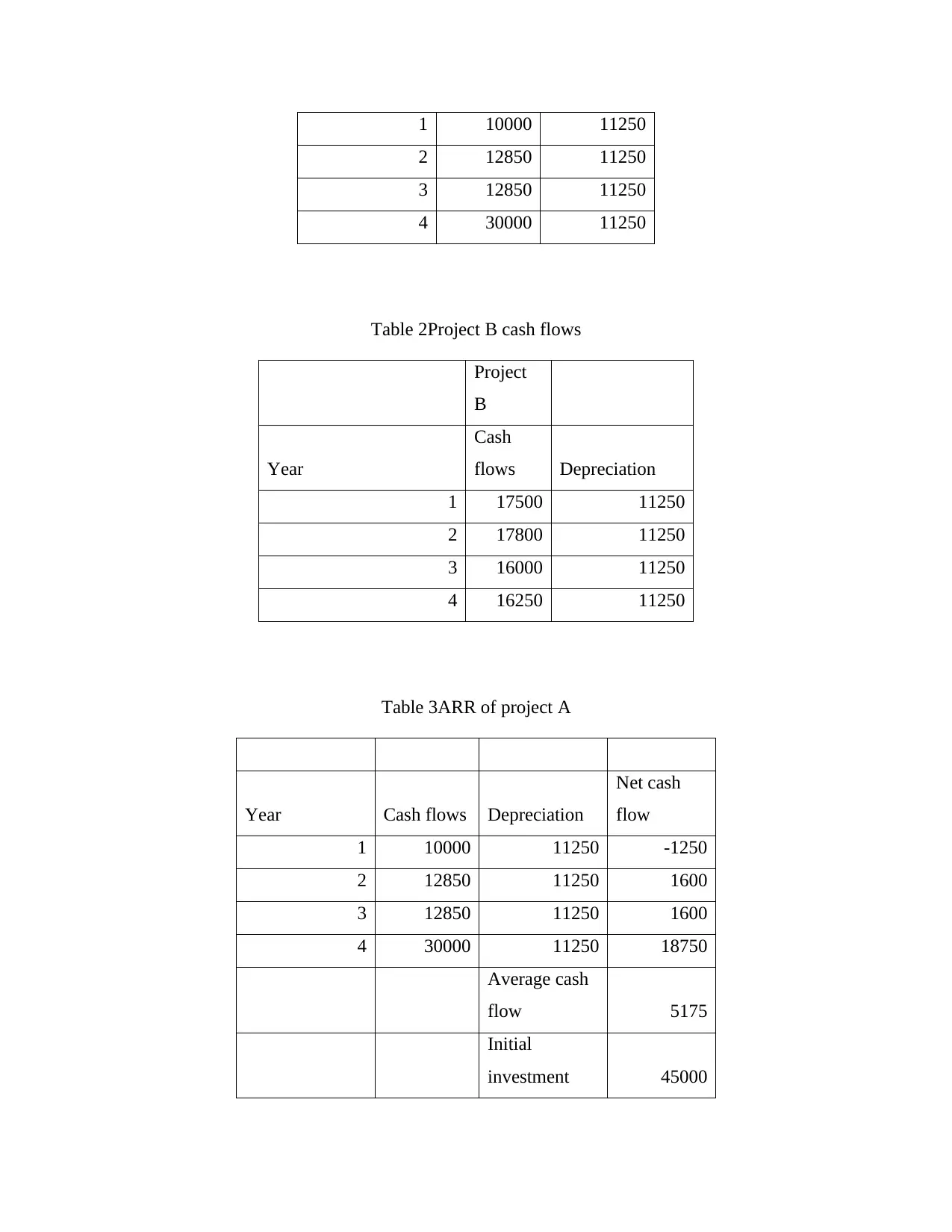

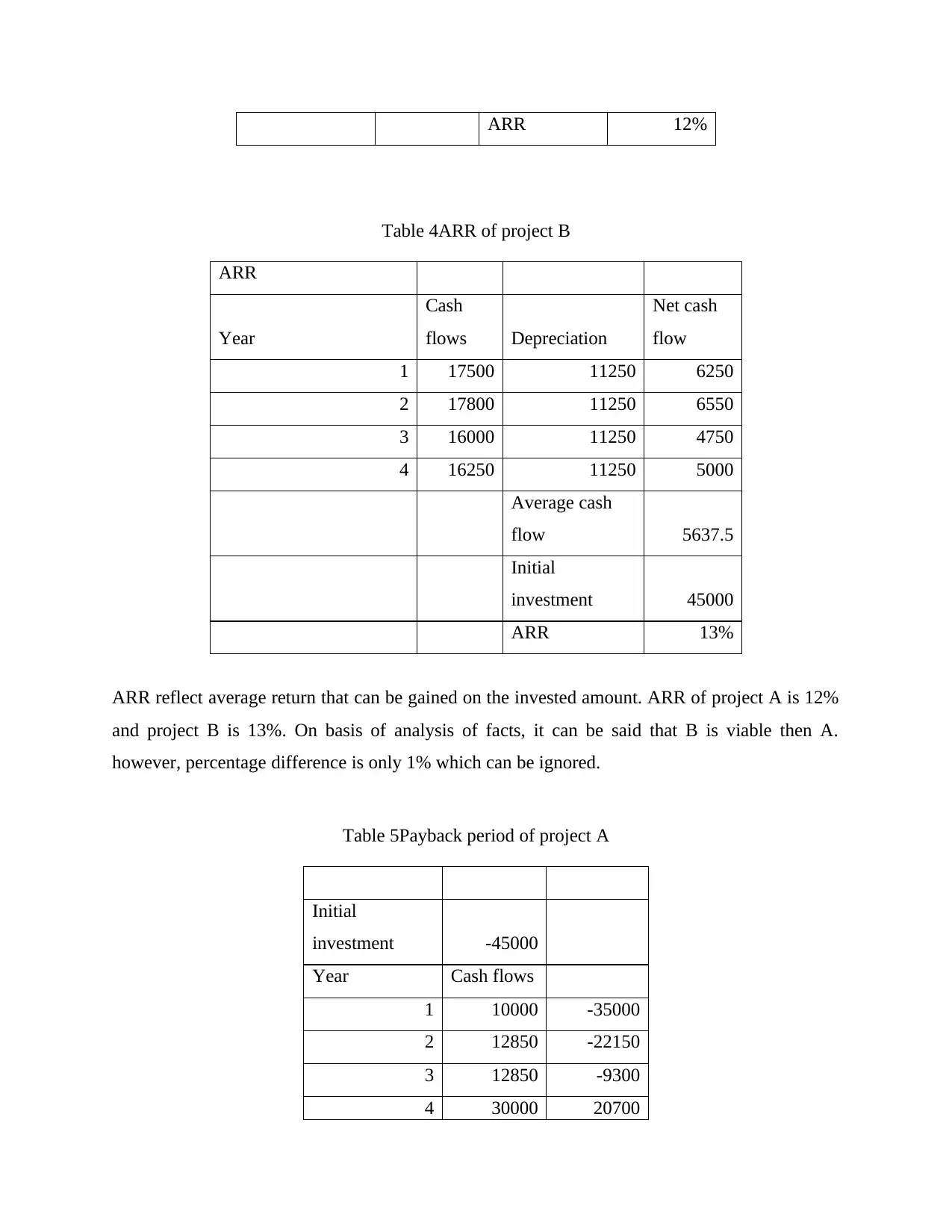

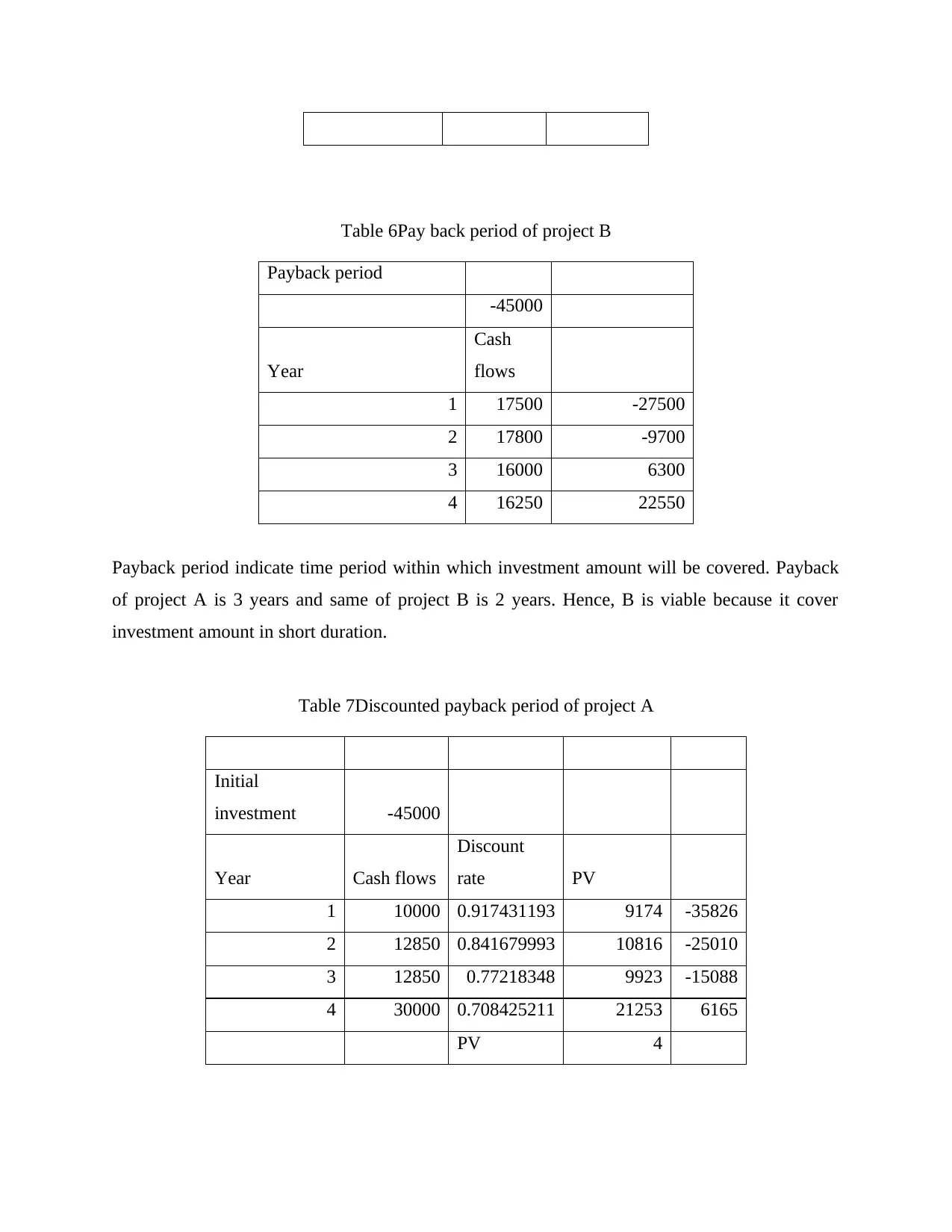

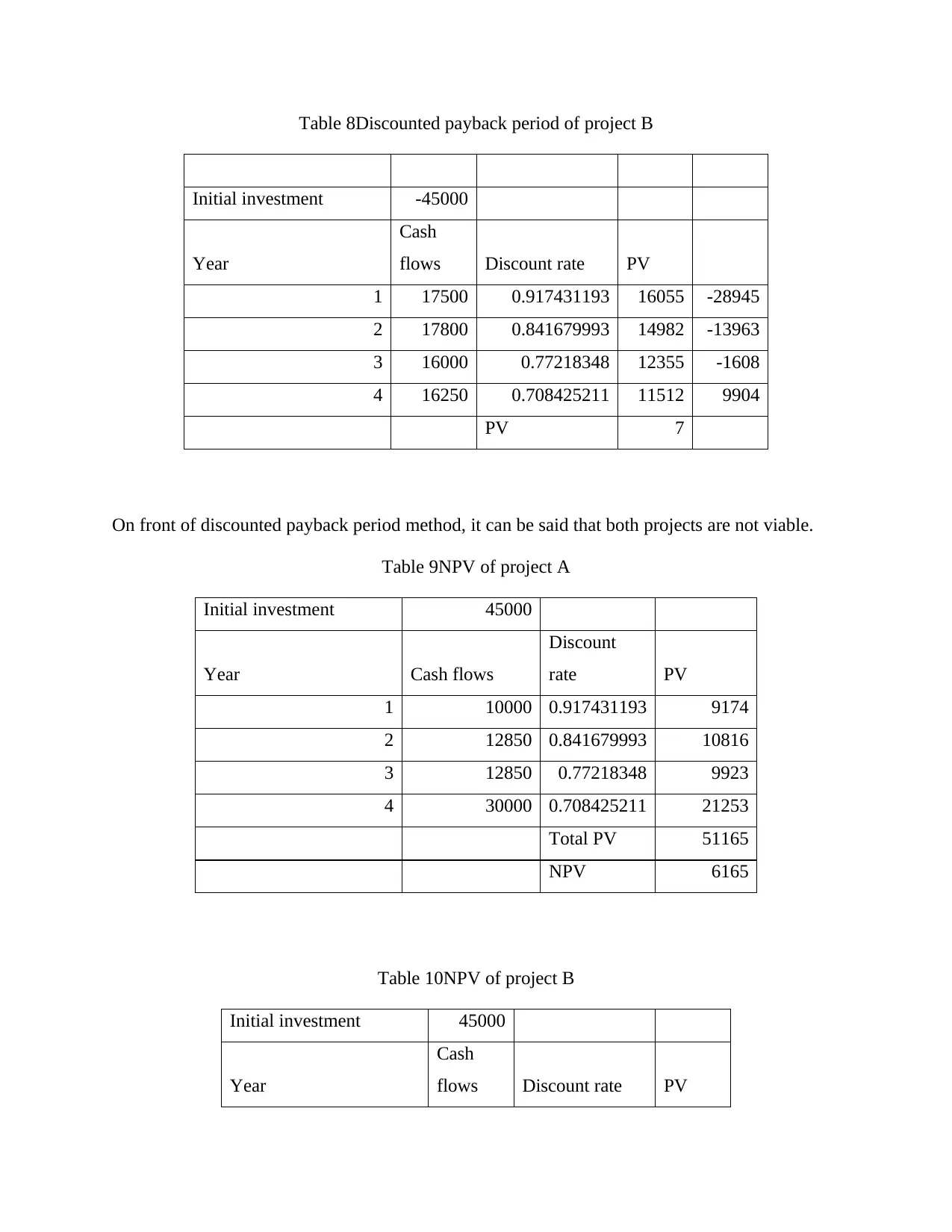

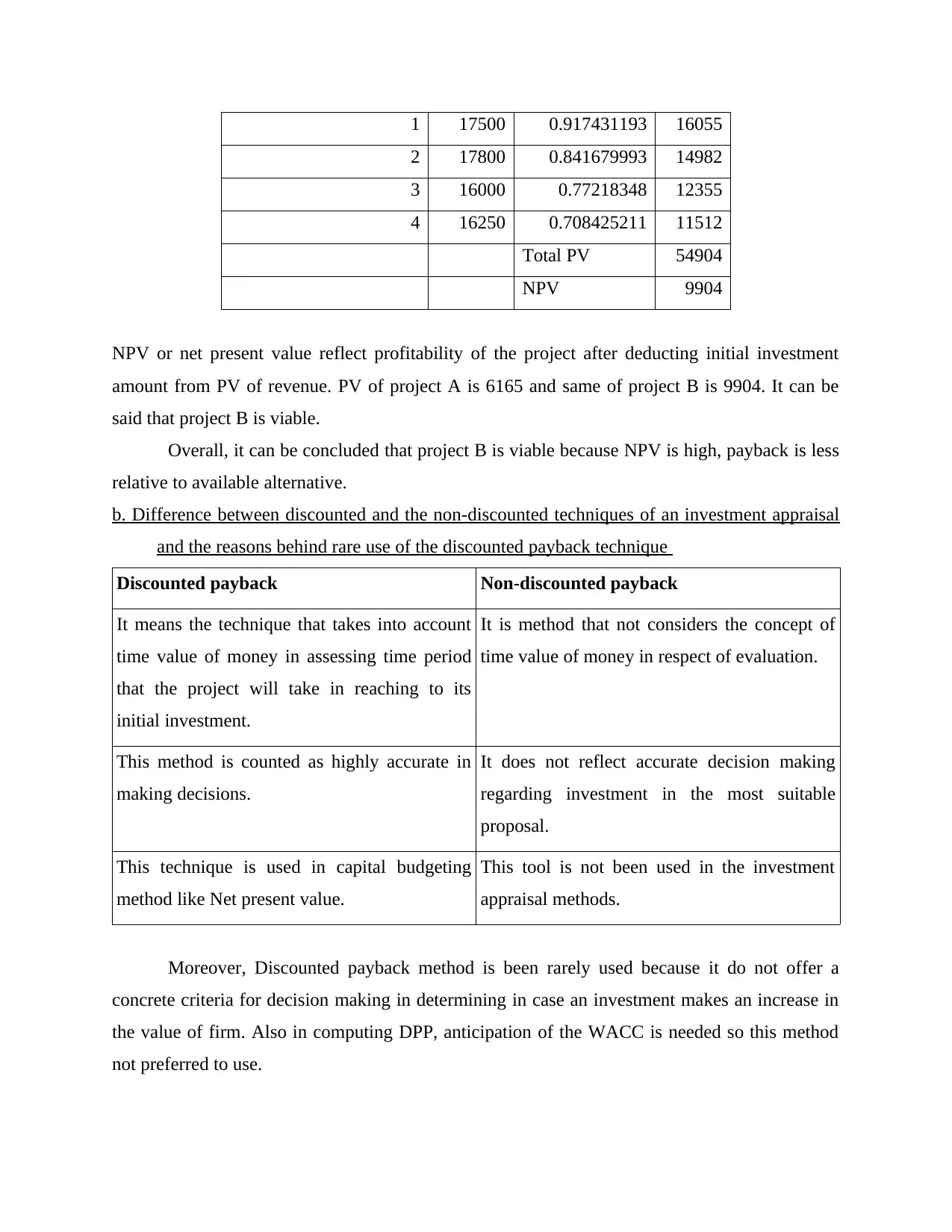

This finance assignment analyzes the financial performance of two companies, Dimetime and Primetime, using various financial ratios such as gross profit margin, net profit margin, current ratio, and debt-equity ratio. The analysis reveals that Dimetime exhibits better liquidity and profitability. The assignment also delves into capital budgeting techniques, including calculating the Average Rate of Return (ARR), payback period, discounted payback period, and Net Present Value (NPV) for two hypothetical projects, Project A and Project B. Based on the analysis, Project B is deemed more viable due to its higher NPV and shorter payback period. The solution also explains the differences between discounted and non-discounted investment appraisal techniques, discussing why the discounted payback technique is rarely used. The assignment concludes with a list of references.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.