UGB105 Introduction to Financial Accounting Assignment

VerifiedAdded on 2023/01/09

|13

|3284

|87

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting assignment, addressing key concepts and practical applications. The solution begins with an introduction to financial accounting, emphasizing the importance of financial statements such as the balance sheet, income statement, and cash flow statement. It then provides a detailed response to the assignment questions. Question 1 includes the preparation of Bob's trading account, profit and loss account, and financial position statement, utilizing the provided trial balance and additional information. Question 1 also discusses the main features of financial information for users of financial statements. Question 2 delves into ratio analysis, calculating and interpreting various financial ratios, including gross profit margin, return on capital employed, current ratio, trade payable period, and trade receivable period. Additionally, the solution demonstrates the creation of a business bank account and explores the depreciation of machinery using the straight-line method. The document offers a complete and well-structured solution for the assignment.

Introduction to Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

QUESTION......................................................................................................................................3

1a). Financial statement of Bob’s account.......................................................................................3

1b). Six of the main features of information for users of financial statements......................5

QUESTION......................................................................................................................................7

2a) Calculation of ratio and interpretation..............................................................................7

(2b) Business bank.................................................................................................................8

(2c) Depreciation of machinery account..............................................................................10

CONCLUSION..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

QUESTION......................................................................................................................................3

1a). Financial statement of Bob’s account.......................................................................................3

1b). Six of the main features of information for users of financial statements......................5

QUESTION......................................................................................................................................7

2a) Calculation of ratio and interpretation..............................................................................7

(2b) Business bank.................................................................................................................8

(2c) Depreciation of machinery account..............................................................................10

CONCLUSION..............................................................................................................................11

INTRODUCTION

Financial accounting is a specific framework with a variety of activity to monitor, assess

and rewrite the results of such statements to stakeholders. The related operations are relevant

with preparation of financial statements like the balance sheet, statement of income and

statement of cash flow in order to show company value and results over a set period of time

which is generally yearly. Financial accounting is specifically concerned with the production of

these records, based on accurate facts and obeying accounting standard known as GAAP.

GAAP provides information management throughout the United States on only a wide

variety of topics, including the review of financial statements (Anantharaman, 2017). The

primary goal is to provide the owners with such results because their capital is spent in the

company. Within this article, the key aspects of details that are useful to consumers are year-end

reports. In addition to this, quantify and explain various forms of financial equation to assess the

financial condition of the company and start writing savings account for each month. In fact,

apply various methods of depreciation and learn different principles of accounting.

QUESTION

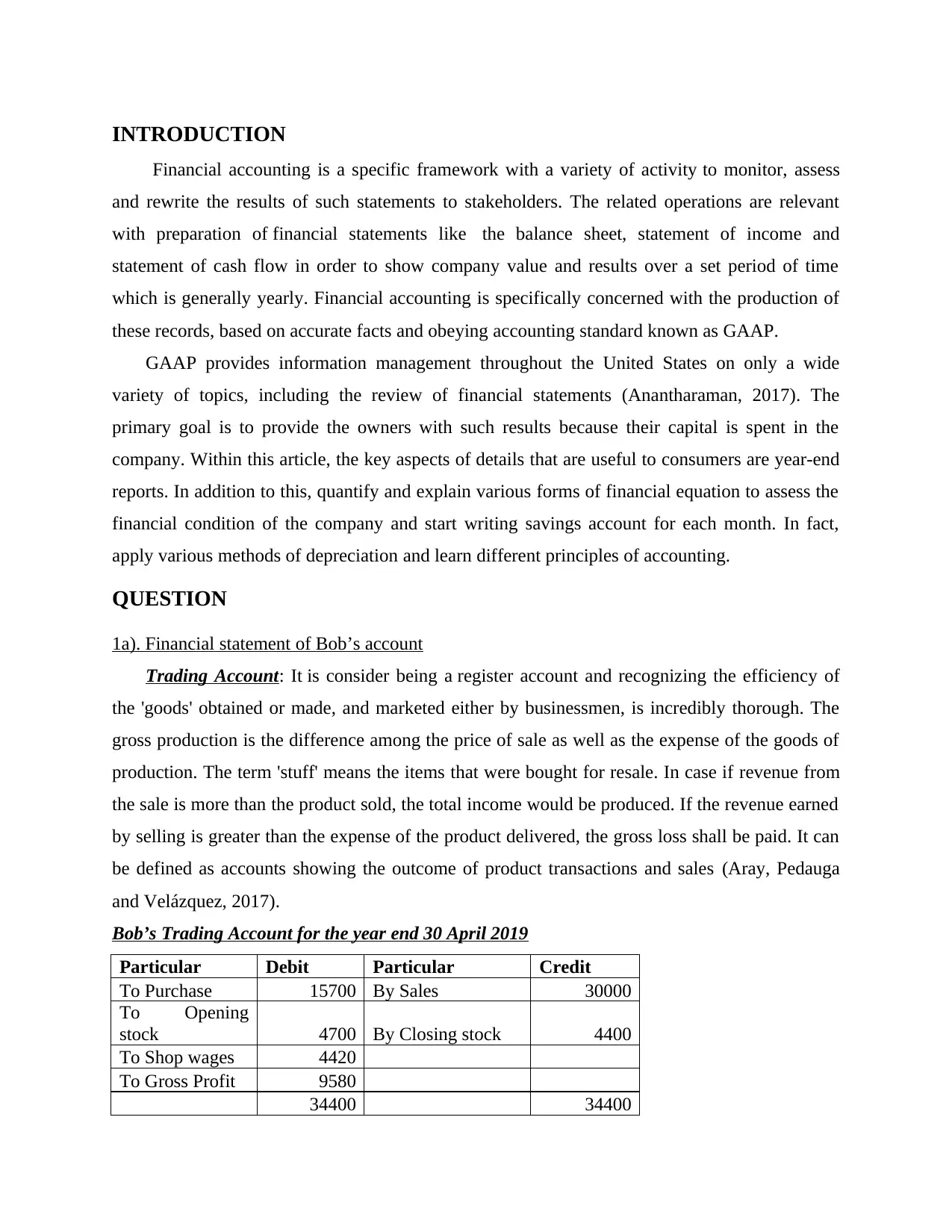

1a). Financial statement of Bob’s account

Trading Account: It is consider being a register account and recognizing the efficiency of

the 'goods' obtained or made, and marketed either by businessmen, is incredibly thorough. The

gross production is the difference among the price of sale as well as the expense of the goods of

production. The term 'stuff' means the items that were bought for resale. In case if revenue from

the sale is more than the product sold, the total income would be produced. If the revenue earned

by selling is greater than the expense of the product delivered, the gross loss shall be paid. It can

be defined as accounts showing the outcome of product transactions and sales (Aray, Pedauga

and Velázquez, 2017).

Bob’s Trading Account for the year end 30 April 2019

Particular Debit Particular Credit

To Purchase 15700 By Sales 30000

To Opening

stock 4700 By Closing stock 4400

To Shop wages 4420

To Gross Profit 9580

34400 34400

Financial accounting is a specific framework with a variety of activity to monitor, assess

and rewrite the results of such statements to stakeholders. The related operations are relevant

with preparation of financial statements like the balance sheet, statement of income and

statement of cash flow in order to show company value and results over a set period of time

which is generally yearly. Financial accounting is specifically concerned with the production of

these records, based on accurate facts and obeying accounting standard known as GAAP.

GAAP provides information management throughout the United States on only a wide

variety of topics, including the review of financial statements (Anantharaman, 2017). The

primary goal is to provide the owners with such results because their capital is spent in the

company. Within this article, the key aspects of details that are useful to consumers are year-end

reports. In addition to this, quantify and explain various forms of financial equation to assess the

financial condition of the company and start writing savings account for each month. In fact,

apply various methods of depreciation and learn different principles of accounting.

QUESTION

1a). Financial statement of Bob’s account

Trading Account: It is consider being a register account and recognizing the efficiency of

the 'goods' obtained or made, and marketed either by businessmen, is incredibly thorough. The

gross production is the difference among the price of sale as well as the expense of the goods of

production. The term 'stuff' means the items that were bought for resale. In case if revenue from

the sale is more than the product sold, the total income would be produced. If the revenue earned

by selling is greater than the expense of the product delivered, the gross loss shall be paid. It can

be defined as accounts showing the outcome of product transactions and sales (Aray, Pedauga

and Velázquez, 2017).

Bob’s Trading Account for the year end 30 April 2019

Particular Debit Particular Credit

To Purchase 15700 By Sales 30000

To Opening

stock 4700 By Closing stock 4400

To Shop wages 4420

To Gross Profit 9580

34400 34400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

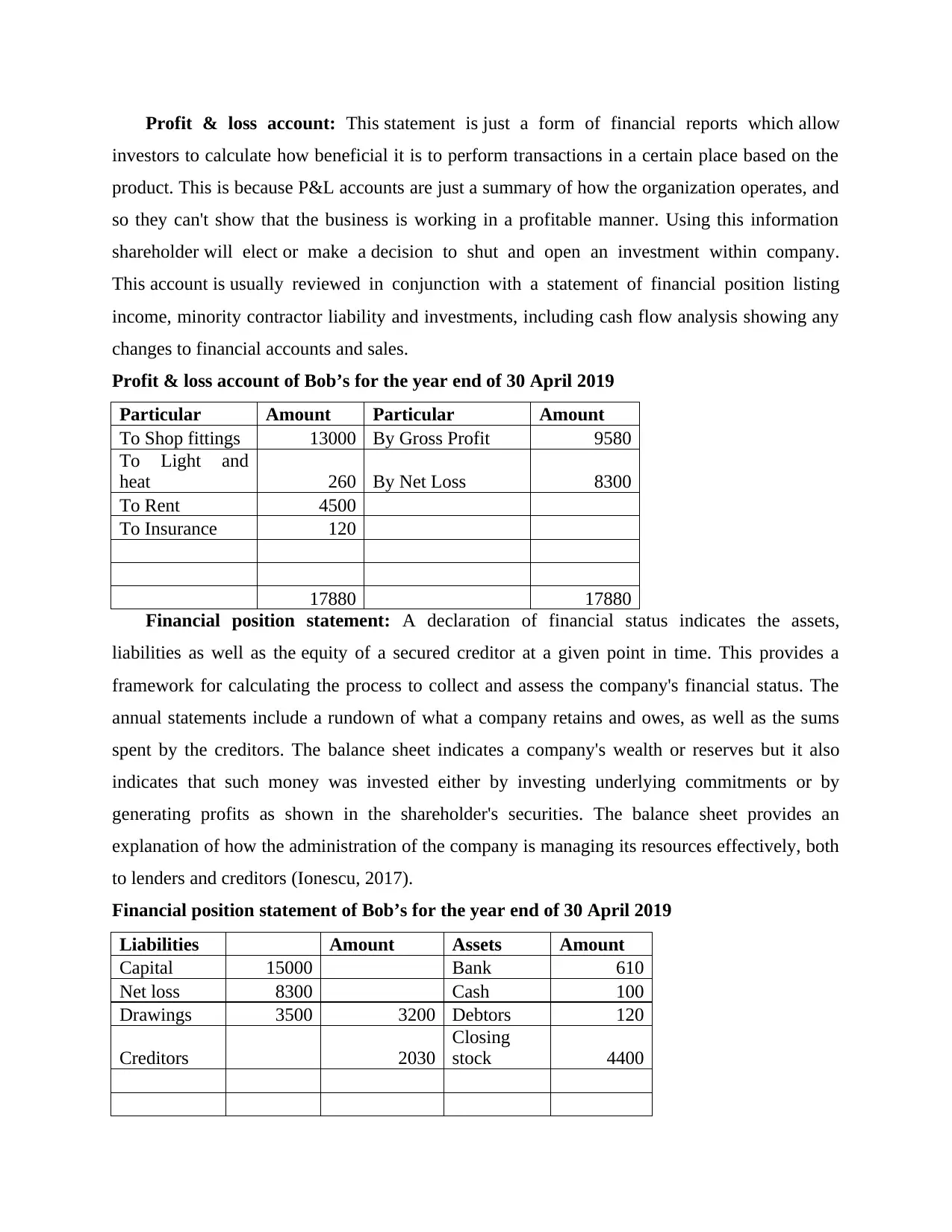

Profit & loss account: This statement is just a form of financial reports which allow

investors to calculate how beneficial it is to perform transactions in a certain place based on the

product. This is because P&L accounts are just a summary of how the organization operates, and

so they can't show that the business is working in a profitable manner. Using this information

shareholder will elect or make a decision to shut and open an investment within company.

This account is usually reviewed in conjunction with a statement of financial position listing

income, minority contractor liability and investments, including cash flow analysis showing any

changes to financial accounts and sales.

Profit & loss account of Bob’s for the year end of 30 April 2019

Particular Amount Particular Amount

To Shop fittings 13000 By Gross Profit 9580

To Light and

heat 260 By Net Loss 8300

To Rent 4500

To Insurance 120

17880 17880

Financial position statement: A declaration of financial status indicates the assets,

liabilities as well as the equity of a secured creditor at a given point in time. This provides a

framework for calculating the process to collect and assess the company's financial status. The

annual statements include a rundown of what a company retains and owes, as well as the sums

spent by the creditors. The balance sheet indicates a company's wealth or reserves but it also

indicates that such money was invested either by investing underlying commitments or by

generating profits as shown in the shareholder's securities. The balance sheet provides an

explanation of how the administration of the company is managing its resources effectively, both

to lenders and creditors (Ionescu, 2017).

Financial position statement of Bob’s for the year end of 30 April 2019

Liabilities Amount Assets Amount

Capital 15000 Bank 610

Net loss 8300 Cash 100

Drawings 3500 3200 Debtors 120

Creditors 2030

Closing

stock 4400

investors to calculate how beneficial it is to perform transactions in a certain place based on the

product. This is because P&L accounts are just a summary of how the organization operates, and

so they can't show that the business is working in a profitable manner. Using this information

shareholder will elect or make a decision to shut and open an investment within company.

This account is usually reviewed in conjunction with a statement of financial position listing

income, minority contractor liability and investments, including cash flow analysis showing any

changes to financial accounts and sales.

Profit & loss account of Bob’s for the year end of 30 April 2019

Particular Amount Particular Amount

To Shop fittings 13000 By Gross Profit 9580

To Light and

heat 260 By Net Loss 8300

To Rent 4500

To Insurance 120

17880 17880

Financial position statement: A declaration of financial status indicates the assets,

liabilities as well as the equity of a secured creditor at a given point in time. This provides a

framework for calculating the process to collect and assess the company's financial status. The

annual statements include a rundown of what a company retains and owes, as well as the sums

spent by the creditors. The balance sheet indicates a company's wealth or reserves but it also

indicates that such money was invested either by investing underlying commitments or by

generating profits as shown in the shareholder's securities. The balance sheet provides an

explanation of how the administration of the company is managing its resources effectively, both

to lenders and creditors (Ionescu, 2017).

Financial position statement of Bob’s for the year end of 30 April 2019

Liabilities Amount Assets Amount

Capital 15000 Bank 610

Net loss 8300 Cash 100

Drawings 3500 3200 Debtors 120

Creditors 2030

Closing

stock 4400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

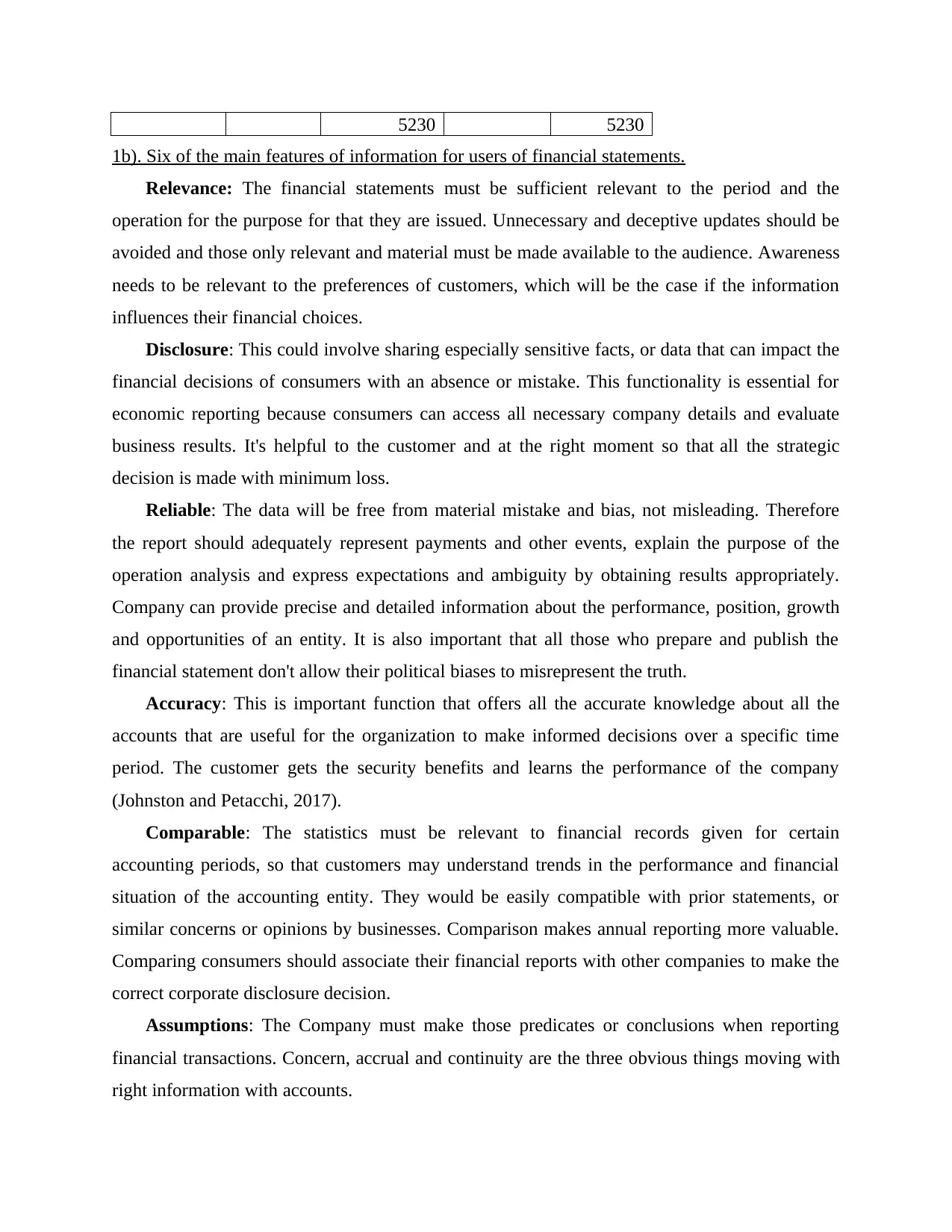

5230 5230

1b). Six of the main features of information for users of financial statements.

Relevance: The financial statements must be sufficient relevant to the period and the

operation for the purpose for that they are issued. Unnecessary and deceptive updates should be

avoided and those only relevant and material must be made available to the audience. Awareness

needs to be relevant to the preferences of customers, which will be the case if the information

influences their financial choices.

Disclosure: This could involve sharing especially sensitive facts, or data that can impact the

financial decisions of consumers with an absence or mistake. This functionality is essential for

economic reporting because consumers can access all necessary company details and evaluate

business results. It's helpful to the customer and at the right moment so that all the strategic

decision is made with minimum loss.

Reliable: The data will be free from material mistake and bias, not misleading. Therefore

the report should adequately represent payments and other events, explain the purpose of the

operation analysis and express expectations and ambiguity by obtaining results appropriately.

Company can provide precise and detailed information about the performance, position, growth

and opportunities of an entity. It is also important that all those who prepare and publish the

financial statement don't allow their political biases to misrepresent the truth.

Accuracy: This is important function that offers all the accurate knowledge about all the

accounts that are useful for the organization to make informed decisions over a specific time

period. The customer gets the security benefits and learns the performance of the company

(Johnston and Petacchi, 2017).

Comparable: The statistics must be relevant to financial records given for certain

accounting periods, so that customers may understand trends in the performance and financial

situation of the accounting entity. They would be easily compatible with prior statements, or

similar concerns or opinions by businesses. Comparison makes annual reporting more valuable.

Comparing consumers should associate their financial reports with other companies to make the

correct corporate disclosure decision.

Assumptions: The Company must make those predicates or conclusions when reporting

financial transactions. Concern, accrual and continuity are the three obvious things moving with

right information with accounts.

1b). Six of the main features of information for users of financial statements.

Relevance: The financial statements must be sufficient relevant to the period and the

operation for the purpose for that they are issued. Unnecessary and deceptive updates should be

avoided and those only relevant and material must be made available to the audience. Awareness

needs to be relevant to the preferences of customers, which will be the case if the information

influences their financial choices.

Disclosure: This could involve sharing especially sensitive facts, or data that can impact the

financial decisions of consumers with an absence or mistake. This functionality is essential for

economic reporting because consumers can access all necessary company details and evaluate

business results. It's helpful to the customer and at the right moment so that all the strategic

decision is made with minimum loss.

Reliable: The data will be free from material mistake and bias, not misleading. Therefore

the report should adequately represent payments and other events, explain the purpose of the

operation analysis and express expectations and ambiguity by obtaining results appropriately.

Company can provide precise and detailed information about the performance, position, growth

and opportunities of an entity. It is also important that all those who prepare and publish the

financial statement don't allow their political biases to misrepresent the truth.

Accuracy: This is important function that offers all the accurate knowledge about all the

accounts that are useful for the organization to make informed decisions over a specific time

period. The customer gets the security benefits and learns the performance of the company

(Johnston and Petacchi, 2017).

Comparable: The statistics must be relevant to financial records given for certain

accounting periods, so that customers may understand trends in the performance and financial

situation of the accounting entity. They would be easily compatible with prior statements, or

similar concerns or opinions by businesses. Comparison makes annual reporting more valuable.

Comparing consumers should associate their financial reports with other companies to make the

correct corporate disclosure decision.

Assumptions: The Company must make those predicates or conclusions when reporting

financial transactions. Concern, accrual and continuity are the three obvious things moving with

right information with accounts.

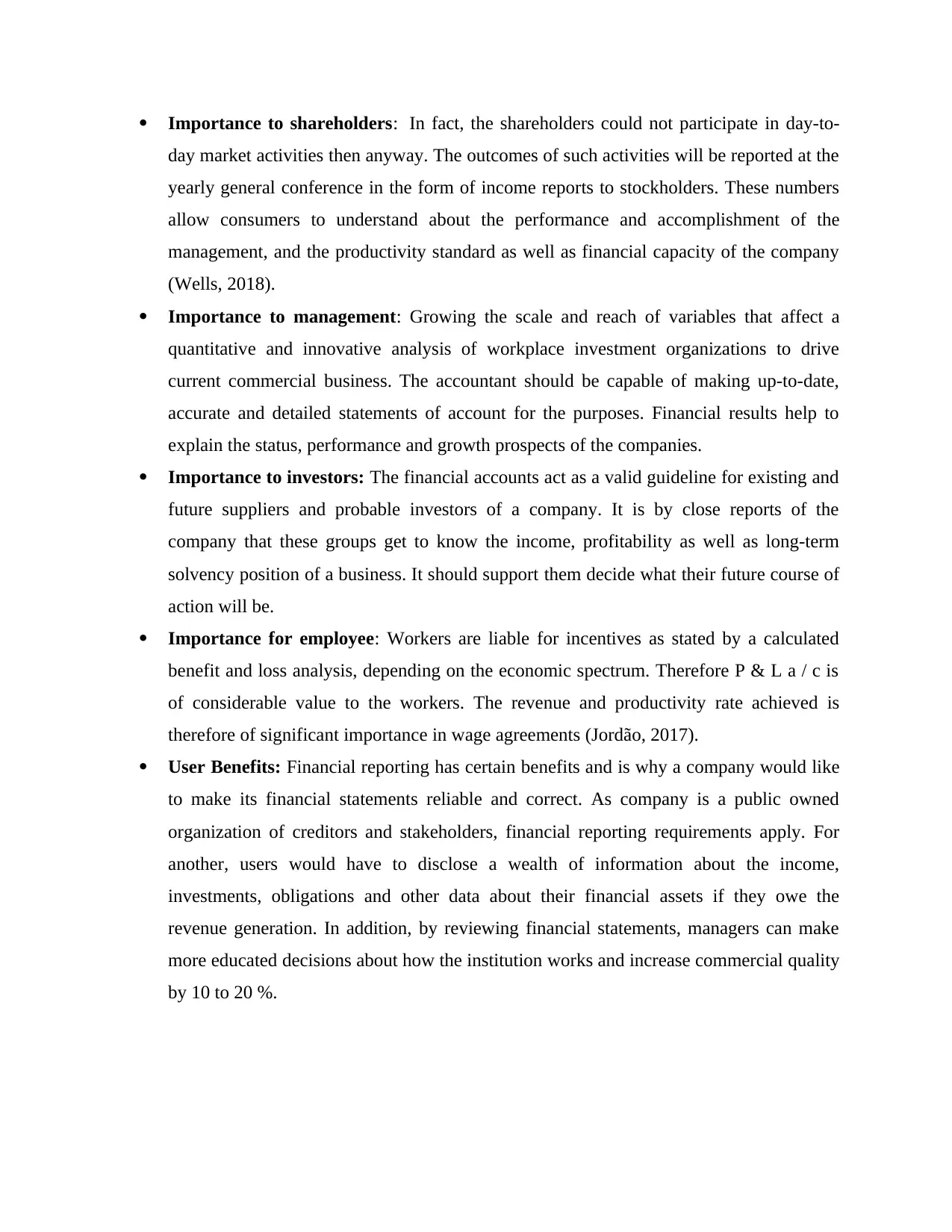

Importance to shareholders: In fact, the shareholders could not participate in day-to-

day market activities then anyway. The outcomes of such activities will be reported at the

yearly general conference in the form of income reports to stockholders. These numbers

allow consumers to understand about the performance and accomplishment of the

management, and the productivity standard as well as financial capacity of the company

(Wells, 2018).

Importance to management: Growing the scale and reach of variables that affect a

quantitative and innovative analysis of workplace investment organizations to drive

current commercial business. The accountant should be capable of making up-to-date,

accurate and detailed statements of account for the purposes. Financial results help to

explain the status, performance and growth prospects of the companies.

Importance to investors: The financial accounts act as a valid guideline for existing and

future suppliers and probable investors of a company. It is by close reports of the

company that these groups get to know the income, profitability as well as long-term

solvency position of a business. It should support them decide what their future course of

action will be.

Importance for employee: Workers are liable for incentives as stated by a calculated

benefit and loss analysis, depending on the economic spectrum. Therefore P & L a / c is

of considerable value to the workers. The revenue and productivity rate achieved is

therefore of significant importance in wage agreements (Jordão, 2017).

User Benefits: Financial reporting has certain benefits and is why a company would like

to make its financial statements reliable and correct. As company is a public owned

organization of creditors and stakeholders, financial reporting requirements apply. For

another, users would have to disclose a wealth of information about the income,

investments, obligations and other data about their financial assets if they owe the

revenue generation. In addition, by reviewing financial statements, managers can make

more educated decisions about how the institution works and increase commercial quality

by 10 to 20 %.

day market activities then anyway. The outcomes of such activities will be reported at the

yearly general conference in the form of income reports to stockholders. These numbers

allow consumers to understand about the performance and accomplishment of the

management, and the productivity standard as well as financial capacity of the company

(Wells, 2018).

Importance to management: Growing the scale and reach of variables that affect a

quantitative and innovative analysis of workplace investment organizations to drive

current commercial business. The accountant should be capable of making up-to-date,

accurate and detailed statements of account for the purposes. Financial results help to

explain the status, performance and growth prospects of the companies.

Importance to investors: The financial accounts act as a valid guideline for existing and

future suppliers and probable investors of a company. It is by close reports of the

company that these groups get to know the income, profitability as well as long-term

solvency position of a business. It should support them decide what their future course of

action will be.

Importance for employee: Workers are liable for incentives as stated by a calculated

benefit and loss analysis, depending on the economic spectrum. Therefore P & L a / c is

of considerable value to the workers. The revenue and productivity rate achieved is

therefore of significant importance in wage agreements (Jordão, 2017).

User Benefits: Financial reporting has certain benefits and is why a company would like

to make its financial statements reliable and correct. As company is a public owned

organization of creditors and stakeholders, financial reporting requirements apply. For

another, users would have to disclose a wealth of information about the income,

investments, obligations and other data about their financial assets if they owe the

revenue generation. In addition, by reviewing financial statements, managers can make

more educated decisions about how the institution works and increase commercial quality

by 10 to 20 %.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION

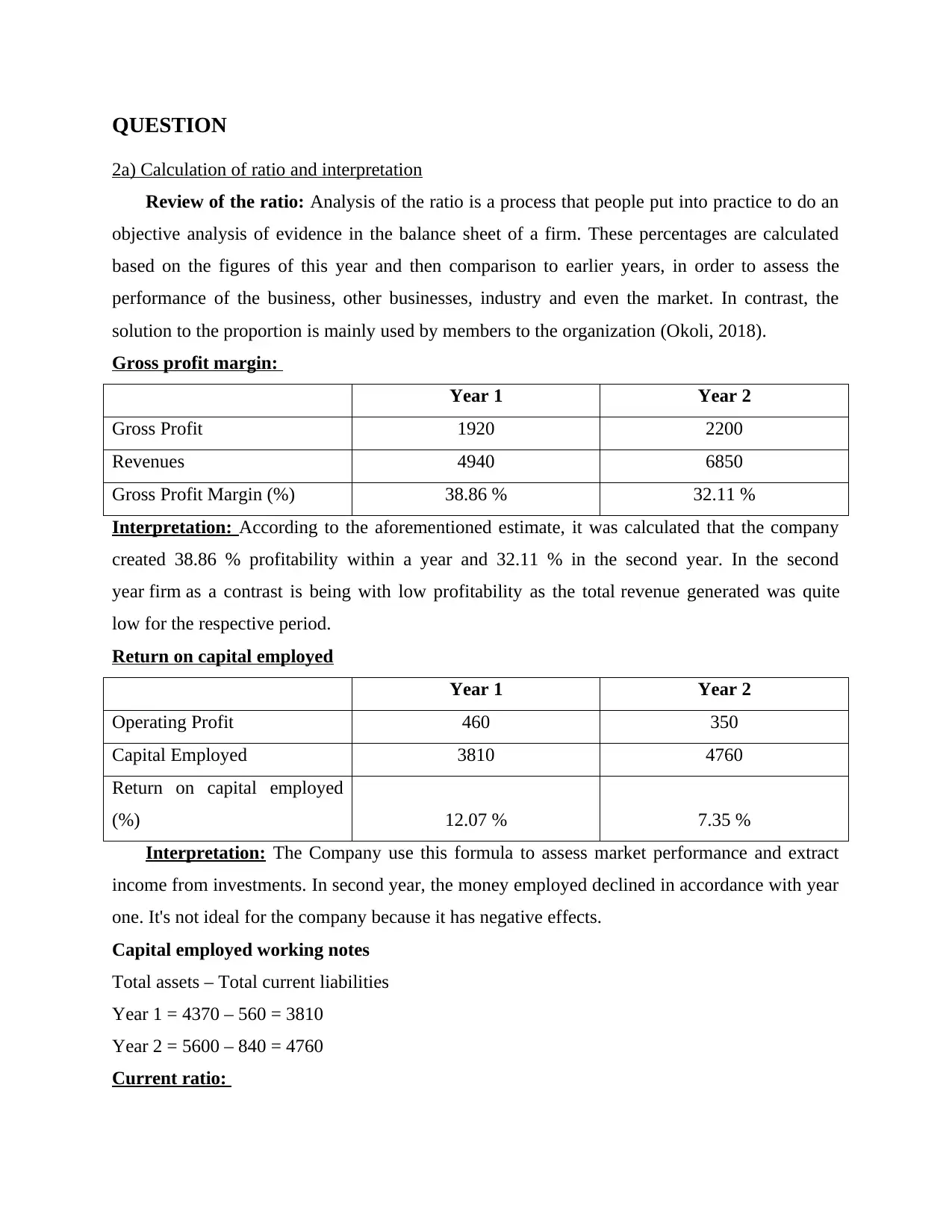

2a) Calculation of ratio and interpretation

Review of the ratio: Analysis of the ratio is a process that people put into practice to do an

objective analysis of evidence in the balance sheet of a firm. These percentages are calculated

based on the figures of this year and then comparison to earlier years, in order to assess the

performance of the business, other businesses, industry and even the market. In contrast, the

solution to the proportion is mainly used by members to the organization (Okoli, 2018).

Gross profit margin:

Year 1 Year 2

Gross Profit 1920 2200

Revenues 4940 6850

Gross Profit Margin (%) 38.86 % 32.11 %

Interpretation: According to the aforementioned estimate, it was calculated that the company

created 38.86 % profitability within a year and 32.11 % in the second year. In the second

year firm as a contrast is being with low profitability as the total revenue generated was quite

low for the respective period.

Return on capital employed

Year 1 Year 2

Operating Profit 460 350

Capital Employed 3810 4760

Return on capital employed

(%) 12.07 % 7.35 %

Interpretation: The Company use this formula to assess market performance and extract

income from investments. In second year, the money employed declined in accordance with year

one. It's not ideal for the company because it has negative effects.

Capital employed working notes

Total assets – Total current liabilities

Year 1 = 4370 – 560 = 3810

Year 2 = 5600 – 840 = 4760

Current ratio:

2a) Calculation of ratio and interpretation

Review of the ratio: Analysis of the ratio is a process that people put into practice to do an

objective analysis of evidence in the balance sheet of a firm. These percentages are calculated

based on the figures of this year and then comparison to earlier years, in order to assess the

performance of the business, other businesses, industry and even the market. In contrast, the

solution to the proportion is mainly used by members to the organization (Okoli, 2018).

Gross profit margin:

Year 1 Year 2

Gross Profit 1920 2200

Revenues 4940 6850

Gross Profit Margin (%) 38.86 % 32.11 %

Interpretation: According to the aforementioned estimate, it was calculated that the company

created 38.86 % profitability within a year and 32.11 % in the second year. In the second

year firm as a contrast is being with low profitability as the total revenue generated was quite

low for the respective period.

Return on capital employed

Year 1 Year 2

Operating Profit 460 350

Capital Employed 3810 4760

Return on capital employed

(%) 12.07 % 7.35 %

Interpretation: The Company use this formula to assess market performance and extract

income from investments. In second year, the money employed declined in accordance with year

one. It's not ideal for the company because it has negative effects.

Capital employed working notes

Total assets – Total current liabilities

Year 1 = 4370 – 560 = 3810

Year 2 = 5600 – 840 = 4760

Current ratio:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

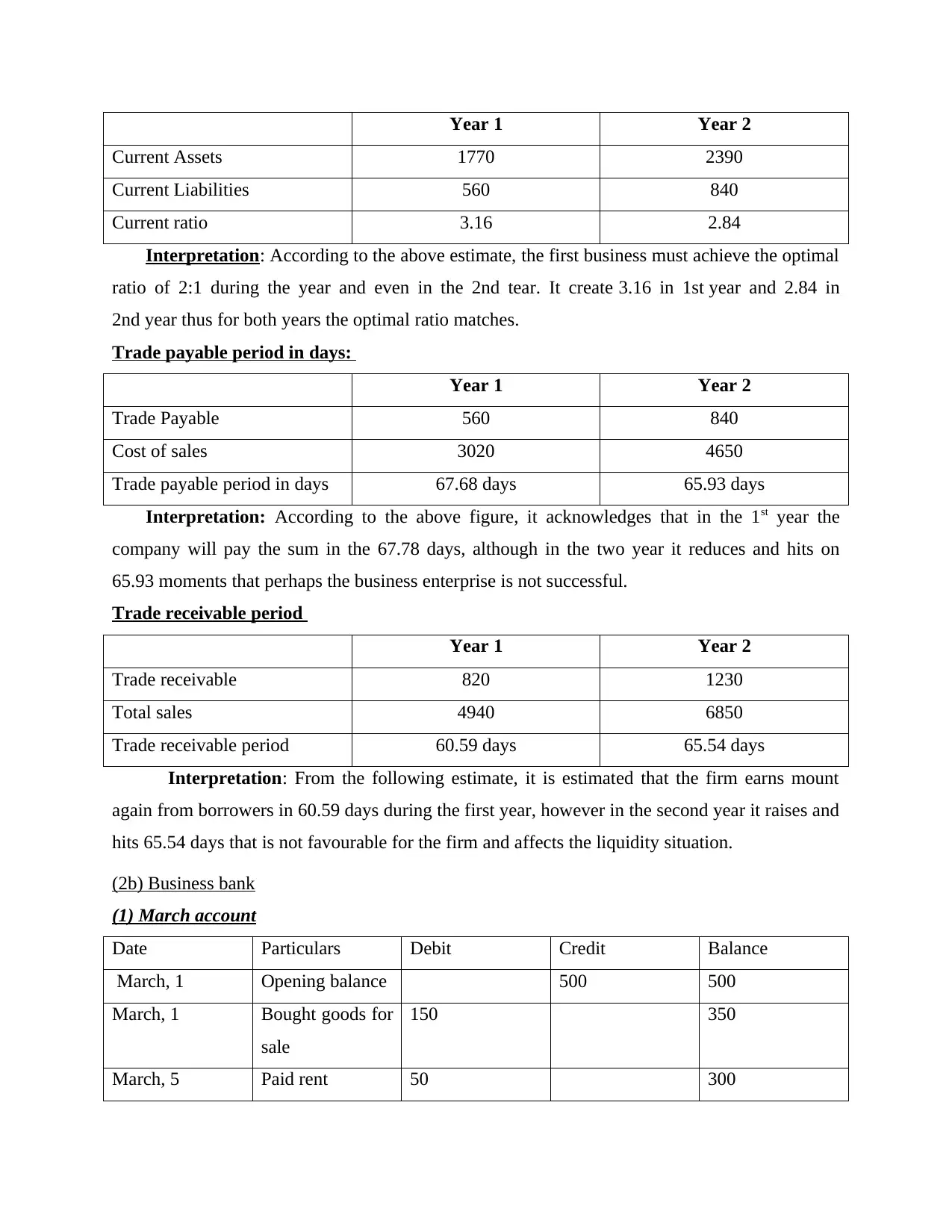

Year 1 Year 2

Current Assets 1770 2390

Current Liabilities 560 840

Current ratio 3.16 2.84

Interpretation: According to the above estimate, the first business must achieve the optimal

ratio of 2:1 during the year and even in the 2nd tear. It create 3.16 in 1st year and 2.84 in

2nd year thus for both years the optimal ratio matches.

Trade payable period in days:

Year 1 Year 2

Trade Payable 560 840

Cost of sales 3020 4650

Trade payable period in days 67.68 days 65.93 days

Interpretation: According to the above figure, it acknowledges that in the 1st year the

company will pay the sum in the 67.78 days, although in the two year it reduces and hits on

65.93 moments that perhaps the business enterprise is not successful.

Trade receivable period

Year 1 Year 2

Trade receivable 820 1230

Total sales 4940 6850

Trade receivable period 60.59 days 65.54 days

Interpretation: From the following estimate, it is estimated that the firm earns mount

again from borrowers in 60.59 days during the first year, however in the second year it raises and

hits 65.54 days that is not favourable for the firm and affects the liquidity situation.

(2b) Business bank

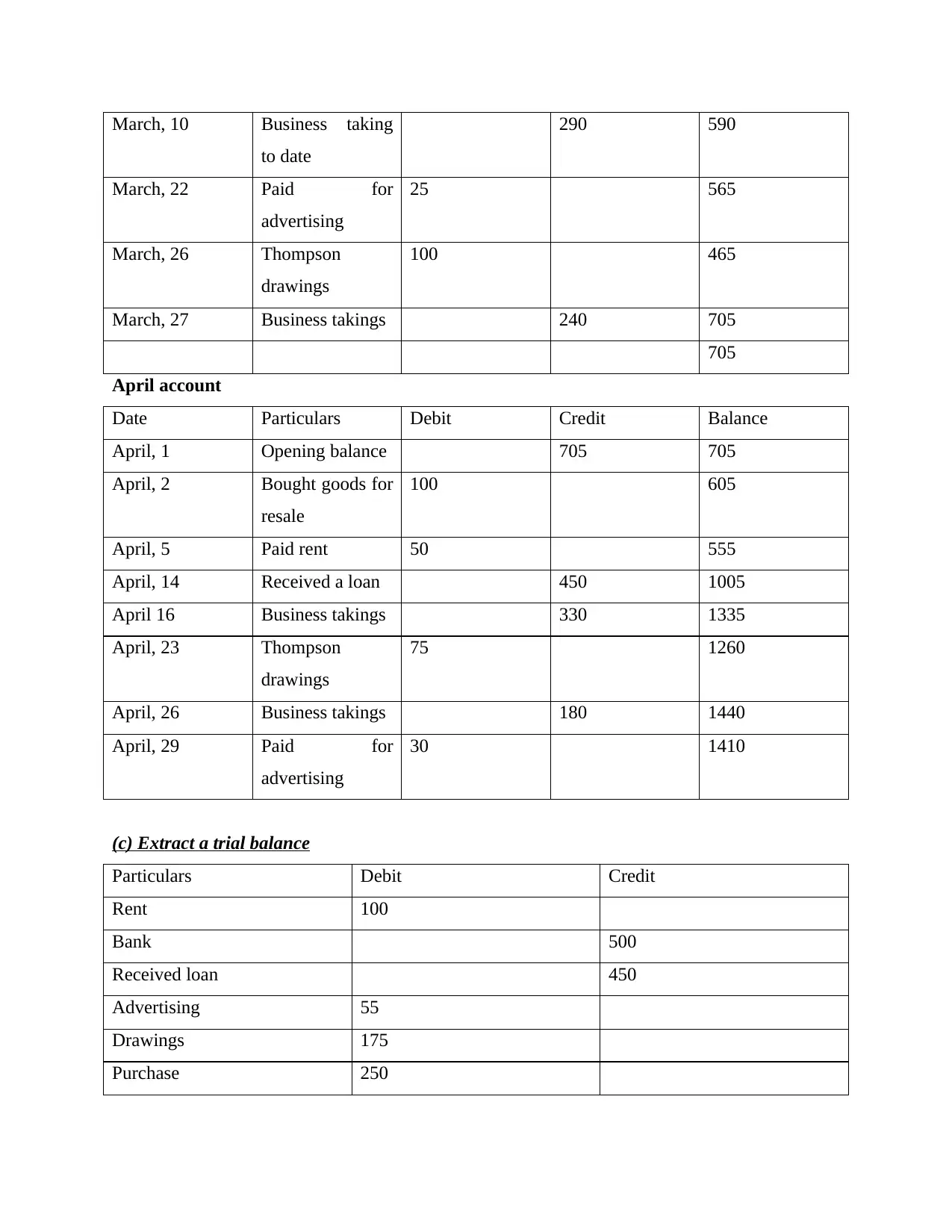

(1) March account

Date Particulars Debit Credit Balance

March, 1 Opening balance 500 500

March, 1 Bought goods for

sale

150 350

March, 5 Paid rent 50 300

Current Assets 1770 2390

Current Liabilities 560 840

Current ratio 3.16 2.84

Interpretation: According to the above estimate, the first business must achieve the optimal

ratio of 2:1 during the year and even in the 2nd tear. It create 3.16 in 1st year and 2.84 in

2nd year thus for both years the optimal ratio matches.

Trade payable period in days:

Year 1 Year 2

Trade Payable 560 840

Cost of sales 3020 4650

Trade payable period in days 67.68 days 65.93 days

Interpretation: According to the above figure, it acknowledges that in the 1st year the

company will pay the sum in the 67.78 days, although in the two year it reduces and hits on

65.93 moments that perhaps the business enterprise is not successful.

Trade receivable period

Year 1 Year 2

Trade receivable 820 1230

Total sales 4940 6850

Trade receivable period 60.59 days 65.54 days

Interpretation: From the following estimate, it is estimated that the firm earns mount

again from borrowers in 60.59 days during the first year, however in the second year it raises and

hits 65.54 days that is not favourable for the firm and affects the liquidity situation.

(2b) Business bank

(1) March account

Date Particulars Debit Credit Balance

March, 1 Opening balance 500 500

March, 1 Bought goods for

sale

150 350

March, 5 Paid rent 50 300

March, 10 Business taking

to date

290 590

March, 22 Paid for

advertising

25 565

March, 26 Thompson

drawings

100 465

March, 27 Business takings 240 705

705

April account

Date Particulars Debit Credit Balance

April, 1 Opening balance 705 705

April, 2 Bought goods for

resale

100 605

April, 5 Paid rent 50 555

April, 14 Received a loan 450 1005

April 16 Business takings 330 1335

April, 23 Thompson

drawings

75 1260

April, 26 Business takings 180 1440

April, 29 Paid for

advertising

30 1410

(c) Extract a trial balance

Particulars Debit Credit

Rent 100

Bank 500

Received loan 450

Advertising 55

Drawings 175

Purchase 250

to date

290 590

March, 22 Paid for

advertising

25 565

March, 26 Thompson

drawings

100 465

March, 27 Business takings 240 705

705

April account

Date Particulars Debit Credit Balance

April, 1 Opening balance 705 705

April, 2 Bought goods for

resale

100 605

April, 5 Paid rent 50 555

April, 14 Received a loan 450 1005

April 16 Business takings 330 1335

April, 23 Thompson

drawings

75 1260

April, 26 Business takings 180 1440

April, 29 Paid for

advertising

30 1410

(c) Extract a trial balance

Particulars Debit Credit

Rent 100

Bank 500

Received loan 450

Advertising 55

Drawings 175

Purchase 250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

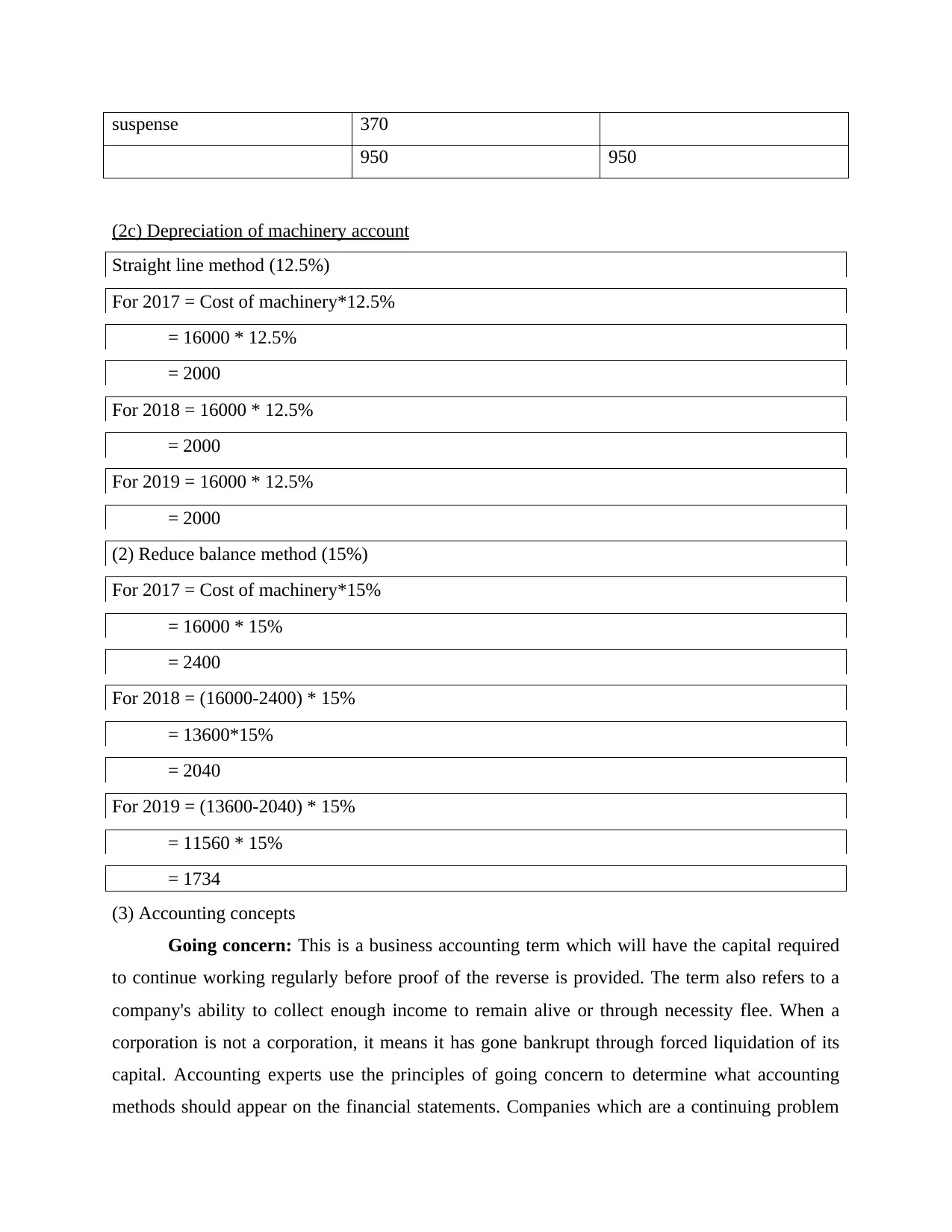

suspense 370

950 950

(2c) Depreciation of machinery account

Straight line method (12.5%)

For 2017 = Cost of machinery*12.5%

= 16000 * 12.5%

= 2000

For 2018 = 16000 * 12.5%

= 2000

For 2019 = 16000 * 12.5%

= 2000

(2) Reduce balance method (15%)

For 2017 = Cost of machinery*15%

= 16000 * 15%

= 2400

For 2018 = (16000-2400) * 15%

= 13600*15%

= 2040

For 2019 = (13600-2040) * 15%

= 11560 * 15%

= 1734

(3) Accounting concepts

Going concern: This is a business accounting term which will have the capital required

to continue working regularly before proof of the reverse is provided. The term also refers to a

company's ability to collect enough income to remain alive or through necessity flee. When a

corporation is not a corporation, it means it has gone bankrupt through forced liquidation of its

capital. Accounting experts use the principles of going concern to determine what accounting

methods should appear on the financial statements. Companies which are a continuing problem

950 950

(2c) Depreciation of machinery account

Straight line method (12.5%)

For 2017 = Cost of machinery*12.5%

= 16000 * 12.5%

= 2000

For 2018 = 16000 * 12.5%

= 2000

For 2019 = 16000 * 12.5%

= 2000

(2) Reduce balance method (15%)

For 2017 = Cost of machinery*15%

= 16000 * 15%

= 2400

For 2018 = (16000-2400) * 15%

= 13600*15%

= 2040

For 2019 = (13600-2040) * 15%

= 11560 * 15%

= 1734

(3) Accounting concepts

Going concern: This is a business accounting term which will have the capital required

to continue working regularly before proof of the reverse is provided. The term also refers to a

company's ability to collect enough income to remain alive or through necessity flee. When a

corporation is not a corporation, it means it has gone bankrupt through forced liquidation of its

capital. Accounting experts use the principles of going concern to determine what accounting

methods should appear on the financial statements. Companies which are a continuing problem

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

may postpone the reporting of long-term assets at the original expense or the price of bankruptcy,

but at further risk. A business holds an continuing dilemma because land sale does not impede its

power to perform activities, including the closing of a small division manager over several other

company units lead to a substantial staffing (Sledgianowski, Gomaa and Tan, 2017).

Materiality: transfers must be documented as negligence to do so might affect the

assessments in a viewer's financial reporting. It thought it was occurring in incredibly limited

expenditures being published, so that the operating results, financial status and working capital

of a company are correctly reflected in the financial reports. The concept or theory of

subjectivity is an accounting rule and should be accounted by using GAAP alone to define all

payments or goods which have a significant material impact on the financial. In other words, if a

cost or event happens during the year and may have an effect on how a customer perceives the

company, it should be recorded in the income statement through using GAAP (Tinoco, Holmes

and Wilson, 2018).

Business entity concept: This simply means that a company's transactions must include

a variation from those of its owners or other bodies. It requires the use of multiple financial

records in the business that completely exclude profits and expenditures of any such entity or

owner. Within this definition, the accounts of various companies would be combined, making it

extremely hard to discern the commercial or tax output of a given entity (Umar, 2017).

Description of the business organization has a number of definitions, like:

Each commercial company is exempt from taxes.

The organisation's financial performance and competitive status must be measured.

Whenever an organization is liquidated, it is necessary to determine the amount of

payments to various managers.

It is crucial to analyse the cash allocated towards such a private company in the case of a

deliberately.

A company's records could not be investigated and the records were combined with those

of other businesses and entities (Wang and Zhang, 2017).

CONCLUSION

In conclusion, various types of companies use financial accounting to assess the overall

position of the company. In this accounting firm, different types of statements are prepared to

reflect actual financial results and allow top executives to make the right decision. Trading,

but at further risk. A business holds an continuing dilemma because land sale does not impede its

power to perform activities, including the closing of a small division manager over several other

company units lead to a substantial staffing (Sledgianowski, Gomaa and Tan, 2017).

Materiality: transfers must be documented as negligence to do so might affect the

assessments in a viewer's financial reporting. It thought it was occurring in incredibly limited

expenditures being published, so that the operating results, financial status and working capital

of a company are correctly reflected in the financial reports. The concept or theory of

subjectivity is an accounting rule and should be accounted by using GAAP alone to define all

payments or goods which have a significant material impact on the financial. In other words, if a

cost or event happens during the year and may have an effect on how a customer perceives the

company, it should be recorded in the income statement through using GAAP (Tinoco, Holmes

and Wilson, 2018).

Business entity concept: This simply means that a company's transactions must include

a variation from those of its owners or other bodies. It requires the use of multiple financial

records in the business that completely exclude profits and expenditures of any such entity or

owner. Within this definition, the accounts of various companies would be combined, making it

extremely hard to discern the commercial or tax output of a given entity (Umar, 2017).

Description of the business organization has a number of definitions, like:

Each commercial company is exempt from taxes.

The organisation's financial performance and competitive status must be measured.

Whenever an organization is liquidated, it is necessary to determine the amount of

payments to various managers.

It is crucial to analyse the cash allocated towards such a private company in the case of a

deliberately.

A company's records could not be investigated and the records were combined with those

of other businesses and entities (Wang and Zhang, 2017).

CONCLUSION

In conclusion, various types of companies use financial accounting to assess the overall

position of the company. In this accounting firm, different types of statements are prepared to

reflect actual financial results and allow top executives to make the right decision. Trading,

income and expense accounts are made to assess the financial results. In this function often

measure with the advantages the research ratio and user experience functions.

measure with the advantages the research ratio and user experience functions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.