Financial Accounting Assignment Solution: UGB105, Aug 2020

VerifiedAdded on 2023/01/07

|15

|3297

|34

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting assignment, addressing key aspects of the subject. The solution begins with the preparation of a trading account, profit and loss account, and a statement of financial position for a fabric shop, demonstrating the application of fundamental accounting principles. It then evaluates the main features of financial information, explaining their importance and benefits to users. The assignment further delves into financial ratio analysis, calculating and interpreting gross profit margin, return on capital employed, current ratio, and trade payables and receivables periods. Additionally, it includes journal entries, trial balance preparation, and depreciation calculations using both straight-line and reducing balance methods. Finally, it explains the meaning and significance of key accounting concepts such as going concern, accrual basis, and consistency, providing a well-rounded understanding of financial accounting practices. The assignment is a complete solution to the UGB105 Introduction to Financial Accounting assignment.

Introduction to

Financial Accounting

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Q1a...................................................................................................................................................3

a. Prepare Trading account..........................................................................................................3

b. Prepare profit and loss account................................................................................................3

c. Draft statement of financial position........................................................................................3

Q1b. Evaluate six of main features of information for users of financial statements. Explain why

they are important and the benefits they will bring to the users......................................................4

Q2a...................................................................................................................................................7

Gross profit Margin.....................................................................................................................7

Return on capital employed.........................................................................................................7

Current ratio.................................................................................................................................8

Trade payables period in days.....................................................................................................8

Trade receivable in days..............................................................................................................9

Q2b..................................................................................................................................................9

a. Bank account............................................................................................................................9

b. All other accounts..................................................................................................................10

c. Trial balance...........................................................................................................................11

Q2c.................................................................................................................................................11

i. Straight-line method at 12.5% per annum..............................................................................11

ii. Reducing balance method at 15% per annum.......................................................................11

iii. Explain the meaning and significance of the following accounting concepts.....................12

References......................................................................................................................................15

Q1a...................................................................................................................................................3

a. Prepare Trading account..........................................................................................................3

b. Prepare profit and loss account................................................................................................3

c. Draft statement of financial position........................................................................................3

Q1b. Evaluate six of main features of information for users of financial statements. Explain why

they are important and the benefits they will bring to the users......................................................4

Q2a...................................................................................................................................................7

Gross profit Margin.....................................................................................................................7

Return on capital employed.........................................................................................................7

Current ratio.................................................................................................................................8

Trade payables period in days.....................................................................................................8

Trade receivable in days..............................................................................................................9

Q2b..................................................................................................................................................9

a. Bank account............................................................................................................................9

b. All other accounts..................................................................................................................10

c. Trial balance...........................................................................................................................11

Q2c.................................................................................................................................................11

i. Straight-line method at 12.5% per annum..............................................................................11

ii. Reducing balance method at 15% per annum.......................................................................11

iii. Explain the meaning and significance of the following accounting concepts.....................12

References......................................................................................................................................15

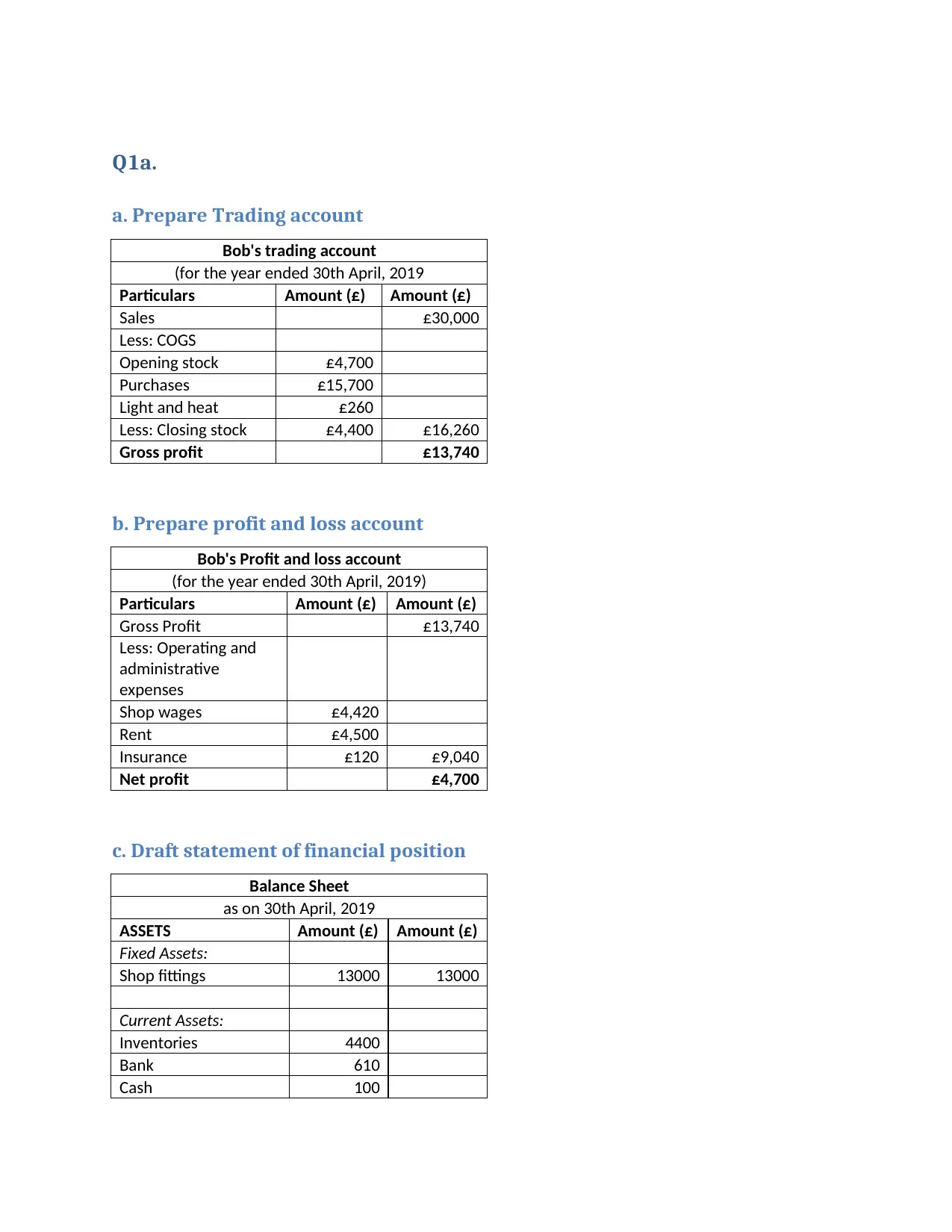

Q1a.

a. Prepare Trading account

Bob's trading account

(for the year ended 30th April, 2019

Particulars Amount (£) Amount (£)

Sales £30,000

Less: COGS

Opening stock £4,700

Purchases £15,700

Light and heat £260

Less: Closing stock £4,400 £16,260

Gross profit £13,740

b. Prepare profit and loss account

Bob's Profit and loss account

(for the year ended 30th April, 2019)

Particulars Amount (£) Amount (£)

Gross Profit £13,740

Less: Operating and

administrative

expenses

Shop wages £4,420

Rent £4,500

Insurance £120 £9,040

Net profit £4,700

c. Draft statement of financial position

Balance Sheet

as on 30th April, 2019

ASSETS Amount (£) Amount (£)

Fixed Assets:

Shop fittings 13000 13000

Current Assets:

Inventories 4400

Bank 610

Cash 100

a. Prepare Trading account

Bob's trading account

(for the year ended 30th April, 2019

Particulars Amount (£) Amount (£)

Sales £30,000

Less: COGS

Opening stock £4,700

Purchases £15,700

Light and heat £260

Less: Closing stock £4,400 £16,260

Gross profit £13,740

b. Prepare profit and loss account

Bob's Profit and loss account

(for the year ended 30th April, 2019)

Particulars Amount (£) Amount (£)

Gross Profit £13,740

Less: Operating and

administrative

expenses

Shop wages £4,420

Rent £4,500

Insurance £120 £9,040

Net profit £4,700

c. Draft statement of financial position

Balance Sheet

as on 30th April, 2019

ASSETS Amount (£) Amount (£)

Fixed Assets:

Shop fittings 13000 13000

Current Assets:

Inventories 4400

Bank 610

Cash 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

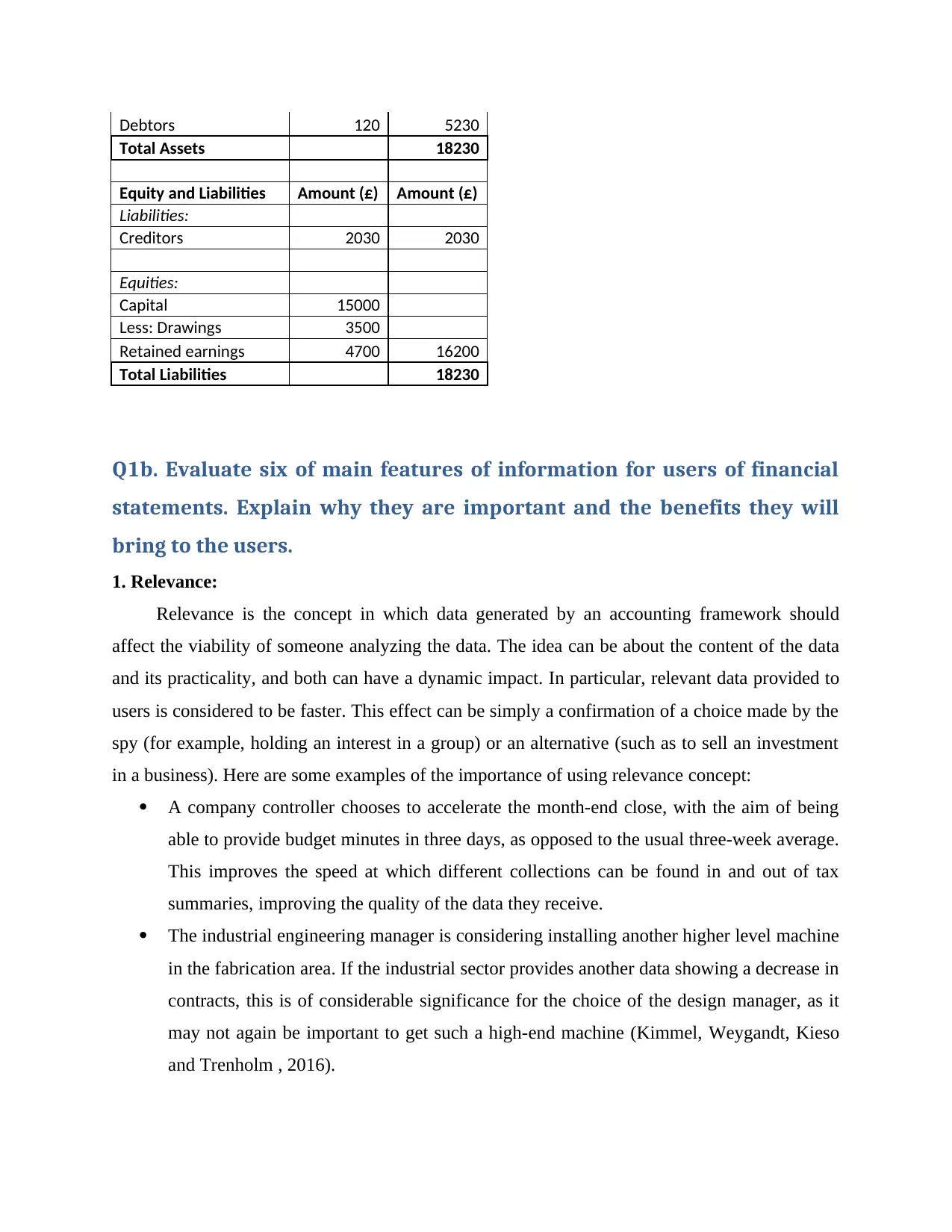

Debtors 120 5230

Total Assets 18230

Equity and Liabilities Amount (£) Amount (£)

Liabilities:

Creditors 2030 2030

Equities:

Capital 15000

Less: Drawings 3500

Retained earnings 4700 16200

Total Liabilities 18230

Q1b. Evaluate six of main features of information for users of financial

statements. Explain why they are important and the benefits they will

bring to the users.

1. Relevance:

Relevance is the concept in which data generated by an accounting framework should

affect the viability of someone analyzing the data. The idea can be about the content of the data

and its practicality, and both can have a dynamic impact. In particular, relevant data provided to

users is considered to be faster. This effect can be simply a confirmation of a choice made by the

spy (for example, holding an interest in a group) or an alternative (such as to sell an investment

in a business). Here are some examples of the importance of using relevance concept:

A company controller chooses to accelerate the month-end close, with the aim of being

able to provide budget minutes in three days, as opposed to the usual three-week average.

This improves the speed at which different collections can be found in and out of tax

summaries, improving the quality of the data they receive.

The industrial engineering manager is considering installing another higher level machine

in the fabrication area. If the industrial sector provides another data showing a decrease in

contracts, this is of considerable significance for the choice of the design manager, as it

may not again be important to get such a high-end machine (Kimmel, Weygandt, Kieso

and Trenholm , 2016).

Total Assets 18230

Equity and Liabilities Amount (£) Amount (£)

Liabilities:

Creditors 2030 2030

Equities:

Capital 15000

Less: Drawings 3500

Retained earnings 4700 16200

Total Liabilities 18230

Q1b. Evaluate six of main features of information for users of financial

statements. Explain why they are important and the benefits they will

bring to the users.

1. Relevance:

Relevance is the concept in which data generated by an accounting framework should

affect the viability of someone analyzing the data. The idea can be about the content of the data

and its practicality, and both can have a dynamic impact. In particular, relevant data provided to

users is considered to be faster. This effect can be simply a confirmation of a choice made by the

spy (for example, holding an interest in a group) or an alternative (such as to sell an investment

in a business). Here are some examples of the importance of using relevance concept:

A company controller chooses to accelerate the month-end close, with the aim of being

able to provide budget minutes in three days, as opposed to the usual three-week average.

This improves the speed at which different collections can be found in and out of tax

summaries, improving the quality of the data they receive.

The industrial engineering manager is considering installing another higher level machine

in the fabrication area. If the industrial sector provides another data showing a decrease in

contracts, this is of considerable significance for the choice of the design manager, as it

may not again be important to get such a high-end machine (Kimmel, Weygandt, Kieso

and Trenholm , 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Reliability:

The reliability includes ensuring that all exchanges, opportunities, and transactions

included in balance sheets are reliable. Information is considered to be an opportunity that cannot

be analyzed, verified, and tested with targeted tests.

3. Understandability:

Understandability is the concept that balance sheet data should be included is

understandable with the aim that a user can appreciate them without too much difficulty. This

idea embraces meaningful business intelligence from the consumer, but does not require

advanced commercial intelligence to maximize value. Adhering to a reasonable level of

understanding would prevent a society from deliberately tampering with money-related data in

order to remove messengers from their balance sheets. Early comments do not mean that baffling

data should be excluded from balance sheets. For example, the ideas identified by annuities and

subsidiaries are difficult to understand. In these cases, use the notion of comprehension for as

long as is expected, but at the same time present the necessary data.

4. Comparability:

Financial statements of one accounting period must be substantially comparable to another

company's accounting information so that customers can make important decisions about money

presentation and content placement patterns over time. The appearance of tax reports on different

accounting periods can be ascertained using comparative accounting methods over time

(Kimmel, Weygandt, Kieso and Trenholm, 2016).

A change in accounting strategies may be required for an element that improves the

dependency and adequacy of tax summaries. A change in accounting strategy can also be

brought about by changes in accounting practices. In these terms, the nature and conditions that

determine the change must be disclosed in the financial statements.

5. Consistency:

In accounting, consistency requires that organization tax reports follow accounting

standards, strategies, practices and procedures, starting with one accounting period and then the

The reliability includes ensuring that all exchanges, opportunities, and transactions

included in balance sheets are reliable. Information is considered to be an opportunity that cannot

be analyzed, verified, and tested with targeted tests.

3. Understandability:

Understandability is the concept that balance sheet data should be included is

understandable with the aim that a user can appreciate them without too much difficulty. This

idea embraces meaningful business intelligence from the consumer, but does not require

advanced commercial intelligence to maximize value. Adhering to a reasonable level of

understanding would prevent a society from deliberately tampering with money-related data in

order to remove messengers from their balance sheets. Early comments do not mean that baffling

data should be excluded from balance sheets. For example, the ideas identified by annuities and

subsidiaries are difficult to understand. In these cases, use the notion of comprehension for as

long as is expected, but at the same time present the necessary data.

4. Comparability:

Financial statements of one accounting period must be substantially comparable to another

company's accounting information so that customers can make important decisions about money

presentation and content placement patterns over time. The appearance of tax reports on different

accounting periods can be ascertained using comparative accounting methods over time

(Kimmel, Weygandt, Kieso and Trenholm, 2016).

A change in accounting strategies may be required for an element that improves the

dependency and adequacy of tax summaries. A change in accounting strategy can also be

brought about by changes in accounting practices. In these terms, the nature and conditions that

determine the change must be disclosed in the financial statements.

5. Consistency:

In accounting, consistency requires that organization tax reports follow accounting

standards, strategies, practices and procedures, starting with one accounting period and then the

next. This allows balance sheet users to make important reviews between years (Kimmel,

Weygandt, Kieso, and Trenholm, 2016).

Consistency allows an organization to implement a preferred accounting method.

However, the change and its impact must be demonstrated to support users of tax summaries.

6. Neutrality:

It implies that fiscal reports must be free from errors or from other biases. Budget reports can't be

set up with the reason to impact certain choices, for example they may be nonpartisan. Clients of

the bookkeeping information ought to have the capacity or plausibility to settle on their own

choices dependent on that data.

Importance of accounting informations:

1. Accounting data is important for evaluating the application of various businesses. Despite

the fact that expense reports are the accounting information tool used to evaluate

businesses, business owners can examine this information more closely as they evaluate

businesses. Respond in cash by using accounting information with explanations of

charges and dividing it into guidance signals.

2. Business owners regularly use accounting information to do money-related planning for

their associations. Information on tax evasion verification provides entrepreneurs with a

top-down analysis of how their associations have spent money on specific business

capabilities. Entrepreneurs often take this accounting information and pass the future

through projects to secure operators money for their associations. These money-related

plans can also be modified by relying on standard accounting information to ensure that a

business owner doesn't stop spending on the underlying assets.

3. Accounting information is commonly used to determine business preferences. To the

detriment of executives, the importance of finance and accounting gives the industry an

important focus. Other options may include the growth of a conventional facility, the use

of various financial resources, the purchase of new equipment or workplaces, compliance

with future agreements or entering into experimentation with new business openings.

Weygandt, Kieso, and Trenholm, 2016).

Consistency allows an organization to implement a preferred accounting method.

However, the change and its impact must be demonstrated to support users of tax summaries.

6. Neutrality:

It implies that fiscal reports must be free from errors or from other biases. Budget reports can't be

set up with the reason to impact certain choices, for example they may be nonpartisan. Clients of

the bookkeeping information ought to have the capacity or plausibility to settle on their own

choices dependent on that data.

Importance of accounting informations:

1. Accounting data is important for evaluating the application of various businesses. Despite

the fact that expense reports are the accounting information tool used to evaluate

businesses, business owners can examine this information more closely as they evaluate

businesses. Respond in cash by using accounting information with explanations of

charges and dividing it into guidance signals.

2. Business owners regularly use accounting information to do money-related planning for

their associations. Information on tax evasion verification provides entrepreneurs with a

top-down analysis of how their associations have spent money on specific business

capabilities. Entrepreneurs often take this accounting information and pass the future

through projects to secure operators money for their associations. These money-related

plans can also be modified by relying on standard accounting information to ensure that a

business owner doesn't stop spending on the underlying assets.

3. Accounting information is commonly used to determine business preferences. To the

detriment of executives, the importance of finance and accounting gives the industry an

important focus. Other options may include the growth of a conventional facility, the use

of various financial resources, the purchase of new equipment or workplaces, compliance

with future agreements or entering into experimentation with new business openings.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Foreign exchange brokers often use accounting information to draw theoretical

conclusions. Banks, loan experts, financial analysts, or private theorists often break down

the collection of accounting information to determine budget quality and operating profit.

This suggests that an autonomous group is a theoretical choice (Yu, Lin and Tang, 2018).

Benefits of accounting information:

1. Increased automation - more consistent output and fewer resources (people) needs

2. Better information - this is important for strategic decision-making

3. Faster turnaround times - this is important for compliance filing as well as

management reporting. For the latter, stale data is not helpful in making strategic

decisions (Kolitz, 2016).

4. Connectivity & flexibility - this allows for increased automation, greater flexibility in

data gathering and reporting and the ability to connect financial and non-financial data

(Kolitz, 2016).

Q2a.

Gross profit Margin

Gross profit margin

Year 1 Year 2

Gross profit £1,920 £2,200

Net Sales £4,940 £6,850

Gross profit margin (a/b)

38.866

%

32.117

%

Interpretation: The above calculation of gross profit margin for two consecutive years shows

that in Year 1 company has records more gross profit margin compares to second year and hence

this indicates poor performance records by the company in Year 2 (Dauderies and Annand,

2019).

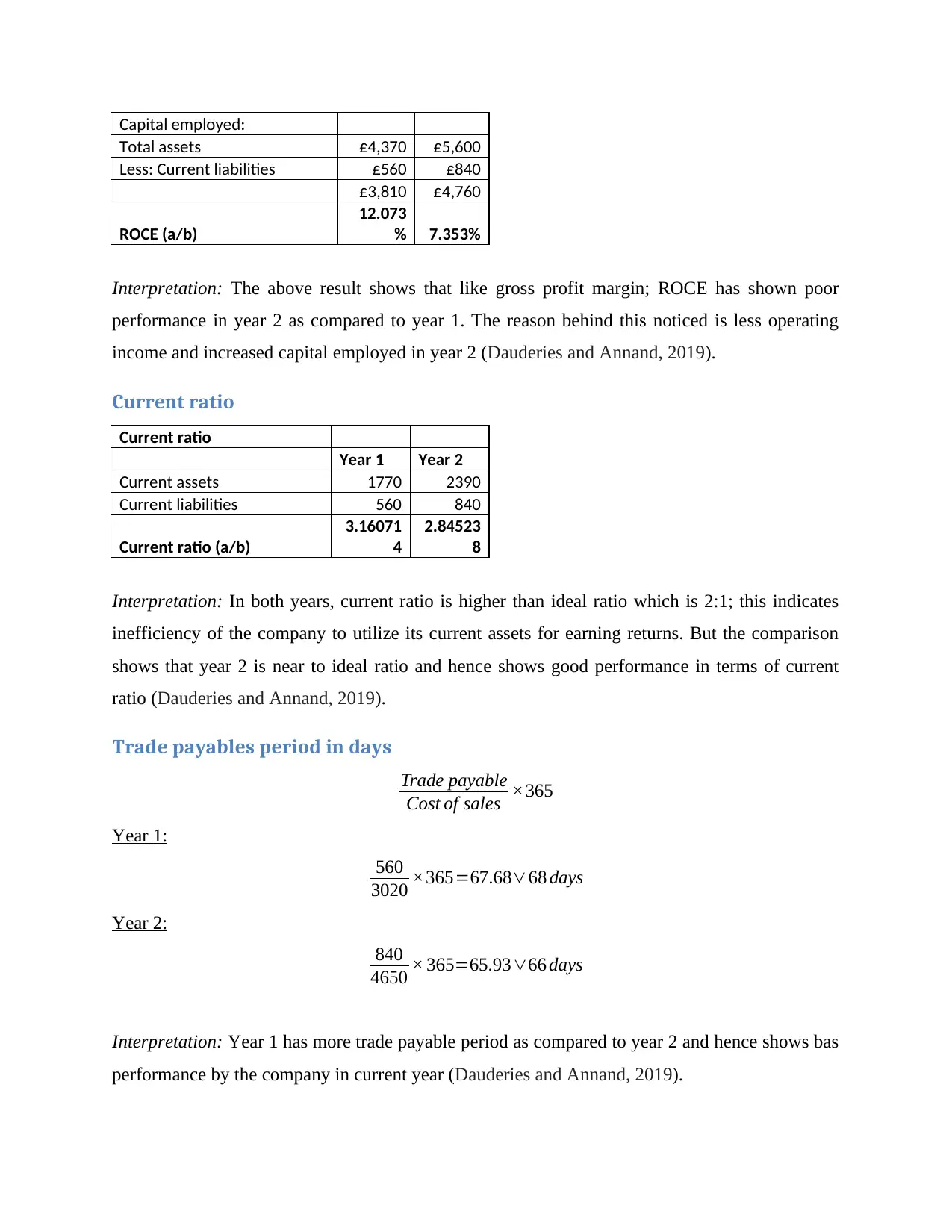

Return on capital employed

Return on capital employed

Year 1 Year 2

Operating profit £460 £350

conclusions. Banks, loan experts, financial analysts, or private theorists often break down

the collection of accounting information to determine budget quality and operating profit.

This suggests that an autonomous group is a theoretical choice (Yu, Lin and Tang, 2018).

Benefits of accounting information:

1. Increased automation - more consistent output and fewer resources (people) needs

2. Better information - this is important for strategic decision-making

3. Faster turnaround times - this is important for compliance filing as well as

management reporting. For the latter, stale data is not helpful in making strategic

decisions (Kolitz, 2016).

4. Connectivity & flexibility - this allows for increased automation, greater flexibility in

data gathering and reporting and the ability to connect financial and non-financial data

(Kolitz, 2016).

Q2a.

Gross profit Margin

Gross profit margin

Year 1 Year 2

Gross profit £1,920 £2,200

Net Sales £4,940 £6,850

Gross profit margin (a/b)

38.866

%

32.117

%

Interpretation: The above calculation of gross profit margin for two consecutive years shows

that in Year 1 company has records more gross profit margin compares to second year and hence

this indicates poor performance records by the company in Year 2 (Dauderies and Annand,

2019).

Return on capital employed

Return on capital employed

Year 1 Year 2

Operating profit £460 £350

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital employed:

Total assets £4,370 £5,600

Less: Current liabilities £560 £840

£3,810 £4,760

ROCE (a/b)

12.073

% 7.353%

Interpretation: The above result shows that like gross profit margin; ROCE has shown poor

performance in year 2 as compared to year 1. The reason behind this noticed is less operating

income and increased capital employed in year 2 (Dauderies and Annand, 2019).

Current ratio

Current ratio

Year 1 Year 2

Current assets 1770 2390

Current liabilities 560 840

Current ratio (a/b)

3.16071

4

2.84523

8

Interpretation: In both years, current ratio is higher than ideal ratio which is 2:1; this indicates

inefficiency of the company to utilize its current assets for earning returns. But the comparison

shows that year 2 is near to ideal ratio and hence shows good performance in terms of current

ratio (Dauderies and Annand, 2019).

Trade payables period in days

Trade payable

Cost of sales ×365

Year 1:

560

3020 ×365=67.68∨68 days

Year 2:

840

4650 × 365=65.93∨66 days

Interpretation: Year 1 has more trade payable period as compared to year 2 and hence shows bas

performance by the company in current year (Dauderies and Annand, 2019).

Total assets £4,370 £5,600

Less: Current liabilities £560 £840

£3,810 £4,760

ROCE (a/b)

12.073

% 7.353%

Interpretation: The above result shows that like gross profit margin; ROCE has shown poor

performance in year 2 as compared to year 1. The reason behind this noticed is less operating

income and increased capital employed in year 2 (Dauderies and Annand, 2019).

Current ratio

Current ratio

Year 1 Year 2

Current assets 1770 2390

Current liabilities 560 840

Current ratio (a/b)

3.16071

4

2.84523

8

Interpretation: In both years, current ratio is higher than ideal ratio which is 2:1; this indicates

inefficiency of the company to utilize its current assets for earning returns. But the comparison

shows that year 2 is near to ideal ratio and hence shows good performance in terms of current

ratio (Dauderies and Annand, 2019).

Trade payables period in days

Trade payable

Cost of sales ×365

Year 1:

560

3020 ×365=67.68∨68 days

Year 2:

840

4650 × 365=65.93∨66 days

Interpretation: Year 1 has more trade payable period as compared to year 2 and hence shows bas

performance by the company in current year (Dauderies and Annand, 2019).

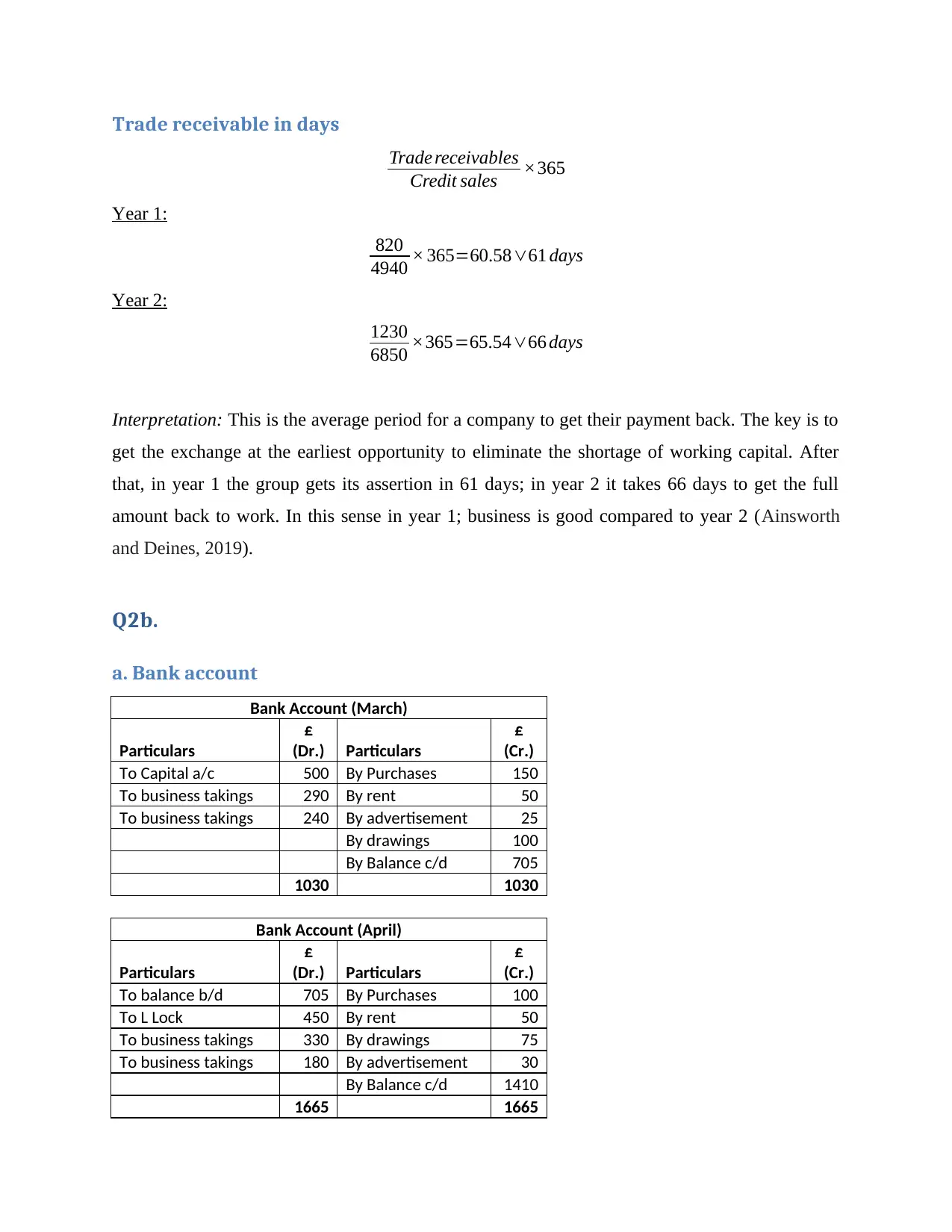

Trade receivable in days

Trade receivables

Credit sales ×365

Year 1:

820

4940 × 365=60.58∨61 days

Year 2:

1230

6850 ×365=65.54∨66 days

Interpretation: This is the average period for a company to get their payment back. The key is to

get the exchange at the earliest opportunity to eliminate the shortage of working capital. After

that, in year 1 the group gets its assertion in 61 days; in year 2 it takes 66 days to get the full

amount back to work. In this sense in year 1; business is good compared to year 2 (Ainsworth

and Deines, 2019).

Q2b.

a. Bank account

Bank Account (March)

Particulars

£

(Dr.) Particulars

£

(Cr.)

To Capital a/c 500 By Purchases 150

To business takings 290 By rent 50

To business takings 240 By advertisement 25

By drawings 100

By Balance c/d 705

1030 1030

Bank Account (April)

Particulars

£

(Dr.) Particulars

£

(Cr.)

To balance b/d 705 By Purchases 100

To L Lock 450 By rent 50

To business takings 330 By drawings 75

To business takings 180 By advertisement 30

By Balance c/d 1410

1665 1665

Trade receivables

Credit sales ×365

Year 1:

820

4940 × 365=60.58∨61 days

Year 2:

1230

6850 ×365=65.54∨66 days

Interpretation: This is the average period for a company to get their payment back. The key is to

get the exchange at the earliest opportunity to eliminate the shortage of working capital. After

that, in year 1 the group gets its assertion in 61 days; in year 2 it takes 66 days to get the full

amount back to work. In this sense in year 1; business is good compared to year 2 (Ainsworth

and Deines, 2019).

Q2b.

a. Bank account

Bank Account (March)

Particulars

£

(Dr.) Particulars

£

(Cr.)

To Capital a/c 500 By Purchases 150

To business takings 290 By rent 50

To business takings 240 By advertisement 25

By drawings 100

By Balance c/d 705

1030 1030

Bank Account (April)

Particulars

£

(Dr.) Particulars

£

(Cr.)

To balance b/d 705 By Purchases 100

To L Lock 450 By rent 50

To business takings 330 By drawings 75

To business takings 180 By advertisement 30

By Balance c/d 1410

1665 1665

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

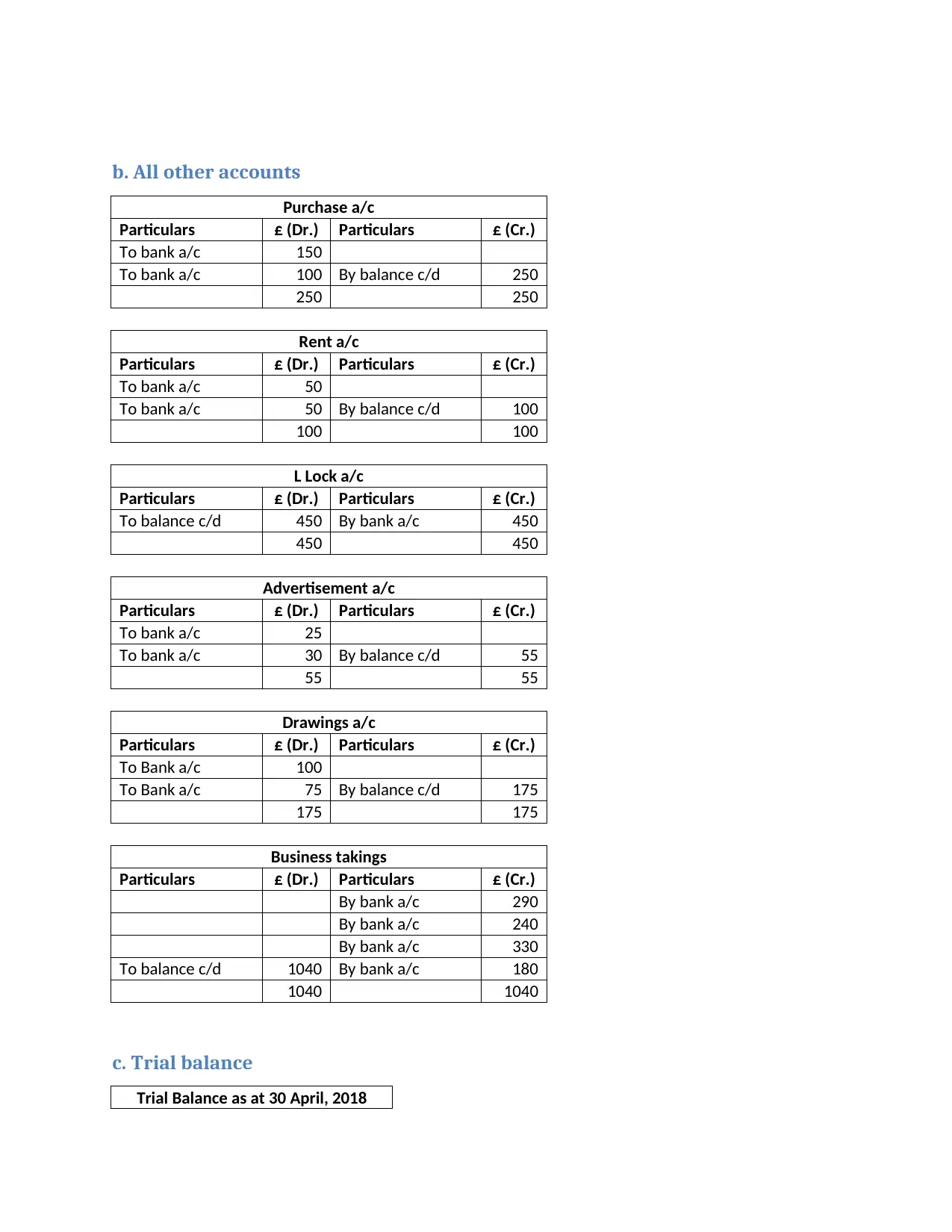

b. All other accounts

Purchase a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 150

To bank a/c 100 By balance c/d 250

250 250

Rent a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 50

To bank a/c 50 By balance c/d 100

100 100

L Lock a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To balance c/d 450 By bank a/c 450

450 450

Advertisement a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 25

To bank a/c 30 By balance c/d 55

55 55

Drawings a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To Bank a/c 100

To Bank a/c 75 By balance c/d 175

175 175

Business takings

Particulars £ (Dr.) Particulars £ (Cr.)

By bank a/c 290

By bank a/c 240

By bank a/c 330

To balance c/d 1040 By bank a/c 180

1040 1040

c. Trial balance

Trial Balance as at 30 April, 2018

Purchase a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 150

To bank a/c 100 By balance c/d 250

250 250

Rent a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 50

To bank a/c 50 By balance c/d 100

100 100

L Lock a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To balance c/d 450 By bank a/c 450

450 450

Advertisement a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 25

To bank a/c 30 By balance c/d 55

55 55

Drawings a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To Bank a/c 100

To Bank a/c 75 By balance c/d 175

175 175

Business takings

Particulars £ (Dr.) Particulars £ (Cr.)

By bank a/c 290

By bank a/c 240

By bank a/c 330

To balance c/d 1040 By bank a/c 180

1040 1040

c. Trial balance

Trial Balance as at 30 April, 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Dr. Cr.

Bank £1,410

Purchases £250

Rent £100

Capital a/c £500

L Lock £450

Advertisement £55

Drawings £175

Business takings £1,040

£1,990 £1,990

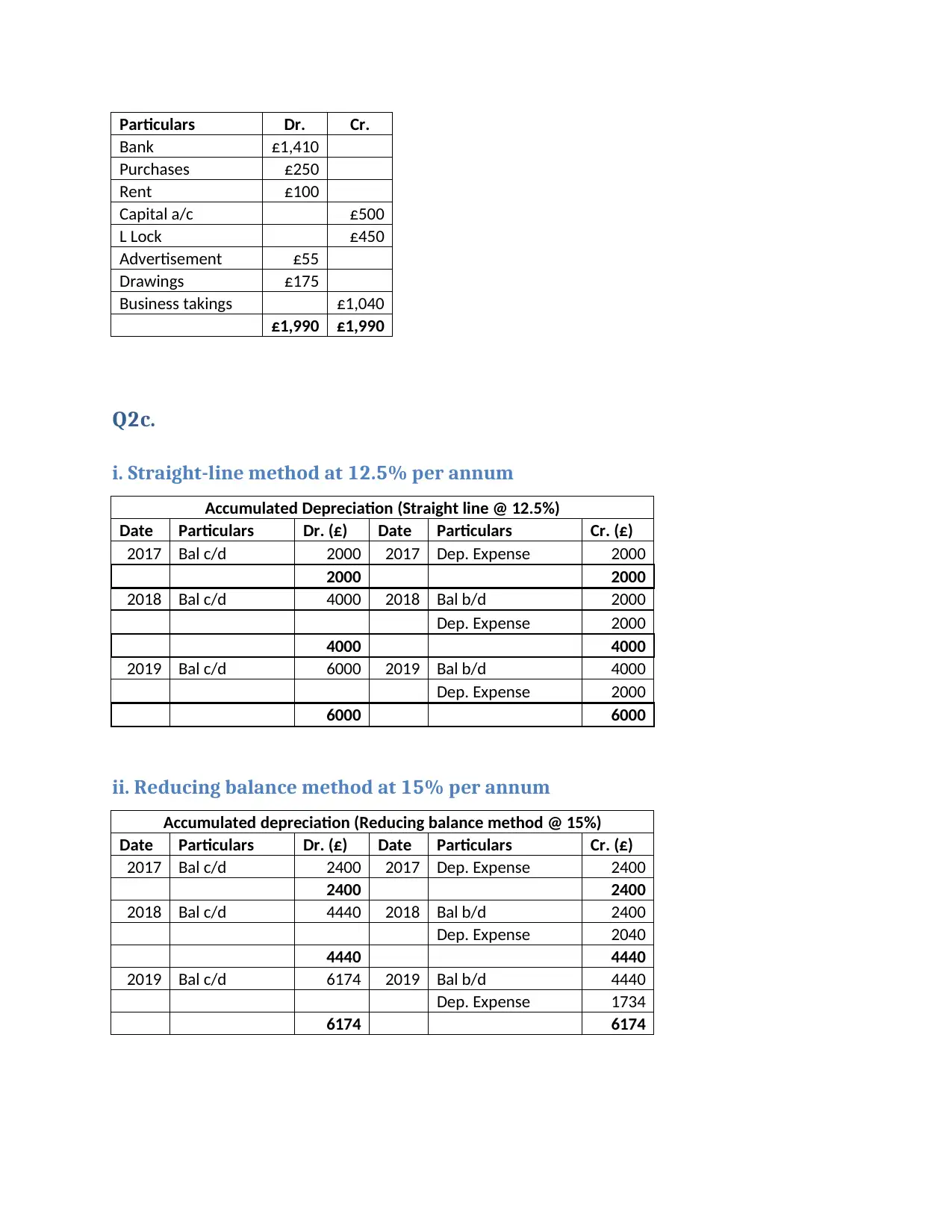

Q2c.

i. Straight-line method at 12.5% per annum

Accumulated Depreciation (Straight line @ 12.5%)

Date Particulars Dr. (£) Date Particulars Cr. (£)

2017 Bal c/d 2000 2017 Dep. Expense 2000

2000 2000

2018 Bal c/d 4000 2018 Bal b/d 2000

Dep. Expense 2000

4000 4000

2019 Bal c/d 6000 2019 Bal b/d 4000

Dep. Expense 2000

6000 6000

ii. Reducing balance method at 15% per annum

Accumulated depreciation (Reducing balance method @ 15%)

Date Particulars Dr. (£) Date Particulars Cr. (£)

2017 Bal c/d 2400 2017 Dep. Expense 2400

2400 2400

2018 Bal c/d 4440 2018 Bal b/d 2400

Dep. Expense 2040

4440 4440

2019 Bal c/d 6174 2019 Bal b/d 4440

Dep. Expense 1734

6174 6174

Bank £1,410

Purchases £250

Rent £100

Capital a/c £500

L Lock £450

Advertisement £55

Drawings £175

Business takings £1,040

£1,990 £1,990

Q2c.

i. Straight-line method at 12.5% per annum

Accumulated Depreciation (Straight line @ 12.5%)

Date Particulars Dr. (£) Date Particulars Cr. (£)

2017 Bal c/d 2000 2017 Dep. Expense 2000

2000 2000

2018 Bal c/d 4000 2018 Bal b/d 2000

Dep. Expense 2000

4000 4000

2019 Bal c/d 6000 2019 Bal b/d 4000

Dep. Expense 2000

6000 6000

ii. Reducing balance method at 15% per annum

Accumulated depreciation (Reducing balance method @ 15%)

Date Particulars Dr. (£) Date Particulars Cr. (£)

2017 Bal c/d 2400 2017 Dep. Expense 2400

2400 2400

2018 Bal c/d 4440 2018 Bal b/d 2400

Dep. Expense 2040

4440 4440

2019 Bal c/d 6174 2019 Bal b/d 4440

Dep. Expense 1734

6174 6174

iii. Explain the meaning and significance of the following accounting concepts

Going Concern

Meaning:

The going concern concept of accounting suggests that the content of the business will continue

with its activities later and will not sell or discontinue activity as a result of any explanation. An

organization works if there is no evidence to accept that it will stop or must stop its activity in

the future (Horngren, Sundem, Elliott & Philbrick, 2002).

Significance:

Going concern is an important part of reasonable accounting rules. Without it, societies

would not be able to control accrued or prepaid expenses.

A model that shows the direct use of business in progress is the estimate of the reduction in

government support. This start-up is based on the prevailing advantage, rather than the

conventional market signal. The associations expect that they will continue to work indefinitely

and that their benefits will be used in the industry until they are completely rejected.

The accounting guidance serves a very useful purpose in regulating how associations carry

out their budgetary activities. It is important that all associations screen their own expense

reports and ensure that they are prepared in a competent and appropriate manner (Horngren,

Sundem, Elliott & Philbrick, 2002).

Materiality

Meaning:

In accounting, materiality refers to the effect of excluding or misinforming data in an

organization's financial statements summaries on the customer of such announcements. At the

point where it is unlikely that the clients of the financial statements have changed their actions on

the off chance that the data had not been excluded or misused, at that point the something is seen

as material. Since clients would not change their actions, the ban or misquote should be

meaningless at that time (Horngren, Sundem, Elliott & Philbrick, 2002).

Significance:

Going Concern

Meaning:

The going concern concept of accounting suggests that the content of the business will continue

with its activities later and will not sell or discontinue activity as a result of any explanation. An

organization works if there is no evidence to accept that it will stop or must stop its activity in

the future (Horngren, Sundem, Elliott & Philbrick, 2002).

Significance:

Going concern is an important part of reasonable accounting rules. Without it, societies

would not be able to control accrued or prepaid expenses.

A model that shows the direct use of business in progress is the estimate of the reduction in

government support. This start-up is based on the prevailing advantage, rather than the

conventional market signal. The associations expect that they will continue to work indefinitely

and that their benefits will be used in the industry until they are completely rejected.

The accounting guidance serves a very useful purpose in regulating how associations carry

out their budgetary activities. It is important that all associations screen their own expense

reports and ensure that they are prepared in a competent and appropriate manner (Horngren,

Sundem, Elliott & Philbrick, 2002).

Materiality

Meaning:

In accounting, materiality refers to the effect of excluding or misinforming data in an

organization's financial statements summaries on the customer of such announcements. At the

point where it is unlikely that the clients of the financial statements have changed their actions on

the off chance that the data had not been excluded or misused, at that point the something is seen

as material. Since clients would not change their actions, the ban or misquote should be

meaningless at that time (Horngren, Sundem, Elliott & Philbrick, 2002).

Significance:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.