Financial Accounting Analysis and Report of Soar Retail Business

VerifiedAdded on 2023/06/18

|11

|2734

|246

Report

AI Summary

This report provides a comprehensive financial accounting analysis of Soar, a retail business in the UK, focusing on events that occurred in June 2021. It includes explanations of various business activities such as sales, sales returns, purchases, purchase returns, cash receipts, and cash payments, along with their respective accounting treatments. The report details the updating of records and reports, including sales books, cash receipt books, purchase books, and purchase returns day books. Furthermore, it presents ledger accounts and explains the principle of prudence in accounting, emphasizing the importance of cautious revenue and expense recognition. The analysis covers examples of how the prudence principle is applied in inventory valuation, revenue recognition, and the treatment of bad debts. The report concludes that accounting is essential for businesses to determine their financial standing and facilitate product design assessment and forecasting.

Introduction to Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Accounting has changed over time in response to changing perceptions of the field's

requirements. Accounting has evolved in a lot of formats in various countries and situations. As

a result, the term accounting does not have a singular definition. Accounting, in broader, exists to

serve a variety of people who interact with businesses, including management, owners, creditors,

workers, vendors, consumers, authorities, and the public at large (Widiastuti, Sukmana and

Hady, 2021). This report based on the Soar which is retail business and established in UK. In this

report consist of explanations of events occurred in business during the financial year. Along

with record all the events in cash flow, ledger and income statement as per their nature. At the

end of the report define principle of prudence to owner in regard of the financial reports.

MAIN BODY

Short explanations of events that occurred in June 2021

An accounting event is an activity that is recorded in an accounting framework. Every

economic event that has an influence on a company’s cash must be recorded in its financial

statements. There are mentioned different events that occurred in Soar in the month of June 2021

these are:

Sales: A Sale Event is the sale of a substantial amount of funds shares or property of a Company

or an Affiliate of such Subsidiary, as decided by the Allocating Committee and approved to by a

plurality of the Board of Directors, such approval not to be unduly delayed, restricted, or

postponed (Blizkiy, Malinenko and Lebedinskaya, 2021). This event occurs in the business when

company selling different items to their customers as per their requirement these are:

2nd June selling goods in 1400 to Mild

5th June selling goods in 1200 to Tup

11th June selling goods in 5700 to Warm

24th June selling goods in 2060 to Wet

Sales return: Customers will return required item to the firm for a variety of reasons, including

receiving the incorrect product, receiving delayed payment, or receiving things that are defective

or faulty (Buszko and Ciechan-Kujawa, 2020). The account for sales depreciation and

Accounting has changed over time in response to changing perceptions of the field's

requirements. Accounting has evolved in a lot of formats in various countries and situations. As

a result, the term accounting does not have a singular definition. Accounting, in broader, exists to

serve a variety of people who interact with businesses, including management, owners, creditors,

workers, vendors, consumers, authorities, and the public at large (Widiastuti, Sukmana and

Hady, 2021). This report based on the Soar which is retail business and established in UK. In this

report consist of explanations of events occurred in business during the financial year. Along

with record all the events in cash flow, ledger and income statement as per their nature. At the

end of the report define principle of prudence to owner in regard of the financial reports.

MAIN BODY

Short explanations of events that occurred in June 2021

An accounting event is an activity that is recorded in an accounting framework. Every

economic event that has an influence on a company’s cash must be recorded in its financial

statements. There are mentioned different events that occurred in Soar in the month of June 2021

these are:

Sales: A Sale Event is the sale of a substantial amount of funds shares or property of a Company

or an Affiliate of such Subsidiary, as decided by the Allocating Committee and approved to by a

plurality of the Board of Directors, such approval not to be unduly delayed, restricted, or

postponed (Blizkiy, Malinenko and Lebedinskaya, 2021). This event occurs in the business when

company selling different items to their customers as per their requirement these are:

2nd June selling goods in 1400 to Mild

5th June selling goods in 1200 to Tup

11th June selling goods in 5700 to Warm

24th June selling goods in 2060 to Wet

Sales return: Customers will return required item to the firm for a variety of reasons, including

receiving the incorrect product, receiving delayed payment, or receiving things that are defective

or faulty (Buszko and Ciechan-Kujawa, 2020). The account for sales depreciation and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amortization is the opposite of the account for sales revenues. In this event mention those

transactions which was rerunning by the customers after selling due to any defect these are:

16 June received selling goods from Cold, 1200

20 June received selling goods from Freeze, 1500

Purchase: In the events variable, the purchase event is a number. This number is important for

businesses who wish to track the money generated by their website. It is very reliant on the

purchased and item factors. This event is playing important role in retail business because it is

main pillar to operate business for effective manner (Nurdiansyah and et.al, 2021). There are

defined those transactions which are occurred in the month of June such as:

5th June purchase by Dark in 2650

6th June purchased goods by Night in 1400

8th June purchased goods by Lin in 2000

10th June purchased goods by Night in 870

Purchase return: Whenever the consumer of commodities, inventories, fixed assets, or other

objects returns the commodities to the seller, this is known as a transaction return. Purchase

refunds can occur for a variety of reasons, including: The consumer purchased an inordinate

amount and would like to recover the remaining (Safari Sarchah, Yazdifar and Pifeh, 2020). The

consumer made a mistake and bought the wrong item. Whenever a buyer of commodities,

inventories, capital assets, or other objects returns the items to the seller, this is known as a

purchase return.

On 9th June returned goods to Dark by amount 2650

On 18th June returned goods to Ray by amount 2200

Cash receipt: All the cash activities in the business of Sour occurred in the month of June from

the different clients underneath as:

12 June take cash from Wind 4600 and allowed discount about 400

14 June selling goods to customer in 920

18 June cash received from Mild for selling in 1300 and provide discount 100

20 June received loan from customers in 20000

transactions which was rerunning by the customers after selling due to any defect these are:

16 June received selling goods from Cold, 1200

20 June received selling goods from Freeze, 1500

Purchase: In the events variable, the purchase event is a number. This number is important for

businesses who wish to track the money generated by their website. It is very reliant on the

purchased and item factors. This event is playing important role in retail business because it is

main pillar to operate business for effective manner (Nurdiansyah and et.al, 2021). There are

defined those transactions which are occurred in the month of June such as:

5th June purchase by Dark in 2650

6th June purchased goods by Night in 1400

8th June purchased goods by Lin in 2000

10th June purchased goods by Night in 870

Purchase return: Whenever the consumer of commodities, inventories, fixed assets, or other

objects returns the commodities to the seller, this is known as a transaction return. Purchase

refunds can occur for a variety of reasons, including: The consumer purchased an inordinate

amount and would like to recover the remaining (Safari Sarchah, Yazdifar and Pifeh, 2020). The

consumer made a mistake and bought the wrong item. Whenever a buyer of commodities,

inventories, capital assets, or other objects returns the items to the seller, this is known as a

purchase return.

On 9th June returned goods to Dark by amount 2650

On 18th June returned goods to Ray by amount 2200

Cash receipt: All the cash activities in the business of Sour occurred in the month of June from

the different clients underneath as:

12 June take cash from Wind 4600 and allowed discount about 400

14 June selling goods to customer in 920

18 June cash received from Mild for selling in 1300 and provide discount 100

20 June received loan from customers in 20000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25 June selling goods to customer in 3400

27 June selling goods to customer in 2500

Cash payment: People who do not have a bank account or who are looking to avoid declaring a

taxable income preferred cash payments (Mustafa, 2020). In an inflationary climate, cash

payments in a hard currency are preferable since all these resources maintain their worth

significantly better than just the domestic currency, which is vulnerable to hyperinflation.

On 10th June payment rent in cash in 4100

On 12th June payment to Dark by 2500 with 150 discount

14th June payment to Shadow 820 with 60 discounts

Carriage inward: Carriage inwards relates to the service fees that the buyer must pay while

receiving items that were bought FOB shipment location. Freight-in or mass transit are other

terms for carriage inwards. The price of carriage inwards is included in the price of the products

ordered.

Return outward: Return items are products that are refunded to the vendor by a consumer. They

are items that were formerly acquired from third parties but were restored to them but they were

unsuitable; they are also known as Purchase returns. Outward returns lower a company's overall

accounting records (Sinaga and et.al, 2021).

Wages expenses: Wages expenditure refers to the cost of hourly pay earned by a business for its

hourly employees. This may be one of a company's biggest expenditures, especially in areas like

transportation and manufacturing where there are a lot of hourly workers. Based on the amount

of extra given, wage expenses might fluctuate significantly from month to period. Due to the

different volume of work hours in each monthly, it might also vary by time. Based on the needs

of weekends and the overall amount of days in the month, certain monthly may have as few as

18 days at work, whereas others have as many as 23.

Rent: The account Rent Expense will bear the value of spaces as during time frame specified in

the revenue document's header, whether or not rent was collected inside that time, underneath the

accrual system of accounting. (Rent received in excess is recorded in the current asset category

Prepaid Rent on the balance sheet.) Total Expenses may show on the income statement as either

27 June selling goods to customer in 2500

Cash payment: People who do not have a bank account or who are looking to avoid declaring a

taxable income preferred cash payments (Mustafa, 2020). In an inflationary climate, cash

payments in a hard currency are preferable since all these resources maintain their worth

significantly better than just the domestic currency, which is vulnerable to hyperinflation.

On 10th June payment rent in cash in 4100

On 12th June payment to Dark by 2500 with 150 discount

14th June payment to Shadow 820 with 60 discounts

Carriage inward: Carriage inwards relates to the service fees that the buyer must pay while

receiving items that were bought FOB shipment location. Freight-in or mass transit are other

terms for carriage inwards. The price of carriage inwards is included in the price of the products

ordered.

Return outward: Return items are products that are refunded to the vendor by a consumer. They

are items that were formerly acquired from third parties but were restored to them but they were

unsuitable; they are also known as Purchase returns. Outward returns lower a company's overall

accounting records (Sinaga and et.al, 2021).

Wages expenses: Wages expenditure refers to the cost of hourly pay earned by a business for its

hourly employees. This may be one of a company's biggest expenditures, especially in areas like

transportation and manufacturing where there are a lot of hourly workers. Based on the amount

of extra given, wage expenses might fluctuate significantly from month to period. Due to the

different volume of work hours in each monthly, it might also vary by time. Based on the needs

of weekends and the overall amount of days in the month, certain monthly may have as few as

18 days at work, whereas others have as many as 23.

Rent: The account Rent Expense will bear the value of spaces as during time frame specified in

the revenue document's header, whether or not rent was collected inside that time, underneath the

accrual system of accounting. (Rent received in excess is recorded in the current asset category

Prepaid Rent on the balance sheet.) Total Expenses may show on the income statement as either

of administration expenditures or selling expenses, dependent on the space's purpose. The rental

would be included in the price of an item generated unless the leased facility was utilised to

manufacture things (Madhuwanthi, 2020).

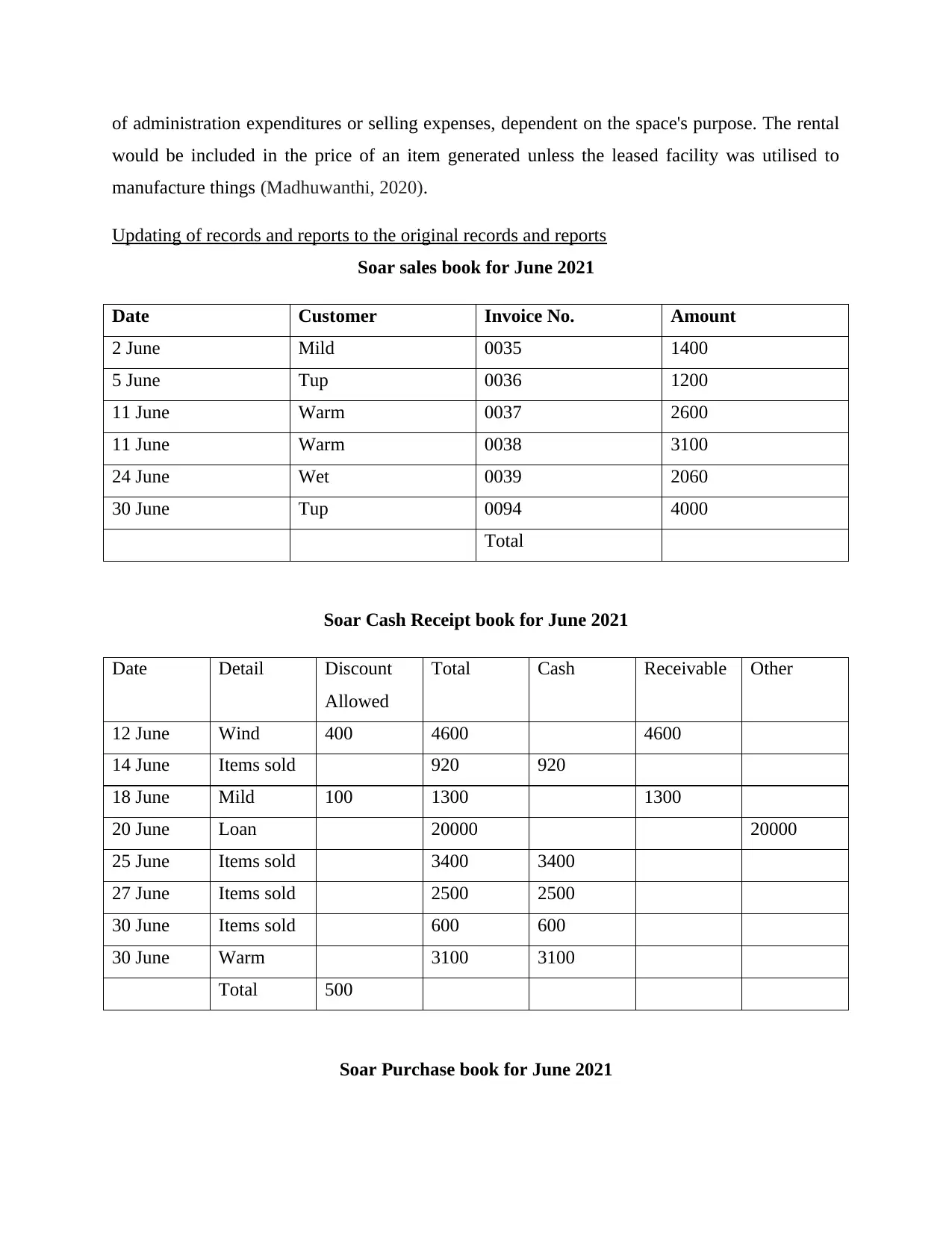

Updating of records and reports to the original records and reports

Soar sales book for June 2021

Date Customer Invoice No. Amount

2 June Mild 0035 1400

5 June Tup 0036 1200

11 June Warm 0037 2600

11 June Warm 0038 3100

24 June Wet 0039 2060

30 June Tup 0094 4000

Total

Soar Cash Receipt book for June 2021

Date Detail Discount

Allowed

Total Cash Receivable Other

12 June Wind 400 4600 4600

14 June Items sold 920 920

18 June Mild 100 1300 1300

20 June Loan 20000 20000

25 June Items sold 3400 3400

27 June Items sold 2500 2500

30 June Items sold 600 600

30 June Warm 3100 3100

Total 500

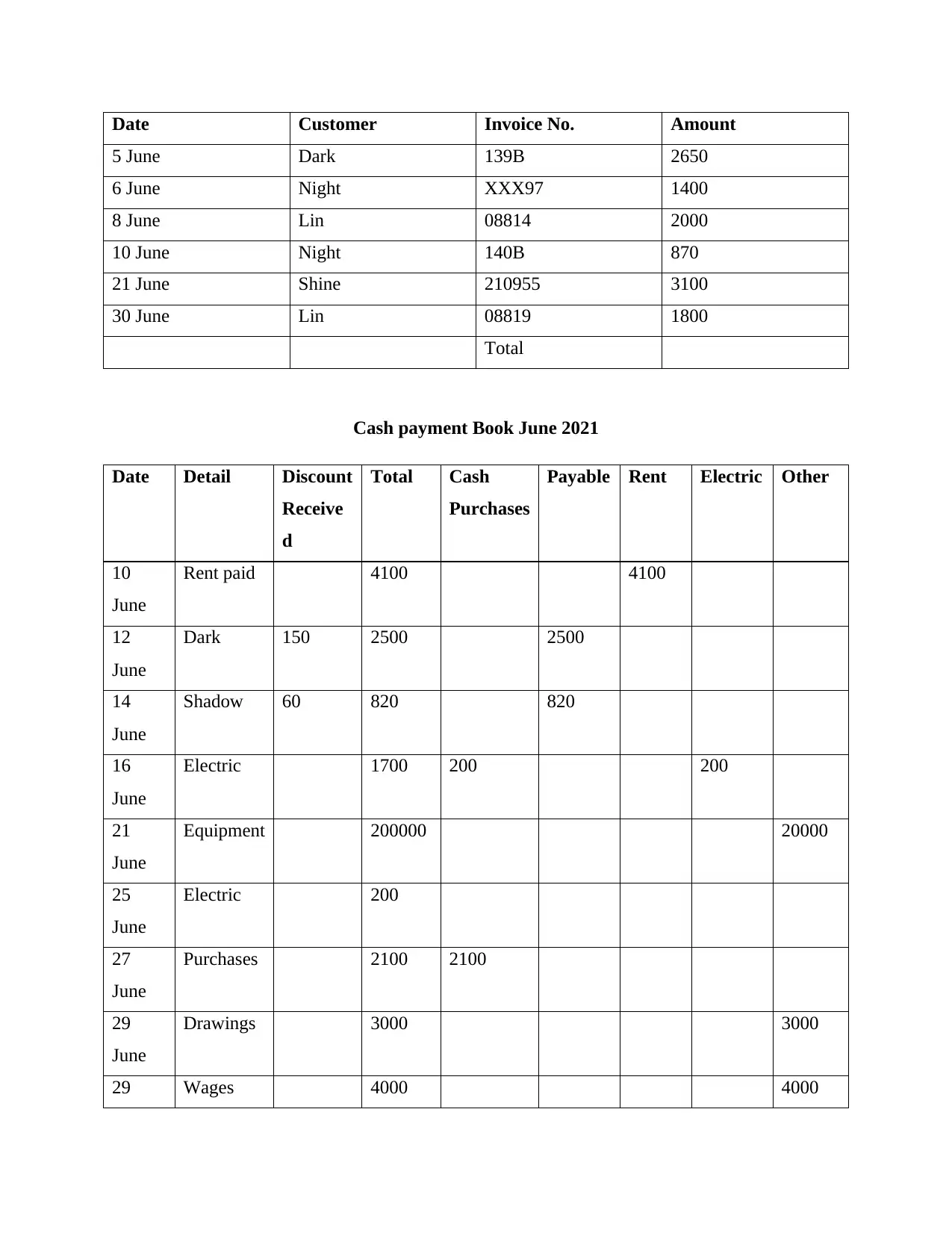

Soar Purchase book for June 2021

would be included in the price of an item generated unless the leased facility was utilised to

manufacture things (Madhuwanthi, 2020).

Updating of records and reports to the original records and reports

Soar sales book for June 2021

Date Customer Invoice No. Amount

2 June Mild 0035 1400

5 June Tup 0036 1200

11 June Warm 0037 2600

11 June Warm 0038 3100

24 June Wet 0039 2060

30 June Tup 0094 4000

Total

Soar Cash Receipt book for June 2021

Date Detail Discount

Allowed

Total Cash Receivable Other

12 June Wind 400 4600 4600

14 June Items sold 920 920

18 June Mild 100 1300 1300

20 June Loan 20000 20000

25 June Items sold 3400 3400

27 June Items sold 2500 2500

30 June Items sold 600 600

30 June Warm 3100 3100

Total 500

Soar Purchase book for June 2021

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Date Customer Invoice No. Amount

5 June Dark 139B 2650

6 June Night XXX97 1400

8 June Lin 08814 2000

10 June Night 140B 870

21 June Shine 210955 3100

30 June Lin 08819 1800

Total

Cash payment Book June 2021

Date Detail Discount

Receive

d

Total Cash

Purchases

Payable Rent Electric Other

10

June

Rent paid 4100 4100

12

June

Dark 150 2500 2500

14

June

Shadow 60 820 820

16

June

Electric 1700 200 200

21

June

Equipment 200000 20000

25

June

Electric 200

27

June

Purchases 2100 2100

29

June

Drawings 3000 3000

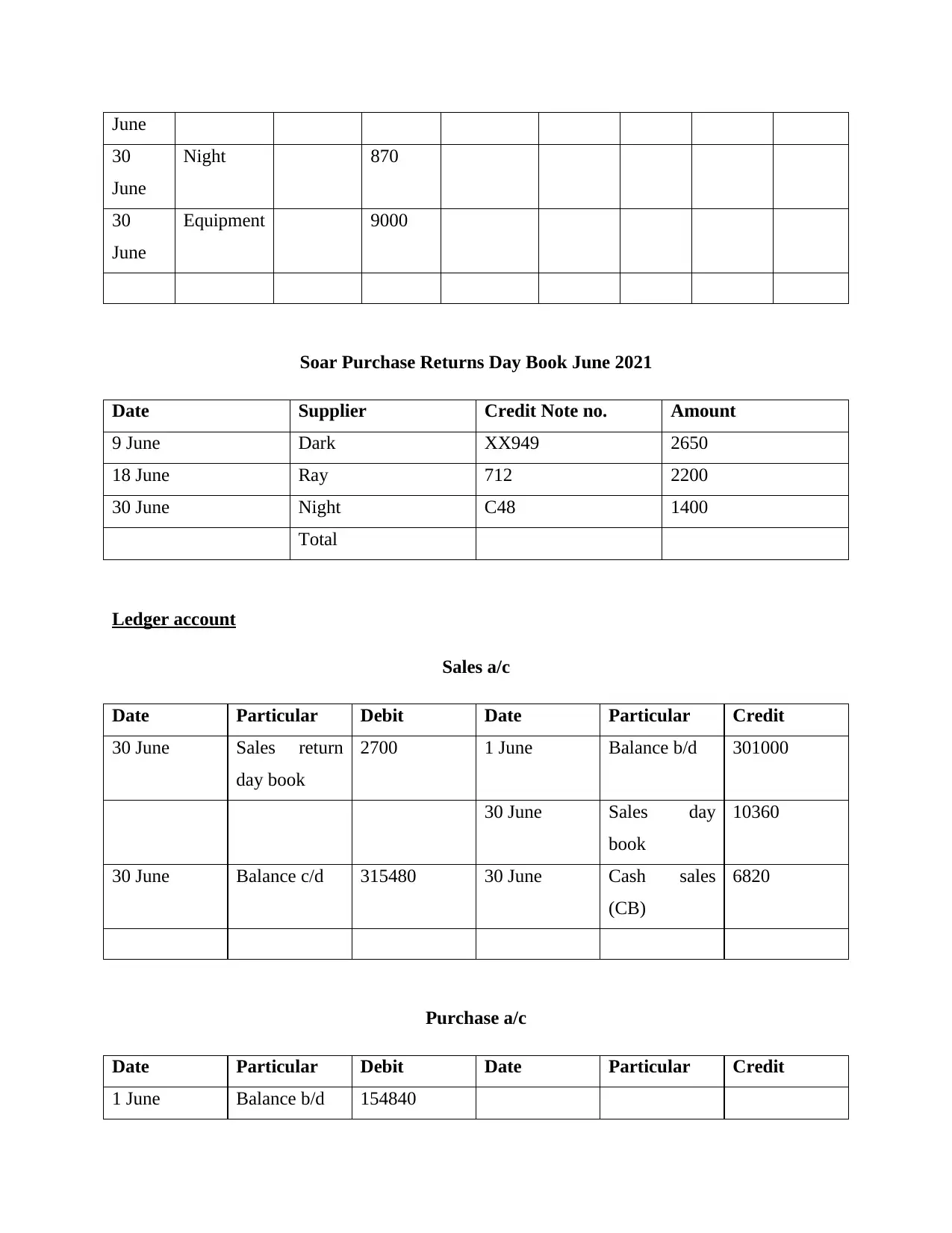

29 Wages 4000 4000

5 June Dark 139B 2650

6 June Night XXX97 1400

8 June Lin 08814 2000

10 June Night 140B 870

21 June Shine 210955 3100

30 June Lin 08819 1800

Total

Cash payment Book June 2021

Date Detail Discount

Receive

d

Total Cash

Purchases

Payable Rent Electric Other

10

June

Rent paid 4100 4100

12

June

Dark 150 2500 2500

14

June

Shadow 60 820 820

16

June

Electric 1700 200 200

21

June

Equipment 200000 20000

25

June

Electric 200

27

June

Purchases 2100 2100

29

June

Drawings 3000 3000

29 Wages 4000 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

June

30

June

Night 870

30

June

Equipment 9000

Soar Purchase Returns Day Book June 2021

Date Supplier Credit Note no. Amount

9 June Dark XX949 2650

18 June Ray 712 2200

30 June Night C48 1400

Total

Ledger account

Sales a/c

Date Particular Debit Date Particular Credit

30 June Sales return

day book

2700 1 June Balance b/d 301000

30 June Sales day

book

10360

30 June Balance c/d 315480 30 June Cash sales

(CB)

6820

Purchase a/c

Date Particular Debit Date Particular Credit

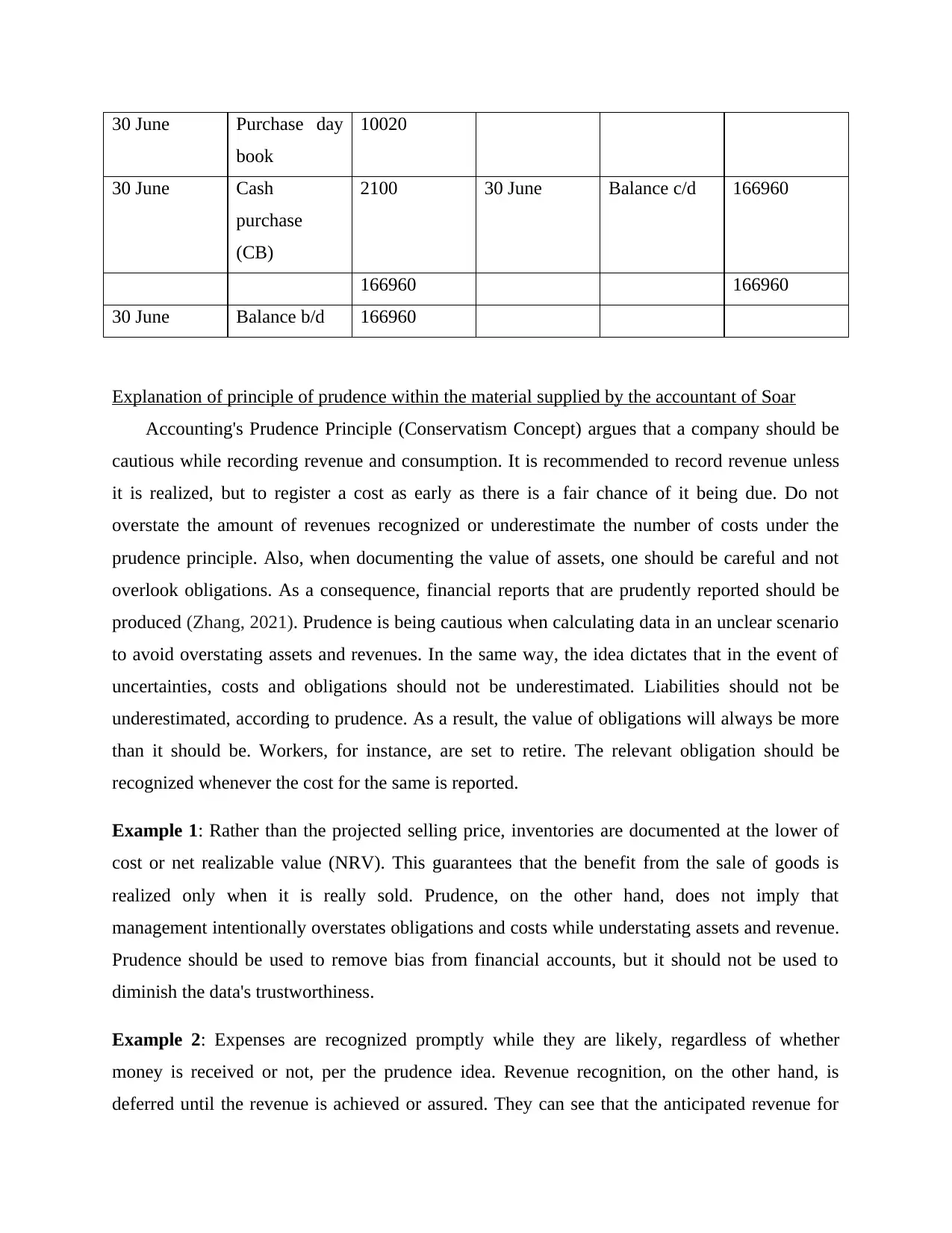

1 June Balance b/d 154840

30

June

Night 870

30

June

Equipment 9000

Soar Purchase Returns Day Book June 2021

Date Supplier Credit Note no. Amount

9 June Dark XX949 2650

18 June Ray 712 2200

30 June Night C48 1400

Total

Ledger account

Sales a/c

Date Particular Debit Date Particular Credit

30 June Sales return

day book

2700 1 June Balance b/d 301000

30 June Sales day

book

10360

30 June Balance c/d 315480 30 June Cash sales

(CB)

6820

Purchase a/c

Date Particular Debit Date Particular Credit

1 June Balance b/d 154840

30 June Purchase day

book

10020

30 June Cash

purchase

(CB)

2100 30 June Balance c/d 166960

166960 166960

30 June Balance b/d 166960

Explanation of principle of prudence within the material supplied by the accountant of Soar

Accounting's Prudence Principle (Conservatism Concept) argues that a company should be

cautious while recording revenue and consumption. It is recommended to record revenue unless

it is realized, but to register a cost as early as there is a fair chance of it being due. Do not

overstate the amount of revenues recognized or underestimate the number of costs under the

prudence principle. Also, when documenting the value of assets, one should be careful and not

overlook obligations. As a consequence, financial reports that are prudently reported should be

produced (Zhang, 2021). Prudence is being cautious when calculating data in an unclear scenario

to avoid overstating assets and revenues. In the same way, the idea dictates that in the event of

uncertainties, costs and obligations should not be underestimated. Liabilities should not be

underestimated, according to prudence. As a result, the value of obligations will always be more

than it should be. Workers, for instance, are set to retire. The relevant obligation should be

recognized whenever the cost for the same is reported.

Example 1: Rather than the projected selling price, inventories are documented at the lower of

cost or net realizable value (NRV). This guarantees that the benefit from the sale of goods is

realized only when it is really sold. Prudence, on the other hand, does not imply that

management intentionally overstates obligations and costs while understating assets and revenue.

Prudence should be used to remove bias from financial accounts, but it should not be used to

diminish the data's trustworthiness.

Example 2: Expenses are recognized promptly while they are likely, regardless of whether

money is received or not, per the prudence idea. Revenue recognition, on the other hand, is

deferred until the revenue is achieved or assured. They can see that the anticipated revenue for

book

10020

30 June Cash

purchase

(CB)

2100 30 June Balance c/d 166960

166960 166960

30 June Balance b/d 166960

Explanation of principle of prudence within the material supplied by the accountant of Soar

Accounting's Prudence Principle (Conservatism Concept) argues that a company should be

cautious while recording revenue and consumption. It is recommended to record revenue unless

it is realized, but to register a cost as early as there is a fair chance of it being due. Do not

overstate the amount of revenues recognized or underestimate the number of costs under the

prudence principle. Also, when documenting the value of assets, one should be careful and not

overlook obligations. As a consequence, financial reports that are prudently reported should be

produced (Zhang, 2021). Prudence is being cautious when calculating data in an unclear scenario

to avoid overstating assets and revenues. In the same way, the idea dictates that in the event of

uncertainties, costs and obligations should not be underestimated. Liabilities should not be

underestimated, according to prudence. As a result, the value of obligations will always be more

than it should be. Workers, for instance, are set to retire. The relevant obligation should be

recognized whenever the cost for the same is reported.

Example 1: Rather than the projected selling price, inventories are documented at the lower of

cost or net realizable value (NRV). This guarantees that the benefit from the sale of goods is

realized only when it is really sold. Prudence, on the other hand, does not imply that

management intentionally overstates obligations and costs while understating assets and revenue.

Prudence should be used to remove bias from financial accounts, but it should not be used to

diminish the data's trustworthiness.

Example 2: Expenses are recognized promptly while they are likely, regardless of whether

money is received or not, per the prudence idea. Revenue recognition, on the other hand, is

deferred until the revenue is achieved or assured. They can see that the anticipated revenue for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Soar is 5,000,000. As a result, Soar will not be able to record the whole amount as revenue right

once. Only 25% of the total income can be recorded as income in the accounting records. For

financial reporting, this approach is known as the phase of calculating (Kollar, 2021). Revenue

recognition using this approach only to the degree that it has been finished. As a result, the

amount of revenue that might be recognized is just 1,250,000.

Example 3: A "provision for bad and doubtful debts" is stated in the collections part of liquid

liability and subtracted from the total bondholder’s amount. This provision does not display

borrowers who have become bad debts; rather, it indicates debtors who may become bad debts as

a consequence of their sold items only with firm or their unusual challenges, and the organization

may not be able to collect money from them. Underneath the prudence principle in accountancy,

these debtors were included in allowance (Sukandani, Istikhoroh and Widodo, 2021).

CONCLUSION

As per the above report it has been concluded that accounting is the process used by many

businesses and corporations to determine their finances. Accounting is used to product design

assessment and forecasting. Accounting is a popular study, and as the globe becomes more

civilized, the necessity for financial management to perform duties grows. Mastering accounting

terminology, on the other hand, is difficult since people are fully bombarded with assignments.

Accounting projects are usually difficult, necessitating the assistance of accounting assignment

assistance to professionals in order to solve the issues. Accounting is all about formulating ideas

and calculating results, which is necessary for future actions.

once. Only 25% of the total income can be recorded as income in the accounting records. For

financial reporting, this approach is known as the phase of calculating (Kollar, 2021). Revenue

recognition using this approach only to the degree that it has been finished. As a result, the

amount of revenue that might be recognized is just 1,250,000.

Example 3: A "provision for bad and doubtful debts" is stated in the collections part of liquid

liability and subtracted from the total bondholder’s amount. This provision does not display

borrowers who have become bad debts; rather, it indicates debtors who may become bad debts as

a consequence of their sold items only with firm or their unusual challenges, and the organization

may not be able to collect money from them. Underneath the prudence principle in accountancy,

these debtors were included in allowance (Sukandani, Istikhoroh and Widodo, 2021).

CONCLUSION

As per the above report it has been concluded that accounting is the process used by many

businesses and corporations to determine their finances. Accounting is used to product design

assessment and forecasting. Accounting is a popular study, and as the globe becomes more

civilized, the necessity for financial management to perform duties grows. Mastering accounting

terminology, on the other hand, is difficult since people are fully bombarded with assignments.

Accounting projects are usually difficult, necessitating the assistance of accounting assignment

assistance to professionals in order to solve the issues. Accounting is all about formulating ideas

and calculating results, which is necessary for future actions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal

Widiastuti, T., Sukmana, R. and Hady, A. F., 2021. Financial Performance Measurement for

Nazhir: A Proposed Model Based On Sharia Accounting Standard. Review of

International Geographical Education Online. 11(4). pp.286-294.

Buszko, M. and Ciechan-Kujawa, M., 2020, February. Influence of Deregulation on Sustainable

Development of Sector of Professional Financial and Accounting Services. In Finance

and Sustainability: Proceedings from the 2nd Finance and Sustainability Conference,

Wroclaw 2018 (p. 277). Springer Nature.

Safari Sarchah, F., Yazdifar, H. and Pifeh, A., 2020. Privatization, changes in management

accounting practices and their impacts on financial performance–evidence from

Iran. Iranian Journal of Finance. 4(3). pp.18-48.

Mustafa, M. R., 2020. The study of problems moving from the unified accounting system to the

international accounting standards. International Journal of Multicultural and

Multireligious Understanding. 7(1). pp.101-116.

Sinaga, M. D. and et.al, 2021. Introduction to MYOB Accounting Basics in Accounting Data

Processing at SMK 2 BM Swasta Medan Putri. JUDIMAS. 2(1). pp.13-22.

Madhuwanthi, J. S. D., 2020. The Impact of IFRS Adoption on Value Relevance of Accounting

Information: Evidence from in Manufacturing & Hotel Sectors in Sri Lanka.

Zhang, E., 2021. Discourses on public sector accounting reforms in China: A brief history

(1949–2019). Accounting History. 26(2). pp.255-279.

Kollar, B., 2021. Web Globalization and Its Possible Consequences on Usage of Different

Creative Accounting Techniques. In SHS Web of Conferences (Vol. 92). EDP Sciences.

Sukandani, Y., Istikhoroh, S. and Widodo, U.P.W., 2021. THE ROLE OF ACCOUNTING

CONSERVATISM AS A MODERATE OF DEBT RATIO EFFECT ON FINANCIAL

DISTRESS. International Journal of Economics, Business and Accounting Research

(IJEBAR). 5(2).

Nurdiansyah, D., Pardistya, I., Mahpudin, E. and Nophiansah, D., 2021. The empirical evidence

of the effect of company size, leverage and profitability on income

smoothing. Accounting. 7(7). pp.1805-1812.

Blizkiy, R. S., Malinenko, V. E. and Lebedinskaya, Y. S., 2021. Recursion of the Temporal

Paradigm of the Digital Economy Accounting. Socio-economic Systems: Paradigms for

the Future, pp.521-529.

Semenyshena, N., Khorunzhak, N. and Zadorozhnyi, Z. M., 2020. The institutionalization of

accounting: the impact of national standards on the development of

economies. Independent Journal of Management & Production. 11(8). pp.695-711.

Books and Journal

Widiastuti, T., Sukmana, R. and Hady, A. F., 2021. Financial Performance Measurement for

Nazhir: A Proposed Model Based On Sharia Accounting Standard. Review of

International Geographical Education Online. 11(4). pp.286-294.

Buszko, M. and Ciechan-Kujawa, M., 2020, February. Influence of Deregulation on Sustainable

Development of Sector of Professional Financial and Accounting Services. In Finance

and Sustainability: Proceedings from the 2nd Finance and Sustainability Conference,

Wroclaw 2018 (p. 277). Springer Nature.

Safari Sarchah, F., Yazdifar, H. and Pifeh, A., 2020. Privatization, changes in management

accounting practices and their impacts on financial performance–evidence from

Iran. Iranian Journal of Finance. 4(3). pp.18-48.

Mustafa, M. R., 2020. The study of problems moving from the unified accounting system to the

international accounting standards. International Journal of Multicultural and

Multireligious Understanding. 7(1). pp.101-116.

Sinaga, M. D. and et.al, 2021. Introduction to MYOB Accounting Basics in Accounting Data

Processing at SMK 2 BM Swasta Medan Putri. JUDIMAS. 2(1). pp.13-22.

Madhuwanthi, J. S. D., 2020. The Impact of IFRS Adoption on Value Relevance of Accounting

Information: Evidence from in Manufacturing & Hotel Sectors in Sri Lanka.

Zhang, E., 2021. Discourses on public sector accounting reforms in China: A brief history

(1949–2019). Accounting History. 26(2). pp.255-279.

Kollar, B., 2021. Web Globalization and Its Possible Consequences on Usage of Different

Creative Accounting Techniques. In SHS Web of Conferences (Vol. 92). EDP Sciences.

Sukandani, Y., Istikhoroh, S. and Widodo, U.P.W., 2021. THE ROLE OF ACCOUNTING

CONSERVATISM AS A MODERATE OF DEBT RATIO EFFECT ON FINANCIAL

DISTRESS. International Journal of Economics, Business and Accounting Research

(IJEBAR). 5(2).

Nurdiansyah, D., Pardistya, I., Mahpudin, E. and Nophiansah, D., 2021. The empirical evidence

of the effect of company size, leverage and profitability on income

smoothing. Accounting. 7(7). pp.1805-1812.

Blizkiy, R. S., Malinenko, V. E. and Lebedinskaya, Y. S., 2021. Recursion of the Temporal

Paradigm of the Digital Economy Accounting. Socio-economic Systems: Paradigms for

the Future, pp.521-529.

Semenyshena, N., Khorunzhak, N. and Zadorozhnyi, Z. M., 2020. The institutionalization of

accounting: the impact of national standards on the development of

economies. Independent Journal of Management & Production. 11(8). pp.695-711.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.