Internal Control and Audit Processes

VerifiedAdded on 2020/01/07

|21

|6572

|375

Essay

AI Summary

This assignment delves into the crucial aspects of internal control systems and audit procedures within organizations. It examines various types of audit tests, the roles of auditors and management in providing reports, and the significance of SOX 404 compliance. The document analyzes case studies and theoretical frameworks to shed light on how internal controls influence financial reporting quality and risk mitigation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial

systems and

auditing

1

systems and

auditing

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1. Description of purpose and use of different accounting records.............................................3

2. Assessment of importance and meaning of fundamental accounting concepts.......................5

3. Evaluation of factors that influence the nature and structure of accounting systems..............7

Task 2...............................................................................................................................................8

1. Identification of different components of business risk...........................................................8

2. Analysis of control system placed in business.........................................................................9

3. Evaluation of risk of fraud within business and suggestion of method for detection............10

Task 3.............................................................................................................................................11

1. Planning of audit with reference to scope, materiality and risk.............................................11

2. Identification and explanation of appropriate audit tests for audit assignment.....................13

3. Types of record to be maintained during audit process.........................................................14

4. Draft of audit report...............................................................................................................15

5. Draft of management report...................................................................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................19

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1. Description of purpose and use of different accounting records.............................................3

2. Assessment of importance and meaning of fundamental accounting concepts.......................5

3. Evaluation of factors that influence the nature and structure of accounting systems..............7

Task 2...............................................................................................................................................8

1. Identification of different components of business risk...........................................................8

2. Analysis of control system placed in business.........................................................................9

3. Evaluation of risk of fraud within business and suggestion of method for detection............10

Task 3.............................................................................................................................................11

1. Planning of audit with reference to scope, materiality and risk.............................................11

2. Identification and explanation of appropriate audit tests for audit assignment.....................13

3. Types of record to be maintained during audit process.........................................................14

4. Draft of audit report...............................................................................................................15

5. Draft of management report...................................................................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................19

2

INTRODUCTION

Corporate entities are required to maintain their financial records in an appropriable

manner by complying norms and provisions described by authorized bodies. Financial

information provided by companies is used by different users in order to make economic

decisions. Due to this aspect, business entities are required to ensure factors such as accuracy,

reliability, relevancy and comparability in their financial records (Hallikas and et al., 2004). For

this purpose, provision of mandatory audit has been introduced by legal authorities to ensure

users that fair and reliable information is provided by companies.

Present study is completed in three parts. First part is related to description of general

accounting procedures that are required to be used in Kingston Limited. For this purpose

description of accounting records and concepts will be provided along with its importance. In

second part of the report, business risks and control systems will be assessed by considering case

study of Tesco plc. Further, in the last part of the report, audit will be conducted of FA Jet Ltd on

the basis of provided financial facts and figures. On the basis of audit work, management report

and audit report will be prepared.

TASK 1

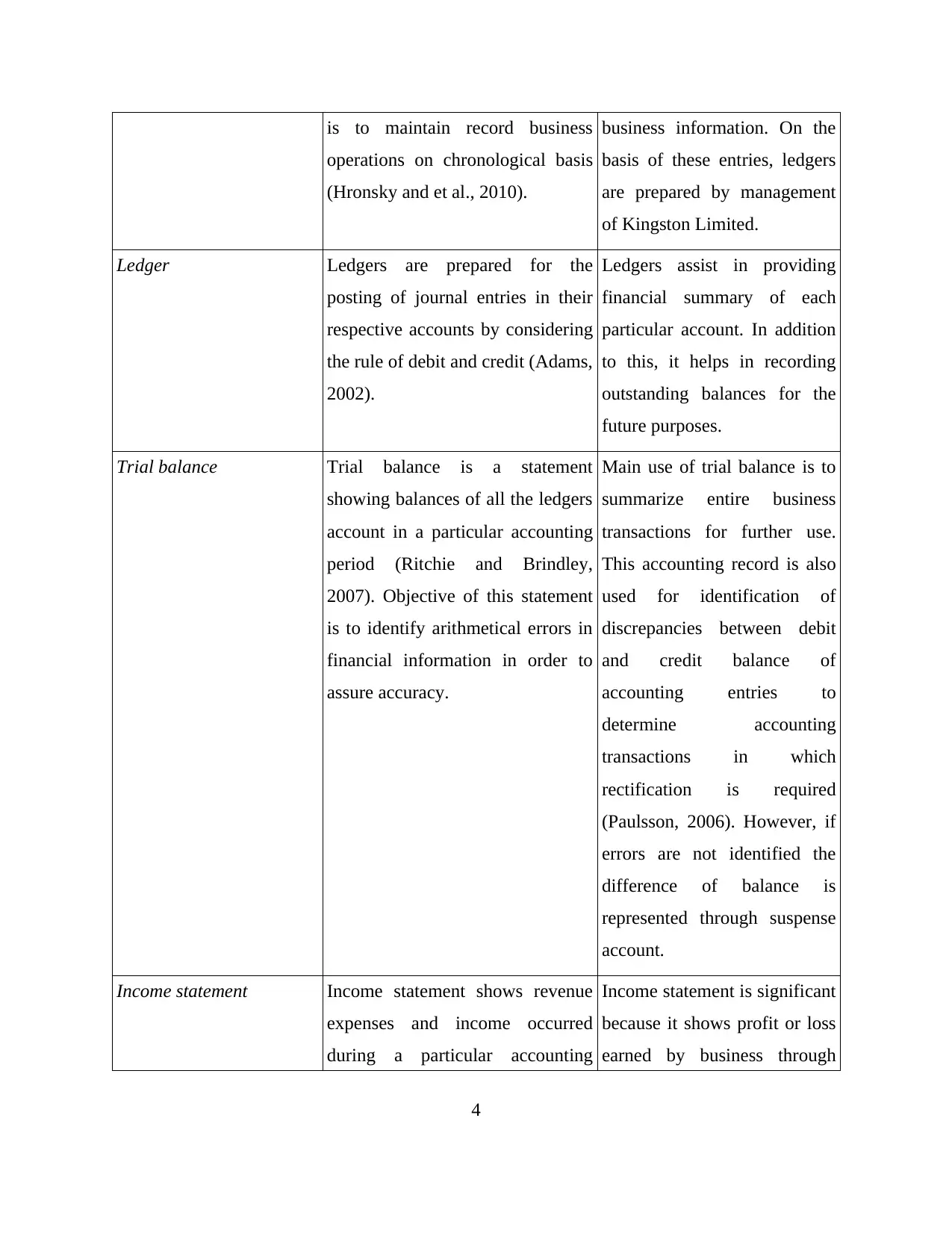

1. Description of purpose and use of different accounting records

Accounting records are prepared by business organization to show monetary business

transactions in a proper manner. Preparation of these records are completed by considering sales,

purchases, expenses and incomes (both revenue and capital). For the effective presentation of

business information different accounting records are prepared such as journals, ledgers, income

statement, cash flow statement and position statement. Each accounting record has its different

objective and different uses for the stakeholders, description of which is as follows:

Accounting record Purpose Use

Journal entries Journal entries are made to record

each business transaction by

considering its debit and credit in

order to provide its double effect.

Objective of this accounting record

Journal entries are

fundamental source of all

accounting records. This

source provide detail

information for each single

3

Corporate entities are required to maintain their financial records in an appropriable

manner by complying norms and provisions described by authorized bodies. Financial

information provided by companies is used by different users in order to make economic

decisions. Due to this aspect, business entities are required to ensure factors such as accuracy,

reliability, relevancy and comparability in their financial records (Hallikas and et al., 2004). For

this purpose, provision of mandatory audit has been introduced by legal authorities to ensure

users that fair and reliable information is provided by companies.

Present study is completed in three parts. First part is related to description of general

accounting procedures that are required to be used in Kingston Limited. For this purpose

description of accounting records and concepts will be provided along with its importance. In

second part of the report, business risks and control systems will be assessed by considering case

study of Tesco plc. Further, in the last part of the report, audit will be conducted of FA Jet Ltd on

the basis of provided financial facts and figures. On the basis of audit work, management report

and audit report will be prepared.

TASK 1

1. Description of purpose and use of different accounting records

Accounting records are prepared by business organization to show monetary business

transactions in a proper manner. Preparation of these records are completed by considering sales,

purchases, expenses and incomes (both revenue and capital). For the effective presentation of

business information different accounting records are prepared such as journals, ledgers, income

statement, cash flow statement and position statement. Each accounting record has its different

objective and different uses for the stakeholders, description of which is as follows:

Accounting record Purpose Use

Journal entries Journal entries are made to record

each business transaction by

considering its debit and credit in

order to provide its double effect.

Objective of this accounting record

Journal entries are

fundamental source of all

accounting records. This

source provide detail

information for each single

3

is to maintain record business

operations on chronological basis

(Hronsky and et al., 2010).

business information. On the

basis of these entries, ledgers

are prepared by management

of Kingston Limited.

Ledger Ledgers are prepared for the

posting of journal entries in their

respective accounts by considering

the rule of debit and credit (Adams,

2002).

Ledgers assist in providing

financial summary of each

particular account. In addition

to this, it helps in recording

outstanding balances for the

future purposes.

Trial balance Trial balance is a statement

showing balances of all the ledgers

account in a particular accounting

period (Ritchie and Brindley,

2007). Objective of this statement

is to identify arithmetical errors in

financial information in order to

assure accuracy.

Main use of trial balance is to

summarize entire business

transactions for further use.

This accounting record is also

used for identification of

discrepancies between debit

and credit balance of

accounting entries to

determine accounting

transactions in which

rectification is required

(Paulsson, 2006). However, if

errors are not identified the

difference of balance is

represented through suspense

account.

Income statement Income statement shows revenue

expenses and income occurred

during a particular accounting

Income statement is significant

because it shows profit or loss

earned by business through

4

operations on chronological basis

(Hronsky and et al., 2010).

business information. On the

basis of these entries, ledgers

are prepared by management

of Kingston Limited.

Ledger Ledgers are prepared for the

posting of journal entries in their

respective accounts by considering

the rule of debit and credit (Adams,

2002).

Ledgers assist in providing

financial summary of each

particular account. In addition

to this, it helps in recording

outstanding balances for the

future purposes.

Trial balance Trial balance is a statement

showing balances of all the ledgers

account in a particular accounting

period (Ritchie and Brindley,

2007). Objective of this statement

is to identify arithmetical errors in

financial information in order to

assure accuracy.

Main use of trial balance is to

summarize entire business

transactions for further use.

This accounting record is also

used for identification of

discrepancies between debit

and credit balance of

accounting entries to

determine accounting

transactions in which

rectification is required

(Paulsson, 2006). However, if

errors are not identified the

difference of balance is

represented through suspense

account.

Income statement Income statement shows revenue

expenses and income occurred

during a particular accounting

Income statement is significant

because it shows profit or loss

earned by business through

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

period. This statement is prepared

by considering accrual approach in

accrual & advance income and

prepaid and outstanding expenses

are also considered.

operational and non-

operational activities. By

making inter and intra

comparison of this statement

efficiency of business can be

determined (Alexander and

Archer, 2010).

Cash flow statement Cash flow statement is prepared to

show inflow and outflow of cash

and cash equivalents during the

accounting year (Romney and et

al., 2006). Objective of this

statement is to keep record of cash

because other accounting records

are prepared by using accrual

approach.

Use of this statement is to

determine sources and

consumption of cash in

business. By tracking cash

activities, organization can

manage liquidity in an

effective manner.

Position statement Position statement is prepared on

the basis of accounting equation

i.e. sum of assets is equivalent to

sum of liabilities and capital.

Objective of this statement is to

show financial position on

particular accounting date.

This statement is useful for

analysis of financial position

of the company. With the

changing position,

organization can plan for

future strategies for the

purpose of growth and

improvement.

2. Assessment of importance and meaning of fundamental accounting concepts

Fundamental accounting concepts are general norms developed by professional bodies

which are required to applied while preparation of accounting record and financial statements.

All the concept are important because they assure relevancy and fairness in financial information

5

by considering accrual approach in

accrual & advance income and

prepaid and outstanding expenses

are also considered.

operational and non-

operational activities. By

making inter and intra

comparison of this statement

efficiency of business can be

determined (Alexander and

Archer, 2010).

Cash flow statement Cash flow statement is prepared to

show inflow and outflow of cash

and cash equivalents during the

accounting year (Romney and et

al., 2006). Objective of this

statement is to keep record of cash

because other accounting records

are prepared by using accrual

approach.

Use of this statement is to

determine sources and

consumption of cash in

business. By tracking cash

activities, organization can

manage liquidity in an

effective manner.

Position statement Position statement is prepared on

the basis of accounting equation

i.e. sum of assets is equivalent to

sum of liabilities and capital.

Objective of this statement is to

show financial position on

particular accounting date.

This statement is useful for

analysis of financial position

of the company. With the

changing position,

organization can plan for

future strategies for the

purpose of growth and

improvement.

2. Assessment of importance and meaning of fundamental accounting concepts

Fundamental accounting concepts are general norms developed by professional bodies

which are required to applied while preparation of accounting record and financial statements.

All the concept are important because they assure relevancy and fairness in financial information

5

provided by the company (Arens, Elder and Beasley, 2010). Objective of implication of these

concepts is to assure that users are not misled by facts and figures provided by corporate entities.

For this aspect, management of Kingston Limited is required to considering following

accounting concepts for recording of business information: Business entity concept: In accordance with this accounting concept, financial activities

of business is different from their owners. It is because; accounting records shows

information of organization not of the parties related to it. This concept segregates entity

from their owners (Clatworthy, 2013). Further, record keepers are required maintain

information by considering business. Accrual system: Business organizations are required to maintain their books of account

on the basis of accrual approach instead of cash approach. Objective of the concept is to

show accurate and fair position of the entity (Fundamental Concepts of Accounting,

2015). By the application of this concept, record keepers are able to portray transactions

related to particular accounting period instead of considering receipts and payments of

cash. Assumption of going concern: It is fundamental assumption which is required to be

considered by all entities. This assumption states that business is running in good position

and there is no planning of closure of business activities in the forseeable future. In

situation where there is contradiction of this concept then company is required to

represent this information to its users. Prudence: This concept is also known as principle of conservatism. In accordance with

this principle, businesses are required to record all possible losses but they cannot do

accounting for potential profits of future (Zadek, Evans and Pruzan, 2013). Objective of

this concept is to prevent overstatement of profits in financial statements as it can

misguide users. Materiality: Fundamental accounting concept of materiality states that minor events can

be ignored for the purpose of full disclosure. However, all vital accounting event must be

provided with complete information to the users (Fundamental Concepts of Accounting,

2015). Purpose of this concept is to enhance relevancy of financial information provided

by the organization.

6

concepts is to assure that users are not misled by facts and figures provided by corporate entities.

For this aspect, management of Kingston Limited is required to considering following

accounting concepts for recording of business information: Business entity concept: In accordance with this accounting concept, financial activities

of business is different from their owners. It is because; accounting records shows

information of organization not of the parties related to it. This concept segregates entity

from their owners (Clatworthy, 2013). Further, record keepers are required maintain

information by considering business. Accrual system: Business organizations are required to maintain their books of account

on the basis of accrual approach instead of cash approach. Objective of the concept is to

show accurate and fair position of the entity (Fundamental Concepts of Accounting,

2015). By the application of this concept, record keepers are able to portray transactions

related to particular accounting period instead of considering receipts and payments of

cash. Assumption of going concern: It is fundamental assumption which is required to be

considered by all entities. This assumption states that business is running in good position

and there is no planning of closure of business activities in the forseeable future. In

situation where there is contradiction of this concept then company is required to

represent this information to its users. Prudence: This concept is also known as principle of conservatism. In accordance with

this principle, businesses are required to record all possible losses but they cannot do

accounting for potential profits of future (Zadek, Evans and Pruzan, 2013). Objective of

this concept is to prevent overstatement of profits in financial statements as it can

misguide users. Materiality: Fundamental accounting concept of materiality states that minor events can

be ignored for the purpose of full disclosure. However, all vital accounting event must be

provided with complete information to the users (Fundamental Concepts of Accounting,

2015). Purpose of this concept is to enhance relevancy of financial information provided

by the organization.

6

Historical cost: As per this accounting concepts, all business assets are required to be

recorded at its cost (i.e. amount incurred by business at the time of its acquire).

Henceforth, business entities are not entitled to use market value for accounting of asset.

Objective of this concept is to prevent undue inflation in asset.

In addition to above described concept, Kingston Limited is also required to consider

matching, consistency, money measurement and full disclosure concept in order to show fair and

reliable information to the users.

3. Evaluation of factors that influence the nature and structure of accounting systems

Accounting systems are developed by business entities by considering nature and scale of

business operations. Description of factors that influenced nature and structure of accounting

systems are enumerated as below: Size of enterprise: Size of organization is important factor for structuring of accounting

system of business. It is because; size of entity directs affects commercial transaction and

its complexity (Wicks, 2009). For example, medium enterprise such as sole proprietor

and partnership firm can record their business transaction by accrual or cash accounting

system as per their convenience. However, companies are in compulsion to use accrual

approach for accounting as it provides comparatively fair information. Nature of business and complexities in transaction: Main advantage of accounting

system is that it stores entire information at central location. Further, it helps in

streamline the flow of information for better access (Robertson and Davis, 2012).

Effective accounting system assists in better data processing by which management can

viable decisions. Thus, accounting system is required to be developed by considering

nature of business and its transactions. Level of training required for staff: Accounting processes are easy in now a days with the

uses of accounting system such as SAP and oracle. These, accounting software assists in

addressing requirements of information of managerial parties in the process of decision

making. However, these systems are considered to be effective if staff members are well

versed with its usage (Power, 2010). Due to this aspect, accounting systems are required

to be developed on the basis of skills and capabilities of workers. Further, if updated

system is used then proper arrangements for training should be done.

7

recorded at its cost (i.e. amount incurred by business at the time of its acquire).

Henceforth, business entities are not entitled to use market value for accounting of asset.

Objective of this concept is to prevent undue inflation in asset.

In addition to above described concept, Kingston Limited is also required to consider

matching, consistency, money measurement and full disclosure concept in order to show fair and

reliable information to the users.

3. Evaluation of factors that influence the nature and structure of accounting systems

Accounting systems are developed by business entities by considering nature and scale of

business operations. Description of factors that influenced nature and structure of accounting

systems are enumerated as below: Size of enterprise: Size of organization is important factor for structuring of accounting

system of business. It is because; size of entity directs affects commercial transaction and

its complexity (Wicks, 2009). For example, medium enterprise such as sole proprietor

and partnership firm can record their business transaction by accrual or cash accounting

system as per their convenience. However, companies are in compulsion to use accrual

approach for accounting as it provides comparatively fair information. Nature of business and complexities in transaction: Main advantage of accounting

system is that it stores entire information at central location. Further, it helps in

streamline the flow of information for better access (Robertson and Davis, 2012).

Effective accounting system assists in better data processing by which management can

viable decisions. Thus, accounting system is required to be developed by considering

nature of business and its transactions. Level of training required for staff: Accounting processes are easy in now a days with the

uses of accounting system such as SAP and oracle. These, accounting software assists in

addressing requirements of information of managerial parties in the process of decision

making. However, these systems are considered to be effective if staff members are well

versed with its usage (Power, 2010). Due to this aspect, accounting systems are required

to be developed on the basis of skills and capabilities of workers. Further, if updated

system is used then proper arrangements for training should be done.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Service provider differentiator: This factor is required to be considered for alignment of

IT strategy with the organizational strategy. Each services provider has its own pros and

cons. It is because; customized systems are not only costly because they are also time

consuming for implementation (No, 2007). Thus, business entity is required to consider

financial impact and potential benefits and along with the costs of using IT services.

System Cost: Organizations are also required to consider the cost of accounting system in

order to assure its financial feasibility. It is because; various accounting software have

cost in millions of dollars which is not affordable by all organization due to which they

are required to general software as per their needs.

TASK 2

1. Identification of different components of business risk

All corporate entities are required to bear risk while commencing their business

operational. However, extent of business risks varies with the nature and scale of operations. For

the survival and long term success, commercial entities are required to mitigate these risks

(Power, 2010). In present era, companies are exposed to several risk components that can have

adverse impact on their profitability, productivity and market reputation. By considering the case

study of Tesco, description of component of business risks is as follows: Risk related to human resources: It is general risk faced by all business organization.

Increasing employee turnover is not a good factor for business because it enhances cost

of recruitment and training (Nelson, 2009). In addition to this, business has to loss

skilled, qualified and experienced employees from the work place. This risk has severe

impact on the productivity of business. Technological risk: Entire operational activities of Tesco are aligned through

information technology. Due to this aspect, single error or issue in technology can have

severe adverse impact on their operational activities. Major influence of this risk is on

their online segment in which each task is completed by use of integrated technology

systems. Regulatory risk:All commercial entities are required to comply legal provisions and

political guidelines in their operational policies and procedures. In situation where they

failed to do so, then they have to pay high penalties (Robertson and Davis, 2012). In

8

IT strategy with the organizational strategy. Each services provider has its own pros and

cons. It is because; customized systems are not only costly because they are also time

consuming for implementation (No, 2007). Thus, business entity is required to consider

financial impact and potential benefits and along with the costs of using IT services.

System Cost: Organizations are also required to consider the cost of accounting system in

order to assure its financial feasibility. It is because; various accounting software have

cost in millions of dollars which is not affordable by all organization due to which they

are required to general software as per their needs.

TASK 2

1. Identification of different components of business risk

All corporate entities are required to bear risk while commencing their business

operational. However, extent of business risks varies with the nature and scale of operations. For

the survival and long term success, commercial entities are required to mitigate these risks

(Power, 2010). In present era, companies are exposed to several risk components that can have

adverse impact on their profitability, productivity and market reputation. By considering the case

study of Tesco, description of component of business risks is as follows: Risk related to human resources: It is general risk faced by all business organization.

Increasing employee turnover is not a good factor for business because it enhances cost

of recruitment and training (Nelson, 2009). In addition to this, business has to loss

skilled, qualified and experienced employees from the work place. This risk has severe

impact on the productivity of business. Technological risk: Entire operational activities of Tesco are aligned through

information technology. Due to this aspect, single error or issue in technology can have

severe adverse impact on their operational activities. Major influence of this risk is on

their online segment in which each task is completed by use of integrated technology

systems. Regulatory risk:All commercial entities are required to comply legal provisions and

political guidelines in their operational policies and procedures. In situation where they

failed to do so, then they have to pay high penalties (Robertson and Davis, 2012). In

8

addition to this, there market reputation is adversely affected. This risk also enhance

intervention by government bodies in business operations. Liquidity and solvency risk: This risk is occurred in situation where organization is not

able to manage their obligations with the assets of company. Due to this aspect,

management of Tesco assure appropriable cash and debt management in business

(Wood, Wrigley and Coe, 2016). However, there are various factors which cannot be

controlled by liquidity management such fluctuations in foreign exchange rate and

market situation. Competitive risk: Increasing competition in retail market also enhances risk component

of Tesco. It is because; increasing rivalry results in reduction of market share and

increase in customer power as they have high substitutes if they are not satisfied with the

products and services of company.

Slow economic growth: Reduction in growth of economy also imposes risk on company

as purchasing power of customers is reduced (Clatworthy, 2013). This factor reduces

sales of business and lead to the situation of recession in market.

2. Analysis of control system placed in business

Effective control system is essential for the success of business because it provides

assurance of accuracy and prevention of material misrepresentation in business operations.

Objective of control system is to assure standard performance of employees through compliance

with the developed policies and procedures (Wright, 2015). By considering the case study of

Tesco, it can be said that management of organization is focused on development of effective

control system in order to reduce risk of fraud. For this purpose, they had implemented risk

management practices for business operations. Strategic and financial matters of the company

are regularly reviewed by Executive Committee and Board and they consider external advice for

further improvement (Jones, Comfort and Hillier, 2015). Further, triennial revaluation is used by

management of Tesco in order prevent deficit funding plan. Management of company is

continuously engaged with the investors to communicate details of their future activities to

involve them in process of decision making.

Tesco had developed effective monitoring procedures in order to identify and deal with

security incidents linked to the information technology. In addition to this, company had

9

intervention by government bodies in business operations. Liquidity and solvency risk: This risk is occurred in situation where organization is not

able to manage their obligations with the assets of company. Due to this aspect,

management of Tesco assure appropriable cash and debt management in business

(Wood, Wrigley and Coe, 2016). However, there are various factors which cannot be

controlled by liquidity management such fluctuations in foreign exchange rate and

market situation. Competitive risk: Increasing competition in retail market also enhances risk component

of Tesco. It is because; increasing rivalry results in reduction of market share and

increase in customer power as they have high substitutes if they are not satisfied with the

products and services of company.

Slow economic growth: Reduction in growth of economy also imposes risk on company

as purchasing power of customers is reduced (Clatworthy, 2013). This factor reduces

sales of business and lead to the situation of recession in market.

2. Analysis of control system placed in business

Effective control system is essential for the success of business because it provides

assurance of accuracy and prevention of material misrepresentation in business operations.

Objective of control system is to assure standard performance of employees through compliance

with the developed policies and procedures (Wright, 2015). By considering the case study of

Tesco, it can be said that management of organization is focused on development of effective

control system in order to reduce risk of fraud. For this purpose, they had implemented risk

management practices for business operations. Strategic and financial matters of the company

are regularly reviewed by Executive Committee and Board and they consider external advice for

further improvement (Jones, Comfort and Hillier, 2015). Further, triennial revaluation is used by

management of Tesco in order prevent deficit funding plan. Management of company is

continuously engaged with the investors to communicate details of their future activities to

involve them in process of decision making.

Tesco had developed effective monitoring procedures in order to identify and deal with

security incidents linked to the information technology. In addition to this, company had

9

developed Cyber Security team in order to mitigate the risks of cyber attacks. Executive

committee of the company also ensures performance risks by considering their targets based on

their new balanced scorecard of performance against KPIs and financial targets. Furthermore,

appropriable controls are place in processes such as product development, supplier management,

compliance with legal provisions and distribution of standards (Schroeder and Shepardson,

2016). For the prevention of financial frauds, dual control system is place in the business. This

system ensures that physical recording and book keeping task is not allocated to the similar

person. With the approach, comparison can be made in both the task for the purpose of

identification of discrepancies. Mainly this approach is applicable for management of cash and

Inventory in Tesco. By considering this approach, purchase of materials are processed by store

department and accounting records of purchase are managed by finance department. Similarly,

physical cash is maintained with treasures and accounting records are kept by finance

department. On the periodical basis, these balances are compared and appropriable actions are

taken for material differences.

3. Evaluation of risk of fraud within business and suggestion of method for detection

Fraud can be defined as deliberate activity conducted by individual from the objective to

deceive another individual. It is not essential that all business frauds have impact on financial

statement of company.

Overstatement of revenue

On the basis of annual report of Tesco, it can be noticed that major risk arises from the

supplier activities and excessive involvement of managerial persons in operational activities.

Annual report of company shows that, recently they had faced severe accounting scandal

regarding overstatement of profits. These misstatements were stated by considering rebate

provided by the suppliers in previous accounting period as profit of current accounting period

(Singh, 2015). In this aspect, directors have commented that this error is occurred by junior

employees of financial department.

For the prevention of such risks of fraud, management of Tesco can make use of IT tools

such as data mining. By making use of this tool, organization can detect accounting errors in an

effective manner. Furthermore, supervisors can monitor the work of subordinates to ensure that

correct accounting principles are followed by them in recording business transactions.

10

committee of the company also ensures performance risks by considering their targets based on

their new balanced scorecard of performance against KPIs and financial targets. Furthermore,

appropriable controls are place in processes such as product development, supplier management,

compliance with legal provisions and distribution of standards (Schroeder and Shepardson,

2016). For the prevention of financial frauds, dual control system is place in the business. This

system ensures that physical recording and book keeping task is not allocated to the similar

person. With the approach, comparison can be made in both the task for the purpose of

identification of discrepancies. Mainly this approach is applicable for management of cash and

Inventory in Tesco. By considering this approach, purchase of materials are processed by store

department and accounting records of purchase are managed by finance department. Similarly,

physical cash is maintained with treasures and accounting records are kept by finance

department. On the periodical basis, these balances are compared and appropriable actions are

taken for material differences.

3. Evaluation of risk of fraud within business and suggestion of method for detection

Fraud can be defined as deliberate activity conducted by individual from the objective to

deceive another individual. It is not essential that all business frauds have impact on financial

statement of company.

Overstatement of revenue

On the basis of annual report of Tesco, it can be noticed that major risk arises from the

supplier activities and excessive involvement of managerial persons in operational activities.

Annual report of company shows that, recently they had faced severe accounting scandal

regarding overstatement of profits. These misstatements were stated by considering rebate

provided by the suppliers in previous accounting period as profit of current accounting period

(Singh, 2015). In this aspect, directors have commented that this error is occurred by junior

employees of financial department.

For the prevention of such risks of fraud, management of Tesco can make use of IT tools

such as data mining. By making use of this tool, organization can detect accounting errors in an

effective manner. Furthermore, supervisors can monitor the work of subordinates to ensure that

correct accounting principles are followed by them in recording business transactions.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Dummy employees and alteration in payroll data

This fraud is identified in most of the organization. Mostly, dummy employees are shown

in payroll record of the company for the overstatement of expenses and this amount is used for

their personal benefits. Data related to the payroll can be easily manipulated by managerial

person provided with this job. This fraud can be detected by audits and surprise visits in which

random comparison of data and employees will be done (Jones, Comfort and Hillier, 2015).

Selection of strata for random evaluation will depend on the number of employees and

department in company. By considering the operational activities of Tesco, this audit will be

conducted separately in each department to identify such kind of frauds. Furthermore, evaluator

will be outsider for the prevention of biasness in checking.

By making use of these techniques, risk can be detected by management of Tesco and

they can take suitable actions for the prevention of such factors.

TASK 3

1. Planning of audit with reference to scope, materiality and risk

For the conduct of successful audit, it is essential for auditor to develop entire plan by

considering all the aspects. Planning procedure of audit work as road map through which auditor

will be able to achieve aims and objective in an effective manner. Planning procedure is required

to be complete before the start up of audit (Collings, 2012). Main objective of audit is to

determine the areas which will be focused in analysis and scrutiny. With this approach, auditor

will be able to cover entire significant area in a cost and time effective manner.

External audit is conducted with the objective to ensure accuracy of financial statement

prepared by company. For this aspect, financial and non financial facts of company are assessed

by auditor. On the basis of this assessment, auditors are able to identify potential frauds and error

and by considering these factors they provide expression of opinion to the stakeholders (Nelson,

2009). This entire process is completed by support of audit planning. In accordance with the

audit standards following three areas are required to be covered: Scope of audit Materiality Audit risk

Scope of audit

11

This fraud is identified in most of the organization. Mostly, dummy employees are shown

in payroll record of the company for the overstatement of expenses and this amount is used for

their personal benefits. Data related to the payroll can be easily manipulated by managerial

person provided with this job. This fraud can be detected by audits and surprise visits in which

random comparison of data and employees will be done (Jones, Comfort and Hillier, 2015).

Selection of strata for random evaluation will depend on the number of employees and

department in company. By considering the operational activities of Tesco, this audit will be

conducted separately in each department to identify such kind of frauds. Furthermore, evaluator

will be outsider for the prevention of biasness in checking.

By making use of these techniques, risk can be detected by management of Tesco and

they can take suitable actions for the prevention of such factors.

TASK 3

1. Planning of audit with reference to scope, materiality and risk

For the conduct of successful audit, it is essential for auditor to develop entire plan by

considering all the aspects. Planning procedure of audit work as road map through which auditor

will be able to achieve aims and objective in an effective manner. Planning procedure is required

to be complete before the start up of audit (Collings, 2012). Main objective of audit is to

determine the areas which will be focused in analysis and scrutiny. With this approach, auditor

will be able to cover entire significant area in a cost and time effective manner.

External audit is conducted with the objective to ensure accuracy of financial statement

prepared by company. For this aspect, financial and non financial facts of company are assessed

by auditor. On the basis of this assessment, auditors are able to identify potential frauds and error

and by considering these factors they provide expression of opinion to the stakeholders (Nelson,

2009). This entire process is completed by support of audit planning. In accordance with the

audit standards following three areas are required to be covered: Scope of audit Materiality Audit risk

Scope of audit

11

Audit scope can be defined as documents and amount of time involved in the procedure

of auditing. This scope depicts the extent to which in-depth analysis will be conducted. Scope of

present audit is to make assessment of corporate governance regarding risk of fraud and internal

control. On the basis of this assessment, opinion will be provided by auditor regarding fairness of

financial information.

In order to achieve this objective, auditor of FA Jet Ltd will evaluate financial statement

and other relevant information to identify frauds and clerical errors. Evaluation of data will be

done on the basis of random sampling in order to prevent biasness (Ismail, Ibrahim and Isa,

2006). In addition to this, meeting will be conducted with the directors who have resigned from

their posts to determine actual reason and their viewpoint regarding performance of company.

Materiality

Materiality is important factor to be considered in audit in order to enhance its reliability

and validity. In audit, materiality is a measure used for estimation of accuracy of financial

information provided by the company. Generally, all commercial information is not equally

information because of its nature and impact on economic decisions (Robertson and Davis,

2012). Due to this aspect, auditors are required to consider all significant aspects in their audit in

detail and remaining factors can be overviewed. With this approach, they will be cover the

significant aspects for detail assessment in order to achieve objectives of audit in an effective

manner. In present audit, main focus of auditor will be on effectiveness of internal control

system and accuracy of financial information provided.

Audit risk

Audit risk can be defined as probability that appointed auditor will be able to identify

errors and frauds in their assessment procedure or not. Audit risk is determined by auditor on the

basis of internal control system and possibility of inherent risk. It is because; effective internal

control reduces the possibilities of error (Nelson, 2009). Further, inherent risk cannot be

controlled or identified by the auditor if this risk is high then auditor is required to keep audit low

for the purpose of mitigation. In accordance with the provided case scenario, directors are

involved in entire department as there is high possibility of material misstatement. By

considering this aspect, auditor will ensure lower risk for the fair assessment.

12

of auditing. This scope depicts the extent to which in-depth analysis will be conducted. Scope of

present audit is to make assessment of corporate governance regarding risk of fraud and internal

control. On the basis of this assessment, opinion will be provided by auditor regarding fairness of

financial information.

In order to achieve this objective, auditor of FA Jet Ltd will evaluate financial statement

and other relevant information to identify frauds and clerical errors. Evaluation of data will be

done on the basis of random sampling in order to prevent biasness (Ismail, Ibrahim and Isa,

2006). In addition to this, meeting will be conducted with the directors who have resigned from

their posts to determine actual reason and their viewpoint regarding performance of company.

Materiality

Materiality is important factor to be considered in audit in order to enhance its reliability

and validity. In audit, materiality is a measure used for estimation of accuracy of financial

information provided by the company. Generally, all commercial information is not equally

information because of its nature and impact on economic decisions (Robertson and Davis,

2012). Due to this aspect, auditors are required to consider all significant aspects in their audit in

detail and remaining factors can be overviewed. With this approach, they will be cover the

significant aspects for detail assessment in order to achieve objectives of audit in an effective

manner. In present audit, main focus of auditor will be on effectiveness of internal control

system and accuracy of financial information provided.

Audit risk

Audit risk can be defined as probability that appointed auditor will be able to identify

errors and frauds in their assessment procedure or not. Audit risk is determined by auditor on the

basis of internal control system and possibility of inherent risk. It is because; effective internal

control reduces the possibilities of error (Nelson, 2009). Further, inherent risk cannot be

controlled or identified by the auditor if this risk is high then auditor is required to keep audit low

for the purpose of mitigation. In accordance with the provided case scenario, directors are

involved in entire department as there is high possibility of material misstatement. By

considering this aspect, auditor will ensure lower risk for the fair assessment.

12

2. Identification and explanation of appropriate audit tests for audit assignment

Audit tests are used by auditors to ensure key control on which they are relying are

effectively designed and supported by proper risk management. These tests can also be termed as

substantive procedures regarding activities performed by auditors for the detection of fraud at

different levels. Explanation of appropriate audit tests for audit assignment is enumerated as

below: Risk assessment procedure: This test is a collective procedure conducted to understand

operational activities and work environment of the entity. In this test, auditor will

evaluate internal control of FA Jet Ltd and on the basis of it they will describe risk

assessment procedures (Five types of audit tests, 2016). Objective of this test is to

identify risk of material misstatement in financial statements of company. Test of control: This test is solely focused on understanding of effectiveness of internal

control system used by company for monitoring and preventing errors. Test of control is

used to assess control risk for transactions related to the objectives of audit (Romney and

et al., 2006). Substantive test of transaction: Substantive test is focused on identification of clerical

errors that have direct impact on accuracy of financial statement prepared by FA Jet Ltd.

By this test, auditor ensures that all transaction related to the objectives of audit are in

accordance with the accounting standards. Analytical procedures: In this test, comparison is made by auditor of actual value

provided by company with the expectations made by them during planning procedure

(Five types of audit tests, 2016). Significant differences in the balances will provide them

areas in which there is high scope material misstatement.

Test for details of balances: This test is focused on assessing monetary correctness by

making comparison of ledger balances with the figures in income and position statement.

Details of this test is based on the results of test of controls.

Evidence for above described tests will be collected from financial records of FA Jet Ltd

and by considering verification from third parties.

13

Audit tests are used by auditors to ensure key control on which they are relying are

effectively designed and supported by proper risk management. These tests can also be termed as

substantive procedures regarding activities performed by auditors for the detection of fraud at

different levels. Explanation of appropriate audit tests for audit assignment is enumerated as

below: Risk assessment procedure: This test is a collective procedure conducted to understand

operational activities and work environment of the entity. In this test, auditor will

evaluate internal control of FA Jet Ltd and on the basis of it they will describe risk

assessment procedures (Five types of audit tests, 2016). Objective of this test is to

identify risk of material misstatement in financial statements of company. Test of control: This test is solely focused on understanding of effectiveness of internal

control system used by company for monitoring and preventing errors. Test of control is

used to assess control risk for transactions related to the objectives of audit (Romney and

et al., 2006). Substantive test of transaction: Substantive test is focused on identification of clerical

errors that have direct impact on accuracy of financial statement prepared by FA Jet Ltd.

By this test, auditor ensures that all transaction related to the objectives of audit are in

accordance with the accounting standards. Analytical procedures: In this test, comparison is made by auditor of actual value

provided by company with the expectations made by them during planning procedure

(Five types of audit tests, 2016). Significant differences in the balances will provide them

areas in which there is high scope material misstatement.

Test for details of balances: This test is focused on assessing monetary correctness by

making comparison of ledger balances with the figures in income and position statement.

Details of this test is based on the results of test of controls.

Evidence for above described tests will be collected from financial records of FA Jet Ltd

and by considering verification from third parties.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Types of record to be maintained during audit process

Auditors have statutory and ethical duty to record entire process of audit in an

appropriable manner. For this aspect, they are required to keep record of entire material

document during the process of audit. In accordance with the audit standards, all the document

work as legal evidence and thus it is required to be documented for the future assistance. This

duty has been described under provisions of IAS 20. Main objective of this standard is to provide

standard guidelines to auditors for recording and documentation of audit work in an proper way

(Ismail, Ibrahim and Isa, 2006). For the compliance of these standards, auditor of FA Jet Ltd

must kept record of their work. With this documentation, they will also be able to enhance

quality of work as it will assist them in preparing audit report. It is because; by reviewing entire

documents they will be able to conclude their opinion on fairness and truthfulness of provided

financial statements by company. Recording of audit process can be done by maintaining record

of following documents: Document of Information provided by company: External auditors of corporate entities

are required to document information provided by company in regular time interval.

Documentation of this information will facilitate auditor in enhancement of accuracy of

conclusion as entire facts and figures will be reviewed (Wicks, 2009). In addition to this,

documentation will work as legal evidence to provide justification of opinion provided by

the auditor of entity. As per the guidelines of ISA UK, documentation must be sufficient

to attain overall audit scope. Working papers of audit: Expression of opinion by auditors is provided on the basis of

analysis done by them by considering financial information of business. This analytical

work is also crucial part of audit because it justifies the final conclusion drawn by

auditor. There are no standard guidelines for preparing of working papers and it is

considered as asset of auditor (No, 2007). Thus, recording of working paper is on will of

audit and they are not in compulsion for it. However, recording of this paper assist them

in the future as it provides framework of previous audit. Communication letters: Auditors are required to maintain record of communication

conducted between their firm and company. For this aspect, they are required to

document appointment letter and management representation report. In addition to this,

14

Auditors have statutory and ethical duty to record entire process of audit in an

appropriable manner. For this aspect, they are required to keep record of entire material

document during the process of audit. In accordance with the audit standards, all the document

work as legal evidence and thus it is required to be documented for the future assistance. This

duty has been described under provisions of IAS 20. Main objective of this standard is to provide

standard guidelines to auditors for recording and documentation of audit work in an proper way

(Ismail, Ibrahim and Isa, 2006). For the compliance of these standards, auditor of FA Jet Ltd

must kept record of their work. With this documentation, they will also be able to enhance

quality of work as it will assist them in preparing audit report. It is because; by reviewing entire

documents they will be able to conclude their opinion on fairness and truthfulness of provided

financial statements by company. Recording of audit process can be done by maintaining record

of following documents: Document of Information provided by company: External auditors of corporate entities

are required to document information provided by company in regular time interval.

Documentation of this information will facilitate auditor in enhancement of accuracy of

conclusion as entire facts and figures will be reviewed (Wicks, 2009). In addition to this,

documentation will work as legal evidence to provide justification of opinion provided by

the auditor of entity. As per the guidelines of ISA UK, documentation must be sufficient

to attain overall audit scope. Working papers of audit: Expression of opinion by auditors is provided on the basis of

analysis done by them by considering financial information of business. This analytical

work is also crucial part of audit because it justifies the final conclusion drawn by

auditor. There are no standard guidelines for preparing of working papers and it is

considered as asset of auditor (No, 2007). Thus, recording of working paper is on will of

audit and they are not in compulsion for it. However, recording of this paper assist them

in the future as it provides framework of previous audit. Communication letters: Auditors are required to maintain record of communication

conducted between their firm and company. For this aspect, they are required to

document appointment letter and management representation report. In addition to this,

14

they are also required to record additional letters such as notice of meetings and circulars

given by board of FA Jet Ltd.

Audit report: This is the most crucial document of the audit process. For the

documentation of report standard guidelines has been described by ISQC. It is done at the

last stage of audit entire process is summarized and it does not include any new

information (Zadek, Evans and Pruzan, 2013). However, in necessary situations

following changes or additional points can be added by auditor:

▪ Collating, sorting and cross referencing of working papers

▪ Removal of unnecessary documents

▪ Audit evidence attained by auditor by relevant third parties.

For these changes auditors are required to provide justification of modification and its

impact on their opinion. Further, they are required to state that when and by whom

changes will take place.

4. Draft of audit report

Draft of Audit report by audit firm

To

Board of Directors of FA Jet Ltd.

Date: 31st December 2013

Executive summary

Auditors of our firm had evaluated financial statements of company FA Jet Ltd of 31st

December 2013. These statements were formulated by finance department thus inherent risk of

inaccuracy of data will be borne by directors and managerial persons of the company. Liability

of external auditors will be restricted to the opinion provided by them regarding financial

position.

Scope of Audit report

1. Assessment of sources of accounting records

2. Evaluation of internal control system of company

3. Verification of information provided by the management

Auditor had completed the audit work by considering provisions described under

international standards of auditing. For the assessment of accuracy of provided information

15

given by board of FA Jet Ltd.

Audit report: This is the most crucial document of the audit process. For the

documentation of report standard guidelines has been described by ISQC. It is done at the

last stage of audit entire process is summarized and it does not include any new

information (Zadek, Evans and Pruzan, 2013). However, in necessary situations

following changes or additional points can be added by auditor:

▪ Collating, sorting and cross referencing of working papers

▪ Removal of unnecessary documents

▪ Audit evidence attained by auditor by relevant third parties.

For these changes auditors are required to provide justification of modification and its

impact on their opinion. Further, they are required to state that when and by whom

changes will take place.

4. Draft of audit report

Draft of Audit report by audit firm

To

Board of Directors of FA Jet Ltd.

Date: 31st December 2013

Executive summary

Auditors of our firm had evaluated financial statements of company FA Jet Ltd of 31st

December 2013. These statements were formulated by finance department thus inherent risk of

inaccuracy of data will be borne by directors and managerial persons of the company. Liability

of external auditors will be restricted to the opinion provided by them regarding financial

position.

Scope of Audit report

1. Assessment of sources of accounting records

2. Evaluation of internal control system of company

3. Verification of information provided by the management

Auditor had completed the audit work by considering provisions described under

international standards of auditing. For the assessment of accuracy of provided information

15

auditor had considered statement from third party (Auditor and Management Reports, 2016).

Present audit also covers comment on the compliance by company of accounting policies and

norms described by the IASB and IFRS.

Opinion of auditor

By considering financial facts and other relevant information of the company it can be

noticed that control system of organization is less effective because managerial parties are

involved in audit committee. However, they provide assurance of accuracy through continuous

review on control system. Financial statements are prepared by considering standard described

in GAAP and IFRS. Third party verification shows that company had provided true and fair

information. On the basis of these facts, auditor had provided unqualified opinion to FA Jet Ltd

as financial statements published by them qualifies as per audit standards and it shows fair and

accurate picture of company.

Name of auditor:___________________

Signature:___________________

Date:___________________

Name of the firm:___________________

Address:___________________

5. Draft of management report

Draft of Management representation letter by FA Jet Ltd.

Name of auditor:___________________

Name of the firm:___________________

Date:___________________

This is to inform (name of firm), auditor of your firm is selected for the audit work of

financial statements prepared on 31st December 2003. Objective of this audit is to attain

expression of opinion of auditor regarding fairness and accuracy of financial statements of

16

Present audit also covers comment on the compliance by company of accounting policies and

norms described by the IASB and IFRS.

Opinion of auditor

By considering financial facts and other relevant information of the company it can be

noticed that control system of organization is less effective because managerial parties are

involved in audit committee. However, they provide assurance of accuracy through continuous

review on control system. Financial statements are prepared by considering standard described

in GAAP and IFRS. Third party verification shows that company had provided true and fair

information. On the basis of these facts, auditor had provided unqualified opinion to FA Jet Ltd

as financial statements published by them qualifies as per audit standards and it shows fair and

accurate picture of company.

Name of auditor:___________________

Signature:___________________

Date:___________________

Name of the firm:___________________

Address:___________________

5. Draft of management report

Draft of Management representation letter by FA Jet Ltd.

Name of auditor:___________________

Name of the firm:___________________

Date:___________________

This is to inform (name of firm), auditor of your firm is selected for the audit work of

financial statements prepared on 31st December 2003. Objective of this audit is to attain

expression of opinion of auditor regarding fairness and accuracy of financial statements of

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

company.

Senior management of company assures audit firm that provided documents and

information for audit is true as per their belief and risk of inaccuracy in this information will be

borne by FA Jet Ltd. Provided financial statements are as per the accounting norms and

principal and there is no material misstatement.

Relevancy of representation will include-

1. Financial information provided by the company is free from material irregularities as

managerial persons are involved in internal control of all departments.

2. Auditors of the firms are provided with the entire material information relevant for the

audit inspection. These documents are attached with directors reports, minutes of AGM

and EGM (Auditor and Management Reports, 2016).

3. Provided document contains completed information free from material defects and

omissions.

Edward W.

Signature:___________________

Date:___________________

Angus S.

Signature:___________________

Date:___________________

Robert B.

Signature:___________________

Date:___________________

CONCLUSION

Present study provides insight of accounting and auditing concepts that are required to be

used by business organization for the assurance of accuracy and reliability of financial

information provided by them. Companies are required to develop effective internal control

system for the prevention of material misstatements. In order to conduct effective audit, auditors

are required to develop complete plan by considering risk, materiality and scope. Furthermore,

they are required to make use of appropriable audit test in order to analyse accuracy and

17

Senior management of company assures audit firm that provided documents and

information for audit is true as per their belief and risk of inaccuracy in this information will be

borne by FA Jet Ltd. Provided financial statements are as per the accounting norms and

principal and there is no material misstatement.

Relevancy of representation will include-

1. Financial information provided by the company is free from material irregularities as

managerial persons are involved in internal control of all departments.

2. Auditors of the firms are provided with the entire material information relevant for the

audit inspection. These documents are attached with directors reports, minutes of AGM

and EGM (Auditor and Management Reports, 2016).

3. Provided document contains completed information free from material defects and

omissions.

Edward W.

Signature:___________________

Date:___________________

Angus S.

Signature:___________________

Date:___________________

Robert B.

Signature:___________________

Date:___________________

CONCLUSION

Present study provides insight of accounting and auditing concepts that are required to be

used by business organization for the assurance of accuracy and reliability of financial

information provided by them. Companies are required to develop effective internal control

system for the prevention of material misstatements. In order to conduct effective audit, auditors

are required to develop complete plan by considering risk, materiality and scope. Furthermore,

they are required to make use of appropriable audit test in order to analyse accuracy and

17

reliability of financial statements. In accordance with the audit standards of UK, they are

required to record entire audit work in proper way as it will work as legal evidence in the future

assistance.

18

required to record entire audit work in proper way as it will work as legal evidence in the future

assistance.

18

REFERENCES

Books and journals

Adams, C. A., 2002. Internal organisational factors influencing corporate social and ethical

reporting: Beyond current theorising. Accounting, Auditing & Accountability Journal.

15(2). pp. 223-250.

Alexander, D. and Archer, S., 2010. On the myth of “Anglo-Saxon” financial accounting. The

International Journal of Accounting. 35(4). pp. 539-557.

Arens, A. A., Elder, R. J. and Beasley, M. S., 2010. Auditing: An integrated approach (Vol. 8).

Upper Saddle River, NJ: Prentice Hall.

Clatworthy, M. A., 2013. The impact of voluntary audit and governance characteristics on

accounting errors in private companies. Journal of Accounting and Public Policy, 32(3),

1-25.

Hallikas, J. and et al., 2004. Risk management processes in supplier networks. International

Journal of Production Economics. 90(1). pp. 47-58.

Hronsky, J. J. and et al., 2010. The meaning of a defined accounting concept: Regulatory

changes and the effect on auditor decision making. Accounting, Organizations and Society.

26(2). pp. 123-139.

Ismail, I., Ibrahim, D. and Isa, S., 2006. Service quality, client satisfaction and loyalty towards

audit firms: Perceptions of Malaysian public listed companies. Managerial Auditing

Journal. 21(7). pp. 738 – 756.

Jones, P., Comfort, D. and Hillier, D., 2015. Materiality in corporate sustainability reporting

within UK retailing. Journal of Public Affairs. 2(3). pp. 15 – 25.

Nelson, M. W., 2009. A model and literature review of professional skepticism in auditing.

Auditing: A Journal of Practice & theory. 28(2). pp. 1 – 34.

No, A. S., 2007. An Audit of Internal Control Over Financial Reporting That Is Integrated with

An Audit of Financial Statements. AUDITING.

Paulsson, G., 2006. Accrual accounting in the public sector: experiences from the central

government in Sweden. Financial Accountability & Management. 22(1). pp. 47-62.

Power, M., 2010. Auditing and environmental expertise: between protest and professionalisation.

Accounting, Auditing & Accountability Journal. 4(3). pp. 1 – 25.

19

Books and journals

Adams, C. A., 2002. Internal organisational factors influencing corporate social and ethical

reporting: Beyond current theorising. Accounting, Auditing & Accountability Journal.

15(2). pp. 223-250.

Alexander, D. and Archer, S., 2010. On the myth of “Anglo-Saxon” financial accounting. The

International Journal of Accounting. 35(4). pp. 539-557.

Arens, A. A., Elder, R. J. and Beasley, M. S., 2010. Auditing: An integrated approach (Vol. 8).

Upper Saddle River, NJ: Prentice Hall.

Clatworthy, M. A., 2013. The impact of voluntary audit and governance characteristics on

accounting errors in private companies. Journal of Accounting and Public Policy, 32(3),

1-25.

Hallikas, J. and et al., 2004. Risk management processes in supplier networks. International

Journal of Production Economics. 90(1). pp. 47-58.

Hronsky, J. J. and et al., 2010. The meaning of a defined accounting concept: Regulatory

changes and the effect on auditor decision making. Accounting, Organizations and Society.

26(2). pp. 123-139.

Ismail, I., Ibrahim, D. and Isa, S., 2006. Service quality, client satisfaction and loyalty towards

audit firms: Perceptions of Malaysian public listed companies. Managerial Auditing

Journal. 21(7). pp. 738 – 756.

Jones, P., Comfort, D. and Hillier, D., 2015. Materiality in corporate sustainability reporting

within UK retailing. Journal of Public Affairs. 2(3). pp. 15 – 25.

Nelson, M. W., 2009. A model and literature review of professional skepticism in auditing.

Auditing: A Journal of Practice & theory. 28(2). pp. 1 – 34.

No, A. S., 2007. An Audit of Internal Control Over Financial Reporting That Is Integrated with

An Audit of Financial Statements. AUDITING.

Paulsson, G., 2006. Accrual accounting in the public sector: experiences from the central

government in Sweden. Financial Accountability & Management. 22(1). pp. 47-62.

Power, M., 2010. Auditing and environmental expertise: between protest and professionalisation.

Accounting, Auditing & Accountability Journal. 4(3). pp. 1 – 25.

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ritchie, B. and Brindley, C., 2007. Supply chain risk management and performance: A guiding

framework for future development. International Journal of Operations & Production

Management. 27(3). pp. 303-322.

Robertson, J. C. and Davis, F. G., 2012. Auditing. Homewood, IL: Irwin.

Romney, M. B. and et al., 2006. Accounting information systems. Englewood Cliffs, NJ: Prentice

Hall.

Schroeder, J.H. and Shepardson, M.L., 2016. Do SOX 404 Control Audits and Management

Assessments Improve Overall Internal Control System Quality?. The Accounting Review.

24(3). pp. 15 – 25.

Singh, S., 2015. Role of internal control system in credit risk identification process of selected

public and private sector banks. ZENITH International Journal of Business Economics &

Management Research. 5(6). pp.276-286.

Wood, S., Wrigley, N. and Coe, N.M., 2016. Capital discipline and financial market relations in

retail globalization: insights from the case of Tesco plc. Journal of Economic Geography.

p.lbv045.

Wright, C. F., 2015. Leveraging reputational risk: Sustainable sourcing campaigns for improving

labour standards in production networks. Journal of Business Ethics. pp.1-16.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building Corporate Accountability: Emerging

Practice in Social and Ethical Accounting and Auditing. Routledge.

Online

Auditor and Management Reports. 2016. [Online] Available through:

<https://www.boundless.com/accounting/textbooks/boundless-accounting-textbook/