Analysis of Costing Methods: Traditional vs. Activity-Based Costing

VerifiedAdded on 2021/05/31

|15

|2611

|225

Homework Assignment

AI Summary

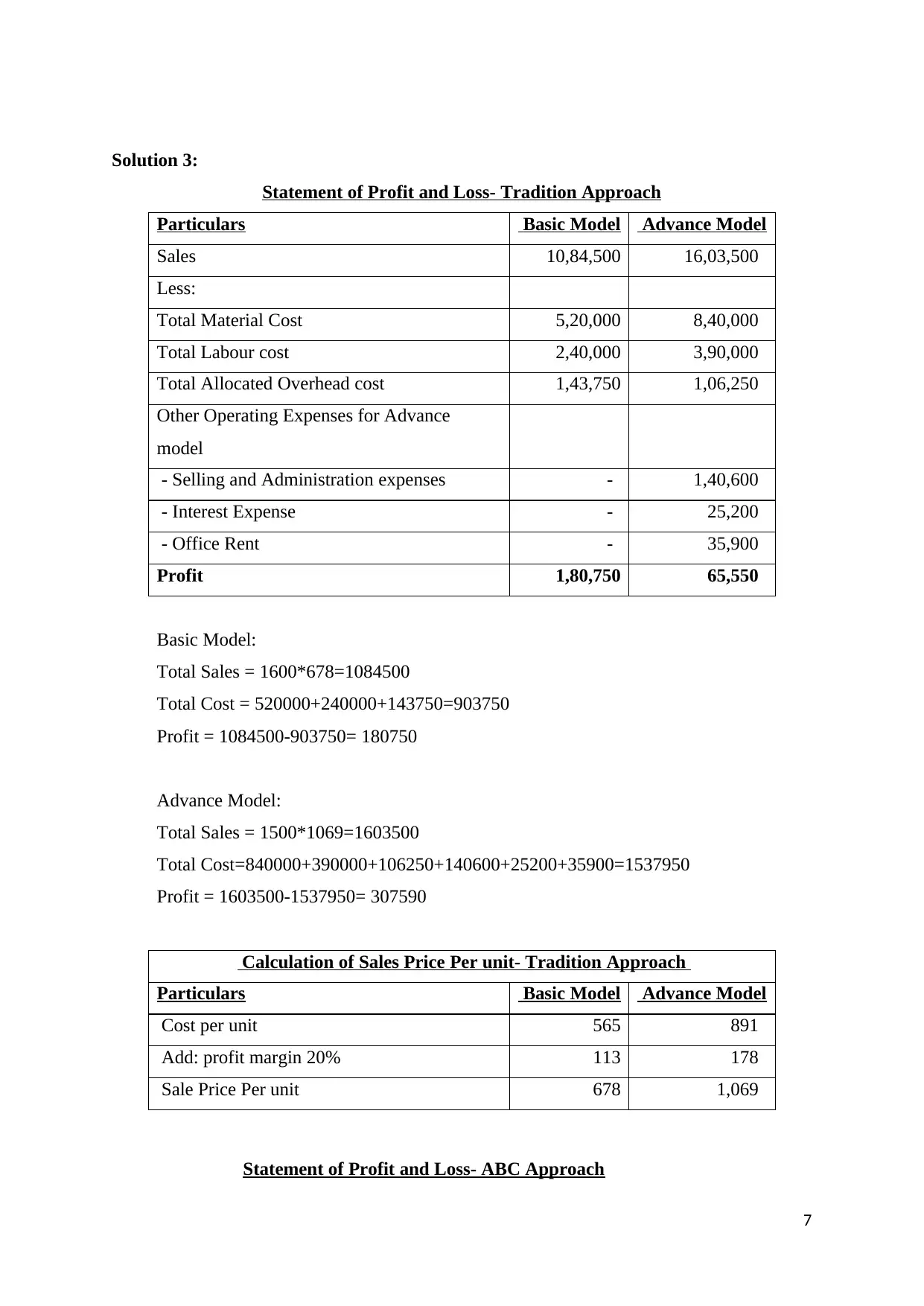

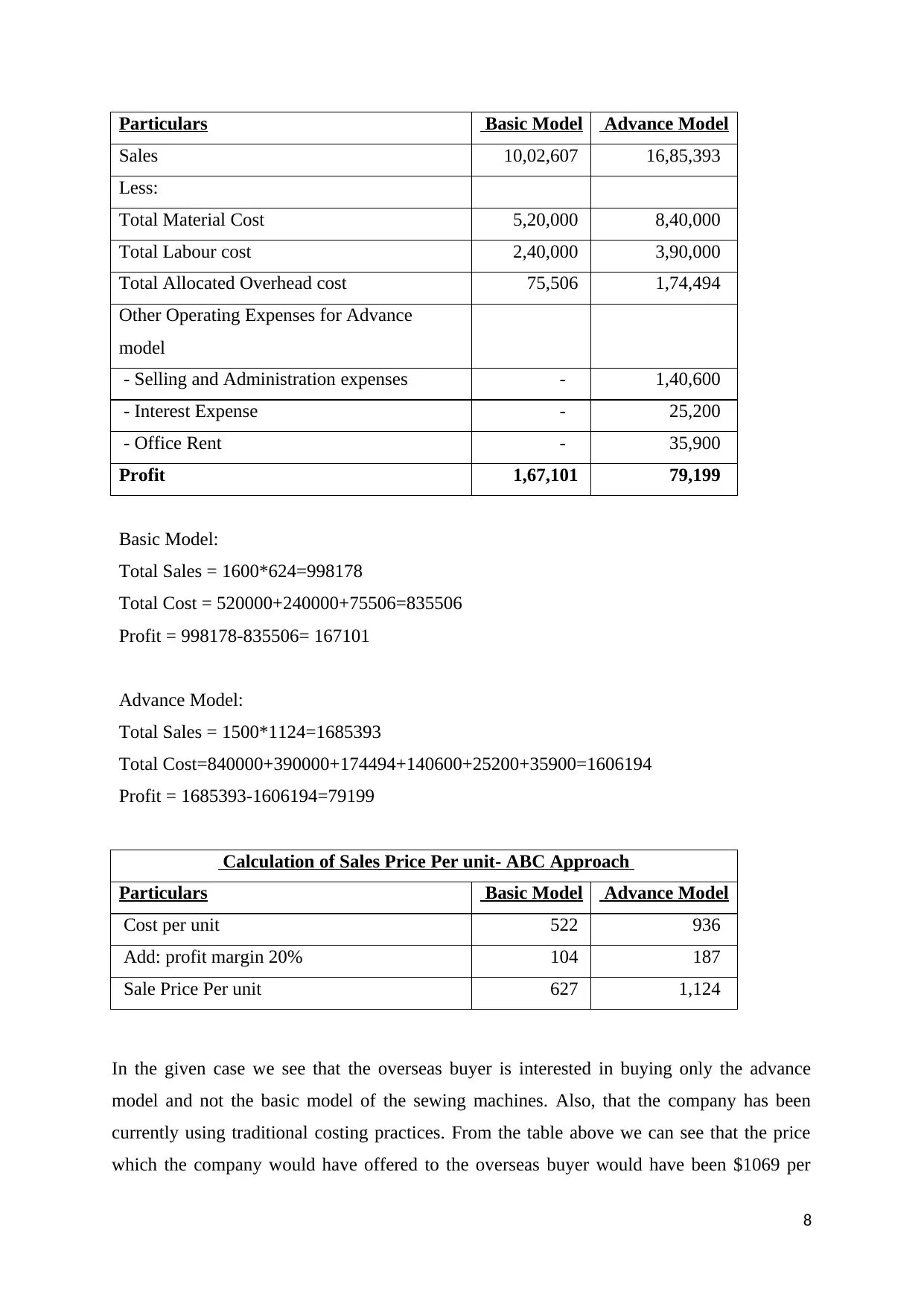

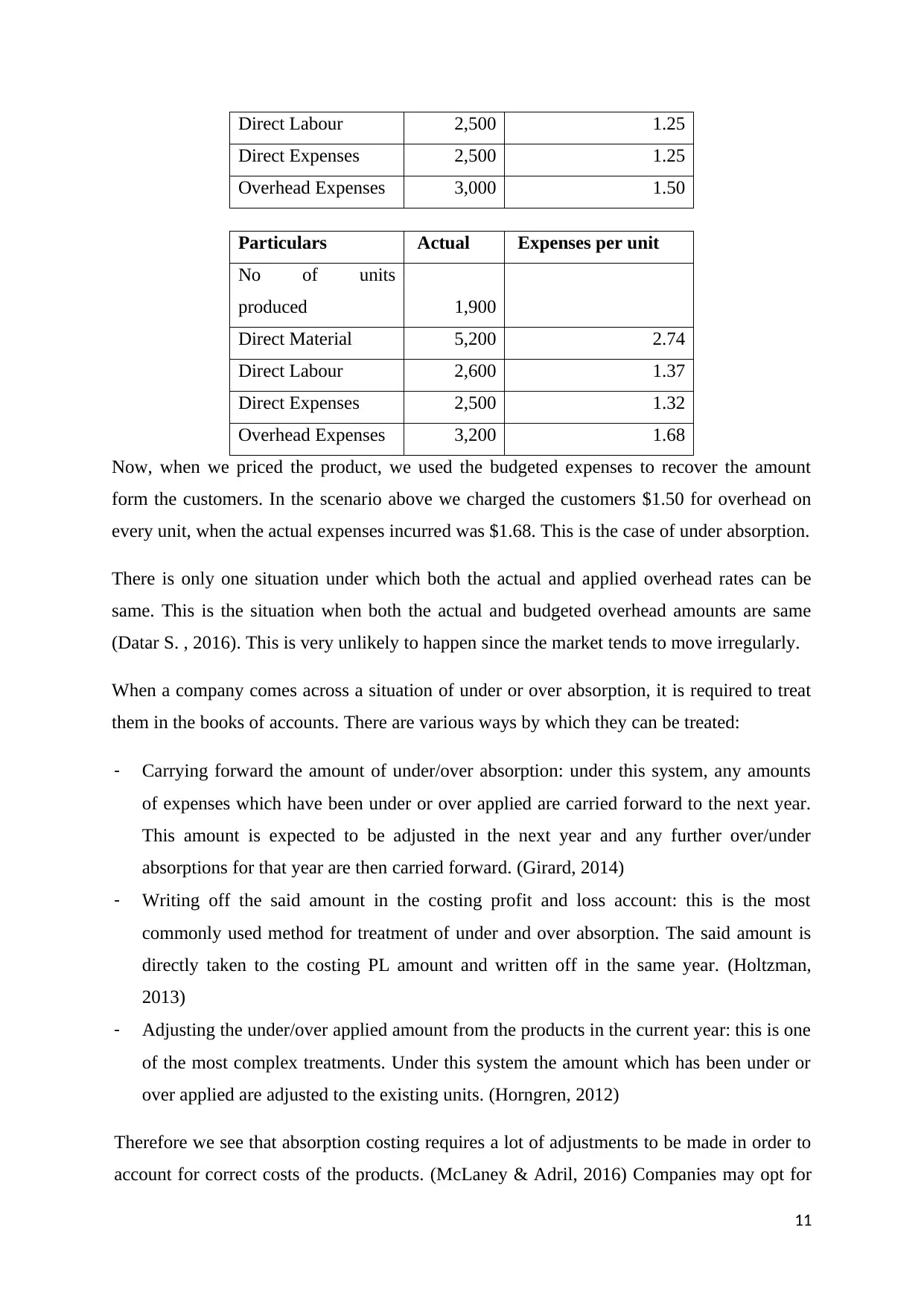

This assignment analyzes cost accounting methods, focusing on traditional and activity-based costing (ABC) approaches. It begins with a comparative analysis of two models, Basic and Advance, using the traditional costing method, calculating total costs and cost per unit. The solution then presents the same models using ABC, demonstrating how overhead costs are allocated differently, impacting the final cost per unit. A profit and loss statement is then created using both costing methods, showing how sales prices and profit margins are affected. The assignment then examines overhead expenses and how they are allocated, discussing the impact of under and over absorption of overheads. Finally, it explores the advantages and disadvantages of ABC, highlighting its accuracy in calculating product costs, its role in cost control, and its limitations, such as complexity and suitability for certain industries. This assignment is a comprehensive overview of cost accounting principles and their practical application.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.