Accounting Information System for Stratford on Murray

VerifiedAdded on 2020/06/04

|8

|1933

|101

AI Summary

This assignment examines the implementation of an Accounting Information System (AIS) for Stratford on Murray. It analyzes the benefits of an AIS, including improved data security through physical measures and anti-virus software, and explores key principles and practices of budgetary control within the system. The document also outlines procedures for recording and storing financial data, emphasizing the importance of accuracy, compliance with legislation, and ethical considerations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

INTRODUCTION TO MARKETING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................3

Key features and code of practices for accounting system..........................................................3

Ethical considerations for financial reconstruction.....................................................................4

Key features of financial legislation related to tax consideration and reporting requirements...4

Outlining a range of consideration for accounting system specification.....................................4

Compare and contrast data protection method............................................................................4

Key principles and practice of budgetary control........................................................................5

Process and procedure for recording and storing financial data..................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................3

Key features and code of practices for accounting system..........................................................3

Ethical considerations for financial reconstruction.....................................................................4

Key features of financial legislation related to tax consideration and reporting requirements...4

Outlining a range of consideration for accounting system specification.....................................4

Compare and contrast data protection method............................................................................4

Key principles and practice of budgetary control........................................................................5

Process and procedure for recording and storing financial data..................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Accounting Information System (AIS) is a software that gathers, warehouse, manage,

process and retrieve finacial data automatically that can be used by the policymakers for

decision-making purpose. Stratford on Murray delivers cosmetic items and giftware to the

buyers. Company had planned to implement AIS in the business, thus, the thrust of the paper is

to prpare a deep plan how the system can be implemented by the business successfully including

key consideration i.e. system specification, design, data protection, testing, configuration,

compliance, integrity, ethical implications and others.

TASK 1 Objectives of Accounting system: Major objective of developing accounting system is to

ensure that firm will receive entire records as per requirement and reports will be

prepared automatically. System specification: In system different options will be developed in respect to

preparing income statement, balance sheet or any other statement. System will be able to

operated in OS like Windows and Ubuntu with small space in hard disk.

System design: In system there will be three functionalities like strategic, tactical and

operational as well as transaction processing systems. Within these functionalities there

will be different options available ( Mancini, Vaassen and Ameri, 2014). For example in

strategic system there will be options for ratio analysis etc.

1 | P a g e

Accounting Information System (AIS) is a software that gathers, warehouse, manage,

process and retrieve finacial data automatically that can be used by the policymakers for

decision-making purpose. Stratford on Murray delivers cosmetic items and giftware to the

buyers. Company had planned to implement AIS in the business, thus, the thrust of the paper is

to prpare a deep plan how the system can be implemented by the business successfully including

key consideration i.e. system specification, design, data protection, testing, configuration,

compliance, integrity, ethical implications and others.

TASK 1 Objectives of Accounting system: Major objective of developing accounting system is to

ensure that firm will receive entire records as per requirement and reports will be

prepared automatically. System specification: In system different options will be developed in respect to

preparing income statement, balance sheet or any other statement. System will be able to

operated in OS like Windows and Ubuntu with small space in hard disk.

System design: In system there will be three functionalities like strategic, tactical and

operational as well as transaction processing systems. Within these functionalities there

will be different options available ( Mancini, Vaassen and Ameri, 2014). For example in

strategic system there will be options for ratio analysis etc.

1 | P a g e

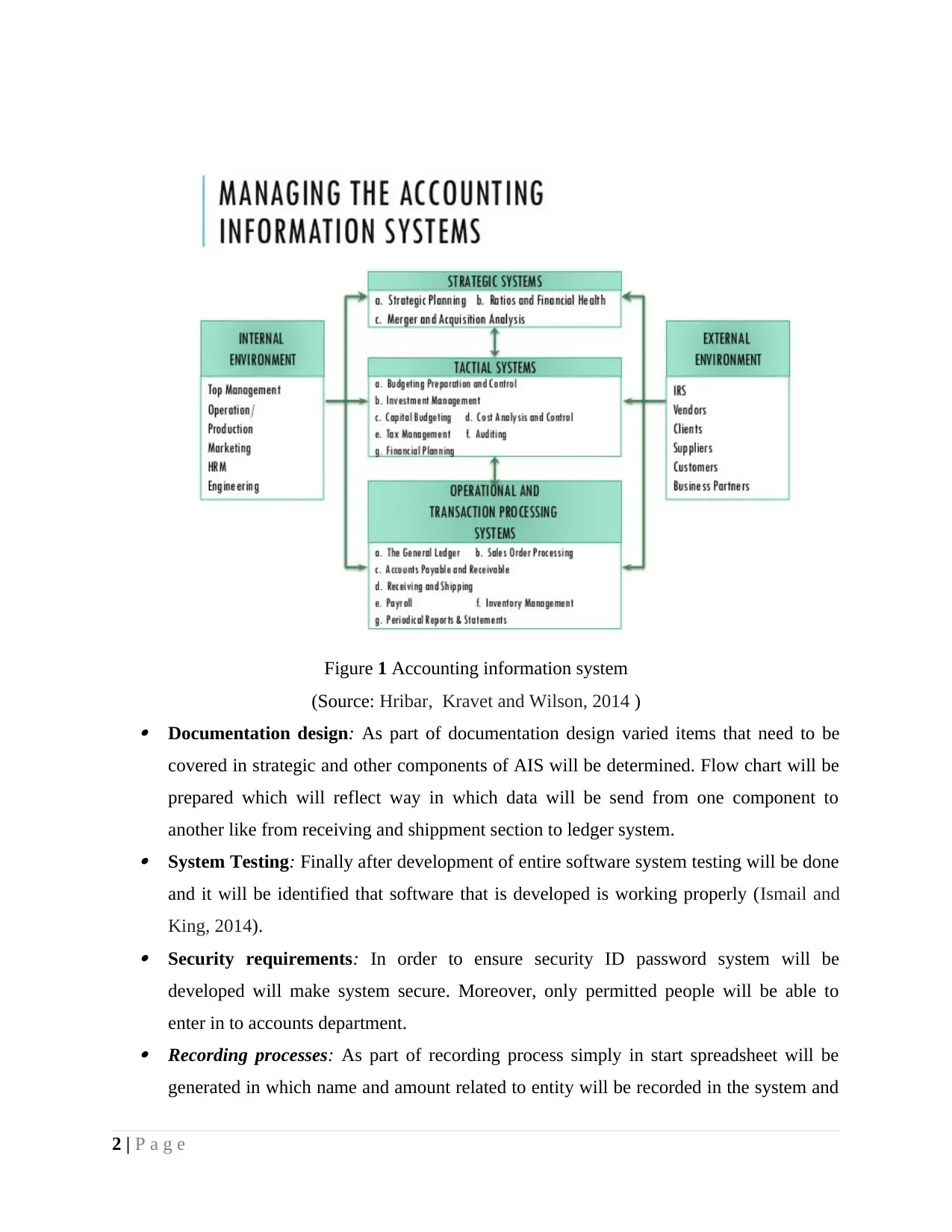

Figure 1 Accounting information system

(Source: Hribar, Kravet and Wilson, 2014 ) Documentation design: As part of documentation design varied items that need to be

covered in strategic and other components of AIS will be determined. Flow chart will be

prepared which will reflect way in which data will be send from one component to

another like from receiving and shippment section to ledger system. System Testing: Finally after development of entire software system testing will be done

and it will be identified that software that is developed is working properly (Ismail and

King, 2014). Security requirements: In order to ensure security ID password system will be

developed will make system secure. Moreover, only permitted people will be able to

enter in to accounts department. Recording processes: As part of recording process simply in start spreadsheet will be

generated in which name and amount related to entity will be recorded in the system and

2 | P a g e

(Source: Hribar, Kravet and Wilson, 2014 ) Documentation design: As part of documentation design varied items that need to be

covered in strategic and other components of AIS will be determined. Flow chart will be

prepared which will reflect way in which data will be send from one component to

another like from receiving and shippment section to ledger system. System Testing: Finally after development of entire software system testing will be done

and it will be identified that software that is developed is working properly (Ismail and

King, 2014). Security requirements: In order to ensure security ID password system will be

developed will make system secure. Moreover, only permitted people will be able to

enter in to accounts department. Recording processes: As part of recording process simply in start spreadsheet will be

generated in which name and amount related to entity will be recorded in the system and

2 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

then same data will be transferred to journal system and ledger system. Thus, data will be

recorded and processed in proper manner Implementation plan: In order to implement system testing will be done by entering

varied transactions and after verification software will be installed in relevant systems. In

this way software will be installed in system (Smith and Binti, 2016). Training Schedules: In respect to training schedules on daily basis up to 10 days training

will be given to the employees at workplace. Compliance: As per requirement time to time company registration statements, annual

profit and loss statement, report of statements made to business and report on purchase

and sale of stock. In system with requirements compliance will be done. Integrity of system: Integrity refers to situation where accounting information must be

complete, unbroken, unimpaired and sound etc (Hribar, Kravet and Wilson, 2014). Reporting requirements: Buisness firms need to report their income statement and

balance sheet time to time to regulatory authority. There are strict rules and regulations in

respect to reporting and it is very important to do all these things perfectly in order to

aboid any legal action. Reporting Procedures: In software automated system will be developed and under this

on entry of transactions automatically different accounts will be developed and forwarded

to the relevant stakeholders like managers. Evaluation and modification of accounting system or continuous improvement: Time

to time accounting system will be evaluated and modified. Researchers will identify if

there any loopholes in same and accordingly changes will be made in the system.

TASK 2

Key features and code of practices for accounting system

There are lots of features of accounting system and under this there must be automatic

report generation feature. Aaprt from this, automatically performnance analysis must also be

supported by system. In accouting system raw values must be inputted for calculation purpose by

following accounting standards, policy and procedures (Adenike and Michael, 2016). By doing

so it can be ensured that right inputs are entered in to system for calculation purpose. There must

be specific accounting policy in an organization and must be followed for calculation purpose

and recording of transactions (Wijaya and et.al.,2015). By doing so it is esnsured that calculation

3 | P a g e

recorded and processed in proper manner Implementation plan: In order to implement system testing will be done by entering

varied transactions and after verification software will be installed in relevant systems. In

this way software will be installed in system (Smith and Binti, 2016). Training Schedules: In respect to training schedules on daily basis up to 10 days training

will be given to the employees at workplace. Compliance: As per requirement time to time company registration statements, annual

profit and loss statement, report of statements made to business and report on purchase

and sale of stock. In system with requirements compliance will be done. Integrity of system: Integrity refers to situation where accounting information must be

complete, unbroken, unimpaired and sound etc (Hribar, Kravet and Wilson, 2014). Reporting requirements: Buisness firms need to report their income statement and

balance sheet time to time to regulatory authority. There are strict rules and regulations in

respect to reporting and it is very important to do all these things perfectly in order to

aboid any legal action. Reporting Procedures: In software automated system will be developed and under this

on entry of transactions automatically different accounts will be developed and forwarded

to the relevant stakeholders like managers. Evaluation and modification of accounting system or continuous improvement: Time

to time accounting system will be evaluated and modified. Researchers will identify if

there any loopholes in same and accordingly changes will be made in the system.

TASK 2

Key features and code of practices for accounting system

There are lots of features of accounting system and under this there must be automatic

report generation feature. Aaprt from this, automatically performnance analysis must also be

supported by system. In accouting system raw values must be inputted for calculation purpose by

following accounting standards, policy and procedures (Adenike and Michael, 2016). By doing

so it can be ensured that right inputs are entered in to system for calculation purpose. There must

be specific accounting policy in an organization and must be followed for calculation purpose

and recording of transactions (Wijaya and et.al.,2015). By doing so it is esnsured that calculation

3 | P a g e

is done in proper manner. In order to check whether accounting policies are performed in proper

manner one can enter fake transaction in system and can check that in what way employees

doing treatment. On loophole areas work can be done to improve system.

Ethical considerations for financial reconstruction

There are several ethical considerations needs to be comply with in implementing AIS.

All the parties engaged with the system need to work ethically without any misleading actiona

and fraudulent activities (Abdallah, 2014). People who entre data into the system must input

authentic data set and do not manipulate the reports and other key findings. In despite of this,

data privacy legislation need to follow to secure data safety.

Key features of financial legislation related to tax consideration and reporting requirements

In Australia, Financial Transaction Reports Act 1988 applies in administrating and

encorcing tax based laws. According to this, Stratford on Murray needs to provide correct

finacnail reports to the taxation authorities and pay tax timely. However, with reference to

financail reporting, company need to comply with Corporation Act 2001 according to which, a

compiled set of annual statement including income statement, balance sheet, cash flow

statements need to be constructed. With respect to AIS, standard business reporting (SBR)

approach also ned to be followed that applied on digital record keeping system and accounting

software. It allow firms to reduce their time invested in collating information in different form

and its submission.

Outlining a range of consideration for accounting system specification

There are range of factors needs to be taken into account for Software Requirement

Specification (SRS) including functional and non-functional requirements, interface and

requirement of software. Moreover, before deciding specfication, Stratford on Murray need to

look over the system specific attributes like reliability, availability, security, maintainability and

portability as well (Smith and Binti, 2016). With reference to product perspective, system

interface, hardware & software interface, communication interface and others. All the factors

need to be examined thoroughly in line with the AIS requirements.

Compare and contrast data protection method

AIS will be a password protected system in which, password will be inserted so that only

the authorized party can access the system. Thus, in order to run system, user will require login

ID and password for authentication. Moreover, system will be placed at a safe place to eliminate

4 | P a g e

manner one can enter fake transaction in system and can check that in what way employees

doing treatment. On loophole areas work can be done to improve system.

Ethical considerations for financial reconstruction

There are several ethical considerations needs to be comply with in implementing AIS.

All the parties engaged with the system need to work ethically without any misleading actiona

and fraudulent activities (Abdallah, 2014). People who entre data into the system must input

authentic data set and do not manipulate the reports and other key findings. In despite of this,

data privacy legislation need to follow to secure data safety.

Key features of financial legislation related to tax consideration and reporting requirements

In Australia, Financial Transaction Reports Act 1988 applies in administrating and

encorcing tax based laws. According to this, Stratford on Murray needs to provide correct

finacnail reports to the taxation authorities and pay tax timely. However, with reference to

financail reporting, company need to comply with Corporation Act 2001 according to which, a

compiled set of annual statement including income statement, balance sheet, cash flow

statements need to be constructed. With respect to AIS, standard business reporting (SBR)

approach also ned to be followed that applied on digital record keeping system and accounting

software. It allow firms to reduce their time invested in collating information in different form

and its submission.

Outlining a range of consideration for accounting system specification

There are range of factors needs to be taken into account for Software Requirement

Specification (SRS) including functional and non-functional requirements, interface and

requirement of software. Moreover, before deciding specfication, Stratford on Murray need to

look over the system specific attributes like reliability, availability, security, maintainability and

portability as well (Smith and Binti, 2016). With reference to product perspective, system

interface, hardware & software interface, communication interface and others. All the factors

need to be examined thoroughly in line with the AIS requirements.

Compare and contrast data protection method

AIS will be a password protected system in which, password will be inserted so that only

the authorized party can access the system. Thus, in order to run system, user will require login

ID and password for authentication. Moreover, system will be placed at a safe place to eliminate

4 | P a g e

the threatening against physical loss or theft. Cables and switches will be keep locked addressing

safety ( Simkin, Norman and Rose, 2014). Computers are subjected to viruses therefore, anti-

virus software will be used to overcome the risk of hackers attack. However, such measures may

consumes too much cost, therefore, it is much better to take preventive measures to protect the

system unfront cost.

Key principles and practice of budgetary control

Budgetary control is a method of developing budget for future plan and examining actual

performance of the business entity with the targeted ones. It is the best way to evalaute

performance and take quality decisions to control cost, boost savings and maximize revenues of

the business. Stratford on Murray had decided to implement Accounting information system

which will utilize past years results of the business and accordingly, budgets will be designed for

the coming year (Abdallah, 2014). The system will enable company to track record of their

trading results and help firm in gaining an insight towards future by developing budget. Such

framework will assist firm in sound business planning and strong decisions.

Process and procedure for recording and storing financial data

Data will be recorded manually by staff member of Stratford on Murray complying with

key legislations and code of conduct. Interim audit or internal check will be maintained to make

sure that correct data is entered that is free from any manipulation and fradulent activities.

CONCLUSION

From the discussion, it become clear that AIS will really helpful for Stratford on Murray

to keep data secure in computerized form and generate customized reports as per the

requirements. The report inferred that ethical aspects, data protection, confidentiality are several

key legislation that must be complied with including adherene with code of conduct.

5 | P a g e

safety ( Simkin, Norman and Rose, 2014). Computers are subjected to viruses therefore, anti-

virus software will be used to overcome the risk of hackers attack. However, such measures may

consumes too much cost, therefore, it is much better to take preventive measures to protect the

system unfront cost.

Key principles and practice of budgetary control

Budgetary control is a method of developing budget for future plan and examining actual

performance of the business entity with the targeted ones. It is the best way to evalaute

performance and take quality decisions to control cost, boost savings and maximize revenues of

the business. Stratford on Murray had decided to implement Accounting information system

which will utilize past years results of the business and accordingly, budgets will be designed for

the coming year (Abdallah, 2014). The system will enable company to track record of their

trading results and help firm in gaining an insight towards future by developing budget. Such

framework will assist firm in sound business planning and strong decisions.

Process and procedure for recording and storing financial data

Data will be recorded manually by staff member of Stratford on Murray complying with

key legislations and code of conduct. Interim audit or internal check will be maintained to make

sure that correct data is entered that is free from any manipulation and fradulent activities.

CONCLUSION

From the discussion, it become clear that AIS will really helpful for Stratford on Murray

to keep data secure in computerized form and generate customized reports as per the

requirements. The report inferred that ethical aspects, data protection, confidentiality are several

key legislation that must be complied with including adherene with code of conduct.

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abdallah, A.A.J., 2014. The impact of using accounting information systems on the quality of

financial statements submitted to the Income and sales tax Department in

Jordan. European Scientific Journal, ESJ. 9(10).

Adenike, A.T. and Michael, A.A., 2016. Effect of Accounting Information System Adoption on

Accounting Activities in Manufacturing Industries in Nigeria.

Hribar, P., Kravet, T. and Wilson, R., 2014. A new measure of accounting quality. Review of

Accounting Studies. 19(1). pp.506-538.

Ismail, N.A. and King, M., 2014. Factors influencing the alignment of accounting information

systems in small and medium sized Malaysian manufacturing firms. Journal of

Information Systems and Small Business. 1(1-2). pp.1-20.

M Ancini, D.A.A., Vaassen, E.H. and D Ameri, R.A.A., 2014. Accounting information systems

for decision making. Springer,.

Simkin, M.G., Norman, C.S. and Rose, J.M., 2014. Core concepts of accounting information

systems. John Wiley & Sons.

Smith, J. and Binti Puasa, S., 2016, February. Critical factors of accounting information systems

(AIS) effectiveness: a qualitative study of the Malaysian federal government. In British

Accounting & Finance Association Annual Conference 2016.

Wijaya, R.E., and et.al.,, 2015. Paradigm Blurred: Opera Cake in Management Accounting

Information Research. Procedia-Social and Behavioral Sciences. 211. pp.859-865.

6 | P a g e

Books and Journals

Abdallah, A.A.J., 2014. The impact of using accounting information systems on the quality of

financial statements submitted to the Income and sales tax Department in

Jordan. European Scientific Journal, ESJ. 9(10).

Adenike, A.T. and Michael, A.A., 2016. Effect of Accounting Information System Adoption on

Accounting Activities in Manufacturing Industries in Nigeria.

Hribar, P., Kravet, T. and Wilson, R., 2014. A new measure of accounting quality. Review of

Accounting Studies. 19(1). pp.506-538.

Ismail, N.A. and King, M., 2014. Factors influencing the alignment of accounting information

systems in small and medium sized Malaysian manufacturing firms. Journal of

Information Systems and Small Business. 1(1-2). pp.1-20.

M Ancini, D.A.A., Vaassen, E.H. and D Ameri, R.A.A., 2014. Accounting information systems

for decision making. Springer,.

Simkin, M.G., Norman, C.S. and Rose, J.M., 2014. Core concepts of accounting information

systems. John Wiley & Sons.

Smith, J. and Binti Puasa, S., 2016, February. Critical factors of accounting information systems

(AIS) effectiveness: a qualitative study of the Malaysian federal government. In British

Accounting & Finance Association Annual Conference 2016.

Wijaya, R.E., and et.al.,, 2015. Paradigm Blurred: Opera Cake in Management Accounting

Information Research. Procedia-Social and Behavioral Sciences. 211. pp.859-865.

6 | P a g e

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.