Introductory Finance and Accounting TCA Answer Book –ACC10032122 1st Examination Module Number

VerifiedAdded on 2023/06/14

|10

|1725

|78

AI Summary

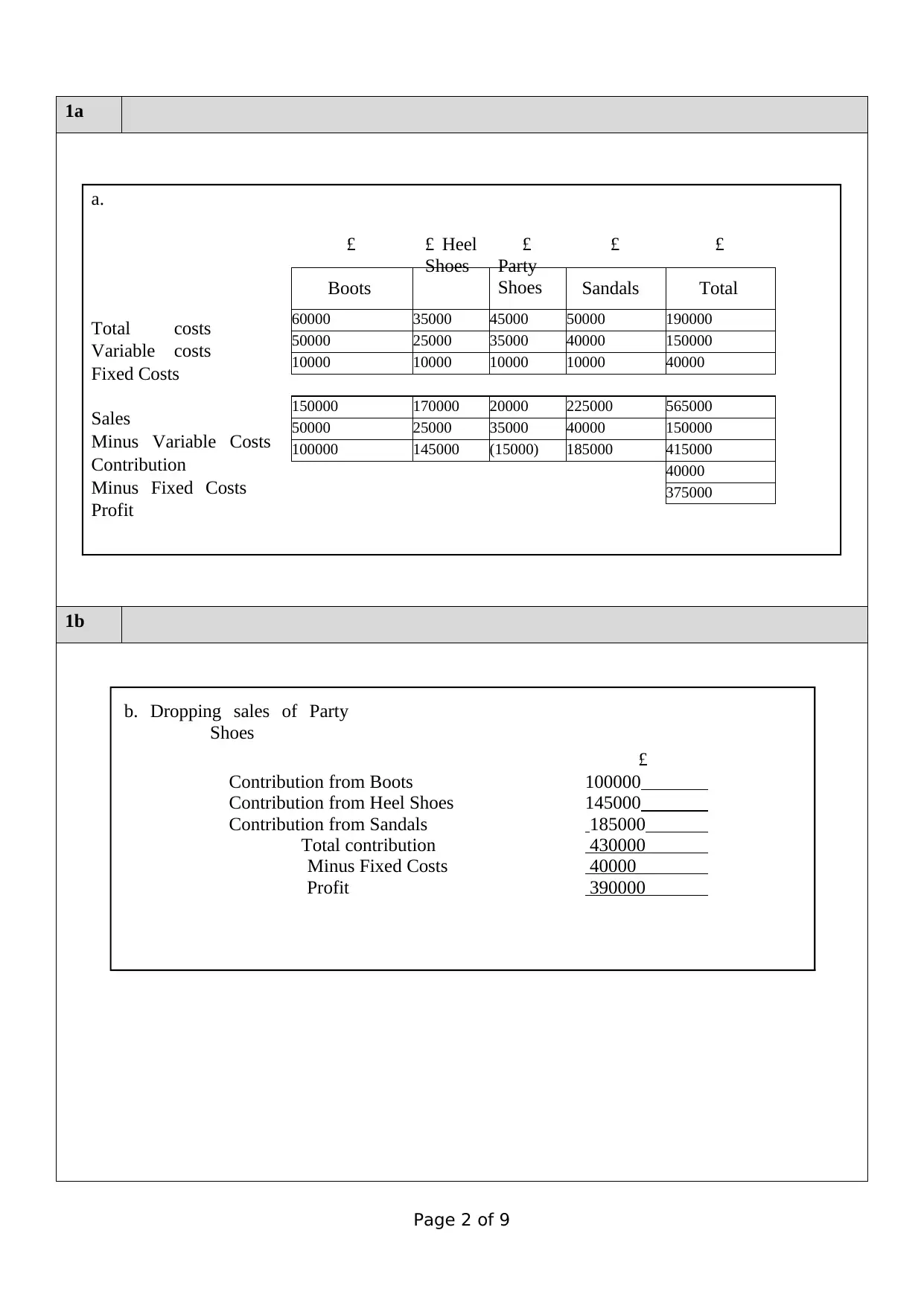

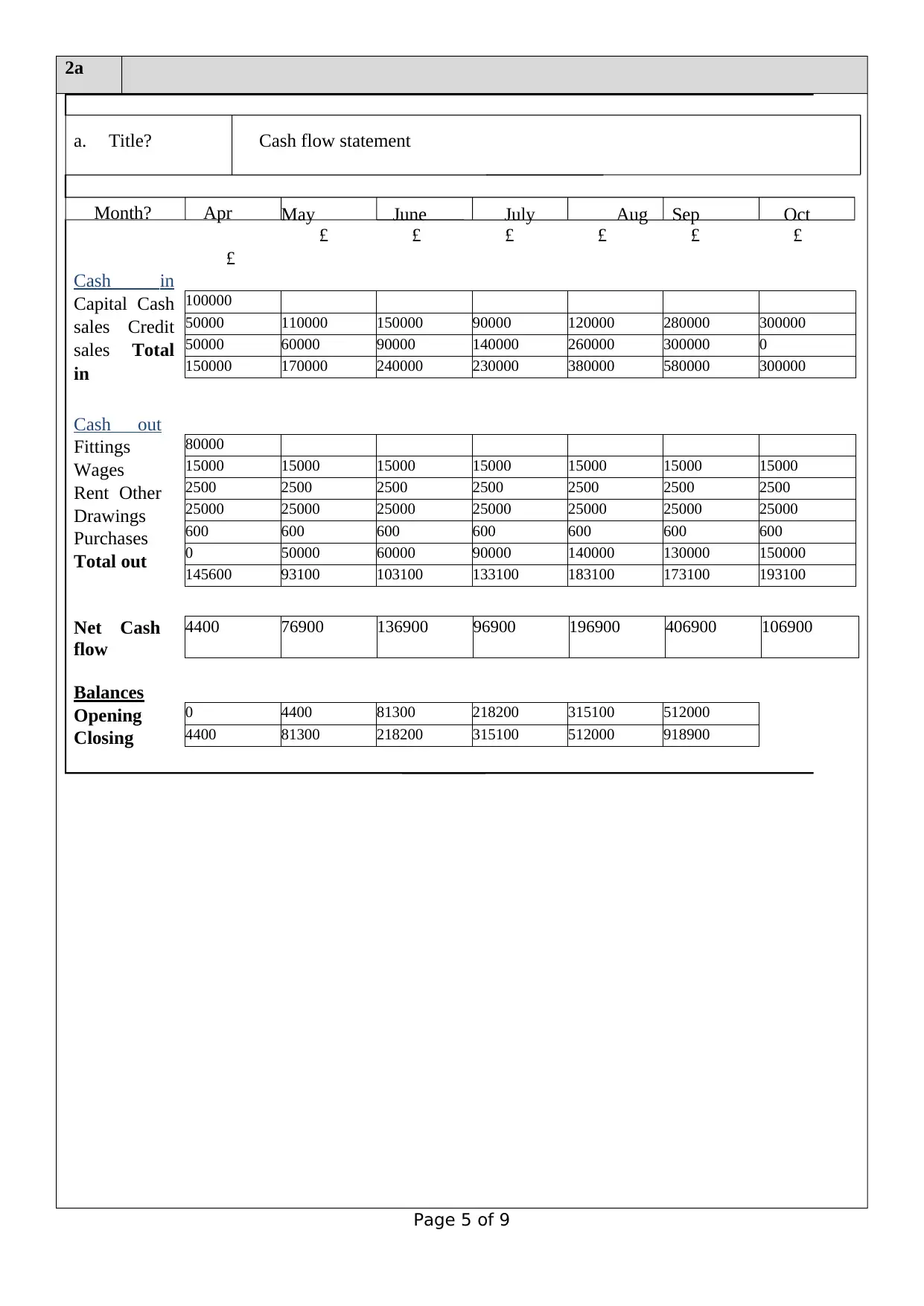

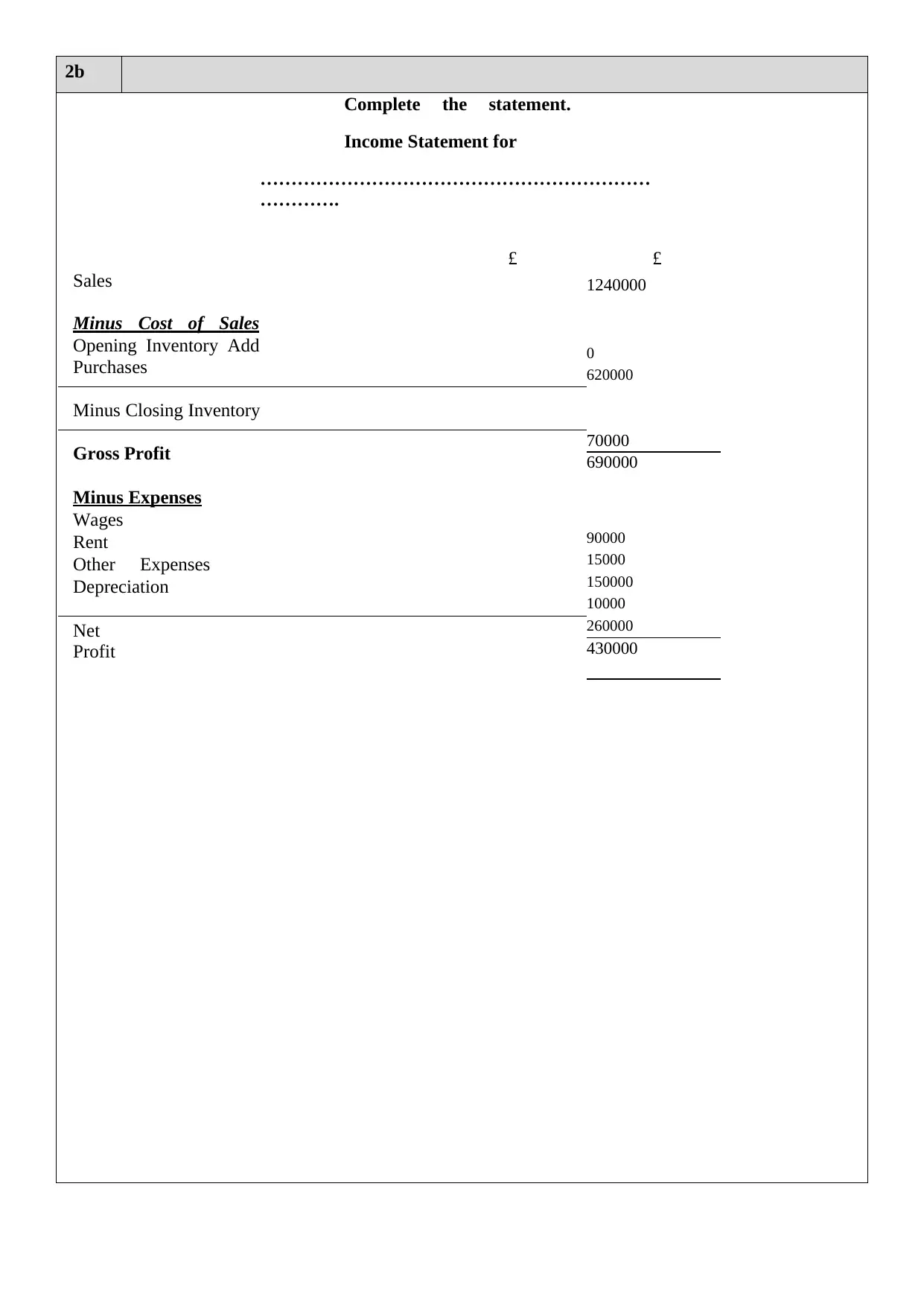

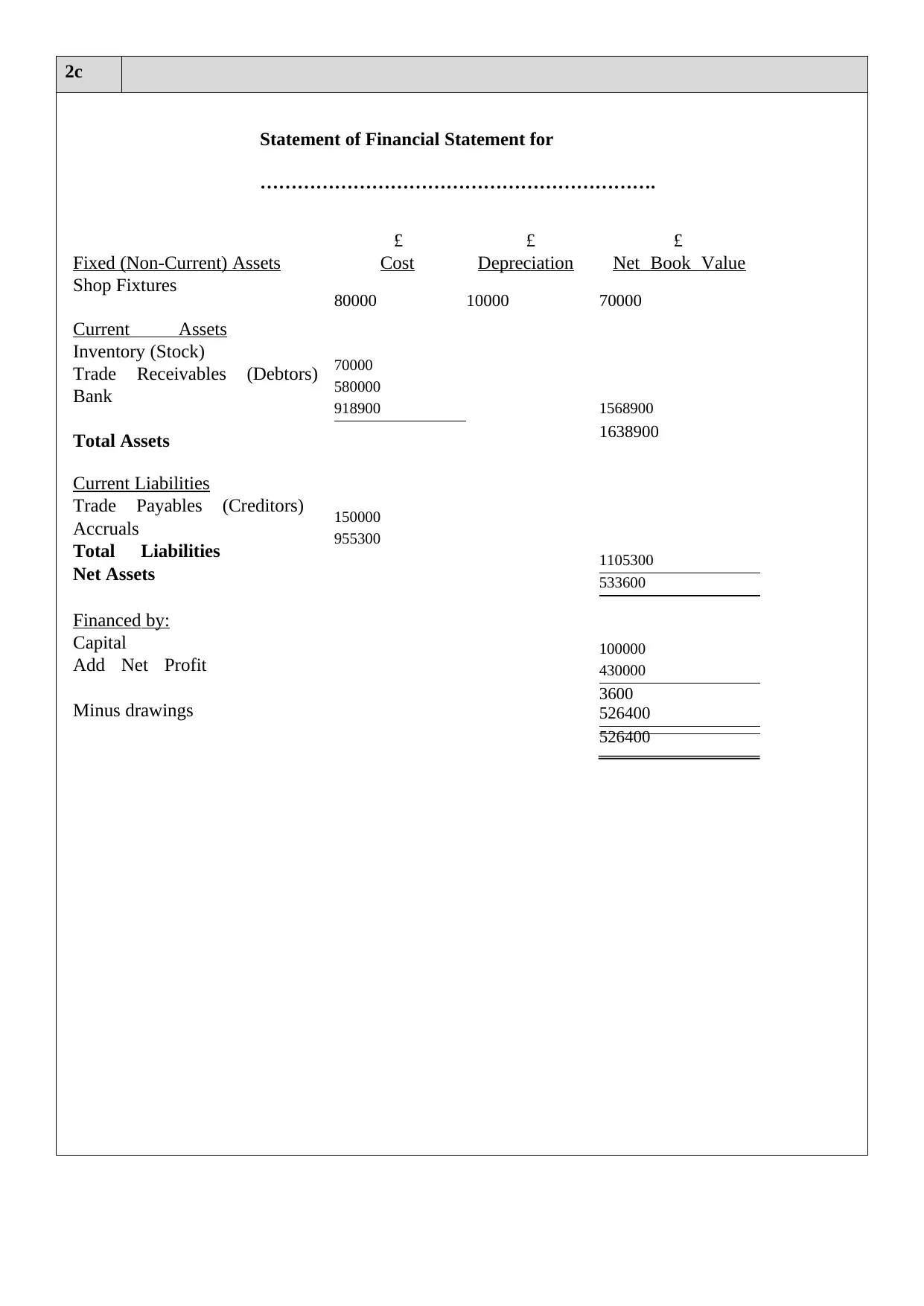

This TCA answer book covers the module title, total number of questions attempted, and student number for the Introductory Finance and Accounting course with code ACC10032122. It includes a cash flow statement, income statement, and statement of financial statement for a proposed business model. The book also discusses the decision-making process for a company considering the production of a product line and the factors that should be considered. The net profit margin and current ratio of the company are also analyzed.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.