Financial Analysis of Schutz Building Services: Report

VerifiedAdded on 2020/05/28

|12

|2955

|81

Report

AI Summary

This report presents an analysis of the financial statements of Schutz Building Services, including the income statement and balance sheet. It calculates and interprets various financial ratios, such as the current ratio, quick ratio, gross profit margin, net profit margin, accounts payable turnover ratio, accounts receivable turnover ratio, debt ratio, and debt-to-equity ratio. The analysis assesses the company's financial health, liquidity, and solvency, with a focus on how these factors impact its ability to meet obligations to suppliers. The report highlights both positive and negative indicators, such as the company's strong current and quick ratios but also the potential concern of a high level of accounts receivable. The report also examines the implications of these financial metrics for suppliers, helping them assess the creditworthiness of Schutz Building Services. The report uses various sources to support its findings, including a discussion of how financial statements can be used to assess a company's financial health.

Running head: INTRODUCTORY FINANCIAL ACCOUNTING

Introductory Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Introductory Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTORY FINANCIAL ACCOUNTING

1

Table of Contents

A. Drafting the Income Statement and Balance Sheet Statement for Schutz Building Services

for the current period:.................................................................................................................2

B.1 Depicting how financial statement could help the supplier of building to trade or not trade

with Johan:.................................................................................................................................3

B.2 Depicting the parts of financial statement, which could have positive indicator for Schutz

Building Services supplier and indicate the item that may be concern for suppliers:...............5

Reference and Bibliography:....................................................................................................10

1

Table of Contents

A. Drafting the Income Statement and Balance Sheet Statement for Schutz Building Services

for the current period:.................................................................................................................2

B.1 Depicting how financial statement could help the supplier of building to trade or not trade

with Johan:.................................................................................................................................3

B.2 Depicting the parts of financial statement, which could have positive indicator for Schutz

Building Services supplier and indicate the item that may be concern for suppliers:...............5

Reference and Bibliography:....................................................................................................10

INTRODUCTORY FINANCIAL ACCOUNTING

2

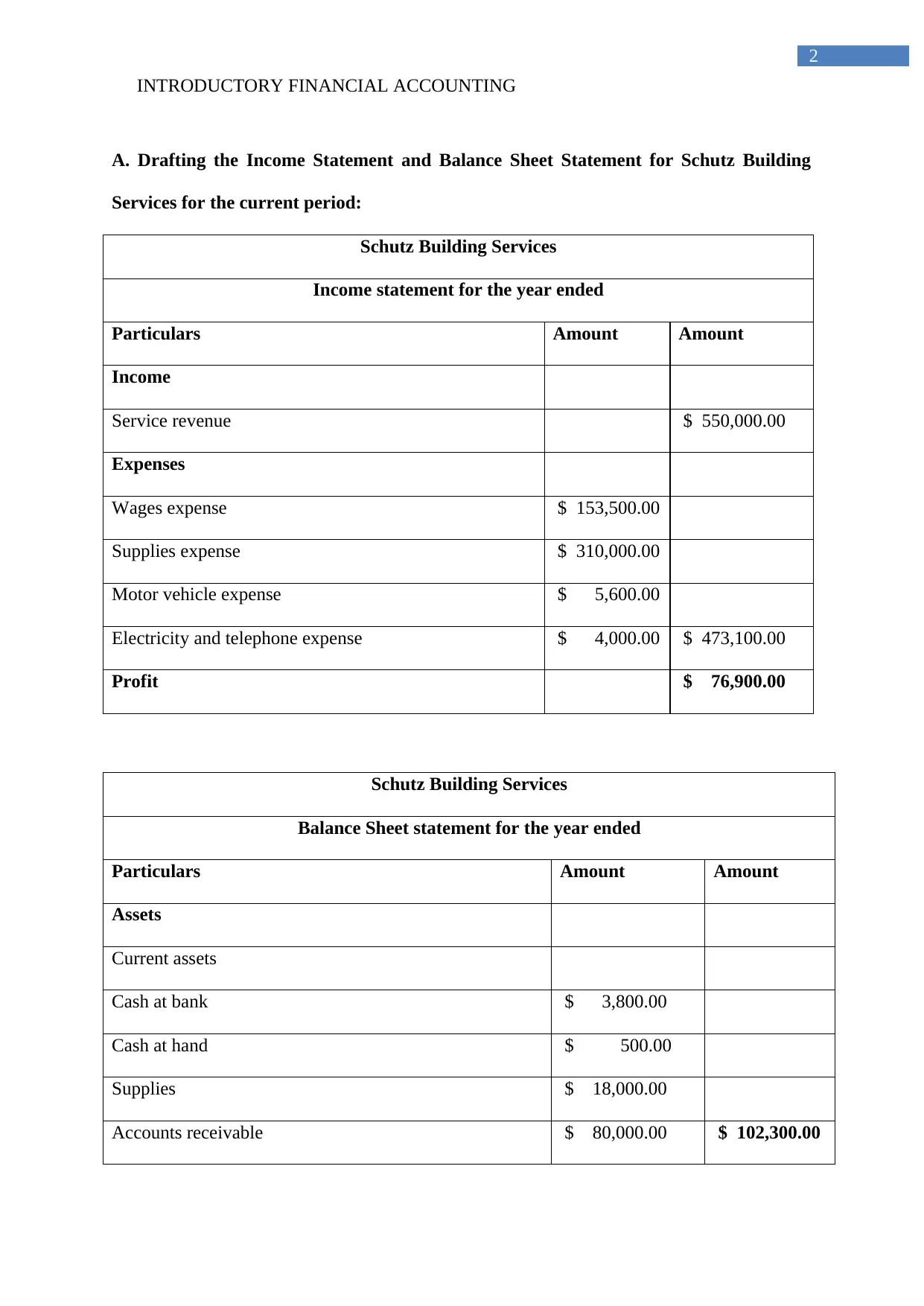

A. Drafting the Income Statement and Balance Sheet Statement for Schutz Building

Services for the current period:

Schutz Building Services

Income statement for the year ended

Particulars Amount Amount

Income

Service revenue $ 550,000.00

Expenses

Wages expense $ 153,500.00

Supplies expense $ 310,000.00

Motor vehicle expense $ 5,600.00

Electricity and telephone expense $ 4,000.00 $ 473,100.00

Profit $ 76,900.00

Schutz Building Services

Balance Sheet statement for the year ended

Particulars Amount Amount

Assets

Current assets

Cash at bank $ 3,800.00

Cash at hand $ 500.00

Supplies $ 18,000.00

Accounts receivable $ 80,000.00 $ 102,300.00

2

A. Drafting the Income Statement and Balance Sheet Statement for Schutz Building

Services for the current period:

Schutz Building Services

Income statement for the year ended

Particulars Amount Amount

Income

Service revenue $ 550,000.00

Expenses

Wages expense $ 153,500.00

Supplies expense $ 310,000.00

Motor vehicle expense $ 5,600.00

Electricity and telephone expense $ 4,000.00 $ 473,100.00

Profit $ 76,900.00

Schutz Building Services

Balance Sheet statement for the year ended

Particulars Amount Amount

Assets

Current assets

Cash at bank $ 3,800.00

Cash at hand $ 500.00

Supplies $ 18,000.00

Accounts receivable $ 80,000.00 $ 102,300.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTORY FINANCIAL ACCOUNTING

3

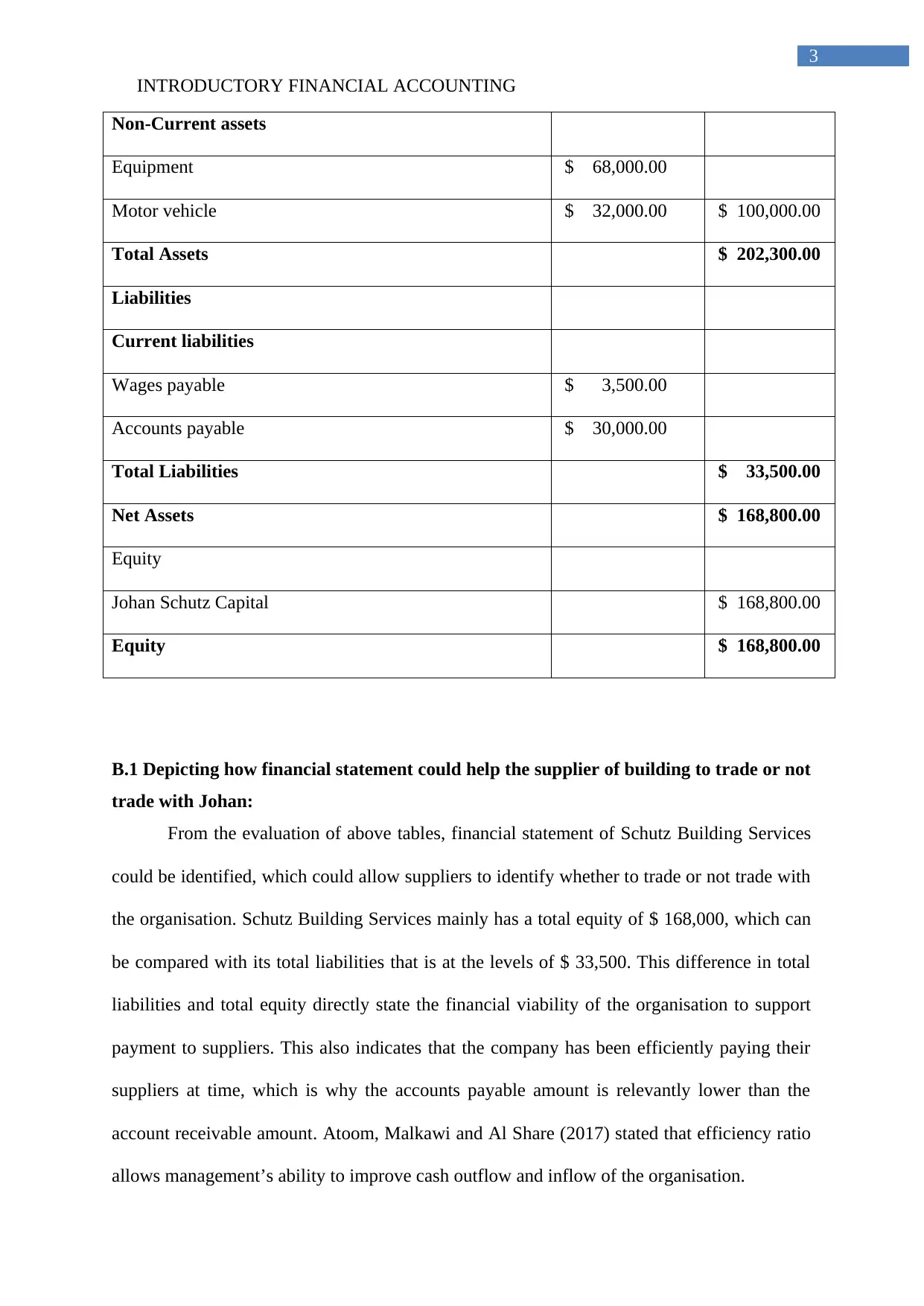

Non-Current assets

Equipment $ 68,000.00

Motor vehicle $ 32,000.00 $ 100,000.00

Total Assets $ 202,300.00

Liabilities

Current liabilities

Wages payable $ 3,500.00

Accounts payable $ 30,000.00

Total Liabilities $ 33,500.00

Net Assets $ 168,800.00

Equity

Johan Schutz Capital $ 168,800.00

Equity $ 168,800.00

B.1 Depicting how financial statement could help the supplier of building to trade or not

trade with Johan:

From the evaluation of above tables, financial statement of Schutz Building Services

could be identified, which could allow suppliers to identify whether to trade or not trade with

the organisation. Schutz Building Services mainly has a total equity of $ 168,000, which can

be compared with its total liabilities that is at the levels of $ 33,500. This difference in total

liabilities and total equity directly state the financial viability of the organisation to support

payment to suppliers. This also indicates that the company has been efficiently paying their

suppliers at time, which is why the accounts payable amount is relevantly lower than the

account receivable amount. Atoom, Malkawi and Al Share (2017) stated that efficiency ratio

allows management’s ability to improve cash outflow and inflow of the organisation.

3

Non-Current assets

Equipment $ 68,000.00

Motor vehicle $ 32,000.00 $ 100,000.00

Total Assets $ 202,300.00

Liabilities

Current liabilities

Wages payable $ 3,500.00

Accounts payable $ 30,000.00

Total Liabilities $ 33,500.00

Net Assets $ 168,800.00

Equity

Johan Schutz Capital $ 168,800.00

Equity $ 168,800.00

B.1 Depicting how financial statement could help the supplier of building to trade or not

trade with Johan:

From the evaluation of above tables, financial statement of Schutz Building Services

could be identified, which could allow suppliers to identify whether to trade or not trade with

the organisation. Schutz Building Services mainly has a total equity of $ 168,000, which can

be compared with its total liabilities that is at the levels of $ 33,500. This difference in total

liabilities and total equity directly state the financial viability of the organisation to support

payment to suppliers. This also indicates that the company has been efficiently paying their

suppliers at time, which is why the accounts payable amount is relevantly lower than the

account receivable amount. Atoom, Malkawi and Al Share (2017) stated that efficiency ratio

allows management’s ability to improve cash outflow and inflow of the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTORY FINANCIAL ACCOUNTING

4

Furthermore, net total assets of the organization are mainly at $168,800, which is

derived by deducting total assets from total liabilities. This indicates that the company's

overall assets are more than the liabilities, which depicts its financial position and strength to

support future financial obligations. The company’s current asset is mainly at the levels of $

102,300 and current liabilities at the levels of $ 33,500, which is relatively adequate to

support Schutz Building Services ability to pay their dues to its suppliers. Bodie, Kane and

Marcus (2014) indicates that companies having low current liabilities and high current assets

are able to support unexpected expenses and conduct smooth operations.

However, the main concern is relatively towards account receivable of Schutz

Building Services, as they are not concerned about receiving payments from customer. This

low concern regarding payment collection from customers could lead to cash stagnation and

directly hamper ability of the company to support its future payment. This negligence in

collecting account receivables is mainly identified as negative indicator, which portray low

capability of Schutz Building Services to support future expenses. The continued negligence

of collecting accounts receivable could eventually reduce trust of suppliers in providing credit

to Schutz Building Services. Therefore, management of Schutz Building Services needs to

increase its account receivable collection for generating adequate cash, which could support

its financial obligations (Brooks 2015).

The analysis of the financial statement also indicates weak current assets of the

organization, as accounts receivable consists of $ 80,000, while total current assets is at the

levels of $ 102,300. This indicates that every organization is unable to collect its receivables

from the customer then immediate cash stagnation could be seen. Therefore, supplier needs to

know all the revenant information about the company's ability to pay for the materials needed

to support its activities. Hence, adequate statement of cash flow can be provided by the

organization to depict its cash flow from operations, cash flow from financing activities and

4

Furthermore, net total assets of the organization are mainly at $168,800, which is

derived by deducting total assets from total liabilities. This indicates that the company's

overall assets are more than the liabilities, which depicts its financial position and strength to

support future financial obligations. The company’s current asset is mainly at the levels of $

102,300 and current liabilities at the levels of $ 33,500, which is relatively adequate to

support Schutz Building Services ability to pay their dues to its suppliers. Bodie, Kane and

Marcus (2014) indicates that companies having low current liabilities and high current assets

are able to support unexpected expenses and conduct smooth operations.

However, the main concern is relatively towards account receivable of Schutz

Building Services, as they are not concerned about receiving payments from customer. This

low concern regarding payment collection from customers could lead to cash stagnation and

directly hamper ability of the company to support its future payment. This negligence in

collecting account receivables is mainly identified as negative indicator, which portray low

capability of Schutz Building Services to support future expenses. The continued negligence

of collecting accounts receivable could eventually reduce trust of suppliers in providing credit

to Schutz Building Services. Therefore, management of Schutz Building Services needs to

increase its account receivable collection for generating adequate cash, which could support

its financial obligations (Brooks 2015).

The analysis of the financial statement also indicates weak current assets of the

organization, as accounts receivable consists of $ 80,000, while total current assets is at the

levels of $ 102,300. This indicates that every organization is unable to collect its receivables

from the customer then immediate cash stagnation could be seen. Therefore, supplier needs to

know all the revenant information about the company's ability to pay for the materials needed

to support its activities. Hence, adequate statement of cash flow can be provided by the

organization to depict its cash flow from operations, cash flow from financing activities and

INTRODUCTORY FINANCIAL ACCOUNTING

5

cash flow from investing activities. This could eventually help in depicting firm’s financial

ability to pay for the materials purchased from suppliers. In this context, Cengiz, Combs and

Samy (2017) mentioned that companies with high receivables are able to generate adequate

cash reserves, which could support its short term compulsions.

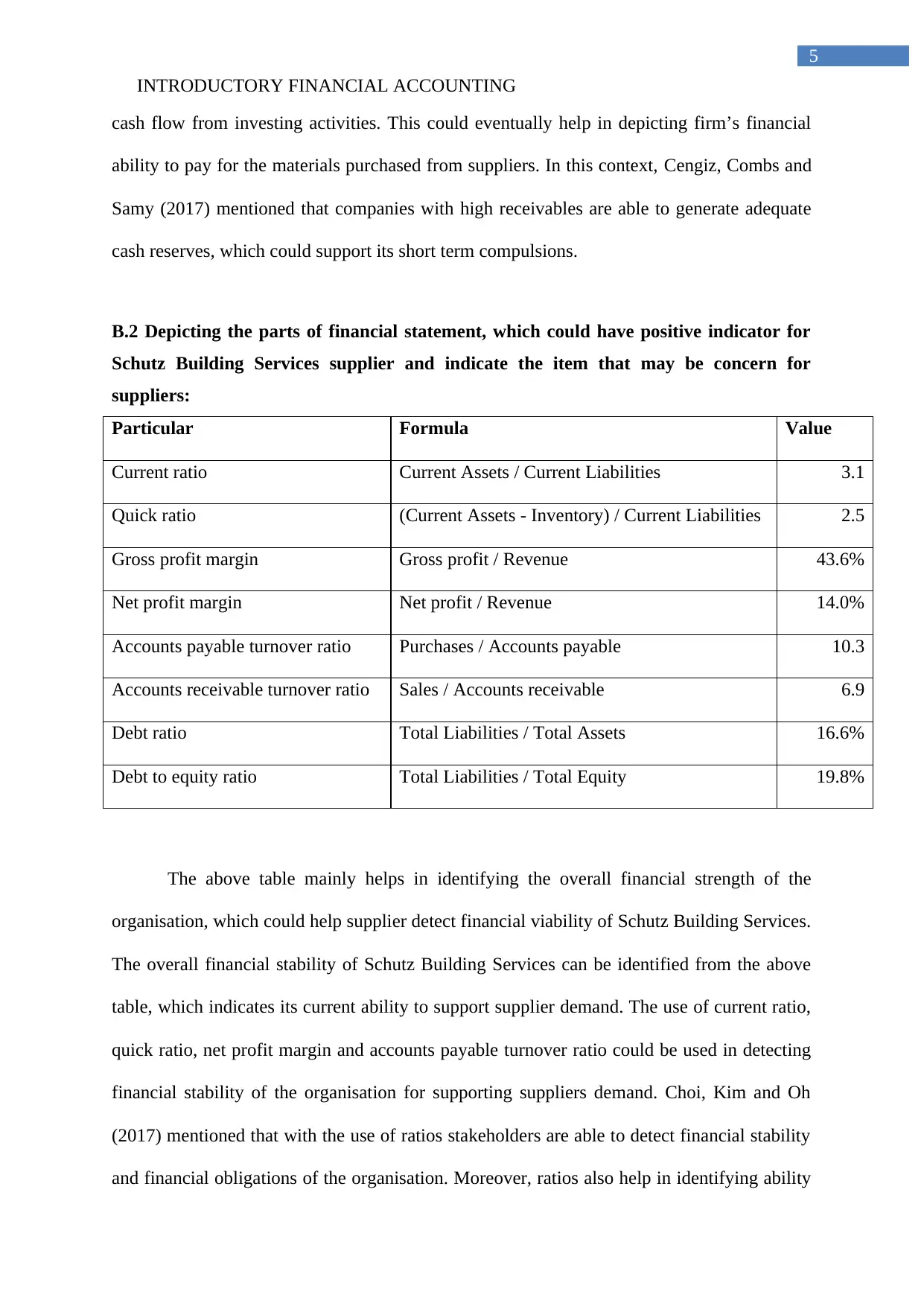

B.2 Depicting the parts of financial statement, which could have positive indicator for

Schutz Building Services supplier and indicate the item that may be concern for

suppliers:

Particular Formula Value

Current ratio Current Assets / Current Liabilities 3.1

Quick ratio (Current Assets - Inventory) / Current Liabilities 2.5

Gross profit margin Gross profit / Revenue 43.6%

Net profit margin Net profit / Revenue 14.0%

Accounts payable turnover ratio Purchases / Accounts payable 10.3

Accounts receivable turnover ratio Sales / Accounts receivable 6.9

Debt ratio Total Liabilities / Total Assets 16.6%

Debt to equity ratio Total Liabilities / Total Equity 19.8%

The above table mainly helps in identifying the overall financial strength of the

organisation, which could help supplier detect financial viability of Schutz Building Services.

The overall financial stability of Schutz Building Services can be identified from the above

table, which indicates its current ability to support supplier demand. The use of current ratio,

quick ratio, net profit margin and accounts payable turnover ratio could be used in detecting

financial stability of the organisation for supporting suppliers demand. Choi, Kim and Oh

(2017) mentioned that with the use of ratios stakeholders are able to detect financial stability

and financial obligations of the organisation. Moreover, ratios also help in identifying ability

5

cash flow from investing activities. This could eventually help in depicting firm’s financial

ability to pay for the materials purchased from suppliers. In this context, Cengiz, Combs and

Samy (2017) mentioned that companies with high receivables are able to generate adequate

cash reserves, which could support its short term compulsions.

B.2 Depicting the parts of financial statement, which could have positive indicator for

Schutz Building Services supplier and indicate the item that may be concern for

suppliers:

Particular Formula Value

Current ratio Current Assets / Current Liabilities 3.1

Quick ratio (Current Assets - Inventory) / Current Liabilities 2.5

Gross profit margin Gross profit / Revenue 43.6%

Net profit margin Net profit / Revenue 14.0%

Accounts payable turnover ratio Purchases / Accounts payable 10.3

Accounts receivable turnover ratio Sales / Accounts receivable 6.9

Debt ratio Total Liabilities / Total Assets 16.6%

Debt to equity ratio Total Liabilities / Total Equity 19.8%

The above table mainly helps in identifying the overall financial strength of the

organisation, which could help supplier detect financial viability of Schutz Building Services.

The overall financial stability of Schutz Building Services can be identified from the above

table, which indicates its current ability to support supplier demand. The use of current ratio,

quick ratio, net profit margin and accounts payable turnover ratio could be used in detecting

financial stability of the organisation for supporting suppliers demand. Choi, Kim and Oh

(2017) mentioned that with the use of ratios stakeholders are able to detect financial stability

and financial obligations of the organisation. Moreover, ratios also help in identifying ability

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTORY FINANCIAL ACCOUNTING

6

of the company to support its financial compulsions and pinpoint loopholes in their financial

stability. However, in the current scenario both financial obligation and stability of Schutz

Building Services is relevantly adequate. Nevertheless, the valuation of financial ratios could

eventually help in identifying the actual financial position of Schutz Building Services.

Current ratio:

The current ratio of the organisation is mainly at 3.1, which is relevant higher than the

minimum requirement needed by organisation. This increased current ratio is mainly helpful

in identifying financial stability of the organisation, which in turn could allow the supplier to

increase their reliability. The increased current ratio indicates that the company has enough

cash for supporting their activities. Moreover, suppliers seeing the current ratio could rely on

ability of Schutz Building Services for providing relevant payments. Czajor and Michalak

(2017) declared that current ratio allows stakeholder to detect liquidity position of the

company to take adequate decision for investment.

Quick ratio:

The quick ratio is mainly at the level of 2.5, which is relatively higher than the

minimum requirement of 1. The company mainly needed a requirement of 1 for the quick

ratio to effectively conduct its operations. This increased quick ratio value mainly indicates

inefficiency in managements work for utilising their available resources. Therefore, the

company has high cash availability for supporting their purchases and payment towards

suppliers. In this context, Ferrer and Tang (2016) mentioned that investors use quick ratio to

understand financial stability of the organisation, which helps in improving their investment

scope. Moreover, the difference in current and quick ratio could eventually help in detecting

the investment conducted by the company in maintaining their inventory. This evaluation

could help in understanding sales condition of the company.

6

of the company to support its financial compulsions and pinpoint loopholes in their financial

stability. However, in the current scenario both financial obligation and stability of Schutz

Building Services is relevantly adequate. Nevertheless, the valuation of financial ratios could

eventually help in identifying the actual financial position of Schutz Building Services.

Current ratio:

The current ratio of the organisation is mainly at 3.1, which is relevant higher than the

minimum requirement needed by organisation. This increased current ratio is mainly helpful

in identifying financial stability of the organisation, which in turn could allow the supplier to

increase their reliability. The increased current ratio indicates that the company has enough

cash for supporting their activities. Moreover, suppliers seeing the current ratio could rely on

ability of Schutz Building Services for providing relevant payments. Czajor and Michalak

(2017) declared that current ratio allows stakeholder to detect liquidity position of the

company to take adequate decision for investment.

Quick ratio:

The quick ratio is mainly at the level of 2.5, which is relatively higher than the

minimum requirement of 1. The company mainly needed a requirement of 1 for the quick

ratio to effectively conduct its operations. This increased quick ratio value mainly indicates

inefficiency in managements work for utilising their available resources. Therefore, the

company has high cash availability for supporting their purchases and payment towards

suppliers. In this context, Ferrer and Tang (2016) mentioned that investors use quick ratio to

understand financial stability of the organisation, which helps in improving their investment

scope. Moreover, the difference in current and quick ratio could eventually help in detecting

the investment conducted by the company in maintaining their inventory. This evaluation

could help in understanding sales condition of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTORY FINANCIAL ACCOUNTING

7

Gross profit margin:

The gross profit margin of the organisation is mainly at the levels of 43.6%, which

indicates the ability of the company to support its administrative expenses. The use of gross

profit could eventually help in identifying ability of the company to conduct certain expenses.

Giordani et al. (2014) mentioned that gross profit margin of the company could eventually

help investors in detecting ability of the company to generate revenue after deducting cost of

goods. The gross profit is mainly not more than 50% indicting rising cost incurred by the

organisation, which might reduce their profitability.

Net profit margin:

The net profit margin of the organisation is mainly at the levels of 14%, which is

relevantly high and indicates the profits incurred by the company. This relevant difference

between gross and net profit margin is mainly high, which indicate increased administrative

expenses of Schutz Building Services. This high administrative expense of the organisation is

mainly reducing actual profits of Schutz Building Services, which is in turn reducing its

ability to support payments. The net profit margin of the organisation is mainly stating its

eligibility to support supplier with relevant payments. Furthermore, high financial stability

could indicate ability of Schutz Building Services to support their payment structure. Goyal

and Bhatia (2016) stated that net profit margin is mainly conducted to compare financial

improvement of an organisation, which helps in detecting its financial stability. However,

suppliers seeing the low net profit obtained by Schutz Building Services could identify its

flaws, which might hamper payments to the suppliers.

Accounts payable turnover ratio:

7

Gross profit margin:

The gross profit margin of the organisation is mainly at the levels of 43.6%, which

indicates the ability of the company to support its administrative expenses. The use of gross

profit could eventually help in identifying ability of the company to conduct certain expenses.

Giordani et al. (2014) mentioned that gross profit margin of the company could eventually

help investors in detecting ability of the company to generate revenue after deducting cost of

goods. The gross profit is mainly not more than 50% indicting rising cost incurred by the

organisation, which might reduce their profitability.

Net profit margin:

The net profit margin of the organisation is mainly at the levels of 14%, which is

relevantly high and indicates the profits incurred by the company. This relevant difference

between gross and net profit margin is mainly high, which indicate increased administrative

expenses of Schutz Building Services. This high administrative expense of the organisation is

mainly reducing actual profits of Schutz Building Services, which is in turn reducing its

ability to support payments. The net profit margin of the organisation is mainly stating its

eligibility to support supplier with relevant payments. Furthermore, high financial stability

could indicate ability of Schutz Building Services to support their payment structure. Goyal

and Bhatia (2016) stated that net profit margin is mainly conducted to compare financial

improvement of an organisation, which helps in detecting its financial stability. However,

suppliers seeing the low net profit obtained by Schutz Building Services could identify its

flaws, which might hamper payments to the suppliers.

Accounts payable turnover ratio:

INTRODUCTORY FINANCIAL ACCOUNTING

8

The accounts payable turnover ratio is mainly at the levels of 10.3, which indicates

that the company is adequately paying for its purchases. The accounts payable turnover ratio

is relevantly high stating ability of the organisation to generate higher revenues. In this

context, Ibrahim et al. (2017) mentioned that investors are able to detect payment capability

of the organisation by identifying its accounts payable turnover ratio, which needs to be high

in comparison with its peer. Therefore, the suppliers seeing high accounts payable turnover

ratio of Schutz Building Services could rely on its ability to conduct relevant payments.

Accounts receivable turnover ratio:

The accounts receivable turnover ratio of the organisation is mainly at the levels of

6.9, which indicates the low receivables conducted by the organisation. The low receivables

mainly indicate company’s ability to generate relevant cash for supporting their expenses,

which is relatively low and can increase cash reduction in future. Therefore, the evaluation of

accounts receivable turnover ratio of the organization directly indicates the problems, which

the suppliers could face while receiving their payments. Hence, the indicator depicts

incapability of Schutz Building Services to support their financial obligations and states

probability of cash shortage during payments. In this situation, Lukason, Laitinen and Suvas

(2015) stated that companies having high cash reserves are able to support their cash outflows

even if the cash inflow is reduced.

Debt ratio:

The debt ratio is mainly at 16.6%, which is relatively low indicating reduced usage of

debt in supporting Assets of Schutz Building Services. This is mainly an indication that your

organization does not borrow money to buy assets, which could be used in increasing its

production. Hence, this reduced debt collection could lead to low finance cost incurred by the

company, which in turns raises its profitability. Therefore, debt ratio is a positive indicator

8

The accounts payable turnover ratio is mainly at the levels of 10.3, which indicates

that the company is adequately paying for its purchases. The accounts payable turnover ratio

is relevantly high stating ability of the organisation to generate higher revenues. In this

context, Ibrahim et al. (2017) mentioned that investors are able to detect payment capability

of the organisation by identifying its accounts payable turnover ratio, which needs to be high

in comparison with its peer. Therefore, the suppliers seeing high accounts payable turnover

ratio of Schutz Building Services could rely on its ability to conduct relevant payments.

Accounts receivable turnover ratio:

The accounts receivable turnover ratio of the organisation is mainly at the levels of

6.9, which indicates the low receivables conducted by the organisation. The low receivables

mainly indicate company’s ability to generate relevant cash for supporting their expenses,

which is relatively low and can increase cash reduction in future. Therefore, the evaluation of

accounts receivable turnover ratio of the organization directly indicates the problems, which

the suppliers could face while receiving their payments. Hence, the indicator depicts

incapability of Schutz Building Services to support their financial obligations and states

probability of cash shortage during payments. In this situation, Lukason, Laitinen and Suvas

(2015) stated that companies having high cash reserves are able to support their cash outflows

even if the cash inflow is reduced.

Debt ratio:

The debt ratio is mainly at 16.6%, which is relatively low indicating reduced usage of

debt in supporting Assets of Schutz Building Services. This is mainly an indication that your

organization does not borrow money to buy assets, which could be used in increasing its

production. Hence, this reduced debt collection could lead to low finance cost incurred by the

company, which in turns raises its profitability. Therefore, debt ratio is a positive indicator

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTORY FINANCIAL ACCOUNTING

9

for the suppliers of the organization, as it helps in depicting its financial capability to support

payments in all conditions. Furthermore, the shallow depth accumulation also indicates the

reduced chance of the company to become insolvent, which is relevantly adequate for the

suppliers. According to Nuryani, Heng and Juliesta (2015), debt ratio is used by investors and

supplies to gauge into the financial position of the organization and detect whether in future it

could become insolvent. The minimum requirement for depth ratio is 40% for most of the

companies, as it helps in declining their finance cost, which is directly related to profitability

and cash reserves. Thus, the debt ratio of 16.6% is fairly viable for Schutz Building Services,

which is a positive sign for their suppliers.

Debt to equity ratio:

The debt to equity ratio is mainly are the levels of 19.8%, which is relatively lower

than the minimum requirements required by an organization. The low debt accumulation and

high usage of equity has allowed the organization to reduce their finance cost and increase

profitability. However, Paul and Mitra (2017) argued that debt financing is one of the major

terms which allows organization to reduce the tax expenses and increase their capacity to

retain income. In this perspective, Pech, Noguera and White (2015) further elaborated that

high debt accumulation by an organization could lead to insolvency, where the management

could not pay its debt with the current present assets. Nevertheless, the insolvency condition

is not present in the case of Schutz Building Services, where the company could generate

high revenue due to low financing cost. This is mainly a positive indicator for the suppliers,

as their payments would be conducted efficiently by Schutz Building Services.

9

for the suppliers of the organization, as it helps in depicting its financial capability to support

payments in all conditions. Furthermore, the shallow depth accumulation also indicates the

reduced chance of the company to become insolvent, which is relevantly adequate for the

suppliers. According to Nuryani, Heng and Juliesta (2015), debt ratio is used by investors and

supplies to gauge into the financial position of the organization and detect whether in future it

could become insolvent. The minimum requirement for depth ratio is 40% for most of the

companies, as it helps in declining their finance cost, which is directly related to profitability

and cash reserves. Thus, the debt ratio of 16.6% is fairly viable for Schutz Building Services,

which is a positive sign for their suppliers.

Debt to equity ratio:

The debt to equity ratio is mainly are the levels of 19.8%, which is relatively lower

than the minimum requirements required by an organization. The low debt accumulation and

high usage of equity has allowed the organization to reduce their finance cost and increase

profitability. However, Paul and Mitra (2017) argued that debt financing is one of the major

terms which allows organization to reduce the tax expenses and increase their capacity to

retain income. In this perspective, Pech, Noguera and White (2015) further elaborated that

high debt accumulation by an organization could lead to insolvency, where the management

could not pay its debt with the current present assets. Nevertheless, the insolvency condition

is not present in the case of Schutz Building Services, where the company could generate

high revenue due to low financing cost. This is mainly a positive indicator for the suppliers,

as their payments would be conducted efficiently by Schutz Building Services.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTORY FINANCIAL ACCOUNTING

10

Reference and Bibliography:

Atoom, R., Malkawi, E. and Al Share, B., 2017. Utilizing Australian Shareholders'

Association (ASA): Fifteen Top Financial Ratios to Evaluate Jordanian Banks'

Performance. Journal of Applied Finance and Banking, 7(1), p.119.

Bodie, Z., Kane, A. and Marcus, A.J., 2014. Investments, 10e. McGraw-Hill Education.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Cengiz, H., Combs, A. and Samy, M., 2017. An Analysis of how Financial Ratios of

Companies in Turkey Are Affected by National Standards, and IFRS. International Business

Research, 10(12), p.183.

Choi, J.Y., Kim, J. and Oh, K.J., 2017. Portfolio optimization strategy based on financial

ratios. The Korean Data & Information Science Society, 28(6), pp.1481-1500.

Czajor, P. and Michalak, M., 2017. Operating Lease Capitalization-Reasons and its Impact on

Financial Ratios of WIG30 and sWIG80 Companies. Przedsiębiorczość i Zarządzanie, 18(1,

cz. 1 Practical and Theoretical Issues in Contemporary Financial Management), pp.23-36.

Ferrer, R.C. and Tang, A., 2016. An Empirical Investigation of the Impact of Financial Ratios

and Business Combination on Stock Price among the Service Firms in the

Philippines. Academy of Accounting and Financial Studies Journal, 20(2), p.104.

Giordani, P., Jacobson, T., von Schedvin, E. and Villani, M., 2014. Taking the twists into

account: Predicting firm bankruptcy risk with splines of financial ratios. Journal of Financial

and Quantitative Analysis, 49(4), pp.1071-1099.

10

Reference and Bibliography:

Atoom, R., Malkawi, E. and Al Share, B., 2017. Utilizing Australian Shareholders'

Association (ASA): Fifteen Top Financial Ratios to Evaluate Jordanian Banks'

Performance. Journal of Applied Finance and Banking, 7(1), p.119.

Bodie, Z., Kane, A. and Marcus, A.J., 2014. Investments, 10e. McGraw-Hill Education.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Cengiz, H., Combs, A. and Samy, M., 2017. An Analysis of how Financial Ratios of

Companies in Turkey Are Affected by National Standards, and IFRS. International Business

Research, 10(12), p.183.

Choi, J.Y., Kim, J. and Oh, K.J., 2017. Portfolio optimization strategy based on financial

ratios. The Korean Data & Information Science Society, 28(6), pp.1481-1500.

Czajor, P. and Michalak, M., 2017. Operating Lease Capitalization-Reasons and its Impact on

Financial Ratios of WIG30 and sWIG80 Companies. Przedsiębiorczość i Zarządzanie, 18(1,

cz. 1 Practical and Theoretical Issues in Contemporary Financial Management), pp.23-36.

Ferrer, R.C. and Tang, A., 2016. An Empirical Investigation of the Impact of Financial Ratios

and Business Combination on Stock Price among the Service Firms in the

Philippines. Academy of Accounting and Financial Studies Journal, 20(2), p.104.

Giordani, P., Jacobson, T., von Schedvin, E. and Villani, M., 2014. Taking the twists into

account: Predicting firm bankruptcy risk with splines of financial ratios. Journal of Financial

and Quantitative Analysis, 49(4), pp.1071-1099.

INTRODUCTORY FINANCIAL ACCOUNTING

11

Goyal, S. and Bhatia, A., 2016. Analysis of Financial Ratios for Measuring Performance of

Indian Public Sector Banks. International Journal of Engineering and Management Research

(IJEMR), 6(2), pp.152-162.

Ibrahim, S.N.S., Arif, H.M. and Paino, H., 2017. The Relationship between Corporate

Governance Disclosures and Balance Sheet Ratios. Gading Journal for the Social

Sciences, 11(02), pp.33-40.

Lukason, O., Laitinen, E.K. and Suvas, A., 2015. Growth patterns of small manufacturing

firms before failure: interconnections with financial ratios and nonfinancial

variables. International Journal of Industrial Engineering and Management, 6(2), pp.59-66.

Nuryani, N., Heng, T.T. and Juliesta, N., 2015. Capitalization of Operating Lease and Its

Impact on Firm's Financial Ratios. Procedia-Social and Behavioral Sciences, 211, pp.268-

276.

Paul, S. and Mitra, G., 2017. Impact of Financial Ratios on Stock Price: A Comparative

Study with Hang Seng and Nifty Data. Research Bulletin, 43(2), pp.64-71.

Pech, C.O.T., Noguera, M. and White, S., 2015. Financial ratios used by equity analysts in

Mexico and stock returns. Contaduría y Administración, 60(3), pp.578-592.

Soares, J. and Pina, J., 2014. Credit Risk assessment and the information content of financial

ratios: a multi-country perspective. WSEAS transactions on business and economics, 11,

pp.175-187.

Yu, Q., Miche, Y., Séverin, E. and Lendasse, A., 2014. Bankruptcy prediction using extreme

learning machine and financial expertise. Neurocomputing, 128, pp.296-302.

11

Goyal, S. and Bhatia, A., 2016. Analysis of Financial Ratios for Measuring Performance of

Indian Public Sector Banks. International Journal of Engineering and Management Research

(IJEMR), 6(2), pp.152-162.

Ibrahim, S.N.S., Arif, H.M. and Paino, H., 2017. The Relationship between Corporate

Governance Disclosures and Balance Sheet Ratios. Gading Journal for the Social

Sciences, 11(02), pp.33-40.

Lukason, O., Laitinen, E.K. and Suvas, A., 2015. Growth patterns of small manufacturing

firms before failure: interconnections with financial ratios and nonfinancial

variables. International Journal of Industrial Engineering and Management, 6(2), pp.59-66.

Nuryani, N., Heng, T.T. and Juliesta, N., 2015. Capitalization of Operating Lease and Its

Impact on Firm's Financial Ratios. Procedia-Social and Behavioral Sciences, 211, pp.268-

276.

Paul, S. and Mitra, G., 2017. Impact of Financial Ratios on Stock Price: A Comparative

Study with Hang Seng and Nifty Data. Research Bulletin, 43(2), pp.64-71.

Pech, C.O.T., Noguera, M. and White, S., 2015. Financial ratios used by equity analysts in

Mexico and stock returns. Contaduría y Administración, 60(3), pp.578-592.

Soares, J. and Pina, J., 2014. Credit Risk assessment and the information content of financial

ratios: a multi-country perspective. WSEAS transactions on business and economics, 11,

pp.175-187.

Yu, Q., Miche, Y., Séverin, E. and Lendasse, A., 2014. Bankruptcy prediction using extreme

learning machine and financial expertise. Neurocomputing, 128, pp.296-302.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.