Investigatory Business Report on Tesco's Financial Performance

VerifiedAdded on 2022/12/15

|12

|3004

|424

AI Summary

This report analyzes and investigates the business performance of Tesco through financial ratio analysis. It examines liquidity, profitability, and efficiency ratios to identify issues and provide solutions. The report highlights a decline in profit margins and inventory management as areas of concern.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Investigatory Business

Report

Report

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

This report pertains to analyse and investigate business performance of Tesco to identify the

issues that its financial performance analysis reflects. This report undertakes financial ratio analysis

using figures from the declared statements of the last two years by the company. Further,

information obtained from ratios has been visually presented so that comment on Tesco’s

profitability, liquidity and efficiency can be made as well as issues related to them can be identified.

Further, solutions and recommendations have been presented.

This report pertains to analyse and investigate business performance of Tesco to identify the

issues that its financial performance analysis reflects. This report undertakes financial ratio analysis

using figures from the declared statements of the last two years by the company. Further,

information obtained from ratios has been visually presented so that comment on Tesco’s

profitability, liquidity and efficiency can be made as well as issues related to them can be identified.

Further, solutions and recommendations have been presented.

Contents

Executive Summary...........................................................................................................................................2

Introduction.......................................................................................................................................................4

Main Body.........................................................................................................................................................4

Ratio Analysis...............................................................................................................................................4

Problem Identification and investigation.......................................................................................................9

Solutions and recommendations..................................................................................................................10

Conclusion.......................................................................................................................................................11

References.......................................................................................................................................................12

Executive Summary...........................................................................................................................................2

Introduction.......................................................................................................................................................4

Main Body.........................................................................................................................................................4

Ratio Analysis...............................................................................................................................................4

Problem Identification and investigation.......................................................................................................9

Solutions and recommendations..................................................................................................................10

Conclusion.......................................................................................................................................................11

References.......................................................................................................................................................12

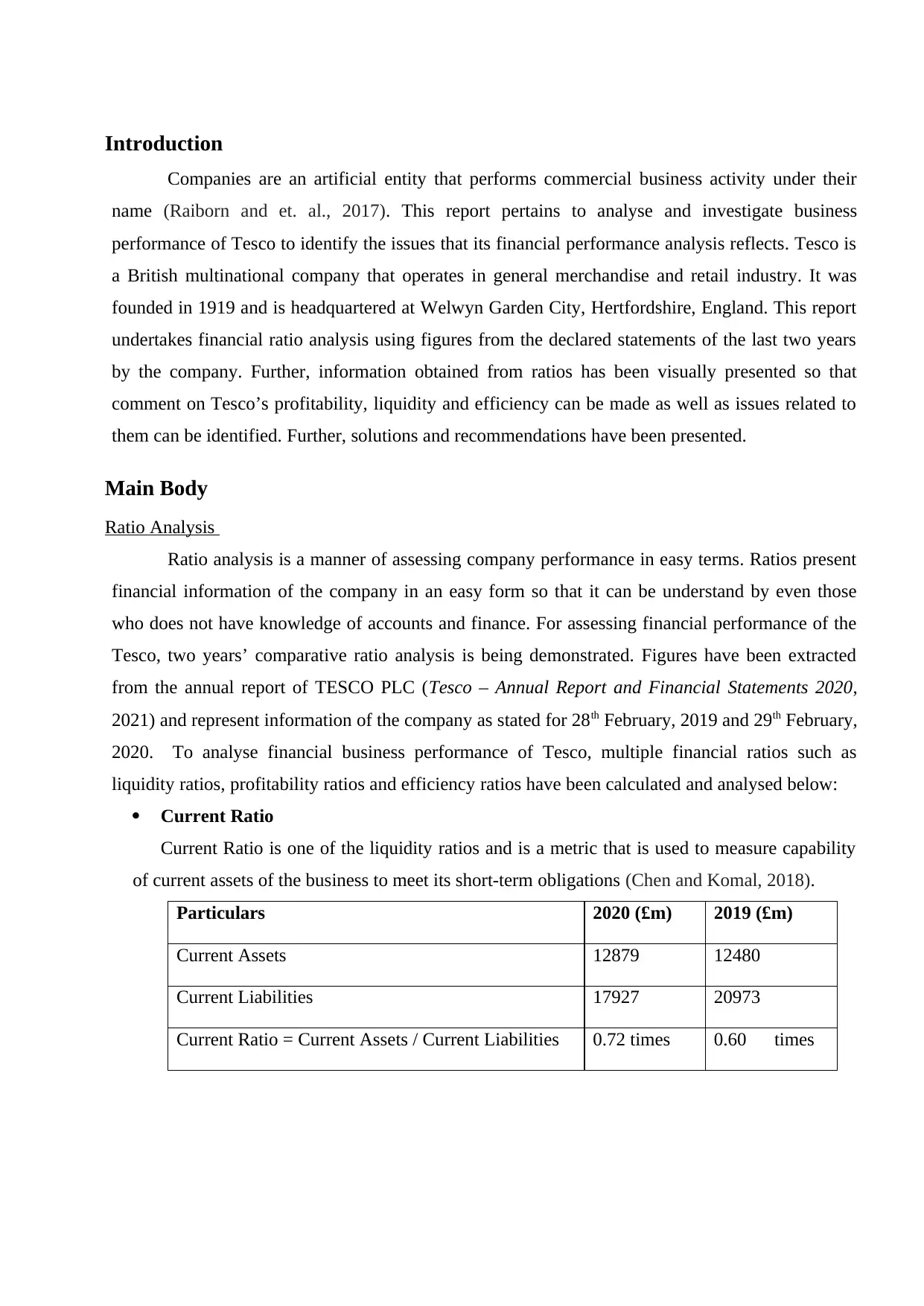

Introduction

Companies are an artificial entity that performs commercial business activity under their

name (Raiborn and et. al., 2017). This report pertains to analyse and investigate business

performance of Tesco to identify the issues that its financial performance analysis reflects. Tesco is

a British multinational company that operates in general merchandise and retail industry. It was

founded in 1919 and is headquartered at Welwyn Garden City, Hertfordshire, England. This report

undertakes financial ratio analysis using figures from the declared statements of the last two years

by the company. Further, information obtained from ratios has been visually presented so that

comment on Tesco’s profitability, liquidity and efficiency can be made as well as issues related to

them can be identified. Further, solutions and recommendations have been presented.

Main Body

Ratio Analysis

Ratio analysis is a manner of assessing company performance in easy terms. Ratios present

financial information of the company in an easy form so that it can be understand by even those

who does not have knowledge of accounts and finance. For assessing financial performance of the

Tesco, two years’ comparative ratio analysis is being demonstrated. Figures have been extracted

from the annual report of TESCO PLC (Tesco – Annual Report and Financial Statements 2020,

2021) and represent information of the company as stated for 28th February, 2019 and 29th February,

2020. To analyse financial business performance of Tesco, multiple financial ratios such as

liquidity ratios, profitability ratios and efficiency ratios have been calculated and analysed below:

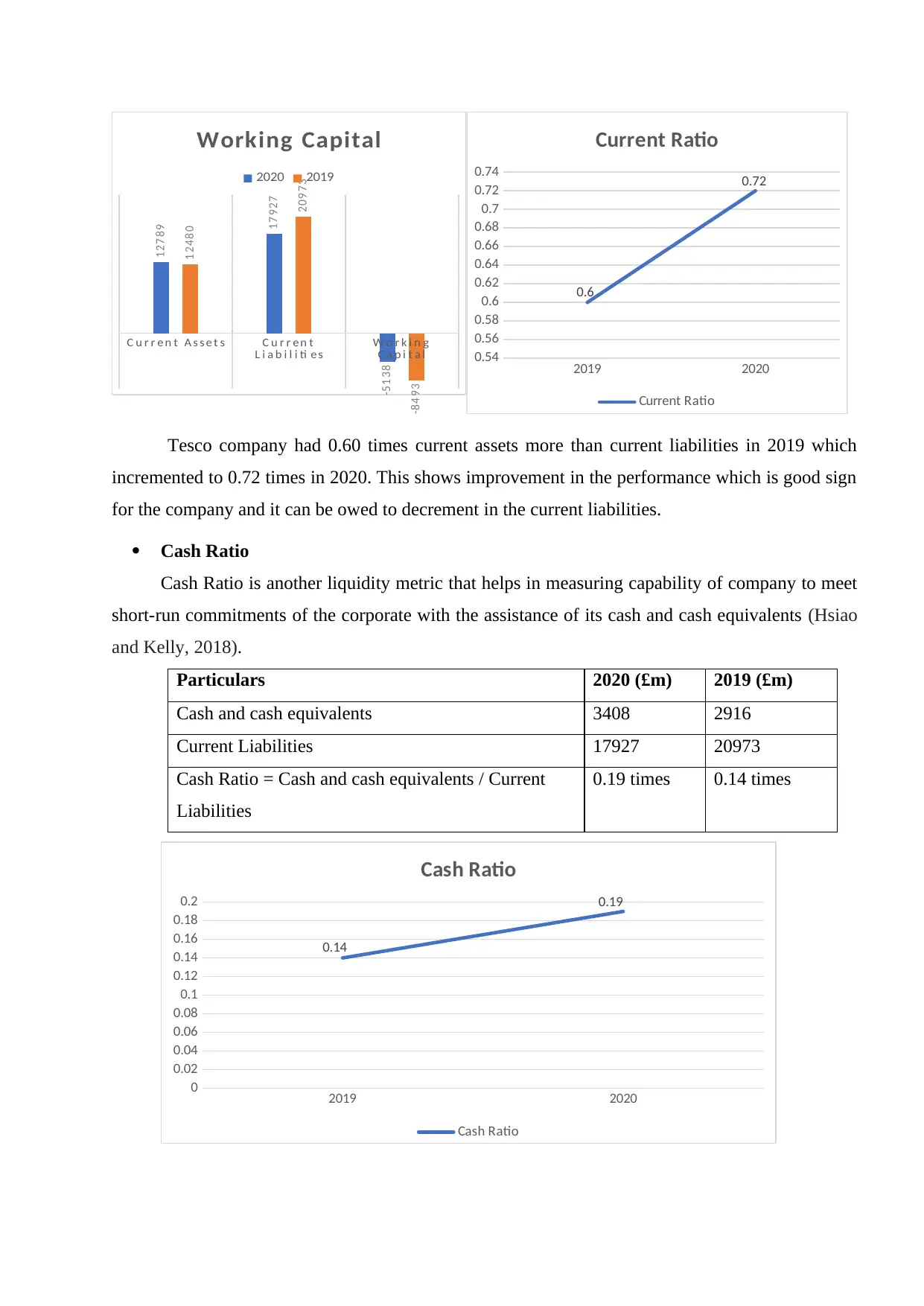

Current Ratio

Current Ratio is one of the liquidity ratios and is a metric that is used to measure capability

of current assets of the business to meet its short-term obligations (Chen and Komal, 2018).

Particulars 2020 (£m) 2019 (£m)

Current Assets 12879 12480

Current Liabilities 17927 20973

Current Ratio = Current Assets / Current Liabilities 0.72 times 0.60 times

Companies are an artificial entity that performs commercial business activity under their

name (Raiborn and et. al., 2017). This report pertains to analyse and investigate business

performance of Tesco to identify the issues that its financial performance analysis reflects. Tesco is

a British multinational company that operates in general merchandise and retail industry. It was

founded in 1919 and is headquartered at Welwyn Garden City, Hertfordshire, England. This report

undertakes financial ratio analysis using figures from the declared statements of the last two years

by the company. Further, information obtained from ratios has been visually presented so that

comment on Tesco’s profitability, liquidity and efficiency can be made as well as issues related to

them can be identified. Further, solutions and recommendations have been presented.

Main Body

Ratio Analysis

Ratio analysis is a manner of assessing company performance in easy terms. Ratios present

financial information of the company in an easy form so that it can be understand by even those

who does not have knowledge of accounts and finance. For assessing financial performance of the

Tesco, two years’ comparative ratio analysis is being demonstrated. Figures have been extracted

from the annual report of TESCO PLC (Tesco – Annual Report and Financial Statements 2020,

2021) and represent information of the company as stated for 28th February, 2019 and 29th February,

2020. To analyse financial business performance of Tesco, multiple financial ratios such as

liquidity ratios, profitability ratios and efficiency ratios have been calculated and analysed below:

Current Ratio

Current Ratio is one of the liquidity ratios and is a metric that is used to measure capability

of current assets of the business to meet its short-term obligations (Chen and Komal, 2018).

Particulars 2020 (£m) 2019 (£m)

Current Assets 12879 12480

Current Liabilities 17927 20973

Current Ratio = Current Assets / Current Liabilities 0.72 times 0.60 times

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

C u r r e n t A s s e t s C u r r e n t

L i a b i l i ti e s

W o r k i n g

C a p i t a l

12789

17927

-5138

12480

20973

-8493

Working Capital

2020 2019

2019 2020

0.54

0.56

0.58

0.6

0.62

0.64

0.66

0.68

0.7

0.72

0.74

0.6

0.72

Current Ratio

Current Ratio

Tesco company had 0.60 times current assets more than current liabilities in 2019 which

incremented to 0.72 times in 2020. This shows improvement in the performance which is good sign

for the company and it can be owed to decrement in the current liabilities.

Cash Ratio

Cash Ratio is another liquidity metric that helps in measuring capability of company to meet

short-run commitments of the corporate with the assistance of its cash and cash equivalents (Hsiao

and Kelly, 2018).

Particulars 2020 (£m) 2019 (£m)

Cash and cash equivalents 3408 2916

Current Liabilities 17927 20973

Cash Ratio = Cash and cash equivalents / Current

Liabilities

0.19 times 0.14 times

2019 2020

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0.14

0.19

Cash Ratio

Cash Ratio

L i a b i l i ti e s

W o r k i n g

C a p i t a l

12789

17927

-5138

12480

20973

-8493

Working Capital

2020 2019

2019 2020

0.54

0.56

0.58

0.6

0.62

0.64

0.66

0.68

0.7

0.72

0.74

0.6

0.72

Current Ratio

Current Ratio

Tesco company had 0.60 times current assets more than current liabilities in 2019 which

incremented to 0.72 times in 2020. This shows improvement in the performance which is good sign

for the company and it can be owed to decrement in the current liabilities.

Cash Ratio

Cash Ratio is another liquidity metric that helps in measuring capability of company to meet

short-run commitments of the corporate with the assistance of its cash and cash equivalents (Hsiao

and Kelly, 2018).

Particulars 2020 (£m) 2019 (£m)

Cash and cash equivalents 3408 2916

Current Liabilities 17927 20973

Cash Ratio = Cash and cash equivalents / Current

Liabilities

0.19 times 0.14 times

2019 2020

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0.14

0.19

Cash Ratio

Cash Ratio

As identified from the above table, Tesco had 0.14 times cash and cash equivalents to cover

current liabilities in 2019 which amplified to 0.19 times in 2020. This shows enhancement in the

performance that is positive for the corporation and can be due to decrease in the current liabilities

as well as improvement in the cash assets.

In summarised words, both the above liquidity ratios reflect positive signs for the operational

performance as well as liquidity position of the company with respect to the complete working

capital management.

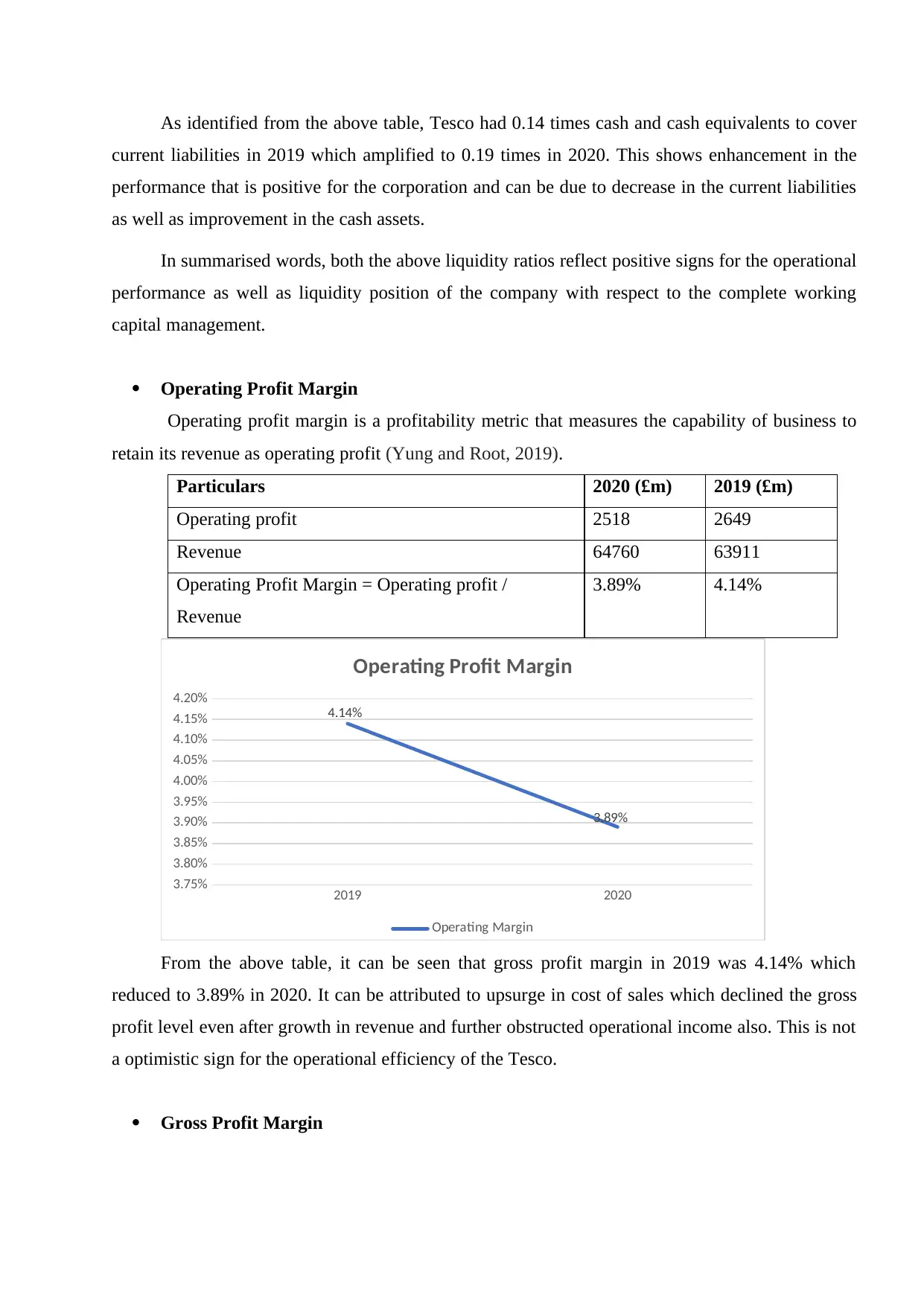

Operating Profit Margin

Operating profit margin is a profitability metric that measures the capability of business to

retain its revenue as operating profit (Yung and Root, 2019).

Particulars 2020 (£m) 2019 (£m)

Operating profit 2518 2649

Revenue 64760 63911

Operating Profit Margin = Operating profit /

Revenue

3.89% 4.14%

2019 2020

3.75%

3.80%

3.85%

3.90%

3.95%

4.00%

4.05%

4.10%

4.15%

4.20%

4.14%

3.89%

Operating Profit Margin

Operating Margin

From the above table, it can be seen that gross profit margin in 2019 was 4.14% which

reduced to 3.89% in 2020. It can be attributed to upsurge in cost of sales which declined the gross

profit level even after growth in revenue and further obstructed operational income also. This is not

a optimistic sign for the operational efficiency of the Tesco.

Gross Profit Margin

current liabilities in 2019 which amplified to 0.19 times in 2020. This shows enhancement in the

performance that is positive for the corporation and can be due to decrease in the current liabilities

as well as improvement in the cash assets.

In summarised words, both the above liquidity ratios reflect positive signs for the operational

performance as well as liquidity position of the company with respect to the complete working

capital management.

Operating Profit Margin

Operating profit margin is a profitability metric that measures the capability of business to

retain its revenue as operating profit (Yung and Root, 2019).

Particulars 2020 (£m) 2019 (£m)

Operating profit 2518 2649

Revenue 64760 63911

Operating Profit Margin = Operating profit /

Revenue

3.89% 4.14%

2019 2020

3.75%

3.80%

3.85%

3.90%

3.95%

4.00%

4.05%

4.10%

4.15%

4.20%

4.14%

3.89%

Operating Profit Margin

Operating Margin

From the above table, it can be seen that gross profit margin in 2019 was 4.14% which

reduced to 3.89% in 2020. It can be attributed to upsurge in cost of sales which declined the gross

profit level even after growth in revenue and further obstructed operational income also. This is not

a optimistic sign for the operational efficiency of the Tesco.

Gross Profit Margin

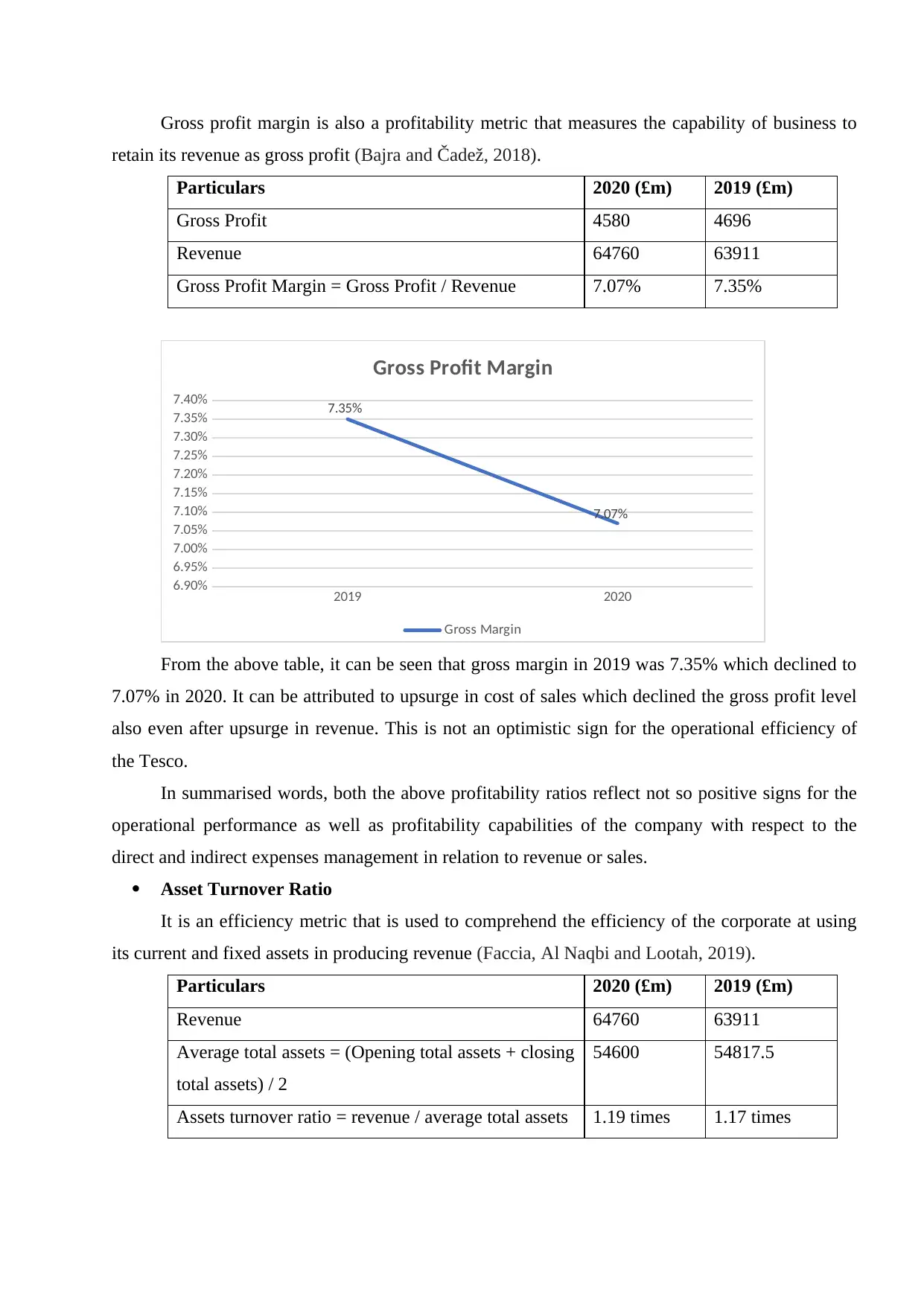

Gross profit margin is also a profitability metric that measures the capability of business to

retain its revenue as gross profit (Bajra and Čadež, 2018).

Particulars 2020 (£m) 2019 (£m)

Gross Profit 4580 4696

Revenue 64760 63911

Gross Profit Margin = Gross Profit / Revenue 7.07% 7.35%

2019 2020

6.90%

6.95%

7.00%

7.05%

7.10%

7.15%

7.20%

7.25%

7.30%

7.35%

7.40% 7.35%

7.07%

Gross Profit Margin

Gross Margin

From the above table, it can be seen that gross margin in 2019 was 7.35% which declined to

7.07% in 2020. It can be attributed to upsurge in cost of sales which declined the gross profit level

also even after upsurge in revenue. This is not an optimistic sign for the operational efficiency of

the Tesco.

In summarised words, both the above profitability ratios reflect not so positive signs for the

operational performance as well as profitability capabilities of the company with respect to the

direct and indirect expenses management in relation to revenue or sales.

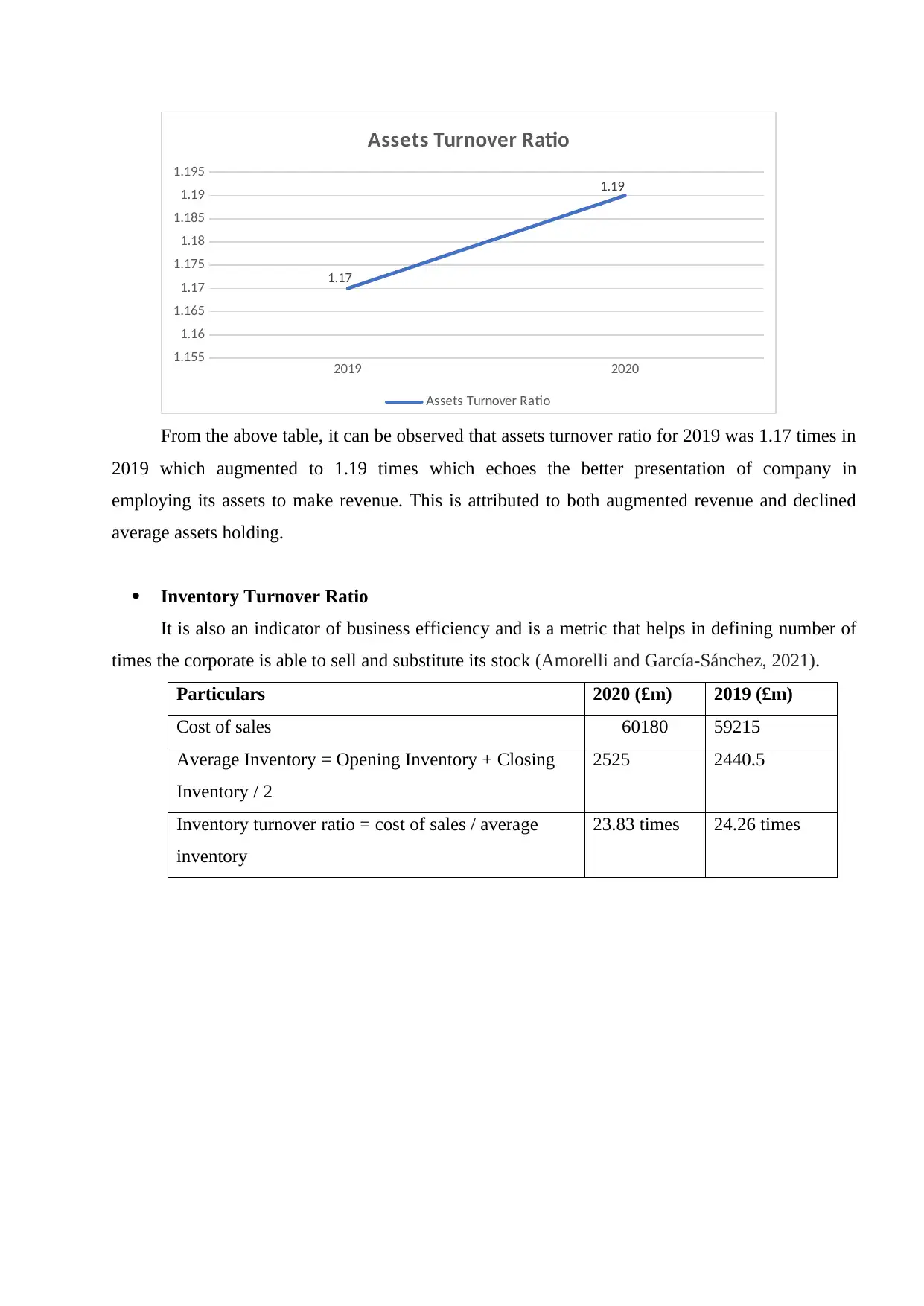

Asset Turnover Ratio

It is an efficiency metric that is used to comprehend the efficiency of the corporate at using

its current and fixed assets in producing revenue (Faccia, Al Naqbi and Lootah, 2019).

Particulars 2020 (£m) 2019 (£m)

Revenue 64760 63911

Average total assets = (Opening total assets + closing

total assets) / 2

54600 54817.5

Assets turnover ratio = revenue / average total assets 1.19 times 1.17 times

retain its revenue as gross profit (Bajra and Čadež, 2018).

Particulars 2020 (£m) 2019 (£m)

Gross Profit 4580 4696

Revenue 64760 63911

Gross Profit Margin = Gross Profit / Revenue 7.07% 7.35%

2019 2020

6.90%

6.95%

7.00%

7.05%

7.10%

7.15%

7.20%

7.25%

7.30%

7.35%

7.40% 7.35%

7.07%

Gross Profit Margin

Gross Margin

From the above table, it can be seen that gross margin in 2019 was 7.35% which declined to

7.07% in 2020. It can be attributed to upsurge in cost of sales which declined the gross profit level

also even after upsurge in revenue. This is not an optimistic sign for the operational efficiency of

the Tesco.

In summarised words, both the above profitability ratios reflect not so positive signs for the

operational performance as well as profitability capabilities of the company with respect to the

direct and indirect expenses management in relation to revenue or sales.

Asset Turnover Ratio

It is an efficiency metric that is used to comprehend the efficiency of the corporate at using

its current and fixed assets in producing revenue (Faccia, Al Naqbi and Lootah, 2019).

Particulars 2020 (£m) 2019 (£m)

Revenue 64760 63911

Average total assets = (Opening total assets + closing

total assets) / 2

54600 54817.5

Assets turnover ratio = revenue / average total assets 1.19 times 1.17 times

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2019 2020

1.155

1.16

1.165

1.17

1.175

1.18

1.185

1.19

1.195

1.17

1.19

Assets Turnover Ratio

Assets Turnover Ratio

From the above table, it can be observed that assets turnover ratio for 2019 was 1.17 times in

2019 which augmented to 1.19 times which echoes the better presentation of company in

employing its assets to make revenue. This is attributed to both augmented revenue and declined

average assets holding.

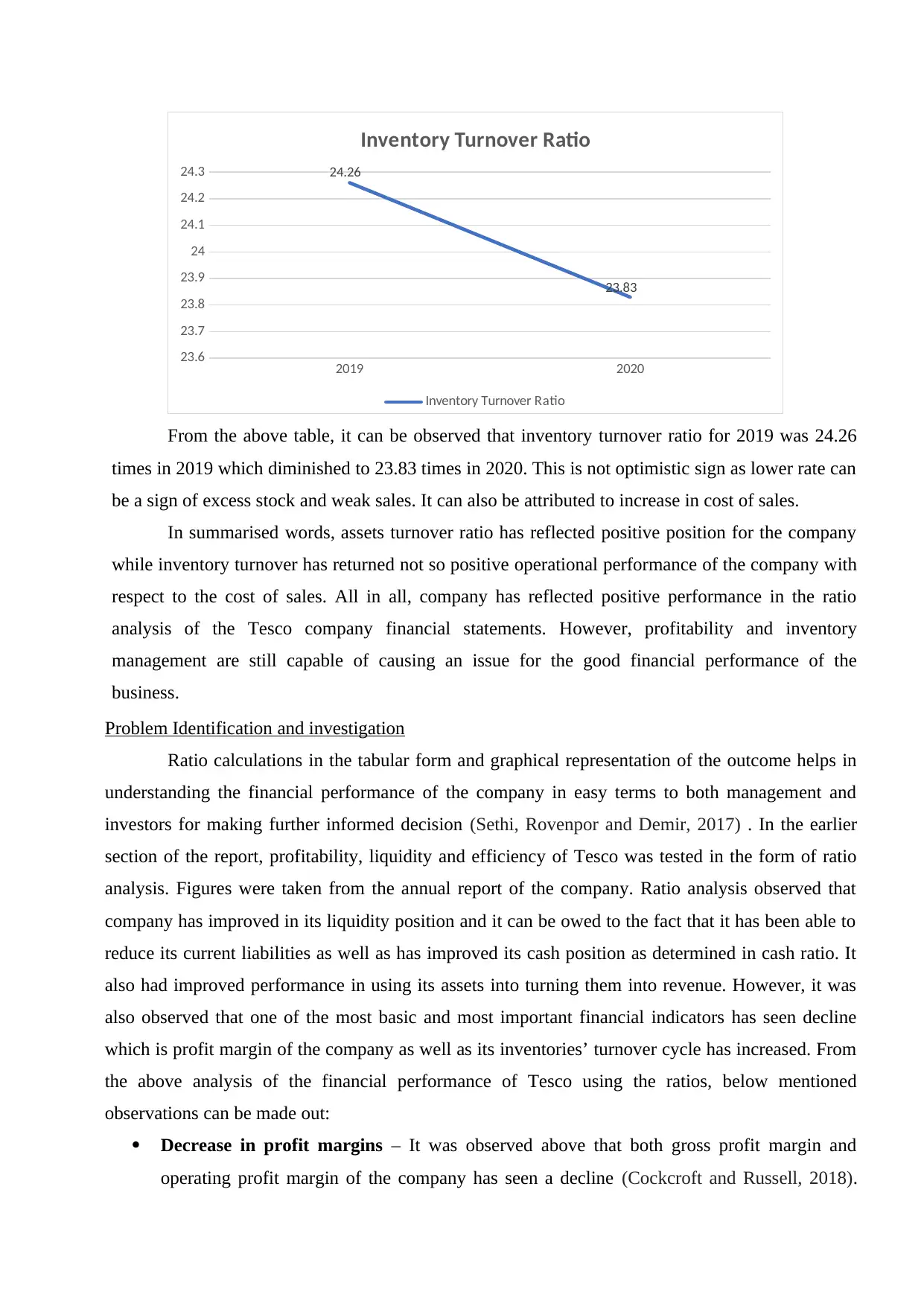

Inventory Turnover Ratio

It is also an indicator of business efficiency and is a metric that helps in defining number of

times the corporate is able to sell and substitute its stock (Amorelli and García‐Sánchez, 2021).

Particulars 2020 (£m) 2019 (£m)

Cost of sales 60180 59215

Average Inventory = Opening Inventory + Closing

Inventory / 2

2525 2440.5

Inventory turnover ratio = cost of sales / average

inventory

23.83 times 24.26 times

1.155

1.16

1.165

1.17

1.175

1.18

1.185

1.19

1.195

1.17

1.19

Assets Turnover Ratio

Assets Turnover Ratio

From the above table, it can be observed that assets turnover ratio for 2019 was 1.17 times in

2019 which augmented to 1.19 times which echoes the better presentation of company in

employing its assets to make revenue. This is attributed to both augmented revenue and declined

average assets holding.

Inventory Turnover Ratio

It is also an indicator of business efficiency and is a metric that helps in defining number of

times the corporate is able to sell and substitute its stock (Amorelli and García‐Sánchez, 2021).

Particulars 2020 (£m) 2019 (£m)

Cost of sales 60180 59215

Average Inventory = Opening Inventory + Closing

Inventory / 2

2525 2440.5

Inventory turnover ratio = cost of sales / average

inventory

23.83 times 24.26 times

2019 2020

23.6

23.7

23.8

23.9

24

24.1

24.2

24.3 24.26

23.83

Inventory Turnover Ratio

Inventory Turnover Ratio

From the above table, it can be observed that inventory turnover ratio for 2019 was 24.26

times in 2019 which diminished to 23.83 times in 2020. This is not optimistic sign as lower rate can

be a sign of excess stock and weak sales. It can also be attributed to increase in cost of sales.

In summarised words, assets turnover ratio has reflected positive position for the company

while inventory turnover has returned not so positive operational performance of the company with

respect to the cost of sales. All in all, company has reflected positive performance in the ratio

analysis of the Tesco company financial statements. However, profitability and inventory

management are still capable of causing an issue for the good financial performance of the

business.

Problem Identification and investigation

Ratio calculations in the tabular form and graphical representation of the outcome helps in

understanding the financial performance of the company in easy terms to both management and

investors for making further informed decision (Sethi, Rovenpor and Demir, 2017) . In the earlier

section of the report, profitability, liquidity and efficiency of Tesco was tested in the form of ratio

analysis. Figures were taken from the annual report of the company. Ratio analysis observed that

company has improved in its liquidity position and it can be owed to the fact that it has been able to

reduce its current liabilities as well as has improved its cash position as determined in cash ratio. It

also had improved performance in using its assets into turning them into revenue. However, it was

also observed that one of the most basic and most important financial indicators has seen decline

which is profit margin of the company as well as its inventories’ turnover cycle has increased. From

the above analysis of the financial performance of Tesco using the ratios, below mentioned

observations can be made out:

Decrease in profit margins – It was observed above that both gross profit margin and

operating profit margin of the company has seen a decline (Cockcroft and Russell, 2018).

23.6

23.7

23.8

23.9

24

24.1

24.2

24.3 24.26

23.83

Inventory Turnover Ratio

Inventory Turnover Ratio

From the above table, it can be observed that inventory turnover ratio for 2019 was 24.26

times in 2019 which diminished to 23.83 times in 2020. This is not optimistic sign as lower rate can

be a sign of excess stock and weak sales. It can also be attributed to increase in cost of sales.

In summarised words, assets turnover ratio has reflected positive position for the company

while inventory turnover has returned not so positive operational performance of the company with

respect to the cost of sales. All in all, company has reflected positive performance in the ratio

analysis of the Tesco company financial statements. However, profitability and inventory

management are still capable of causing an issue for the good financial performance of the

business.

Problem Identification and investigation

Ratio calculations in the tabular form and graphical representation of the outcome helps in

understanding the financial performance of the company in easy terms to both management and

investors for making further informed decision (Sethi, Rovenpor and Demir, 2017) . In the earlier

section of the report, profitability, liquidity and efficiency of Tesco was tested in the form of ratio

analysis. Figures were taken from the annual report of the company. Ratio analysis observed that

company has improved in its liquidity position and it can be owed to the fact that it has been able to

reduce its current liabilities as well as has improved its cash position as determined in cash ratio. It

also had improved performance in using its assets into turning them into revenue. However, it was

also observed that one of the most basic and most important financial indicators has seen decline

which is profit margin of the company as well as its inventories’ turnover cycle has increased. From

the above analysis of the financial performance of Tesco using the ratios, below mentioned

observations can be made out:

Decrease in profit margins – It was observed above that both gross profit margin and

operating profit margin of the company has seen a decline (Cockcroft and Russell, 2018).

These ratios have two components’ sales or revenue and expenses which on being reduced

from revenue, forms profit. For gross profit, direct expenses or cost of sales has to be

reduced from revenue to ascertain gross profit. On assessing the financial statements further,

it was identified that revenue of the group has improved by 1.33% but cost of sales has

increased by 1.63% which might has resulted in decline. This apparently looks like the

reason behind decline in operating margin as well for the administrative expenses has only

increased by 0.73% which is considered routine in nature. Prima Facie it looks like that

increased cost is due to disrupted supply chain because of global pandemic however, this

reason has to be ruled out since, the results being compared are up to 29th February, 2020 by

when the pandemic had not erupted violently. Therefore, these are due to other reasons such

as due to policy confusions due to Brexit or due to inflationary conditions in the economy,

etc. One point worth noting more is that though the comparison period is not marred by

pandemic but subsequent year would be affected by the pandemic. Therefore, declining

profitability is not a positive sign for the operational efficiency as well as financial

performance of the company (Wang and Sarkis, 2017).

Decline in inventory management – It was further observed from the ratio analysis that

inventory turnover ratio of the company has decreased. Inventory turnover ratio depicts the

number of times that inventory of the company rotates from raw material to delivery. It

forms the very important part of both working capital management as well as operational

efficiency of the company as it forms the basis of debtors’ and creditors’ management

policies and affects cash management of the company. This ratio has two components – one,

cost of sales and another, average inventory. As identified earlier, cost of sales had an

increase of 1.63% from 2019 to 2020. Average inventory refers to the average amount of the

inventory in the whole year. Therefore, closing and opening inventory is averaged to

determine average annual inventory figure. It denotes the mean figure of inventory holding in

the year by the company. Average inventory holding went up by 34.56% which must have

been the reason for the decline in the inventory turnover ratio. This is not a positive sign for

the inventory management of the company as Tesco is a retail company and increase in

average inventory holding means that company performance has declined (Moşteanu, Faccia

and Cavaliere, 2020).

from revenue, forms profit. For gross profit, direct expenses or cost of sales has to be

reduced from revenue to ascertain gross profit. On assessing the financial statements further,

it was identified that revenue of the group has improved by 1.33% but cost of sales has

increased by 1.63% which might has resulted in decline. This apparently looks like the

reason behind decline in operating margin as well for the administrative expenses has only

increased by 0.73% which is considered routine in nature. Prima Facie it looks like that

increased cost is due to disrupted supply chain because of global pandemic however, this

reason has to be ruled out since, the results being compared are up to 29th February, 2020 by

when the pandemic had not erupted violently. Therefore, these are due to other reasons such

as due to policy confusions due to Brexit or due to inflationary conditions in the economy,

etc. One point worth noting more is that though the comparison period is not marred by

pandemic but subsequent year would be affected by the pandemic. Therefore, declining

profitability is not a positive sign for the operational efficiency as well as financial

performance of the company (Wang and Sarkis, 2017).

Decline in inventory management – It was further observed from the ratio analysis that

inventory turnover ratio of the company has decreased. Inventory turnover ratio depicts the

number of times that inventory of the company rotates from raw material to delivery. It

forms the very important part of both working capital management as well as operational

efficiency of the company as it forms the basis of debtors’ and creditors’ management

policies and affects cash management of the company. This ratio has two components – one,

cost of sales and another, average inventory. As identified earlier, cost of sales had an

increase of 1.63% from 2019 to 2020. Average inventory refers to the average amount of the

inventory in the whole year. Therefore, closing and opening inventory is averaged to

determine average annual inventory figure. It denotes the mean figure of inventory holding in

the year by the company. Average inventory holding went up by 34.56% which must have

been the reason for the decline in the inventory turnover ratio. This is not a positive sign for

the inventory management of the company as Tesco is a retail company and increase in

average inventory holding means that company performance has declined (Moşteanu, Faccia

and Cavaliere, 2020).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Solutions and recommendations

In the above section of the report, two challenges for the company were identified. It was

identified that company has to deal with reduced profitability and reduced inventory turnover in the

comparative analysis of 2019 and 2020 performance. Further, period subsequent to the comparison

has been marred by the disruptions caused by the combined impacts of global pandemic, Brexit,

increased inflation, etc. Therefore, in order to reduce the negative impacts that these challenges are

capable of causing or to not increase the decline further, it is very important for company to

undertake the management of the inventory very seriously as underlying cause of both the declines

lies in the inventory management (Landi and Sciarelli, 2019).

To improve inventory management company should review its inventory order, holding and

delivery policies according to the changes that are required as per the present situation which has

additional challenges. Further, company is a retail business which operates in a low-cost model so

that profitability can be optimised. So, in order to increased its profitability level, company shall

check its cost structure again and make revised budgets and budgetary allocation.

Conclusion

Above report has been prepared for assessing business performance of a company. It was

analysed that ratio analysis is an easy form to understand and make observations about the

profitability, liquidity and efficiency of the company. Further, information observed from ratio

analysis helps determine the issues and challenges that are reflected in the financial statements. It is

very important as only after the issues are determined that, they can be worked upon to solve. All

this makes important contribution to ensure sound financial health of the company.

In the above section of the report, two challenges for the company were identified. It was

identified that company has to deal with reduced profitability and reduced inventory turnover in the

comparative analysis of 2019 and 2020 performance. Further, period subsequent to the comparison

has been marred by the disruptions caused by the combined impacts of global pandemic, Brexit,

increased inflation, etc. Therefore, in order to reduce the negative impacts that these challenges are

capable of causing or to not increase the decline further, it is very important for company to

undertake the management of the inventory very seriously as underlying cause of both the declines

lies in the inventory management (Landi and Sciarelli, 2019).

To improve inventory management company should review its inventory order, holding and

delivery policies according to the changes that are required as per the present situation which has

additional challenges. Further, company is a retail business which operates in a low-cost model so

that profitability can be optimised. So, in order to increased its profitability level, company shall

check its cost structure again and make revised budgets and budgetary allocation.

Conclusion

Above report has been prepared for assessing business performance of a company. It was

analysed that ratio analysis is an easy form to understand and make observations about the

profitability, liquidity and efficiency of the company. Further, information observed from ratio

analysis helps determine the issues and challenges that are reflected in the financial statements. It is

very important as only after the issues are determined that, they can be worked upon to solve. All

this makes important contribution to ensure sound financial health of the company.

References

Books and Journal

Amorelli, M. F. and García‐Sánchez, I. M., 2021. Trends in the dynamic evolution of board gender

diversity and corporate social responsibility. Corporate Social Responsibility and

Environmental Management. 28(2). pp.537-554.

Bajra, U. and Čadež, S., 2018. Audit committees and financial reporting quality: The 8th EU

Company Law Directive perspective. Economic Systems. 42(1). pp.151-163.

Chen, S. and Komal, B., 2018. Audit committee financial expertise and earnings quality: A meta-

analysis. Journal of Business Research. 84. pp.253-270.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice and

research. Australian Accounting Review. 28(3). pp.323-333.

Faccia, A., Al Naqbi, M. Y. K. and Lootah, S. A., 2019, August. Integrated Cloud Financial

Accounting Cycle: How Artificial Intelligence, Blockchain, and XBRL will Change the

Accounting, Fiscal and Auditing Practices. In Proceedings of the 2019 3rd International

Conference on Cloud and Big Data Computing (pp. 31-37).

Hsiao, P. C. K. and Kelly, M., 2018. Investment considerations and impressions of integrated

reporting. Sustainability Accounting, Management and Policy Journal.

Landi, G. and Sciarelli, M., 2019. Towards a more ethical market: the impact of ESG rating on

corporate financial performance. Social Responsibility Journal.

Moşteanu, N. R., Faccia, A. and Cavaliere, L. P. L., 2020, August. Disaster Management,

Digitalization and Financial Resources: key factors to keep the organization ongoing.

In Proceedings of the 2020 4th International Conference on Cloud and Big Data

Computing (pp. 118-122).

Raiborn, C. and et. al., 2017. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting & Finance. 28(2). pp.10-21.

Sethi, S. P., Rovenpor, J. L. and Demir, M., 2017. Enhancing the quality of reporting in corporate

social responsibility guidance documents: The roles of ISO 26000, global reporting

initiative and CSR‐sustainability monitor. Business and Society Review. 122(2). pp.139-163.

Wang, Z. and Sarkis, J., 2017. Corporate social responsibility governance, outcomes, and financial

performance. Journal of Cleaner Production. 162. pp.1607-1616.

Yung, K. and Root, A., 2019. Policy uncertainty and earnings management: International

evidence. Journal of Business Research. 100. pp.255-267.

Online

Tesco – Annual Report and Financial Statements 2020. 2021. [Online]. Available through:<

https://www.tescoplc.com/media/755761/tes006_ar2020_web_updated_200505.pdf>

Books and Journal

Amorelli, M. F. and García‐Sánchez, I. M., 2021. Trends in the dynamic evolution of board gender

diversity and corporate social responsibility. Corporate Social Responsibility and

Environmental Management. 28(2). pp.537-554.

Bajra, U. and Čadež, S., 2018. Audit committees and financial reporting quality: The 8th EU

Company Law Directive perspective. Economic Systems. 42(1). pp.151-163.

Chen, S. and Komal, B., 2018. Audit committee financial expertise and earnings quality: A meta-

analysis. Journal of Business Research. 84. pp.253-270.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice and

research. Australian Accounting Review. 28(3). pp.323-333.

Faccia, A., Al Naqbi, M. Y. K. and Lootah, S. A., 2019, August. Integrated Cloud Financial

Accounting Cycle: How Artificial Intelligence, Blockchain, and XBRL will Change the

Accounting, Fiscal and Auditing Practices. In Proceedings of the 2019 3rd International

Conference on Cloud and Big Data Computing (pp. 31-37).

Hsiao, P. C. K. and Kelly, M., 2018. Investment considerations and impressions of integrated

reporting. Sustainability Accounting, Management and Policy Journal.

Landi, G. and Sciarelli, M., 2019. Towards a more ethical market: the impact of ESG rating on

corporate financial performance. Social Responsibility Journal.

Moşteanu, N. R., Faccia, A. and Cavaliere, L. P. L., 2020, August. Disaster Management,

Digitalization and Financial Resources: key factors to keep the organization ongoing.

In Proceedings of the 2020 4th International Conference on Cloud and Big Data

Computing (pp. 118-122).

Raiborn, C. and et. al., 2017. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting & Finance. 28(2). pp.10-21.

Sethi, S. P., Rovenpor, J. L. and Demir, M., 2017. Enhancing the quality of reporting in corporate

social responsibility guidance documents: The roles of ISO 26000, global reporting

initiative and CSR‐sustainability monitor. Business and Society Review. 122(2). pp.139-163.

Wang, Z. and Sarkis, J., 2017. Corporate social responsibility governance, outcomes, and financial

performance. Journal of Cleaner Production. 162. pp.1607-1616.

Yung, K. and Root, A., 2019. Policy uncertainty and earnings management: International

evidence. Journal of Business Research. 100. pp.255-267.

Online

Tesco – Annual Report and Financial Statements 2020. 2021. [Online]. Available through:<

https://www.tescoplc.com/media/755761/tes006_ar2020_web_updated_200505.pdf>

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.