Investment Analysis and Portfolio Management Assignment Solution

VerifiedAdded on 2023/01/18

|9

|1647

|98

Homework Assignment

AI Summary

This document presents a comprehensive solution to an investment analysis and portfolio management assignment, focusing on the analysis of BHP Billiton Limited and Telstra Corporation Limited. The solution includes calculations for the minimum variance portfolio, plotting the efficient frontier, and determining the risk aversion utility function. It also calculates the optimal risky portfolio and indicates the slope of the capital asset line. Furthermore, the assignment addresses the advantages and disadvantages of the index model compared to the Markowitz model, and explores the trade-offs in actively managed portfolios. Finally, the solution evaluates investor performance based on abnormal returns, considering different T-bill rates. This assignment, contributed by a student, provides a detailed analysis of investment strategies and portfolio optimization techniques.

Running head: INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

Investment Analysis and Portfolio Management

Name of the Student:

Name of the University:

Authors Note:

Investment Analysis and Portfolio Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

1

Table of Contents

Question 2:.................................................................................................................................2

a. Calculating the Minimum variance portfolio:........................................................................2

b. Plotting the efficient frontier:.................................................................................................3

c. Calculating the risk aversion utility function:........................................................................3

d. Calculating the optimal risky portfolio:.................................................................................4

e. Indicating the slope of the capital asset line of this optimal risky portfolio:.........................4

f. Calculating the risk aversion utility function:.........................................................................4

Question 3:.................................................................................................................................5

1. Advantages and disadvantages of index model compared with Markowitz:.........................5

2. Stating the basic trade-off when departing from pure indexing in favour of an actively

managed portfolio:.....................................................................................................................5

3a. Detecting which investors were better selector:...................................................................6

3b. Detecting which investors were better selector when T-bill is 5%:.....................................6

3c. Detecting which investors was better selector when T-bill is 3%:.......................................6

References and Bibliography:....................................................................................................8

1

Table of Contents

Question 2:.................................................................................................................................2

a. Calculating the Minimum variance portfolio:........................................................................2

b. Plotting the efficient frontier:.................................................................................................3

c. Calculating the risk aversion utility function:........................................................................3

d. Calculating the optimal risky portfolio:.................................................................................4

e. Indicating the slope of the capital asset line of this optimal risky portfolio:.........................4

f. Calculating the risk aversion utility function:.........................................................................4

Question 3:.................................................................................................................................5

1. Advantages and disadvantages of index model compared with Markowitz:.........................5

2. Stating the basic trade-off when departing from pure indexing in favour of an actively

managed portfolio:.....................................................................................................................5

3a. Detecting which investors were better selector:...................................................................6

3b. Detecting which investors were better selector when T-bill is 5%:.....................................6

3c. Detecting which investors was better selector when T-bill is 3%:.......................................6

References and Bibliography:....................................................................................................8

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

2

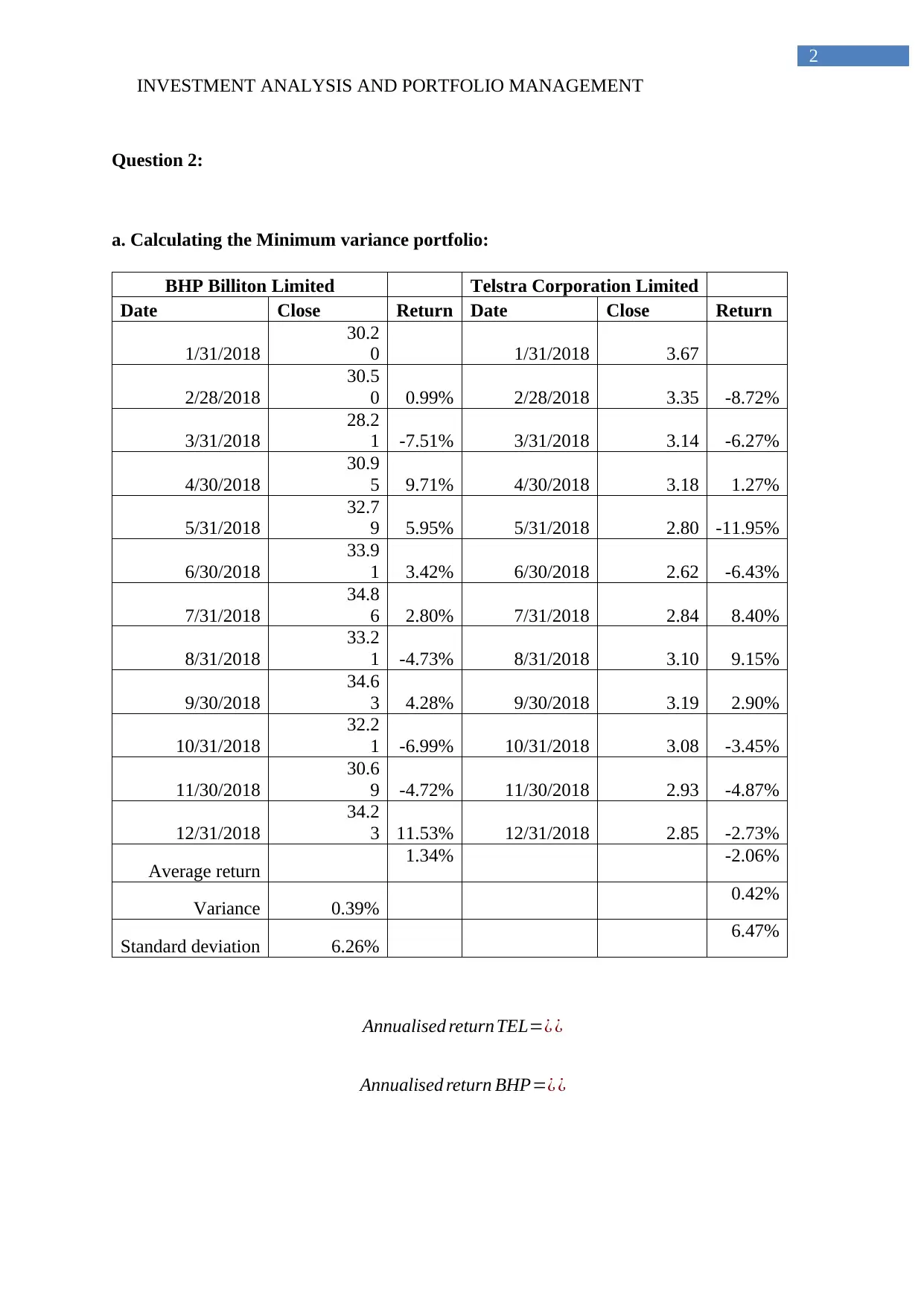

Question 2:

a. Calculating the Minimum variance portfolio:

BHP Billiton Limited Telstra Corporation Limited

Date Close Return Date Close Return

1/31/2018

30.2

0 1/31/2018 3.67

2/28/2018

30.5

0 0.99% 2/28/2018 3.35 -8.72%

3/31/2018

28.2

1 -7.51% 3/31/2018 3.14 -6.27%

4/30/2018

30.9

5 9.71% 4/30/2018 3.18 1.27%

5/31/2018

32.7

9 5.95% 5/31/2018 2.80 -11.95%

6/30/2018

33.9

1 3.42% 6/30/2018 2.62 -6.43%

7/31/2018

34.8

6 2.80% 7/31/2018 2.84 8.40%

8/31/2018

33.2

1 -4.73% 8/31/2018 3.10 9.15%

9/30/2018

34.6

3 4.28% 9/30/2018 3.19 2.90%

10/31/2018

32.2

1 -6.99% 10/31/2018 3.08 -3.45%

11/30/2018

30.6

9 -4.72% 11/30/2018 2.93 -4.87%

12/31/2018

34.2

3 11.53% 12/31/2018 2.85 -2.73%

Average return 1.34% -2.06%

Variance 0.39% 0.42%

Standard deviation 6.26% 6.47%

Annualised return TEL=¿ ¿

Annualised return BHP=¿ ¿

2

Question 2:

a. Calculating the Minimum variance portfolio:

BHP Billiton Limited Telstra Corporation Limited

Date Close Return Date Close Return

1/31/2018

30.2

0 1/31/2018 3.67

2/28/2018

30.5

0 0.99% 2/28/2018 3.35 -8.72%

3/31/2018

28.2

1 -7.51% 3/31/2018 3.14 -6.27%

4/30/2018

30.9

5 9.71% 4/30/2018 3.18 1.27%

5/31/2018

32.7

9 5.95% 5/31/2018 2.80 -11.95%

6/30/2018

33.9

1 3.42% 6/30/2018 2.62 -6.43%

7/31/2018

34.8

6 2.80% 7/31/2018 2.84 8.40%

8/31/2018

33.2

1 -4.73% 8/31/2018 3.10 9.15%

9/30/2018

34.6

3 4.28% 9/30/2018 3.19 2.90%

10/31/2018

32.2

1 -6.99% 10/31/2018 3.08 -3.45%

11/30/2018

30.6

9 -4.72% 11/30/2018 2.93 -4.87%

12/31/2018

34.2

3 11.53% 12/31/2018 2.85 -2.73%

Average return 1.34% -2.06%

Variance 0.39% 0.42%

Standard deviation 6.26% 6.47%

Annualised return TEL=¿ ¿

Annualised return BHP=¿ ¿

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

3

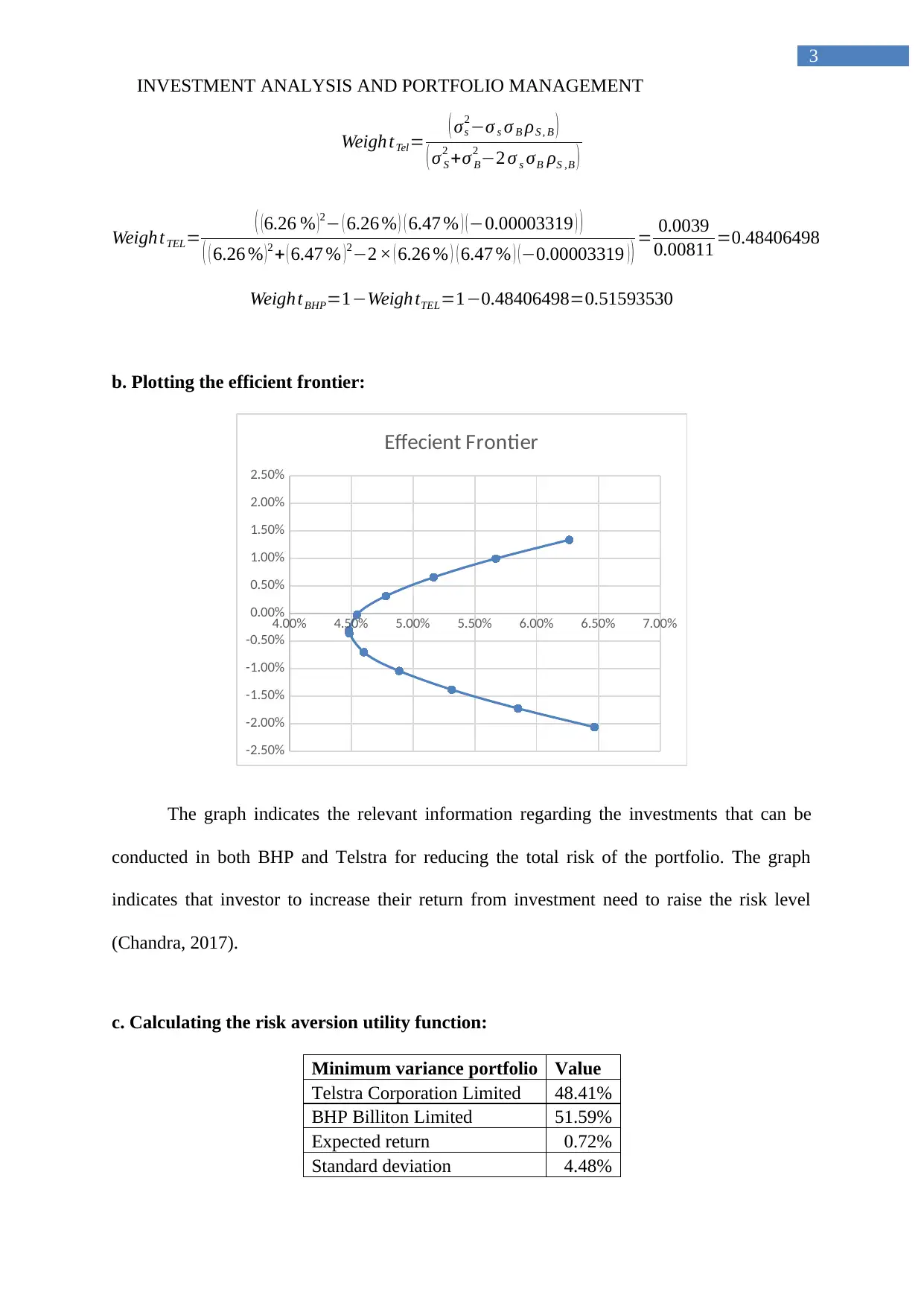

Weigh tTel= ( σs

2−σ s σ B ρS , B )

( σ S

2 +σ B

2 −2 σ s σB ρS ,B )

Weigh tTEL= ( ( 6.26 % ) 2− ( 6.26 % ) ( 6.47 % ) ( −0.00003319 ) )

( ( 6.26 % ) 2 + ( 6.47 % ) 2−2 × ( 6.26 % ) ( 6.47 % ) ( −0.00003319 ) ) = 0.0039

0.00811 =0.48406498

Weigh tBHP=1−Weigh tTEL=1−0.48406498=0.51593530

b. Plotting the efficient frontier:

4.00% 4.50% 5.00% 5.50% 6.00% 6.50% 7.00%

-2.50%

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

Effecient Frontier

The graph indicates the relevant information regarding the investments that can be

conducted in both BHP and Telstra for reducing the total risk of the portfolio. The graph

indicates that investor to increase their return from investment need to raise the risk level

(Chandra, 2017).

c. Calculating the risk aversion utility function:

Minimum variance portfolio Value

Telstra Corporation Limited 48.41%

BHP Billiton Limited 51.59%

Expected return 0.72%

Standard deviation 4.48%

3

Weigh tTel= ( σs

2−σ s σ B ρS , B )

( σ S

2 +σ B

2 −2 σ s σB ρS ,B )

Weigh tTEL= ( ( 6.26 % ) 2− ( 6.26 % ) ( 6.47 % ) ( −0.00003319 ) )

( ( 6.26 % ) 2 + ( 6.47 % ) 2−2 × ( 6.26 % ) ( 6.47 % ) ( −0.00003319 ) ) = 0.0039

0.00811 =0.48406498

Weigh tBHP=1−Weigh tTEL=1−0.48406498=0.51593530

b. Plotting the efficient frontier:

4.00% 4.50% 5.00% 5.50% 6.00% 6.50% 7.00%

-2.50%

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

Effecient Frontier

The graph indicates the relevant information regarding the investments that can be

conducted in both BHP and Telstra for reducing the total risk of the portfolio. The graph

indicates that investor to increase their return from investment need to raise the risk level

(Chandra, 2017).

c. Calculating the risk aversion utility function:

Minimum variance portfolio Value

Telstra Corporation Limited 48.41%

BHP Billiton Limited 51.59%

Expected return 0.72%

Standard deviation 4.48%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

4

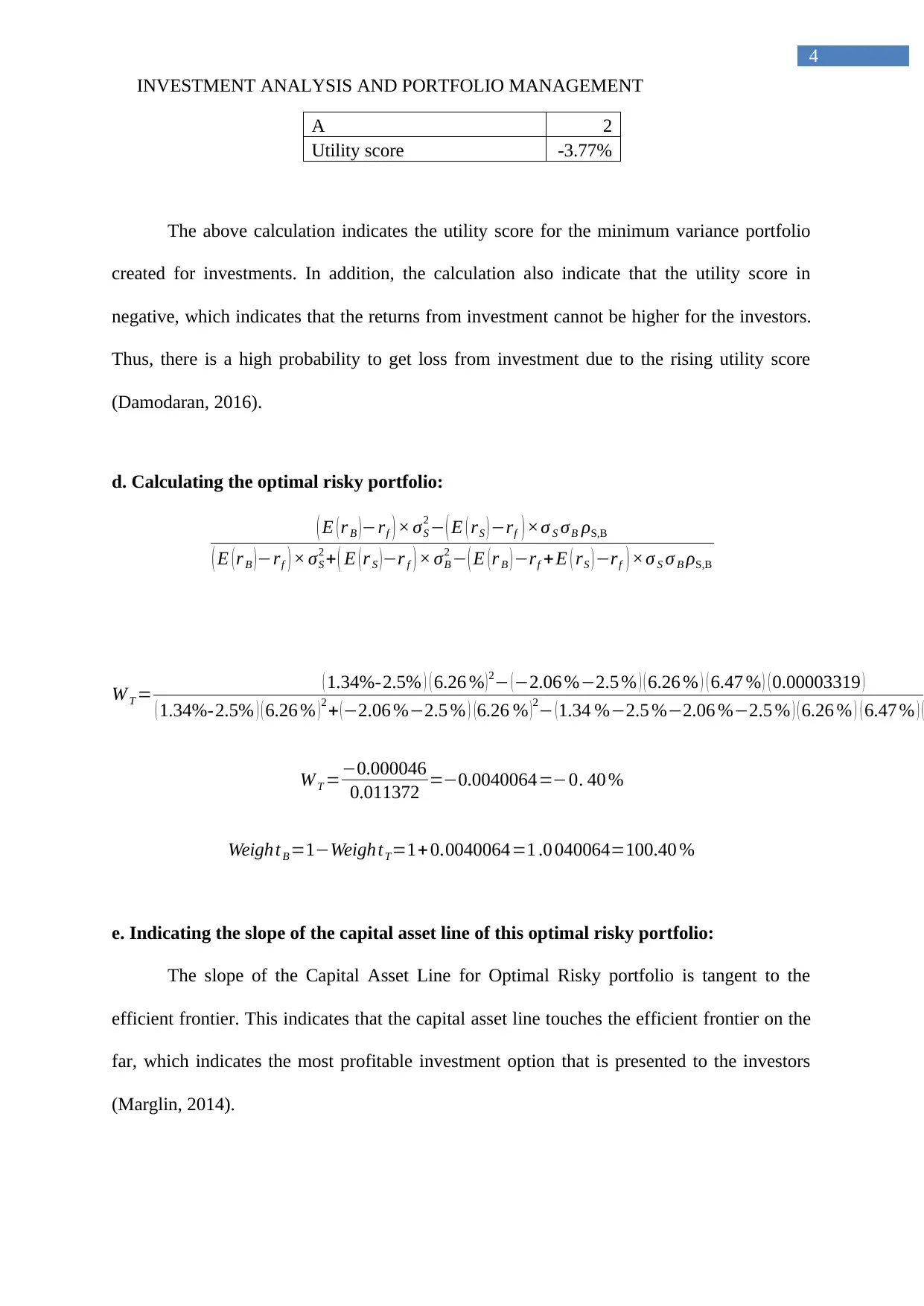

A 2

Utility score -3.77%

The above calculation indicates the utility score for the minimum variance portfolio

created for investments. In addition, the calculation also indicate that the utility score in

negative, which indicates that the returns from investment cannot be higher for the investors.

Thus, there is a high probability to get loss from investment due to the rising utility score

(Damodaran, 2016).

d. Calculating the optimal risky portfolio:

( E ( r B )−rf ) × σS

2 − ( E ( rS ) −rf ) ×σ S σB ρS,B

( E ( r B )−rf ) × σS

2 + ( E ( r S )−r f ) × σB

2 − ( E (r B ) −rf + E ( rS ) −rf ) ×σ S σ B ρS,B

W T = ( 1.34%-2.5% ) ( 6.26 % )2− (−2.06 %−2.5 % ) ( 6.26 % ) ( 6.47 % ) ( 0.00003319 )

( 1.34%-2.5% ) ( 6.26 % )2 + (−2.06 %−2.5 % ) (6.26 % )2− (1.34 %−2.5 %−2.06 %−2.5 % ) ( 6.26 % ) ( 6.47 % ) (

W T =−0.000046

0.011372 =−0.0040064=−0. 40 %

Weight B =1−WeightT=1+ 0.0040064=1 .0 040064=100.40 %

e. Indicating the slope of the capital asset line of this optimal risky portfolio:

The slope of the Capital Asset Line for Optimal Risky portfolio is tangent to the

efficient frontier. This indicates that the capital asset line touches the efficient frontier on the

far, which indicates the most profitable investment option that is presented to the investors

(Marglin, 2014).

4

A 2

Utility score -3.77%

The above calculation indicates the utility score for the minimum variance portfolio

created for investments. In addition, the calculation also indicate that the utility score in

negative, which indicates that the returns from investment cannot be higher for the investors.

Thus, there is a high probability to get loss from investment due to the rising utility score

(Damodaran, 2016).

d. Calculating the optimal risky portfolio:

( E ( r B )−rf ) × σS

2 − ( E ( rS ) −rf ) ×σ S σB ρS,B

( E ( r B )−rf ) × σS

2 + ( E ( r S )−r f ) × σB

2 − ( E (r B ) −rf + E ( rS ) −rf ) ×σ S σ B ρS,B

W T = ( 1.34%-2.5% ) ( 6.26 % )2− (−2.06 %−2.5 % ) ( 6.26 % ) ( 6.47 % ) ( 0.00003319 )

( 1.34%-2.5% ) ( 6.26 % )2 + (−2.06 %−2.5 % ) (6.26 % )2− (1.34 %−2.5 %−2.06 %−2.5 % ) ( 6.26 % ) ( 6.47 % ) (

W T =−0.000046

0.011372 =−0.0040064=−0. 40 %

Weight B =1−WeightT=1+ 0.0040064=1 .0 040064=100.40 %

e. Indicating the slope of the capital asset line of this optimal risky portfolio:

The slope of the Capital Asset Line for Optimal Risky portfolio is tangent to the

efficient frontier. This indicates that the capital asset line touches the efficient frontier on the

far, which indicates the most profitable investment option that is presented to the investors

(Marglin, 2014).

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

5

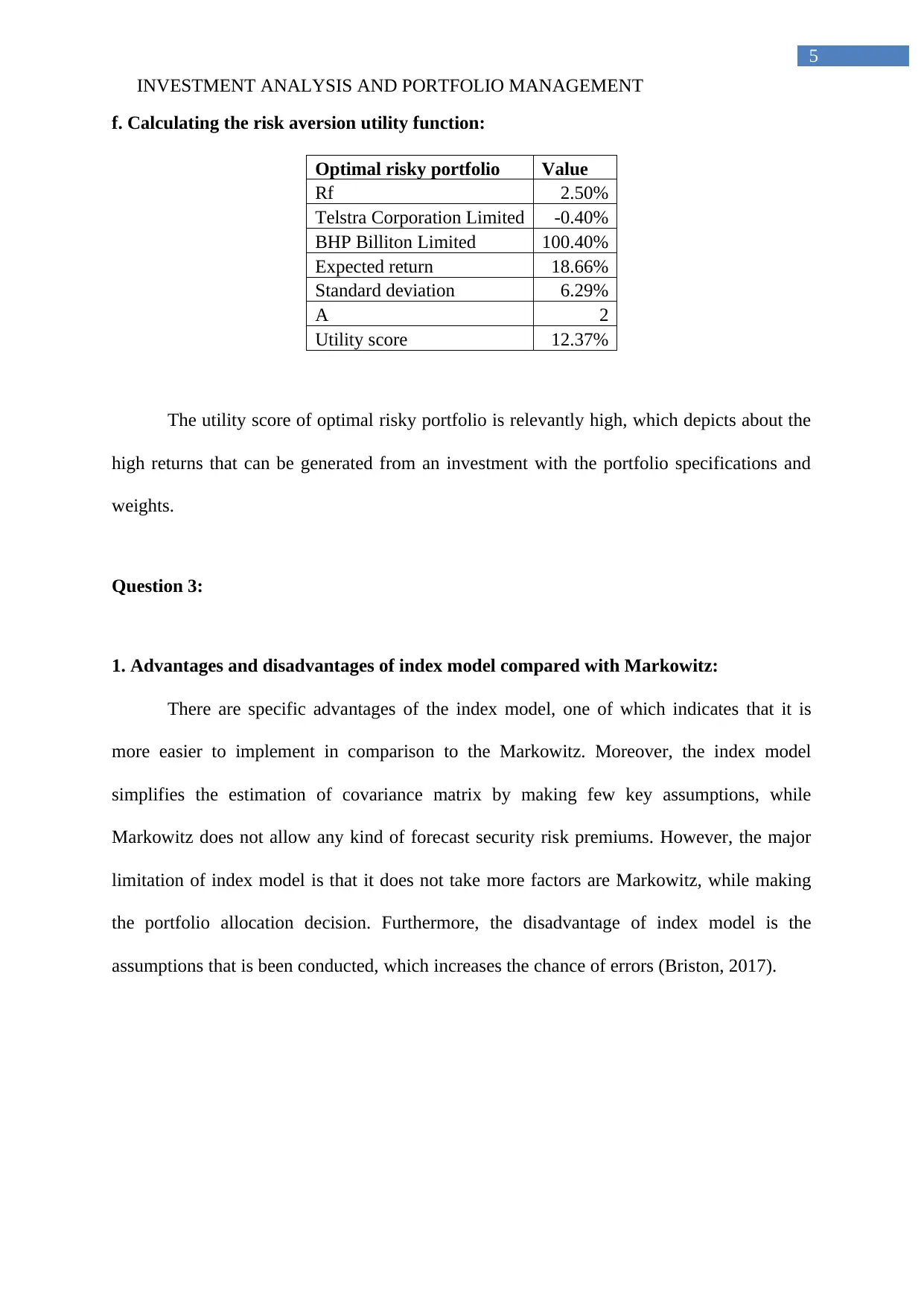

f. Calculating the risk aversion utility function:

Optimal risky portfolio Value

Rf 2.50%

Telstra Corporation Limited -0.40%

BHP Billiton Limited 100.40%

Expected return 18.66%

Standard deviation 6.29%

A 2

Utility score 12.37%

The utility score of optimal risky portfolio is relevantly high, which depicts about the

high returns that can be generated from an investment with the portfolio specifications and

weights.

Question 3:

1. Advantages and disadvantages of index model compared with Markowitz:

There are specific advantages of the index model, one of which indicates that it is

more easier to implement in comparison to the Markowitz. Moreover, the index model

simplifies the estimation of covariance matrix by making few key assumptions, while

Markowitz does not allow any kind of forecast security risk premiums. However, the major

limitation of index model is that it does not take more factors are Markowitz, while making

the portfolio allocation decision. Furthermore, the disadvantage of index model is the

assumptions that is been conducted, which increases the chance of errors (Briston, 2017).

5

f. Calculating the risk aversion utility function:

Optimal risky portfolio Value

Rf 2.50%

Telstra Corporation Limited -0.40%

BHP Billiton Limited 100.40%

Expected return 18.66%

Standard deviation 6.29%

A 2

Utility score 12.37%

The utility score of optimal risky portfolio is relevantly high, which depicts about the

high returns that can be generated from an investment with the portfolio specifications and

weights.

Question 3:

1. Advantages and disadvantages of index model compared with Markowitz:

There are specific advantages of the index model, one of which indicates that it is

more easier to implement in comparison to the Markowitz. Moreover, the index model

simplifies the estimation of covariance matrix by making few key assumptions, while

Markowitz does not allow any kind of forecast security risk premiums. However, the major

limitation of index model is that it does not take more factors are Markowitz, while making

the portfolio allocation decision. Furthermore, the disadvantage of index model is the

assumptions that is been conducted, which increases the chance of errors (Briston, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

6

2. Stating the basic trade-off when departing from pure indexing in favour of an

actively managed portfolio:

The additional management fees incurred towards managing the portfolio with a

possibility of superior performance is known as the basic trade-off when departing from pure-

indexing activity.

3a. Detecting which investors were better selector:

The determination of the better selector is not possible without the detection of the

abnormal returns. There is no information regarding the parameters such as risk free rate and

market return, which is used for detecting the abnormal return from an investment. Without

the detection for the abnormal returns it is hard to say which investor is the better selector.

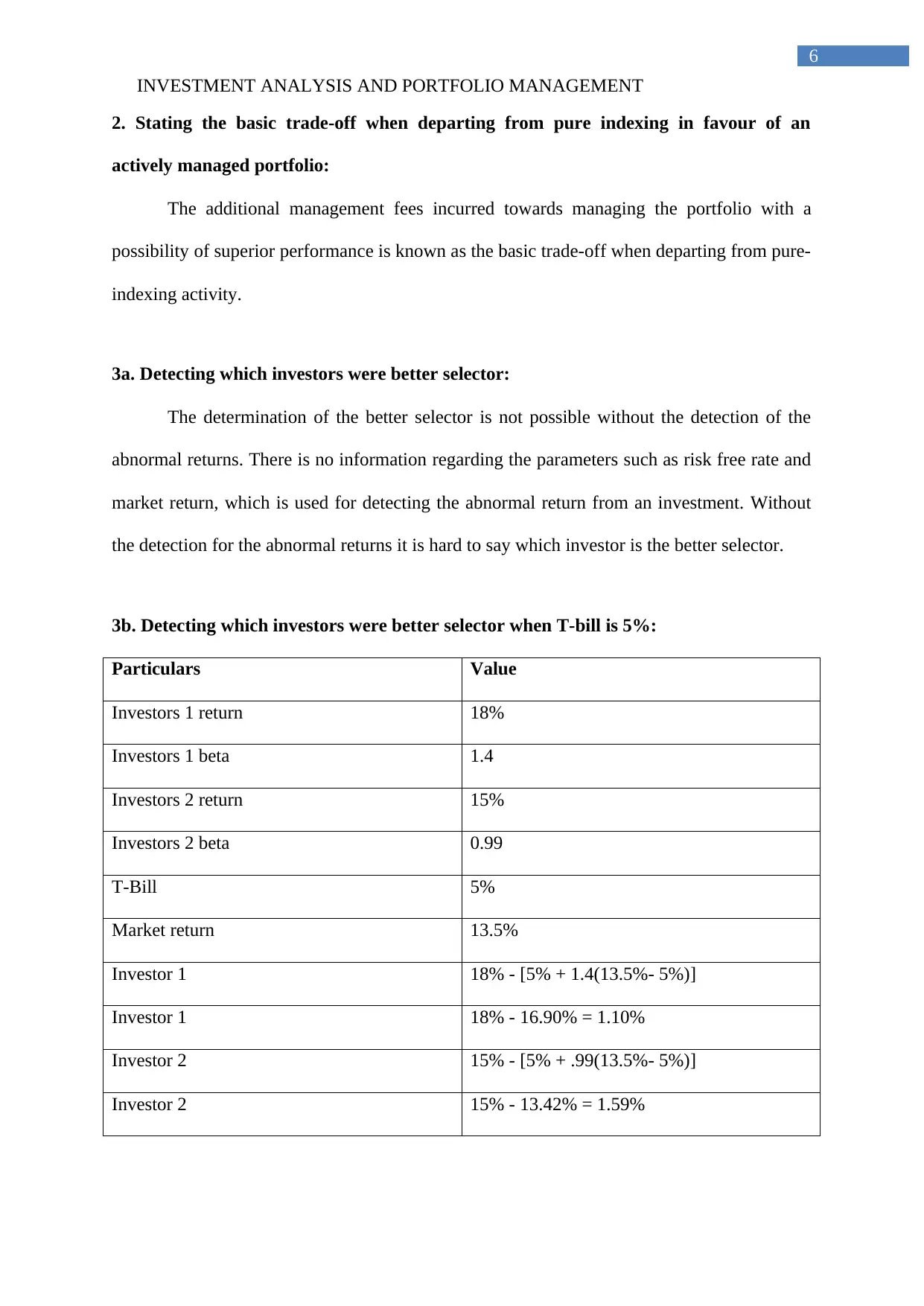

3b. Detecting which investors were better selector when T-bill is 5%:

Particulars Value

Investors 1 return 18%

Investors 1 beta 1.4

Investors 2 return 15%

Investors 2 beta 0.99

T-Bill 5%

Market return 13.5%

Investor 1 18% - [5% + 1.4(13.5%- 5%)]

Investor 1 18% - 16.90% = 1.10%

Investor 2 15% - [5% + .99(13.5%- 5%)]

Investor 2 15% - 13.42% = 1.59%

6

2. Stating the basic trade-off when departing from pure indexing in favour of an

actively managed portfolio:

The additional management fees incurred towards managing the portfolio with a

possibility of superior performance is known as the basic trade-off when departing from pure-

indexing activity.

3a. Detecting which investors were better selector:

The determination of the better selector is not possible without the detection of the

abnormal returns. There is no information regarding the parameters such as risk free rate and

market return, which is used for detecting the abnormal return from an investment. Without

the detection for the abnormal returns it is hard to say which investor is the better selector.

3b. Detecting which investors were better selector when T-bill is 5%:

Particulars Value

Investors 1 return 18%

Investors 1 beta 1.4

Investors 2 return 15%

Investors 2 beta 0.99

T-Bill 5%

Market return 13.5%

Investor 1 18% - [5% + 1.4(13.5%- 5%)]

Investor 1 18% - 16.90% = 1.10%

Investor 2 15% - [5% + .99(13.5%- 5%)]

Investor 2 15% - 13.42% = 1.59%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

7

Investor 2 will be selected as the better selector, as its abnormal returns are higher

than investor 1.

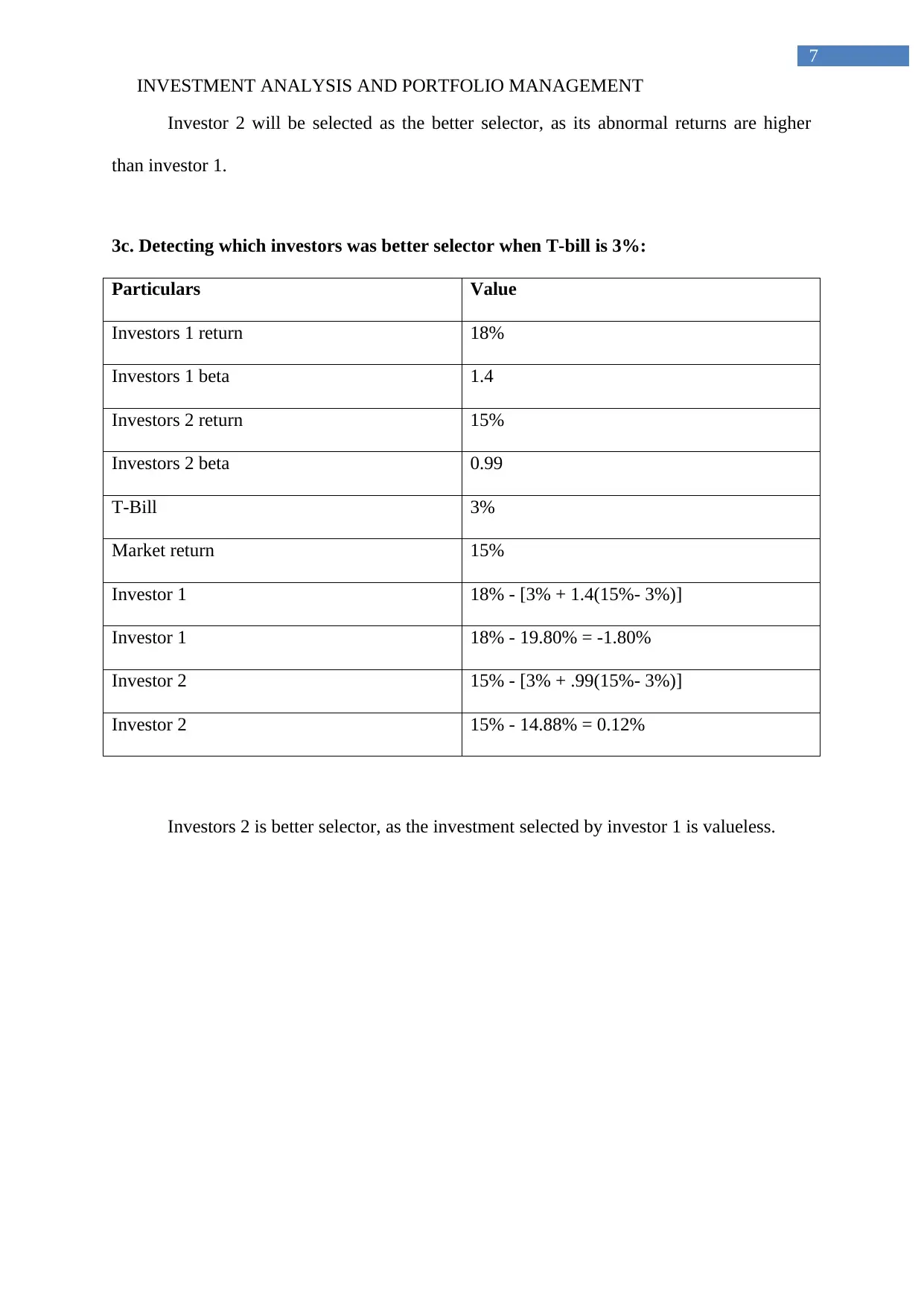

3c. Detecting which investors was better selector when T-bill is 3%:

Particulars Value

Investors 1 return 18%

Investors 1 beta 1.4

Investors 2 return 15%

Investors 2 beta 0.99

T-Bill 3%

Market return 15%

Investor 1 18% - [3% + 1.4(15%- 3%)]

Investor 1 18% - 19.80% = -1.80%

Investor 2 15% - [3% + .99(15%- 3%)]

Investor 2 15% - 14.88% = 0.12%

Investors 2 is better selector, as the investment selected by investor 1 is valueless.

7

Investor 2 will be selected as the better selector, as its abnormal returns are higher

than investor 1.

3c. Detecting which investors was better selector when T-bill is 3%:

Particulars Value

Investors 1 return 18%

Investors 1 beta 1.4

Investors 2 return 15%

Investors 2 beta 0.99

T-Bill 3%

Market return 15%

Investor 1 18% - [3% + 1.4(15%- 3%)]

Investor 1 18% - 19.80% = -1.80%

Investor 2 15% - [3% + .99(15%- 3%)]

Investor 2 15% - 14.88% = 0.12%

Investors 2 is better selector, as the investment selected by investor 1 is valueless.

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

8

References and Bibliography:

Briston, R. J. (2017). The stock exchange and investment analysis. Routledge.

Chandra, P. (2017). Investment analysis and portfolio management. McGraw-Hill Education.

Chisholm, D., Sweeny, K., Sheehan, P., Rasmussen, B., Smit, F., Cuijpers, P., & Saxena, S.

(2016). Scaling-up treatment of depression and anxiety: a global return on investment

analysis. The Lancet Psychiatry, 3(5), 415-424.

Damodaran, A. (2016). Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., Anson, M. J., & Runkle, D. E.

(2015). Quantitative investment analysis. John Wiley & Sons.

Marglin, S. A. (2014). Public Investment Criteria (Routledge Revivals): Benefit-Cost

Analysis for Planned Economic Growth. Routledge.

8

References and Bibliography:

Briston, R. J. (2017). The stock exchange and investment analysis. Routledge.

Chandra, P. (2017). Investment analysis and portfolio management. McGraw-Hill Education.

Chisholm, D., Sweeny, K., Sheehan, P., Rasmussen, B., Smit, F., Cuijpers, P., & Saxena, S.

(2016). Scaling-up treatment of depression and anxiety: a global return on investment

analysis. The Lancet Psychiatry, 3(5), 415-424.

Damodaran, A. (2016). Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., Anson, M. J., & Runkle, D. E.

(2015). Quantitative investment analysis. John Wiley & Sons.

Marglin, S. A. (2014). Public Investment Criteria (Routledge Revivals): Benefit-Cost

Analysis for Planned Economic Growth. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.