Investment and Portfolio Management

VerifiedAdded on 2021/06/18

|18

|3614

|47

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: INVESTMENT AND PORTFOLIO MANAGEMENT

Investment and portfolio management

University Name

Student Name

Authors’ Note

Investment and portfolio management

University Name

Student Name

Authors’ Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2INVESTMENT AND PORTFOLIO MANAGEMENT

Answer to question 2.2:

Vanguard MSCI Australian small companies index is an exchange traded fund that

intends to match the return in terms of capital appreciation and income of the MSCI small cap

index Australian shares. The fund is a small capitalisation index that generally involves

smaller companies on the equity market of Australia that target coverage of around 14% of

free float of market capitalisation of share market that is adjusted. Such return from fund is

considered before the expenses, tax and fees are taken into consideration. The fund intends to

provide investors with diversified exposure and low cost to the small companies that is listed

on stock exchange of Australia. This is indicative of the fact that investors are provided with

the low cost way for making investment in the portfolio of smallest companies of Australia.

A sector in which the investment is made by the fund involves materials, industrial,

financials, real estate, information technology, healthcare, Utilities, energy, consumer staples

and customer discretionary (Stettina and Hörz 2015). It can therefore be seen that the fund

makes investment in diversified sectors with maximum percentage of allocation made in

materials sector and minimum allocation made in 1.2. A long term potential capital growth is

offered by the fund that can be typical to the market sector of small company.

Objective and strategies of fund:

The objective of fund is to track the appreciation of capita and income of the FTSE

ASFA Australia index high dividend yield. Most of the securities of fund will involve FTSE

ASFA Australia index high dividend yield that will allow weighting on individual security to

vary marginally from index. In addition to this, investment in securities may be made by fund

that is expected to be included in the index it has been removed form index. The fund

provides investors with benefits of diversification, potential return that is tax effective, risks

and potential of capital growth and income that is tax effective. Moreover, fund has potential

Answer to question 2.2:

Vanguard MSCI Australian small companies index is an exchange traded fund that

intends to match the return in terms of capital appreciation and income of the MSCI small cap

index Australian shares. The fund is a small capitalisation index that generally involves

smaller companies on the equity market of Australia that target coverage of around 14% of

free float of market capitalisation of share market that is adjusted. Such return from fund is

considered before the expenses, tax and fees are taken into consideration. The fund intends to

provide investors with diversified exposure and low cost to the small companies that is listed

on stock exchange of Australia. This is indicative of the fact that investors are provided with

the low cost way for making investment in the portfolio of smallest companies of Australia.

A sector in which the investment is made by the fund involves materials, industrial,

financials, real estate, information technology, healthcare, Utilities, energy, consumer staples

and customer discretionary (Stettina and Hörz 2015). It can therefore be seen that the fund

makes investment in diversified sectors with maximum percentage of allocation made in

materials sector and minimum allocation made in 1.2. A long term potential capital growth is

offered by the fund that can be typical to the market sector of small company.

Objective and strategies of fund:

The objective of fund is to track the appreciation of capita and income of the FTSE

ASFA Australia index high dividend yield. Most of the securities of fund will involve FTSE

ASFA Australia index high dividend yield that will allow weighting on individual security to

vary marginally from index. In addition to this, investment in securities may be made by fund

that is expected to be included in the index it has been removed form index. The fund

provides investors with benefits of diversification, potential return that is tax effective, risks

and potential of capital growth and income that is tax effective. Moreover, fund has potential

3INVESTMENT AND PORTFOLIO MANAGEMENT

for some loss of capital and generating returns that is below average with higher risk level.

Investors are able to achieve broad range of diversification across multiple classes of assets

with exchange funds of lower class. A label fixed interest strategy is offered by fund that

helps in preservation of risk characteristics and diversification of varied range of assets by

making investment in securities of higher grade (Klingebiel and Rammer 2014).

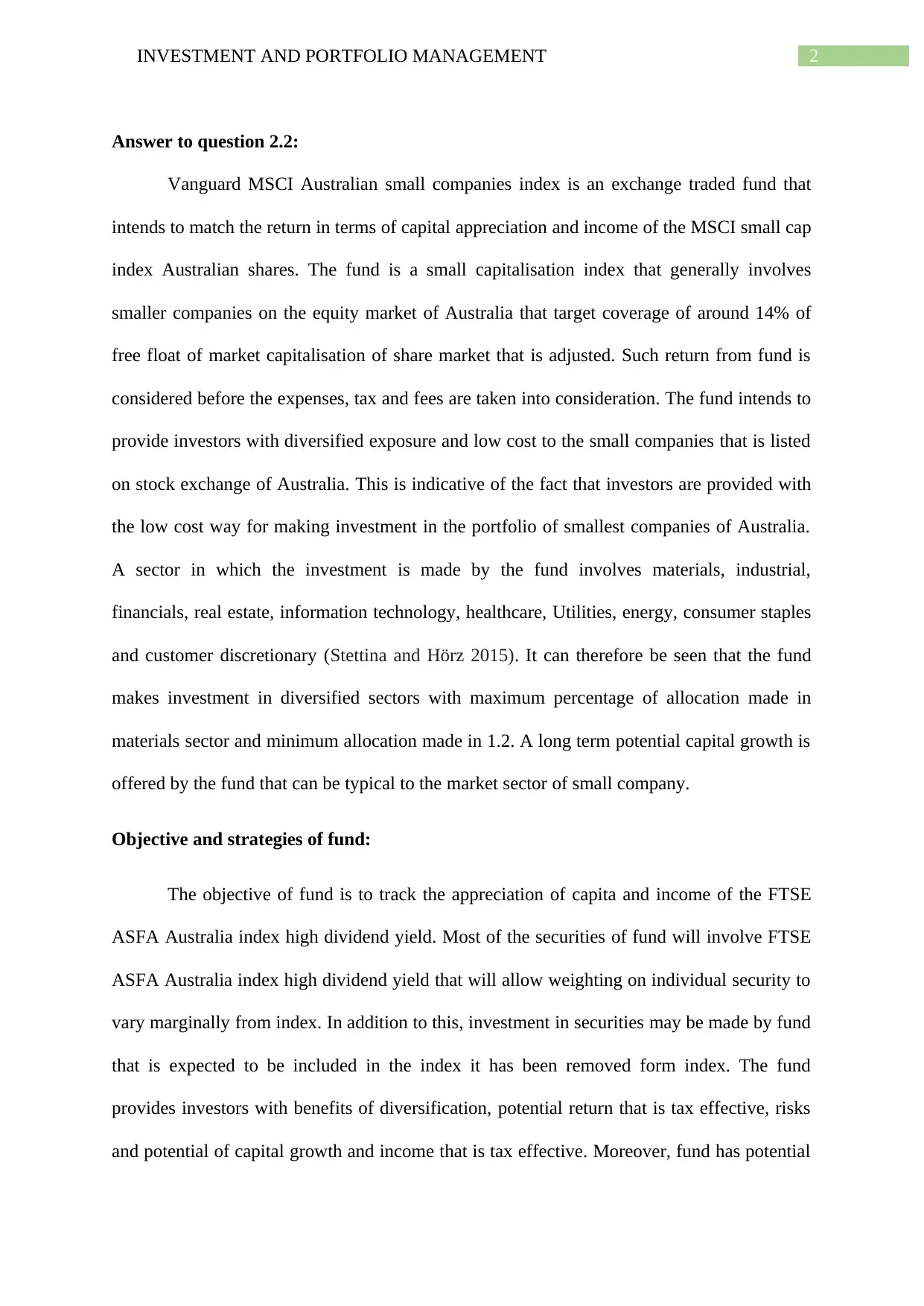

Performance history of fund:

Performance history:

(Source: investsmart.com.au 2018)

The above graph depicts that the performance of fund has improved over the years.

The closing price of fund as on 5th May, 2018 stood at AUD 57.34 and has a share class size

of 153.28.

for some loss of capital and generating returns that is below average with higher risk level.

Investors are able to achieve broad range of diversification across multiple classes of assets

with exchange funds of lower class. A label fixed interest strategy is offered by fund that

helps in preservation of risk characteristics and diversification of varied range of assets by

making investment in securities of higher grade (Klingebiel and Rammer 2014).

Performance history of fund:

Performance history:

(Source: investsmart.com.au 2018)

The above graph depicts that the performance of fund has improved over the years.

The closing price of fund as on 5th May, 2018 stood at AUD 57.34 and has a share class size

of 153.28.

4INVESTMENT AND PORTFOLIO MANAGEMENT

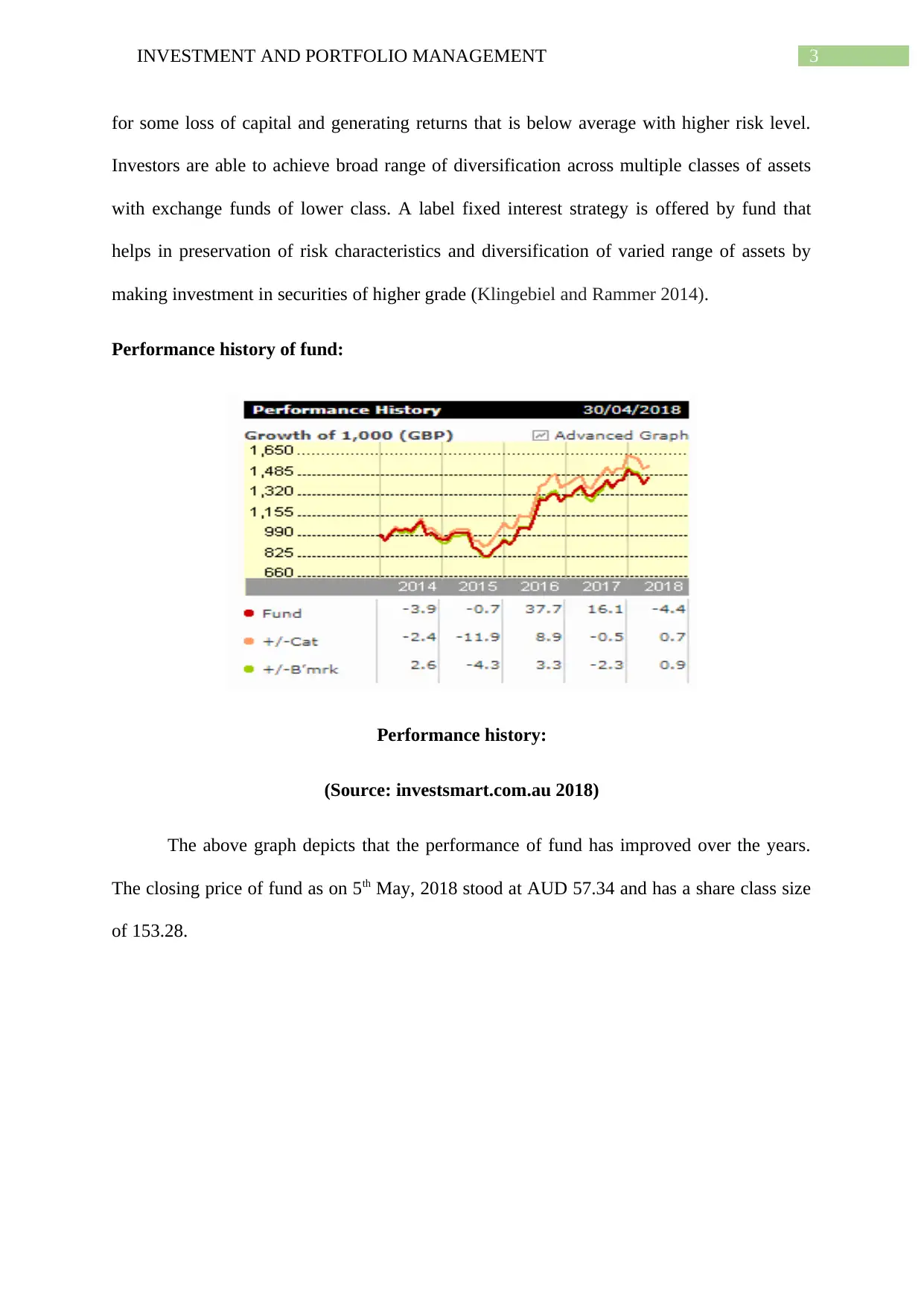

Performance of funds

(Source: investsmart.com.au 2018)

The above table depicts the performance of fund ranging from time period of 1 month

to 10 years. Growth of fund during the time period of one month was negative at -1.97 while

that of five years growth stood at 3.09. Highest growth was recorded during six months and

one year. Portfolio of assets incorporated into this particular fund comprises of top ten

holdings namely Iluka resources Ltd, Star entertainment group limited, Spark Infrastructure

group, Northern star resources limited, Evolution mining limited, ALS limited, Ansell

Limited, Downer EDI Limited and Link Administration holding limited (DeFusco et al.

2015).

Dividend history of fund:

Performance of funds

(Source: investsmart.com.au 2018)

The above table depicts the performance of fund ranging from time period of 1 month

to 10 years. Growth of fund during the time period of one month was negative at -1.97 while

that of five years growth stood at 3.09. Highest growth was recorded during six months and

one year. Portfolio of assets incorporated into this particular fund comprises of top ten

holdings namely Iluka resources Ltd, Star entertainment group limited, Spark Infrastructure

group, Northern star resources limited, Evolution mining limited, ALS limited, Ansell

Limited, Downer EDI Limited and Link Administration holding limited (DeFusco et al.

2015).

Dividend history of fund:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5INVESTMENT AND PORTFOLIO MANAGEMENT

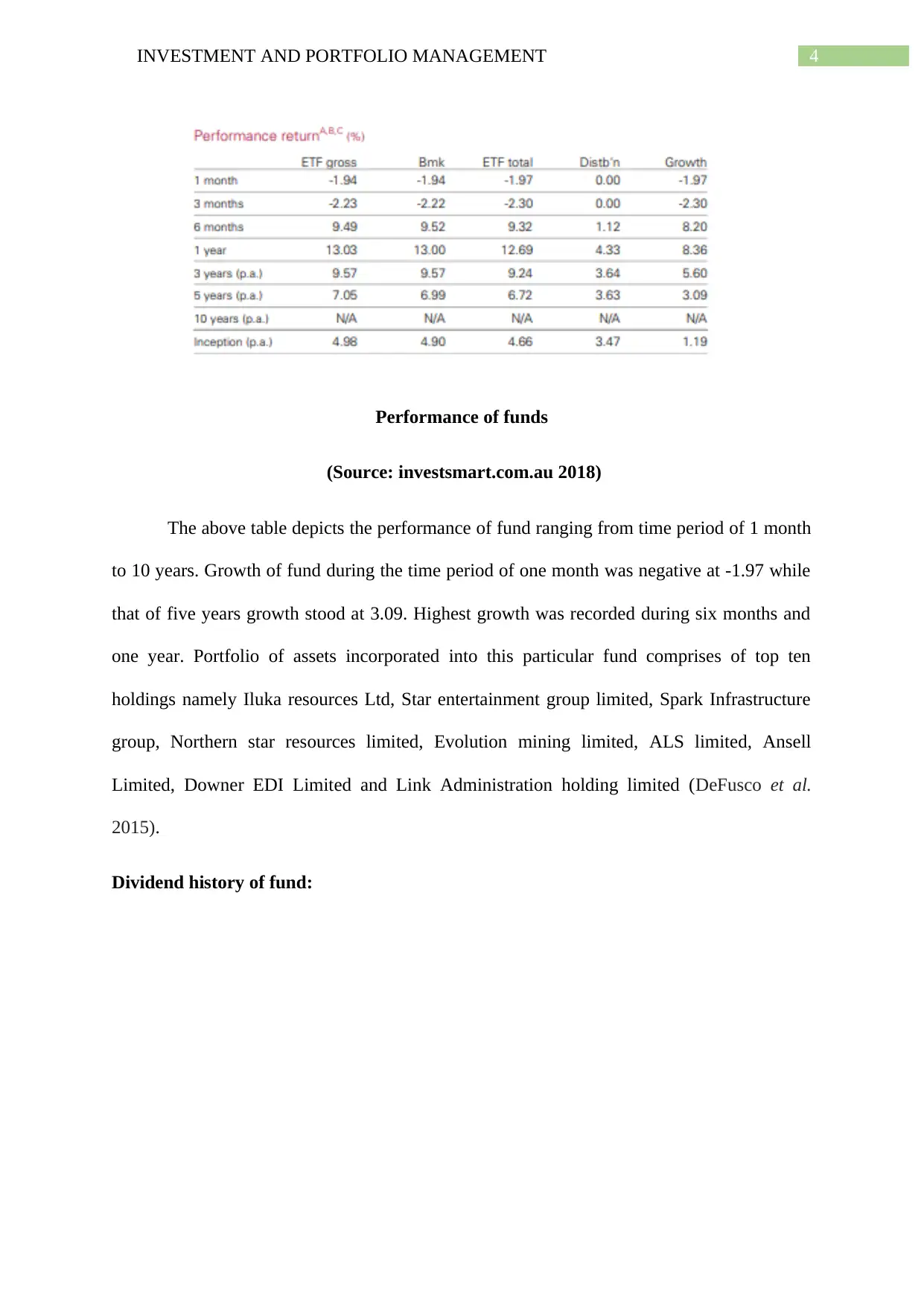

Total amount of dividend

(Source: investsmart.com.au 2018)

The above chart represents the payment of dividend to investors by vanguard fund.

From above chart, it can be seen that total amount of annual dividend paid to investors was

highest in year 2017 at $ 2.17, whereas total amount of franked dividend was highest in year

2016 at $ 0.97. Year 2018 witnessed lowest amount of dividend both in terms of franked

dividend and total dividend at $ 0.57 and $ 0.44.

Answer to question 2.3:

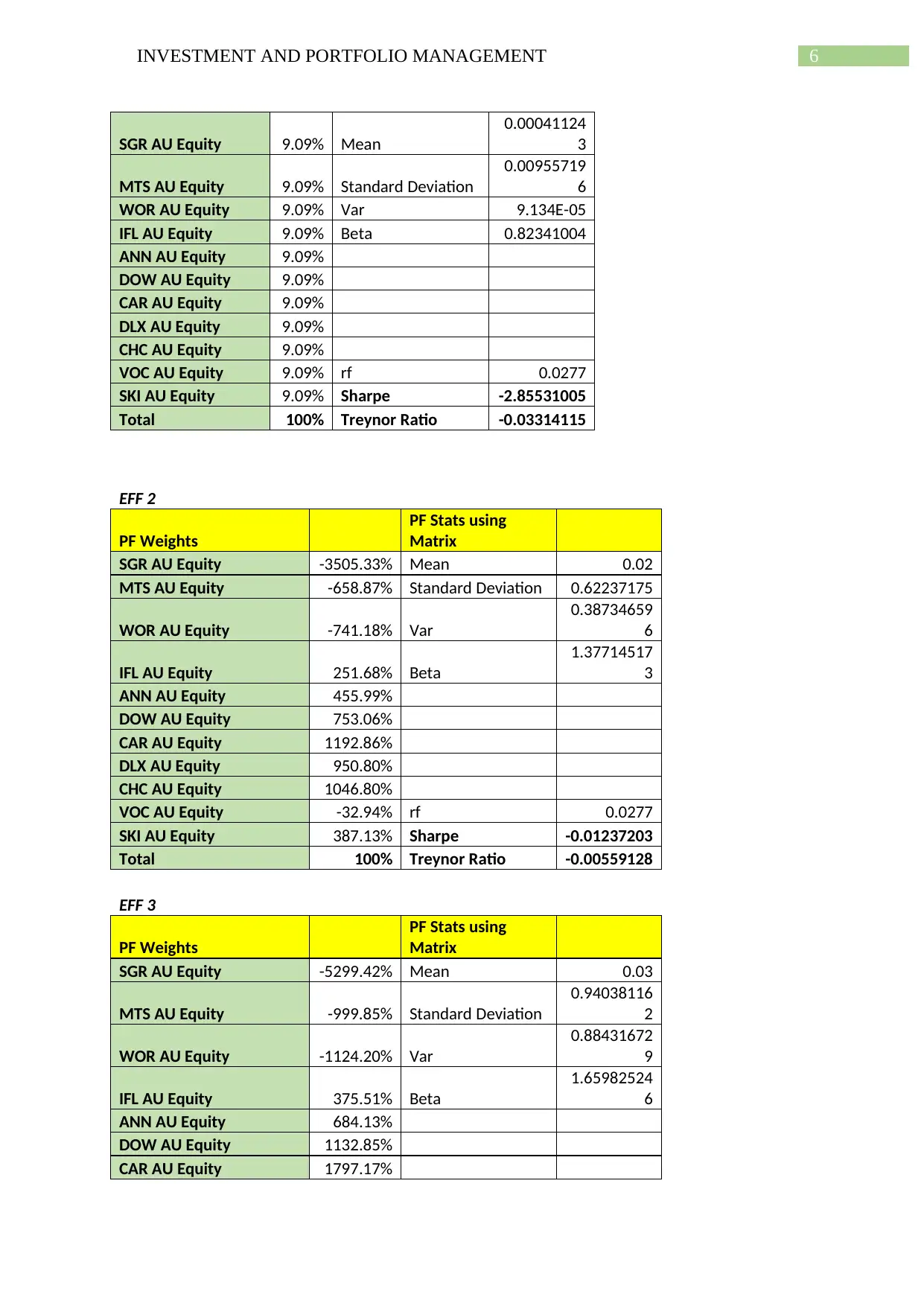

The performance of portfolio of stocks is analyzed using the Sharpe and Teynor ratio.

Equally Weighted Portfolio:

PF Weights

PF Stats using

Matrix

Total amount of dividend

(Source: investsmart.com.au 2018)

The above chart represents the payment of dividend to investors by vanguard fund.

From above chart, it can be seen that total amount of annual dividend paid to investors was

highest in year 2017 at $ 2.17, whereas total amount of franked dividend was highest in year

2016 at $ 0.97. Year 2018 witnessed lowest amount of dividend both in terms of franked

dividend and total dividend at $ 0.57 and $ 0.44.

Answer to question 2.3:

The performance of portfolio of stocks is analyzed using the Sharpe and Teynor ratio.

Equally Weighted Portfolio:

PF Weights

PF Stats using

Matrix

6INVESTMENT AND PORTFOLIO MANAGEMENT

SGR AU Equity 9.09% Mean

0.00041124

3

MTS AU Equity 9.09% Standard Deviation

0.00955719

6

WOR AU Equity 9.09% Var 9.134E-05

IFL AU Equity 9.09% Beta 0.82341004

ANN AU Equity 9.09%

DOW AU Equity 9.09%

CAR AU Equity 9.09%

DLX AU Equity 9.09%

CHC AU Equity 9.09%

VOC AU Equity 9.09% rf 0.0277

SKI AU Equity 9.09% Sharpe -2.85531005

Total 100% Treynor Ratio -0.03314115

EFF 2

PF Weights

PF Stats using

Matrix

SGR AU Equity -3505.33% Mean 0.02

MTS AU Equity -658.87% Standard Deviation 0.62237175

WOR AU Equity -741.18% Var

0.38734659

6

IFL AU Equity 251.68% Beta

1.37714517

3

ANN AU Equity 455.99%

DOW AU Equity 753.06%

CAR AU Equity 1192.86%

DLX AU Equity 950.80%

CHC AU Equity 1046.80%

VOC AU Equity -32.94% rf 0.0277

SKI AU Equity 387.13% Sharpe -0.01237203

Total 100% Treynor Ratio -0.00559128

EFF 3

PF Weights

PF Stats using

Matrix

SGR AU Equity -5299.42% Mean 0.03

MTS AU Equity -999.85% Standard Deviation

0.94038116

2

WOR AU Equity -1124.20% Var

0.88431672

9

IFL AU Equity 375.51% Beta

1.65982524

6

ANN AU Equity 684.13%

DOW AU Equity 1132.85%

CAR AU Equity 1797.17%

SGR AU Equity 9.09% Mean

0.00041124

3

MTS AU Equity 9.09% Standard Deviation

0.00955719

6

WOR AU Equity 9.09% Var 9.134E-05

IFL AU Equity 9.09% Beta 0.82341004

ANN AU Equity 9.09%

DOW AU Equity 9.09%

CAR AU Equity 9.09%

DLX AU Equity 9.09%

CHC AU Equity 9.09%

VOC AU Equity 9.09% rf 0.0277

SKI AU Equity 9.09% Sharpe -2.85531005

Total 100% Treynor Ratio -0.03314115

EFF 2

PF Weights

PF Stats using

Matrix

SGR AU Equity -3505.33% Mean 0.02

MTS AU Equity -658.87% Standard Deviation 0.62237175

WOR AU Equity -741.18% Var

0.38734659

6

IFL AU Equity 251.68% Beta

1.37714517

3

ANN AU Equity 455.99%

DOW AU Equity 753.06%

CAR AU Equity 1192.86%

DLX AU Equity 950.80%

CHC AU Equity 1046.80%

VOC AU Equity -32.94% rf 0.0277

SKI AU Equity 387.13% Sharpe -0.01237203

Total 100% Treynor Ratio -0.00559128

EFF 3

PF Weights

PF Stats using

Matrix

SGR AU Equity -5299.42% Mean 0.03

MTS AU Equity -999.85% Standard Deviation

0.94038116

2

WOR AU Equity -1124.20% Var

0.88431672

9

IFL AU Equity 375.51% Beta

1.65982524

6

ANN AU Equity 684.13%

DOW AU Equity 1132.85%

CAR AU Equity 1797.17%

7INVESTMENT AND PORTFOLIO MANAGEMENT

DLX AU Equity 1431.54%

CHC AU Equity 1576.55%

VOC AU Equity -54.39% rf 0.0277

SKI AU Equity 580.12% Sharpe

0.00244581

7

Total 100% Treynor Ratio

0.00138568

8

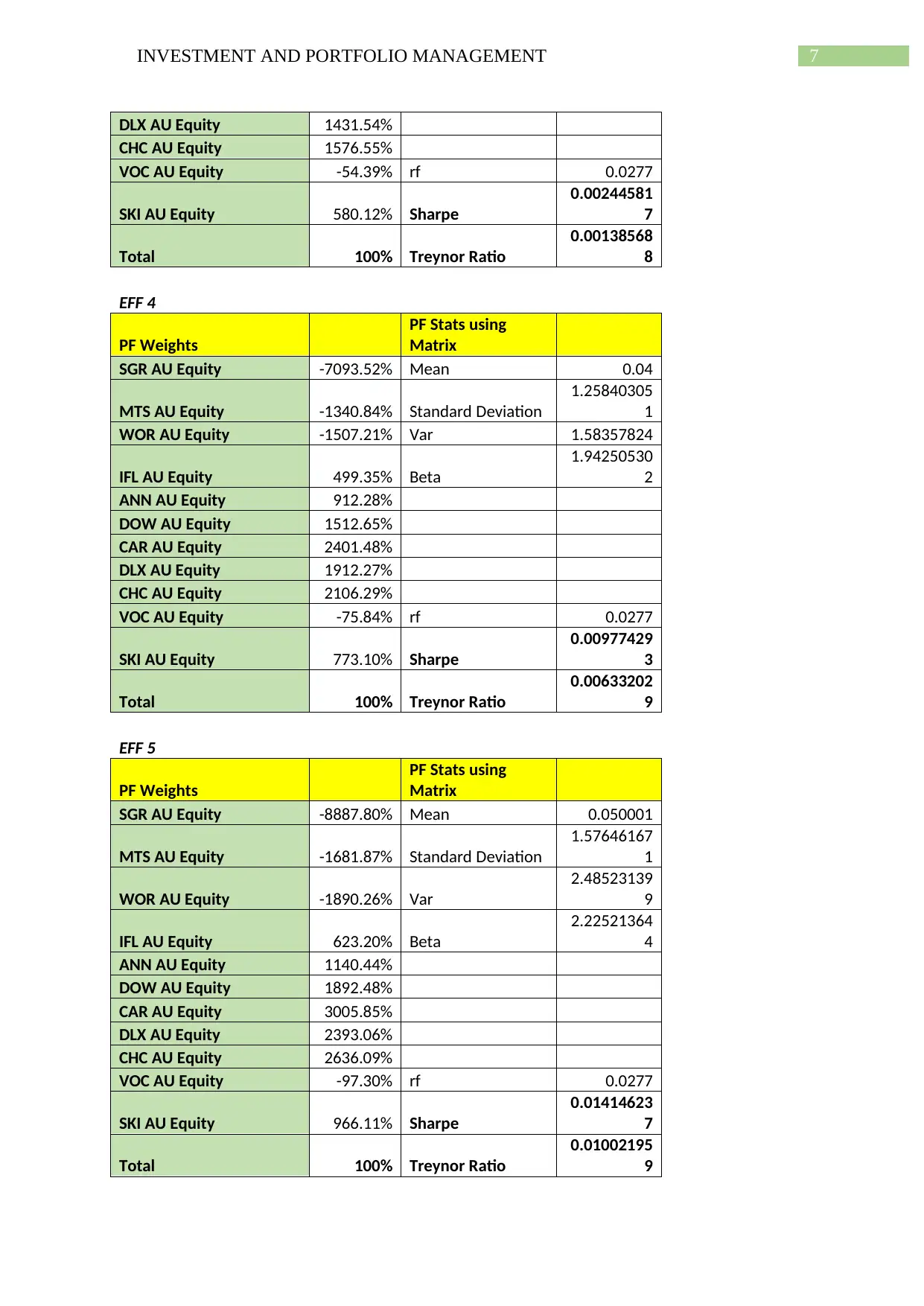

EFF 4

PF Weights

PF Stats using

Matrix

SGR AU Equity -7093.52% Mean 0.04

MTS AU Equity -1340.84% Standard Deviation

1.25840305

1

WOR AU Equity -1507.21% Var 1.58357824

IFL AU Equity 499.35% Beta

1.94250530

2

ANN AU Equity 912.28%

DOW AU Equity 1512.65%

CAR AU Equity 2401.48%

DLX AU Equity 1912.27%

CHC AU Equity 2106.29%

VOC AU Equity -75.84% rf 0.0277

SKI AU Equity 773.10% Sharpe

0.00977429

3

Total 100% Treynor Ratio

0.00633202

9

EFF 5

PF Weights

PF Stats using

Matrix

SGR AU Equity -8887.80% Mean 0.050001

MTS AU Equity -1681.87% Standard Deviation

1.57646167

1

WOR AU Equity -1890.26% Var

2.48523139

9

IFL AU Equity 623.20% Beta

2.22521364

4

ANN AU Equity 1140.44%

DOW AU Equity 1892.48%

CAR AU Equity 3005.85%

DLX AU Equity 2393.06%

CHC AU Equity 2636.09%

VOC AU Equity -97.30% rf 0.0277

SKI AU Equity 966.11% Sharpe

0.01414623

7

Total 100% Treynor Ratio

0.01002195

9

DLX AU Equity 1431.54%

CHC AU Equity 1576.55%

VOC AU Equity -54.39% rf 0.0277

SKI AU Equity 580.12% Sharpe

0.00244581

7

Total 100% Treynor Ratio

0.00138568

8

EFF 4

PF Weights

PF Stats using

Matrix

SGR AU Equity -7093.52% Mean 0.04

MTS AU Equity -1340.84% Standard Deviation

1.25840305

1

WOR AU Equity -1507.21% Var 1.58357824

IFL AU Equity 499.35% Beta

1.94250530

2

ANN AU Equity 912.28%

DOW AU Equity 1512.65%

CAR AU Equity 2401.48%

DLX AU Equity 1912.27%

CHC AU Equity 2106.29%

VOC AU Equity -75.84% rf 0.0277

SKI AU Equity 773.10% Sharpe

0.00977429

3

Total 100% Treynor Ratio

0.00633202

9

EFF 5

PF Weights

PF Stats using

Matrix

SGR AU Equity -8887.80% Mean 0.050001

MTS AU Equity -1681.87% Standard Deviation

1.57646167

1

WOR AU Equity -1890.26% Var

2.48523139

9

IFL AU Equity 623.20% Beta

2.22521364

4

ANN AU Equity 1140.44%

DOW AU Equity 1892.48%

CAR AU Equity 3005.85%

DLX AU Equity 2393.06%

CHC AU Equity 2636.09%

VOC AU Equity -97.30% rf 0.0277

SKI AU Equity 966.11% Sharpe

0.01414623

7

Total 100% Treynor Ratio

0.01002195

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8INVESTMENT AND PORTFOLIO MANAGEMENT

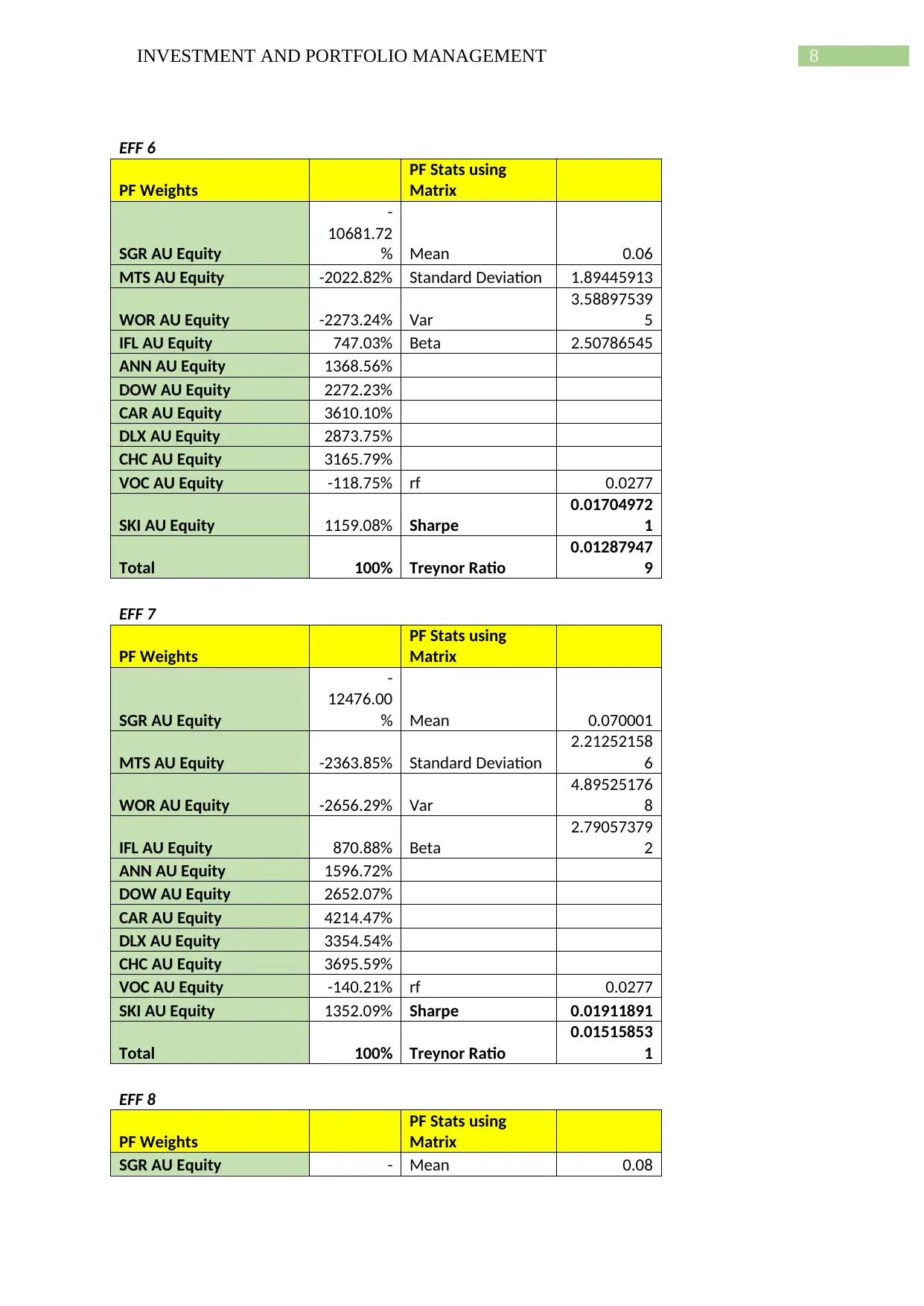

EFF 6

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

10681.72

% Mean 0.06

MTS AU Equity -2022.82% Standard Deviation 1.89445913

WOR AU Equity -2273.24% Var

3.58897539

5

IFL AU Equity 747.03% Beta 2.50786545

ANN AU Equity 1368.56%

DOW AU Equity 2272.23%

CAR AU Equity 3610.10%

DLX AU Equity 2873.75%

CHC AU Equity 3165.79%

VOC AU Equity -118.75% rf 0.0277

SKI AU Equity 1159.08% Sharpe

0.01704972

1

Total 100% Treynor Ratio

0.01287947

9

EFF 7

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

12476.00

% Mean 0.070001

MTS AU Equity -2363.85% Standard Deviation

2.21252158

6

WOR AU Equity -2656.29% Var

4.89525176

8

IFL AU Equity 870.88% Beta

2.79057379

2

ANN AU Equity 1596.72%

DOW AU Equity 2652.07%

CAR AU Equity 4214.47%

DLX AU Equity 3354.54%

CHC AU Equity 3695.59%

VOC AU Equity -140.21% rf 0.0277

SKI AU Equity 1352.09% Sharpe 0.01911891

Total 100% Treynor Ratio

0.01515853

1

EFF 8

PF Weights

PF Stats using

Matrix

SGR AU Equity - Mean 0.08

EFF 6

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

10681.72

% Mean 0.06

MTS AU Equity -2022.82% Standard Deviation 1.89445913

WOR AU Equity -2273.24% Var

3.58897539

5

IFL AU Equity 747.03% Beta 2.50786545

ANN AU Equity 1368.56%

DOW AU Equity 2272.23%

CAR AU Equity 3610.10%

DLX AU Equity 2873.75%

CHC AU Equity 3165.79%

VOC AU Equity -118.75% rf 0.0277

SKI AU Equity 1159.08% Sharpe

0.01704972

1

Total 100% Treynor Ratio

0.01287947

9

EFF 7

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

12476.00

% Mean 0.070001

MTS AU Equity -2363.85% Standard Deviation

2.21252158

6

WOR AU Equity -2656.29% Var

4.89525176

8

IFL AU Equity 870.88% Beta

2.79057379

2

ANN AU Equity 1596.72%

DOW AU Equity 2652.07%

CAR AU Equity 4214.47%

DLX AU Equity 3354.54%

CHC AU Equity 3695.59%

VOC AU Equity -140.21% rf 0.0277

SKI AU Equity 1352.09% Sharpe 0.01911891

Total 100% Treynor Ratio

0.01515853

1

EFF 8

PF Weights

PF Stats using

Matrix

SGR AU Equity - Mean 0.08

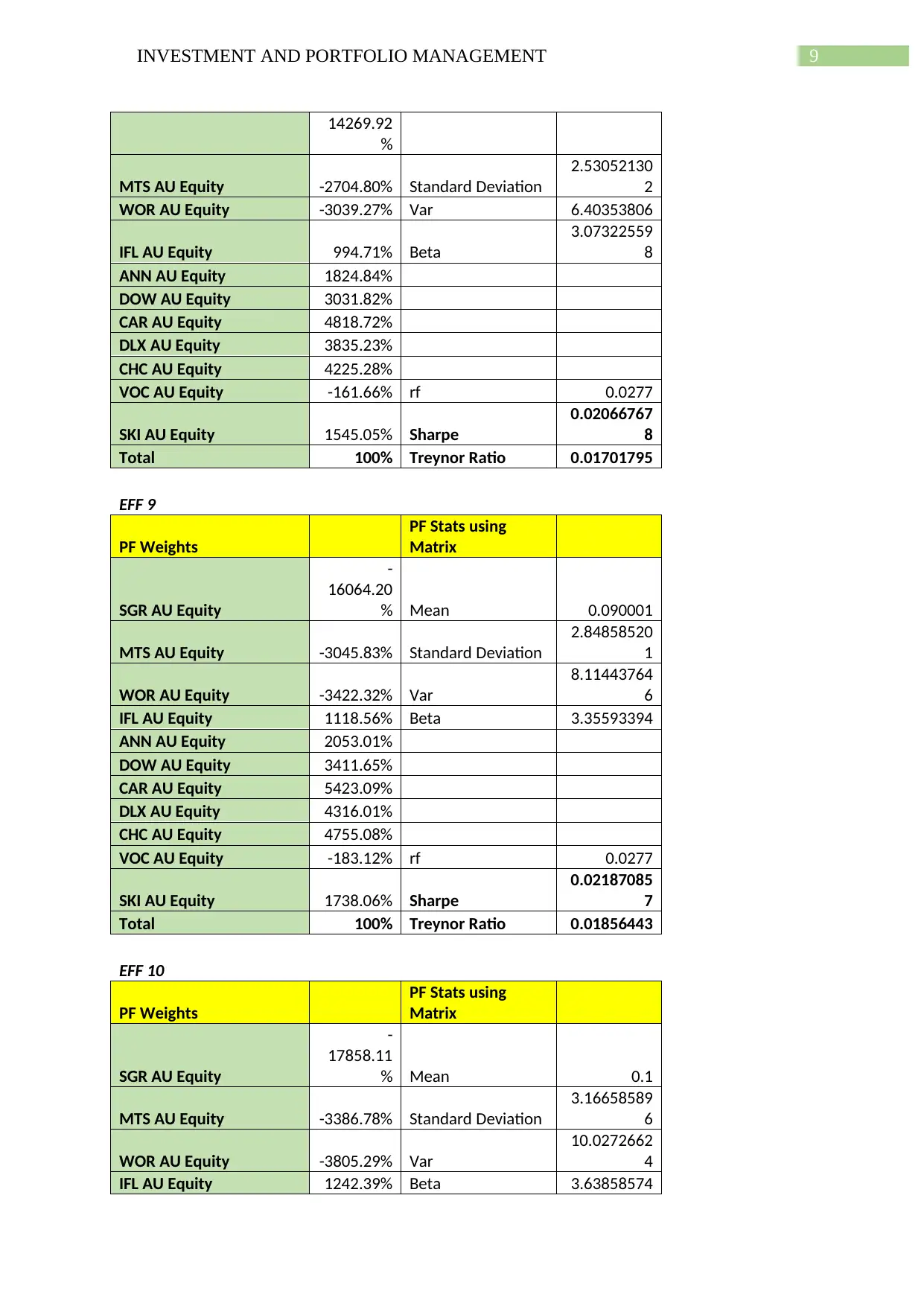

9INVESTMENT AND PORTFOLIO MANAGEMENT

14269.92

%

MTS AU Equity -2704.80% Standard Deviation

2.53052130

2

WOR AU Equity -3039.27% Var 6.40353806

IFL AU Equity 994.71% Beta

3.07322559

8

ANN AU Equity 1824.84%

DOW AU Equity 3031.82%

CAR AU Equity 4818.72%

DLX AU Equity 3835.23%

CHC AU Equity 4225.28%

VOC AU Equity -161.66% rf 0.0277

SKI AU Equity 1545.05% Sharpe

0.02066767

8

Total 100% Treynor Ratio 0.01701795

EFF 9

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

16064.20

% Mean 0.090001

MTS AU Equity -3045.83% Standard Deviation

2.84858520

1

WOR AU Equity -3422.32% Var

8.11443764

6

IFL AU Equity 1118.56% Beta 3.35593394

ANN AU Equity 2053.01%

DOW AU Equity 3411.65%

CAR AU Equity 5423.09%

DLX AU Equity 4316.01%

CHC AU Equity 4755.08%

VOC AU Equity -183.12% rf 0.0277

SKI AU Equity 1738.06% Sharpe

0.02187085

7

Total 100% Treynor Ratio 0.01856443

EFF 10

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

17858.11

% Mean 0.1

MTS AU Equity -3386.78% Standard Deviation

3.16658589

6

WOR AU Equity -3805.29% Var

10.0272662

4

IFL AU Equity 1242.39% Beta 3.63858574

14269.92

%

MTS AU Equity -2704.80% Standard Deviation

2.53052130

2

WOR AU Equity -3039.27% Var 6.40353806

IFL AU Equity 994.71% Beta

3.07322559

8

ANN AU Equity 1824.84%

DOW AU Equity 3031.82%

CAR AU Equity 4818.72%

DLX AU Equity 3835.23%

CHC AU Equity 4225.28%

VOC AU Equity -161.66% rf 0.0277

SKI AU Equity 1545.05% Sharpe

0.02066767

8

Total 100% Treynor Ratio 0.01701795

EFF 9

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

16064.20

% Mean 0.090001

MTS AU Equity -3045.83% Standard Deviation

2.84858520

1

WOR AU Equity -3422.32% Var

8.11443764

6

IFL AU Equity 1118.56% Beta 3.35593394

ANN AU Equity 2053.01%

DOW AU Equity 3411.65%

CAR AU Equity 5423.09%

DLX AU Equity 4316.01%

CHC AU Equity 4755.08%

VOC AU Equity -183.12% rf 0.0277

SKI AU Equity 1738.06% Sharpe

0.02187085

7

Total 100% Treynor Ratio 0.01856443

EFF 10

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

17858.11

% Mean 0.1

MTS AU Equity -3386.78% Standard Deviation

3.16658589

6

WOR AU Equity -3805.29% Var

10.0272662

4

IFL AU Equity 1242.39% Beta 3.63858574

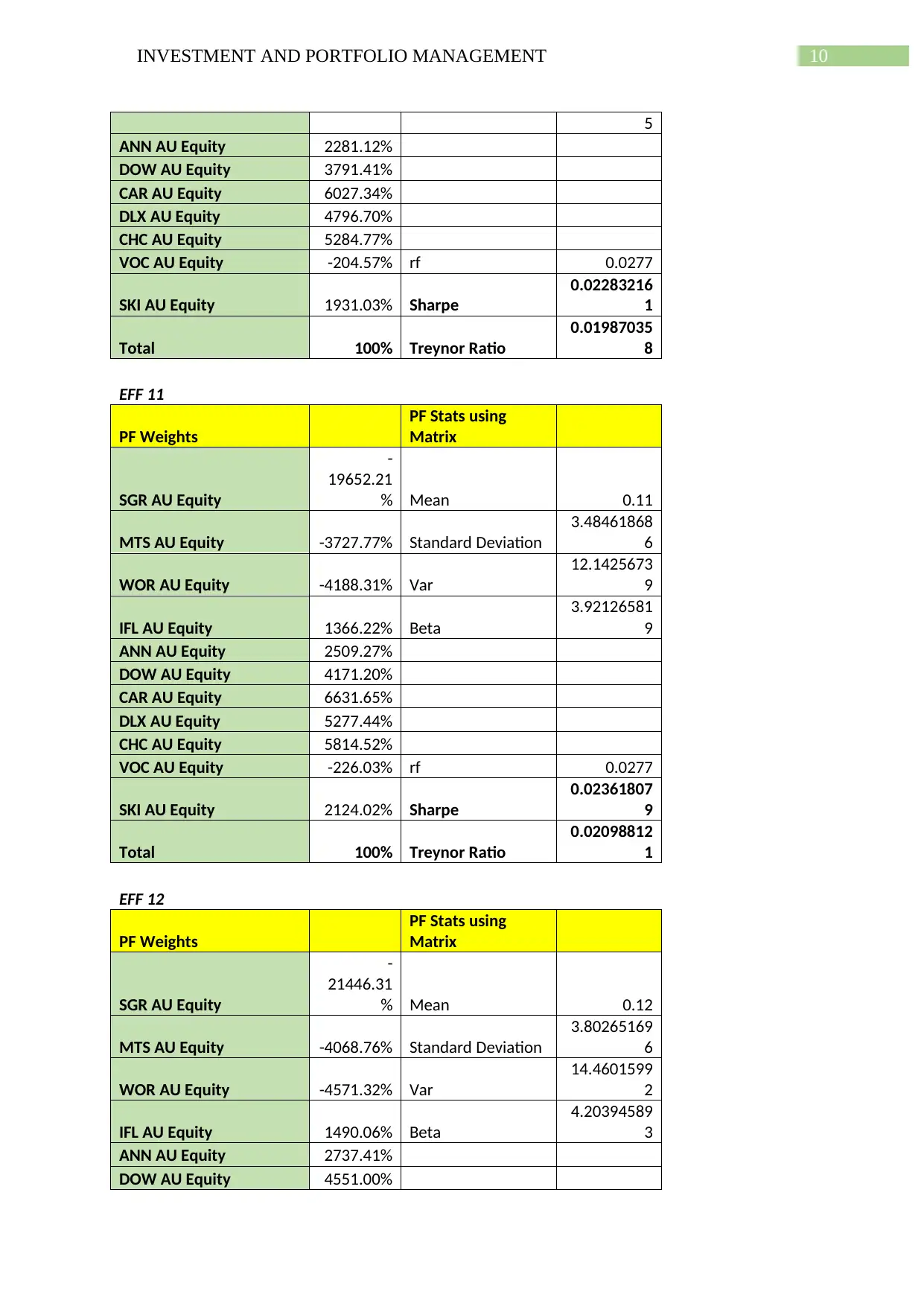

10INVESTMENT AND PORTFOLIO MANAGEMENT

5

ANN AU Equity 2281.12%

DOW AU Equity 3791.41%

CAR AU Equity 6027.34%

DLX AU Equity 4796.70%

CHC AU Equity 5284.77%

VOC AU Equity -204.57% rf 0.0277

SKI AU Equity 1931.03% Sharpe

0.02283216

1

Total 100% Treynor Ratio

0.01987035

8

EFF 11

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

19652.21

% Mean 0.11

MTS AU Equity -3727.77% Standard Deviation

3.48461868

6

WOR AU Equity -4188.31% Var

12.1425673

9

IFL AU Equity 1366.22% Beta

3.92126581

9

ANN AU Equity 2509.27%

DOW AU Equity 4171.20%

CAR AU Equity 6631.65%

DLX AU Equity 5277.44%

CHC AU Equity 5814.52%

VOC AU Equity -226.03% rf 0.0277

SKI AU Equity 2124.02% Sharpe

0.02361807

9

Total 100% Treynor Ratio

0.02098812

1

EFF 12

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

21446.31

% Mean 0.12

MTS AU Equity -4068.76% Standard Deviation

3.80265169

6

WOR AU Equity -4571.32% Var

14.4601599

2

IFL AU Equity 1490.06% Beta

4.20394589

3

ANN AU Equity 2737.41%

DOW AU Equity 4551.00%

5

ANN AU Equity 2281.12%

DOW AU Equity 3791.41%

CAR AU Equity 6027.34%

DLX AU Equity 4796.70%

CHC AU Equity 5284.77%

VOC AU Equity -204.57% rf 0.0277

SKI AU Equity 1931.03% Sharpe

0.02283216

1

Total 100% Treynor Ratio

0.01987035

8

EFF 11

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

19652.21

% Mean 0.11

MTS AU Equity -3727.77% Standard Deviation

3.48461868

6

WOR AU Equity -4188.31% Var

12.1425673

9

IFL AU Equity 1366.22% Beta

3.92126581

9

ANN AU Equity 2509.27%

DOW AU Equity 4171.20%

CAR AU Equity 6631.65%

DLX AU Equity 5277.44%

CHC AU Equity 5814.52%

VOC AU Equity -226.03% rf 0.0277

SKI AU Equity 2124.02% Sharpe

0.02361807

9

Total 100% Treynor Ratio

0.02098812

1

EFF 12

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

21446.31

% Mean 0.12

MTS AU Equity -4068.76% Standard Deviation

3.80265169

6

WOR AU Equity -4571.32% Var

14.4601599

2

IFL AU Equity 1490.06% Beta

4.20394589

3

ANN AU Equity 2737.41%

DOW AU Equity 4551.00%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

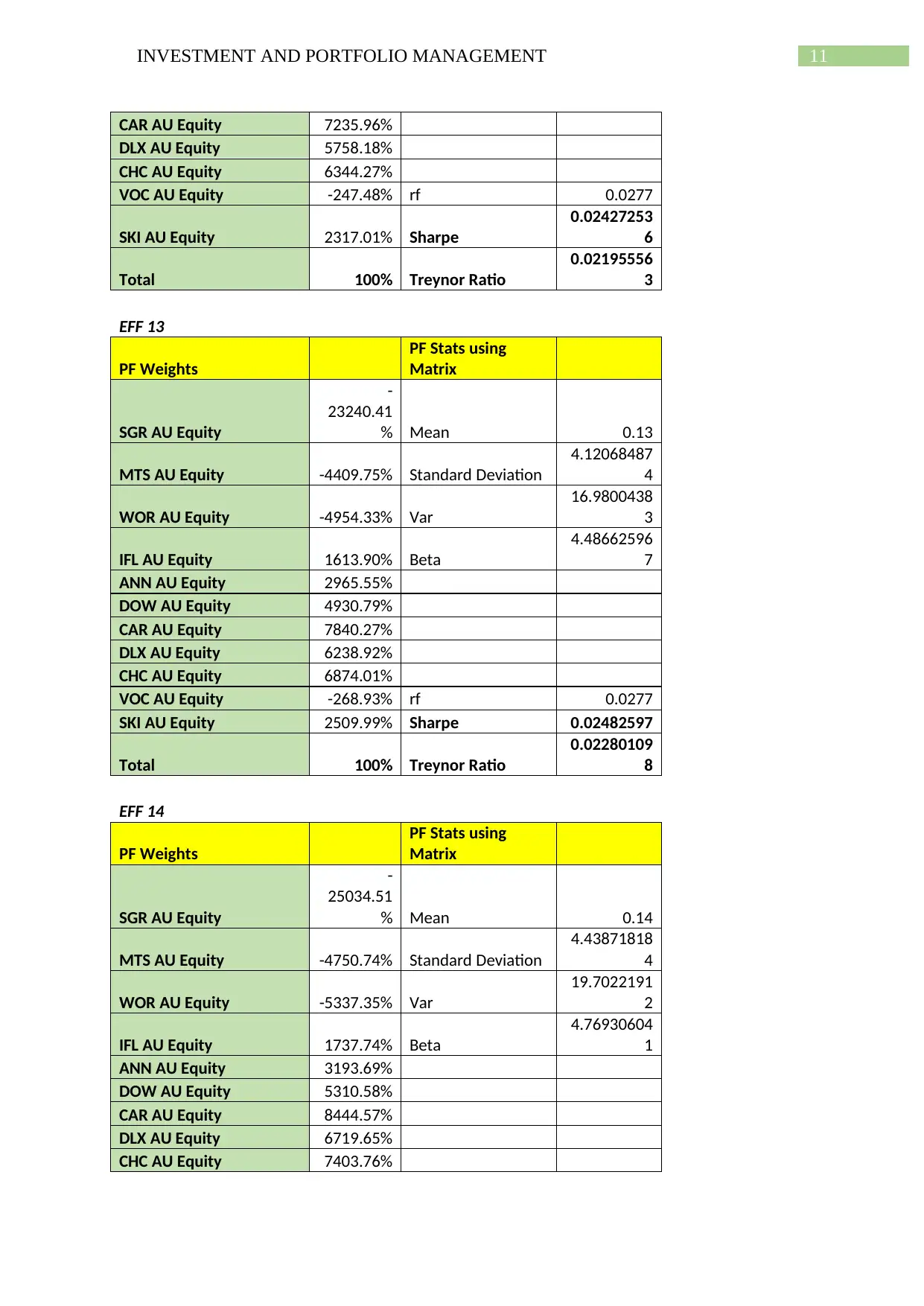

11INVESTMENT AND PORTFOLIO MANAGEMENT

CAR AU Equity 7235.96%

DLX AU Equity 5758.18%

CHC AU Equity 6344.27%

VOC AU Equity -247.48% rf 0.0277

SKI AU Equity 2317.01% Sharpe

0.02427253

6

Total 100% Treynor Ratio

0.02195556

3

EFF 13

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

23240.41

% Mean 0.13

MTS AU Equity -4409.75% Standard Deviation

4.12068487

4

WOR AU Equity -4954.33% Var

16.9800438

3

IFL AU Equity 1613.90% Beta

4.48662596

7

ANN AU Equity 2965.55%

DOW AU Equity 4930.79%

CAR AU Equity 7840.27%

DLX AU Equity 6238.92%

CHC AU Equity 6874.01%

VOC AU Equity -268.93% rf 0.0277

SKI AU Equity 2509.99% Sharpe 0.02482597

Total 100% Treynor Ratio

0.02280109

8

EFF 14

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

25034.51

% Mean 0.14

MTS AU Equity -4750.74% Standard Deviation

4.43871818

4

WOR AU Equity -5337.35% Var

19.7022191

2

IFL AU Equity 1737.74% Beta

4.76930604

1

ANN AU Equity 3193.69%

DOW AU Equity 5310.58%

CAR AU Equity 8444.57%

DLX AU Equity 6719.65%

CHC AU Equity 7403.76%

CAR AU Equity 7235.96%

DLX AU Equity 5758.18%

CHC AU Equity 6344.27%

VOC AU Equity -247.48% rf 0.0277

SKI AU Equity 2317.01% Sharpe

0.02427253

6

Total 100% Treynor Ratio

0.02195556

3

EFF 13

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

23240.41

% Mean 0.13

MTS AU Equity -4409.75% Standard Deviation

4.12068487

4

WOR AU Equity -4954.33% Var

16.9800438

3

IFL AU Equity 1613.90% Beta

4.48662596

7

ANN AU Equity 2965.55%

DOW AU Equity 4930.79%

CAR AU Equity 7840.27%

DLX AU Equity 6238.92%

CHC AU Equity 6874.01%

VOC AU Equity -268.93% rf 0.0277

SKI AU Equity 2509.99% Sharpe 0.02482597

Total 100% Treynor Ratio

0.02280109

8

EFF 14

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

25034.51

% Mean 0.14

MTS AU Equity -4750.74% Standard Deviation

4.43871818

4

WOR AU Equity -5337.35% Var

19.7022191

2

IFL AU Equity 1737.74% Beta

4.76930604

1

ANN AU Equity 3193.69%

DOW AU Equity 5310.58%

CAR AU Equity 8444.57%

DLX AU Equity 6719.65%

CHC AU Equity 7403.76%

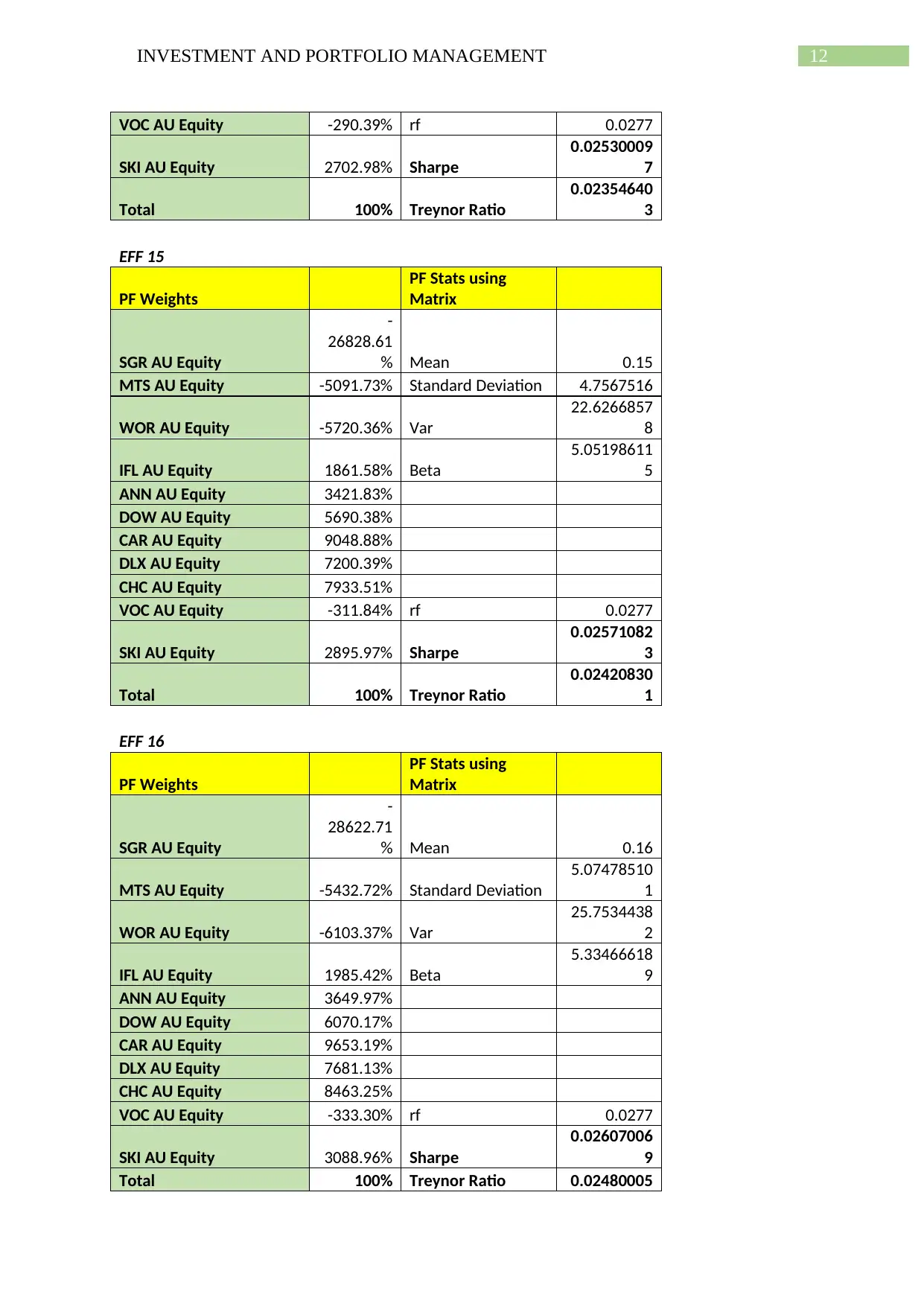

12INVESTMENT AND PORTFOLIO MANAGEMENT

VOC AU Equity -290.39% rf 0.0277

SKI AU Equity 2702.98% Sharpe

0.02530009

7

Total 100% Treynor Ratio

0.02354640

3

EFF 15

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

26828.61

% Mean 0.15

MTS AU Equity -5091.73% Standard Deviation 4.7567516

WOR AU Equity -5720.36% Var

22.6266857

8

IFL AU Equity 1861.58% Beta

5.05198611

5

ANN AU Equity 3421.83%

DOW AU Equity 5690.38%

CAR AU Equity 9048.88%

DLX AU Equity 7200.39%

CHC AU Equity 7933.51%

VOC AU Equity -311.84% rf 0.0277

SKI AU Equity 2895.97% Sharpe

0.02571082

3

Total 100% Treynor Ratio

0.02420830

1

EFF 16

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

28622.71

% Mean 0.16

MTS AU Equity -5432.72% Standard Deviation

5.07478510

1

WOR AU Equity -6103.37% Var

25.7534438

2

IFL AU Equity 1985.42% Beta

5.33466618

9

ANN AU Equity 3649.97%

DOW AU Equity 6070.17%

CAR AU Equity 9653.19%

DLX AU Equity 7681.13%

CHC AU Equity 8463.25%

VOC AU Equity -333.30% rf 0.0277

SKI AU Equity 3088.96% Sharpe

0.02607006

9

Total 100% Treynor Ratio 0.02480005

VOC AU Equity -290.39% rf 0.0277

SKI AU Equity 2702.98% Sharpe

0.02530009

7

Total 100% Treynor Ratio

0.02354640

3

EFF 15

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

26828.61

% Mean 0.15

MTS AU Equity -5091.73% Standard Deviation 4.7567516

WOR AU Equity -5720.36% Var

22.6266857

8

IFL AU Equity 1861.58% Beta

5.05198611

5

ANN AU Equity 3421.83%

DOW AU Equity 5690.38%

CAR AU Equity 9048.88%

DLX AU Equity 7200.39%

CHC AU Equity 7933.51%

VOC AU Equity -311.84% rf 0.0277

SKI AU Equity 2895.97% Sharpe

0.02571082

3

Total 100% Treynor Ratio

0.02420830

1

EFF 16

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

28622.71

% Mean 0.16

MTS AU Equity -5432.72% Standard Deviation

5.07478510

1

WOR AU Equity -6103.37% Var

25.7534438

2

IFL AU Equity 1985.42% Beta

5.33466618

9

ANN AU Equity 3649.97%

DOW AU Equity 6070.17%

CAR AU Equity 9653.19%

DLX AU Equity 7681.13%

CHC AU Equity 8463.25%

VOC AU Equity -333.30% rf 0.0277

SKI AU Equity 3088.96% Sharpe

0.02607006

9

Total 100% Treynor Ratio 0.02480005

13INVESTMENT AND PORTFOLIO MANAGEMENT

2

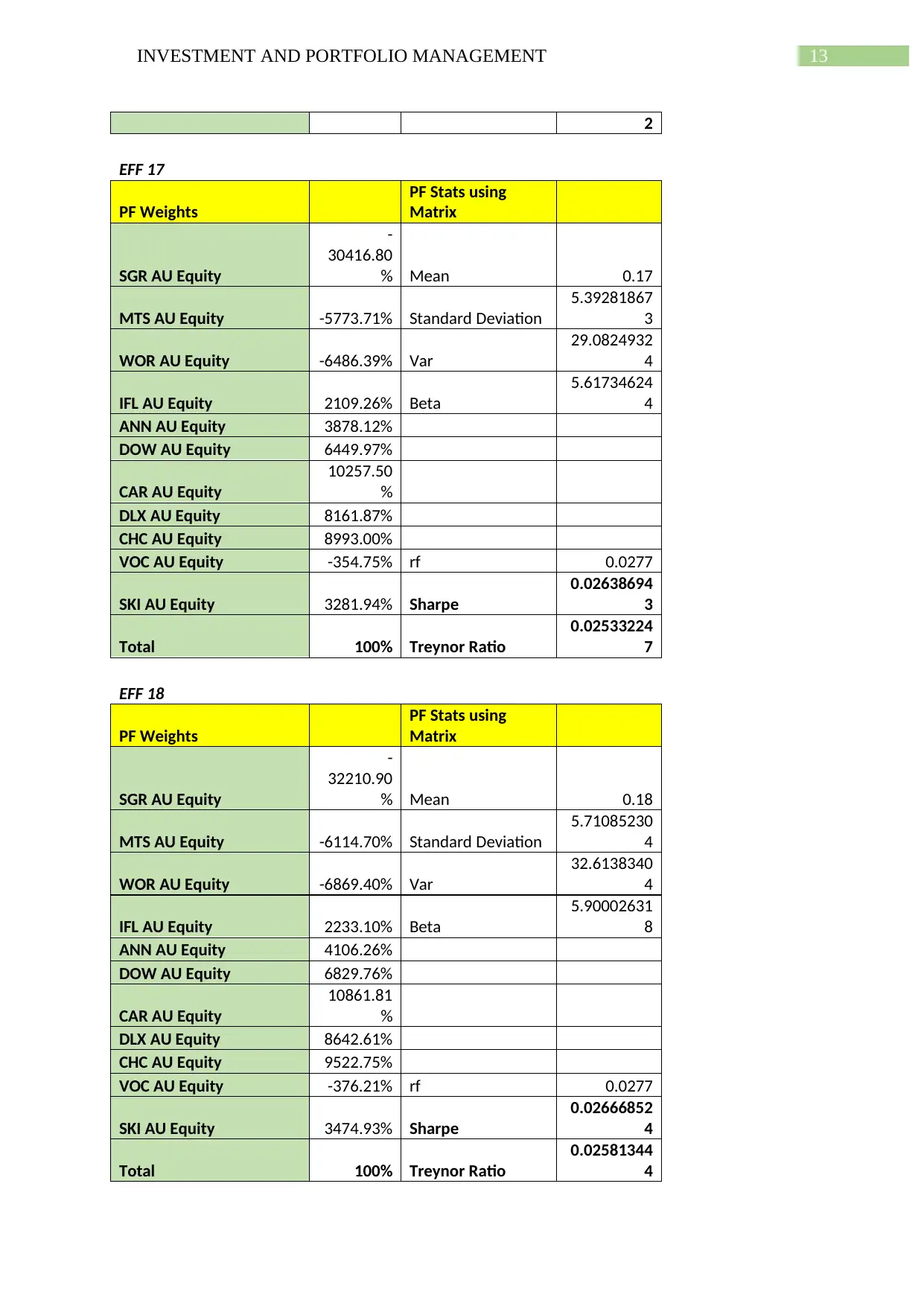

EFF 17

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

30416.80

% Mean 0.17

MTS AU Equity -5773.71% Standard Deviation

5.39281867

3

WOR AU Equity -6486.39% Var

29.0824932

4

IFL AU Equity 2109.26% Beta

5.61734624

4

ANN AU Equity 3878.12%

DOW AU Equity 6449.97%

CAR AU Equity

10257.50

%

DLX AU Equity 8161.87%

CHC AU Equity 8993.00%

VOC AU Equity -354.75% rf 0.0277

SKI AU Equity 3281.94% Sharpe

0.02638694

3

Total 100% Treynor Ratio

0.02533224

7

EFF 18

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

32210.90

% Mean 0.18

MTS AU Equity -6114.70% Standard Deviation

5.71085230

4

WOR AU Equity -6869.40% Var

32.6138340

4

IFL AU Equity 2233.10% Beta

5.90002631

8

ANN AU Equity 4106.26%

DOW AU Equity 6829.76%

CAR AU Equity

10861.81

%

DLX AU Equity 8642.61%

CHC AU Equity 9522.75%

VOC AU Equity -376.21% rf 0.0277

SKI AU Equity 3474.93% Sharpe

0.02666852

4

Total 100% Treynor Ratio

0.02581344

4

2

EFF 17

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

30416.80

% Mean 0.17

MTS AU Equity -5773.71% Standard Deviation

5.39281867

3

WOR AU Equity -6486.39% Var

29.0824932

4

IFL AU Equity 2109.26% Beta

5.61734624

4

ANN AU Equity 3878.12%

DOW AU Equity 6449.97%

CAR AU Equity

10257.50

%

DLX AU Equity 8161.87%

CHC AU Equity 8993.00%

VOC AU Equity -354.75% rf 0.0277

SKI AU Equity 3281.94% Sharpe

0.02638694

3

Total 100% Treynor Ratio

0.02533224

7

EFF 18

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

32210.90

% Mean 0.18

MTS AU Equity -6114.70% Standard Deviation

5.71085230

4

WOR AU Equity -6869.40% Var

32.6138340

4

IFL AU Equity 2233.10% Beta

5.90002631

8

ANN AU Equity 4106.26%

DOW AU Equity 6829.76%

CAR AU Equity

10861.81

%

DLX AU Equity 8642.61%

CHC AU Equity 9522.75%

VOC AU Equity -376.21% rf 0.0277

SKI AU Equity 3474.93% Sharpe

0.02666852

4

Total 100% Treynor Ratio

0.02581344

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14INVESTMENT AND PORTFOLIO MANAGEMENT

EFF 20

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

35799.28

% Mean 0.200001

MTS AU Equity -6796.71% Standard Deviation 6.34695151

WOR AU Equity -7635.46% Var

40.2837934

7

IFL AU Equity 2480.78% Beta

6.46541473

4

ANN AU Equity 4562.56%

DOW AU Equity 7589.38%

CAR AU Equity

12070.49

%

DLX AU Equity 9604.13%

CHC AU Equity

10582.29

%

VOC AU Equity -419.12% rf 0.0277

SKI AU Equity 3860.92% Sharpe

0.02714704

8

Total 100% Treynor Ratio

0.02664964

4

EFF 25

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

44769.59

% Mean 0.25

MTS AU Equity -8501.63% Standard Deviation

7.93708877

3

WOR AU Equity -9550.49% Var

62.9973781

8

IFL AU Equity 3099.97% Beta

7.87878683

5

ANN AU Equity 5703.25%

DOW AU Equity 9488.31%

CAR AU Equity

15091.98

%

DLX AU Equity

12007.77

%

CHC AU Equity

13230.97

%

VOC AU Equity -526.39% rf 0.0277

SKI AU Equity 4825.84% Sharpe 0.02800775

Total 100% Treynor Ratio

0.02821500

4

EFF 20

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

35799.28

% Mean 0.200001

MTS AU Equity -6796.71% Standard Deviation 6.34695151

WOR AU Equity -7635.46% Var

40.2837934

7

IFL AU Equity 2480.78% Beta

6.46541473

4

ANN AU Equity 4562.56%

DOW AU Equity 7589.38%

CAR AU Equity

12070.49

%

DLX AU Equity 9604.13%

CHC AU Equity

10582.29

%

VOC AU Equity -419.12% rf 0.0277

SKI AU Equity 3860.92% Sharpe

0.02714704

8

Total 100% Treynor Ratio

0.02664964

4

EFF 25

PF Weights

PF Stats using

Matrix

SGR AU Equity

-

44769.59

% Mean 0.25

MTS AU Equity -8501.63% Standard Deviation

7.93708877

3

WOR AU Equity -9550.49% Var

62.9973781

8

IFL AU Equity 3099.97% Beta

7.87878683

5

ANN AU Equity 5703.25%

DOW AU Equity 9488.31%

CAR AU Equity

15091.98

%

DLX AU Equity

12007.77

%

CHC AU Equity

13230.97

%

VOC AU Equity -526.39% rf 0.0277

SKI AU Equity 4825.84% Sharpe 0.02800775

Total 100% Treynor Ratio

0.02821500

4

15INVESTMENT AND PORTFOLIO MANAGEMENT

It can be seen from the table that the portfolio of assets have negative Sharpe ratio at -

2.85 that is indicative of the fact that portfolio is generating negative return. Negative value

depicts that investors that there is higher volatility in the market but return is negative.

Treynor ratio is also negative at value -0.03. This negative value depicts that portfolio of

stocks has not generated risk adjusted return. The beta value of portfolio stood at 0.823 and

the standard deviation stood at 0.009. Therefore, the performance of stocks is negative and

investors should not make investment into such portfolio.

Portfolio

Return

Rate

Standard

Deviation Beta

Sharpe

Ratio

Treynor

Ratio

Equally weighted 0.041% 0.01 0.82

-

285.53

% -3.31%

EFF 1 1.000% 0.30 1.09 -5.81% -1.62%

EFF 2 2.000% 0.62 1.38 -1.24% -0.56%

EFF 3 3.000% 0.94 1.66 0.24% 0.14%

EFF 4 4.000% 1.26 1.94 0.98% 0.63%

EFF 5 5.000% 1.58 2.23 1.41% 1.00%

EFF 6 6.000% 1.89 2.51 1.70% 1.29%

EFF 7 7.000% 2.21 2.79 1.91% 1.52%

EFF 8 8.000% 2.53 3.07 2.07% 1.70%

EFF 9 9.000% 2.85 3.36 2.19% 1.86%

EFF 10 10.000% 3.17 3.64 2.28% 1.99%

EFF 11 11.000% 3.48 3.92 2.36% 2.10%

EFF 12 12.000% 3.80 4.20 2.43% 2.20%

EFF 13 13.000% 4.12 4.49 2.48% 2.28%

EFF 14 14.000% 4.44 4.77 2.53% 2.35%

EFF 15 15.000% 4.76 5.05 2.57% 2.42%

EFF 16 16.000% 5.07 5.33 2.61% 2.48%

EFF 17 17.000% 5.39 5.62 2.64% 2.53%

EFF 18 18.000% 5.71 5.90 2.67% 2.58%

EFF 20 20.000% 6.35 6.47 2.71% 2.66%

EFF 25 25.000% 7.94 7.88 2.80% 2.82%

It can be seen from the table that the portfolio of assets have negative Sharpe ratio at -

2.85 that is indicative of the fact that portfolio is generating negative return. Negative value

depicts that investors that there is higher volatility in the market but return is negative.

Treynor ratio is also negative at value -0.03. This negative value depicts that portfolio of

stocks has not generated risk adjusted return. The beta value of portfolio stood at 0.823 and

the standard deviation stood at 0.009. Therefore, the performance of stocks is negative and

investors should not make investment into such portfolio.

Portfolio

Return

Rate

Standard

Deviation Beta

Sharpe

Ratio

Treynor

Ratio

Equally weighted 0.041% 0.01 0.82

-

285.53

% -3.31%

EFF 1 1.000% 0.30 1.09 -5.81% -1.62%

EFF 2 2.000% 0.62 1.38 -1.24% -0.56%

EFF 3 3.000% 0.94 1.66 0.24% 0.14%

EFF 4 4.000% 1.26 1.94 0.98% 0.63%

EFF 5 5.000% 1.58 2.23 1.41% 1.00%

EFF 6 6.000% 1.89 2.51 1.70% 1.29%

EFF 7 7.000% 2.21 2.79 1.91% 1.52%

EFF 8 8.000% 2.53 3.07 2.07% 1.70%

EFF 9 9.000% 2.85 3.36 2.19% 1.86%

EFF 10 10.000% 3.17 3.64 2.28% 1.99%

EFF 11 11.000% 3.48 3.92 2.36% 2.10%

EFF 12 12.000% 3.80 4.20 2.43% 2.20%

EFF 13 13.000% 4.12 4.49 2.48% 2.28%

EFF 14 14.000% 4.44 4.77 2.53% 2.35%

EFF 15 15.000% 4.76 5.05 2.57% 2.42%

EFF 16 16.000% 5.07 5.33 2.61% 2.48%

EFF 17 17.000% 5.39 5.62 2.64% 2.53%

EFF 18 18.000% 5.71 5.90 2.67% 2.58%

EFF 20 20.000% 6.35 6.47 2.71% 2.66%

EFF 25 25.000% 7.94 7.88 2.80% 2.82%

16INVESTMENT AND PORTFOLIO MANAGEMENT

The efficient portfolio is constructed by using different target returns for the eleven

stocks that have formed the portfolio. For target return of 1%, value of both Sharpe as well as

Treynor ratio stood at negative at -0.05 and -0.01. For target return of 2%, Sharpe ratio and

Treynor ratio stood at -0.012 and -0.005. For these two levels of target returns, return of the

stocks of portfolio is negative depicting that making investment in portfolio of these stocks is

risky.

When considering the target return of 3%, 4%, 5%, 6%, 7%, 8%, 9%, 10%, 11%,

12%, 13%, 14%, 15%, 16%, 17%, 18%, 20% and 25%, the value of Sharpe and Treynor ratio

has come to positive indicating that stocks will be generating positive return and higher the

value of ratios depicts that returns from the stocks will be return adjusted (Schyns 2016). It

can be seen that when the percentage of target return is increasing, then the value of Sharpe

as well as Treynor ratio is also increasing.

The following table depicts the comparison between Treynor ratio and Sharpe ratio in

the construction of efficient frontier for different level of target returns.

For the returns that are equally weighted, the return generated using Sharpe ratio

stood at -285.53% and that of Treynor ratio stood at -3.31%. For the target level of return that

is lower, it can be seen that value of both the ratio is negative indicating that returns are not

adjusted for risks and stocks are generating negative return. With the increase in level of

target return, the returns generated by the portfolio of stocks are increasing. Furthermore, it

can also be seen that the value of Sharpe ratio for every level of target return is more than

Treynor ratio. However, for the target return at 25%, it can be seen that value of Sharpe ratio

is more than that of Treynor ratio. In addition to this, there is increasing deviation from

average return of the portfolio of stocks when there is increase in target return. Therefore, the

deviation from mean value increases when there is increase in set target value.

The efficient portfolio is constructed by using different target returns for the eleven

stocks that have formed the portfolio. For target return of 1%, value of both Sharpe as well as

Treynor ratio stood at negative at -0.05 and -0.01. For target return of 2%, Sharpe ratio and

Treynor ratio stood at -0.012 and -0.005. For these two levels of target returns, return of the

stocks of portfolio is negative depicting that making investment in portfolio of these stocks is

risky.

When considering the target return of 3%, 4%, 5%, 6%, 7%, 8%, 9%, 10%, 11%,

12%, 13%, 14%, 15%, 16%, 17%, 18%, 20% and 25%, the value of Sharpe and Treynor ratio

has come to positive indicating that stocks will be generating positive return and higher the

value of ratios depicts that returns from the stocks will be return adjusted (Schyns 2016). It

can be seen that when the percentage of target return is increasing, then the value of Sharpe

as well as Treynor ratio is also increasing.

The following table depicts the comparison between Treynor ratio and Sharpe ratio in

the construction of efficient frontier for different level of target returns.

For the returns that are equally weighted, the return generated using Sharpe ratio

stood at -285.53% and that of Treynor ratio stood at -3.31%. For the target level of return that

is lower, it can be seen that value of both the ratio is negative indicating that returns are not

adjusted for risks and stocks are generating negative return. With the increase in level of

target return, the returns generated by the portfolio of stocks are increasing. Furthermore, it

can also be seen that the value of Sharpe ratio for every level of target return is more than

Treynor ratio. However, for the target return at 25%, it can be seen that value of Sharpe ratio

is more than that of Treynor ratio. In addition to this, there is increasing deviation from

average return of the portfolio of stocks when there is increase in target return. Therefore, the

deviation from mean value increases when there is increase in set target value.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17INVESTMENT AND PORTFOLIO MANAGEMENT

When looking the performance of portfolio using Sharpe ratio as performance

measure, it can be seen that the return of stocks is negative at the target return of 1% and 2%.

Using Teynor ratio as the performance measure, the return of stocks is negative for the target

return of 1% and 2%. On other hand, for all the other target returns that have been set, the

performance of portfolio is favourable as depicted from both the performance measures.

References list:

Cornell, B., Hsu, J. and Nanigian, D., 2017. Does Past Performance Matter in Investment

Manager Selection?. The Journal of Portfolio Management, 43(4), pp.33-43.

Cosio, R.M., Estrada, J. and Kritzman, M., 2015. New Frontiers in Portfolio Management.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

InvestSMART. (2018). Vanguard MSCI Australian Small Companies Index ETF. [online]

Available at: https://www.investsmart.com.au/shares/asx-vso/vanguard-msci-australian-

small-companies-index-etf [Accessed 10 May 2018].

Kahn, R.N. and Lemmon, M., 2016. The asset manager’s dilemma: How smart beta is

disrupting the investment management industry. Financial Analysts Journal, 72(1), pp.15-20.

Kaiser, M.G., El Arbi, F. and Ahlemann, F., 2015. Successful project portfolio management

beyond project selection techniques: Understanding the role of structural

alignment. International Journal of Project Management, 33(1), pp.126-139.

Kevin, S., 2015. Security analysis and portfolio management. PHI Learning Pvt. Ltd..

When looking the performance of portfolio using Sharpe ratio as performance

measure, it can be seen that the return of stocks is negative at the target return of 1% and 2%.

Using Teynor ratio as the performance measure, the return of stocks is negative for the target

return of 1% and 2%. On other hand, for all the other target returns that have been set, the

performance of portfolio is favourable as depicted from both the performance measures.

References list:

Cornell, B., Hsu, J. and Nanigian, D., 2017. Does Past Performance Matter in Investment

Manager Selection?. The Journal of Portfolio Management, 43(4), pp.33-43.

Cosio, R.M., Estrada, J. and Kritzman, M., 2015. New Frontiers in Portfolio Management.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

InvestSMART. (2018). Vanguard MSCI Australian Small Companies Index ETF. [online]

Available at: https://www.investsmart.com.au/shares/asx-vso/vanguard-msci-australian-

small-companies-index-etf [Accessed 10 May 2018].

Kahn, R.N. and Lemmon, M., 2016. The asset manager’s dilemma: How smart beta is

disrupting the investment management industry. Financial Analysts Journal, 72(1), pp.15-20.

Kaiser, M.G., El Arbi, F. and Ahlemann, F., 2015. Successful project portfolio management

beyond project selection techniques: Understanding the role of structural

alignment. International Journal of Project Management, 33(1), pp.126-139.

Kevin, S., 2015. Security analysis and portfolio management. PHI Learning Pvt. Ltd..

18INVESTMENT AND PORTFOLIO MANAGEMENT

Klingebiel, R. and Rammer, C., 2014. Resource allocation strategy for innovation portfolio

management. Strategic Management Journal, 35(2), pp.246-268.

Lashley, G., Parker, G., Singh, S., Wise, J. and Polwitoon, P., 2017. Managing Your

Investment Portfolio: All Things ETF.

Schyns, P.F.M., 2016. The technological future of the wealth management industry for

portfolio management investment services (Bachelor's thesis, University of Twente).

Stettina, C.J. and Hörz, J., 2015. Agile portfolio management: An empirical perspective on

the practice in use. International Journal of Project Management, 33(1), pp.140-152.

Vincent, K., Hsu, Y.C. and Lin, H.W., 2018. Analyzing the Performance of Multifactor

Investment Strategies under a Multiple Testing Framework. The Journal of Portfolio

Management, 44(4), pp.113-126.

Klingebiel, R. and Rammer, C., 2014. Resource allocation strategy for innovation portfolio

management. Strategic Management Journal, 35(2), pp.246-268.

Lashley, G., Parker, G., Singh, S., Wise, J. and Polwitoon, P., 2017. Managing Your

Investment Portfolio: All Things ETF.

Schyns, P.F.M., 2016. The technological future of the wealth management industry for

portfolio management investment services (Bachelor's thesis, University of Twente).

Stettina, C.J. and Hörz, J., 2015. Agile portfolio management: An empirical perspective on

the practice in use. International Journal of Project Management, 33(1), pp.140-152.

Vincent, K., Hsu, Y.C. and Lin, H.W., 2018. Analyzing the Performance of Multifactor

Investment Strategies under a Multiple Testing Framework. The Journal of Portfolio

Management, 44(4), pp.113-126.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.