University Portfolio Construction and Performance Analysis Report

VerifiedAdded on 2020/07/23

|15

|3787

|63

Report

AI Summary

This report presents a detailed analysis of a constructed investment portfolio, focusing on the selection of companies within the healthcare, aviation, and media sectors. The report outlines the rationale behind company choices, considering factors like PE ratios, EPS, and growth rates. Asset allocation strategies, including the use of equity and debt, are discussed, along with the selection of the FTSE 100 unit trust as a benchmark. The performance of the portfolio is evaluated, highlighting the impact of market events such as BREXIT on investment returns. Finally, the report critically assesses the portfolio's performance using the Trenyor ratio, comparing its risk-adjusted return to that of the benchmark, and concluding with an evaluation of passive and active management strategies in business. The report provides a comprehensive overview of portfolio construction, performance analysis, and investment strategies, offering valuable insights into financial management.

INVESTMENT AND PORTFOLIO

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

(A)Selection of companies..........................................................................................................1

(b)Asset allocation by using judgement and theories..................................................................3

© Selection of benchmark index in order to evaluate firm performance....................................3

Part 2................................................................................................................................................4

Performance of portfolio and reason for change in return...........................................................4

Part 3................................................................................................................................................4

Critical evaluation of performance of portfolio by using Trenyor ratio......................................4

Part 4................................................................................................................................................5

Passive and active management strategy in business..................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

Table 1Selection of companies on basis of parameters...................................................................3

Table 2Trenyor ratio performnance.................................................................................................6

Table 3Classification of corpus.....................................................................................................10

Table 4Allocation details...............................................................................................................10

Table 5First week investment........................................................................................................10

Table 6Second week investment...................................................................................................11

Table 7Third portfolio...................................................................................................................11

Table 8Fourth portfolio..................................................................................................................12

Table 9Net return gained on portfolio...........................................................................................13

Table 10Benchmark return and portfolio return............................................................................13

Table 11Portfolio comparison.......................................................................................................13

1 | P a g e

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

(A)Selection of companies..........................................................................................................1

(b)Asset allocation by using judgement and theories..................................................................3

© Selection of benchmark index in order to evaluate firm performance....................................3

Part 2................................................................................................................................................4

Performance of portfolio and reason for change in return...........................................................4

Part 3................................................................................................................................................4

Critical evaluation of performance of portfolio by using Trenyor ratio......................................4

Part 4................................................................................................................................................5

Passive and active management strategy in business..................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

Table 1Selection of companies on basis of parameters...................................................................3

Table 2Trenyor ratio performnance.................................................................................................6

Table 3Classification of corpus.....................................................................................................10

Table 4Allocation details...............................................................................................................10

Table 5First week investment........................................................................................................10

Table 6Second week investment...................................................................................................11

Table 7Third portfolio...................................................................................................................11

Table 8Fourth portfolio..................................................................................................................12

Table 9Net return gained on portfolio...........................................................................................13

Table 10Benchmark return and portfolio return............................................................................13

Table 11Portfolio comparison.......................................................................................................13

1 | P a g e

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

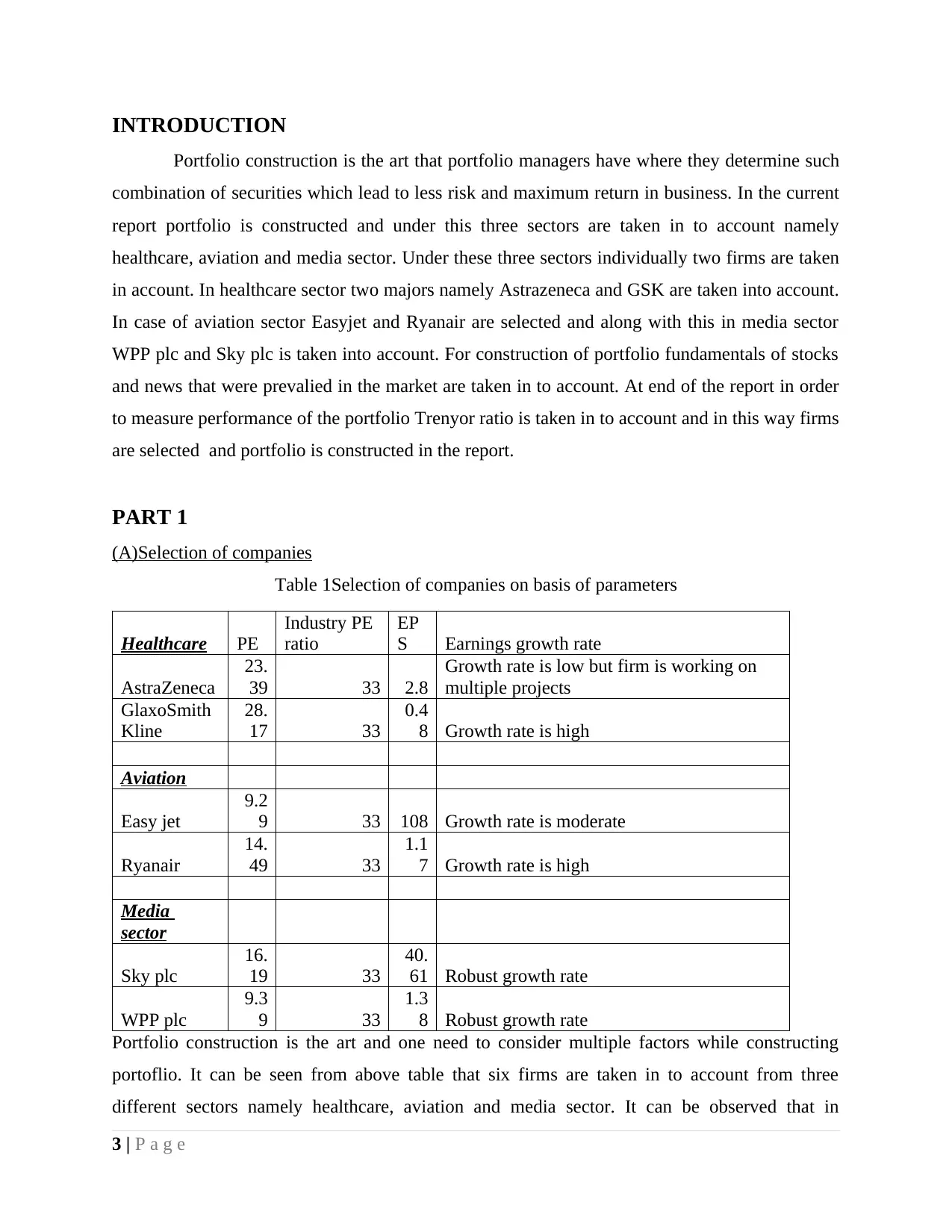

INTRODUCTION

Portfolio construction is the art that portfolio managers have where they determine such

combination of securities which lead to less risk and maximum return in business. In the current

report portfolio is constructed and under this three sectors are taken in to account namely

healthcare, aviation and media sector. Under these three sectors individually two firms are taken

in account. In healthcare sector two majors namely Astrazeneca and GSK are taken into account.

In case of aviation sector Easyjet and Ryanair are selected and along with this in media sector

WPP plc and Sky plc is taken into account. For construction of portfolio fundamentals of stocks

and news that were prevalied in the market are taken in to account. At end of the report in order

to measure performance of the portfolio Trenyor ratio is taken in to account and in this way firms

are selected and portfolio is constructed in the report.

PART 1

(A)Selection of companies

Table 1Selection of companies on basis of parameters

Healthcare PE

Industry PE

ratio

EP

S Earnings growth rate

AstraZeneca

23.

39 33 2.8

Growth rate is low but firm is working on

multiple projects

GlaxoSmith

Kline

28.

17 33

0.4

8 Growth rate is high

Aviation

Easy jet

9.2

9 33 108 Growth rate is moderate

Ryanair

14.

49 33

1.1

7 Growth rate is high

Media

sector

Sky plc

16.

19 33

40.

61 Robust growth rate

WPP plc

9.3

9 33

1.3

8 Robust growth rate

Portfolio construction is the art and one need to consider multiple factors while constructing

portoflio. It can be seen from above table that six firms are taken in to account from three

different sectors namely healthcare, aviation and media sector. It can be observed that in

3 | P a g e

Portfolio construction is the art that portfolio managers have where they determine such

combination of securities which lead to less risk and maximum return in business. In the current

report portfolio is constructed and under this three sectors are taken in to account namely

healthcare, aviation and media sector. Under these three sectors individually two firms are taken

in account. In healthcare sector two majors namely Astrazeneca and GSK are taken into account.

In case of aviation sector Easyjet and Ryanair are selected and along with this in media sector

WPP plc and Sky plc is taken into account. For construction of portfolio fundamentals of stocks

and news that were prevalied in the market are taken in to account. At end of the report in order

to measure performance of the portfolio Trenyor ratio is taken in to account and in this way firms

are selected and portfolio is constructed in the report.

PART 1

(A)Selection of companies

Table 1Selection of companies on basis of parameters

Healthcare PE

Industry PE

ratio

EP

S Earnings growth rate

AstraZeneca

23.

39 33 2.8

Growth rate is low but firm is working on

multiple projects

GlaxoSmith

Kline

28.

17 33

0.4

8 Growth rate is high

Aviation

Easy jet

9.2

9 33 108 Growth rate is moderate

Ryanair

14.

49 33

1.1

7 Growth rate is high

Media

sector

Sky plc

16.

19 33

40.

61 Robust growth rate

WPP plc

9.3

9 33

1.3

8 Robust growth rate

Portfolio construction is the art and one need to consider multiple factors while constructing

portoflio. It can be seen from above table that six firms are taken in to account from three

different sectors namely healthcare, aviation and media sector. It can be observed that in

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

healthcare sector there are two firms that are taken in to account namely AstraZeneca and

Glaxosmithklin. Apart from this, in other industry like aviation industry two firms that are

selected is Easyjet and Ryanair. In media sector firms take are Sky plc and WPP plc. These three

sectors are taken in to account because of several reasons. Healthcare sector is one of fastest

growing domain across the world. In single tim relevant firms carry out multiple projects and

with cancelation of patent of any drug firms launch generic drug in market and earn good amount

of profit. Thus, there is scope of earning of good amount of profit in the business (Bodie, 2013).

Hence, healthcare sector is taken in to account. AstraZeneca is one of pharma firm that is taken

into account. Currently, firm is earning less profit in its business but it is expected that in near

time its stocks may generate good return because firm is carrying on multiple project in respect

to development of generic drugs (Astrazeneca plc, 2017). Filling for some of drug in done in

USFDA by considering nearby expiry of patents of few of medicines. Hence, in future good

return can be generated by firm stocks. Glaxosmithkline is another firm that is taken in to

account because it is one of the fastest growing firm across the globe and currently performing

well in the market (GlaxoSmithKline plc, 2017). There is positive sentiments about firm in the

market among investors and due to this reason it is expected that good amount of return will be

generated by the business firm.

Aviation sector is also growing in UK as toruism in category of business, students and

other increased at fast rate in past couple of years. On this basis it is estimaetd that good amount

of return can be generated by firms operating in this sector. In case of aviation sector there are

two firms namely Easyjet and Ryanair. Easyjet is the low cost airline company in UK and it is

giving stiff competition to firms like British Airways. Currently, firm is looking for expanding its

operations on new routes and improving operations internally (Easyjet plc, 2017). Thus, it can be

said that Easyjet is the one of the best choice as its PE ratio is below market and EPS is perfect.

Ryanair is another firm that is selected as it is currently focusing on its fleet capability in terms

of enhancement in its size (Xidonas, Mavrotas and Psarras, 2010). Firm will expand its business

operations in upcoming time period. PE ratio of firm is 14.49 which is less then market PE ratio

which is 33 and on this basis it can be said that firm shares are undervalued and there is scope for

growth in firm shares (Ryanair Holdings plc, 2017).

Media sector is another domain that is increasing at fast pace and people are looking for

more and more entertainment so that stress level can be reduced to great extent. PE ratio in case

4 | P a g e

Glaxosmithklin. Apart from this, in other industry like aviation industry two firms that are

selected is Easyjet and Ryanair. In media sector firms take are Sky plc and WPP plc. These three

sectors are taken in to account because of several reasons. Healthcare sector is one of fastest

growing domain across the world. In single tim relevant firms carry out multiple projects and

with cancelation of patent of any drug firms launch generic drug in market and earn good amount

of profit. Thus, there is scope of earning of good amount of profit in the business (Bodie, 2013).

Hence, healthcare sector is taken in to account. AstraZeneca is one of pharma firm that is taken

into account. Currently, firm is earning less profit in its business but it is expected that in near

time its stocks may generate good return because firm is carrying on multiple project in respect

to development of generic drugs (Astrazeneca plc, 2017). Filling for some of drug in done in

USFDA by considering nearby expiry of patents of few of medicines. Hence, in future good

return can be generated by firm stocks. Glaxosmithkline is another firm that is taken in to

account because it is one of the fastest growing firm across the globe and currently performing

well in the market (GlaxoSmithKline plc, 2017). There is positive sentiments about firm in the

market among investors and due to this reason it is expected that good amount of return will be

generated by the business firm.

Aviation sector is also growing in UK as toruism in category of business, students and

other increased at fast rate in past couple of years. On this basis it is estimaetd that good amount

of return can be generated by firms operating in this sector. In case of aviation sector there are

two firms namely Easyjet and Ryanair. Easyjet is the low cost airline company in UK and it is

giving stiff competition to firms like British Airways. Currently, firm is looking for expanding its

operations on new routes and improving operations internally (Easyjet plc, 2017). Thus, it can be

said that Easyjet is the one of the best choice as its PE ratio is below market and EPS is perfect.

Ryanair is another firm that is selected as it is currently focusing on its fleet capability in terms

of enhancement in its size (Xidonas, Mavrotas and Psarras, 2010). Firm will expand its business

operations in upcoming time period. PE ratio of firm is 14.49 which is less then market PE ratio

which is 33 and on this basis it can be said that firm shares are undervalued and there is scope for

growth in firm shares (Ryanair Holdings plc, 2017).

Media sector is another domain that is increasing at fast pace and people are looking for

more and more entertainment so that stress level can be reduced to great extent. PE ratio in case

4 | P a g e

of firm Sky plc is 16.19 which is less then market and this means shares are undervalued. Sky plc

genrated huge amount of revenue in its business and sales growth rate is quite high which make

firm performance impressive (Sky plc, 2017). On this basis it can be said that good choice is

made for portfolio construction. Apart from this, other company taken in to account is WPP plc

which is one of the fastest growing company in UK. Firm is currently innovating its business

operations and this technology innovation may boost firm sales in upcoming time period. By

considering this factor business firm is selected in portfolio (WPP plc, 2017). PE ratio of WPP

plc is 9.39 and same of industry is 33. This means firm shares are undervalued and EPS is 1.38

and on this basis it can be said that it is one of the best option to make investment in portfolio.

(b)Asset allocation by using judgement and theories

Asset allocation play an important role in determining return that can gained on portfolio.

This is because if one will give more proportion to an asset that give less return that those assets

that give higher return then in that situation portoflio can not give high amount of return to the

investors. On other hand, if higher proportion is given to assset that generate good amount of

return and less to those assets that generate less return in business then in that situation portfolio

can generate good amount of return for investor (Kemp, 2011). Hence, it can be said that there is

huge significence of asset allocation in portfolio management. Main aim of portfolio is earn

return of 16% on annual basis and in order to earn return of target amount majority of portion

which is 80% given to equity and 20% portion is given to debt. Majority of portion is given to

equity because debt does not generate good amount of return in business it simply guarantee that

principle amount will be safe and low amount of return will be earned which is fixed will be

earned on invested amount. Markwowitz portfolio theory is taken in to consideration for

portfolio construction as this theory state that in the portfolio allocation made must be

diversified in nature. This is because by doing so risk can be controlled and reduced as well as

good amount of return can be earned on invested amount. By following this theory both equity

and debt are taken in to account as proportion of equity is kept 80% and same of debt is 20%. In

equity also there are six stocks on which allocated cash is utilized. Apart from this, in debt across

six corporate bond and government bond invstment is made. This reflects that allocation is made

in proper manner to earn target return of 16%.

5 | P a g e

genrated huge amount of revenue in its business and sales growth rate is quite high which make

firm performance impressive (Sky plc, 2017). On this basis it can be said that good choice is

made for portfolio construction. Apart from this, other company taken in to account is WPP plc

which is one of the fastest growing company in UK. Firm is currently innovating its business

operations and this technology innovation may boost firm sales in upcoming time period. By

considering this factor business firm is selected in portfolio (WPP plc, 2017). PE ratio of WPP

plc is 9.39 and same of industry is 33. This means firm shares are undervalued and EPS is 1.38

and on this basis it can be said that it is one of the best option to make investment in portfolio.

(b)Asset allocation by using judgement and theories

Asset allocation play an important role in determining return that can gained on portfolio.

This is because if one will give more proportion to an asset that give less return that those assets

that give higher return then in that situation portoflio can not give high amount of return to the

investors. On other hand, if higher proportion is given to assset that generate good amount of

return and less to those assets that generate less return in business then in that situation portfolio

can generate good amount of return for investor (Kemp, 2011). Hence, it can be said that there is

huge significence of asset allocation in portfolio management. Main aim of portfolio is earn

return of 16% on annual basis and in order to earn return of target amount majority of portion

which is 80% given to equity and 20% portion is given to debt. Majority of portion is given to

equity because debt does not generate good amount of return in business it simply guarantee that

principle amount will be safe and low amount of return will be earned which is fixed will be

earned on invested amount. Markwowitz portfolio theory is taken in to consideration for

portfolio construction as this theory state that in the portfolio allocation made must be

diversified in nature. This is because by doing so risk can be controlled and reduced as well as

good amount of return can be earned on invested amount. By following this theory both equity

and debt are taken in to account as proportion of equity is kept 80% and same of debt is 20%. In

equity also there are six stocks on which allocated cash is utilized. Apart from this, in debt across

six corporate bond and government bond invstment is made. This reflects that allocation is made

in proper manner to earn target return of 16%.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

© Selection of benchmark index in order to evaluate firm performance

As part of benchmark FTSE 100 unit trust is taken in to account because 80% of

investment is made in the equity and remaining amount is invested in debt. It must be noted that

because large portion must be invested in equity there is need to take equity index as benchmark.

Due to this reason FTSE 100 unit trust is taken in to consideration as benchmark. This mutual

fund is basically an index fund where in specific proportion investment is made in the company

stocks. It must be noted that index funds are those funds where proportion that securities have in

the index is taken in to account for allocation of fund for specific security in the portfolio that is

constructed in respect to mutual fund scheme (Chaves and et.al., 2010). Elements of the portfolio

also belonged to the FTSE 100 index and due to this reason FTSE 100 unit trust is taken in to

account. Thus, it can be said that appropriate mutual fund scheme is taken in to account as

benchmark index for the current portfolio that is prepared and discussed in the report.

Part 2

Performance of portfolio and reason for change in return

It can be observed that in portfolio return gained on Astrazeenca declined consistently as

it can be observed that in February month there was high level of uncertainity and turmoil in the

market. Due to all these reasons investors loose confidence in the market and they sale their

units. Consistent increase in sales pressure decrease in demand lead to decline in share price.

Same thing is observed in case of other pharmaceutical firm which is GSK. In case of Ryanair

and Easyjet also flcutuation is observed and sometimes positive and sometimes negative returns

are observed (How has the BREXIST vote affected the UK economy?February verdict., 2017). In

month of February due to BREXIT factor negative comments given by many experts give

negative information to the general public. It must be observed that this create negative

investment sentiments and due to this reason less people make purchase and share price

tumbeled down. Same trend is observed in case of firms that are in media sector. Thus, overall it

can be said that news of BREEXIT and poor economic condition at global level are one of the

basic reason that are responsible for fluctuation in return in February month.

Part 3

Critical evaluation of performance of portfolio by using Trenyor ratio

Trenyor ratio reflect return that is earned on each unit of risk that is taken on investment.

It must be noted that here risk is measured by using beta not by using standard deviation which is

6 | P a g e

As part of benchmark FTSE 100 unit trust is taken in to account because 80% of

investment is made in the equity and remaining amount is invested in debt. It must be noted that

because large portion must be invested in equity there is need to take equity index as benchmark.

Due to this reason FTSE 100 unit trust is taken in to consideration as benchmark. This mutual

fund is basically an index fund where in specific proportion investment is made in the company

stocks. It must be noted that index funds are those funds where proportion that securities have in

the index is taken in to account for allocation of fund for specific security in the portfolio that is

constructed in respect to mutual fund scheme (Chaves and et.al., 2010). Elements of the portfolio

also belonged to the FTSE 100 index and due to this reason FTSE 100 unit trust is taken in to

account. Thus, it can be said that appropriate mutual fund scheme is taken in to account as

benchmark index for the current portfolio that is prepared and discussed in the report.

Part 2

Performance of portfolio and reason for change in return

It can be observed that in portfolio return gained on Astrazeenca declined consistently as

it can be observed that in February month there was high level of uncertainity and turmoil in the

market. Due to all these reasons investors loose confidence in the market and they sale their

units. Consistent increase in sales pressure decrease in demand lead to decline in share price.

Same thing is observed in case of other pharmaceutical firm which is GSK. In case of Ryanair

and Easyjet also flcutuation is observed and sometimes positive and sometimes negative returns

are observed (How has the BREXIST vote affected the UK economy?February verdict., 2017). In

month of February due to BREXIT factor negative comments given by many experts give

negative information to the general public. It must be observed that this create negative

investment sentiments and due to this reason less people make purchase and share price

tumbeled down. Same trend is observed in case of firms that are in media sector. Thus, overall it

can be said that news of BREEXIT and poor economic condition at global level are one of the

basic reason that are responsible for fluctuation in return in February month.

Part 3

Critical evaluation of performance of portfolio by using Trenyor ratio

Trenyor ratio reflect return that is earned on each unit of risk that is taken on investment.

It must be noted that here risk is measured by using beta not by using standard deviation which is

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

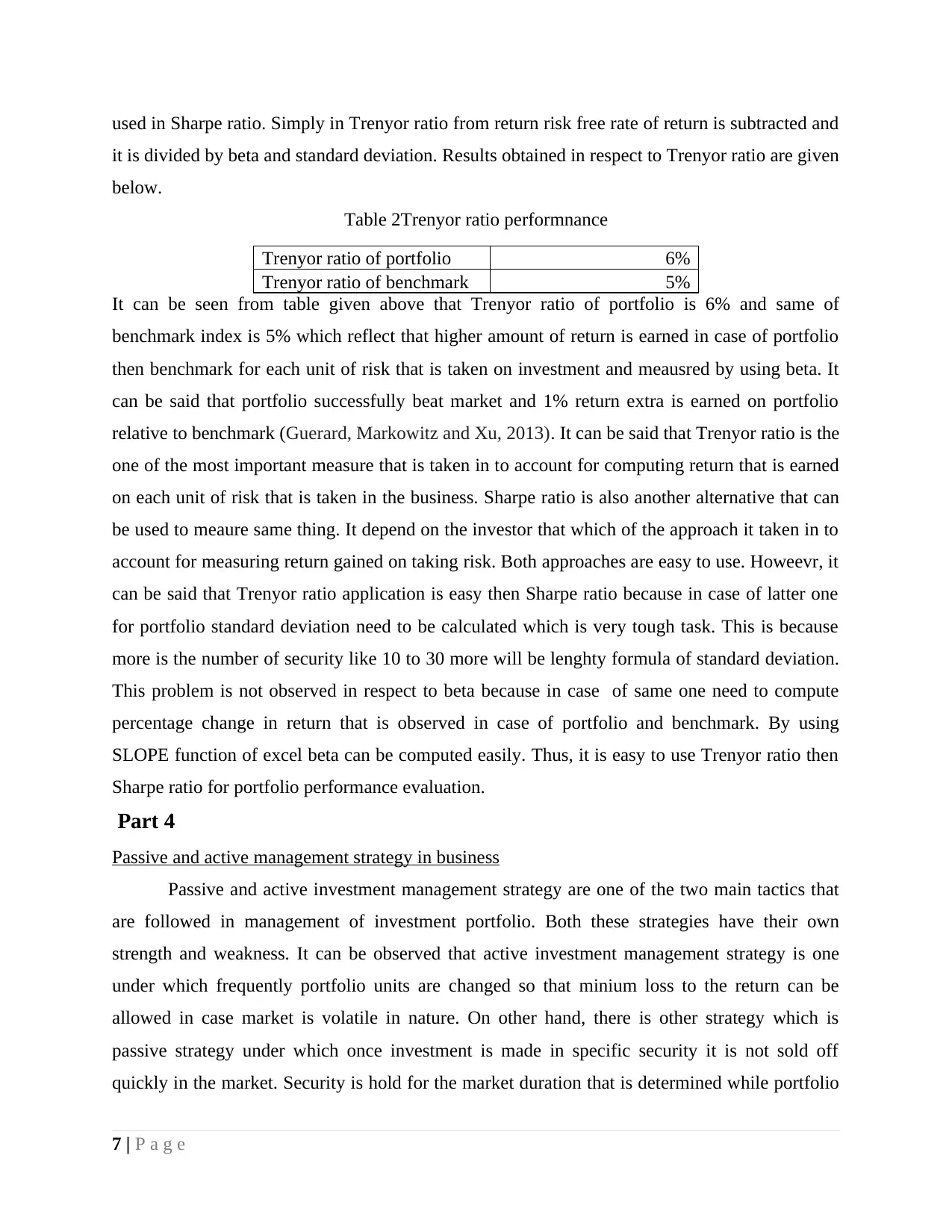

used in Sharpe ratio. Simply in Trenyor ratio from return risk free rate of return is subtracted and

it is divided by beta and standard deviation. Results obtained in respect to Trenyor ratio are given

below.

Table 2Trenyor ratio performnance

Trenyor ratio of portfolio 6%

Trenyor ratio of benchmark 5%

It can be seen from table given above that Trenyor ratio of portfolio is 6% and same of

benchmark index is 5% which reflect that higher amount of return is earned in case of portfolio

then benchmark for each unit of risk that is taken on investment and meausred by using beta. It

can be said that portfolio successfully beat market and 1% return extra is earned on portfolio

relative to benchmark (Guerard, Markowitz and Xu, 2013). It can be said that Trenyor ratio is the

one of the most important measure that is taken in to account for computing return that is earned

on each unit of risk that is taken in the business. Sharpe ratio is also another alternative that can

be used to meaure same thing. It depend on the investor that which of the approach it taken in to

account for measuring return gained on taking risk. Both approaches are easy to use. Howeevr, it

can be said that Trenyor ratio application is easy then Sharpe ratio because in case of latter one

for portfolio standard deviation need to be calculated which is very tough task. This is because

more is the number of security like 10 to 30 more will be lenghty formula of standard deviation.

This problem is not observed in respect to beta because in case of same one need to compute

percentage change in return that is observed in case of portfolio and benchmark. By using

SLOPE function of excel beta can be computed easily. Thus, it is easy to use Trenyor ratio then

Sharpe ratio for portfolio performance evaluation.

Part 4

Passive and active management strategy in business

Passive and active investment management strategy are one of the two main tactics that

are followed in management of investment portfolio. Both these strategies have their own

strength and weakness. It can be observed that active investment management strategy is one

under which frequently portfolio units are changed so that minium loss to the return can be

allowed in case market is volatile in nature. On other hand, there is other strategy which is

passive strategy under which once investment is made in specific security it is not sold off

quickly in the market. Security is hold for the market duration that is determined while portfolio

7 | P a g e

it is divided by beta and standard deviation. Results obtained in respect to Trenyor ratio are given

below.

Table 2Trenyor ratio performnance

Trenyor ratio of portfolio 6%

Trenyor ratio of benchmark 5%

It can be seen from table given above that Trenyor ratio of portfolio is 6% and same of

benchmark index is 5% which reflect that higher amount of return is earned in case of portfolio

then benchmark for each unit of risk that is taken on investment and meausred by using beta. It

can be said that portfolio successfully beat market and 1% return extra is earned on portfolio

relative to benchmark (Guerard, Markowitz and Xu, 2013). It can be said that Trenyor ratio is the

one of the most important measure that is taken in to account for computing return that is earned

on each unit of risk that is taken in the business. Sharpe ratio is also another alternative that can

be used to meaure same thing. It depend on the investor that which of the approach it taken in to

account for measuring return gained on taking risk. Both approaches are easy to use. Howeevr, it

can be said that Trenyor ratio application is easy then Sharpe ratio because in case of latter one

for portfolio standard deviation need to be calculated which is very tough task. This is because

more is the number of security like 10 to 30 more will be lenghty formula of standard deviation.

This problem is not observed in respect to beta because in case of same one need to compute

percentage change in return that is observed in case of portfolio and benchmark. By using

SLOPE function of excel beta can be computed easily. Thus, it is easy to use Trenyor ratio then

Sharpe ratio for portfolio performance evaluation.

Part 4

Passive and active management strategy in business

Passive and active investment management strategy are one of the two main tactics that

are followed in management of investment portfolio. Both these strategies have their own

strength and weakness. It can be observed that active investment management strategy is one

under which frequently portfolio units are changed so that minium loss to the return can be

allowed in case market is volatile in nature. On other hand, there is other strategy which is

passive strategy under which once investment is made in specific security it is not sold off

quickly in the market. Security is hold for the market duration that is determined while portfolio

7 | P a g e

was constructed. Thus, it can be said that both active and passive strategy are opposite of each

other (Bodie, 2013). It must be noted that disadvantage of passive strategy is that if investment is

made for long term when market is in declining stage heavy loss is faced on investment. In case

of portoflio prepared passive strategy is followed as it can be observed that investment in any

unit or company is not changed and all positions were long. Similarly, in case of benchmark also

same thing is observed as it is also passive fund. Thus, it can be said that there is absence of

divergence between portfolio and benchmark. Investment was made for short term which is just

4 weeks and due to this reason no need was observed to sale any of position from portfolio.

CONCLUSION

On the basis of above discussion it is concluded that there is significent importance

portfolio management for the business firms. There are number of tools and techniques that can

be used in construction of portfolio. It depend on the portfolio manager that which of method it

think is appropriate for portfolio construction. In order to construct portofolio basically one must

take in to account economic environment, press release and firm fundamentals. On the basis of

these factors it can be identified whether stock will be able to perform better in the market. This

is one of the important aspect that must always be remembered while constructing portfolio.

Apart from this, one have to select appropriate strategy which may be active or passive portfolio

strategy. There are advantage and disadvantage of both strategies and while selecting one of

them investor must consider number of factors. It is also concluded that in order to measure

performance of portfolio appropriate benchmark must be determined so that performance can be

measured accurately.

8 | P a g e

other (Bodie, 2013). It must be noted that disadvantage of passive strategy is that if investment is

made for long term when market is in declining stage heavy loss is faced on investment. In case

of portoflio prepared passive strategy is followed as it can be observed that investment in any

unit or company is not changed and all positions were long. Similarly, in case of benchmark also

same thing is observed as it is also passive fund. Thus, it can be said that there is absence of

divergence between portfolio and benchmark. Investment was made for short term which is just

4 weeks and due to this reason no need was observed to sale any of position from portfolio.

CONCLUSION

On the basis of above discussion it is concluded that there is significent importance

portfolio management for the business firms. There are number of tools and techniques that can

be used in construction of portfolio. It depend on the portfolio manager that which of method it

think is appropriate for portfolio construction. In order to construct portofolio basically one must

take in to account economic environment, press release and firm fundamentals. On the basis of

these factors it can be identified whether stock will be able to perform better in the market. This

is one of the important aspect that must always be remembered while constructing portfolio.

Apart from this, one have to select appropriate strategy which may be active or passive portfolio

strategy. There are advantage and disadvantage of both strategies and while selecting one of

them investor must consider number of factors. It is also concluded that in order to measure

performance of portfolio appropriate benchmark must be determined so that performance can be

measured accurately.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bodie, Z., 2013. Investments. McGraw-Hill.

Chaves, D. and et.al., 2011. Risk parity portfolio vs. other asset allocation heuristic

portfolios. The Journal of Investing. 20(1). pp.108-118.

Guerard, J.B., Markowitz, H. and Xu, G., 2013. Global stock selection modeling and efficient

portfolio construction and management. The Journal of Investing. 22(4). pp.121-128.

Kemp, M., 2011. Extreme Events-Robust Portfolio Construction in the Presence of Fat Tails.

John Wiley & Sons.

Xidonas, P., Mavrotas, G. and Psarras, J., 2010. Equity portfolio construction and selection using

multiobjective mathematical programming. Journal of Global Optimization. 47(2). pp.185-

209.

Online

How has the BREXIST vote affected the UK economy?February verdict., 2017. [Online].

Available through:<

https://www.theguardian.com/business/ng-interactive/2017/feb/22/how-has-the-brexit-vote-

affected-the-uk-economy-february-verdict>.

Astrazeneca plc, 2017. [Online]. Available through:<

https://www.bloomberg.com/quote/AZN:LN>.

GlaxoSmithKline plc, 2017. [Online]. Available through:<

https://www.bloomberg.com/quote/GSK:LN>.

Easyjet plc, 2017. [Online]. Available through:< https://www.bloomberg.com/quote/EZJ:LN>.

Ryanair Holdings plc, 2017. [Online]. Available through:<

https://www.bloomberg.com/quote/RYA:ID>.

Sky plc, 2017. [Online]. Available through:< https://www.bloomberg.com/quote/SKY:LN>.

WPP plc, 2017. [Online]. Available through:< https://www.bloomberg.com/quote/WPP:LN>.

9 | P a g e

Books and Journals

Bodie, Z., 2013. Investments. McGraw-Hill.

Chaves, D. and et.al., 2011. Risk parity portfolio vs. other asset allocation heuristic

portfolios. The Journal of Investing. 20(1). pp.108-118.

Guerard, J.B., Markowitz, H. and Xu, G., 2013. Global stock selection modeling and efficient

portfolio construction and management. The Journal of Investing. 22(4). pp.121-128.

Kemp, M., 2011. Extreme Events-Robust Portfolio Construction in the Presence of Fat Tails.

John Wiley & Sons.

Xidonas, P., Mavrotas, G. and Psarras, J., 2010. Equity portfolio construction and selection using

multiobjective mathematical programming. Journal of Global Optimization. 47(2). pp.185-

209.

Online

How has the BREXIST vote affected the UK economy?February verdict., 2017. [Online].

Available through:<

https://www.theguardian.com/business/ng-interactive/2017/feb/22/how-has-the-brexit-vote-

affected-the-uk-economy-february-verdict>.

Astrazeneca plc, 2017. [Online]. Available through:<

https://www.bloomberg.com/quote/AZN:LN>.

GlaxoSmithKline plc, 2017. [Online]. Available through:<

https://www.bloomberg.com/quote/GSK:LN>.

Easyjet plc, 2017. [Online]. Available through:< https://www.bloomberg.com/quote/EZJ:LN>.

Ryanair Holdings plc, 2017. [Online]. Available through:<

https://www.bloomberg.com/quote/RYA:ID>.

Sky plc, 2017. [Online]. Available through:< https://www.bloomberg.com/quote/SKY:LN>.

WPP plc, 2017. [Online]. Available through:< https://www.bloomberg.com/quote/WPP:LN>.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

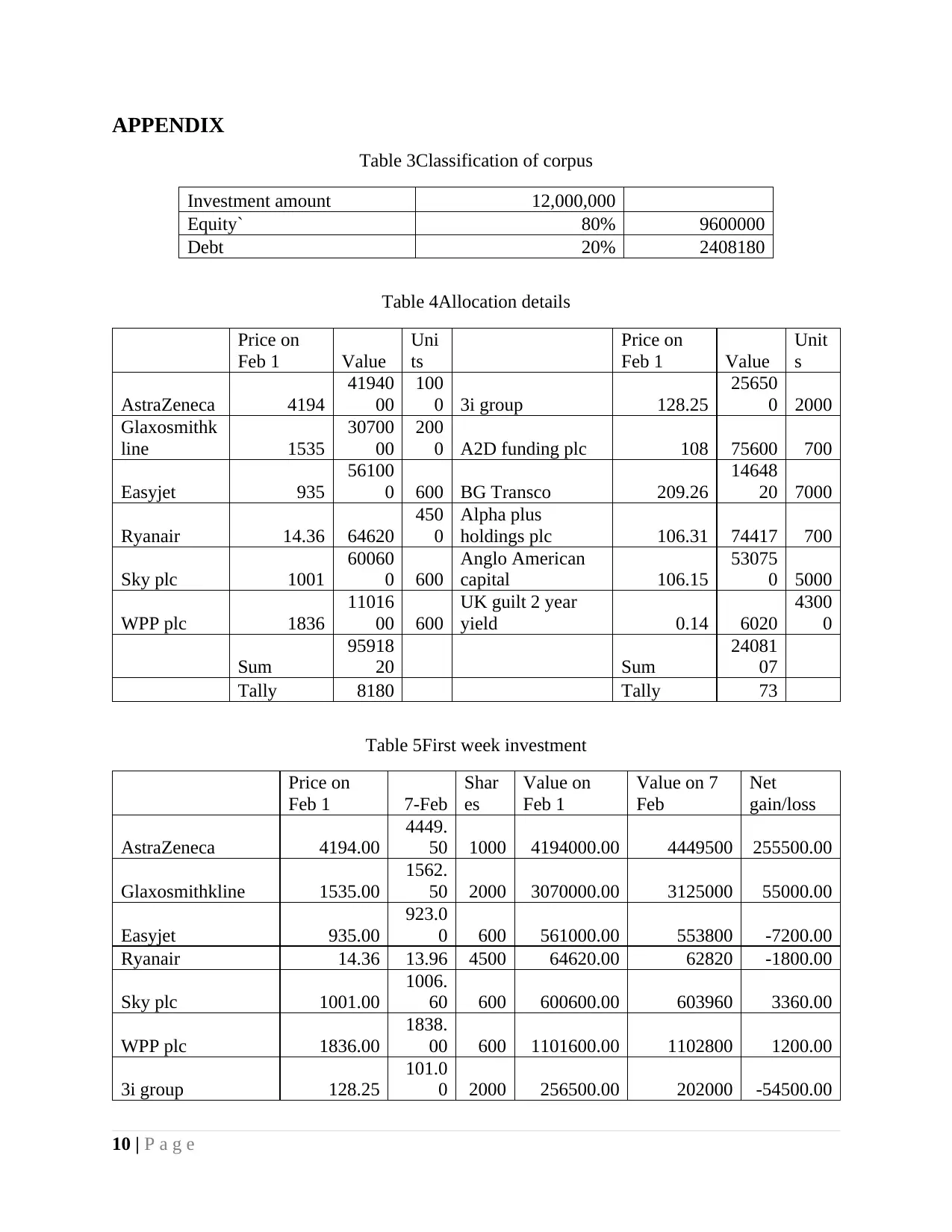

APPENDIX

Table 3Classification of corpus

Investment amount 12,000,000

Equity` 80% 9600000

Debt 20% 2408180

Table 4Allocation details

Price on

Feb 1 Value

Uni

ts

Price on

Feb 1 Value

Unit

s

AstraZeneca 4194

41940

00

100

0 3i group 128.25

25650

0 2000

Glaxosmithk

line 1535

30700

00

200

0 A2D funding plc 108 75600 700

Easyjet 935

56100

0 600 BG Transco 209.26

14648

20 7000

Ryanair 14.36 64620

450

0

Alpha plus

holdings plc 106.31 74417 700

Sky plc 1001

60060

0 600

Anglo American

capital 106.15

53075

0 5000

WPP plc 1836

11016

00 600

UK guilt 2 year

yield 0.14 6020

4300

0

Sum

95918

20 Sum

24081

07

Tally 8180 Tally 73

Table 5First week investment

Price on

Feb 1 7-Feb

Shar

es

Value on

Feb 1

Value on 7

Feb

Net

gain/loss

AstraZeneca 4194.00

4449.

50 1000 4194000.00 4449500 255500.00

Glaxosmithkline 1535.00

1562.

50 2000 3070000.00 3125000 55000.00

Easyjet 935.00

923.0

0 600 561000.00 553800 -7200.00

Ryanair 14.36 13.96 4500 64620.00 62820 -1800.00

Sky plc 1001.00

1006.

60 600 600600.00 603960 3360.00

WPP plc 1836.00

1838.

00 600 1101600.00 1102800 1200.00

3i group 128.25

101.0

0 2000 256500.00 202000 -54500.00

10 | P a g e

Table 3Classification of corpus

Investment amount 12,000,000

Equity` 80% 9600000

Debt 20% 2408180

Table 4Allocation details

Price on

Feb 1 Value

Uni

ts

Price on

Feb 1 Value

Unit

s

AstraZeneca 4194

41940

00

100

0 3i group 128.25

25650

0 2000

Glaxosmithk

line 1535

30700

00

200

0 A2D funding plc 108 75600 700

Easyjet 935

56100

0 600 BG Transco 209.26

14648

20 7000

Ryanair 14.36 64620

450

0

Alpha plus

holdings plc 106.31 74417 700

Sky plc 1001

60060

0 600

Anglo American

capital 106.15

53075

0 5000

WPP plc 1836

11016

00 600

UK guilt 2 year

yield 0.14 6020

4300

0

Sum

95918

20 Sum

24081

07

Tally 8180 Tally 73

Table 5First week investment

Price on

Feb 1 7-Feb

Shar

es

Value on

Feb 1

Value on 7

Feb

Net

gain/loss

AstraZeneca 4194.00

4449.

50 1000 4194000.00 4449500 255500.00

Glaxosmithkline 1535.00

1562.

50 2000 3070000.00 3125000 55000.00

Easyjet 935.00

923.0

0 600 561000.00 553800 -7200.00

Ryanair 14.36 13.96 4500 64620.00 62820 -1800.00

Sky plc 1001.00

1006.

60 600 600600.00 603960 3360.00

WPP plc 1836.00

1838.

00 600 1101600.00 1102800 1200.00

3i group 128.25

101.0

0 2000 256500.00 202000 -54500.00

10 | P a g e

A2D funding plc 108.00

108.1

2 700 75600.00 75684 84.00

BG Transco 209.26

209.2

5 7000 1464820.00 1464750 -70.00

Alpha plus holdings

plc 106.31

106.3

0 700 74417.00 74410 -7.00

Anglo American

capital 106.15

106.1

5 5000 530750.00 530750 0.00

UK guilt 2 year

yield 0.14 0.09

4300

0 6020.00 3784 -2236.00

249331.00

Table 6Second week investment

7-Feb 14-Feb Units

Value on 7

Feb

Value on 14

Feb

Net

gain/loss

AstraZeneca

4449.5

0

4684.0

0 1000 4449500.00 4684000 234500.00

Glaxosmithkline

1562.5

0

1580.0

0 2000 3125000.00 3160000 35000.00

Easyjet 923.00 955.00 600 553800.00 573000 19200.00

Ryanair 13.96 14.35 4500 62820.00 64575 1755.00

Sky plc

1006.6

0

1002.5

0 600 603960.00 601500 -2460.00

WPP plc

1838.0

0

1891.0

0 600 1102800.00 1134600 31800.00

3i group 101.00 128.12 2000 202000.00 256240 54240.00

A2D funding plc 108.12 108.50 700 75684.00 75950 266.00

BG Transco 209.25 209.28 7000 1464750.00 1464960 210.00

Alpha plus holdings

plc 106.30 106.33 700 74410.00 74431 21.00

Anglo American

capital 106.15 107.00 5000 530750.00 535000 4250.00

UK guilt 2 year yield 0.09 0.12

4300

0 3784.00 4988 1204.00

379986.00

Table 7Third portfolio

2/14/20

17

2/21/20

17 Units

Value on 14th

Feb

Value on 21st

Feb

Net

gain/loss

AstraZeneca

4684.0

0

4562.0

0

1000.0

0 4684000 4562000 -122000

Glaxosmithkline

1580.0

0

1645.0

0

2000.0

0 3160000 3290000 130000

11 | P a g e

108.1

2 700 75600.00 75684 84.00

BG Transco 209.26

209.2

5 7000 1464820.00 1464750 -70.00

Alpha plus holdings

plc 106.31

106.3

0 700 74417.00 74410 -7.00

Anglo American

capital 106.15

106.1

5 5000 530750.00 530750 0.00

UK guilt 2 year

yield 0.14 0.09

4300

0 6020.00 3784 -2236.00

249331.00

Table 6Second week investment

7-Feb 14-Feb Units

Value on 7

Feb

Value on 14

Feb

Net

gain/loss

AstraZeneca

4449.5

0

4684.0

0 1000 4449500.00 4684000 234500.00

Glaxosmithkline

1562.5

0

1580.0

0 2000 3125000.00 3160000 35000.00

Easyjet 923.00 955.00 600 553800.00 573000 19200.00

Ryanair 13.96 14.35 4500 62820.00 64575 1755.00

Sky plc

1006.6

0

1002.5

0 600 603960.00 601500 -2460.00

WPP plc

1838.0

0

1891.0

0 600 1102800.00 1134600 31800.00

3i group 101.00 128.12 2000 202000.00 256240 54240.00

A2D funding plc 108.12 108.50 700 75684.00 75950 266.00

BG Transco 209.25 209.28 7000 1464750.00 1464960 210.00

Alpha plus holdings

plc 106.30 106.33 700 74410.00 74431 21.00

Anglo American

capital 106.15 107.00 5000 530750.00 535000 4250.00

UK guilt 2 year yield 0.09 0.12

4300

0 3784.00 4988 1204.00

379986.00

Table 7Third portfolio

2/14/20

17

2/21/20

17 Units

Value on 14th

Feb

Value on 21st

Feb

Net

gain/loss

AstraZeneca

4684.0

0

4562.0

0

1000.0

0 4684000 4562000 -122000

Glaxosmithkline

1580.0

0

1645.0

0

2000.0

0 3160000 3290000 130000

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.