Comparative Analysis of Investment Appraisal Techniques

VerifiedAdded on 2022/12/30

|13

|2010

|26

Project

AI Summary

This project delves into investment appraisal techniques, comparing two projects, A and B, using several financial methods. The assignment begins with an introduction outlining the objectives, followed by a detailed analysis of payback period, discounted payback period, net present value (NPV), internal rate of return (IRR), and accounting rate of return (ARR) for both projects. The analysis includes comprehensive calculations, tables, and sensitivity analyses to evaluate the financial viability and stability of each project. The project also provides a comparative assessment of the advantages and disadvantages of each appraisal technique and concludes with a recommendation based on the findings. References to relevant literature are included to support the analysis. The project aims to determine which project is more financially sound by applying various investment appraisal techniques.

INVESTMENT APPRAISAL

(CAPITAL BUDGETING)

TECHNIQUES

(CAPITAL BUDGETING)

TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question: 1..................................................................................................................................3

Question 2...................................................................................................................................9

Question 3.................................................................................................................................10

Question 4.................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question: 1..................................................................................................................................3

Question 2...................................................................................................................................9

Question 3.................................................................................................................................10

Question 4.................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

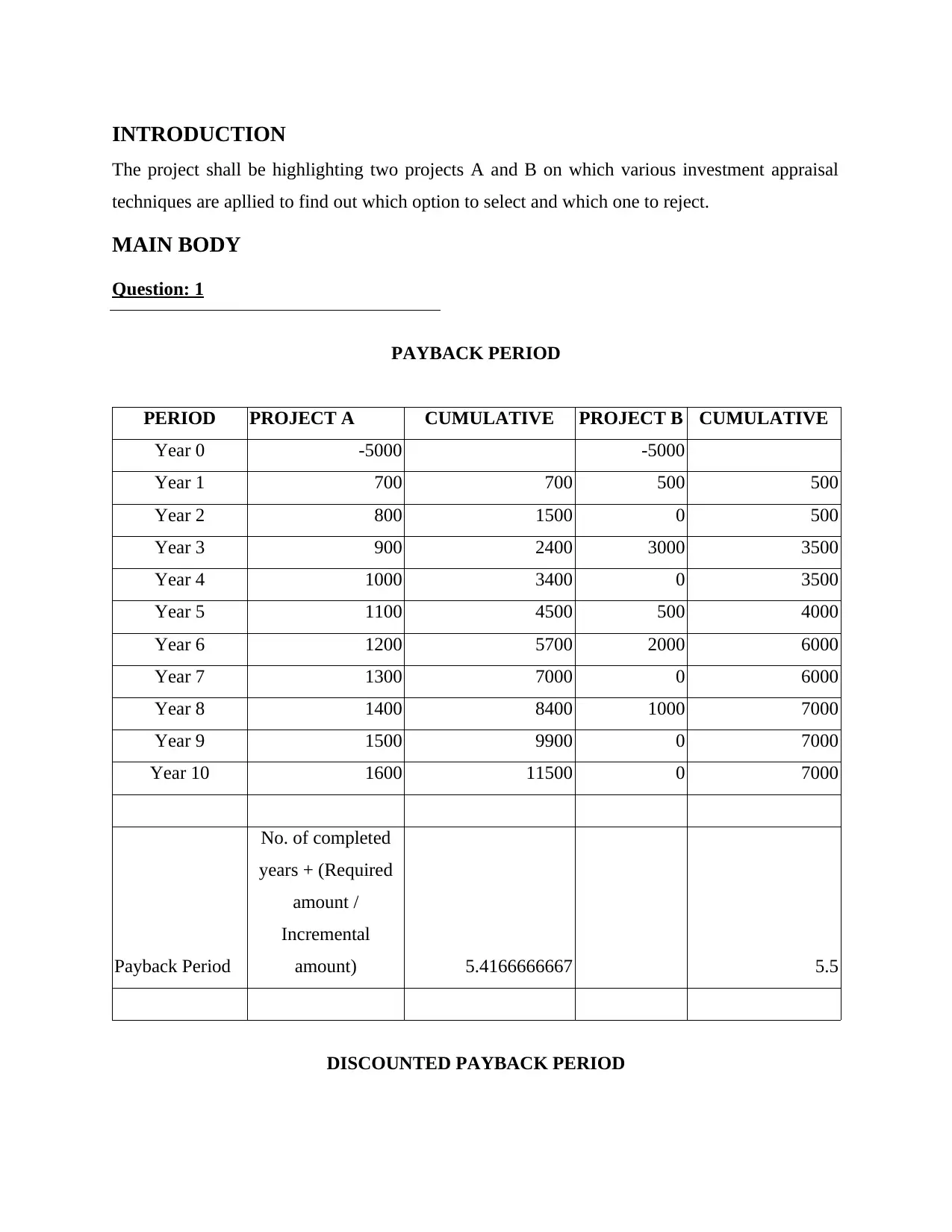

INTRODUCTION

The project shall be highlighting two projects A and B on which various investment appraisal

techniques are apllied to find out which option to select and which one to reject.

MAIN BODY

Question: 1

PAYBACK PERIOD

PERIOD PROJECT A CUMULATIVE PROJECT B CUMULATIVE

Year 0 -5000 -5000

Year 1 700 700 500 500

Year 2 800 1500 0 500

Year 3 900 2400 3000 3500

Year 4 1000 3400 0 3500

Year 5 1100 4500 500 4000

Year 6 1200 5700 2000 6000

Year 7 1300 7000 0 6000

Year 8 1400 8400 1000 7000

Year 9 1500 9900 0 7000

Year 10 1600 11500 0 7000

Payback Period

No. of completed

years + (Required

amount /

Incremental

amount) 5.4166666667 5.5

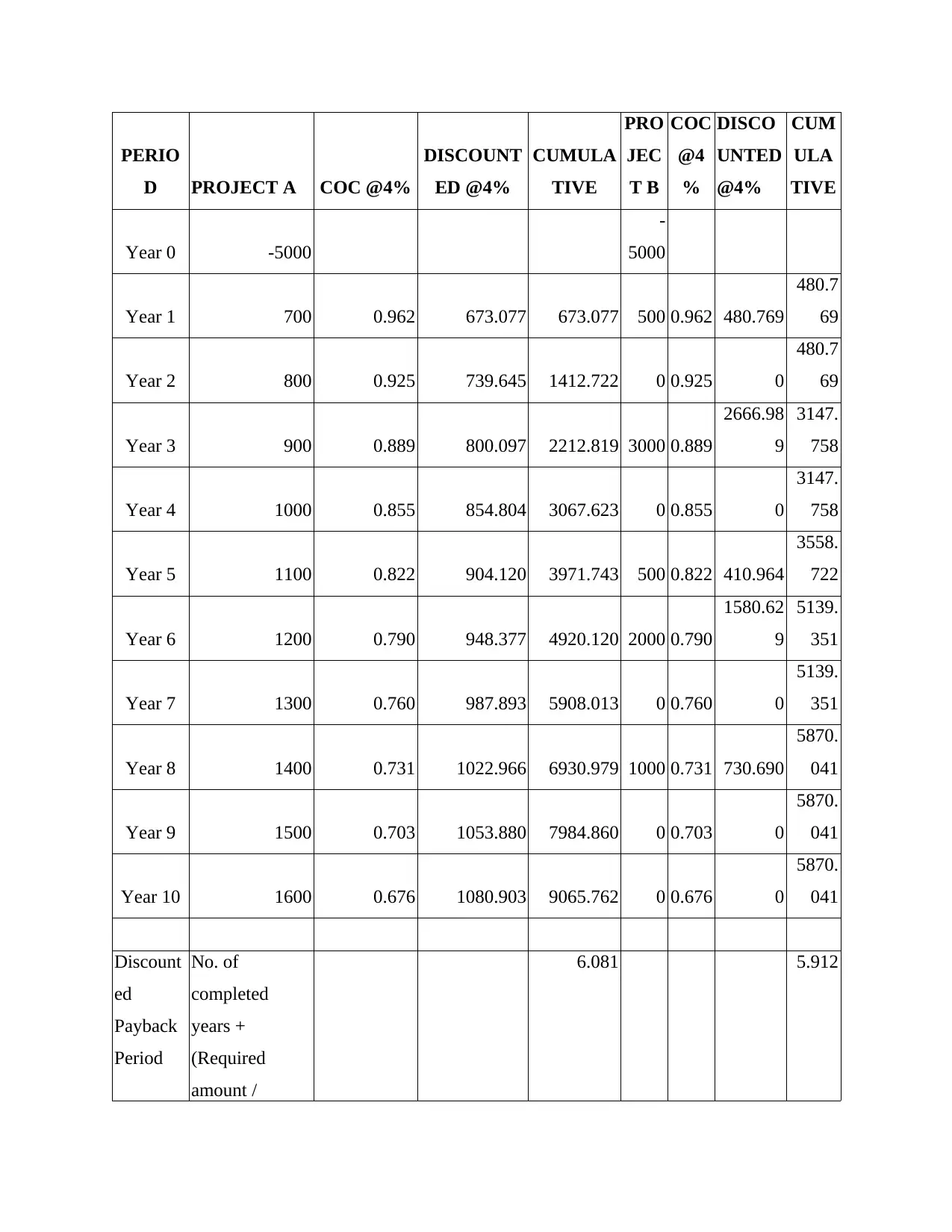

DISCOUNTED PAYBACK PERIOD

The project shall be highlighting two projects A and B on which various investment appraisal

techniques are apllied to find out which option to select and which one to reject.

MAIN BODY

Question: 1

PAYBACK PERIOD

PERIOD PROJECT A CUMULATIVE PROJECT B CUMULATIVE

Year 0 -5000 -5000

Year 1 700 700 500 500

Year 2 800 1500 0 500

Year 3 900 2400 3000 3500

Year 4 1000 3400 0 3500

Year 5 1100 4500 500 4000

Year 6 1200 5700 2000 6000

Year 7 1300 7000 0 6000

Year 8 1400 8400 1000 7000

Year 9 1500 9900 0 7000

Year 10 1600 11500 0 7000

Payback Period

No. of completed

years + (Required

amount /

Incremental

amount) 5.4166666667 5.5

DISCOUNTED PAYBACK PERIOD

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PERIO

D PROJECT A COC @4%

DISCOUNT

ED @4%

CUMULA

TIVE

PRO

JEC

T B

COC

@4

%

DISCO

UNTED

@4%

CUM

ULA

TIVE

Year 0 -5000

-

5000

Year 1 700 0.962 673.077 673.077 500 0.962 480.769

480.7

69

Year 2 800 0.925 739.645 1412.722 0 0.925 0

480.7

69

Year 3 900 0.889 800.097 2212.819 3000 0.889

2666.98

9

3147.

758

Year 4 1000 0.855 854.804 3067.623 0 0.855 0

3147.

758

Year 5 1100 0.822 904.120 3971.743 500 0.822 410.964

3558.

722

Year 6 1200 0.790 948.377 4920.120 2000 0.790

1580.62

9

5139.

351

Year 7 1300 0.760 987.893 5908.013 0 0.760 0

5139.

351

Year 8 1400 0.731 1022.966 6930.979 1000 0.731 730.690

5870.

041

Year 9 1500 0.703 1053.880 7984.860 0 0.703 0

5870.

041

Year 10 1600 0.676 1080.903 9065.762 0 0.676 0

5870.

041

Discount

ed

Payback

Period

No. of

completed

years +

(Required

amount /

6.081 5.912

D PROJECT A COC @4%

DISCOUNT

ED @4%

CUMULA

TIVE

PRO

JEC

T B

COC

@4

%

DISCO

UNTED

@4%

CUM

ULA

TIVE

Year 0 -5000

-

5000

Year 1 700 0.962 673.077 673.077 500 0.962 480.769

480.7

69

Year 2 800 0.925 739.645 1412.722 0 0.925 0

480.7

69

Year 3 900 0.889 800.097 2212.819 3000 0.889

2666.98

9

3147.

758

Year 4 1000 0.855 854.804 3067.623 0 0.855 0

3147.

758

Year 5 1100 0.822 904.120 3971.743 500 0.822 410.964

3558.

722

Year 6 1200 0.790 948.377 4920.120 2000 0.790

1580.62

9

5139.

351

Year 7 1300 0.760 987.893 5908.013 0 0.760 0

5139.

351

Year 8 1400 0.731 1022.966 6930.979 1000 0.731 730.690

5870.

041

Year 9 1500 0.703 1053.880 7984.860 0 0.703 0

5870.

041

Year 10 1600 0.676 1080.903 9065.762 0 0.676 0

5870.

041

Discount

ed

Payback

Period

No. of

completed

years +

(Required

amount /

6.081 5.912

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Incremental

amount)

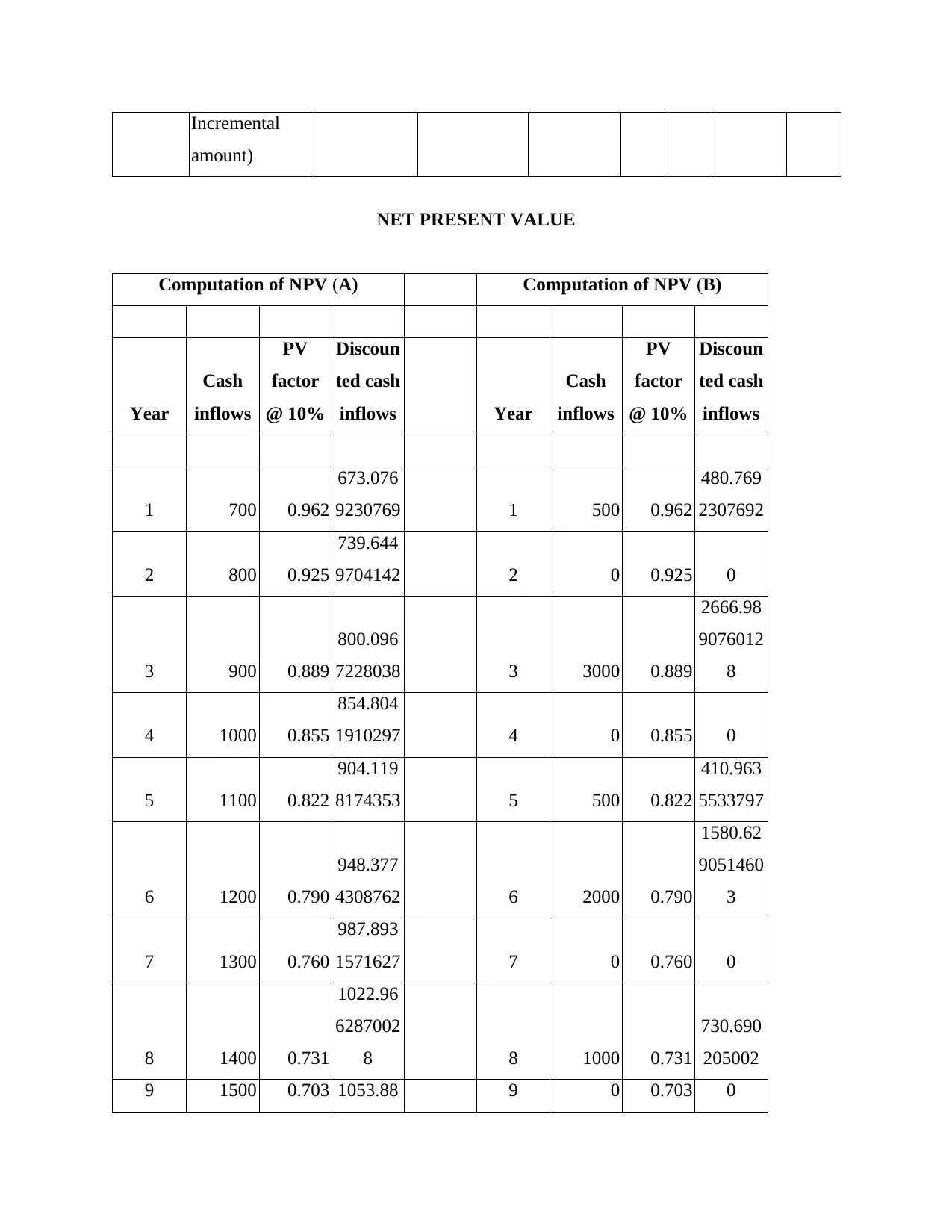

NET PRESENT VALUE

Computation of NPV (A) Computation of NPV (B)

Year

Cash

inflows

PV

factor

@ 10%

Discoun

ted cash

inflows Year

Cash

inflows

PV

factor

@ 10%

Discoun

ted cash

inflows

1 700 0.962

673.076

9230769 1 500 0.962

480.769

2307692

2 800 0.925

739.644

9704142 2 0 0.925 0

3 900 0.889

800.096

7228038 3 3000 0.889

2666.98

9076012

8

4 1000 0.855

854.804

1910297 4 0 0.855 0

5 1100 0.822

904.119

8174353 5 500 0.822

410.963

5533797

6 1200 0.790

948.377

4308762 6 2000 0.790

1580.62

9051460

3

7 1300 0.760

987.893

1571627 7 0 0.760 0

8 1400 0.731

1022.96

6287002

8 8 1000 0.731

730.690

205002

9 1500 0.703 1053.88 9 0 0.703 0

amount)

NET PRESENT VALUE

Computation of NPV (A) Computation of NPV (B)

Year

Cash

inflows

PV

factor

@ 10%

Discoun

ted cash

inflows Year

Cash

inflows

PV

factor

@ 10%

Discoun

ted cash

inflows

1 700 0.962

673.076

9230769 1 500 0.962

480.769

2307692

2 800 0.925

739.644

9704142 2 0 0.925 0

3 900 0.889

800.096

7228038 3 3000 0.889

2666.98

9076012

8

4 1000 0.855

854.804

1910297 4 0 0.855 0

5 1100 0.822

904.119

8174353 5 500 0.822

410.963

5533797

6 1200 0.790

948.377

4308762 6 2000 0.790

1580.62

9051460

3

7 1300 0.760

987.893

1571627 7 0 0.760 0

8 1400 0.731

1022.96

6287002

8 8 1000 0.731

730.690

205002

9 1500 0.703 1053.88 9 0 0.703 0

0103368

3

10 1600 0.676

1080.90

2670121

3 10 0 0.676 0

Total

discount

ed cash

inflow 9066

Total

discount

ed cash

inflow 5870

Initial

investme

nt 5000

Initial

investme

nt 5000

NPV

(Total

discount

ed cash

inflows -

initial

investm

ent) 4066

NPV

(Total

discount

ed cash

inflows -

initial

investm

ent) 870

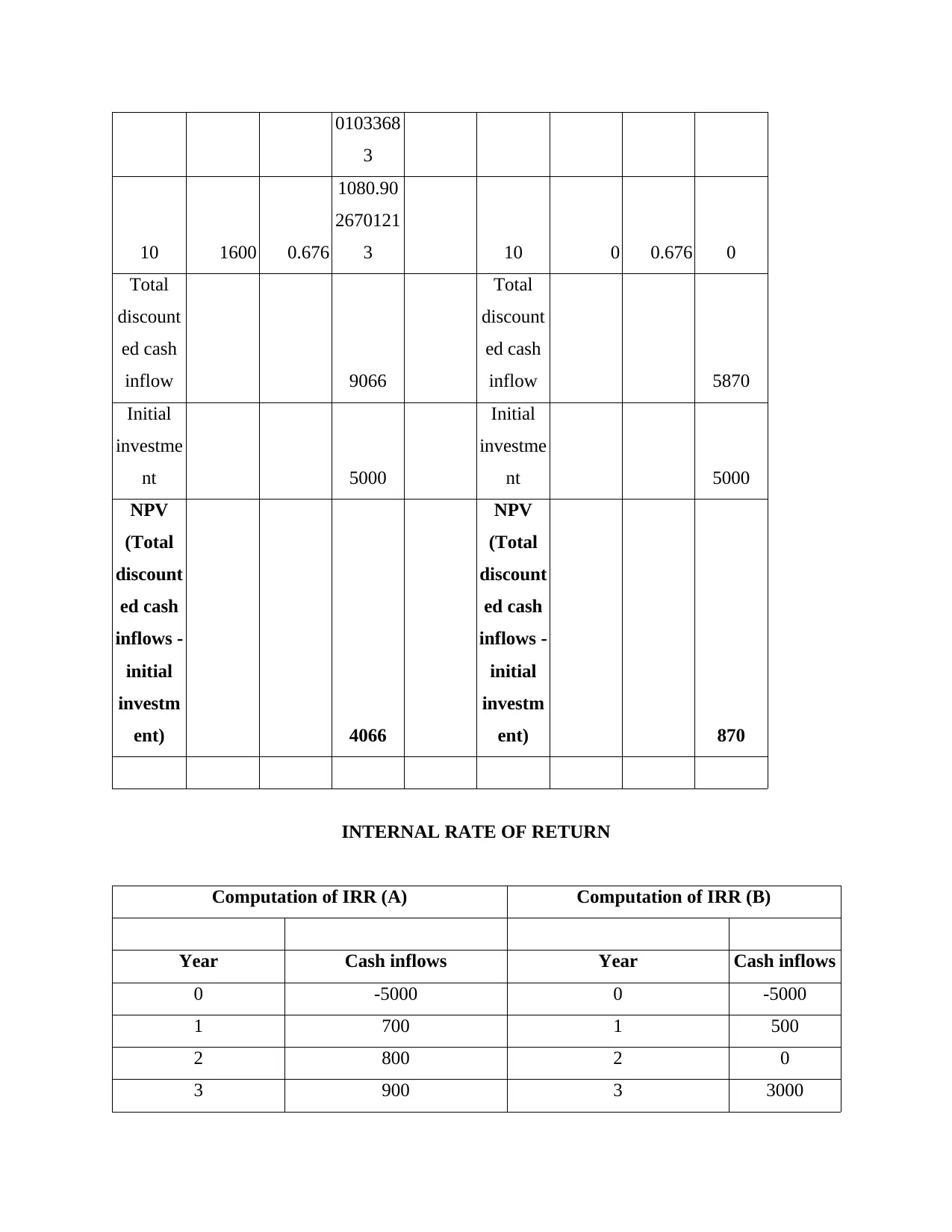

INTERNAL RATE OF RETURN

Computation of IRR (A) Computation of IRR (B)

Year Cash inflows Year Cash inflows

0 -5000 0 -5000

1 700 1 500

2 800 2 0

3 900 3 3000

3

10 1600 0.676

1080.90

2670121

3 10 0 0.676 0

Total

discount

ed cash

inflow 9066

Total

discount

ed cash

inflow 5870

Initial

investme

nt 5000

Initial

investme

nt 5000

NPV

(Total

discount

ed cash

inflows -

initial

investm

ent) 4066

NPV

(Total

discount

ed cash

inflows -

initial

investm

ent) 870

INTERNAL RATE OF RETURN

Computation of IRR (A) Computation of IRR (B)

Year Cash inflows Year Cash inflows

0 -5000 0 -5000

1 700 1 500

2 800 2 0

3 900 3 3000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 1000 4 0

5 1100 5 500

6 1200 6 2000

7 1300 7 0

8 1400 8 1000

9 1500 9 0

10 1600 10 0

Internal rate of

return (IRR) 16%

Internal rate of return

(IRR) 8%

ACCOUNTING RATE OF RETURN

Computation of Average rate of return (A) Computation of Average rate of return (B)

Year Cash inflows Year

Cash

inflows

1 700 1 500

2 800 2 0

3 900 3 3000

4 1000 4 0

5 1100 5 500

6 1200 6 2000

7 1300 7 0

8 1400 8 1000

9 1500 9 0

10 1600 10 0

Average profit or

cash inflow 1150 Average profit or cash inflow 700

Average initial 5000 Average initial investment 5000

5 1100 5 500

6 1200 6 2000

7 1300 7 0

8 1400 8 1000

9 1500 9 0

10 1600 10 0

Internal rate of

return (IRR) 16%

Internal rate of return

(IRR) 8%

ACCOUNTING RATE OF RETURN

Computation of Average rate of return (A) Computation of Average rate of return (B)

Year Cash inflows Year

Cash

inflows

1 700 1 500

2 800 2 0

3 900 3 3000

4 1000 4 0

5 1100 5 500

6 1200 6 2000

7 1300 7 0

8 1400 8 1000

9 1500 9 0

10 1600 10 0

Average profit or

cash inflow 1150 Average profit or cash inflow 700

Average initial 5000 Average initial investment 5000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

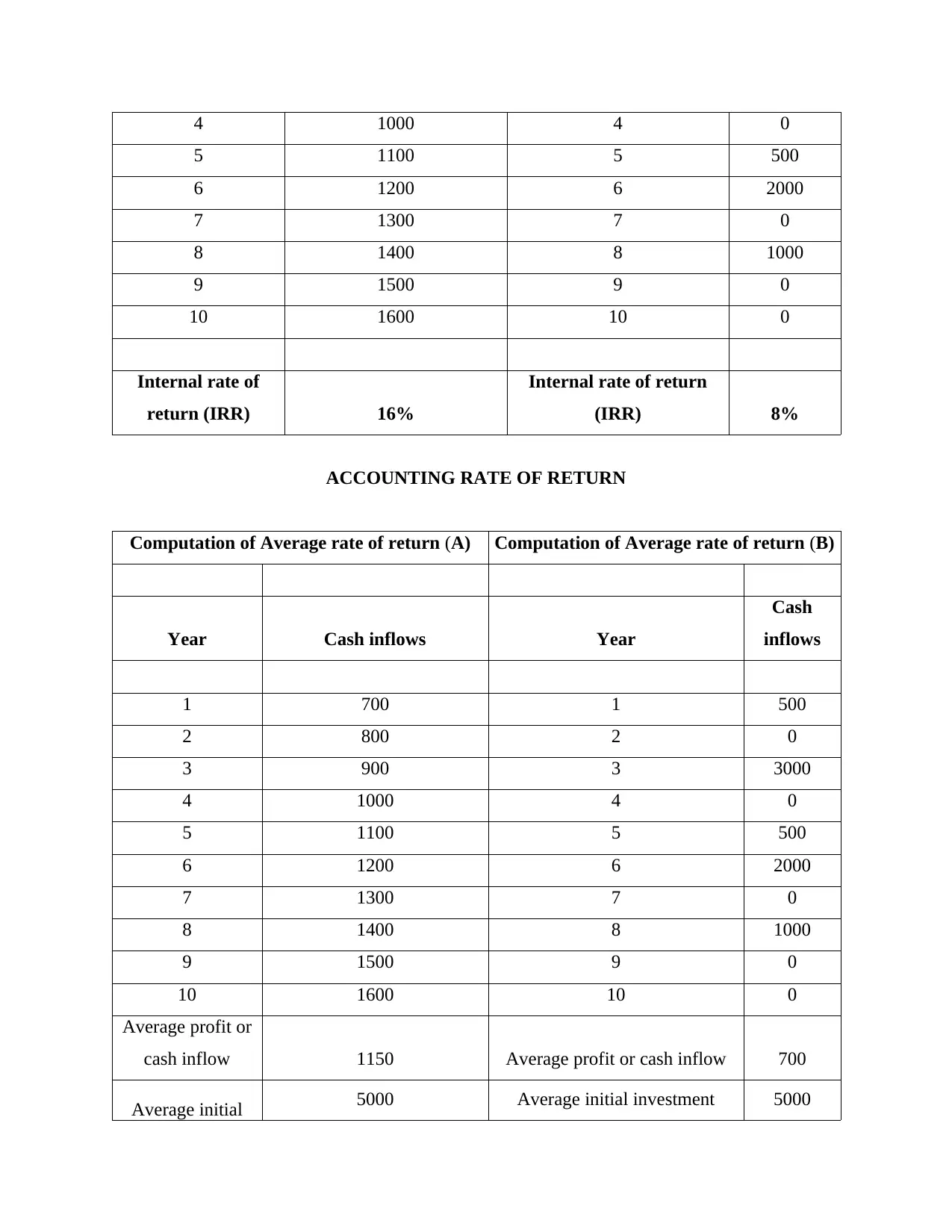

investment

average initial

investment [(initial

investment + scrap

value) / 2]

average initial investment

[(initial investment + scrap

value) / 2]

ARR 23% ARR 14%

SENSITIVITY ANALYSIS

PERIOD PROJECT A 10% up PROJECT B 10% up

Year 1 700 770 500 550

Year 2 800 880 0 0

Year 3 900 990 3000 3300

Year 4 1000 1100 0 0

Year 5 1100 1210 500 550

Year 6 1200 1320 2000 2200

Year 7 1300 1430 0 0

Year 8 1400 1540 1000 1100

Year 9 1500 1650 0 0

Year 10 1600 1760 0 0

PERIOD PROJECT A 10% down PROJECT B 10% down

Year 1 700 630 500 450

Year 2 800 720 0 0

Year 3 900 810 3000 2700

Year 4 1000 900 0 0

Year 5 1100 990 500 450

average initial

investment [(initial

investment + scrap

value) / 2]

average initial investment

[(initial investment + scrap

value) / 2]

ARR 23% ARR 14%

SENSITIVITY ANALYSIS

PERIOD PROJECT A 10% up PROJECT B 10% up

Year 1 700 770 500 550

Year 2 800 880 0 0

Year 3 900 990 3000 3300

Year 4 1000 1100 0 0

Year 5 1100 1210 500 550

Year 6 1200 1320 2000 2200

Year 7 1300 1430 0 0

Year 8 1400 1540 1000 1100

Year 9 1500 1650 0 0

Year 10 1600 1760 0 0

PERIOD PROJECT A 10% down PROJECT B 10% down

Year 1 700 630 500 450

Year 2 800 720 0 0

Year 3 900 810 3000 2700

Year 4 1000 900 0 0

Year 5 1100 990 500 450

Year 6 1200 1080 2000 1800

Year 7 1300 1170 0 0

Year 8 1400 1260 1000 900

Year 9 1500 1350 0 0

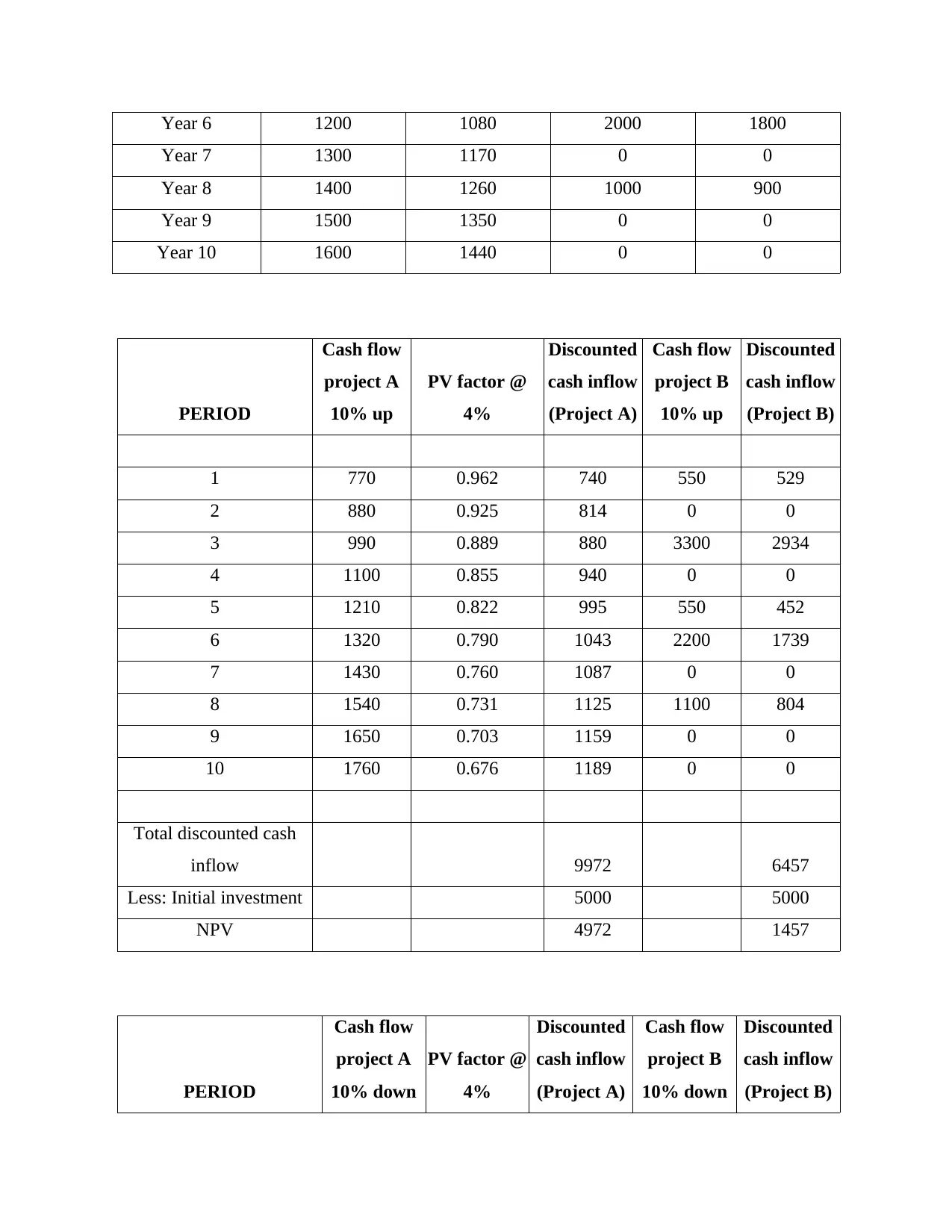

Year 10 1600 1440 0 0

PERIOD

Cash flow

project A

10% up

PV factor @

4%

Discounted

cash inflow

(Project A)

Cash flow

project B

10% up

Discounted

cash inflow

(Project B)

1 770 0.962 740 550 529

2 880 0.925 814 0 0

3 990 0.889 880 3300 2934

4 1100 0.855 940 0 0

5 1210 0.822 995 550 452

6 1320 0.790 1043 2200 1739

7 1430 0.760 1087 0 0

8 1540 0.731 1125 1100 804

9 1650 0.703 1159 0 0

10 1760 0.676 1189 0 0

Total discounted cash

inflow 9972 6457

Less: Initial investment 5000 5000

NPV 4972 1457

PERIOD

Cash flow

project A

10% down

PV factor @

4%

Discounted

cash inflow

(Project A)

Cash flow

project B

10% down

Discounted

cash inflow

(Project B)

Year 7 1300 1170 0 0

Year 8 1400 1260 1000 900

Year 9 1500 1350 0 0

Year 10 1600 1440 0 0

PERIOD

Cash flow

project A

10% up

PV factor @

4%

Discounted

cash inflow

(Project A)

Cash flow

project B

10% up

Discounted

cash inflow

(Project B)

1 770 0.962 740 550 529

2 880 0.925 814 0 0

3 990 0.889 880 3300 2934

4 1100 0.855 940 0 0

5 1210 0.822 995 550 452

6 1320 0.790 1043 2200 1739

7 1430 0.760 1087 0 0

8 1540 0.731 1125 1100 804

9 1650 0.703 1159 0 0

10 1760 0.676 1189 0 0

Total discounted cash

inflow 9972 6457

Less: Initial investment 5000 5000

NPV 4972 1457

PERIOD

Cash flow

project A

10% down

PV factor @

4%

Discounted

cash inflow

(Project A)

Cash flow

project B

10% down

Discounted

cash inflow

(Project B)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

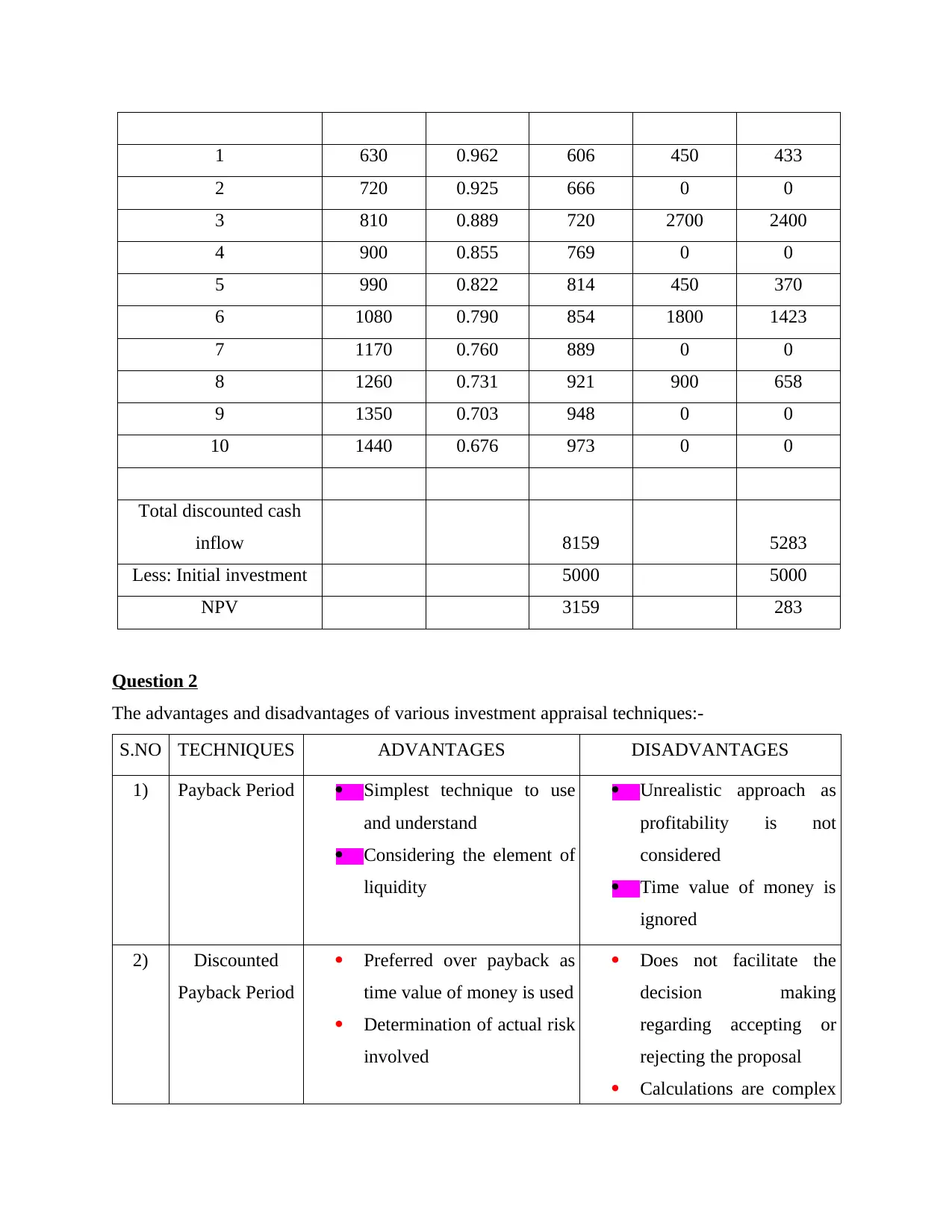

1 630 0.962 606 450 433

2 720 0.925 666 0 0

3 810 0.889 720 2700 2400

4 900 0.855 769 0 0

5 990 0.822 814 450 370

6 1080 0.790 854 1800 1423

7 1170 0.760 889 0 0

8 1260 0.731 921 900 658

9 1350 0.703 948 0 0

10 1440 0.676 973 0 0

Total discounted cash

inflow 8159 5283

Less: Initial investment 5000 5000

NPV 3159 283

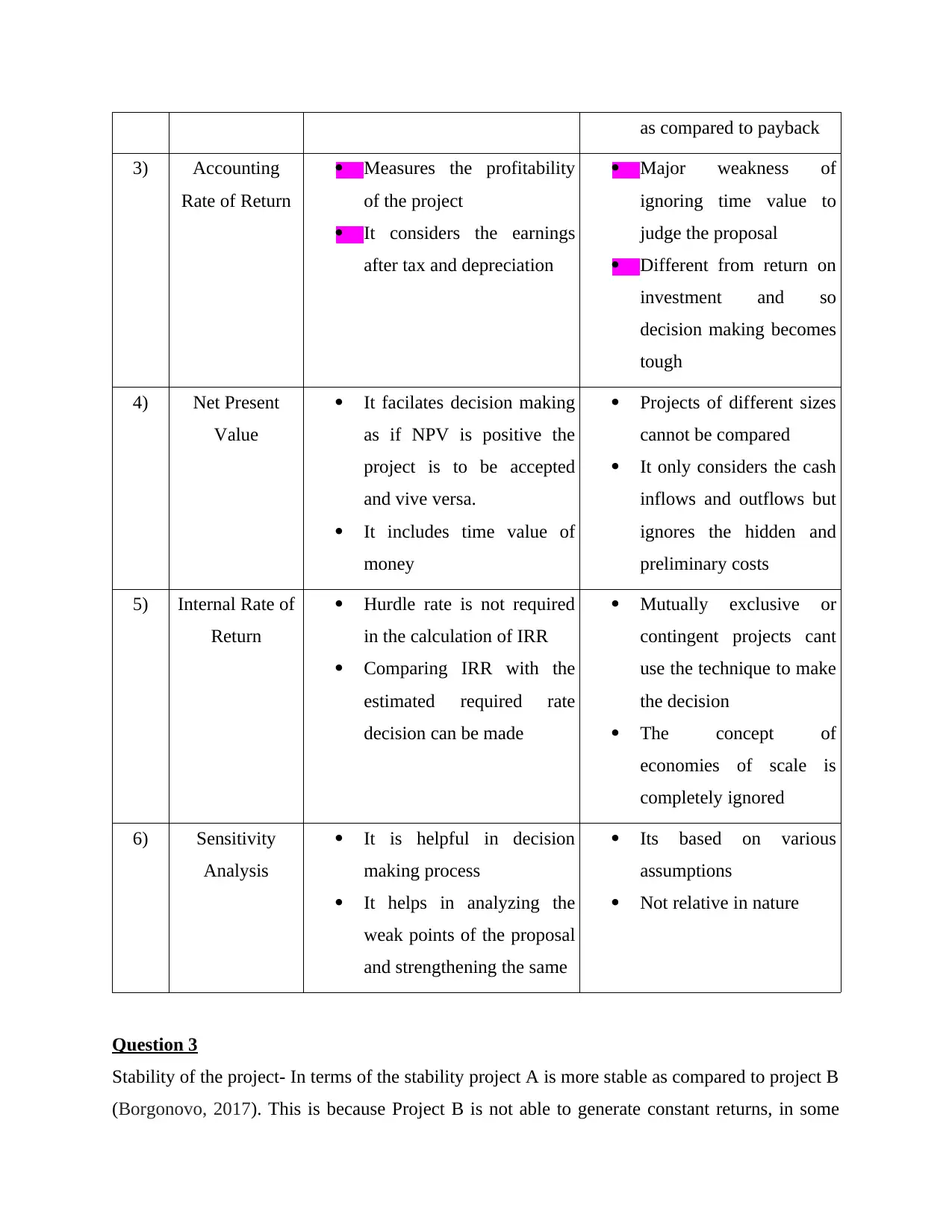

Question 2

The advantages and disadvantages of various investment appraisal techniques:-

S.NO TECHNIQUES ADVANTAGES DISADVANTAGES

1) Payback Period Simplest technique to use

and understand

Considering the element of

liquidity

Unrealistic approach as

profitability is not

considered

Time value of money is

ignored

2) Discounted

Payback Period

Preferred over payback as

time value of money is used

Determination of actual risk

involved

Does not facilitate the

decision making

regarding accepting or

rejecting the proposal

Calculations are complex

2 720 0.925 666 0 0

3 810 0.889 720 2700 2400

4 900 0.855 769 0 0

5 990 0.822 814 450 370

6 1080 0.790 854 1800 1423

7 1170 0.760 889 0 0

8 1260 0.731 921 900 658

9 1350 0.703 948 0 0

10 1440 0.676 973 0 0

Total discounted cash

inflow 8159 5283

Less: Initial investment 5000 5000

NPV 3159 283

Question 2

The advantages and disadvantages of various investment appraisal techniques:-

S.NO TECHNIQUES ADVANTAGES DISADVANTAGES

1) Payback Period Simplest technique to use

and understand

Considering the element of

liquidity

Unrealistic approach as

profitability is not

considered

Time value of money is

ignored

2) Discounted

Payback Period

Preferred over payback as

time value of money is used

Determination of actual risk

involved

Does not facilitate the

decision making

regarding accepting or

rejecting the proposal

Calculations are complex

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as compared to payback

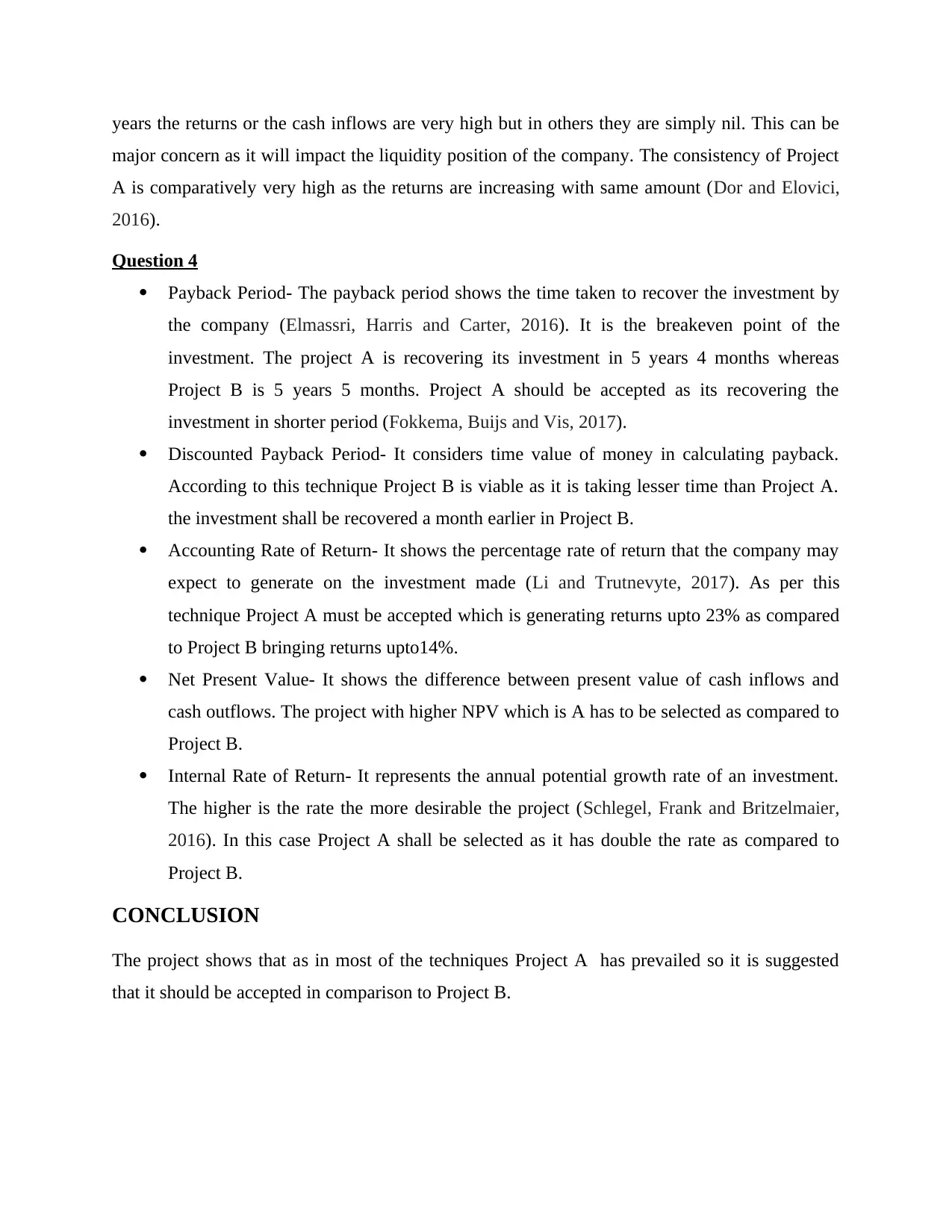

3) Accounting

Rate of Return

Measures the profitability

of the project

It considers the earnings

after tax and depreciation

Major weakness of

ignoring time value to

judge the proposal

Different from return on

investment and so

decision making becomes

tough

4) Net Present

Value

It facilates decision making

as if NPV is positive the

project is to be accepted

and vive versa.

It includes time value of

money

Projects of different sizes

cannot be compared

It only considers the cash

inflows and outflows but

ignores the hidden and

preliminary costs

5) Internal Rate of

Return

Hurdle rate is not required

in the calculation of IRR

Comparing IRR with the

estimated required rate

decision can be made

Mutually exclusive or

contingent projects cant

use the technique to make

the decision

The concept of

economies of scale is

completely ignored

6) Sensitivity

Analysis

It is helpful in decision

making process

It helps in analyzing the

weak points of the proposal

and strengthening the same

Its based on various

assumptions

Not relative in nature

Question 3

Stability of the project- In terms of the stability project A is more stable as compared to project B

(Borgonovo, 2017). This is because Project B is not able to generate constant returns, in some

3) Accounting

Rate of Return

Measures the profitability

of the project

It considers the earnings

after tax and depreciation

Major weakness of

ignoring time value to

judge the proposal

Different from return on

investment and so

decision making becomes

tough

4) Net Present

Value

It facilates decision making

as if NPV is positive the

project is to be accepted

and vive versa.

It includes time value of

money

Projects of different sizes

cannot be compared

It only considers the cash

inflows and outflows but

ignores the hidden and

preliminary costs

5) Internal Rate of

Return

Hurdle rate is not required

in the calculation of IRR

Comparing IRR with the

estimated required rate

decision can be made

Mutually exclusive or

contingent projects cant

use the technique to make

the decision

The concept of

economies of scale is

completely ignored

6) Sensitivity

Analysis

It is helpful in decision

making process

It helps in analyzing the

weak points of the proposal

and strengthening the same

Its based on various

assumptions

Not relative in nature

Question 3

Stability of the project- In terms of the stability project A is more stable as compared to project B

(Borgonovo, 2017). This is because Project B is not able to generate constant returns, in some

years the returns or the cash inflows are very high but in others they are simply nil. This can be

major concern as it will impact the liquidity position of the company. The consistency of Project

A is comparatively very high as the returns are increasing with same amount (Dor and Elovici,

2016).

Question 4

Payback Period- The payback period shows the time taken to recover the investment by

the company (Elmassri, Harris and Carter, 2016). It is the breakeven point of the

investment. The project A is recovering its investment in 5 years 4 months whereas

Project B is 5 years 5 months. Project A should be accepted as its recovering the

investment in shorter period (Fokkema, Buijs and Vis, 2017).

Discounted Payback Period- It considers time value of money in calculating payback.

According to this technique Project B is viable as it is taking lesser time than Project A.

the investment shall be recovered a month earlier in Project B.

Accounting Rate of Return- It shows the percentage rate of return that the company may

expect to generate on the investment made (Li and Trutnevyte, 2017). As per this

technique Project A must be accepted which is generating returns upto 23% as compared

to Project B bringing returns upto14%.

Net Present Value- It shows the difference between present value of cash inflows and

cash outflows. The project with higher NPV which is A has to be selected as compared to

Project B.

Internal Rate of Return- It represents the annual potential growth rate of an investment.

The higher is the rate the more desirable the project (Schlegel, Frank and Britzelmaier,

2016). In this case Project A shall be selected as it has double the rate as compared to

Project B.

CONCLUSION

The project shows that as in most of the techniques Project A has prevailed so it is suggested

that it should be accepted in comparison to Project B.

major concern as it will impact the liquidity position of the company. The consistency of Project

A is comparatively very high as the returns are increasing with same amount (Dor and Elovici,

2016).

Question 4

Payback Period- The payback period shows the time taken to recover the investment by

the company (Elmassri, Harris and Carter, 2016). It is the breakeven point of the

investment. The project A is recovering its investment in 5 years 4 months whereas

Project B is 5 years 5 months. Project A should be accepted as its recovering the

investment in shorter period (Fokkema, Buijs and Vis, 2017).

Discounted Payback Period- It considers time value of money in calculating payback.

According to this technique Project B is viable as it is taking lesser time than Project A.

the investment shall be recovered a month earlier in Project B.

Accounting Rate of Return- It shows the percentage rate of return that the company may

expect to generate on the investment made (Li and Trutnevyte, 2017). As per this

technique Project A must be accepted which is generating returns upto 23% as compared

to Project B bringing returns upto14%.

Net Present Value- It shows the difference between present value of cash inflows and

cash outflows. The project with higher NPV which is A has to be selected as compared to

Project B.

Internal Rate of Return- It represents the annual potential growth rate of an investment.

The higher is the rate the more desirable the project (Schlegel, Frank and Britzelmaier,

2016). In this case Project A shall be selected as it has double the rate as compared to

Project B.

CONCLUSION

The project shows that as in most of the techniques Project A has prevailed so it is suggested

that it should be accepted in comparison to Project B.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.