Financial Management Report: Investment Appraisal and Dividend Policy

VerifiedAdded on 2023/06/10

|16

|3902

|304

Report

AI Summary

This financial management report delves into investment appraisal techniques, including Payback Period, Net Present Value (NPV), and Accounting Rate of Return (ARR), to evaluate project feasibility. The report provides detailed calculations for two projects, offering recommendations based on each method's outcomes. It also examines the merits and demerits of each appraisal technique. Furthermore, the report analyzes the valuation of Carport Plc, considering its dividend policy and the impact of a proposed change in dividend strategy. The report utilizes the dividend discount model to determine share price and discusses various theories surrounding dividend payments and their effect on market prices, concluding with a comprehensive overview of the financial implications.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question No 1:.................................................................................................................................3

a) Calculation of Payback Period, Net Present Value and Accounting Rate of Return along

with recommendation regarding selection of the project:......................................................3

b) Merits and Demerits of each of the different appraisal techniques:...................................7

Question No 3..................................................................................................................................9

a) Calculation of share price of Carport Plc if company does not change its current dividend

policy:.....................................................................................................................................9

b) Valuation of company’s share if managing director proposed dividend policy are

considered upon:...................................................................................................................10

c) Critical evaluation of different models or theories supporting and against the dividend

payment made by the entity on its market price:..................................................................10

CONCLUTION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question No 1:.................................................................................................................................3

a) Calculation of Payback Period, Net Present Value and Accounting Rate of Return along

with recommendation regarding selection of the project:......................................................3

b) Merits and Demerits of each of the different appraisal techniques:...................................7

Question No 3..................................................................................................................................9

a) Calculation of share price of Carport Plc if company does not change its current dividend

policy:.....................................................................................................................................9

b) Valuation of company’s share if managing director proposed dividend policy are

considered upon:...................................................................................................................10

c) Critical evaluation of different models or theories supporting and against the dividend

payment made by the entity on its market price:..................................................................10

CONCLUTION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial management is that managerial activity that is involved with making plans and

controlling of the firm’s monetary resources. In different phrases it's far involved with acquiring,

financing and handling belongings to perform the general purpose of an enterprise (specially to

maximize the shareholder’s wealth). In this report the investment appraisal techniques have been

implemented in order to select the project. The techniques that have been applied are being Net

present value, accounting rate of return and Payback period. After application of all the above

methods the recommendation has been made that which method is feasible for the entity along

with selection of the project. Another discussion in the statement has been made regarding the

valuation of Carport Plc considering the existing dividend policy of the corporation. Further the

market price has been evaluated after taking the viewpoint of managing director. At the end of

the report the theories have been discussed considering the impact on market price when

dividend is paid or not by the business (Allen, Botton, and Uña, 2019).

MAIN BODY

Question No 1:

a) Calculation of Payback Period, Net Present Value and Accounting Rate of Return along with

recommendation regarding selection of the project:

Payback Period:

This method shows the time required by the desired project to recover the initial

investment that has been made by the corporation. This method helps in providing an idea

that in how must time the organisation will start earning the profits for its investors.

Decision making is based on the time taken by the project and that project will be selected

whose payback period is lower (Barroy and Gupta, 2020).

The formula for calculating the payback is mentioned below:

Payback Period = Initial Investment / Cash flows per year

The calculation of payback with respect to Project A and Project B are being mentioned

below:

Project A: (Figures in £)

Years Cash Flows Cumulative Cash Flows

Financial management is that managerial activity that is involved with making plans and

controlling of the firm’s monetary resources. In different phrases it's far involved with acquiring,

financing and handling belongings to perform the general purpose of an enterprise (specially to

maximize the shareholder’s wealth). In this report the investment appraisal techniques have been

implemented in order to select the project. The techniques that have been applied are being Net

present value, accounting rate of return and Payback period. After application of all the above

methods the recommendation has been made that which method is feasible for the entity along

with selection of the project. Another discussion in the statement has been made regarding the

valuation of Carport Plc considering the existing dividend policy of the corporation. Further the

market price has been evaluated after taking the viewpoint of managing director. At the end of

the report the theories have been discussed considering the impact on market price when

dividend is paid or not by the business (Allen, Botton, and Uña, 2019).

MAIN BODY

Question No 1:

a) Calculation of Payback Period, Net Present Value and Accounting Rate of Return along with

recommendation regarding selection of the project:

Payback Period:

This method shows the time required by the desired project to recover the initial

investment that has been made by the corporation. This method helps in providing an idea

that in how must time the organisation will start earning the profits for its investors.

Decision making is based on the time taken by the project and that project will be selected

whose payback period is lower (Barroy and Gupta, 2020).

The formula for calculating the payback is mentioned below:

Payback Period = Initial Investment / Cash flows per year

The calculation of payback with respect to Project A and Project B are being mentioned

below:

Project A: (Figures in £)

Years Cash Flows Cumulative Cash Flows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

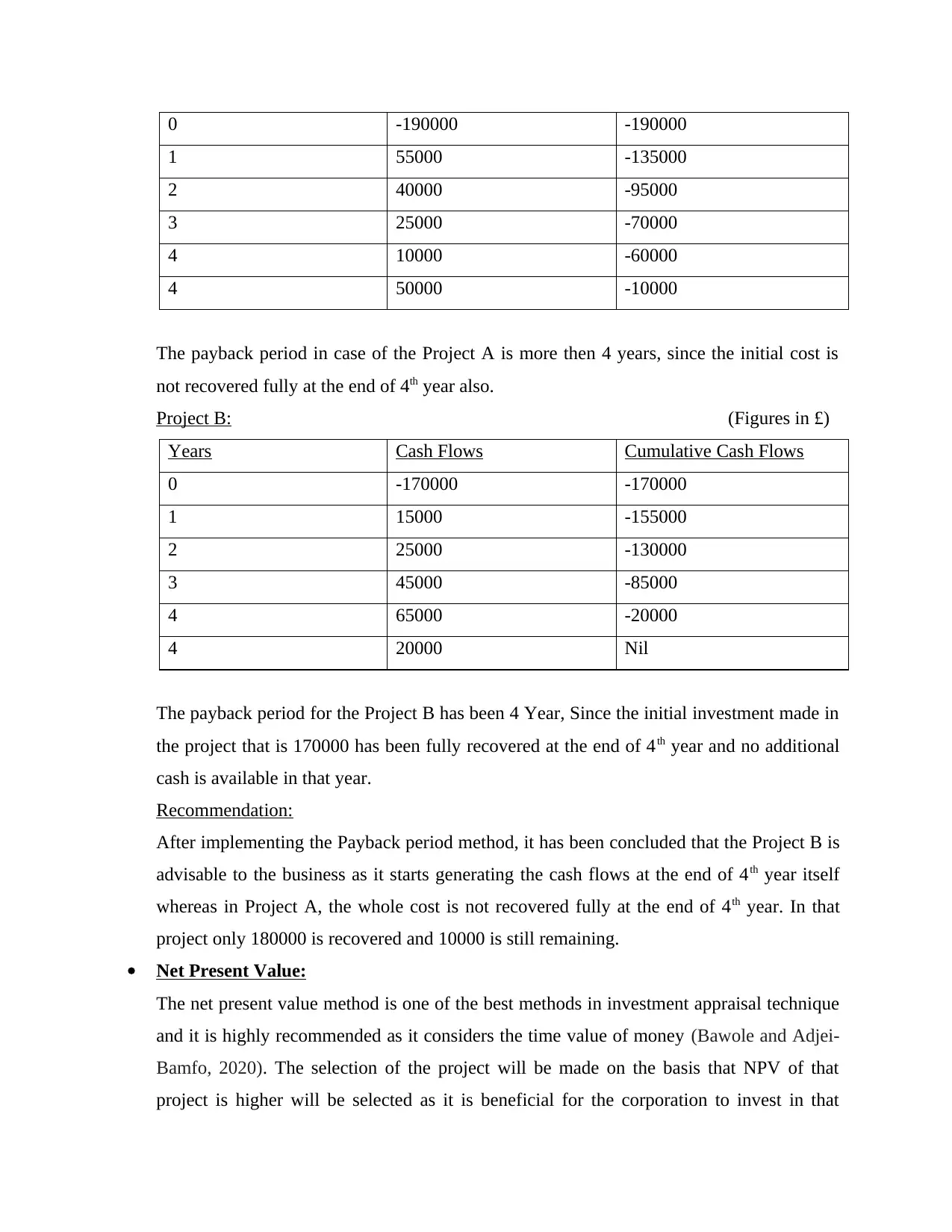

0 -190000 -190000

1 55000 -135000

2 40000 -95000

3 25000 -70000

4 10000 -60000

4 50000 -10000

The payback period in case of the Project A is more then 4 years, since the initial cost is

not recovered fully at the end of 4th year also.

Project B: (Figures in £)

Years Cash Flows Cumulative Cash Flows

0 -170000 -170000

1 15000 -155000

2 25000 -130000

3 45000 -85000

4 65000 -20000

4 20000 Nil

The payback period for the Project B has been 4 Year, Since the initial investment made in

the project that is 170000 has been fully recovered at the end of 4th year and no additional

cash is available in that year.

Recommendation:

After implementing the Payback period method, it has been concluded that the Project B is

advisable to the business as it starts generating the cash flows at the end of 4th year itself

whereas in Project A, the whole cost is not recovered fully at the end of 4th year. In that

project only 180000 is recovered and 10000 is still remaining.

Net Present Value:

The net present value method is one of the best methods in investment appraisal technique

and it is highly recommended as it considers the time value of money (Bawole and Adjei-

Bamfo, 2020). The selection of the project will be made on the basis that NPV of that

project is higher will be selected as it is beneficial for the corporation to invest in that

1 55000 -135000

2 40000 -95000

3 25000 -70000

4 10000 -60000

4 50000 -10000

The payback period in case of the Project A is more then 4 years, since the initial cost is

not recovered fully at the end of 4th year also.

Project B: (Figures in £)

Years Cash Flows Cumulative Cash Flows

0 -170000 -170000

1 15000 -155000

2 25000 -130000

3 45000 -85000

4 65000 -20000

4 20000 Nil

The payback period for the Project B has been 4 Year, Since the initial investment made in

the project that is 170000 has been fully recovered at the end of 4th year and no additional

cash is available in that year.

Recommendation:

After implementing the Payback period method, it has been concluded that the Project B is

advisable to the business as it starts generating the cash flows at the end of 4th year itself

whereas in Project A, the whole cost is not recovered fully at the end of 4th year. In that

project only 180000 is recovered and 10000 is still remaining.

Net Present Value:

The net present value method is one of the best methods in investment appraisal technique

and it is highly recommended as it considers the time value of money (Bawole and Adjei-

Bamfo, 2020). The selection of the project will be made on the basis that NPV of that

project is higher will be selected as it is beneficial for the corporation to invest in that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

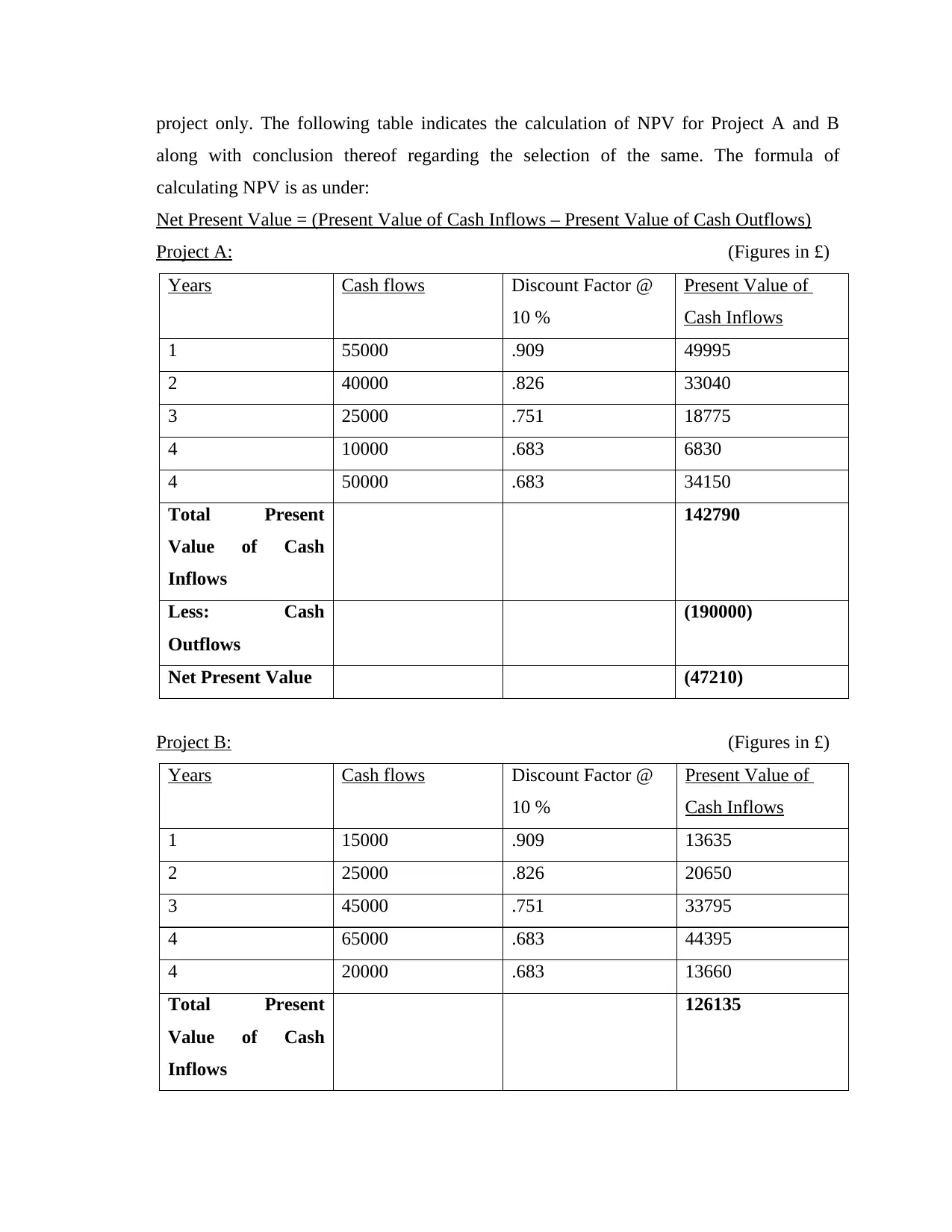

project only. The following table indicates the calculation of NPV for Project A and B

along with conclusion thereof regarding the selection of the same. The formula of

calculating NPV is as under:

Net Present Value = (Present Value of Cash Inflows – Present Value of Cash Outflows)

Project A: (Figures in £)

Years Cash flows Discount Factor @

10 %

Present Value of

Cash Inflows

1 55000 .909 49995

2 40000 .826 33040

3 25000 .751 18775

4 10000 .683 6830

4 50000 .683 34150

Total Present

Value of Cash

Inflows

142790

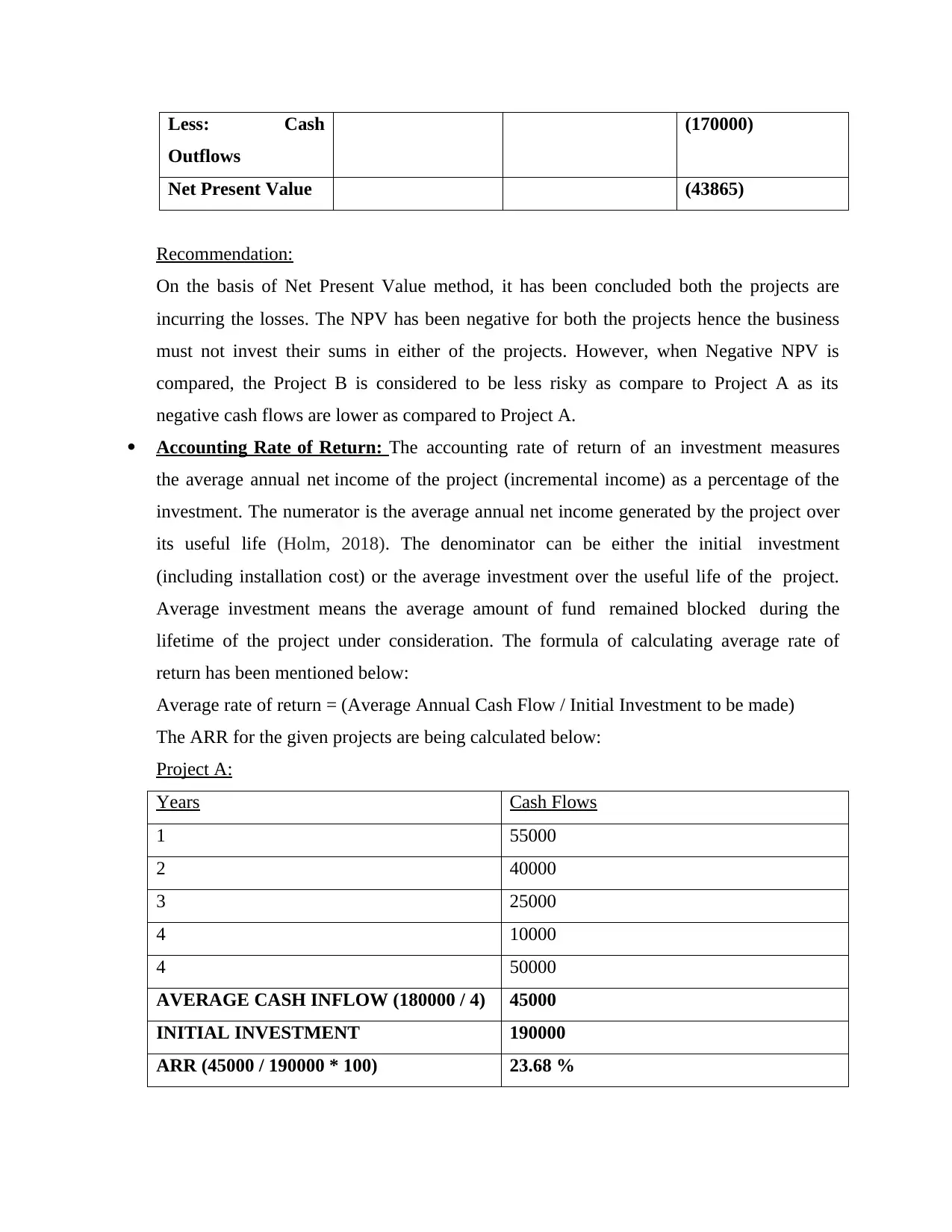

Less: Cash

Outflows

(190000)

Net Present Value (47210)

Project B: (Figures in £)

Years Cash flows Discount Factor @

10 %

Present Value of

Cash Inflows

1 15000 .909 13635

2 25000 .826 20650

3 45000 .751 33795

4 65000 .683 44395

4 20000 .683 13660

Total Present

Value of Cash

Inflows

126135

along with conclusion thereof regarding the selection of the same. The formula of

calculating NPV is as under:

Net Present Value = (Present Value of Cash Inflows – Present Value of Cash Outflows)

Project A: (Figures in £)

Years Cash flows Discount Factor @

10 %

Present Value of

Cash Inflows

1 55000 .909 49995

2 40000 .826 33040

3 25000 .751 18775

4 10000 .683 6830

4 50000 .683 34150

Total Present

Value of Cash

Inflows

142790

Less: Cash

Outflows

(190000)

Net Present Value (47210)

Project B: (Figures in £)

Years Cash flows Discount Factor @

10 %

Present Value of

Cash Inflows

1 15000 .909 13635

2 25000 .826 20650

3 45000 .751 33795

4 65000 .683 44395

4 20000 .683 13660

Total Present

Value of Cash

Inflows

126135

Less: Cash

Outflows

(170000)

Net Present Value (43865)

Recommendation:

On the basis of Net Present Value method, it has been concluded both the projects are

incurring the losses. The NPV has been negative for both the projects hence the business

must not invest their sums in either of the projects. However, when Negative NPV is

compared, the Project B is considered to be less risky as compare to Project A as its

negative cash flows are lower as compared to Project A.

Accounting Rate of Return: The accounting rate of return of an investment measures

the average annual net income of the project (incremental income) as a percentage of the

investment. The numerator is the average annual net income generated by the project over

its useful life (Holm, 2018). The denominator can be either the initial investment

(including installation cost) or the average investment over the useful life of the project.

Average investment means the average amount of fund remained blocked during the

lifetime of the project under consideration. The formula of calculating average rate of

return has been mentioned below:

Average rate of return = (Average Annual Cash Flow / Initial Investment to be made)

The ARR for the given projects are being calculated below:

Project A:

Years Cash Flows

1 55000

2 40000

3 25000

4 10000

4 50000

AVERAGE CASH INFLOW (180000 / 4) 45000

INITIAL INVESTMENT 190000

ARR (45000 / 190000 * 100) 23.68 %

Outflows

(170000)

Net Present Value (43865)

Recommendation:

On the basis of Net Present Value method, it has been concluded both the projects are

incurring the losses. The NPV has been negative for both the projects hence the business

must not invest their sums in either of the projects. However, when Negative NPV is

compared, the Project B is considered to be less risky as compare to Project A as its

negative cash flows are lower as compared to Project A.

Accounting Rate of Return: The accounting rate of return of an investment measures

the average annual net income of the project (incremental income) as a percentage of the

investment. The numerator is the average annual net income generated by the project over

its useful life (Holm, 2018). The denominator can be either the initial investment

(including installation cost) or the average investment over the useful life of the project.

Average investment means the average amount of fund remained blocked during the

lifetime of the project under consideration. The formula of calculating average rate of

return has been mentioned below:

Average rate of return = (Average Annual Cash Flow / Initial Investment to be made)

The ARR for the given projects are being calculated below:

Project A:

Years Cash Flows

1 55000

2 40000

3 25000

4 10000

4 50000

AVERAGE CASH INFLOW (180000 / 4) 45000

INITIAL INVESTMENT 190000

ARR (45000 / 190000 * 100) 23.68 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

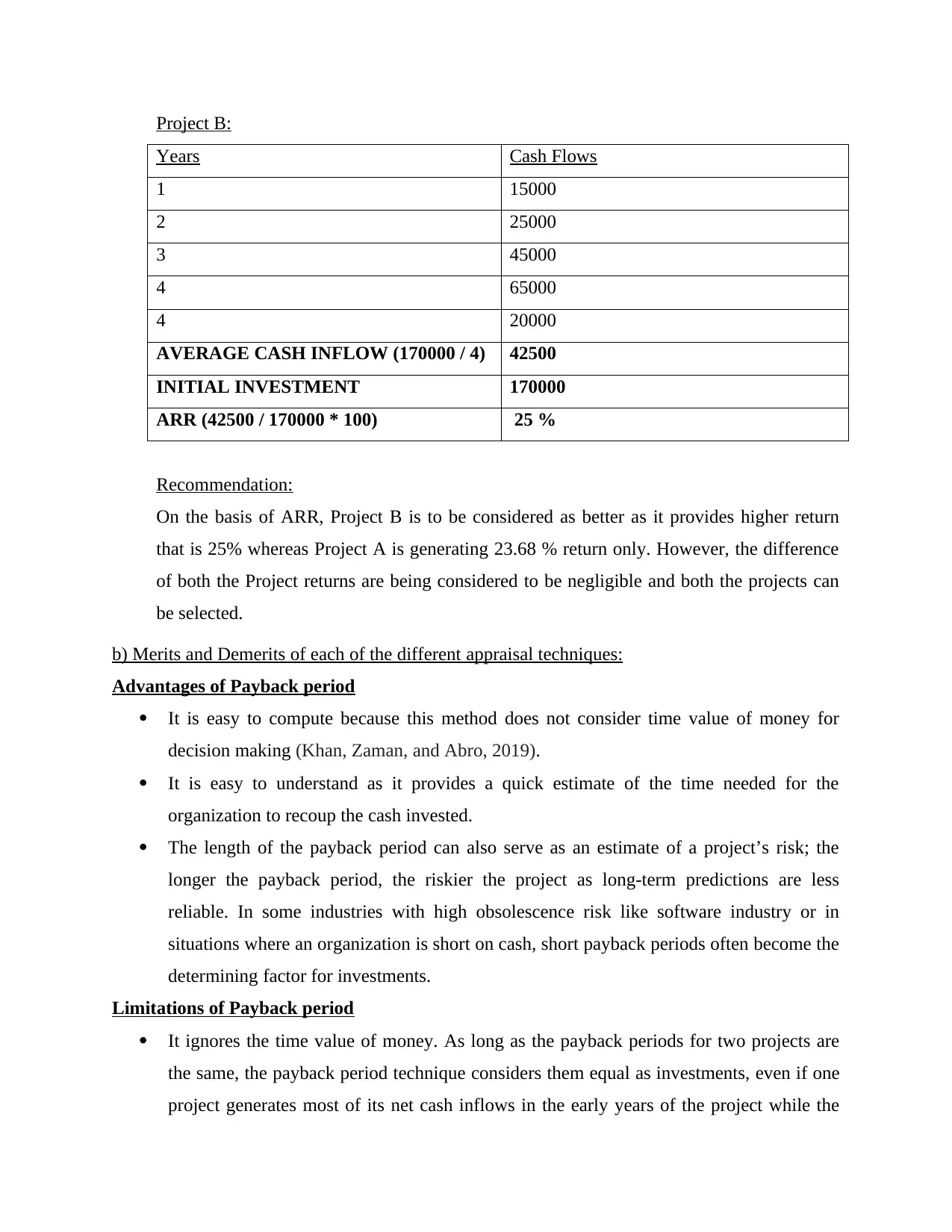

Project B:

Years Cash Flows

1 15000

2 25000

3 45000

4 65000

4 20000

AVERAGE CASH INFLOW (170000 / 4) 42500

INITIAL INVESTMENT 170000

ARR (42500 / 170000 * 100) 25 %

Recommendation:

On the basis of ARR, Project B is to be considered as better as it provides higher return

that is 25% whereas Project A is generating 23.68 % return only. However, the difference

of both the Project returns are being considered to be negligible and both the projects can

be selected.

b) Merits and Demerits of each of the different appraisal techniques:

Advantages of Payback period

It is easy to compute because this method does not consider time value of money for

decision making (Khan, Zaman, and Abro, 2019).

It is easy to understand as it provides a quick estimate of the time needed for the

organization to recoup the cash invested.

The length of the payback period can also serve as an estimate of a project’s risk; the

longer the payback period, the riskier the project as long-term predictions are less

reliable. In some industries with high obsolescence risk like software industry or in

situations where an organization is short on cash, short payback periods often become the

determining factor for investments.

Limitations of Payback period

It ignores the time value of money. As long as the payback periods for two projects are

the same, the payback period technique considers them equal as investments, even if one

project generates most of its net cash inflows in the early years of the project while the

Years Cash Flows

1 15000

2 25000

3 45000

4 65000

4 20000

AVERAGE CASH INFLOW (170000 / 4) 42500

INITIAL INVESTMENT 170000

ARR (42500 / 170000 * 100) 25 %

Recommendation:

On the basis of ARR, Project B is to be considered as better as it provides higher return

that is 25% whereas Project A is generating 23.68 % return only. However, the difference

of both the Project returns are being considered to be negligible and both the projects can

be selected.

b) Merits and Demerits of each of the different appraisal techniques:

Advantages of Payback period

It is easy to compute because this method does not consider time value of money for

decision making (Khan, Zaman, and Abro, 2019).

It is easy to understand as it provides a quick estimate of the time needed for the

organization to recoup the cash invested.

The length of the payback period can also serve as an estimate of a project’s risk; the

longer the payback period, the riskier the project as long-term predictions are less

reliable. In some industries with high obsolescence risk like software industry or in

situations where an organization is short on cash, short payback periods often become the

determining factor for investments.

Limitations of Payback period

It ignores the time value of money. As long as the payback periods for two projects are

the same, the payback period technique considers them equal as investments, even if one

project generates most of its net cash inflows in the early years of the project while the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

other project generates most of its net cash inflows in the latter years of the payback

period (Kumar and Nagaraju, 2018).

A second limitation of this technique is its failure to consider an investment’s total

profitability; it only considers cash inflows up-to the period in which initial investment is

fully recovered and ignores cash flows after the payback period.

Payback technique places much emphasis on short payback periods thereby ignoring

long-term projects.

Advantages of ARR

This technique uses readily available data that is routinely generated for financial reports

and does not require any special procedures to generate data.

This method may also mirror the method used to evaluate performance on the operating

results of an investment and management performance. Using the same procedure in both

decision-making and performance evaluation ensures consistency (Oleghe, 2019).

Calculation of the accounting rate of return method considers all net incomes over the

entire life of the project and provides a measure of the investment’s profitability.

Limitations of ARR

The accounting rate of return technique, like the payback period technique, ignores the

time value of money and considers the value of all cash flows to be equal.

The technique uses accounting numbers that are dependent on the organization’s choice

of accounting procedures, and different accounting procedures, e.g., depreciation

methods, can lead to substantially different amounts for an investment’s net income and

book values.

The method uses net income rather than cash flows; while net income is a useful measure

of profitability, the net cash flow is a better measure of an investment’s performance.

Furthermore, inclusion of only the book value of the invested asset ignores the fact that a

project can require commitments of working capital and other outlays that are not

included in the book value of the project (Pinckney, Cohen, and Leonard, 2019).

Advantages of NPV

NPV method takes into account the time value of money that provide more accurate

results for the enterprise.

period (Kumar and Nagaraju, 2018).

A second limitation of this technique is its failure to consider an investment’s total

profitability; it only considers cash inflows up-to the period in which initial investment is

fully recovered and ignores cash flows after the payback period.

Payback technique places much emphasis on short payback periods thereby ignoring

long-term projects.

Advantages of ARR

This technique uses readily available data that is routinely generated for financial reports

and does not require any special procedures to generate data.

This method may also mirror the method used to evaluate performance on the operating

results of an investment and management performance. Using the same procedure in both

decision-making and performance evaluation ensures consistency (Oleghe, 2019).

Calculation of the accounting rate of return method considers all net incomes over the

entire life of the project and provides a measure of the investment’s profitability.

Limitations of ARR

The accounting rate of return technique, like the payback period technique, ignores the

time value of money and considers the value of all cash flows to be equal.

The technique uses accounting numbers that are dependent on the organization’s choice

of accounting procedures, and different accounting procedures, e.g., depreciation

methods, can lead to substantially different amounts for an investment’s net income and

book values.

The method uses net income rather than cash flows; while net income is a useful measure

of profitability, the net cash flow is a better measure of an investment’s performance.

Furthermore, inclusion of only the book value of the invested asset ignores the fact that a

project can require commitments of working capital and other outlays that are not

included in the book value of the project (Pinckney, Cohen, and Leonard, 2019).

Advantages of NPV

NPV method takes into account the time value of money that provide more accurate

results for the enterprise.

The whole stream of cash flows is considered which makes the result more feasible and

that can be trusted for decision making for selection of the project.

The net present value can be seen as the addition to the wealth of shareholders. The

criterion of NPV is thus in conformity with basic financial objectives.

The NPV uses the discounted cash flows i.e., expresses cash flows in terms of current

rupees. The NPVs of different projects therefore can be compared. It implies that each

project can be evaluated independent of others on its own merit (Rivai, 2021).

Limitations of NPV

It involves difficult calculations which takes usually longer time period.

The application of this method necessitates forecasting cash flows and the discount rate.

Thus, accuracy of NPV depends on accurate estimation of these two factors which may

be quite difficult in practice.

The decision under NPV method is based on absolute measure. It ignores the difference

in initial outflows, size of different proposals etc. while evaluating mutually exclusive

projects.

Question No 3

a) Calculation of share price of Carport Plc if company does not change its current dividend

policy:

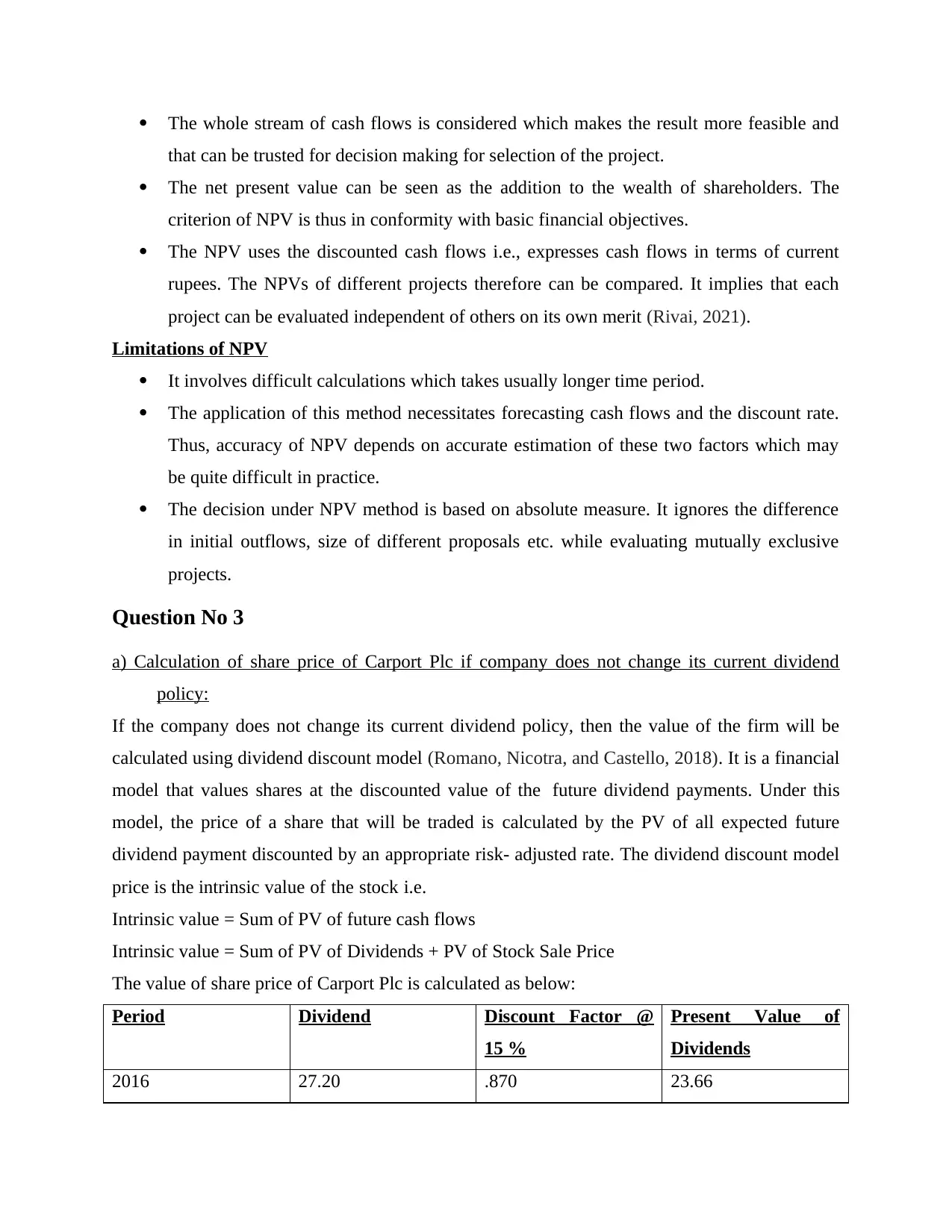

If the company does not change its current dividend policy, then the value of the firm will be

calculated using dividend discount model (Romano, Nicotra, and Castello, 2018). It is a financial

model that values shares at the discounted value of the future dividend payments. Under this

model, the price of a share that will be traded is calculated by the PV of all expected future

dividend payment discounted by an appropriate risk- adjusted rate. The dividend discount model

price is the intrinsic value of the stock i.e.

Intrinsic value = Sum of PV of future cash flows

Intrinsic value = Sum of PV of Dividends + PV of Stock Sale Price

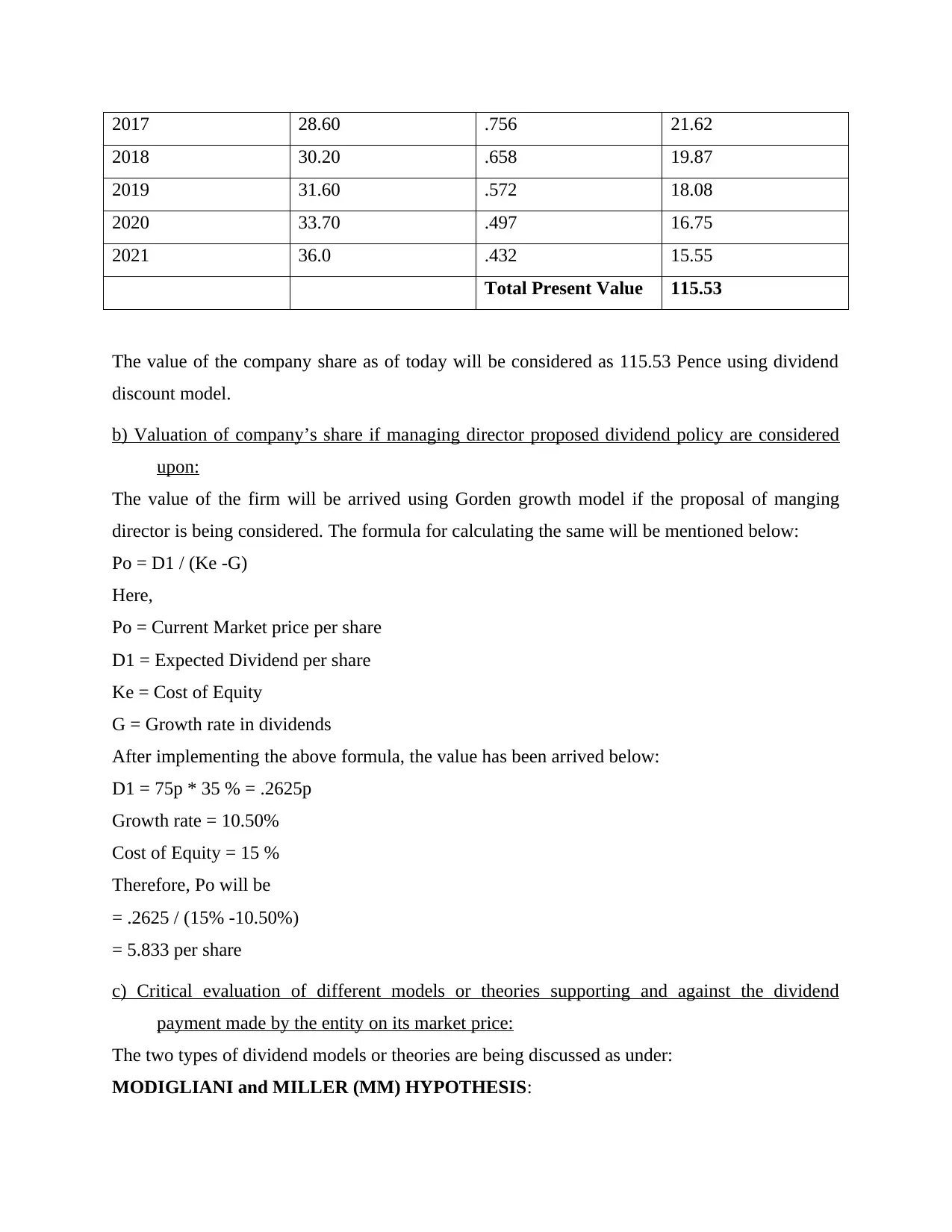

The value of share price of Carport Plc is calculated as below:

Period Dividend Discount Factor @

15 %

Present Value of

Dividends

2016 27.20 .870 23.66

that can be trusted for decision making for selection of the project.

The net present value can be seen as the addition to the wealth of shareholders. The

criterion of NPV is thus in conformity with basic financial objectives.

The NPV uses the discounted cash flows i.e., expresses cash flows in terms of current

rupees. The NPVs of different projects therefore can be compared. It implies that each

project can be evaluated independent of others on its own merit (Rivai, 2021).

Limitations of NPV

It involves difficult calculations which takes usually longer time period.

The application of this method necessitates forecasting cash flows and the discount rate.

Thus, accuracy of NPV depends on accurate estimation of these two factors which may

be quite difficult in practice.

The decision under NPV method is based on absolute measure. It ignores the difference

in initial outflows, size of different proposals etc. while evaluating mutually exclusive

projects.

Question No 3

a) Calculation of share price of Carport Plc if company does not change its current dividend

policy:

If the company does not change its current dividend policy, then the value of the firm will be

calculated using dividend discount model (Romano, Nicotra, and Castello, 2018). It is a financial

model that values shares at the discounted value of the future dividend payments. Under this

model, the price of a share that will be traded is calculated by the PV of all expected future

dividend payment discounted by an appropriate risk- adjusted rate. The dividend discount model

price is the intrinsic value of the stock i.e.

Intrinsic value = Sum of PV of future cash flows

Intrinsic value = Sum of PV of Dividends + PV of Stock Sale Price

The value of share price of Carport Plc is calculated as below:

Period Dividend Discount Factor @

15 %

Present Value of

Dividends

2016 27.20 .870 23.66

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 28.60 .756 21.62

2018 30.20 .658 19.87

2019 31.60 .572 18.08

2020 33.70 .497 16.75

2021 36.0 .432 15.55

Total Present Value 115.53

The value of the company share as of today will be considered as 115.53 Pence using dividend

discount model.

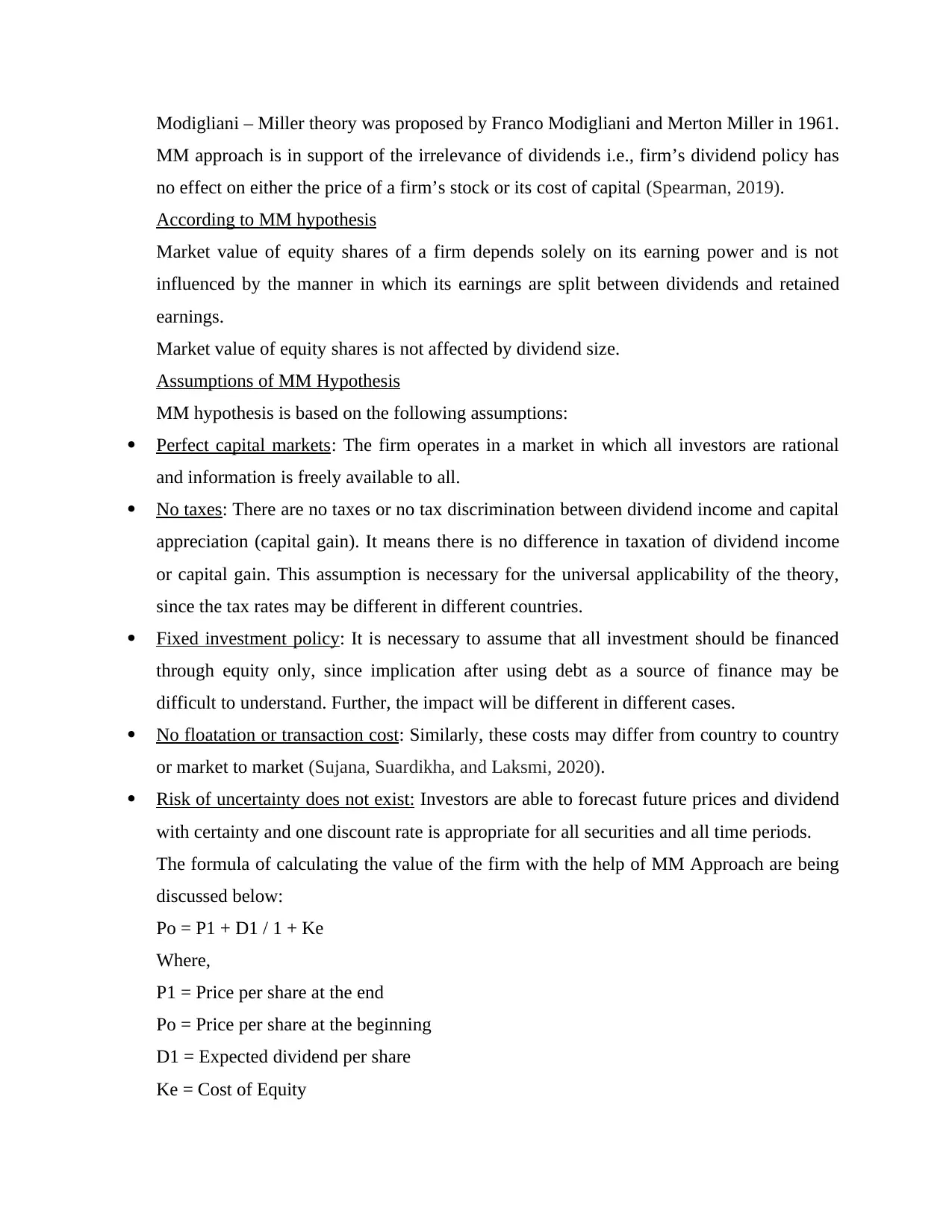

b) Valuation of company’s share if managing director proposed dividend policy are considered

upon:

The value of the firm will be arrived using Gorden growth model if the proposal of manging

director is being considered. The formula for calculating the same will be mentioned below:

Po = D1 / (Ke -G)

Here,

Po = Current Market price per share

D1 = Expected Dividend per share

Ke = Cost of Equity

G = Growth rate in dividends

After implementing the above formula, the value has been arrived below:

D1 = 75p * 35 % = .2625p

Growth rate = 10.50%

Cost of Equity = 15 %

Therefore, Po will be

= .2625 / (15% -10.50%)

= 5.833 per share

c) Critical evaluation of different models or theories supporting and against the dividend

payment made by the entity on its market price:

The two types of dividend models or theories are being discussed as under:

MODIGLIANI and MILLER (MM) HYPOTHESIS:

2018 30.20 .658 19.87

2019 31.60 .572 18.08

2020 33.70 .497 16.75

2021 36.0 .432 15.55

Total Present Value 115.53

The value of the company share as of today will be considered as 115.53 Pence using dividend

discount model.

b) Valuation of company’s share if managing director proposed dividend policy are considered

upon:

The value of the firm will be arrived using Gorden growth model if the proposal of manging

director is being considered. The formula for calculating the same will be mentioned below:

Po = D1 / (Ke -G)

Here,

Po = Current Market price per share

D1 = Expected Dividend per share

Ke = Cost of Equity

G = Growth rate in dividends

After implementing the above formula, the value has been arrived below:

D1 = 75p * 35 % = .2625p

Growth rate = 10.50%

Cost of Equity = 15 %

Therefore, Po will be

= .2625 / (15% -10.50%)

= 5.833 per share

c) Critical evaluation of different models or theories supporting and against the dividend

payment made by the entity on its market price:

The two types of dividend models or theories are being discussed as under:

MODIGLIANI and MILLER (MM) HYPOTHESIS:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Modigliani – Miller theory was proposed by Franco Modigliani and Merton Miller in 1961.

MM approach is in support of the irrelevance of dividends i.e., firm’s dividend policy has

no effect on either the price of a firm’s stock or its cost of capital (Spearman, 2019).

According to MM hypothesis

Market value of equity shares of a firm depends solely on its earning power and is not

influenced by the manner in which its earnings are split between dividends and retained

earnings.

Market value of equity shares is not affected by dividend size.

Assumptions of MM Hypothesis

MM hypothesis is based on the following assumptions:

Perfect capital markets: The firm operates in a market in which all investors are rational

and information is freely available to all.

No taxes: There are no taxes or no tax discrimination between dividend income and capital

appreciation (capital gain). It means there is no difference in taxation of dividend income

or capital gain. This assumption is necessary for the universal applicability of the theory,

since the tax rates may be different in different countries.

Fixed investment policy: It is necessary to assume that all investment should be financed

through equity only, since implication after using debt as a source of finance may be

difficult to understand. Further, the impact will be different in different cases.

No floatation or transaction cost: Similarly, these costs may differ from country to country

or market to market (Sujana, Suardikha, and Laksmi, 2020).

Risk of uncertainty does not exist: Investors are able to forecast future prices and dividend

with certainty and one discount rate is appropriate for all securities and all time periods.

The formula of calculating the value of the firm with the help of MM Approach are being

discussed below:

Po = P1 + D1 / 1 + Ke

Where,

P1 = Price per share at the end

Po = Price per share at the beginning

D1 = Expected dividend per share

Ke = Cost of Equity

MM approach is in support of the irrelevance of dividends i.e., firm’s dividend policy has

no effect on either the price of a firm’s stock or its cost of capital (Spearman, 2019).

According to MM hypothesis

Market value of equity shares of a firm depends solely on its earning power and is not

influenced by the manner in which its earnings are split between dividends and retained

earnings.

Market value of equity shares is not affected by dividend size.

Assumptions of MM Hypothesis

MM hypothesis is based on the following assumptions:

Perfect capital markets: The firm operates in a market in which all investors are rational

and information is freely available to all.

No taxes: There are no taxes or no tax discrimination between dividend income and capital

appreciation (capital gain). It means there is no difference in taxation of dividend income

or capital gain. This assumption is necessary for the universal applicability of the theory,

since the tax rates may be different in different countries.

Fixed investment policy: It is necessary to assume that all investment should be financed

through equity only, since implication after using debt as a source of finance may be

difficult to understand. Further, the impact will be different in different cases.

No floatation or transaction cost: Similarly, these costs may differ from country to country

or market to market (Sujana, Suardikha, and Laksmi, 2020).

Risk of uncertainty does not exist: Investors are able to forecast future prices and dividend

with certainty and one discount rate is appropriate for all securities and all time periods.

The formula of calculating the value of the firm with the help of MM Approach are being

discussed below:

Po = P1 + D1 / 1 + Ke

Where,

P1 = Price per share at the end

Po = Price per share at the beginning

D1 = Expected dividend per share

Ke = Cost of Equity

Advantages of MM Hypothesis

This model is logically consistent.

It provides a satisfactory framework on dividend policy with the concept of Arbitrage

process.

Limitations of MM Hypothesis

Validity of various assumptions is questionable.

This model may not be valid under uncertainty (Vavrek, Papcunová, and Tej, 2020).

WALTER’S MODEL

Assumptions of Walter’s Model

Walter’s approach is based on the following assumptions:

All investment proposals of the firm are to be financed through retained earnings only.

‘r’ rate of return & ‘Ke’ cost of capital are constant.

Perfect capital markets: The firm operates in a market in which all investors are rational

and information is freely available to all.

No taxes or no tax discrimination between dividend income and capital appreciation

(capital gain). It means there is no difference in taxation of dividend income or capital

gain. This assumption is necessary for the universal applicability of the theory, since, the

tax rates may be different in different countries.

No floatation or transaction cost: Similarly, these costs may differ country to country or

market to market.

The firm has perpetual life

The formula for calculate price of the firm by using the Walter model will be:

Market Price = D + r / Ke (E – D) / Ke

Here,

D = Dividend per share

R = Return on investment

E = Earnings per share

Ke = Cost of Equity

Advantages of Walter’s Model

The formula is simple to understand and easy to compute.

It can envisage different possible market prices in different situations and considers

internal rate of return, market capitalisation rate and dividend pay-out ratio in the

determination of market value of shares.

This model is logically consistent.

It provides a satisfactory framework on dividend policy with the concept of Arbitrage

process.

Limitations of MM Hypothesis

Validity of various assumptions is questionable.

This model may not be valid under uncertainty (Vavrek, Papcunová, and Tej, 2020).

WALTER’S MODEL

Assumptions of Walter’s Model

Walter’s approach is based on the following assumptions:

All investment proposals of the firm are to be financed through retained earnings only.

‘r’ rate of return & ‘Ke’ cost of capital are constant.

Perfect capital markets: The firm operates in a market in which all investors are rational

and information is freely available to all.

No taxes or no tax discrimination between dividend income and capital appreciation

(capital gain). It means there is no difference in taxation of dividend income or capital

gain. This assumption is necessary for the universal applicability of the theory, since, the

tax rates may be different in different countries.

No floatation or transaction cost: Similarly, these costs may differ country to country or

market to market.

The firm has perpetual life

The formula for calculate price of the firm by using the Walter model will be:

Market Price = D + r / Ke (E – D) / Ke

Here,

D = Dividend per share

R = Return on investment

E = Earnings per share

Ke = Cost of Equity

Advantages of Walter’s Model

The formula is simple to understand and easy to compute.

It can envisage different possible market prices in different situations and considers

internal rate of return, market capitalisation rate and dividend pay-out ratio in the

determination of market value of shares.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.