Investment Appraisal Techniques and Liquidity Ratios for Company A

VerifiedAdded on 2023/05/28

|12

|2339

|77

AI Summary

This article discusses investment appraisal techniques and liquidity ratios for Company A. It provides advantages and disadvantages of each investment appraisal method and suggests ways to improve the liquidity ratios. The article also identifies cash flow and overtrading problems faced by the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE 0

Finance

Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE 1

Contents

PART A......................................................................................................................................2

PART B......................................................................................................................................7

References................................................................................................................................11

Contents

PART A......................................................................................................................................2

PART B......................................................................................................................................7

References................................................................................................................................11

FINANCE 2

PART A

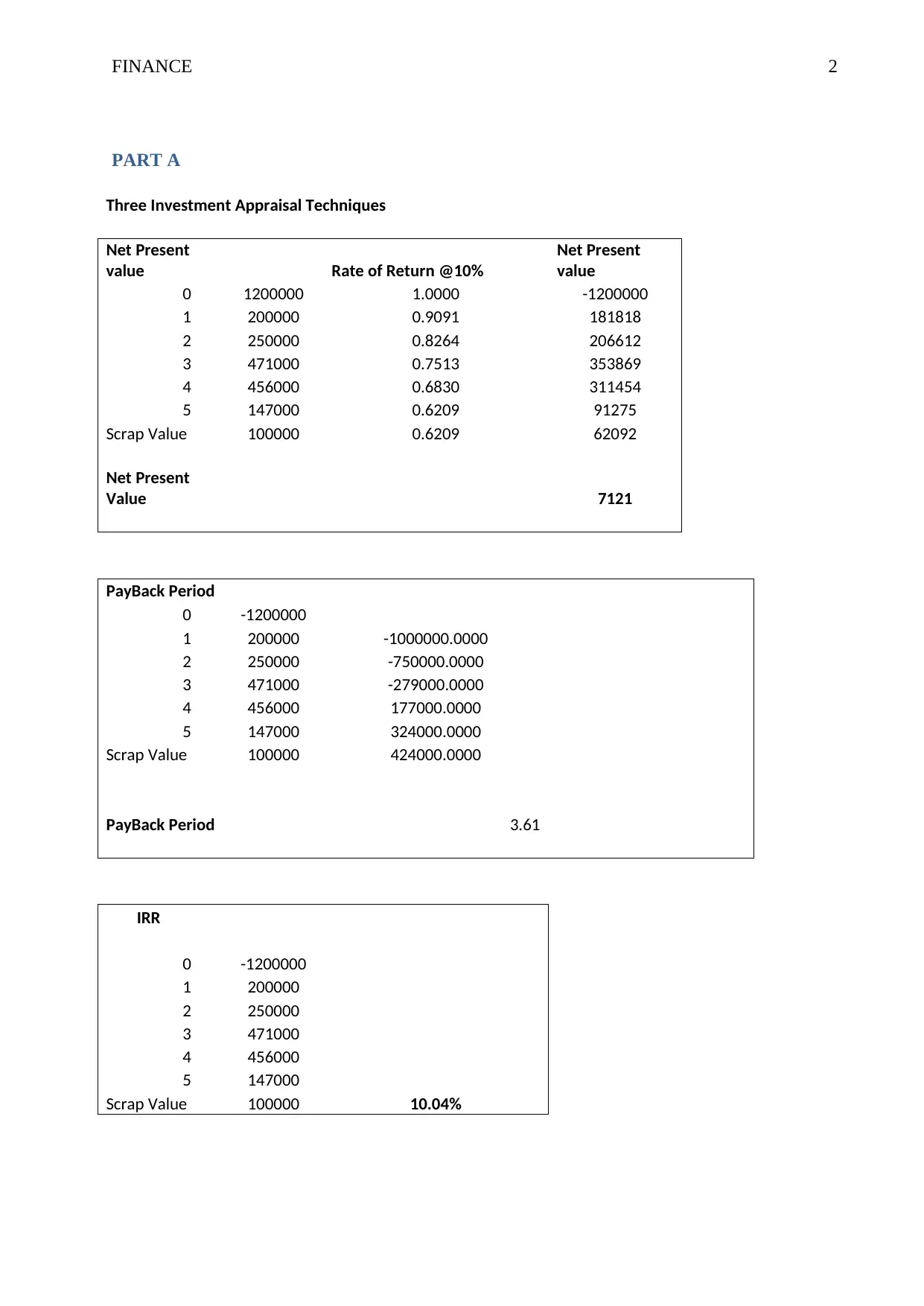

Three Investment Appraisal Techniques

Net Present

value Rate of Return @10%

Net Present

value

0 1200000 1.0000 -1200000

1 200000 0.9091 181818

2 250000 0.8264 206612

3 471000 0.7513 353869

4 456000 0.6830 311454

5 147000 0.6209 91275

Scrap Value 100000 0.6209 62092

Net Present

Value 7121

PayBack Period

0 -1200000

1 200000 -1000000.0000

2 250000 -750000.0000

3 471000 -279000.0000

4 456000 177000.0000

5 147000 324000.0000

Scrap Value 100000 424000.0000

PayBack Period 3.61

IRR

0 -1200000

1 200000

2 250000

3 471000

4 456000

5 147000

Scrap Value 100000 10.04%

PART A

Three Investment Appraisal Techniques

Net Present

value Rate of Return @10%

Net Present

value

0 1200000 1.0000 -1200000

1 200000 0.9091 181818

2 250000 0.8264 206612

3 471000 0.7513 353869

4 456000 0.6830 311454

5 147000 0.6209 91275

Scrap Value 100000 0.6209 62092

Net Present

Value 7121

PayBack Period

0 -1200000

1 200000 -1000000.0000

2 250000 -750000.0000

3 471000 -279000.0000

4 456000 177000.0000

5 147000 324000.0000

Scrap Value 100000 424000.0000

PayBack Period 3.61

IRR

0 -1200000

1 200000

2 250000

3 471000

4 456000

5 147000

Scrap Value 100000 10.04%

FINANCE 3

It is advised to company to buy the project because the IRR is more than the present rate, the

payback period is 3.61 and in comparison to the 4 years and the net present value is positive

therefore the project can be bought. The other relevant considerations that are used in

decision making of the company are adjusted present value, relative rankings of the projects

and the modified internal rate of return and apart from this the factors affecting the company

(Osborne, 2010).

Advantages of investment appraisal methods

Net Present value method

Under the net present value method the main motive of the firm is to create the wealth with

the help of the existing and the future resources to produce the goods and the services. It is

basically the difference between the present value of the inflow of the cash and the outflow of

cash. This method is used to determine the profitability of the projected investment (Setiawan

and Fahrurrozi, 2017).

The advantages of using the net present value to determine the viability of the business

are as follows.

The most obvious advantage of the net present value method is the consideration of

the value of the dollar. According to the NPV method the value of the future dollar is

less than a dollar today. NPV basically gives importance to the time value of money.

Secondly the NPV method also deals with the creation of the value of the investment

for the potential investors and by how much in terms of the dollars. This helps in

maximisation of the value of the firm (Schwarzbichler, Steiner and Turnheim, 2018)

Thirdly it recognises the total merits that are arising from the proposals over the life

time. Since this method is particularly helpful in selection of the mutually exclusive

It is advised to company to buy the project because the IRR is more than the present rate, the

payback period is 3.61 and in comparison to the 4 years and the net present value is positive

therefore the project can be bought. The other relevant considerations that are used in

decision making of the company are adjusted present value, relative rankings of the projects

and the modified internal rate of return and apart from this the factors affecting the company

(Osborne, 2010).

Advantages of investment appraisal methods

Net Present value method

Under the net present value method the main motive of the firm is to create the wealth with

the help of the existing and the future resources to produce the goods and the services. It is

basically the difference between the present value of the inflow of the cash and the outflow of

cash. This method is used to determine the profitability of the projected investment (Setiawan

and Fahrurrozi, 2017).

The advantages of using the net present value to determine the viability of the business

are as follows.

The most obvious advantage of the net present value method is the consideration of

the value of the dollar. According to the NPV method the value of the future dollar is

less than a dollar today. NPV basically gives importance to the time value of money.

Secondly the NPV method also deals with the creation of the value of the investment

for the potential investors and by how much in terms of the dollars. This helps in

maximisation of the value of the firm (Schwarzbichler, Steiner and Turnheim, 2018)

Thirdly it recognises the total merits that are arising from the proposals over the life

time. Since this method is particularly helpful in selection of the mutually exclusive

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE 4

projects there are many alternatives available to create the new opportunities for the

investor.

The NPV method assists in the wealth maximisation of the shareholders.

Demerits

The biggest advantage of this method is the cost of capital is not the accurate cost of capital.

Since the cost of capital vary between too low and too high the opportunities for the

investments also vary and from making the suboptimal investments to forgoing too many

good investments Christersson, Vimpari and Junnila, 2015).

When the size of the two projects is different the application of the NPV value fails.

Since the size of the output is mostly determined by the size of the input the

comparison becomes impossible for the investors.

The appropriate discounted rate is difficult to calculate and becomes complex in

nature. This method may not give the satisfactory results and the shorter economic life

of the project does is not associated with much of the importance.

Payback Period

The payback period of an investment is determined in the number of years. This method

generally recognises the return of the original initial investment in a particular project. When

the payback period is calculated, the cash inflows from the project are equivalent the

outflows of the same. The length of the time the process takes is ultimately the payback

period for the investment made (Kaplan and Atkinson, 2015).

Following are some of the advantages of the payback period.

projects there are many alternatives available to create the new opportunities for the

investor.

The NPV method assists in the wealth maximisation of the shareholders.

Demerits

The biggest advantage of this method is the cost of capital is not the accurate cost of capital.

Since the cost of capital vary between too low and too high the opportunities for the

investments also vary and from making the suboptimal investments to forgoing too many

good investments Christersson, Vimpari and Junnila, 2015).

When the size of the two projects is different the application of the NPV value fails.

Since the size of the output is mostly determined by the size of the input the

comparison becomes impossible for the investors.

The appropriate discounted rate is difficult to calculate and becomes complex in

nature. This method may not give the satisfactory results and the shorter economic life

of the project does is not associated with much of the importance.

Payback Period

The payback period of an investment is determined in the number of years. This method

generally recognises the return of the original initial investment in a particular project. When

the payback period is calculated, the cash inflows from the project are equivalent the

outflows of the same. The length of the time the process takes is ultimately the payback

period for the investment made (Kaplan and Atkinson, 2015).

Following are some of the advantages of the payback period.

FINANCE 5

This is the simplest form of method of the investment appraisal. It is easy to

understand and is most cores to the business which lacks the appropriate skills and is

necessary to fulfil the other techniques as well.

The companies are compelled to make investments in the projects that are off shortest

payback period.

This method is most suitable when the near future is quite uncertain. The risk of the

project is determined by payback period of the project. Higher the payback period,

higher is the risk, lower the payback period, the risk is cumulatively less. Therefore it

exhibits the direct relationship (Copiello, 2016)

. After discussing the pros of the company there are some cons as well that are

outlined below.

Payback period requires the secondary comparison factor to make a relevance of it. It

becomes impossible to decode whether the investment shall be accepted or rejected

when the payback period is compared to the arbitrary managerial target.

This method is a reliable measure of liquidity more rather than the profitability. This

method ignore the generation of cash beyond the payback period. Therefore it fails to

consider the entire life of the project (Santandrea, Sironi, Grassi and Giorgino, 2017)

IRR

Under the IRR method the rate is in terms of the percentage that organises the capital

investment appraisals and makes the future cash flows and the cost of capital equivalent. It is

the return equating the net cash flows with the initial outlay. Also the rate of computing the

IRR depends on rates of the bank and the cost of the funds often called as the personal

discounting rate (Patrick and French, 2016)

.

This is the simplest form of method of the investment appraisal. It is easy to

understand and is most cores to the business which lacks the appropriate skills and is

necessary to fulfil the other techniques as well.

The companies are compelled to make investments in the projects that are off shortest

payback period.

This method is most suitable when the near future is quite uncertain. The risk of the

project is determined by payback period of the project. Higher the payback period,

higher is the risk, lower the payback period, the risk is cumulatively less. Therefore it

exhibits the direct relationship (Copiello, 2016)

. After discussing the pros of the company there are some cons as well that are

outlined below.

Payback period requires the secondary comparison factor to make a relevance of it. It

becomes impossible to decode whether the investment shall be accepted or rejected

when the payback period is compared to the arbitrary managerial target.

This method is a reliable measure of liquidity more rather than the profitability. This

method ignore the generation of cash beyond the payback period. Therefore it fails to

consider the entire life of the project (Santandrea, Sironi, Grassi and Giorgino, 2017)

IRR

Under the IRR method the rate is in terms of the percentage that organises the capital

investment appraisals and makes the future cash flows and the cost of capital equivalent. It is

the return equating the net cash flows with the initial outlay. Also the rate of computing the

IRR depends on rates of the bank and the cost of the funds often called as the personal

discounting rate (Patrick and French, 2016)

.

FINANCE 6

Following are the merits of the IRR method

This method takes into consideration the time value of money.

Both the indirect and the direct cash flows are considered in this method

Lastly this method is the easiest method to operate and understand and thereafter the

implications of these methods are higher in comparison to the other methods.

Demerits of IRR

IRR produces the variety of rates which at times can be confusing.

Projects selected based on the IRR may or may not be profitable

The fluctuating interest rates are ignored completely.

Methods which are widely used in industry are outlined below

The most commonly used method of the appraisal of the investment which is used by the

industry is the payback period. This method is mostly common for the energy efficient

investments and the operational ones followed by the IRR and the NPV methods. The main

reason behind the utilisation of this method in the industry is the simplicity in terms of the

voluminous investments. This helps the organisations in ranking of the projects according to

the ability of the repayment of the money in the quickest manner. The control of the cash is

usually done with the help of this method (Osborne and O'Reilly, 2015)

PART B

Liquidity Ratios

Current ratio 2017 2016

Following are the merits of the IRR method

This method takes into consideration the time value of money.

Both the indirect and the direct cash flows are considered in this method

Lastly this method is the easiest method to operate and understand and thereafter the

implications of these methods are higher in comparison to the other methods.

Demerits of IRR

IRR produces the variety of rates which at times can be confusing.

Projects selected based on the IRR may or may not be profitable

The fluctuating interest rates are ignored completely.

Methods which are widely used in industry are outlined below

The most commonly used method of the appraisal of the investment which is used by the

industry is the payback period. This method is mostly common for the energy efficient

investments and the operational ones followed by the IRR and the NPV methods. The main

reason behind the utilisation of this method in the industry is the simplicity in terms of the

voluminous investments. This helps the organisations in ranking of the projects according to

the ability of the repayment of the money in the quickest manner. The control of the cash is

usually done with the help of this method (Osborne and O'Reilly, 2015)

PART B

Liquidity Ratios

Current ratio 2017 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 7

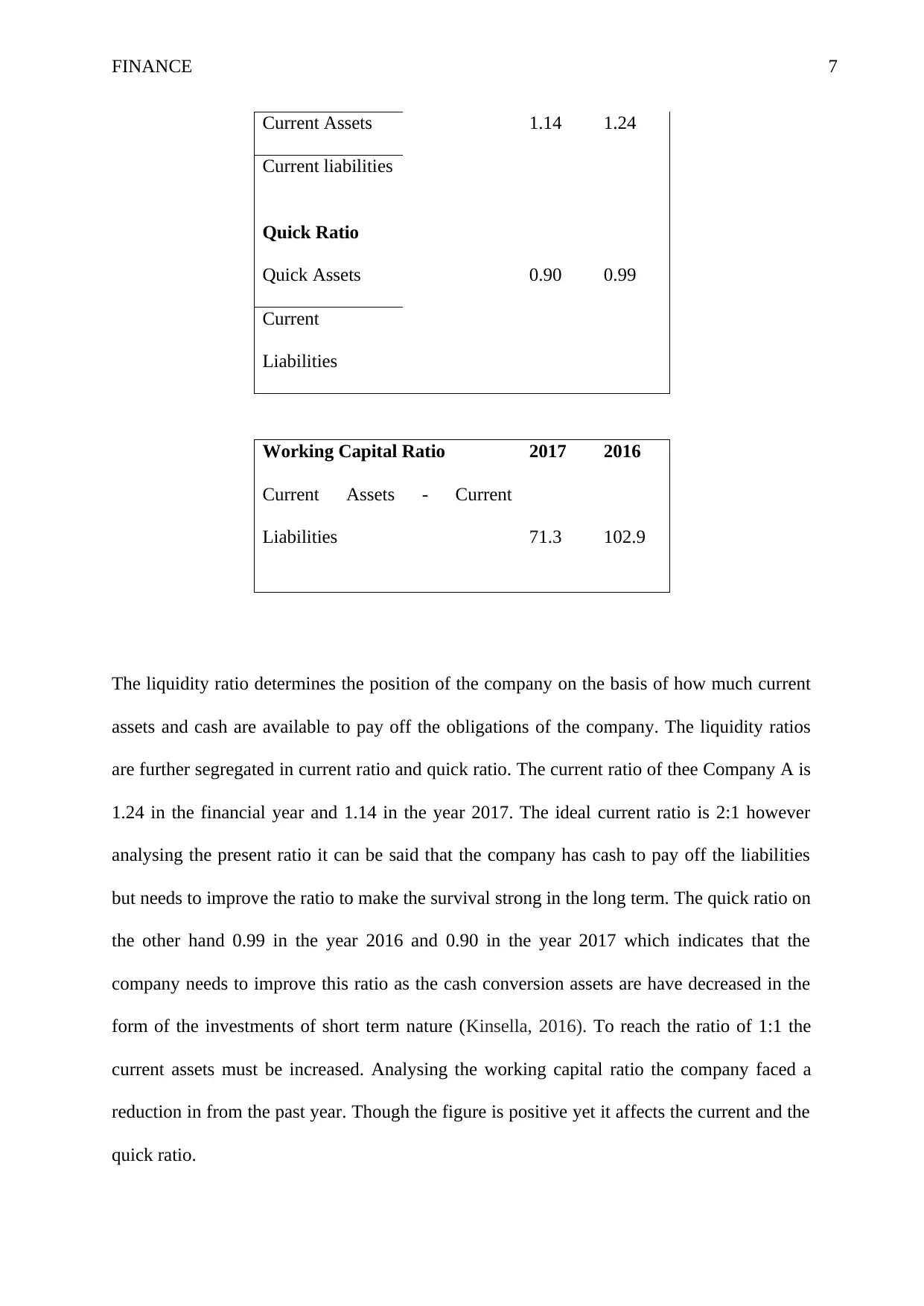

Current Assets 1.14 1.24

Current liabilities

Quick Ratio

Quick Assets 0.90 0.99

Current

Liabilities

Working Capital Ratio 2017 2016

Current Assets - Current

Liabilities 71.3 102.9

The liquidity ratio determines the position of the company on the basis of how much current

assets and cash are available to pay off the obligations of the company. The liquidity ratios

are further segregated in current ratio and quick ratio. The current ratio of thee Company A is

1.24 in the financial year and 1.14 in the year 2017. The ideal current ratio is 2:1 however

analysing the present ratio it can be said that the company has cash to pay off the liabilities

but needs to improve the ratio to make the survival strong in the long term. The quick ratio on

the other hand 0.99 in the year 2016 and 0.90 in the year 2017 which indicates that the

company needs to improve this ratio as the cash conversion assets are have decreased in the

form of the investments of short term nature (Kinsella, 2016). To reach the ratio of 1:1 the

current assets must be increased. Analysing the working capital ratio the company faced a

reduction in from the past year. Though the figure is positive yet it affects the current and the

quick ratio.

Current Assets 1.14 1.24

Current liabilities

Quick Ratio

Quick Assets 0.90 0.99

Current

Liabilities

Working Capital Ratio 2017 2016

Current Assets - Current

Liabilities 71.3 102.9

The liquidity ratio determines the position of the company on the basis of how much current

assets and cash are available to pay off the obligations of the company. The liquidity ratios

are further segregated in current ratio and quick ratio. The current ratio of thee Company A is

1.24 in the financial year and 1.14 in the year 2017. The ideal current ratio is 2:1 however

analysing the present ratio it can be said that the company has cash to pay off the liabilities

but needs to improve the ratio to make the survival strong in the long term. The quick ratio on

the other hand 0.99 in the year 2016 and 0.90 in the year 2017 which indicates that the

company needs to improve this ratio as the cash conversion assets are have decreased in the

form of the investments of short term nature (Kinsella, 2016). To reach the ratio of 1:1 the

current assets must be increased. Analysing the working capital ratio the company faced a

reduction in from the past year. Though the figure is positive yet it affects the current and the

quick ratio.

FINANCE 8

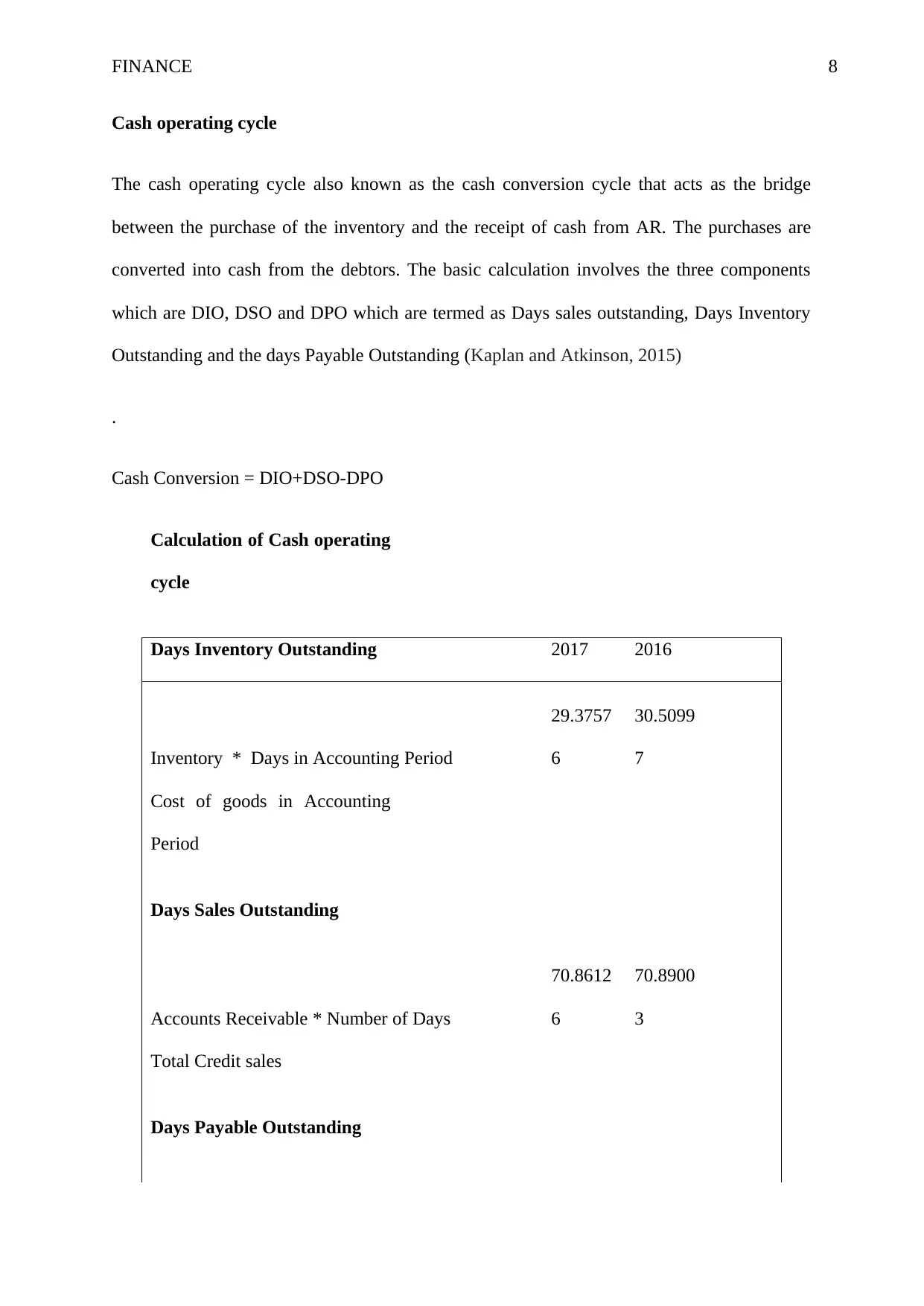

Cash operating cycle

The cash operating cycle also known as the cash conversion cycle that acts as the bridge

between the purchase of the inventory and the receipt of cash from AR. The purchases are

converted into cash from the debtors. The basic calculation involves the three components

which are DIO, DSO and DPO which are termed as Days sales outstanding, Days Inventory

Outstanding and the days Payable Outstanding (Kaplan and Atkinson, 2015)

.

Cash Conversion = DIO+DSO-DPO

Calculation of Cash operating

cycle

Days Inventory Outstanding 2017 2016

Inventory * Days in Accounting Period

29.3757

6

30.5099

7

Cost of goods in Accounting

Period

Days Sales Outstanding

Accounts Receivable * Number of Days

70.8612

6

70.8900

3

Total Credit sales

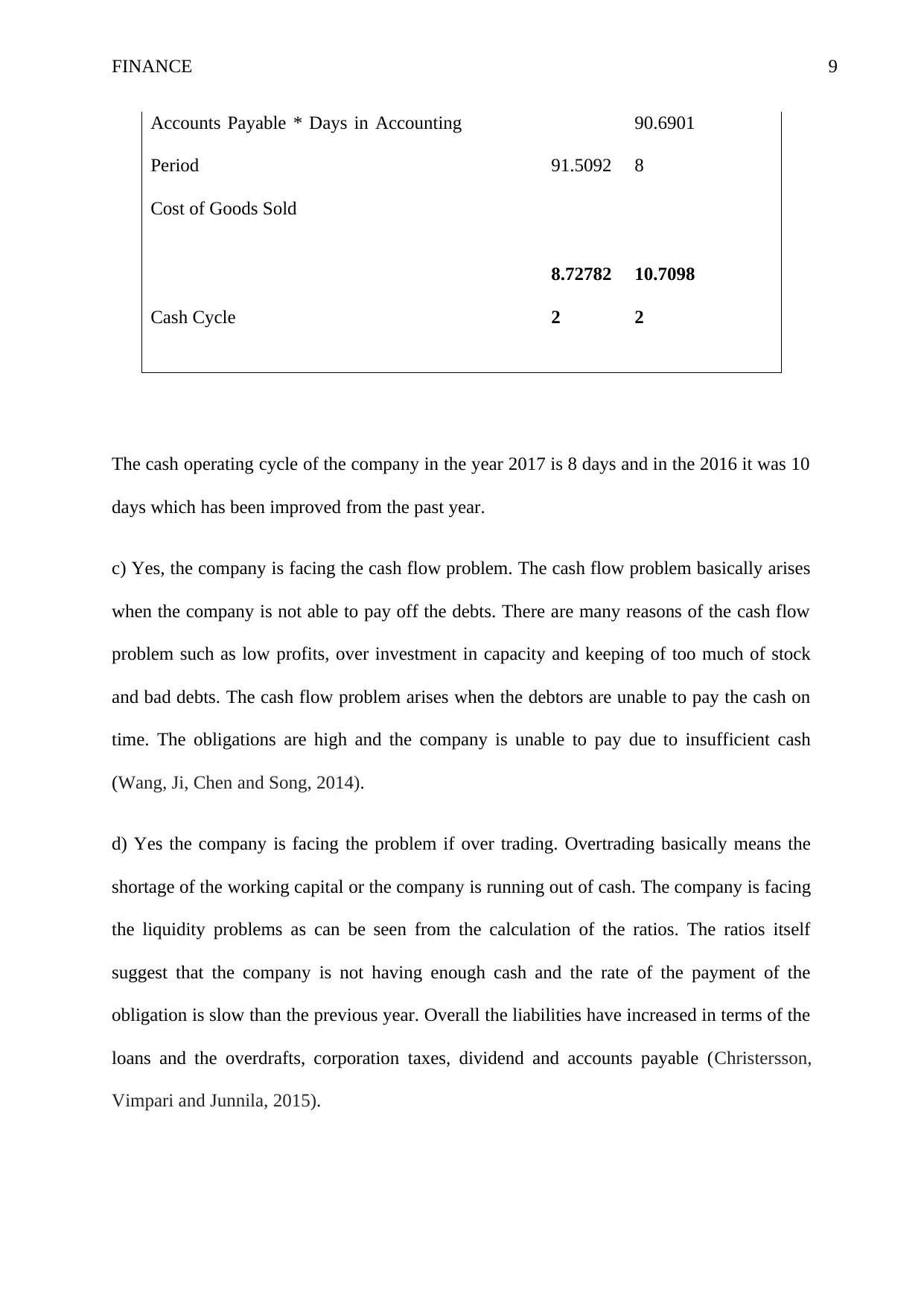

Days Payable Outstanding

Cash operating cycle

The cash operating cycle also known as the cash conversion cycle that acts as the bridge

between the purchase of the inventory and the receipt of cash from AR. The purchases are

converted into cash from the debtors. The basic calculation involves the three components

which are DIO, DSO and DPO which are termed as Days sales outstanding, Days Inventory

Outstanding and the days Payable Outstanding (Kaplan and Atkinson, 2015)

.

Cash Conversion = DIO+DSO-DPO

Calculation of Cash operating

cycle

Days Inventory Outstanding 2017 2016

Inventory * Days in Accounting Period

29.3757

6

30.5099

7

Cost of goods in Accounting

Period

Days Sales Outstanding

Accounts Receivable * Number of Days

70.8612

6

70.8900

3

Total Credit sales

Days Payable Outstanding

FINANCE 9

Accounts Payable * Days in Accounting

Period 91.5092

90.6901

8

Cost of Goods Sold

Cash Cycle

8.72782

2

10.7098

2

The cash operating cycle of the company in the year 2017 is 8 days and in the 2016 it was 10

days which has been improved from the past year.

c) Yes, the company is facing the cash flow problem. The cash flow problem basically arises

when the company is not able to pay off the debts. There are many reasons of the cash flow

problem such as low profits, over investment in capacity and keeping of too much of stock

and bad debts. The cash flow problem arises when the debtors are unable to pay the cash on

time. The obligations are high and the company is unable to pay due to insufficient cash

(Wang, Ji, Chen and Song, 2014).

d) Yes the company is facing the problem if over trading. Overtrading basically means the

shortage of the working capital or the company is running out of cash. The company is facing

the liquidity problems as can be seen from the calculation of the ratios. The ratios itself

suggest that the company is not having enough cash and the rate of the payment of the

obligation is slow than the previous year. Overall the liabilities have increased in terms of the

loans and the overdrafts, corporation taxes, dividend and accounts payable (Christersson,

Vimpari and Junnila, 2015).

Accounts Payable * Days in Accounting

Period 91.5092

90.6901

8

Cost of Goods Sold

Cash Cycle

8.72782

2

10.7098

2

The cash operating cycle of the company in the year 2017 is 8 days and in the 2016 it was 10

days which has been improved from the past year.

c) Yes, the company is facing the cash flow problem. The cash flow problem basically arises

when the company is not able to pay off the debts. There are many reasons of the cash flow

problem such as low profits, over investment in capacity and keeping of too much of stock

and bad debts. The cash flow problem arises when the debtors are unable to pay the cash on

time. The obligations are high and the company is unable to pay due to insufficient cash

(Wang, Ji, Chen and Song, 2014).

d) Yes the company is facing the problem if over trading. Overtrading basically means the

shortage of the working capital or the company is running out of cash. The company is facing

the liquidity problems as can be seen from the calculation of the ratios. The ratios itself

suggest that the company is not having enough cash and the rate of the payment of the

obligation is slow than the previous year. Overall the liabilities have increased in terms of the

loans and the overdrafts, corporation taxes, dividend and accounts payable (Christersson,

Vimpari and Junnila, 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE 10

References

Ben-Horin, M. and Kroll, Y., (2017) A simple intuitive NPV-IRR consistent ranking. The

Quarterly Review of Economics and Finance, 66, pp.108-114.

Christersson, M., Vimpari, J. and Junnila, S., (2015) Assessment of financial potential of real

estate energy efficiency investments–a discounted cash flow approach. Sustainable Cities and

Society, 18, pp.66-73.

Copiello, S., (2016) A Discounted Cash Flow variant to detect the optimal amount of

additional burdens in Public-Private Partnership transactions. MethodsX, 3, pp.195-204.

Del Fabbro, B., Valentinčič, A. and Gubina, A.F., (2016) An adequate required rate of return

for grid-connected PV systems. Solar Energy, 132, pp.73-83.

Kaplan, R.S. and Atkinson, A.A., (2015) Advanced management accounting. PHI Learning.

Kinsella, J.J., (2016) Ratio metric current measurement. U.S. Patent Application 14/971,939.

Lane, K. and Rosewall, T., (2015) Firms’ investment decisions and interest rates. Reserve

Bank of Australia Bulletin. June quarter, pp.1-7.

Osborne, M. and O'Reilly, E., (2015) A model illustrating multiple interest rate analysis

(MIRA).

Osborne, M.J., (2010) A resolution to the NPV–IRR debate?. The Quarterly Review of

Economics and Finance, 50(2), pp.234-239.

Patrick, M. and French, N., (2016) The internal rate of return (IRR): projections, benchmarks

and pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

References

Ben-Horin, M. and Kroll, Y., (2017) A simple intuitive NPV-IRR consistent ranking. The

Quarterly Review of Economics and Finance, 66, pp.108-114.

Christersson, M., Vimpari, J. and Junnila, S., (2015) Assessment of financial potential of real

estate energy efficiency investments–a discounted cash flow approach. Sustainable Cities and

Society, 18, pp.66-73.

Copiello, S., (2016) A Discounted Cash Flow variant to detect the optimal amount of

additional burdens in Public-Private Partnership transactions. MethodsX, 3, pp.195-204.

Del Fabbro, B., Valentinčič, A. and Gubina, A.F., (2016) An adequate required rate of return

for grid-connected PV systems. Solar Energy, 132, pp.73-83.

Kaplan, R.S. and Atkinson, A.A., (2015) Advanced management accounting. PHI Learning.

Kinsella, J.J., (2016) Ratio metric current measurement. U.S. Patent Application 14/971,939.

Lane, K. and Rosewall, T., (2015) Firms’ investment decisions and interest rates. Reserve

Bank of Australia Bulletin. June quarter, pp.1-7.

Osborne, M. and O'Reilly, E., (2015) A model illustrating multiple interest rate analysis

(MIRA).

Osborne, M.J., (2010) A resolution to the NPV–IRR debate?. The Quarterly Review of

Economics and Finance, 50(2), pp.234-239.

Patrick, M. and French, N., (2016) The internal rate of return (IRR): projections, benchmarks

and pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

FINANCE 11

Santandrea, M., Sironi, A., Grassi, L. and Giorgino, M., (2017) Concentration risk and

internal rate of return: Evidence from the infrastructure equity market. International Journal

of Project Management, 35(3), pp.241-251.

Schwarzbichler, M., Steiner, C. and Turnheim, D., (2018) Economic Portfolio Decisions.

In Financial Steering (pp. 253-264). Springer, Cham.

Setiawan, D. and Fahrurrozi, N.R., (2017) November. Feasibility analysis with capital

budgeting backbone network fiber optic cable west palapa ring. In Broadband

Communication, Wireless Sensors and Powering (BCWSP), 2017 International Conference

on (pp. 1-4). IEEE.

Wang, Y., Ji, Y., Chen, X. and Song, C., (2014) Inflation, operating cycle, and cash

holdings. China Journal of Accounting Research, 7(4), pp.263-276.

Santandrea, M., Sironi, A., Grassi, L. and Giorgino, M., (2017) Concentration risk and

internal rate of return: Evidence from the infrastructure equity market. International Journal

of Project Management, 35(3), pp.241-251.

Schwarzbichler, M., Steiner, C. and Turnheim, D., (2018) Economic Portfolio Decisions.

In Financial Steering (pp. 253-264). Springer, Cham.

Setiawan, D. and Fahrurrozi, N.R., (2017) November. Feasibility analysis with capital

budgeting backbone network fiber optic cable west palapa ring. In Broadband

Communication, Wireless Sensors and Powering (BCWSP), 2017 International Conference

on (pp. 1-4). IEEE.

Wang, Y., Ji, Y., Chen, X. and Song, C., (2014) Inflation, operating cycle, and cash

holdings. China Journal of Accounting Research, 7(4), pp.263-276.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.