Investment Appraisal Techniques: NPV, IRR, Payback Period

VerifiedAdded on 2023/06/11

|16

|3941

|239

AI Summary

This report is primarily concerned with assessing the understanding and ability to analyse capital investment decisions. It presents different investment appraisal techniques such as net present value, internal rate of return, payback period and accounting rate of return to the finance director of Tap Vim Plc. The report covers how these techniques will help the company in selecting the best, suitable and highly profitable investment projects out of the alternative projects. Real-life examples are provided to present an accurate report to the finance director of the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Primarily concerned with

assessing your understanding

of and ability to analyse

capital investment decisions

assessing your understanding

of and ability to analyse

capital investment decisions

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

Investment Appraisal Techniques................................................................................................3

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

Investment Appraisal Techniques................................................................................................3

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION

Investment appraisal which is also known as capital budgeting is an analysis which is used

by the finance manager of the company to consider the profitability of an investment over the

period of time along with the consideration of affordability and strategic fit (Pawlak and

Zarzecki, 2020). The report will be based on TapVim Plc. The report will present the different

investment appraisal techniques such as net present value, internal rate of return, payback period

and accounting rate of return to the finance director of Tap Vim Plc. The report will discuss the

meaning of each techniques definition, advantage, disadvantage as well as the potential practical

problems associated with the deployment of techniques in real life world. The report will cover

how this technique will help the TapVim Plc in selecting the best, suitable and highly profitable

investment projects out of the alternative projects. Further, the report will also cover the real life

practical examples of each investment appraisal techniques to present an accurate report to

finance director of the company. Lastly, the report will also summarize the overall information of

various investment appraisal techniques.

Investment Appraisal Techniques

Net present value

Definition

Net present value can be defined as the amount in terms of current value that left after

paying off for the cost of capital during each period. In other words, NPV is the amount obtained

by subtracting present value of outflows from the present value of inflows over a defined period

of time (Broomhead and et.al., 2021). It is one of the discounted cash flow method which takes

into account the time value of money at the time when capital investments are evaluated. Hence,

it is an investment appraisal technique used for analysing the profitability of the proposed

investment at the time when investment planning is going on.

Formula of Net Present Value = Present value of cash inflows – Present value of cash outflows

Present value of cash outflows is generally the initial cost of investment.

To determine the present value of cash inflows, the following formula should be used:

NPV = ∑ (CFn / (1 + i)n) – Initial Investment

n = it is the period from which the cash flows taken into account belongs to ranging from 0 to nth.

CFn = Cash flows take place in nth period

Investment appraisal which is also known as capital budgeting is an analysis which is used

by the finance manager of the company to consider the profitability of an investment over the

period of time along with the consideration of affordability and strategic fit (Pawlak and

Zarzecki, 2020). The report will be based on TapVim Plc. The report will present the different

investment appraisal techniques such as net present value, internal rate of return, payback period

and accounting rate of return to the finance director of Tap Vim Plc. The report will discuss the

meaning of each techniques definition, advantage, disadvantage as well as the potential practical

problems associated with the deployment of techniques in real life world. The report will cover

how this technique will help the TapVim Plc in selecting the best, suitable and highly profitable

investment projects out of the alternative projects. Further, the report will also cover the real life

practical examples of each investment appraisal techniques to present an accurate report to

finance director of the company. Lastly, the report will also summarize the overall information of

various investment appraisal techniques.

Investment Appraisal Techniques

Net present value

Definition

Net present value can be defined as the amount in terms of current value that left after

paying off for the cost of capital during each period. In other words, NPV is the amount obtained

by subtracting present value of outflows from the present value of inflows over a defined period

of time (Broomhead and et.al., 2021). It is one of the discounted cash flow method which takes

into account the time value of money at the time when capital investments are evaluated. Hence,

it is an investment appraisal technique used for analysing the profitability of the proposed

investment at the time when investment planning is going on.

Formula of Net Present Value = Present value of cash inflows – Present value of cash outflows

Present value of cash outflows is generally the initial cost of investment.

To determine the present value of cash inflows, the following formula should be used:

NPV = ∑ (CFn / (1 + i)n) – Initial Investment

n = it is the period from which the cash flows taken into account belongs to ranging from 0 to nth.

CFn = Cash flows take place in nth period

i = discounting rate or cost of capital

Advantages of Net Present Value

The primary benefit for which NPV technique is used is that it takes into account the time

value of money concept while evaluating investment proposals of different durations.

This concept allows weighing a dollar earn today as more in comparison to the dollar

earns tomorrow because of its earning capacity. Therefore, considering discounted cash

flows during investment evaluation indicates viability of an investment in better way.

The entire stream of cash flows that is, cash flows that are expected throughout the life of

the project is taken into consideration. Therefore, provide comprehensive view of

profitability of an investment (Warren and Seal, 2018).

Obtaining the difference between present value of cash inflows and present value of cash

outflows facilitates understanding of how much exactly added to the wealth of the

investor. Thus, provides conformity for the attainment of basis financial objective. NPV of different projects can be compared for selecting the best and highly potential

projects out of the available alternatives.

Disadvantages of Net Present Value

It is quite difficult to calculate the discounted cash flows for determining the NPV which

needs financial expertise and thus is not possible for a layman to determine, interpret and

compare the value of NPV.

While applying this technique, it is necessary to forecast future cash flows along with an

appropriate rate for discounting these cash flows to bring them at present value.

Accordingly, the accuracy of NPV is always questionable and dependent on the accuracy

with which the estimation has been made which in reality is considered to be difficult

(Alkaraan, 2020).

At the evaluation of mutually exclusive projects, several crucial factors are ignored such as size

of investment proposals, difference in the amount of initial investment, etc.

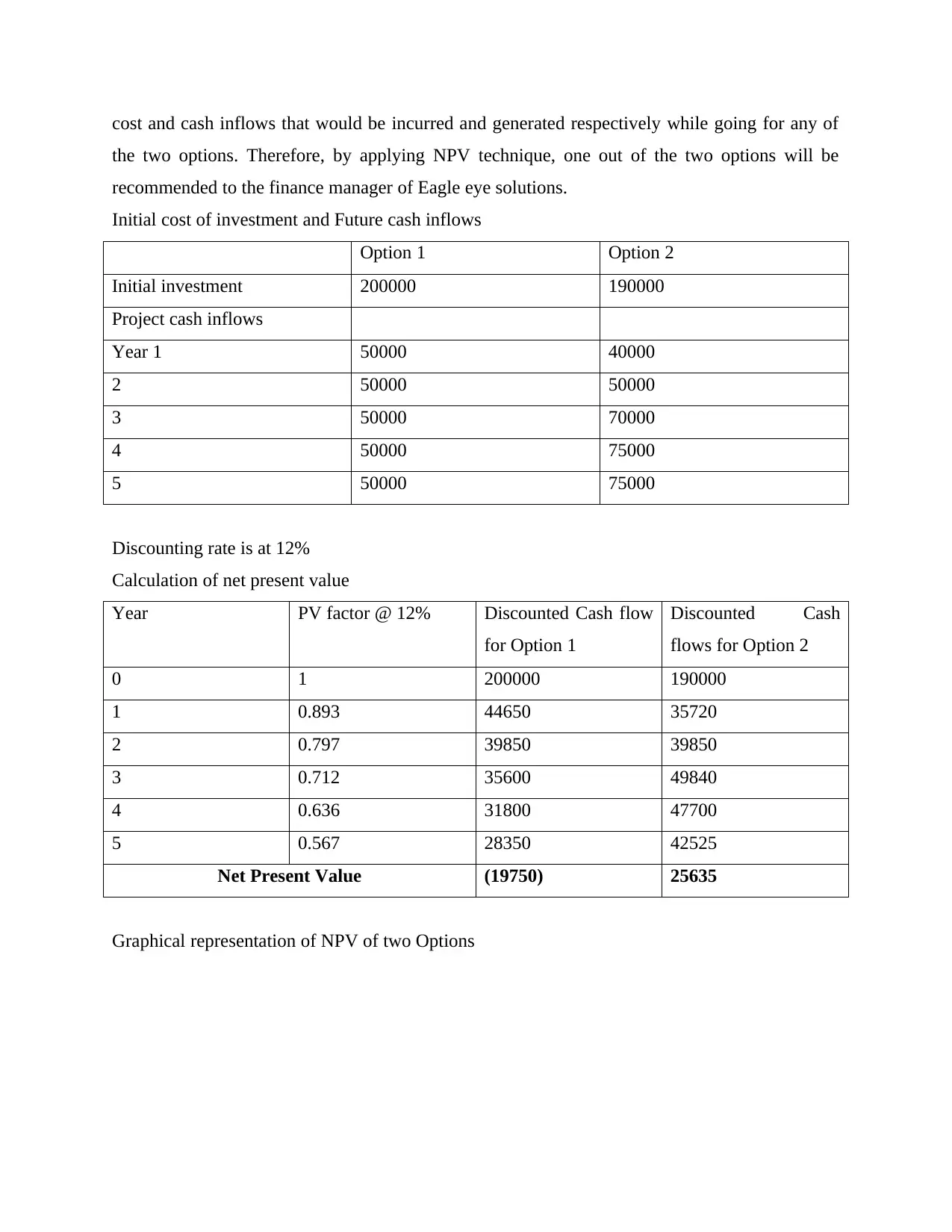

Real Life example for the application of NPV technique

Eagle eye solutions is a UK based IT company providing marketing technology which is meant

for creating digital connections facilitating personalised marketing that too in real time. The

company is considering upgrading its software system, for which they have two proposals and

they have to choose only one of it. The following is the information available pertaining to the

Advantages of Net Present Value

The primary benefit for which NPV technique is used is that it takes into account the time

value of money concept while evaluating investment proposals of different durations.

This concept allows weighing a dollar earn today as more in comparison to the dollar

earns tomorrow because of its earning capacity. Therefore, considering discounted cash

flows during investment evaluation indicates viability of an investment in better way.

The entire stream of cash flows that is, cash flows that are expected throughout the life of

the project is taken into consideration. Therefore, provide comprehensive view of

profitability of an investment (Warren and Seal, 2018).

Obtaining the difference between present value of cash inflows and present value of cash

outflows facilitates understanding of how much exactly added to the wealth of the

investor. Thus, provides conformity for the attainment of basis financial objective. NPV of different projects can be compared for selecting the best and highly potential

projects out of the available alternatives.

Disadvantages of Net Present Value

It is quite difficult to calculate the discounted cash flows for determining the NPV which

needs financial expertise and thus is not possible for a layman to determine, interpret and

compare the value of NPV.

While applying this technique, it is necessary to forecast future cash flows along with an

appropriate rate for discounting these cash flows to bring them at present value.

Accordingly, the accuracy of NPV is always questionable and dependent on the accuracy

with which the estimation has been made which in reality is considered to be difficult

(Alkaraan, 2020).

At the evaluation of mutually exclusive projects, several crucial factors are ignored such as size

of investment proposals, difference in the amount of initial investment, etc.

Real Life example for the application of NPV technique

Eagle eye solutions is a UK based IT company providing marketing technology which is meant

for creating digital connections facilitating personalised marketing that too in real time. The

company is considering upgrading its software system, for which they have two proposals and

they have to choose only one of it. The following is the information available pertaining to the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

cost and cash inflows that would be incurred and generated respectively while going for any of

the two options. Therefore, by applying NPV technique, one out of the two options will be

recommended to the finance manager of Eagle eye solutions.

Initial cost of investment and Future cash inflows

Option 1 Option 2

Initial investment 200000 190000

Project cash inflows

Year 1 50000 40000

2 50000 50000

3 50000 70000

4 50000 75000

5 50000 75000

Discounting rate is at 12%

Calculation of net present value

Year PV factor @ 12% Discounted Cash flow

for Option 1

Discounted Cash

flows for Option 2

0 1 200000 190000

1 0.893 44650 35720

2 0.797 39850 39850

3 0.712 35600 49840

4 0.636 31800 47700

5 0.567 28350 42525

Net Present Value (19750) 25635

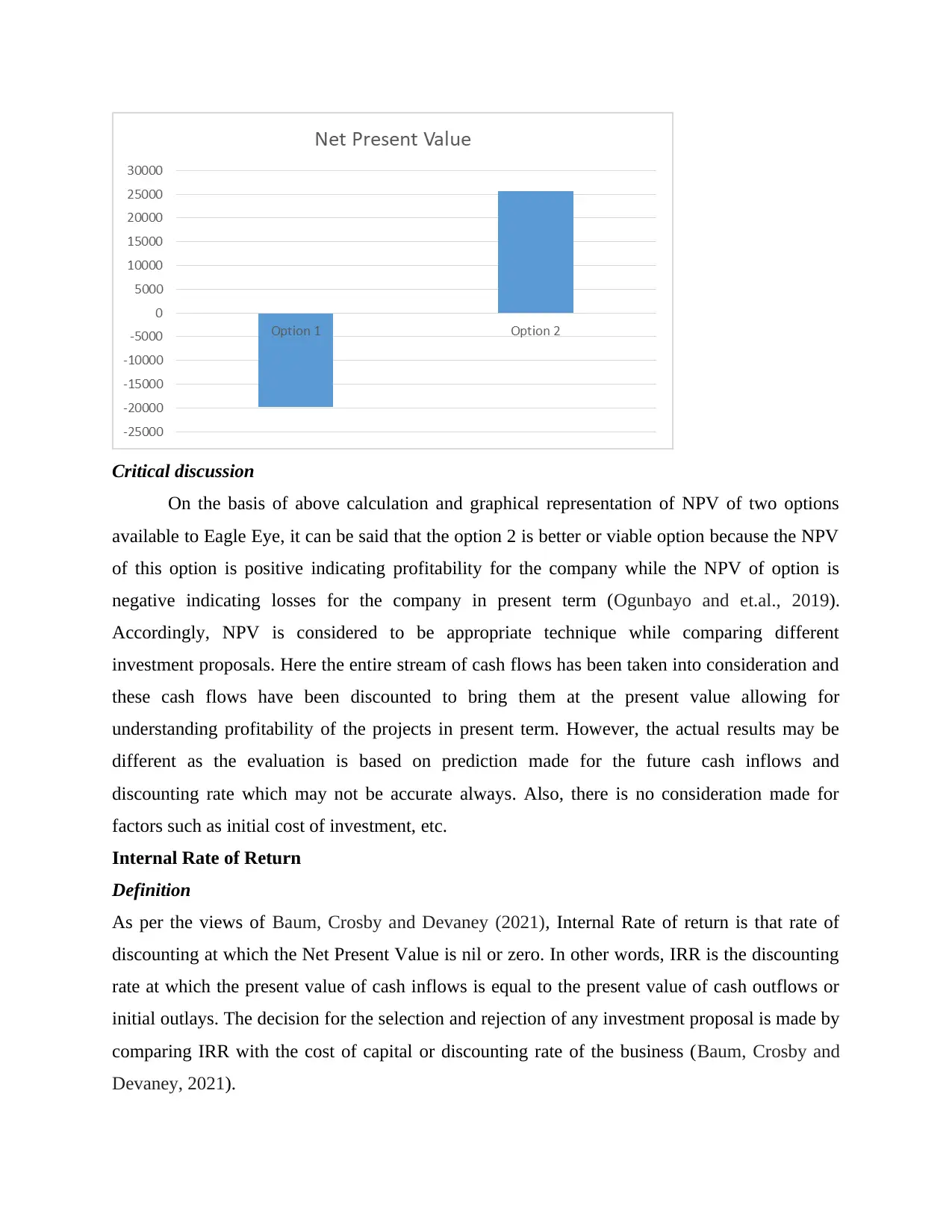

Graphical representation of NPV of two Options

the two options. Therefore, by applying NPV technique, one out of the two options will be

recommended to the finance manager of Eagle eye solutions.

Initial cost of investment and Future cash inflows

Option 1 Option 2

Initial investment 200000 190000

Project cash inflows

Year 1 50000 40000

2 50000 50000

3 50000 70000

4 50000 75000

5 50000 75000

Discounting rate is at 12%

Calculation of net present value

Year PV factor @ 12% Discounted Cash flow

for Option 1

Discounted Cash

flows for Option 2

0 1 200000 190000

1 0.893 44650 35720

2 0.797 39850 39850

3 0.712 35600 49840

4 0.636 31800 47700

5 0.567 28350 42525

Net Present Value (19750) 25635

Graphical representation of NPV of two Options

Critical discussion

On the basis of above calculation and graphical representation of NPV of two options

available to Eagle Eye, it can be said that the option 2 is better or viable option because the NPV

of this option is positive indicating profitability for the company while the NPV of option is

negative indicating losses for the company in present term (Ogunbayo and et.al., 2019).

Accordingly, NPV is considered to be appropriate technique while comparing different

investment proposals. Here the entire stream of cash flows has been taken into consideration and

these cash flows have been discounted to bring them at the present value allowing for

understanding profitability of the projects in present term. However, the actual results may be

different as the evaluation is based on prediction made for the future cash inflows and

discounting rate which may not be accurate always. Also, there is no consideration made for

factors such as initial cost of investment, etc.

Internal Rate of Return

Definition

As per the views of Baum, Crosby and Devaney (2021), Internal Rate of return is that rate of

discounting at which the Net Present Value is nil or zero. In other words, IRR is the discounting

rate at which the present value of cash inflows is equal to the present value of cash outflows or

initial outlays. The decision for the selection and rejection of any investment proposal is made by

comparing IRR with the cost of capital or discounting rate of the business (Baum, Crosby and

Devaney, 2021).

On the basis of above calculation and graphical representation of NPV of two options

available to Eagle Eye, it can be said that the option 2 is better or viable option because the NPV

of this option is positive indicating profitability for the company while the NPV of option is

negative indicating losses for the company in present term (Ogunbayo and et.al., 2019).

Accordingly, NPV is considered to be appropriate technique while comparing different

investment proposals. Here the entire stream of cash flows has been taken into consideration and

these cash flows have been discounted to bring them at the present value allowing for

understanding profitability of the projects in present term. However, the actual results may be

different as the evaluation is based on prediction made for the future cash inflows and

discounting rate which may not be accurate always. Also, there is no consideration made for

factors such as initial cost of investment, etc.

Internal Rate of Return

Definition

As per the views of Baum, Crosby and Devaney (2021), Internal Rate of return is that rate of

discounting at which the Net Present Value is nil or zero. In other words, IRR is the discounting

rate at which the present value of cash inflows is equal to the present value of cash outflows or

initial outlays. The decision for the selection and rejection of any investment proposal is made by

comparing IRR with the cost of capital or discounting rate of the business (Baum, Crosby and

Devaney, 2021).

Formula for determining the internal rate of return is as follows:

IRR = lower discounting rate + (NPV at lower rate / NPV at lower rate – NPV at higher rate) *

(Higher rate – Lower rate)

Advantages of Internal Rate of Return

Likewise, the case of NPV, IRR is based on the utilization of the concept of time value of

money which bring the future cash flows at their present value, making investment

evaluation more viable. On the basis of IRR, comparison and selection procedure for various projects become

easier where the IRR is compared with the firm’s cost of capital. Accordingly, a project

with IRR which is greater than the cost of capital is selected due to being profitable in

terms of returns are higher than the cost (Soka, 2020).

Disadvantages of Internal Rate of Return

The calculation of IRR is quite difficult and is not possible for layman to perform and

understand the differences among various outcomes.

Projects with different patterns of inflows and outflows could not be easily evaluated

through IRR.

The technique is backed by an assumption that all the cash inflows from the investment

gets reinvested at IRR by ignoring the ability of the firm to invest at different rates. In case of mutually exclusive projects, a project having lower IRR but larger fund

commitment generally has greater contribution in terms of absolute NPV (Jifar, 2021).

Therefore, decisions made on the basis of IRR becomes less attractive.

Real Life example for the application of NPV technique

There are two projects considering Sainsbury’s Plc for the investment in convenience stores at

two different locations. The investment is mutually exclusive and have the following initial

outlays and patterns within future cash inflows:

Year Project at location 1 Project at location 2

0 -250000 -200000

1 60000 52000

2 68000 56000

3 72000 58000

4 74000 59000

IRR = lower discounting rate + (NPV at lower rate / NPV at lower rate – NPV at higher rate) *

(Higher rate – Lower rate)

Advantages of Internal Rate of Return

Likewise, the case of NPV, IRR is based on the utilization of the concept of time value of

money which bring the future cash flows at their present value, making investment

evaluation more viable. On the basis of IRR, comparison and selection procedure for various projects become

easier where the IRR is compared with the firm’s cost of capital. Accordingly, a project

with IRR which is greater than the cost of capital is selected due to being profitable in

terms of returns are higher than the cost (Soka, 2020).

Disadvantages of Internal Rate of Return

The calculation of IRR is quite difficult and is not possible for layman to perform and

understand the differences among various outcomes.

Projects with different patterns of inflows and outflows could not be easily evaluated

through IRR.

The technique is backed by an assumption that all the cash inflows from the investment

gets reinvested at IRR by ignoring the ability of the firm to invest at different rates. In case of mutually exclusive projects, a project having lower IRR but larger fund

commitment generally has greater contribution in terms of absolute NPV (Jifar, 2021).

Therefore, decisions made on the basis of IRR becomes less attractive.

Real Life example for the application of NPV technique

There are two projects considering Sainsbury’s Plc for the investment in convenience stores at

two different locations. The investment is mutually exclusive and have the following initial

outlays and patterns within future cash inflows:

Year Project at location 1 Project at location 2

0 -250000 -200000

1 60000 52000

2 68000 56000

3 72000 58000

4 74000 59000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 77000 60000

Assuming the higher and lower rate of discounting as 15% and 5%

NPV at higher rate

Year Project

at

location

1

Project

at

location

2

0 1 -

250000

-250000 -

200000

-200000

1 0.86957 60000 52173.91304 52000 45217.39

2 0.75614 68000 51417.76938 56000 42344.05

3 0.65752 72000 47341.16874 58000 38135.94

4 0.57175 74000 42309.74017 59000 33733.44

5 0.49718 77000 38282.60862 60000 29830.6

NPV -18474.8001 -10738.6

NPV at lower rate

Year Project

at

location

1

Project

at

location

2

0 1 -

250000

-250000 -

200000

-200000

1 0.95238 60000 57142.85714 52000 49523.81

2 0.90703 68000 61678.00454 56000 50793.65

3 0.86384 72000 62196.30709 58000 50102.58

4 0.8227 74000 60879.98313 59000 48539.45

5 0.78353 77000 60331.51482 60000 47011.57

NPV 52228.66672 45971.06

IRR for project at location 1 = IRR = lower discounting rate + (NPV at lower rate / NPV at lower

rate – NPV at higher rate) * (Higher rate – Lower rate)

IRR = 5% + (52229 / 52229 – (-18475) * (15 - 5)

IRR = 5% + (52229 / 70704) * 10

IRR = 5% + 7.4 = 12.4%

IRR for project at location 1 = IRR = lower discounting rate + (NPV at lower rate / NPV at lower

rate – NPV at higher rate) * (Higher rate – Lower rate)

Assuming the higher and lower rate of discounting as 15% and 5%

NPV at higher rate

Year Project

at

location

1

Project

at

location

2

0 1 -

250000

-250000 -

200000

-200000

1 0.86957 60000 52173.91304 52000 45217.39

2 0.75614 68000 51417.76938 56000 42344.05

3 0.65752 72000 47341.16874 58000 38135.94

4 0.57175 74000 42309.74017 59000 33733.44

5 0.49718 77000 38282.60862 60000 29830.6

NPV -18474.8001 -10738.6

NPV at lower rate

Year Project

at

location

1

Project

at

location

2

0 1 -

250000

-250000 -

200000

-200000

1 0.95238 60000 57142.85714 52000 49523.81

2 0.90703 68000 61678.00454 56000 50793.65

3 0.86384 72000 62196.30709 58000 50102.58

4 0.8227 74000 60879.98313 59000 48539.45

5 0.78353 77000 60331.51482 60000 47011.57

NPV 52228.66672 45971.06

IRR for project at location 1 = IRR = lower discounting rate + (NPV at lower rate / NPV at lower

rate – NPV at higher rate) * (Higher rate – Lower rate)

IRR = 5% + (52229 / 52229 – (-18475) * (15 - 5)

IRR = 5% + (52229 / 70704) * 10

IRR = 5% + 7.4 = 12.4%

IRR for project at location 1 = IRR = lower discounting rate + (NPV at lower rate / NPV at lower

rate – NPV at higher rate) * (Higher rate – Lower rate)

IRR = 5% + (45971 / 45971 – (-10739)) * (15 - 5)

IRR = 5% + (45971 / 56710) * 10

IRR = 5% + 8.1

IRR = 13.1%

Critical Discussion

On the basis of calculation, it has been identified that the project at location 2 is having higher

IRR as compared to the project at location 1, thus, the finance manager at Sainsbury’s must go

for investing in the project at location 2. This would allow the company in generating higher

returns at a given cost of capital along with lower requirement of funds for the initial outlay

(Broomhead and et.al., 2021). However, project at location 1 is having greater NPV derived at

higher rate as compared to the project at location 2 and this is what the limitation of IRR when

decisions are made just by considering the IRR of the projects.

Payback Period

Definition

Payback period is being defined by Ogunbayo and et.al., (2019) as the duration that an

investment would take in bringing back the initial cost of investment to the investor. Shorter the

term, lower the risky proposal for investment is.

Formula for calculating payback period = Initial investment / cash flows per year

Advantages of Payback period It is easy to estimate and provide estimations for the time to get back the initial amount of

investment.

Disadvantages of Payback period

It ignores the concept of time value of money, thus making the evaluation quite non-

viable in present terms (Egbunike, 2021). Also, the cash flows generated after the payback period is not being taken into

consideration and therefore, does not provide for comprehensive view of project

profitability.

Real life practical problem

The Two mutually exclusive projects that Morrison is considering for expansion having the

following cash inflows and initial investment.

Year Annual cash Cumulative Annual cash Cumulative cash

IRR = 5% + (45971 / 56710) * 10

IRR = 5% + 8.1

IRR = 13.1%

Critical Discussion

On the basis of calculation, it has been identified that the project at location 2 is having higher

IRR as compared to the project at location 1, thus, the finance manager at Sainsbury’s must go

for investing in the project at location 2. This would allow the company in generating higher

returns at a given cost of capital along with lower requirement of funds for the initial outlay

(Broomhead and et.al., 2021). However, project at location 1 is having greater NPV derived at

higher rate as compared to the project at location 2 and this is what the limitation of IRR when

decisions are made just by considering the IRR of the projects.

Payback Period

Definition

Payback period is being defined by Ogunbayo and et.al., (2019) as the duration that an

investment would take in bringing back the initial cost of investment to the investor. Shorter the

term, lower the risky proposal for investment is.

Formula for calculating payback period = Initial investment / cash flows per year

Advantages of Payback period It is easy to estimate and provide estimations for the time to get back the initial amount of

investment.

Disadvantages of Payback period

It ignores the concept of time value of money, thus making the evaluation quite non-

viable in present terms (Egbunike, 2021). Also, the cash flows generated after the payback period is not being taken into

consideration and therefore, does not provide for comprehensive view of project

profitability.

Real life practical problem

The Two mutually exclusive projects that Morrison is considering for expansion having the

following cash inflows and initial investment.

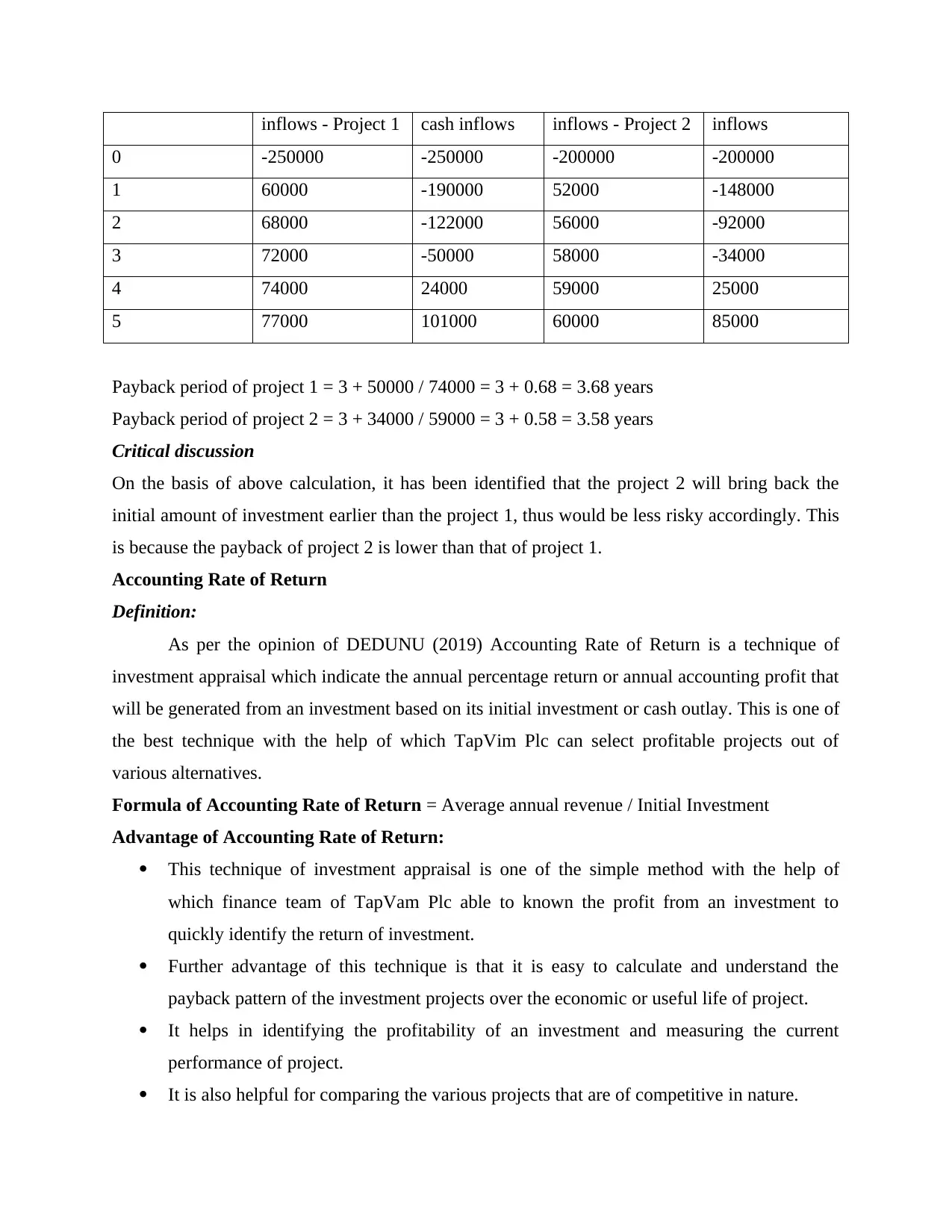

Year Annual cash Cumulative Annual cash Cumulative cash

inflows - Project 1 cash inflows inflows - Project 2 inflows

0 -250000 -250000 -200000 -200000

1 60000 -190000 52000 -148000

2 68000 -122000 56000 -92000

3 72000 -50000 58000 -34000

4 74000 24000 59000 25000

5 77000 101000 60000 85000

Payback period of project 1 = 3 + 50000 / 74000 = 3 + 0.68 = 3.68 years

Payback period of project 2 = 3 + 34000 / 59000 = 3 + 0.58 = 3.58 years

Critical discussion

On the basis of above calculation, it has been identified that the project 2 will bring back the

initial amount of investment earlier than the project 1, thus would be less risky accordingly. This

is because the payback of project 2 is lower than that of project 1.

Accounting Rate of Return

Definition:

As per the opinion of DEDUNU (2019) Accounting Rate of Return is a technique of

investment appraisal which indicate the annual percentage return or annual accounting profit that

will be generated from an investment based on its initial investment or cash outlay. This is one of

the best technique with the help of which TapVim Plc can select profitable projects out of

various alternatives.

Formula of Accounting Rate of Return = Average annual revenue / Initial Investment

Advantage of Accounting Rate of Return:

This technique of investment appraisal is one of the simple method with the help of

which finance team of TapVam Plc able to known the profit from an investment to

quickly identify the return of investment.

Further advantage of this technique is that it is easy to calculate and understand the

payback pattern of the investment projects over the economic or useful life of project.

It helps in identifying the profitability of an investment and measuring the current

performance of project.

It is also helpful for comparing the various projects that are of competitive in nature.

0 -250000 -250000 -200000 -200000

1 60000 -190000 52000 -148000

2 68000 -122000 56000 -92000

3 72000 -50000 58000 -34000

4 74000 24000 59000 25000

5 77000 101000 60000 85000

Payback period of project 1 = 3 + 50000 / 74000 = 3 + 0.68 = 3.68 years

Payback period of project 2 = 3 + 34000 / 59000 = 3 + 0.58 = 3.58 years

Critical discussion

On the basis of above calculation, it has been identified that the project 2 will bring back the

initial amount of investment earlier than the project 1, thus would be less risky accordingly. This

is because the payback of project 2 is lower than that of project 1.

Accounting Rate of Return

Definition:

As per the opinion of DEDUNU (2019) Accounting Rate of Return is a technique of

investment appraisal which indicate the annual percentage return or annual accounting profit that

will be generated from an investment based on its initial investment or cash outlay. This is one of

the best technique with the help of which TapVim Plc can select profitable projects out of

various alternatives.

Formula of Accounting Rate of Return = Average annual revenue / Initial Investment

Advantage of Accounting Rate of Return:

This technique of investment appraisal is one of the simple method with the help of

which finance team of TapVam Plc able to known the profit from an investment to

quickly identify the return of investment.

Further advantage of this technique is that it is easy to calculate and understand the

payback pattern of the investment projects over the economic or useful life of project.

It helps in identifying the profitability of an investment and measuring the current

performance of project.

It is also helpful for comparing the various projects that are of competitive in nature.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

This is best for small time investment as the this helps the small-time investors to use this

method more frequently for appraising their investment decision (Farhi and Gourio,

2018).

Disadvantage of Accounting Rate of Return:

This method is basically considering only accounting profit and do not consider cash

flow and taxes. Also, it includes non-cash item such as depreciation in decision-making

which is not possible in real world.

Another most significant disadvantage of this factor is such that it does not consider the

time value of money and discounting factor concept which are basically the base of

investment decision.

At the time of comparing the project of different period, this technique does not consider

the life period of various projects. The impact of which the result produce by this method

is inaccurate for the real world investment projects decision (Marchioni and Magni

2018).

On the other hand, ARR method also ignores the external factors which is also one of the

disadvantage. In simple term, this is not suitable for the huge as well as long term

investment project that have to be consider by the TapVim Plc.

Real Life Practical Problem or example of Accounting Rate of return:

Tesco Plc is a UK based retail organization that uses the accounting rate of return

technique of investment appraisal to make the decision regarding the investment on fixed assets

such as property, plant and equipment. For example, Tesco Plc have two option regarding the

purchase of machinery for the production of Cloths. The information of both Machinery are as

follows:

Machinery 1

Initial Investment = €250000

Expected Profit per year = €70000

Depreciation = 10% on straight line basis

Time Frame = 5 Years

method more frequently for appraising their investment decision (Farhi and Gourio,

2018).

Disadvantage of Accounting Rate of Return:

This method is basically considering only accounting profit and do not consider cash

flow and taxes. Also, it includes non-cash item such as depreciation in decision-making

which is not possible in real world.

Another most significant disadvantage of this factor is such that it does not consider the

time value of money and discounting factor concept which are basically the base of

investment decision.

At the time of comparing the project of different period, this technique does not consider

the life period of various projects. The impact of which the result produce by this method

is inaccurate for the real world investment projects decision (Marchioni and Magni

2018).

On the other hand, ARR method also ignores the external factors which is also one of the

disadvantage. In simple term, this is not suitable for the huge as well as long term

investment project that have to be consider by the TapVim Plc.

Real Life Practical Problem or example of Accounting Rate of return:

Tesco Plc is a UK based retail organization that uses the accounting rate of return

technique of investment appraisal to make the decision regarding the investment on fixed assets

such as property, plant and equipment. For example, Tesco Plc have two option regarding the

purchase of machinery for the production of Cloths. The information of both Machinery are as

follows:

Machinery 1

Initial Investment = €250000

Expected Profit per year = €70000

Depreciation = 10% on straight line basis

Time Frame = 5 Years

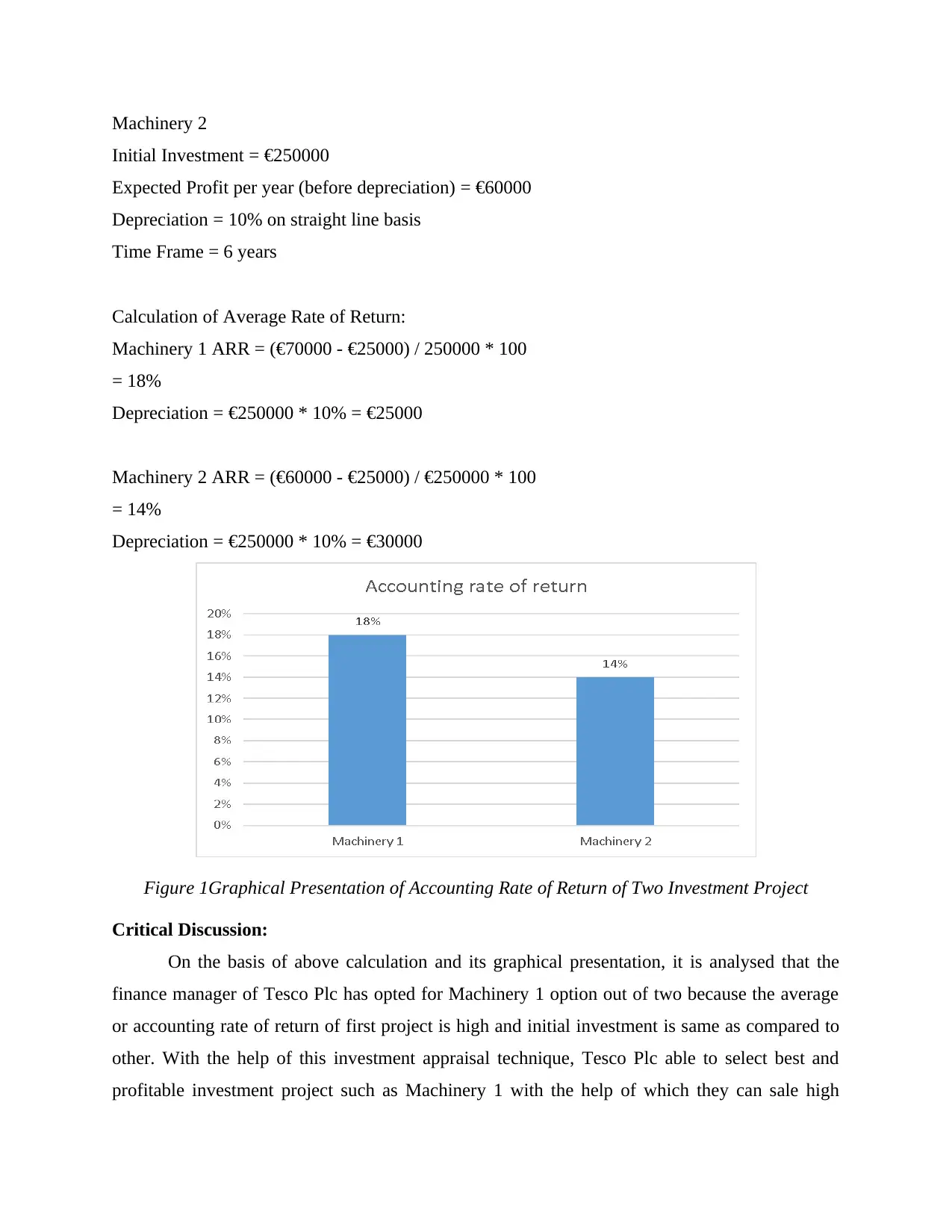

Machinery 2

Initial Investment = €250000

Expected Profit per year (before depreciation) = €60000

Depreciation = 10% on straight line basis

Time Frame = 6 years

Calculation of Average Rate of Return:

Machinery 1 ARR = (€70000 - €25000) / 250000 * 100

= 18%

Depreciation = €250000 * 10% = €25000

Machinery 2 ARR = (€60000 - €25000) / €250000 * 100

= 14%

Depreciation = €250000 * 10% = €30000

Figure 1Graphical Presentation of Accounting Rate of Return of Two Investment Project

Critical Discussion:

On the basis of above calculation and its graphical presentation, it is analysed that the

finance manager of Tesco Plc has opted for Machinery 1 option out of two because the average

or accounting rate of return of first project is high and initial investment is same as compared to

other. With the help of this investment appraisal technique, Tesco Plc able to select best and

profitable investment project such as Machinery 1 with the help of which they can sale high

Initial Investment = €250000

Expected Profit per year (before depreciation) = €60000

Depreciation = 10% on straight line basis

Time Frame = 6 years

Calculation of Average Rate of Return:

Machinery 1 ARR = (€70000 - €25000) / 250000 * 100

= 18%

Depreciation = €250000 * 10% = €25000

Machinery 2 ARR = (€60000 - €25000) / €250000 * 100

= 14%

Depreciation = €250000 * 10% = €30000

Figure 1Graphical Presentation of Accounting Rate of Return of Two Investment Project

Critical Discussion:

On the basis of above calculation and its graphical presentation, it is analysed that the

finance manager of Tesco Plc has opted for Machinery 1 option out of two because the average

or accounting rate of return of first project is high and initial investment is same as compared to

other. With the help of this investment appraisal technique, Tesco Plc able to select best and

profitable investment project such as Machinery 1 with the help of which they can sale high

amount of cloth products (Gorshkov and et.al., 2018). The sales of Tesco plc has highly

enhnaced due to its investment decision on macheinery for the new cloth product production and

sales.

However, on the other hand, the implementation of this technique for the assessment of

potential profit of an assets is not always good and work in the favour of the organization. It is

because ARR technique does not consider the time value of money and discounting factor

concept. The impact of which the profit of Tesco Plc started decreasing in the future rather than

increasing because of its decision based on ARR technique. The time value of money is a

concept which state that the present value of money will always higher than the furture value of

same sum of money because of its potential earning capacity. Also, the use of ARR investment

appraisal technique for selecting projects that yield uneven annual return. It is because it might

be chance that one project yield more revenue in early year while as compared to other project

which the company can further reinvest to earn more returns.

Further, the other potential problem that have to be consider by TapVim Plc associated

with accounting rate of return which is not consider by Tesco Plc is that the ARR is based on

profits rather than cashflows. This method also consider the non-cash item such as depreciation

in profit calculation (Florio, Morretta and Willak, 2018). The impact of which the result is

became useless for the organization to make proper decision. It also fails to take into account the

timing of profit thus it is important for the finance team of TapVim Plc that they should consider

this technique potential problem in details before adopting it. It is because a wrong decision may

leads to heavy loss to the company.

CONCLUSION

After summing up the above information, it has been concluded that the different investment

appraisal techniques play vital role in the decision-making process. The report has concluded the

four investment appraisal technique along with their advantage, disadvantage and real life

example. The report has also identified that the net present value method and internal rate of

return is two techniques that TapVim Plc have to consider more as compared to other two

methods such as payback and ARR. It is because NRV and IRR consider the time value of

money and other two techniques not. Also, the report has critically discussed on the potential

enhnaced due to its investment decision on macheinery for the new cloth product production and

sales.

However, on the other hand, the implementation of this technique for the assessment of

potential profit of an assets is not always good and work in the favour of the organization. It is

because ARR technique does not consider the time value of money and discounting factor

concept. The impact of which the profit of Tesco Plc started decreasing in the future rather than

increasing because of its decision based on ARR technique. The time value of money is a

concept which state that the present value of money will always higher than the furture value of

same sum of money because of its potential earning capacity. Also, the use of ARR investment

appraisal technique for selecting projects that yield uneven annual return. It is because it might

be chance that one project yield more revenue in early year while as compared to other project

which the company can further reinvest to earn more returns.

Further, the other potential problem that have to be consider by TapVim Plc associated

with accounting rate of return which is not consider by Tesco Plc is that the ARR is based on

profits rather than cashflows. This method also consider the non-cash item such as depreciation

in profit calculation (Florio, Morretta and Willak, 2018). The impact of which the result is

became useless for the organization to make proper decision. It also fails to take into account the

timing of profit thus it is important for the finance team of TapVim Plc that they should consider

this technique potential problem in details before adopting it. It is because a wrong decision may

leads to heavy loss to the company.

CONCLUSION

After summing up the above information, it has been concluded that the different investment

appraisal techniques play vital role in the decision-making process. The report has concluded the

four investment appraisal technique along with their advantage, disadvantage and real life

example. The report has also identified that the net present value method and internal rate of

return is two techniques that TapVim Plc have to consider more as compared to other two

methods such as payback and ARR. It is because NRV and IRR consider the time value of

money and other two techniques not. Also, the report has critically discussed on the potential

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

problem that might face by TapVim Plc finance team while using this investment appraisal

techniques or methods.

techniques or methods.

REFERENCES

Books and journals

Pawlak, M. and Zarzecki, D., 2020. Investment Appraisal Practice in the European Union

Countries. European Research Studies. 23(2). pp.687-699.

DEDUNU, H., 2019. Management Accounting Practices in Sri Lanka: An Empirical

Investigation in Banking Sector.

Farhi, E. and Gourio, F., 2018. Accounting for macro-finance trends: Market power, intangibles,

and risk premia (No. w25282). National Bureau of Economic Research.

Marchioni, A. and Magni, C. A., 2018. Investment decisions and sensitivity analysis: NPV-

consistency of rates of return. European Journal of Operational Research. 268(1).

pp.361-372.

Gorshkov, A. S. and et.al., 2018. Payback period of investments in energy saving. Magazine of

Civil Engineering, (2).

Florio, M., Morretta, V. and Willak, W., 2018. Cost-benefit analysis and European Union

cohesion policy: Economic versus financial returns in investment project

appraisal. Journal of Benefit-Cost Analysis. 9(1). pp.147-180.

Egbunike, W. S. I. P. A., 2021. USE OF INVESTMENT APPRAISAL TECHNIQUES AND

CAPITAL INVESTMENT DECISIONS OF CROSS RIVER STATE GOVERNMENT

OF NIGERIA.

Broomhead, S. C., and et.al., 2021. EHealth Investment Appraisal in Africa: A Scoping

Review. INQUIRY: The Journal of Health Care Organization, Provision, and

Financing, 58, p.00469580211059999.

Jifar, T., 2021. Investment Appraisal Techniques of Small and Medium Scale Enterprises in

Ethiopia (A Case Study in Selected Wored as of Wolaita Zone).

Soka, I. M., 2020. Impact of Appraisal Techniques on Investment Returns A Survey of

Institutional Investors (Doctoral dissertation, The Open University of Tanzania).

Baum, A. E., Crosby, N. and Devaney, S., 2021. Property investment appraisal. John Wiley &

Sons.

Ogunbayo, O. T., and et.al., 2019. The significance of real estate development process analysis

to residential property investment appraisal in Abuja, Nigeria. International Journal of

Construction Management, 19(3), pp.270-279.

1

Books and journals

Pawlak, M. and Zarzecki, D., 2020. Investment Appraisal Practice in the European Union

Countries. European Research Studies. 23(2). pp.687-699.

DEDUNU, H., 2019. Management Accounting Practices in Sri Lanka: An Empirical

Investigation in Banking Sector.

Farhi, E. and Gourio, F., 2018. Accounting for macro-finance trends: Market power, intangibles,

and risk premia (No. w25282). National Bureau of Economic Research.

Marchioni, A. and Magni, C. A., 2018. Investment decisions and sensitivity analysis: NPV-

consistency of rates of return. European Journal of Operational Research. 268(1).

pp.361-372.

Gorshkov, A. S. and et.al., 2018. Payback period of investments in energy saving. Magazine of

Civil Engineering, (2).

Florio, M., Morretta, V. and Willak, W., 2018. Cost-benefit analysis and European Union

cohesion policy: Economic versus financial returns in investment project

appraisal. Journal of Benefit-Cost Analysis. 9(1). pp.147-180.

Egbunike, W. S. I. P. A., 2021. USE OF INVESTMENT APPRAISAL TECHNIQUES AND

CAPITAL INVESTMENT DECISIONS OF CROSS RIVER STATE GOVERNMENT

OF NIGERIA.

Broomhead, S. C., and et.al., 2021. EHealth Investment Appraisal in Africa: A Scoping

Review. INQUIRY: The Journal of Health Care Organization, Provision, and

Financing, 58, p.00469580211059999.

Jifar, T., 2021. Investment Appraisal Techniques of Small and Medium Scale Enterprises in

Ethiopia (A Case Study in Selected Wored as of Wolaita Zone).

Soka, I. M., 2020. Impact of Appraisal Techniques on Investment Returns A Survey of

Institutional Investors (Doctoral dissertation, The Open University of Tanzania).

Baum, A. E., Crosby, N. and Devaney, S., 2021. Property investment appraisal. John Wiley &

Sons.

Ogunbayo, O. T., and et.al., 2019. The significance of real estate development process analysis

to residential property investment appraisal in Abuja, Nigeria. International Journal of

Construction Management, 19(3), pp.270-279.

1

Alkaraan, F., 2020. Strategic investment decision-making practices in large manufacturing

companies: a role for emergent analysis techniques?. Meditari Accountancy Research.

Warren, L. and Seal, W., 2018. Using investment appraisal models in strategic negotiation: The

cultural political economy of electricity generation. Accounting, organizations and

society, 70, pp.16-32.

2

companies: a role for emergent analysis techniques?. Meditari Accountancy Research.

Warren, L. and Seal, W., 2018. Using investment appraisal models in strategic negotiation: The

cultural political economy of electricity generation. Accounting, organizations and

society, 70, pp.16-32.

2

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.