Investment Appraisal Techniques: Risk Assessment and CAPM Analysis

VerifiedAdded on 2023/06/10

|9

|1696

|367

Report

AI Summary

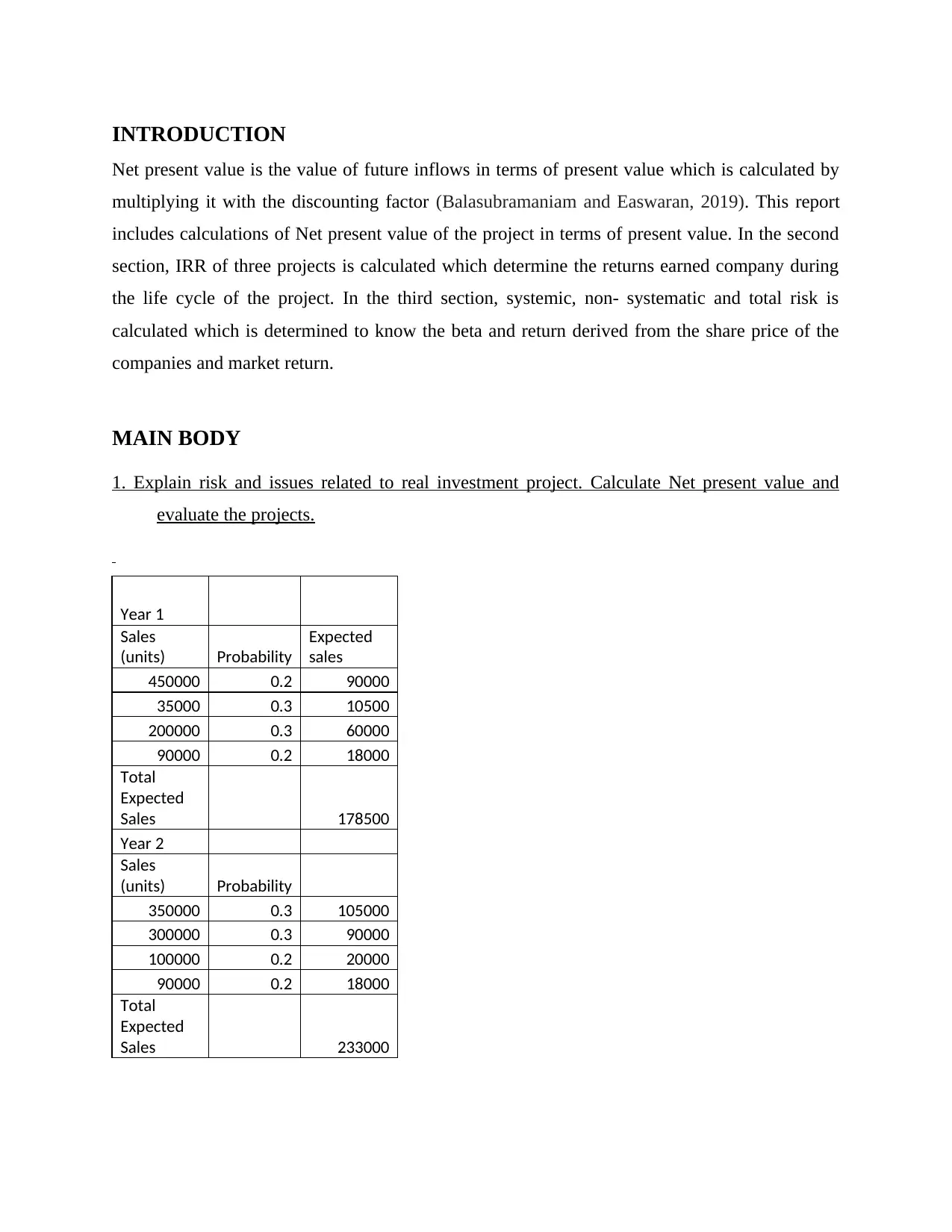

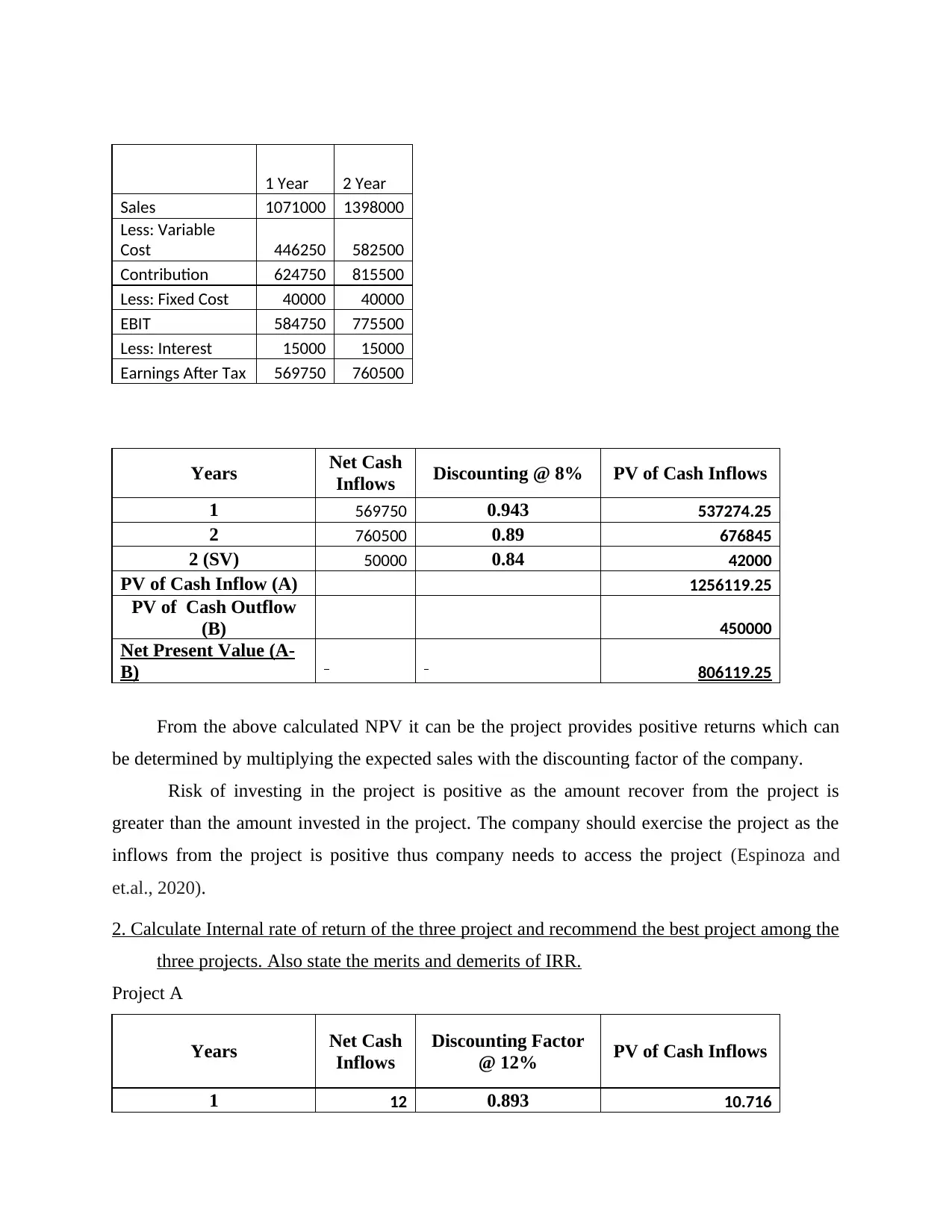

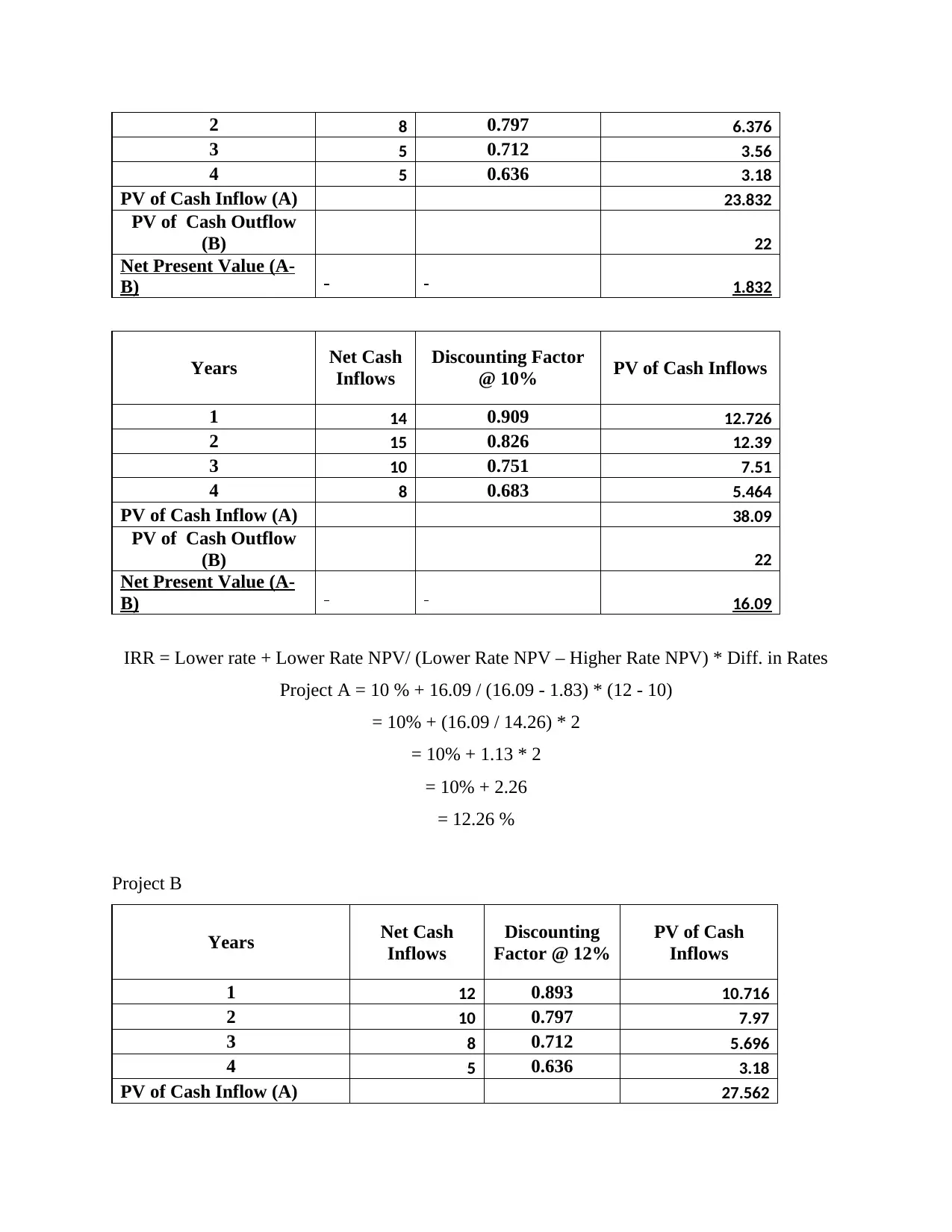

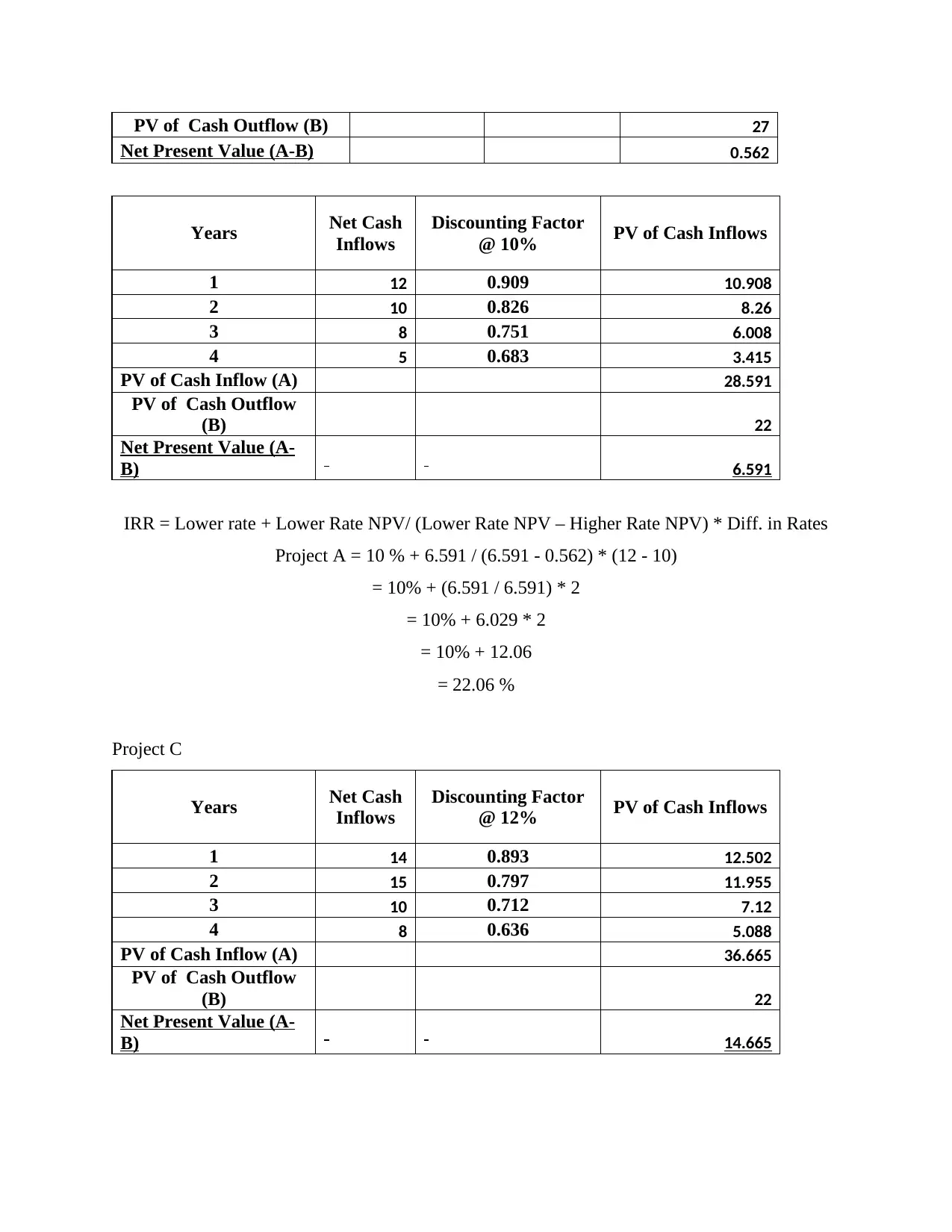

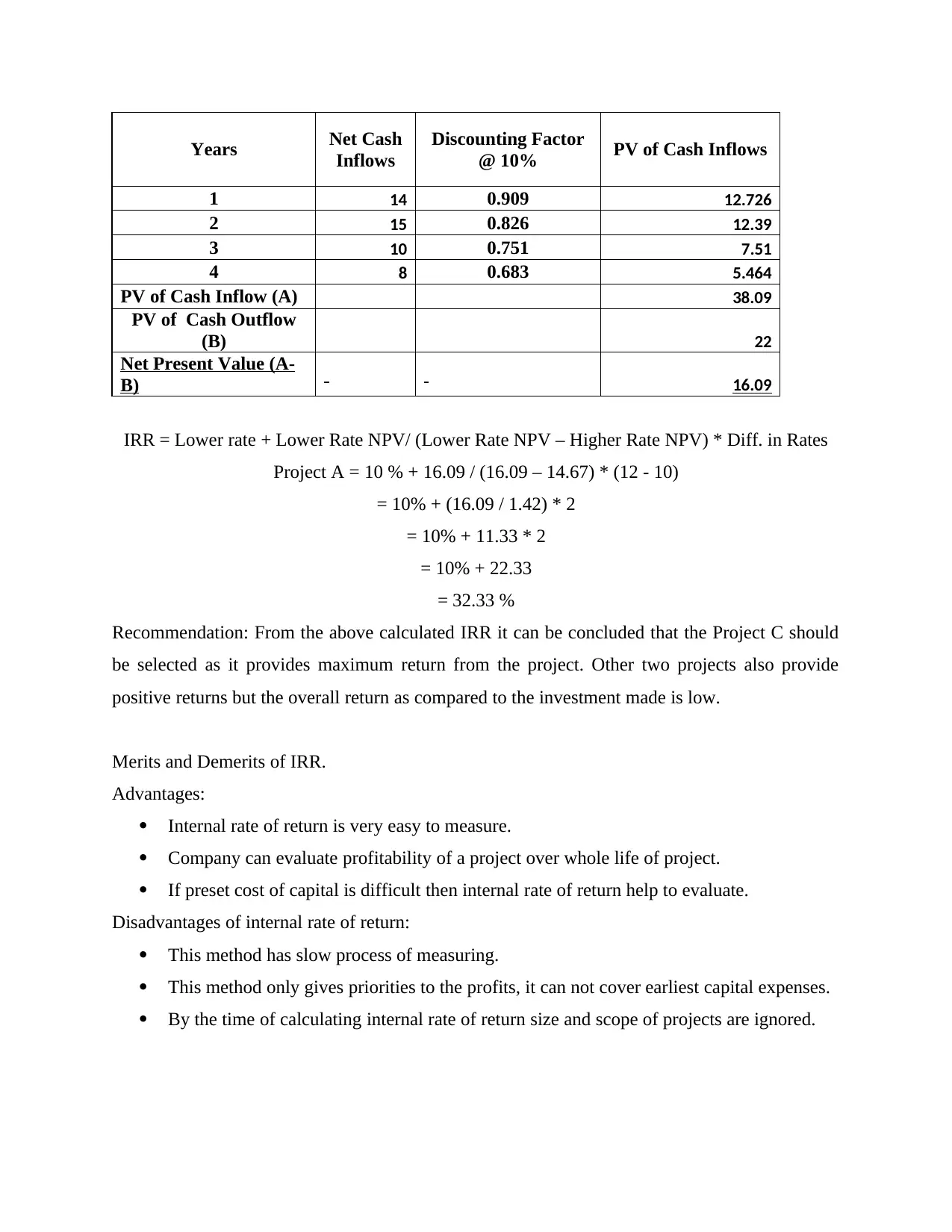

This report provides a comprehensive analysis of investment appraisal techniques, focusing on risk assessment and the Capital Asset Pricing Model (CAPM). It includes calculations of Net Present Value (NPV) for a project, determining its potential profitability by discounting future cash inflows. Furthermore, the report calculates the Internal Rate of Return (IRR) for three different projects to identify the most lucrative investment opportunity, while also discussing the advantages and disadvantages of using the IRR method. Finally, the report delves into risk analysis by calculating systematic, non-systematic, and total risk for two companies, using market returns and share prices to assess their investment viability. The report concludes with a recommendation based on the IRR analysis and emphasizes the importance of investment appraisal techniques in making informed financial decisions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.