Financial Management and Analysis

VerifiedAdded on 2020/07/23

|35

|8776

|124

AI Summary

This assignment provides an in-depth examination of financial management concepts, including valuation methods, risk assessment, and cash flow analysis. It covers various topics such as discounted cash flow (DCF) models, net present value (NPV), and internal rate of return (IRR). The study guide also delves into the importance of dividend policies, stock returns, and asset growth. Furthermore, it discusses the application of financial management theories in real-world scenarios, including logistics, renewable energy, and mergers and acquisitions. The assignment aims to equip students with a solid understanding of financial management principles and their practical implications.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

INVESTMENT HORIZON OF EXPECTED

RETURN FORECASTS ISSUES

RETURN FORECASTS ISSUES

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACKNOWLEDGEMENT

I am thankful to my tutor, friends and relatives who gave me guidance and support for

this project. In completing my dissertation on the suitability of equity and bond valuation

pertaining to short and long run they always encouraged me to do it in the best possible way. In

addition to this, I also appreciate my mentor for giving me guidance in preparing dissertation.

From his support and experience I was in the position to complete dissertation in a right manner.

I am thankful to my tutor, friends and relatives who gave me guidance and support for

this project. In completing my dissertation on the suitability of equity and bond valuation

pertaining to short and long run they always encouraged me to do it in the best possible way. In

addition to this, I also appreciate my mentor for giving me guidance in preparing dissertation.

From his support and experience I was in the position to complete dissertation in a right manner.

ABSTRACT

In the present era, investors undertake valuation techniques to assess the suitability of an

investment when investment horizon is short. In this, to analyze the level to which valuation

techniques help in predicting return for short investment horizon deductive approach and

positivism philosophy has been used. In this, to analyze the suitability and effectiveness of

valuation techniques in predicting returns for short duration data has been collected by the

researcher from secondary sources. By applying the financial tools like DCF and bond valuation

techniques researcher has assessed the extent to which they give optimal solution in short term

investments. From evaluation, it can be stated that DCF model is highly effectual which in turn

provides investors with appropriate signal when horizon of investment is short. In addition to

this, outcome of DCF model can also be supported with the secondary data findings that entails it

is highly significant and assists in measuring the business risk more effectually. DCF model

considers both short and long term factors that have impact on the operations of firm. Thus, by

using such model investors can make idea about the suitability of investment when horizon is

short. Data pertaining to the five companies like IHG, AZN, BAE system, Associated British

food and Admiral group shows that intrinsic value of majority of the companies are same under

both horizon. Thus, it can be stated that valuation techniques present fair view in both short and

long investment horizon.

In the present era, investors undertake valuation techniques to assess the suitability of an

investment when investment horizon is short. In this, to analyze the level to which valuation

techniques help in predicting return for short investment horizon deductive approach and

positivism philosophy has been used. In this, to analyze the suitability and effectiveness of

valuation techniques in predicting returns for short duration data has been collected by the

researcher from secondary sources. By applying the financial tools like DCF and bond valuation

techniques researcher has assessed the extent to which they give optimal solution in short term

investments. From evaluation, it can be stated that DCF model is highly effectual which in turn

provides investors with appropriate signal when horizon of investment is short. In addition to

this, outcome of DCF model can also be supported with the secondary data findings that entails it

is highly significant and assists in measuring the business risk more effectually. DCF model

considers both short and long term factors that have impact on the operations of firm. Thus, by

using such model investors can make idea about the suitability of investment when horizon is

short. Data pertaining to the five companies like IHG, AZN, BAE system, Associated British

food and Admiral group shows that intrinsic value of majority of the companies are same under

both horizon. Thus, it can be stated that valuation techniques present fair view in both short and

long investment horizon.

TABLE OF CONTENTS

CHPATER 1: INTRODUCTION....................................................................................................1

1.1 Background of the study........................................................................................................1

1.2 Research aims and objectives................................................................................................1

1.3 Research questions.................................................................................................................2

1.4 Rationale of the study............................................................................................................2

1.5 Significance of the study.......................................................................................................2

1.6 Structure of dissertation.........................................................................................................3

CHAPTER 2: LITERATURE REVIEW.........................................................................................5

2.1 Introduction............................................................................................................................5

2.2 Valuation techniques that assist in predicting future returns.................................................5

2.3 Suitability of valuation techniques for predicting the return on investments in short horizon

.....................................................................................................................................................7

2.4 Literature gap.........................................................................................................................9

CHAPTER 3: RESEARCH METHODOLOGY...........................................................................10

3.1 Introduction..........................................................................................................................10

3.2 Research type.......................................................................................................................10

3.3 Research approach...............................................................................................................10

3.4 Research philosophy............................................................................................................10

3.4 Data collection.....................................................................................................................11

3.5 Data analysis........................................................................................................................11

3.6 Reliability and validity........................................................................................................12

CHPATER 1: INTRODUCTION....................................................................................................1

1.1 Background of the study........................................................................................................1

1.2 Research aims and objectives................................................................................................1

1.3 Research questions.................................................................................................................2

1.4 Rationale of the study............................................................................................................2

1.5 Significance of the study.......................................................................................................2

1.6 Structure of dissertation.........................................................................................................3

CHAPTER 2: LITERATURE REVIEW.........................................................................................5

2.1 Introduction............................................................................................................................5

2.2 Valuation techniques that assist in predicting future returns.................................................5

2.3 Suitability of valuation techniques for predicting the return on investments in short horizon

.....................................................................................................................................................7

2.4 Literature gap.........................................................................................................................9

CHAPTER 3: RESEARCH METHODOLOGY...........................................................................10

3.1 Introduction..........................................................................................................................10

3.2 Research type.......................................................................................................................10

3.3 Research approach...............................................................................................................10

3.4 Research philosophy............................................................................................................10

3.4 Data collection.....................................................................................................................11

3.5 Data analysis........................................................................................................................11

3.6 Reliability and validity........................................................................................................12

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

3.7 Ethical considerations..........................................................................................................12

3.8 Research limitations.............................................................................................................12

CHAPTER 4: DATA ANALYSIS AND FINDINGS...................................................................13

CHAPTER 5: CONCLUSION AND RECOMMENDATIONS...................................................26

REFERENCES..............................................................................................................................28

3.8 Research limitations.............................................................................................................12

CHAPTER 4: DATA ANALYSIS AND FINDINGS...................................................................13

CHAPTER 5: CONCLUSION AND RECOMMENDATIONS...................................................26

REFERENCES..............................................................................................................................28

Research title: Do valuation techniques for bonds and equities generate investment predictions

for short-term?

CHPATER 1: INTRODUCTION

1.1 Background of the study

In the present times, with the motive to get high returns from investment, investors

undertake three stock market components namely dividend payout, earning growth, cash flows

and price-earnings ratio. All such three are the main indicators that provide deeper insight to the

investors about the extent to which concerned equity investment will prove to be beneficial for

them. Moreover, such valuation technique indicates the trend in which business unit is

performing and offering higher returns to the investors. PE ratio is one of the most effectual

indicators that furnish information about then manner in which stock valued in the market. Along

with this, such ratio also helps in assessing the amount that investors are willing to pay for

company’s earning (Arce, Mayordomo, and Peña, 2013). However, equity market predictability

though such valuation technique is appropriate when time horizon of investment is long. In

addition to this, in the case of bond valuation predictability through different techniques is

possible when the period of investment is long. In this, dissertation will present the level to

which valuation techniques are suitable for the prediction of investment return in short run. It

will also depict the techniques through which future value of an investment can be assessed and

predictability for the same improved.

1.2 Research aims and objectives

The main aim behind carrying out the present study is to assess the extent to which

valuation techniques assist in predicting investment returns for short-term horizon.

Research objectives

To evaluate existing valuation techniques for predicting the future value of investment.

To evaluate the suitability of valuation techniques for the predicting the return

investments having short horizon.

for short-term?

CHPATER 1: INTRODUCTION

1.1 Background of the study

In the present times, with the motive to get high returns from investment, investors

undertake three stock market components namely dividend payout, earning growth, cash flows

and price-earnings ratio. All such three are the main indicators that provide deeper insight to the

investors about the extent to which concerned equity investment will prove to be beneficial for

them. Moreover, such valuation technique indicates the trend in which business unit is

performing and offering higher returns to the investors. PE ratio is one of the most effectual

indicators that furnish information about then manner in which stock valued in the market. Along

with this, such ratio also helps in assessing the amount that investors are willing to pay for

company’s earning (Arce, Mayordomo, and Peña, 2013). However, equity market predictability

though such valuation technique is appropriate when time horizon of investment is long. In

addition to this, in the case of bond valuation predictability through different techniques is

possible when the period of investment is long. In this, dissertation will present the level to

which valuation techniques are suitable for the prediction of investment return in short run. It

will also depict the techniques through which future value of an investment can be assessed and

predictability for the same improved.

1.2 Research aims and objectives

The main aim behind carrying out the present study is to assess the extent to which

valuation techniques assist in predicting investment returns for short-term horizon.

Research objectives

To evaluate existing valuation techniques for predicting the future value of investment.

To evaluate the suitability of valuation techniques for the predicting the return

investments having short horizon.

To estimate & compare the value of selected bonds & stocks for short-term and long-

term.

To investigate whether forecast based on yield and other techniques provide suitable

short term signals or not.

To recommend the ways through which short term predictability can be enhanced.

1.3 Research questions

By taking into account the research aim and objectives following questions have been

drafted by the scholar. Such questions will provide direction to the researcher during whole

study:

Question 1: What is the significance of Valuation ratios in the case of short investment horizon?

Question 2: Which kind of techniques can be undertaken by the investors to predict the return

when investment horizon is short?

1.4 Rationale of the study

The rationale behind conducting the present study is to highlight whether valuation

techniques helps in predicting the return on short term investment or not. It is the researcher

issues because usually PE ratio, dividend payout ratio etc helps in making appropriate estimation

of return only when the time horizon of investment in long. It is the major issue now because in

the absence of having appropriate short term signals investors would not be in position to assess

return on concerned investment. Thus, by conducting secondary data investigation scholar will

present the ways through which short term predictability regarding the investment can be

improved. Hence, by using such measures investors would become able to take suitable decision

in the near future.

1.5 Significance of the study

The present study and its outcome are significant which in turn offers benefit to several

stakeholders such as investors, other scholars etc. Moreover, in the case of bond and stock

investors take decision about investment by predicting the level of return. Thus, study and its

outcome will provide deeper insight to the investors through which they can make appropriate

estimation about the returns when duration of investment is short. In addition to this, other

scholars who are going to do study on similar topic also would become able to get high level of

term.

To investigate whether forecast based on yield and other techniques provide suitable

short term signals or not.

To recommend the ways through which short term predictability can be enhanced.

1.3 Research questions

By taking into account the research aim and objectives following questions have been

drafted by the scholar. Such questions will provide direction to the researcher during whole

study:

Question 1: What is the significance of Valuation ratios in the case of short investment horizon?

Question 2: Which kind of techniques can be undertaken by the investors to predict the return

when investment horizon is short?

1.4 Rationale of the study

The rationale behind conducting the present study is to highlight whether valuation

techniques helps in predicting the return on short term investment or not. It is the researcher

issues because usually PE ratio, dividend payout ratio etc helps in making appropriate estimation

of return only when the time horizon of investment in long. It is the major issue now because in

the absence of having appropriate short term signals investors would not be in position to assess

return on concerned investment. Thus, by conducting secondary data investigation scholar will

present the ways through which short term predictability regarding the investment can be

improved. Hence, by using such measures investors would become able to take suitable decision

in the near future.

1.5 Significance of the study

The present study and its outcome are significant which in turn offers benefit to several

stakeholders such as investors, other scholars etc. Moreover, in the case of bond and stock

investors take decision about investment by predicting the level of return. Thus, study and its

outcome will provide deeper insight to the investors through which they can make appropriate

estimation about the returns when duration of investment is short. In addition to this, other

scholars who are going to do study on similar topic also would become able to get high level of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assistance from such study and its findings. Moreover, study will develop their understanding

about the valuation techniques that can be used to assess short term signals. Hence, study and its

findings will help other scholars in assessing gap and thereby assists them in developing suitable

hypothesis for further research.

1.6 Structure of dissertation

Chapter 1: Introduction

In the first chapter of dissertation, scholar frames and presents objectives behind

undertaking the present study. Besides this, researcher has also mentioned background and

significance of introductory section. Further, in this, structure has also been mentioned by the

researcher in this chapter.

Chapter 2: Literature review

Under the second chapter of dissertation, scholar will summarize the findings mentioned

books, journals and scholarly articles that are related to valuation ratios as well as forecasting of

return. Hence, by developing several themes as per the research objectives secondary data

analysis has been conducted.

Chapter 3: Research methodology

Researcher mentioned all the tools and techniques, in this chapter, that have been

undertaken to find out the level to which valuation ratios and other techniques support short term

predictability. In this, approach, philosophy, data collection and analysis techniques have been

mentioned by the researcher that suitable for the present study.

Chapter 4: Data analysis and findings

This chapter of dissertation is the main parts that clear present the outcome of issue

which is going to be investigated. In this, by doing empirical analysis scholar has presented the

level to which valuation ratios are suitable in making prediction about return on investment in

short horizon. Besides this, graphs and charts also have been added by the researcher to develop

better understanding about the issue.

Chapter 5: Conclusion and recommendations

about the valuation techniques that can be used to assess short term signals. Hence, study and its

findings will help other scholars in assessing gap and thereby assists them in developing suitable

hypothesis for further research.

1.6 Structure of dissertation

Chapter 1: Introduction

In the first chapter of dissertation, scholar frames and presents objectives behind

undertaking the present study. Besides this, researcher has also mentioned background and

significance of introductory section. Further, in this, structure has also been mentioned by the

researcher in this chapter.

Chapter 2: Literature review

Under the second chapter of dissertation, scholar will summarize the findings mentioned

books, journals and scholarly articles that are related to valuation ratios as well as forecasting of

return. Hence, by developing several themes as per the research objectives secondary data

analysis has been conducted.

Chapter 3: Research methodology

Researcher mentioned all the tools and techniques, in this chapter, that have been

undertaken to find out the level to which valuation ratios and other techniques support short term

predictability. In this, approach, philosophy, data collection and analysis techniques have been

mentioned by the researcher that suitable for the present study.

Chapter 4: Data analysis and findings

This chapter of dissertation is the main parts that clear present the outcome of issue

which is going to be investigated. In this, by doing empirical analysis scholar has presented the

level to which valuation ratios are suitable in making prediction about return on investment in

short horizon. Besides this, graphs and charts also have been added by the researcher to develop

better understanding about the issue.

Chapter 5: Conclusion and recommendations

In the final chapter of dissertation, scholar concluded the findings that are assessed

through the means of investigation about the suitability of valuation techniques for short term

investment. In addition to this, recommendations have also been provided about the aspects

through investors can make appropriate prediction about future returns.

through the means of investigation about the suitability of valuation techniques for short term

investment. In addition to this, recommendations have also been provided about the aspects

through investors can make appropriate prediction about future returns.

CHAPTER 2: LITERATURE REVIEW

2.1 Introduction

Literature review may be defined as a process that is undertaken by the scholar to prepare

brief thesis on the basis of secondary data findings. Moreover, in this scholar makes evaluation

of journals and scholarly articles that are related to the research topic or issue. In this, scholar has

prepared theme in relation to valuation techniques that can be used by the investors for equity

and bond valuation. Hence, in this, research has summarized articles that are highly related to the

research issue.

2.2 Valuation techniques that assist in predicting future returns

According to the views of Jordan (2014) by undertaking P/E ratio technique investors can

assess the market value of stock in relation to its earnings. Hence, by dividing market price per

share in against to EPS P/E ratio can be assessed by the investors. Further, by using such ratio

analysts can make idea about the value that investors are willing to pay in accordance with the

current earning level of company. Usually, investors use this ratio to identify the fair market

value of stock. Hence, by employing such measure future earnings per share can be predicted by

the investors. This in turn helps investors to take suitable decision about investment that make

value addition in money. Moreover, companies with higher future earnings having possibility

that it will offer high dividend and appreciate stock in the near future. By considering this, it can

be said that P/E ratio measure helps investors in analyzing the amount that they should pay for

the company’s stock.

On the other side, Jordan (2014) mentioned in their study that dividend payout ratio

provides assistance to the investors in predicting future value or return. Moreover, such measure

indicates the percentage of net income that is distributed by the company to shareholders in the

form of dividend. Such ratio clearly depicts the fund that will be used by the firm for the

management of business operations and functions. Besides this, it also helps investors in

identifying the portion of profit that firm will use to distribute among the shareholders. This

valuation technique is highly significant which in turn provides information to the investors that

whether business units are offering enough return to the investors out of net profit or not.

2.1 Introduction

Literature review may be defined as a process that is undertaken by the scholar to prepare

brief thesis on the basis of secondary data findings. Moreover, in this scholar makes evaluation

of journals and scholarly articles that are related to the research topic or issue. In this, scholar has

prepared theme in relation to valuation techniques that can be used by the investors for equity

and bond valuation. Hence, in this, research has summarized articles that are highly related to the

research issue.

2.2 Valuation techniques that assist in predicting future returns

According to the views of Jordan (2014) by undertaking P/E ratio technique investors can

assess the market value of stock in relation to its earnings. Hence, by dividing market price per

share in against to EPS P/E ratio can be assessed by the investors. Further, by using such ratio

analysts can make idea about the value that investors are willing to pay in accordance with the

current earning level of company. Usually, investors use this ratio to identify the fair market

value of stock. Hence, by employing such measure future earnings per share can be predicted by

the investors. This in turn helps investors to take suitable decision about investment that make

value addition in money. Moreover, companies with higher future earnings having possibility

that it will offer high dividend and appreciate stock in the near future. By considering this, it can

be said that P/E ratio measure helps investors in analyzing the amount that they should pay for

the company’s stock.

On the other side, Jordan (2014) mentioned in their study that dividend payout ratio

provides assistance to the investors in predicting future value or return. Moreover, such measure

indicates the percentage of net income that is distributed by the company to shareholders in the

form of dividend. Such ratio clearly depicts the fund that will be used by the firm for the

management of business operations and functions. Besides this, it also helps investors in

identifying the portion of profit that firm will use to distribute among the shareholders. This

valuation technique is highly significant which in turn provides information to the investors that

whether business units are offering enough return to the investors out of net profit or not.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

However, on the critical note, Chen (2009) said that dividend pay-out ratio of the company

fluctuates in line with the net income generated during the year. Hence, investors can also make

prediction about future returns by employing dividend growth model. By using this, investors

can assess the fair value of stock by assuming the aspect that either dividend grows at stable or

different rates. This model of equity valuation includes mainly three elements such as DPS,

growth % in dividend and rate of return expected. This model of equity valuation is highly

effectual because it clearly indicates whether they should purchase or make investment in

company’s stock or not.

On the other side, Hussainey, Oscar Mgbame and Chijoke-Mgbame (2011) depicted that

Gordon growth model assumes that firm will offer dividend on a stable rate. In real life, it is not

possible for the organization to follow stable dividend policy. The main reason behind this, net

income of the company fluctuates from one year to another. Besides this, dividend decision of

the company is highly based on the net income generated during the year. Thus, it is one of the

main aspects that affect the significance of such valuation technique. By considering such aspect,

Cooper, Gulen and Schill (2008) mentioned in their study that price earnings growth ratio is one

of the most effective measures that provide suitable view of financial aspects as compared to PE

ratio. In this, by dividing P/E ratio from growth rate in earnings investors can determine the

suitable value of stock. In this, lower price earnings growth (PEG) ratio stock is considered as

undervalued. PEG is the most effectual valuation metric that helps in assessing the relative trade-

off which takes place between the price of stock, EPS and expected growth rate. Thus, it can be

stated that PEG ratio presents value by taking into account future growth and helps investors in

gauging whether high growth stocks may be undervalued or not.

Further, Lier and Grünewald (2011) found in their study that by using present value

technique one can perform bond valuation in an effectual way. Moreover, present value

technique helps investors in determining the suitable price of bond. The reason behind this, such

method or tool exhibits the return will be generated by the investors through purchasing bonds.

Hence, by discounting the future cash flows on the basis of assumption that each interest will be

re-invested at specific rate value can be determined. Hence, by undertaking the time value of

money concept investors can assess bond value and associated return more effectually.

fluctuates in line with the net income generated during the year. Hence, investors can also make

prediction about future returns by employing dividend growth model. By using this, investors

can assess the fair value of stock by assuming the aspect that either dividend grows at stable or

different rates. This model of equity valuation includes mainly three elements such as DPS,

growth % in dividend and rate of return expected. This model of equity valuation is highly

effectual because it clearly indicates whether they should purchase or make investment in

company’s stock or not.

On the other side, Hussainey, Oscar Mgbame and Chijoke-Mgbame (2011) depicted that

Gordon growth model assumes that firm will offer dividend on a stable rate. In real life, it is not

possible for the organization to follow stable dividend policy. The main reason behind this, net

income of the company fluctuates from one year to another. Besides this, dividend decision of

the company is highly based on the net income generated during the year. Thus, it is one of the

main aspects that affect the significance of such valuation technique. By considering such aspect,

Cooper, Gulen and Schill (2008) mentioned in their study that price earnings growth ratio is one

of the most effective measures that provide suitable view of financial aspects as compared to PE

ratio. In this, by dividing P/E ratio from growth rate in earnings investors can determine the

suitable value of stock. In this, lower price earnings growth (PEG) ratio stock is considered as

undervalued. PEG is the most effectual valuation metric that helps in assessing the relative trade-

off which takes place between the price of stock, EPS and expected growth rate. Thus, it can be

stated that PEG ratio presents value by taking into account future growth and helps investors in

gauging whether high growth stocks may be undervalued or not.

Further, Lier and Grünewald (2011) found in their study that by using present value

technique one can perform bond valuation in an effectual way. Moreover, present value

technique helps investors in determining the suitable price of bond. The reason behind this, such

method or tool exhibits the return will be generated by the investors through purchasing bonds.

Hence, by discounting the future cash flows on the basis of assumption that each interest will be

re-invested at specific rate value can be determined. Hence, by undertaking the time value of

money concept investors can assess bond value and associated return more effectually.

2.3 Suitability of valuation techniques for predicting the return on investments in short horizon

As per the views of Alam, Hassan and Haque (2013), investigated that P/E ratio helps

investors in finding the extent to which stock of business unit is cheaper or expensive in

comparison to its earning level. For instance: if p/e ratio of the stock is 12 then it indicates that

investors are willing to make payment of 12 times of company’s earning to buy a stock. If P/E

ratio of the stock is higher than 12 then it is considered as expensive and vice versa. However,

Albuquerque and et.al., (2016), argued that during the period of inflation, P/E ratio tends to

decrease that does not gives a clear picture for stock valuation. Besides this, as per cooking the

books practices, companies can easily manipulate their return and EPS which distort P/E ratio as

well. Many academicians founded the use of P/E ratio more suitable and appropriate for

performing prediction of investment return for longer duration. It is because, considering the

period of current market the rate of discount changes over time. During weak economic period,

cost of capital along with risk averse behaviour tends to increase, as a result, investors expects

greater premium on equity which leads to increase discounting rate and decline stock prices.

Thus, it becomes clear that low P/E ratios are consistently followed with high return expectations

of investors and high discounting factor.

Ammann (2013), commented that currently, as market took places changes suddenly

therefore, investors are more concerned about future earnings perspective of their investment

holdings, in such case, P/E ratio can’t be taken as an appropriate variable because it just

considers the historical return only. In order to overcome such issue, the study suggested the use

of dividend discount model (DDM) which is a technique to anticipate the current value of

forecasted dividend that is expected to gain in future. The method considered stock undervalued

if the predicted value is above the current market price and encourage investor to buy or vice-

versa. Thus, the technique facilitates scholar to examine potential dividend on their holdings.

Vaguard (2012) stated that price earning ratio is the strongest indicator for predicting future

stock but not for the point estimate hence; cannot be applied for the short-term horizon.

Evidencing it, in the study, researcher estimated stock return over a time period of 10 years

ranging from 2012-2022.

As per the views of Alam, Hassan and Haque (2013), investigated that P/E ratio helps

investors in finding the extent to which stock of business unit is cheaper or expensive in

comparison to its earning level. For instance: if p/e ratio of the stock is 12 then it indicates that

investors are willing to make payment of 12 times of company’s earning to buy a stock. If P/E

ratio of the stock is higher than 12 then it is considered as expensive and vice versa. However,

Albuquerque and et.al., (2016), argued that during the period of inflation, P/E ratio tends to

decrease that does not gives a clear picture for stock valuation. Besides this, as per cooking the

books practices, companies can easily manipulate their return and EPS which distort P/E ratio as

well. Many academicians founded the use of P/E ratio more suitable and appropriate for

performing prediction of investment return for longer duration. It is because, considering the

period of current market the rate of discount changes over time. During weak economic period,

cost of capital along with risk averse behaviour tends to increase, as a result, investors expects

greater premium on equity which leads to increase discounting rate and decline stock prices.

Thus, it becomes clear that low P/E ratios are consistently followed with high return expectations

of investors and high discounting factor.

Ammann (2013), commented that currently, as market took places changes suddenly

therefore, investors are more concerned about future earnings perspective of their investment

holdings, in such case, P/E ratio can’t be taken as an appropriate variable because it just

considers the historical return only. In order to overcome such issue, the study suggested the use

of dividend discount model (DDM) which is a technique to anticipate the current value of

forecasted dividend that is expected to gain in future. The method considered stock undervalued

if the predicted value is above the current market price and encourage investor to buy or vice-

versa. Thus, the technique facilitates scholar to examine potential dividend on their holdings.

Vaguard (2012) stated that price earning ratio is the strongest indicator for predicting future

stock but not for the point estimate hence; cannot be applied for the short-term horizon.

Evidencing it, in the study, researcher estimated stock return over a time period of 10 years

ranging from 2012-2022.

However, again, Arce, Mayordomo, and Peña (2013), criticized DDM by arguing that the

method has no practical importance to examine such stock on which firms are not distributing

any dividend. Therefore, the method has been design on flawed assumption that stock value is

ROI only which is delivered in the form of dividend. Besides this, assumptions of growth rate,

required return might be inaccurate which may affects the quality of valuation.

Likewise, Bernstein (2015), commented that Gordon Growth Model do not consider

outside market conditions, however, in the current era where market took change at a faster

pace, investor cannot ignore the market volatility in valuation therefore, the method is not

founded as an effective technique. Besides this, non-dividend factors are not taken into account

by this method i.e. consumer retention, brand loyalty and others. Moreover, the assumptions of

stable dividend growth not look realistic and justifiable.

Bingham and Kiesel (2013), viewed discounted cash flow (DCF) model realistic and

appropriate technique of stock valuation, more importantly, in the case, where either firm does

not pay any dividend or its dividend distribution pattern indicates irregular trend. Hence, by this

way, it overcomes the shortcoming of DDM which can be applied only for the companies that

pay dividend to the investors. Many financial professionals used the method in order to examine

the attractiveness of investment opportunity. If the model predicts a higher value in comparison

to the current cost of investment, then, it indicates a good investment opportunity or vice-versa.

DCF makes use of FCF (Free Cash Flow) projections & discount it to reflect today’s

prices which are used to perform analysis of investment potential. However, on the critical side,

Brigham and Ehrhardt (2013)< commented that like DDM, the method also uses various

assumptions i.e. future cash flows, timing, cost of capital, growth rate and others. Hence, slightly

error in the assumptions may mislead the results.

Brigham and Houston (2012), enlightened focus on bond valuation that is a way to find

out the fair value of a specific bond. It requires computation of current or present value of the

potential interest payment on the bond. It can be valued following below provided equation:

Bond value: C[1-(1/1+r)t/r] + F/(1+r)t

In order to determine current value of the bond, market rate is used as a discounting

factor. Interest rate can be founded through either stock market or bond market. Coupon rate on

method has no practical importance to examine such stock on which firms are not distributing

any dividend. Therefore, the method has been design on flawed assumption that stock value is

ROI only which is delivered in the form of dividend. Besides this, assumptions of growth rate,

required return might be inaccurate which may affects the quality of valuation.

Likewise, Bernstein (2015), commented that Gordon Growth Model do not consider

outside market conditions, however, in the current era where market took change at a faster

pace, investor cannot ignore the market volatility in valuation therefore, the method is not

founded as an effective technique. Besides this, non-dividend factors are not taken into account

by this method i.e. consumer retention, brand loyalty and others. Moreover, the assumptions of

stable dividend growth not look realistic and justifiable.

Bingham and Kiesel (2013), viewed discounted cash flow (DCF) model realistic and

appropriate technique of stock valuation, more importantly, in the case, where either firm does

not pay any dividend or its dividend distribution pattern indicates irregular trend. Hence, by this

way, it overcomes the shortcoming of DDM which can be applied only for the companies that

pay dividend to the investors. Many financial professionals used the method in order to examine

the attractiveness of investment opportunity. If the model predicts a higher value in comparison

to the current cost of investment, then, it indicates a good investment opportunity or vice-versa.

DCF makes use of FCF (Free Cash Flow) projections & discount it to reflect today’s

prices which are used to perform analysis of investment potential. However, on the critical side,

Brigham and Ehrhardt (2013)< commented that like DDM, the method also uses various

assumptions i.e. future cash flows, timing, cost of capital, growth rate and others. Hence, slightly

error in the assumptions may mislead the results.

Brigham and Houston (2012), enlightened focus on bond valuation that is a way to find

out the fair value of a specific bond. It requires computation of current or present value of the

potential interest payment on the bond. It can be valued following below provided equation:

Bond value: C[1-(1/1+r)t/r] + F/(1+r)t

In order to determine current value of the bond, market rate is used as a discounting

factor. Interest rate can be founded through either stock market or bond market. Coupon rate on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

bond is considered as the interest rate that is required to be paid on principal amount. Bond’s

present value calculation consists of two components that are interest rate and principal amount,

both are discounted at market value.

2.4 Literature gap

From the literature review analysis, it becomes clear that although various studies

conducted in the pasts to predict stock return, security analysis & portfolio management, still,

none of the scholar investigated the suitability of valuation techniques for the stock & bond in

the short-time investment horizon; hence, it still remains an issue. Therefore, this research will

bridge such literature gap by undertaking analysis of various valuation techniques and their

comparison for both the short-term and long-term investment horizon.

present value calculation consists of two components that are interest rate and principal amount,

both are discounted at market value.

2.4 Literature gap

From the literature review analysis, it becomes clear that although various studies

conducted in the pasts to predict stock return, security analysis & portfolio management, still,

none of the scholar investigated the suitability of valuation techniques for the stock & bond in

the short-time investment horizon; hence, it still remains an issue. Therefore, this research will

bridge such literature gap by undertaking analysis of various valuation techniques and their

comparison for both the short-term and long-term investment horizon.

CHAPTER 3: RESEARCH METHODOLOGY

3.1 Introduction

Research methodology may be served as a pathway that has been followed by the scholar

during the whole investigation. It contains the approaches, philosophies and other methods that

have been undertaken by scholars to evaluate whether bond and equity valuation techniques help

in predicting the return for investments having short time horizon. Lastly, the chapter focuses on

research limitations, ethical considerations & the reliability and validity aspects also.

3.2 Research type

Research type can be divided into two types such as qualitative and quantitative that

researcher can undertake during the study. Selection of suitable research type is vital because

other techniques are highly influenced from such aspect specifically approach and philosophy

(Flick, 2015). In this, quantitative research type has been selected by the researcher to investigate

the suitability of valuation techniques for predicting returns in short run. Thus, by doing

evaluation of quantitative figures scholar has presented the extent to which valuation technique

gives suitable short term signals regarding return on investment. In this, numerical information

regarding stock market prices, bond rates, free cash flow, dividend, coupon rates and others will

be used for performing prediction of investment and bond return in the short-time horizon.

3.3 Research approach

In order to conduct study in an effectual way scholar is required to select one of the

research approaches out of two namely inductive and deductive. Both such approaches are highly

influenced from the type and nature of investigation conducted (Gast and Ledford, 2014). In this,

to analyze the level to which valuation techniques help in predicting return for short investment

horizon deductive approach has been used. The main reasons behind the selection of such

research approach are that it assists in conducting and determining suitable solution from

quantitative data set.

3.4 Research philosophy

Interpretivism and positivism are the main two types of philosophies that scholar can

undertake to present the solution of issue. Interpretivism philosophy is suitable when qualitative

3.1 Introduction

Research methodology may be served as a pathway that has been followed by the scholar

during the whole investigation. It contains the approaches, philosophies and other methods that

have been undertaken by scholars to evaluate whether bond and equity valuation techniques help

in predicting the return for investments having short time horizon. Lastly, the chapter focuses on

research limitations, ethical considerations & the reliability and validity aspects also.

3.2 Research type

Research type can be divided into two types such as qualitative and quantitative that

researcher can undertake during the study. Selection of suitable research type is vital because

other techniques are highly influenced from such aspect specifically approach and philosophy

(Flick, 2015). In this, quantitative research type has been selected by the researcher to investigate

the suitability of valuation techniques for predicting returns in short run. Thus, by doing

evaluation of quantitative figures scholar has presented the extent to which valuation technique

gives suitable short term signals regarding return on investment. In this, numerical information

regarding stock market prices, bond rates, free cash flow, dividend, coupon rates and others will

be used for performing prediction of investment and bond return in the short-time horizon.

3.3 Research approach

In order to conduct study in an effectual way scholar is required to select one of the

research approaches out of two namely inductive and deductive. Both such approaches are highly

influenced from the type and nature of investigation conducted (Gast and Ledford, 2014). In this,

to analyze the level to which valuation techniques help in predicting return for short investment

horizon deductive approach has been used. The main reasons behind the selection of such

research approach are that it assists in conducting and determining suitable solution from

quantitative data set.

3.4 Research philosophy

Interpretivism and positivism are the main two types of philosophies that scholar can

undertake to present the solution of issue. Interpretivism philosophy is suitable when qualitative

investigation is conducted. On the other side, scholar is required to consider positivism

philosophy for presenting the fair view of study in the case of quantitative investigation

(Hunleth, 2011). Hence, by keeping in mind the type of investigation such as quantitative

positivism philosophy has been selected by the researcher. Moreover, in this, researcher has

presented solution by doing bond and equity valuation that it helps in predicting the future

returns or not when investment duration is short.

3.4 Data collection

It is the process by which researcher attempt to extract required information for

undertaking the investigation in thoroughly and deeply manner. Data collection sources can be

distinguished into two parts such as primary and secondary. Primary data implies for the one

that researcher gathers through observation, focus group, survey method to specifically meet the

research aims and objectives. Hence, primary data is highly significant which in turn helps in

resolving research issue more effectually. In addition to this, secondary data refers to those that

already gathered, analyzed and published by other scholars (Mackey and Gass, 2015). Hence,

through the means of internet scholar can gather data because it has wide of wide collection of

books, journals and research articles. In this, to analyze the suitability and effectiveness of

valuation techniques in predicting returns for short duration data has been collected by the

researcher from secondary sources. Hence, by evaluating books, journals and scholarly articles

related to valuation techniques and their suitability in assessing predicting returns in short run

secondary data has been collected.

For the investigation, the required data has been extracted from the London Stock

Exchange, Financial Times, Bloomberg and annual financial report of the business so as to create

portfolio and compare return thereon. Thus, by accessing the annual reports of five selected

companies namely IHG, AZN, Associated British food, BAE system and Admiral data

pertaining to income, assets as well debt has been gathered.

3.5 Data analysis

It is the process that lays high level of emphasis on inspecting, cleansing, transforming

and modelling data set for discovering suitable information. Selection of data analysis techniques

are highly influenced from the type of investigation (Neuman and Robson, 2012). Taking into

account the quantitative nature of the study, various valuation techniques has been performed in

philosophy for presenting the fair view of study in the case of quantitative investigation

(Hunleth, 2011). Hence, by keeping in mind the type of investigation such as quantitative

positivism philosophy has been selected by the researcher. Moreover, in this, researcher has

presented solution by doing bond and equity valuation that it helps in predicting the future

returns or not when investment duration is short.

3.4 Data collection

It is the process by which researcher attempt to extract required information for

undertaking the investigation in thoroughly and deeply manner. Data collection sources can be

distinguished into two parts such as primary and secondary. Primary data implies for the one

that researcher gathers through observation, focus group, survey method to specifically meet the

research aims and objectives. Hence, primary data is highly significant which in turn helps in

resolving research issue more effectually. In addition to this, secondary data refers to those that

already gathered, analyzed and published by other scholars (Mackey and Gass, 2015). Hence,

through the means of internet scholar can gather data because it has wide of wide collection of

books, journals and research articles. In this, to analyze the suitability and effectiveness of

valuation techniques in predicting returns for short duration data has been collected by the

researcher from secondary sources. Hence, by evaluating books, journals and scholarly articles

related to valuation techniques and their suitability in assessing predicting returns in short run

secondary data has been collected.

For the investigation, the required data has been extracted from the London Stock

Exchange, Financial Times, Bloomberg and annual financial report of the business so as to create

portfolio and compare return thereon. Thus, by accessing the annual reports of five selected

companies namely IHG, AZN, Associated British food, BAE system and Admiral data

pertaining to income, assets as well debt has been gathered.

3.5 Data analysis

It is the process that lays high level of emphasis on inspecting, cleansing, transforming

and modelling data set for discovering suitable information. Selection of data analysis techniques

are highly influenced from the type of investigation (Neuman and Robson, 2012). Taking into

account the quantitative nature of the study, various valuation techniques has been performed in

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the MS spreadsheet for the portfolio creation considering different variables like price to

earnings, dividend payout ratio and others. However, on the other hand, financial techniques and

methods has been undertaken and applied through excel for the purpose of making comparative

valuation of the bond and equity values for both the short-term and long-term time horizon. The

application of the financial techniques facilitates investigator in examining whether forecasts

depends upon yield and other variables provides substantially significant short-term signals or

not to the investors. Hence, by applying the financial tools like DCF and bond valuation

techniques researcher has assessed the extent to which they give optimal solution in short term

investments.

3.6 Reliability and validity

In order to give value to reliability & validity aspect, required data set regarding stock

price, bond rates and other required information has been extracted from the authentic websites

such as London Stock Exchange, Bloomberg, company’s annual reports and financial times as

well.

3.7 Ethical considerations

Ethnicity is the most important aspect and scholar had cited all the data sources

appropriately to ensure authenticity and no use of manipulated dataset. Besides this, citation have

been provided to give credit to the original investigator. All the information has been accessed

only after the formal acceptance and approval of the authority, for instance, annual report is

available for access after the formal approval of business managers.

3.8 Research limitations

The most important drawback of the study is that it applied valuation techniques for

equities and bonds prediction for the short-term time horizon only. Investigator did not pay

attention on examining the long-term investment prediction. Besides this, lack of sufficient data

availability due to failure of getting approval from the authority might limit the research purpose.

earnings, dividend payout ratio and others. However, on the other hand, financial techniques and

methods has been undertaken and applied through excel for the purpose of making comparative

valuation of the bond and equity values for both the short-term and long-term time horizon. The

application of the financial techniques facilitates investigator in examining whether forecasts

depends upon yield and other variables provides substantially significant short-term signals or

not to the investors. Hence, by applying the financial tools like DCF and bond valuation

techniques researcher has assessed the extent to which they give optimal solution in short term

investments.

3.6 Reliability and validity

In order to give value to reliability & validity aspect, required data set regarding stock

price, bond rates and other required information has been extracted from the authentic websites

such as London Stock Exchange, Bloomberg, company’s annual reports and financial times as

well.

3.7 Ethical considerations

Ethnicity is the most important aspect and scholar had cited all the data sources

appropriately to ensure authenticity and no use of manipulated dataset. Besides this, citation have

been provided to give credit to the original investigator. All the information has been accessed

only after the formal acceptance and approval of the authority, for instance, annual report is

available for access after the formal approval of business managers.

3.8 Research limitations

The most important drawback of the study is that it applied valuation techniques for

equities and bonds prediction for the short-term time horizon only. Investigator did not pay

attention on examining the long-term investment prediction. Besides this, lack of sufficient data

availability due to failure of getting approval from the authority might limit the research purpose.

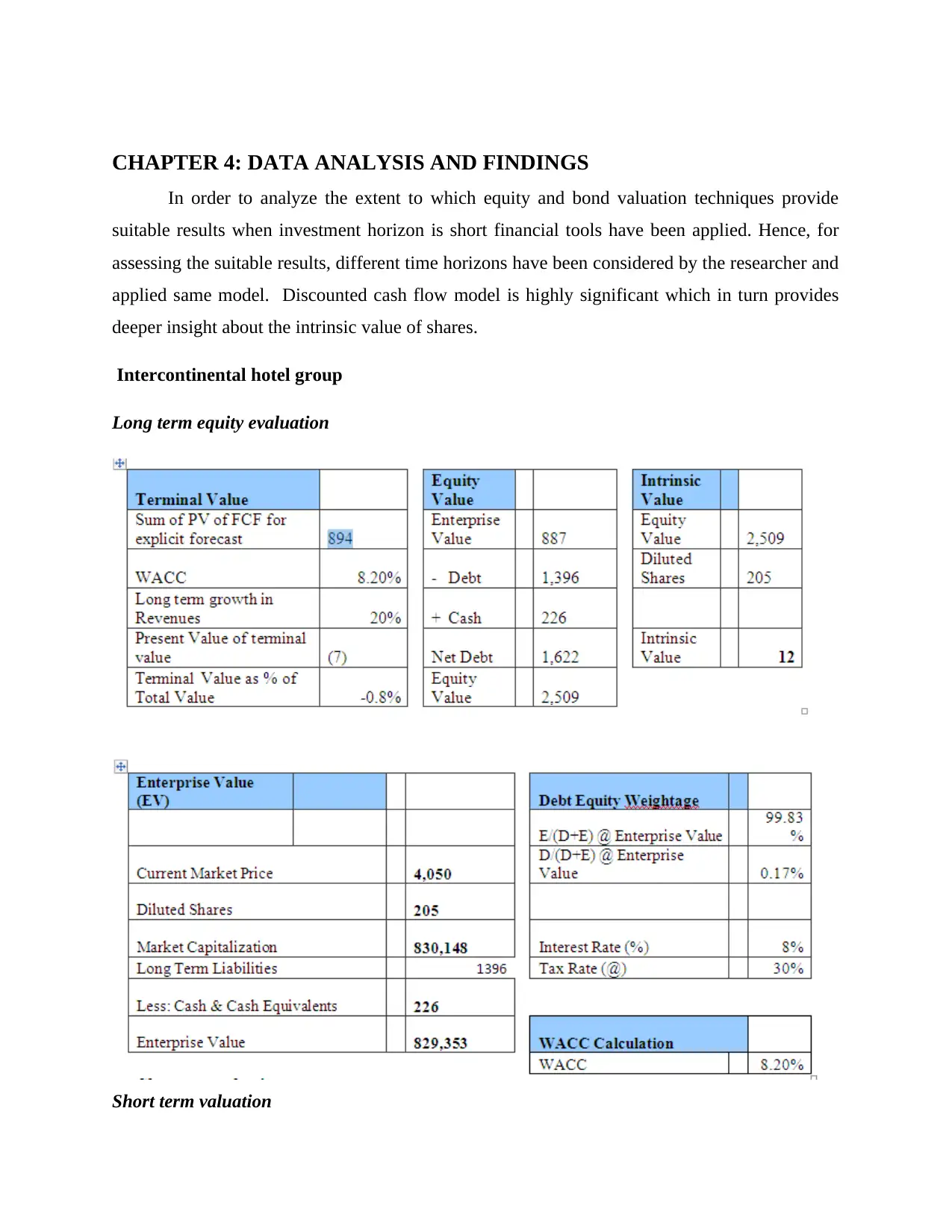

CHAPTER 4: DATA ANALYSIS AND FINDINGS

In order to analyze the extent to which equity and bond valuation techniques provide

suitable results when investment horizon is short financial tools have been applied. Hence, for

assessing the suitable results, different time horizons have been considered by the researcher and

applied same model. Discounted cash flow model is highly significant which in turn provides

deeper insight about the intrinsic value of shares.

Intercontinental hotel group

Long term equity evaluation

Short term valuation

In order to analyze the extent to which equity and bond valuation techniques provide

suitable results when investment horizon is short financial tools have been applied. Hence, for

assessing the suitable results, different time horizons have been considered by the researcher and

applied same model. Discounted cash flow model is highly significant which in turn provides

deeper insight about the intrinsic value of shares.

Intercontinental hotel group

Long term equity evaluation

Short term valuation

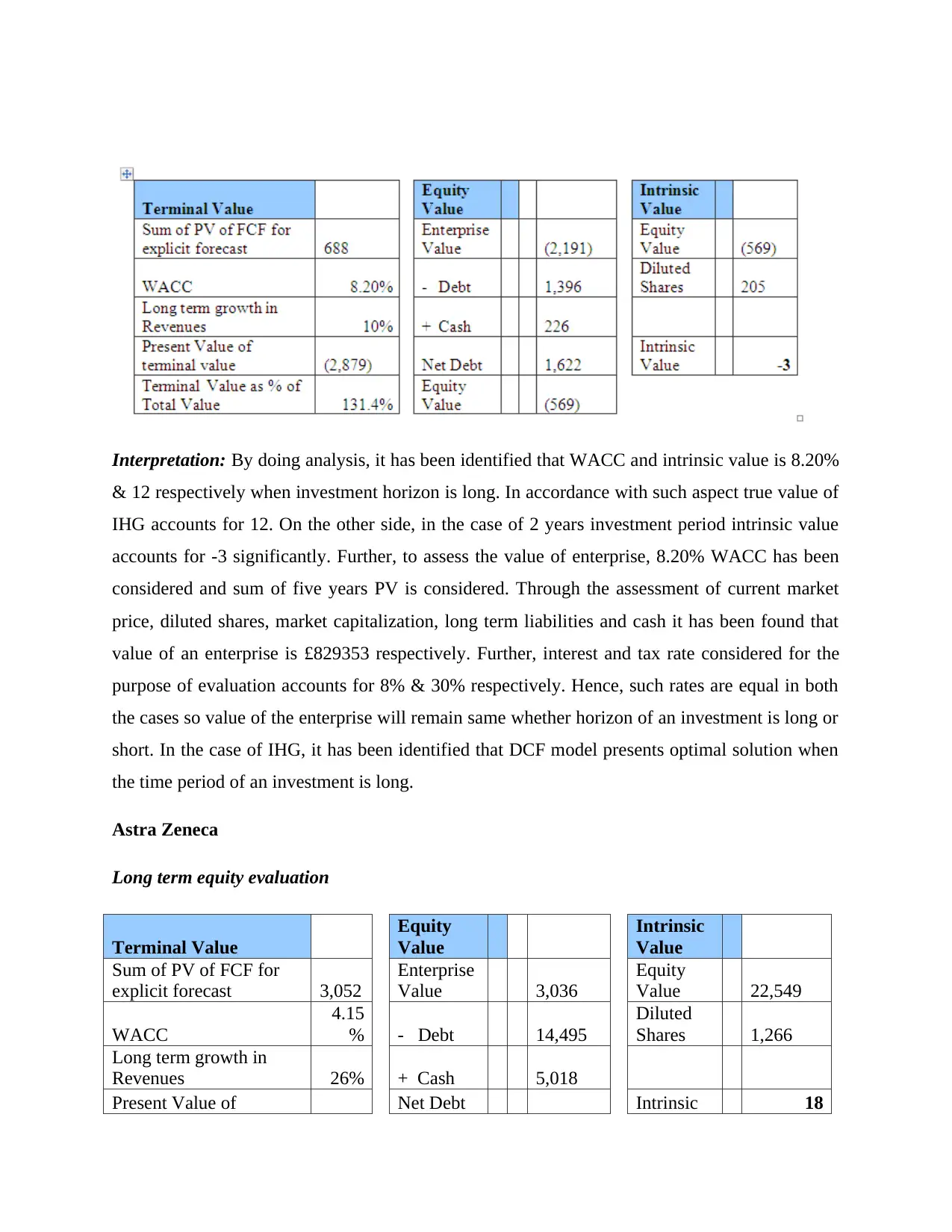

Interpretation: By doing analysis, it has been identified that WACC and intrinsic value is 8.20%

& 12 respectively when investment horizon is long. In accordance with such aspect true value of

IHG accounts for 12. On the other side, in the case of 2 years investment period intrinsic value

accounts for -3 significantly. Further, to assess the value of enterprise, 8.20% WACC has been

considered and sum of five years PV is considered. Through the assessment of current market

price, diluted shares, market capitalization, long term liabilities and cash it has been found that

value of an enterprise is £829353 respectively. Further, interest and tax rate considered for the

purpose of evaluation accounts for 8% & 30% respectively. Hence, such rates are equal in both

the cases so value of the enterprise will remain same whether horizon of an investment is long or

short. In the case of IHG, it has been identified that DCF model presents optimal solution when

the time period of an investment is long.

Astra Zeneca

Long term equity evaluation

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 3,052

Enterprise

Value 3,036

Equity

Value 22,549

WACC

4.15

% - Debt 14,495

Diluted

Shares 1,266

Long term growth in

Revenues 26% + Cash 5,018

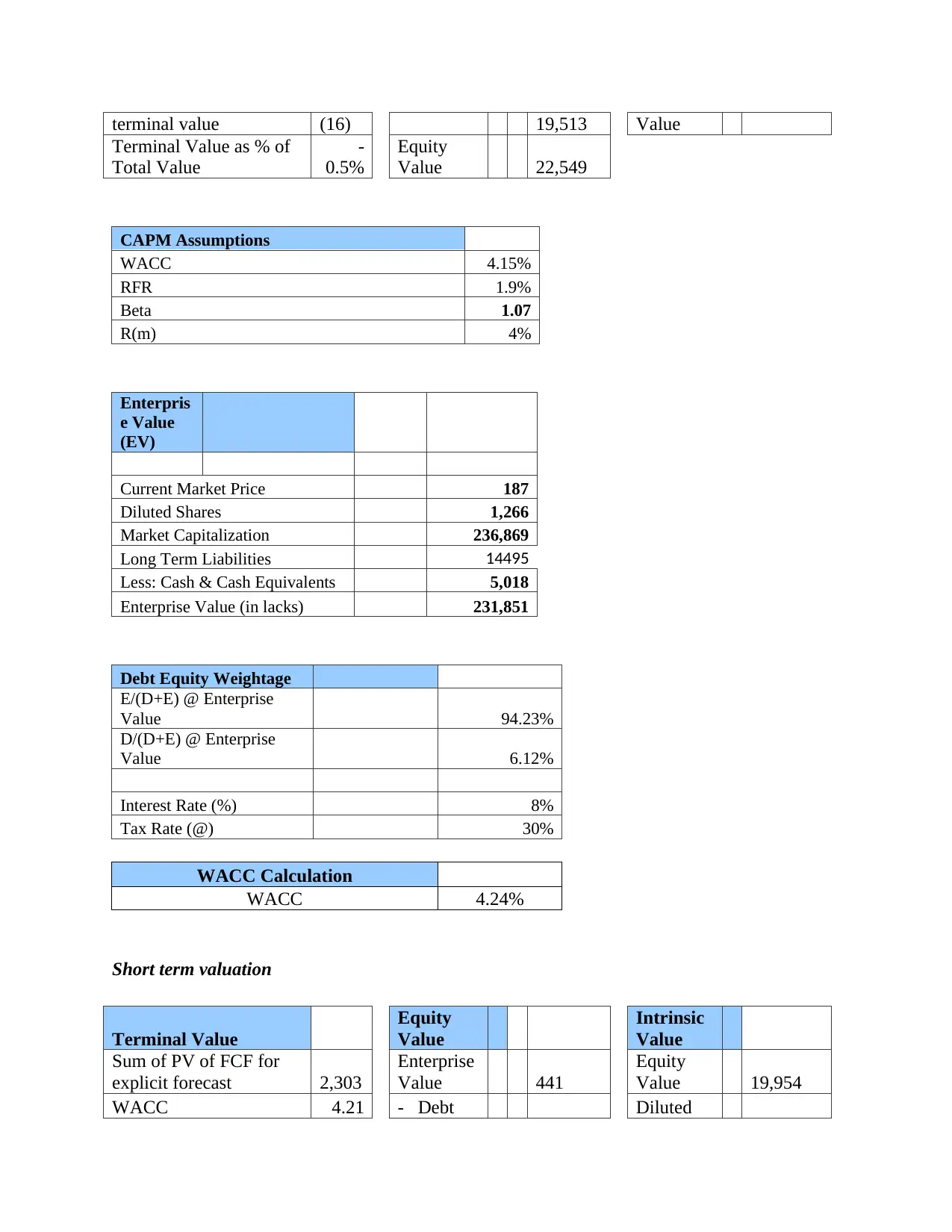

Present Value of Net Debt Intrinsic 18

& 12 respectively when investment horizon is long. In accordance with such aspect true value of

IHG accounts for 12. On the other side, in the case of 2 years investment period intrinsic value

accounts for -3 significantly. Further, to assess the value of enterprise, 8.20% WACC has been

considered and sum of five years PV is considered. Through the assessment of current market

price, diluted shares, market capitalization, long term liabilities and cash it has been found that

value of an enterprise is £829353 respectively. Further, interest and tax rate considered for the

purpose of evaluation accounts for 8% & 30% respectively. Hence, such rates are equal in both

the cases so value of the enterprise will remain same whether horizon of an investment is long or

short. In the case of IHG, it has been identified that DCF model presents optimal solution when

the time period of an investment is long.

Astra Zeneca

Long term equity evaluation

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 3,052

Enterprise

Value 3,036

Equity

Value 22,549

WACC

4.15

% - Debt 14,495

Diluted

Shares 1,266

Long term growth in

Revenues 26% + Cash 5,018

Present Value of Net Debt Intrinsic 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

terminal value (16) 19,513 Value

Terminal Value as % of

Total Value

-

0.5%

Equity

Value 22,549

CAPM Assumptions

WACC 4.15%

RFR 1.9%

Beta 1.07

R(m) 4%

Enterpris

e Value

(EV)

Current Market Price 187

Diluted Shares 1,266

Market Capitalization 236,869

Long Term Liabilities 14495

Less: Cash & Cash Equivalents 5,018

Enterprise Value (in lacks) 231,851

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 94.23%

D/(D+E) @ Enterprise

Value 6.12%

Interest Rate (%) 8%

Tax Rate (@) 30%

WACC Calculation

WACC 4.24%

Short term valuation

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 2,303

Enterprise

Value 441

Equity

Value 19,954

WACC 4.21 - Debt Diluted

Terminal Value as % of

Total Value

-

0.5%

Equity

Value 22,549

CAPM Assumptions

WACC 4.15%

RFR 1.9%

Beta 1.07

R(m) 4%

Enterpris

e Value

(EV)

Current Market Price 187

Diluted Shares 1,266

Market Capitalization 236,869

Long Term Liabilities 14495

Less: Cash & Cash Equivalents 5,018

Enterprise Value (in lacks) 231,851

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 94.23%

D/(D+E) @ Enterprise

Value 6.12%

Interest Rate (%) 8%

Tax Rate (@) 30%

WACC Calculation

WACC 4.24%

Short term valuation

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 2,303

Enterprise

Value 441

Equity

Value 19,954

WACC 4.21 - Debt Diluted

% 14,495 Shares 1,266

Long term growth in

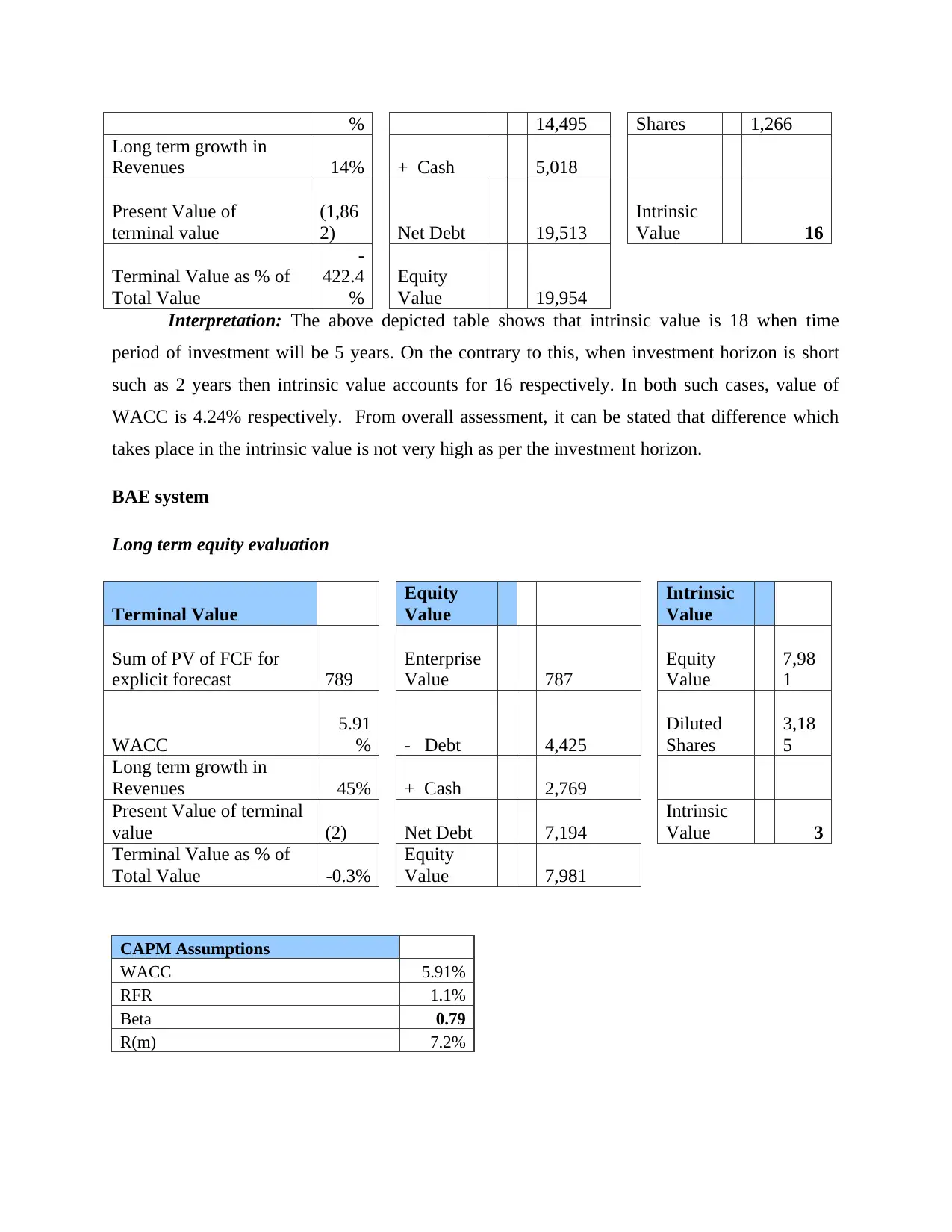

Revenues 14% + Cash 5,018

Present Value of

terminal value

(1,86

2) Net Debt 19,513

Intrinsic

Value 16

Terminal Value as % of

Total Value

-

422.4

%

Equity

Value 19,954

Interpretation: The above depicted table shows that intrinsic value is 18 when time

period of investment will be 5 years. On the contrary to this, when investment horizon is short

such as 2 years then intrinsic value accounts for 16 respectively. In both such cases, value of

WACC is 4.24% respectively. From overall assessment, it can be stated that difference which

takes place in the intrinsic value is not very high as per the investment horizon.

BAE system

Long term equity evaluation

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 789

Enterprise

Value 787

Equity

Value

7,98

1

WACC

5.91

% - Debt 4,425

Diluted

Shares

3,18

5

Long term growth in

Revenues 45% + Cash 2,769

Present Value of terminal

value (2) Net Debt 7,194

Intrinsic

Value 3

Terminal Value as % of

Total Value -0.3%

Equity

Value 7,981

CAPM Assumptions

WACC 5.91%

RFR 1.1%

Beta 0.79

R(m) 7.2%

Long term growth in

Revenues 14% + Cash 5,018

Present Value of

terminal value

(1,86

2) Net Debt 19,513

Intrinsic

Value 16

Terminal Value as % of

Total Value

-

422.4

%

Equity

Value 19,954

Interpretation: The above depicted table shows that intrinsic value is 18 when time

period of investment will be 5 years. On the contrary to this, when investment horizon is short

such as 2 years then intrinsic value accounts for 16 respectively. In both such cases, value of

WACC is 4.24% respectively. From overall assessment, it can be stated that difference which

takes place in the intrinsic value is not very high as per the investment horizon.

BAE system

Long term equity evaluation

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 789

Enterprise

Value 787

Equity

Value

7,98

1

WACC

5.91

% - Debt 4,425

Diluted

Shares

3,18

5

Long term growth in

Revenues 45% + Cash 2,769

Present Value of terminal

value (2) Net Debt 7,194

Intrinsic

Value 3

Terminal Value as % of

Total Value -0.3%

Equity

Value 7,981

CAPM Assumptions

WACC 5.91%

RFR 1.1%

Beta 0.79

R(m) 7.2%

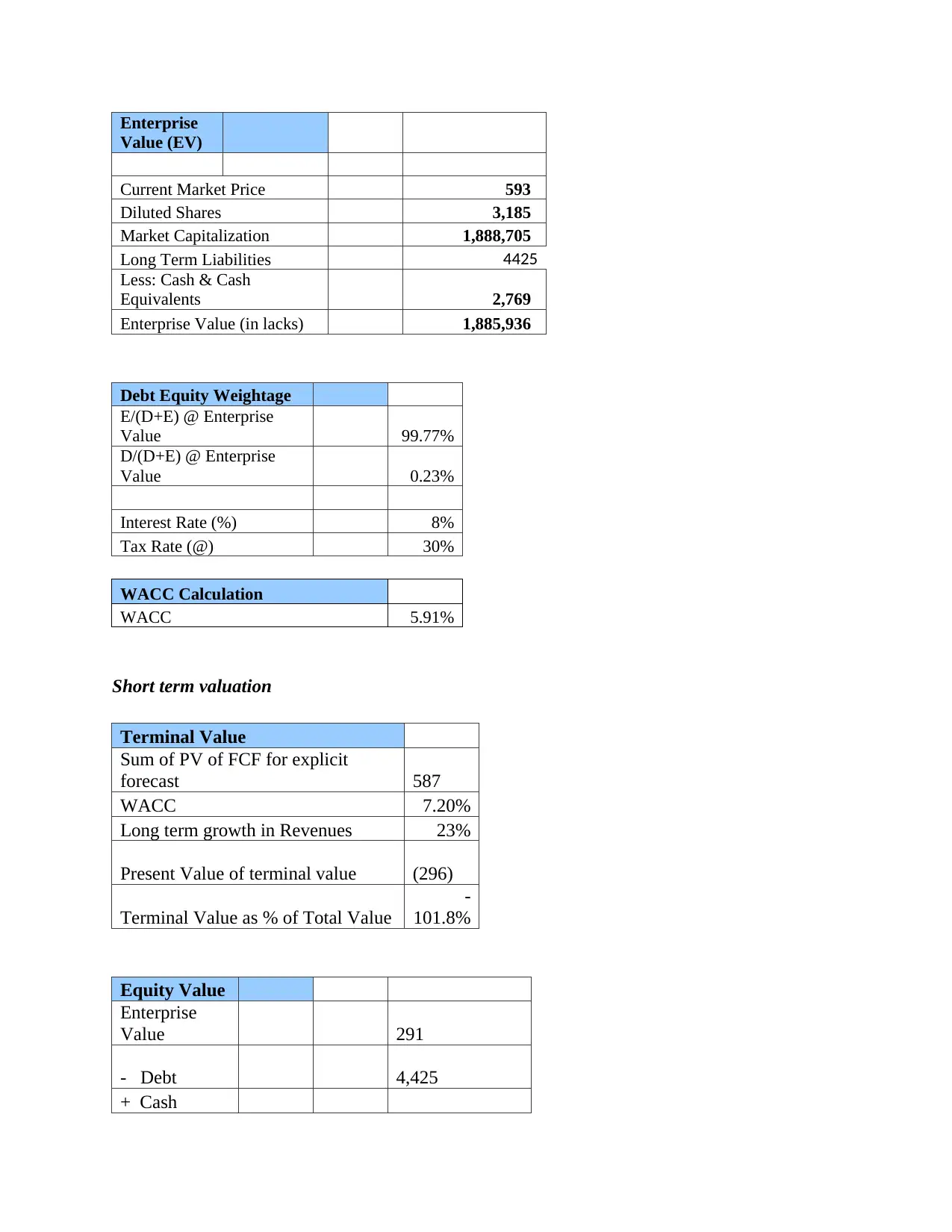

Enterprise

Value (EV)

Current Market Price 593

Diluted Shares 3,185

Market Capitalization 1,888,705

Long Term Liabilities 4425

Less: Cash & Cash

Equivalents 2,769

Enterprise Value (in lacks) 1,885,936

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 99.77%

D/(D+E) @ Enterprise

Value 0.23%

Interest Rate (%) 8%

Tax Rate (@) 30%

WACC Calculation

WACC 5.91%

Short term valuation

Terminal Value

Sum of PV of FCF for explicit

forecast 587

WACC 7.20%

Long term growth in Revenues 23%

Present Value of terminal value (296)

Terminal Value as % of Total Value

-

101.8%

Equity Value

Enterprise

Value 291

- Debt 4,425

+ Cash

Value (EV)

Current Market Price 593

Diluted Shares 3,185

Market Capitalization 1,888,705

Long Term Liabilities 4425

Less: Cash & Cash

Equivalents 2,769

Enterprise Value (in lacks) 1,885,936

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 99.77%

D/(D+E) @ Enterprise

Value 0.23%

Interest Rate (%) 8%

Tax Rate (@) 30%

WACC Calculation

WACC 5.91%

Short term valuation

Terminal Value

Sum of PV of FCF for explicit

forecast 587

WACC 7.20%

Long term growth in Revenues 23%

Present Value of terminal value (296)

Terminal Value as % of Total Value

-

101.8%

Equity Value

Enterprise

Value 291

- Debt 4,425

+ Cash

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

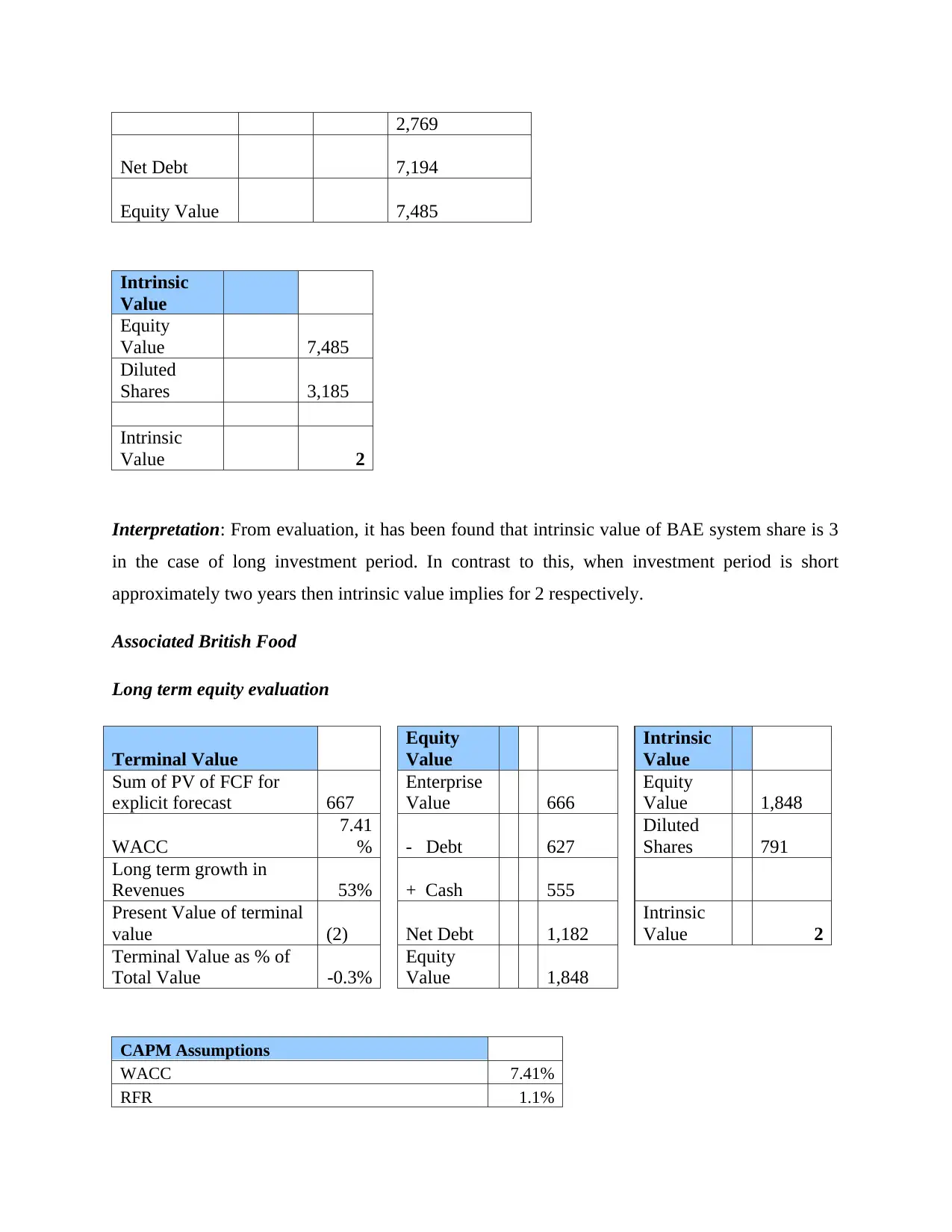

2,769

Net Debt 7,194

Equity Value 7,485

Intrinsic

Value

Equity

Value 7,485

Diluted

Shares 3,185

Intrinsic

Value 2

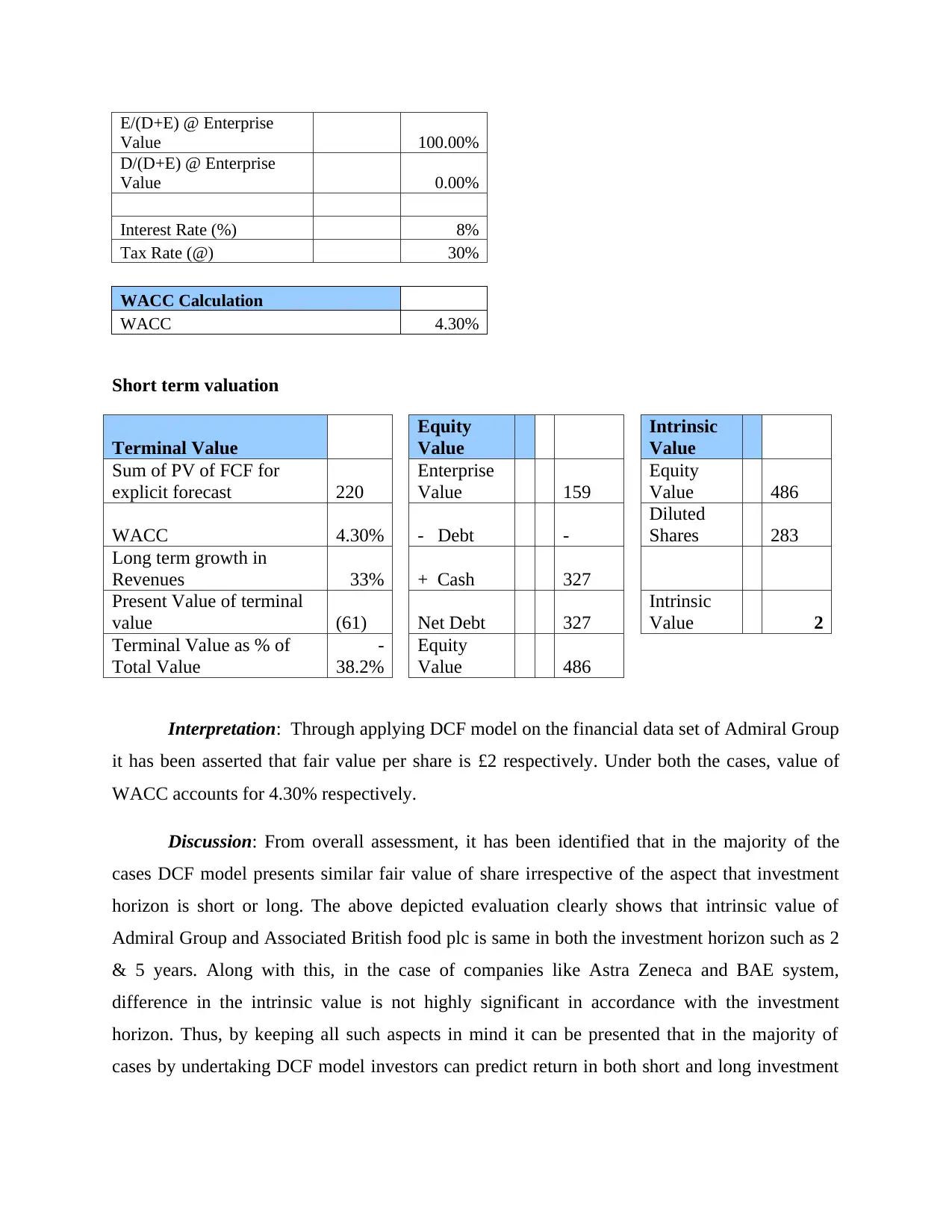

Interpretation: From evaluation, it has been found that intrinsic value of BAE system share is 3

in the case of long investment period. In contrast to this, when investment period is short

approximately two years then intrinsic value implies for 2 respectively.

Associated British Food

Long term equity evaluation

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 667

Enterprise

Value 666

Equity

Value 1,848

WACC

7.41

% - Debt 627

Diluted

Shares 791

Long term growth in

Revenues 53% + Cash 555

Present Value of terminal

value (2) Net Debt 1,182

Intrinsic

Value 2

Terminal Value as % of

Total Value -0.3%

Equity

Value 1,848

CAPM Assumptions

WACC 7.41%

RFR 1.1%

Net Debt 7,194

Equity Value 7,485

Intrinsic

Value

Equity

Value 7,485

Diluted

Shares 3,185

Intrinsic

Value 2

Interpretation: From evaluation, it has been found that intrinsic value of BAE system share is 3

in the case of long investment period. In contrast to this, when investment period is short

approximately two years then intrinsic value implies for 2 respectively.

Associated British Food

Long term equity evaluation

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 667

Enterprise

Value 666

Equity

Value 1,848

WACC

7.41

% - Debt 627

Diluted

Shares 791

Long term growth in

Revenues 53% + Cash 555

Present Value of terminal

value (2) Net Debt 1,182

Intrinsic

Value 2

Terminal Value as % of

Total Value -0.3%

Equity

Value 1,848

CAPM Assumptions

WACC 7.41%

RFR 1.1%

Beta 1.19

R(m) 6.4%

Enterprise

Value (EV)

Current Market Price 3,181

Diluted Shares 791

Market Capitalization 2,516,274

Long Term Liabilities 627

Less: Cash & Cash

Equivalents 555

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 99.98%

D/(D+E) @ Enterprise

Value 0.02%

Interest Rate (%) 8%

Tax Rate (@) 30%

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 494

Enterprise

Value 280

Equity

Value 1,462

WACC

7.41

% - Debt 627

Diluted

Shares 791

Long term growth in

Revenues 25% + Cash 555

Present Value of terminal

value (214) Net Debt 1,182

Intrinsic

Value 2

Terminal Value as % of

Total Value

-

76.4

%

Equity

Value 1,462

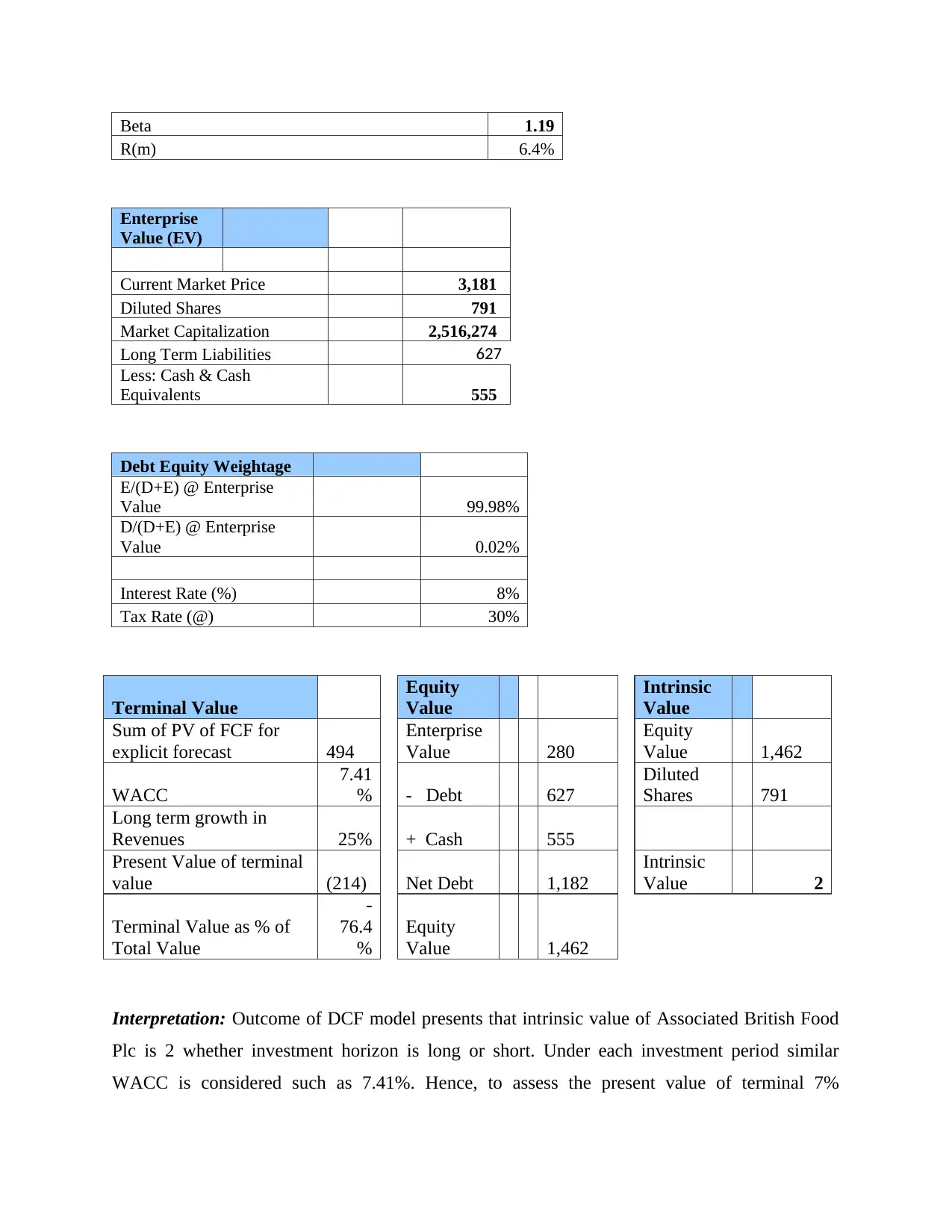

Interpretation: Outcome of DCF model presents that intrinsic value of Associated British Food

Plc is 2 whether investment horizon is long or short. Under each investment period similar

WACC is considered such as 7.41%. Hence, to assess the present value of terminal 7%

R(m) 6.4%

Enterprise

Value (EV)

Current Market Price 3,181

Diluted Shares 791

Market Capitalization 2,516,274

Long Term Liabilities 627

Less: Cash & Cash

Equivalents 555

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 99.98%

D/(D+E) @ Enterprise

Value 0.02%

Interest Rate (%) 8%

Tax Rate (@) 30%

Terminal Value

Equity

Value

Intrinsic

Value

Sum of PV of FCF for

explicit forecast 494

Enterprise

Value 280

Equity

Value 1,462

WACC

7.41

% - Debt 627

Diluted

Shares 791

Long term growth in

Revenues 25% + Cash 555

Present Value of terminal

value (214) Net Debt 1,182

Intrinsic

Value 2

Terminal Value as % of

Total Value

-

76.4

%

Equity

Value 1,462

Interpretation: Outcome of DCF model presents that intrinsic value of Associated British Food

Plc is 2 whether investment horizon is long or short. Under each investment period similar

WACC is considered such as 7.41%. Hence, to assess the present value of terminal 7%

discounting factor is considered. From overall assessment, it can be presented that intrinsic value

of share is 2.

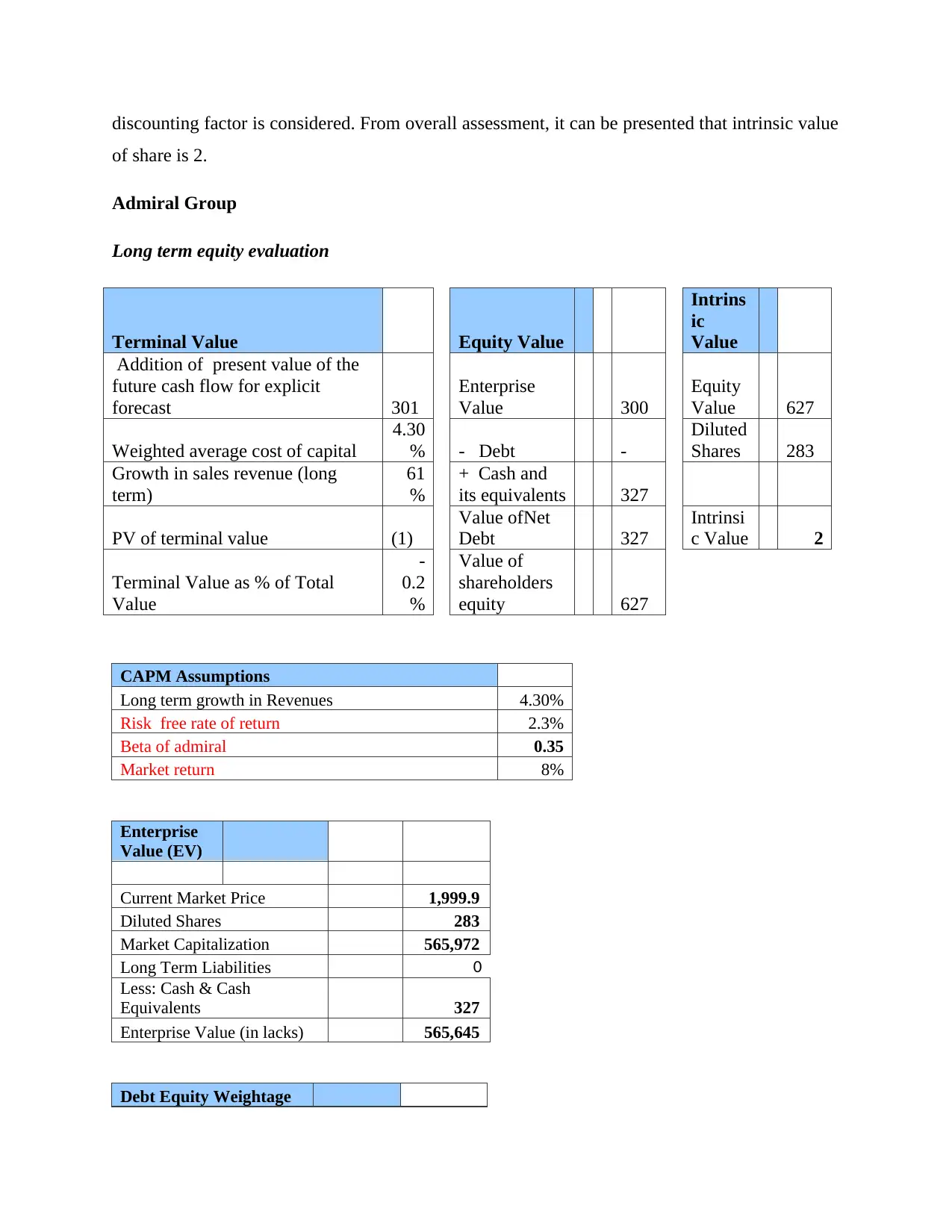

Admiral Group

Long term equity evaluation

Terminal Value Equity Value

Intrins

ic

Value

Addition of present value of the

future cash flow for explicit

forecast 301

Enterprise

Value 300

Equity

Value 627

Weighted average cost of capital

4.30

% - Debt -

Diluted

Shares 283

Growth in sales revenue (long

term)

61

%

+ Cash and

its equivalents 327

PV of terminal value (1)

Value ofNet

Debt 327

Intrinsi

c Value 2

Terminal Value as % of Total

Value

-

0.2

%

Value of

shareholders

equity 627

CAPM Assumptions

Long term growth in Revenues 4.30%

Risk free rate of return 2.3%

Beta of admiral 0.35

Market return 8%

Enterprise

Value (EV)

Current Market Price 1,999.9

Diluted Shares 283

Market Capitalization 565,972

Long Term Liabilities 0

Less: Cash & Cash

Equivalents 327

Enterprise Value (in lacks) 565,645

Debt Equity Weightage

of share is 2.

Admiral Group

Long term equity evaluation

Terminal Value Equity Value

Intrins

ic

Value

Addition of present value of the

future cash flow for explicit

forecast 301

Enterprise

Value 300

Equity

Value 627

Weighted average cost of capital

4.30

% - Debt -

Diluted