Comprehensive Investment Report: CAPM, Dividend, and FCFE Analysis

VerifiedAdded on 2021/04/21

|10

|1731

|24

Report

AI Summary

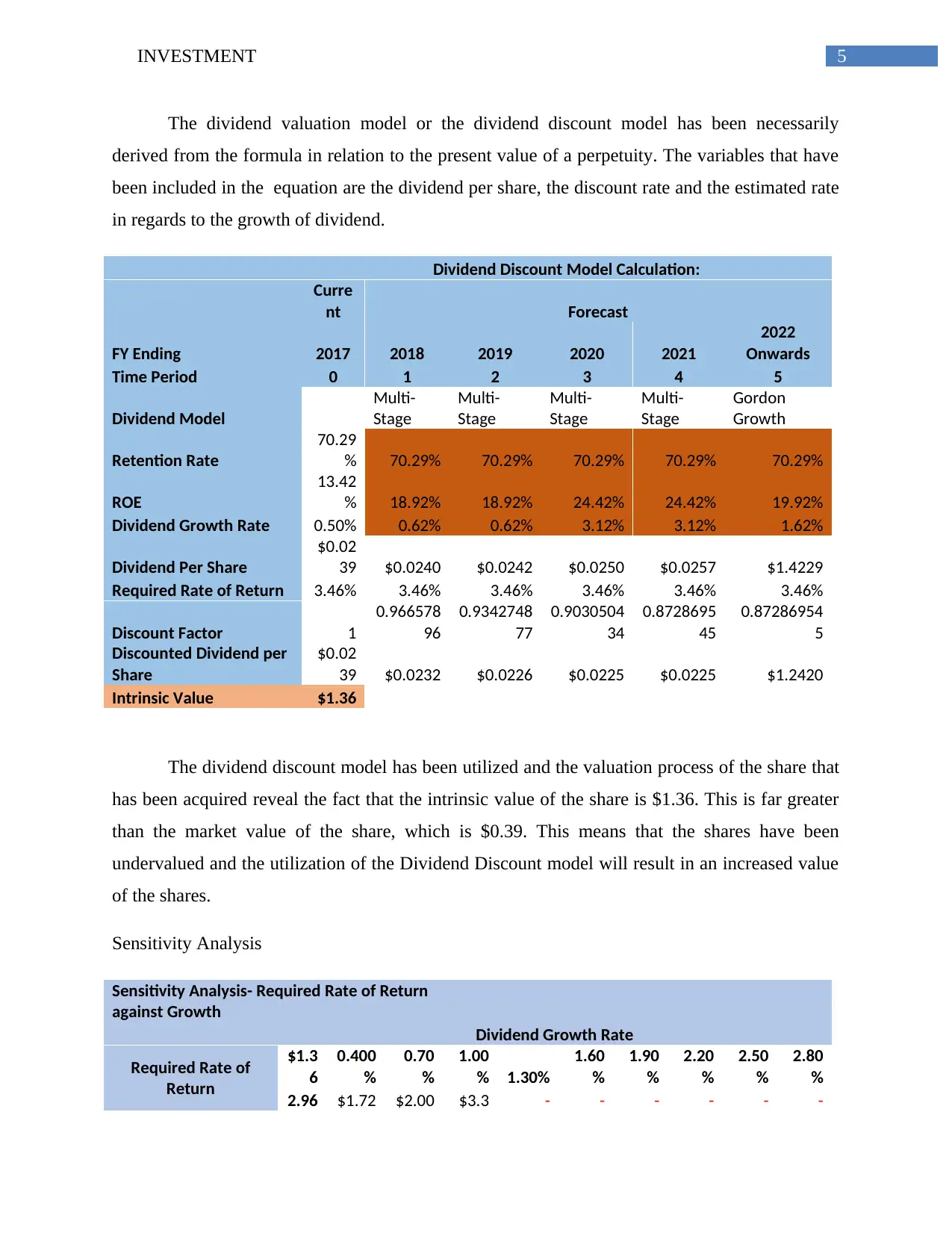

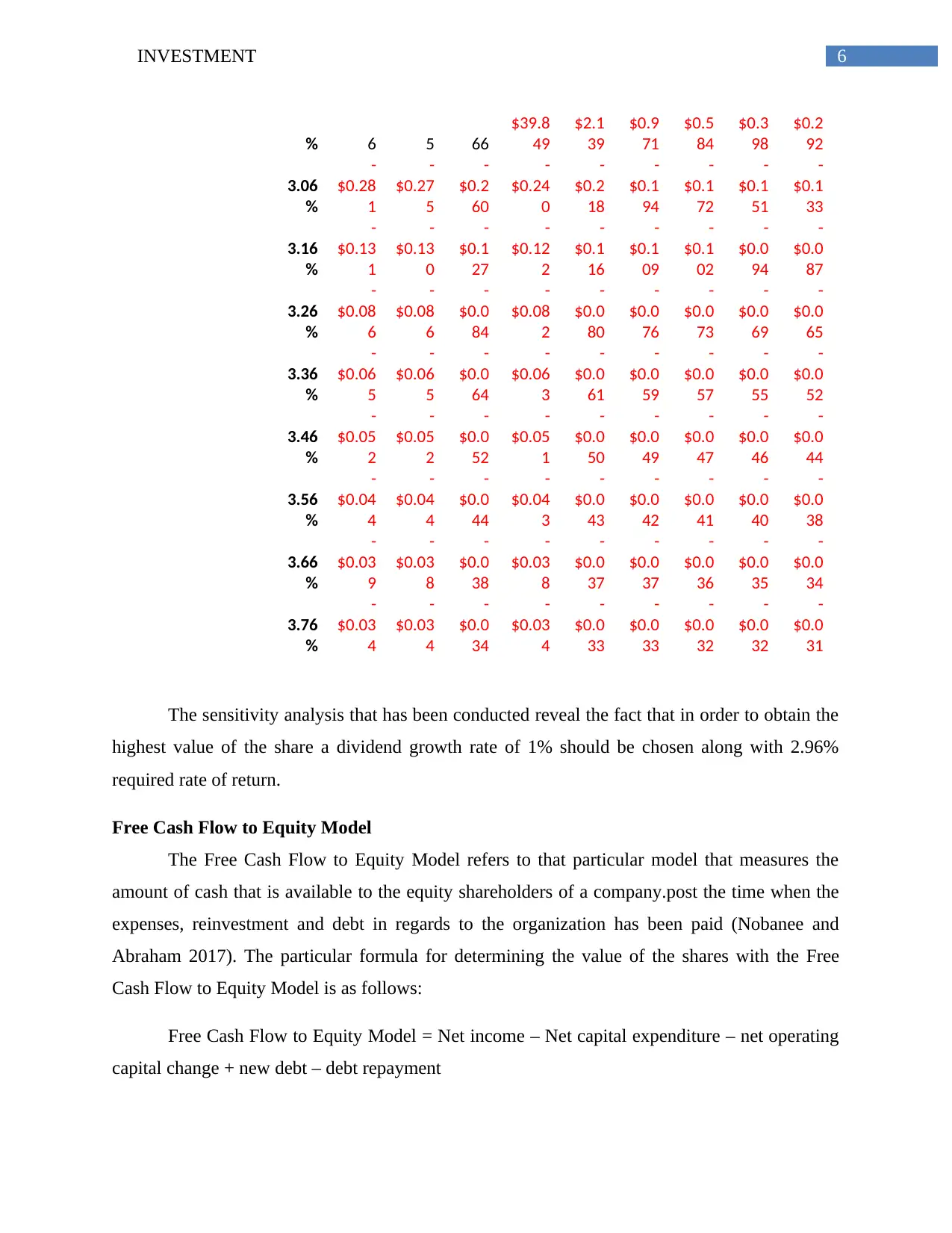

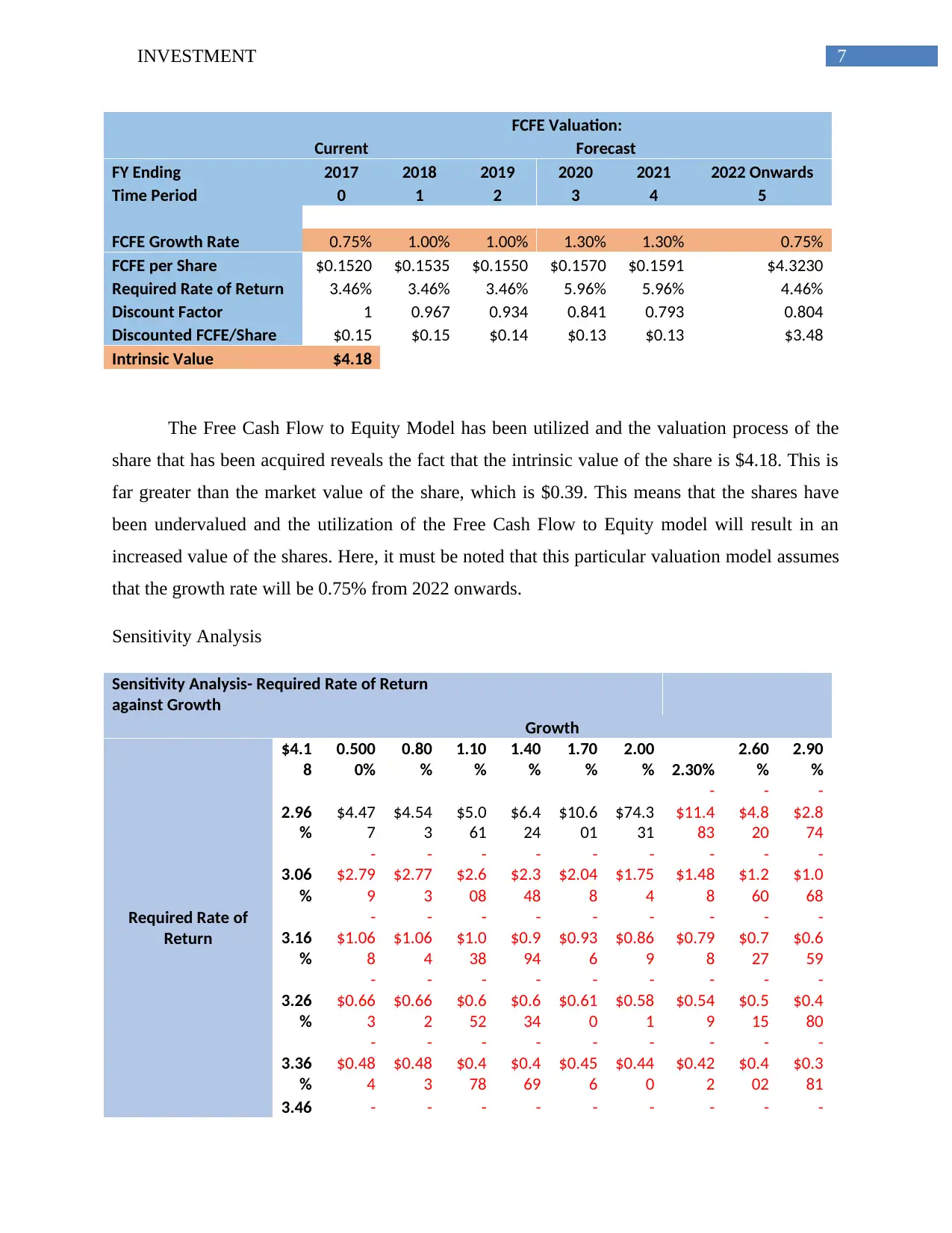

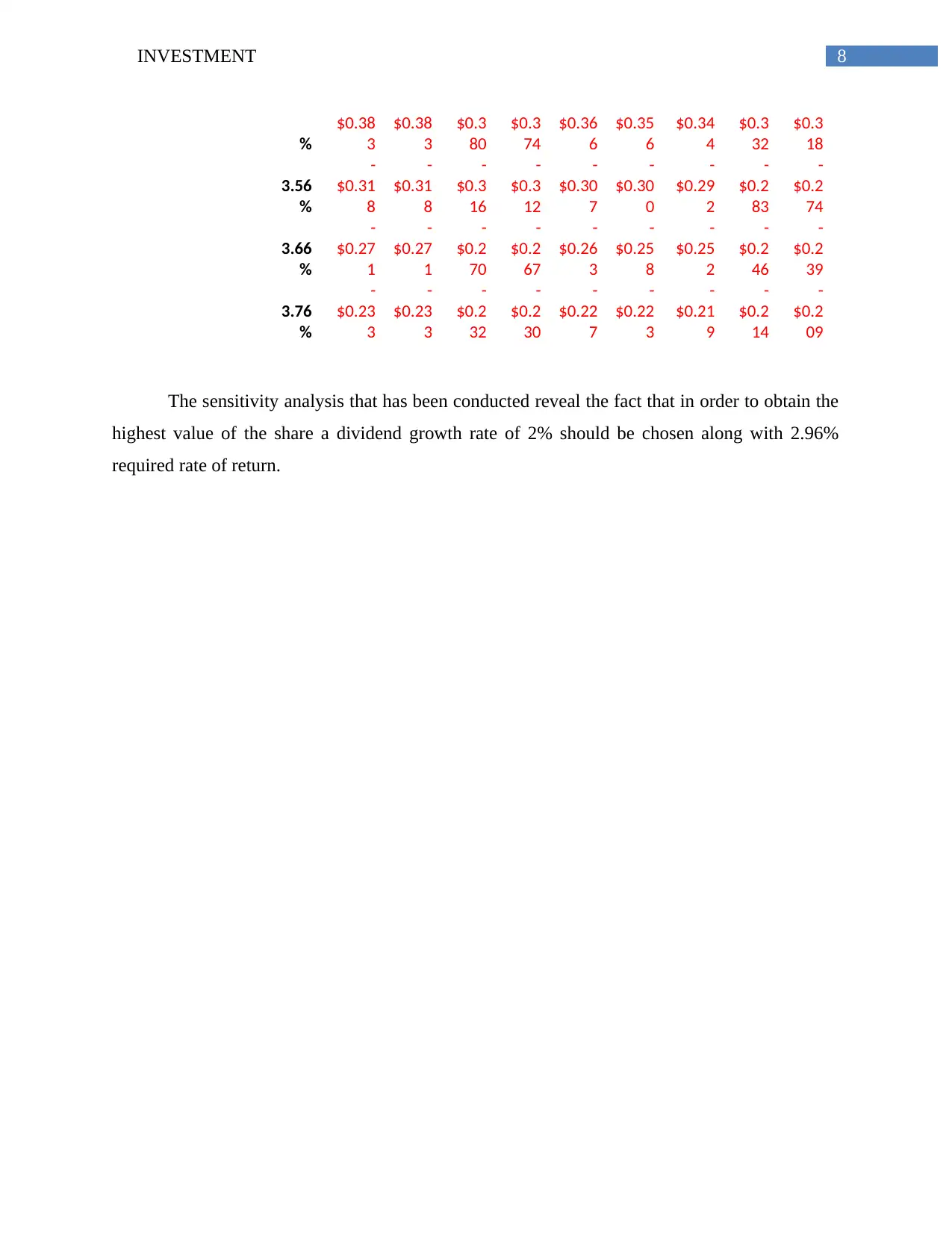

This report presents an investment analysis, employing the Capital Asset Pricing Model (CAPM) to determine the cost of capital, incorporating risk-free rate and estimated beta. The report then proceeds to estimate the value of company shares using two valuation models: the Dividend Discount Model (DDM) and the Free Cash Flow to Equity (FCFE) model. The DDM calculates the intrinsic value based on future dividend payments, while the FCFE model assesses the cash available to equity shareholders. The report includes detailed calculations, assumptions, and sensitivity analyses for both models, comparing the intrinsic values derived from each with the market value to assess whether the shares are undervalued or overvalued. The conclusion highlights the implications of the valuation results and offers insights into the investment potential of the company's shares.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.