Detailed Investment Management Report: Bond Valuation and Strategies

VerifiedAdded on 2020/07/22

|9

|1092

|199

Report

AI Summary

This investment management report provides a comprehensive analysis of bond valuation and investment strategies. It begins with calculating bond prices using provided data, followed by an explanation of the yield curve and an exploration of arbitrage opportunities and dollar profit calculations. Th...

INVESTMENT MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1........................................................................................................................................1

(a)Calculating bond price............................................................................................................1

(B) Yield curve and explaination.................................................................................................1

© Arbitrage and dollar profit.......................................................................................................3

Question 2........................................................................................................................................4

(A)Computation of HPR..............................................................................................................4

© Risk in long and short trading strategy....................................................................................4

Question 3........................................................................................................................................5

(A)Maculay duration...................................................................................................................5

(B) Assessing investment amount...............................................................................................6

© Present value of liability and percentage change in bond portfolio.........................................6

Question 1........................................................................................................................................1

(a)Calculating bond price............................................................................................................1

(B) Yield curve and explaination.................................................................................................1

© Arbitrage and dollar profit.......................................................................................................3

Question 2........................................................................................................................................4

(A)Computation of HPR..............................................................................................................4

© Risk in long and short trading strategy....................................................................................4

Question 3........................................................................................................................................5

(A)Maculay duration...................................................................................................................5

(B) Assessing investment amount...............................................................................................6

© Present value of liability and percentage change in bond portfolio.........................................6

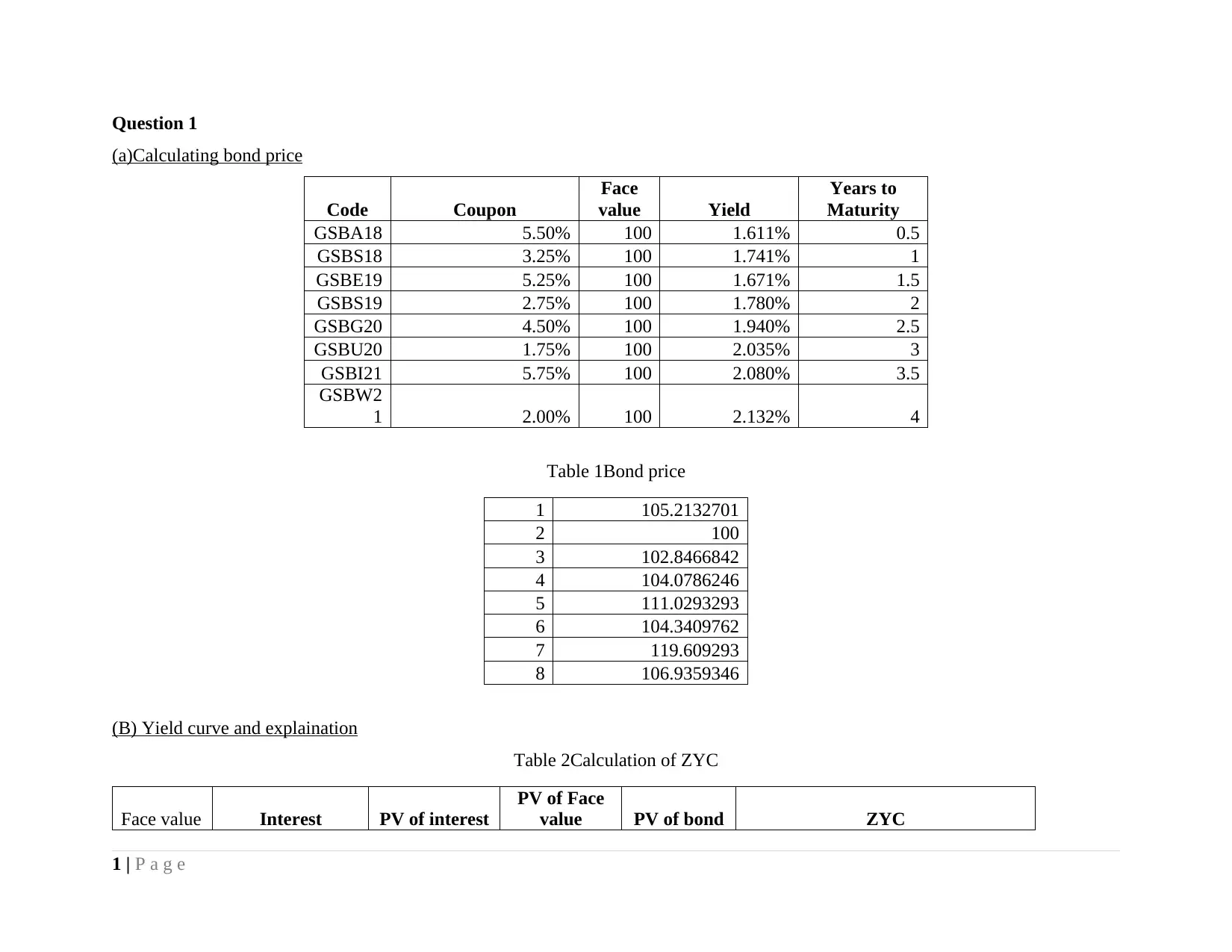

Question 1

(a)Calculating bond price

Code Coupon

Face

value Yield

Years to

Maturity

GSBA18 5.50% 100 1.611% 0.5

GSBS18 3.25% 100 1.741% 1

GSBE19 5.25% 100 1.671% 1.5

GSBS19 2.75% 100 1.780% 2

GSBG20 4.50% 100 1.940% 2.5

GSBU20 1.75% 100 2.035% 3

GSBI21 5.75% 100 2.080% 3.5

GSBW2

1 2.00% 100 2.132% 4

Table 1Bond price

1 105.2132701

2 100

3 102.8466842

4 104.0786246

5 111.0293293

6 104.3409762

7 119.609293

8 106.9359346

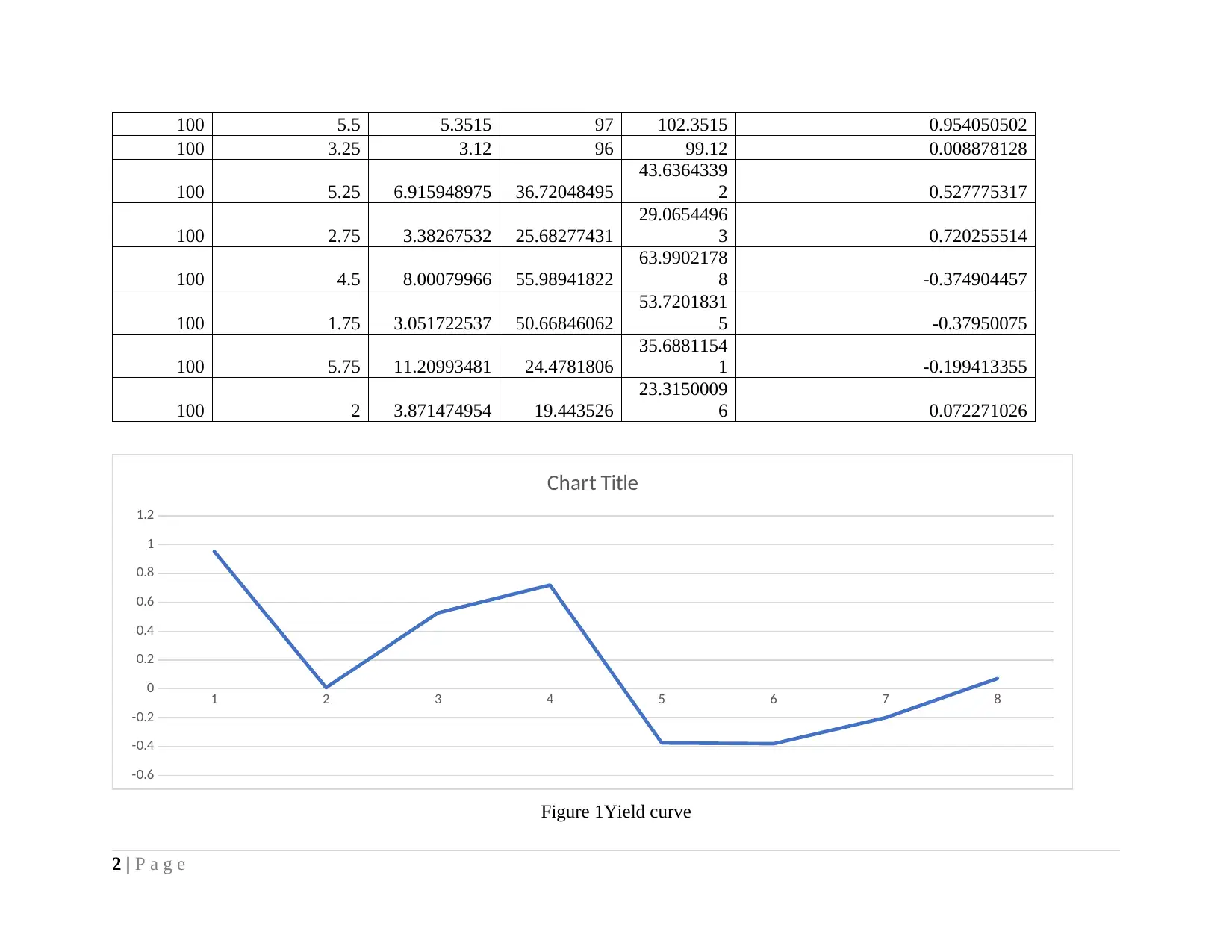

(B) Yield curve and explaination

Table 2Calculation of ZYC

Face value Interest PV of interest

PV of Face

value PV of bond ZYC

1 | P a g e

(a)Calculating bond price

Code Coupon

Face

value Yield

Years to

Maturity

GSBA18 5.50% 100 1.611% 0.5

GSBS18 3.25% 100 1.741% 1

GSBE19 5.25% 100 1.671% 1.5

GSBS19 2.75% 100 1.780% 2

GSBG20 4.50% 100 1.940% 2.5

GSBU20 1.75% 100 2.035% 3

GSBI21 5.75% 100 2.080% 3.5

GSBW2

1 2.00% 100 2.132% 4

Table 1Bond price

1 105.2132701

2 100

3 102.8466842

4 104.0786246

5 111.0293293

6 104.3409762

7 119.609293

8 106.9359346

(B) Yield curve and explaination

Table 2Calculation of ZYC

Face value Interest PV of interest

PV of Face

value PV of bond ZYC

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

100 5.5 5.3515 97 102.3515 0.954050502

100 3.25 3.12 96 99.12 0.008878128

100 5.25 6.915948975 36.72048495

43.6364339

2 0.527775317

100 2.75 3.38267532 25.68277431

29.0654496

3 0.720255514

100 4.5 8.00079966 55.98941822

63.9902178

8 -0.374904457

100 1.75 3.051722537 50.66846062

53.7201831

5 -0.37950075

100 5.75 11.20993481 24.4781806

35.6881154

1 -0.199413355

100 2 3.871474954 19.443526

23.3150009

6 0.072271026

1 2 3 4 5 6 7 8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

Chart Title

Figure 1Yield curve

2 | P a g e

100 3.25 3.12 96 99.12 0.008878128

100 5.25 6.915948975 36.72048495

43.6364339

2 0.527775317

100 2.75 3.38267532 25.68277431

29.0654496

3 0.720255514

100 4.5 8.00079966 55.98941822

63.9902178

8 -0.374904457

100 1.75 3.051722537 50.66846062

53.7201831

5 -0.37950075

100 5.75 11.20993481 24.4781806

35.6881154

1 -0.199413355

100 2 3.871474954 19.443526

23.3150009

6 0.072271026

1 2 3 4 5 6 7 8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

Chart Title

Figure 1Yield curve

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

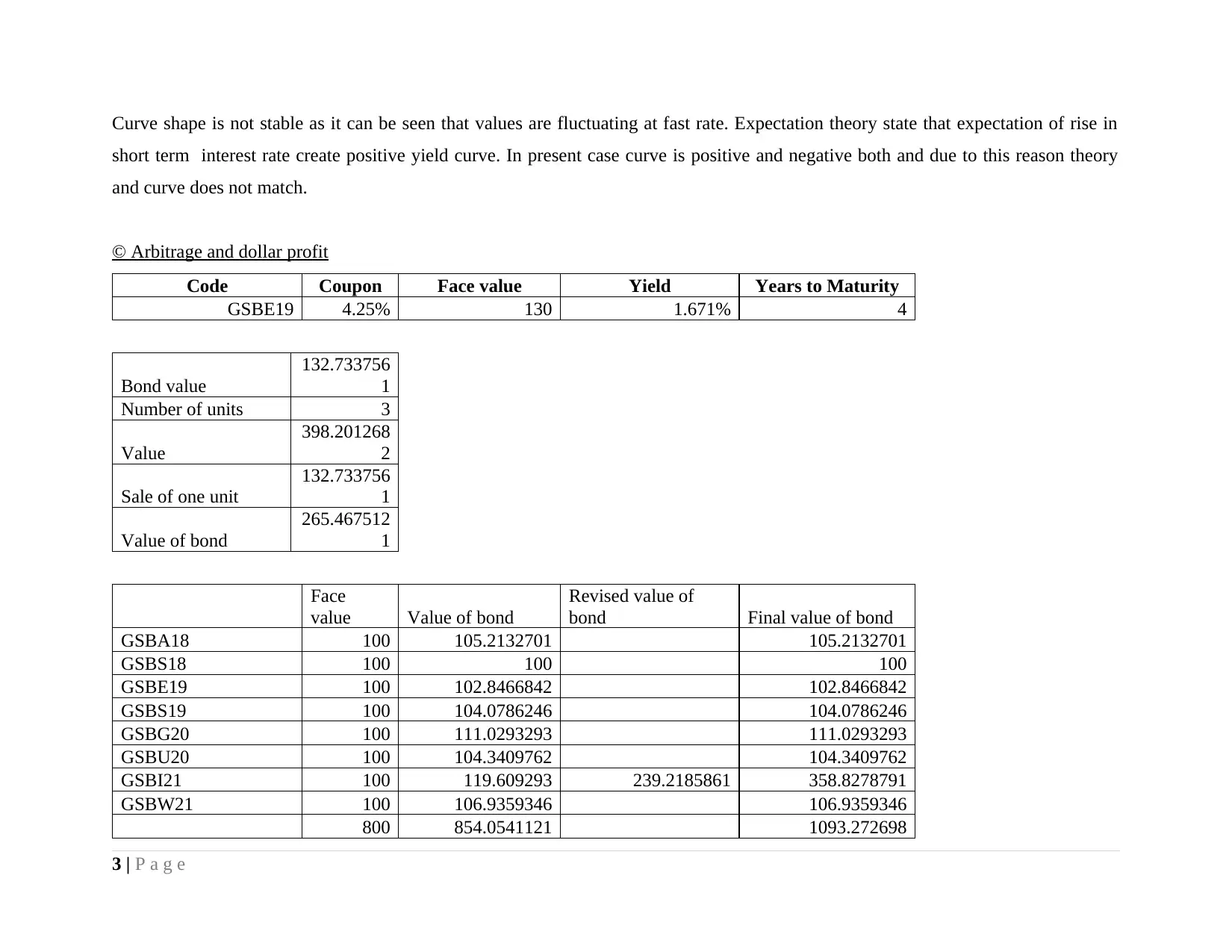

Curve shape is not stable as it can be seen that values are fluctuating at fast rate. Expectation theory state that expectation of rise in

short term interest rate create positive yield curve. In present case curve is positive and negative both and due to this reason theory

and curve does not match.

© Arbitrage and dollar profit

Code Coupon Face value Yield Years to Maturity

GSBE19 4.25% 130 1.671% 4

Bond value

132.733756

1

Number of units 3

Value

398.201268

2

Sale of one unit

132.733756

1

Value of bond

265.467512

1

Face

value Value of bond

Revised value of

bond Final value of bond

GSBA18 100 105.2132701 105.2132701

GSBS18 100 100 100

GSBE19 100 102.8466842 102.8466842

GSBS19 100 104.0786246 104.0786246

GSBG20 100 111.0293293 111.0293293

GSBU20 100 104.3409762 104.3409762

GSBI21 100 119.609293 239.2185861 358.8278791

GSBW21 100 106.9359346 106.9359346

800 854.0541121 1093.272698

3 | P a g e

short term interest rate create positive yield curve. In present case curve is positive and negative both and due to this reason theory

and curve does not match.

© Arbitrage and dollar profit

Code Coupon Face value Yield Years to Maturity

GSBE19 4.25% 130 1.671% 4

Bond value

132.733756

1

Number of units 3

Value

398.201268

2

Sale of one unit

132.733756

1

Value of bond

265.467512

1

Face

value Value of bond

Revised value of

bond Final value of bond

GSBA18 100 105.2132701 105.2132701

GSBS18 100 100 100

GSBE19 100 102.8466842 102.8466842

GSBS19 100 104.0786246 104.0786246

GSBG20 100 111.0293293 111.0293293

GSBU20 100 104.3409762 104.3409762

GSBI21 100 119.609293 239.2185861 358.8278791

GSBW21 100 106.9359346 106.9359346

800 854.0541121 1093.272698

3 | P a g e

Profit 54.0541121 293.2726982

Arbitrage profit amount to 293 in case single unit of bond at 4.25% coupon rate will be sold in the market and same is invested

in exisitng portfolio. Hence, dollar profit on arbitrage is equal to 293. Arbitrage is possible in this case because single security is

purchased and then sold. Received proceeds are again invested in portfolio and in this way gain is made.

Question 2

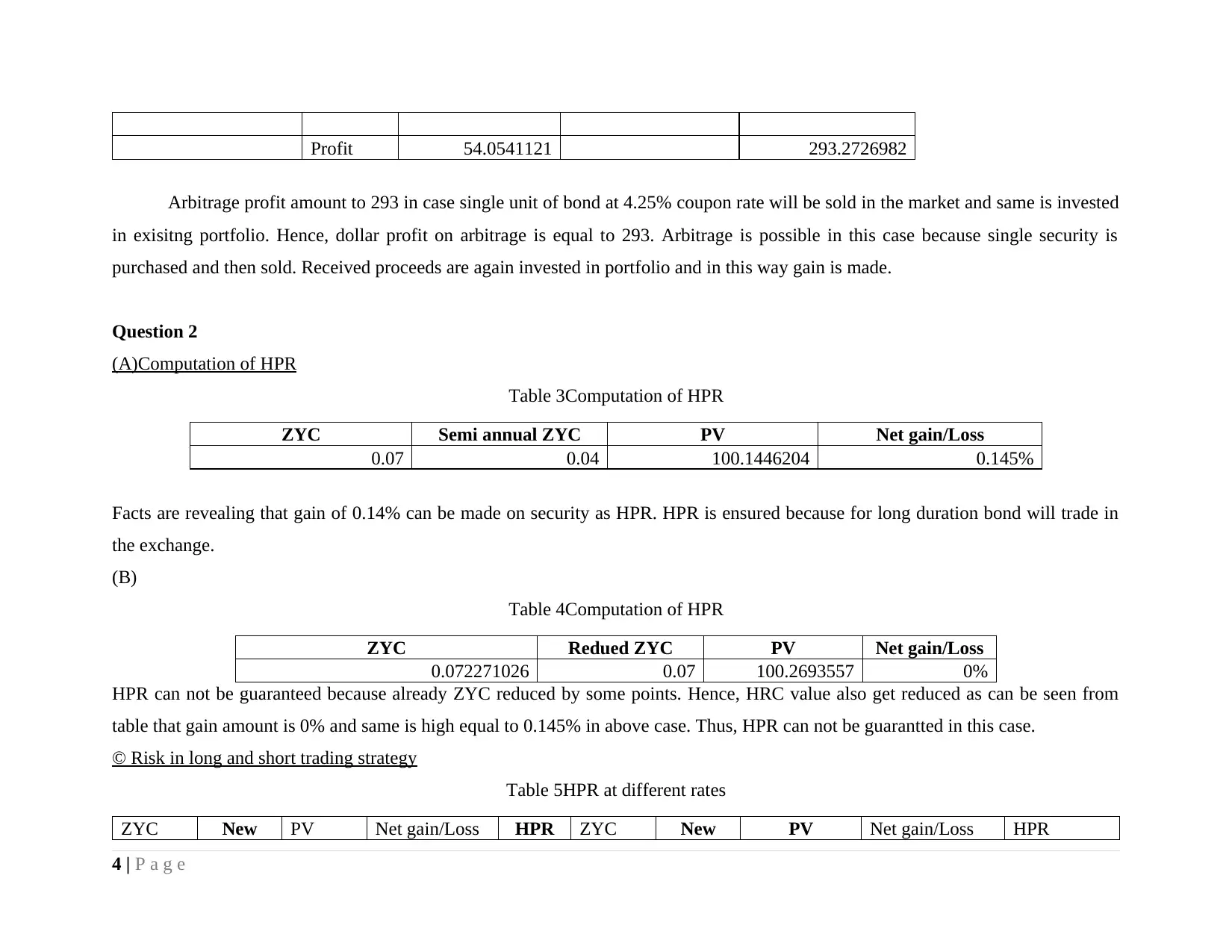

(A)Computation of HPR

Table 3Computation of HPR

ZYC Semi annual ZYC PV Net gain/Loss

0.07 0.04 100.1446204 0.145%

Facts are revealing that gain of 0.14% can be made on security as HPR. HPR is ensured because for long duration bond will trade in

the exchange.

(B)

Table 4Computation of HPR

ZYC Redued ZYC PV Net gain/Loss

0.072271026 0.07 100.2693557 0%

HPR can not be guaranteed because already ZYC reduced by some points. Hence, HRC value also get reduced as can be seen from

table that gain amount is 0% and same is high equal to 0.145% in above case. Thus, HPR can not be guarantted in this case.

© Risk in long and short trading strategy

Table 5HPR at different rates

ZYC New PV Net gain/Loss HPR ZYC New PV Net gain/Loss HPR

4 | P a g e

Arbitrage profit amount to 293 in case single unit of bond at 4.25% coupon rate will be sold in the market and same is invested

in exisitng portfolio. Hence, dollar profit on arbitrage is equal to 293. Arbitrage is possible in this case because single security is

purchased and then sold. Received proceeds are again invested in portfolio and in this way gain is made.

Question 2

(A)Computation of HPR

Table 3Computation of HPR

ZYC Semi annual ZYC PV Net gain/Loss

0.07 0.04 100.1446204 0.145%

Facts are revealing that gain of 0.14% can be made on security as HPR. HPR is ensured because for long duration bond will trade in

the exchange.

(B)

Table 4Computation of HPR

ZYC Redued ZYC PV Net gain/Loss

0.072271026 0.07 100.2693557 0%

HPR can not be guaranteed because already ZYC reduced by some points. Hence, HRC value also get reduced as can be seen from

table that gain amount is 0% and same is high equal to 0.145% in above case. Thus, HPR can not be guarantted in this case.

© Risk in long and short trading strategy

Table 5HPR at different rates

ZYC New PV Net gain/Loss HPR ZYC New PV Net gain/Loss HPR

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ZYC ZYC

0.07227

1

0.06727

1

99.7313

7 0.268632174 0.26%

0.07227

1

0.07227

1 99.71143745 -$0.29 0.28%

There is heavy risk associated with HPR in case of long and short strategy. This is because in case of long strategy one have to

buy position and in short same need to be sold. It is very difficult task to keep close eye on open long and short positions closely.

Hence, there is heavy risk in long short strategy then former one.

Question 3

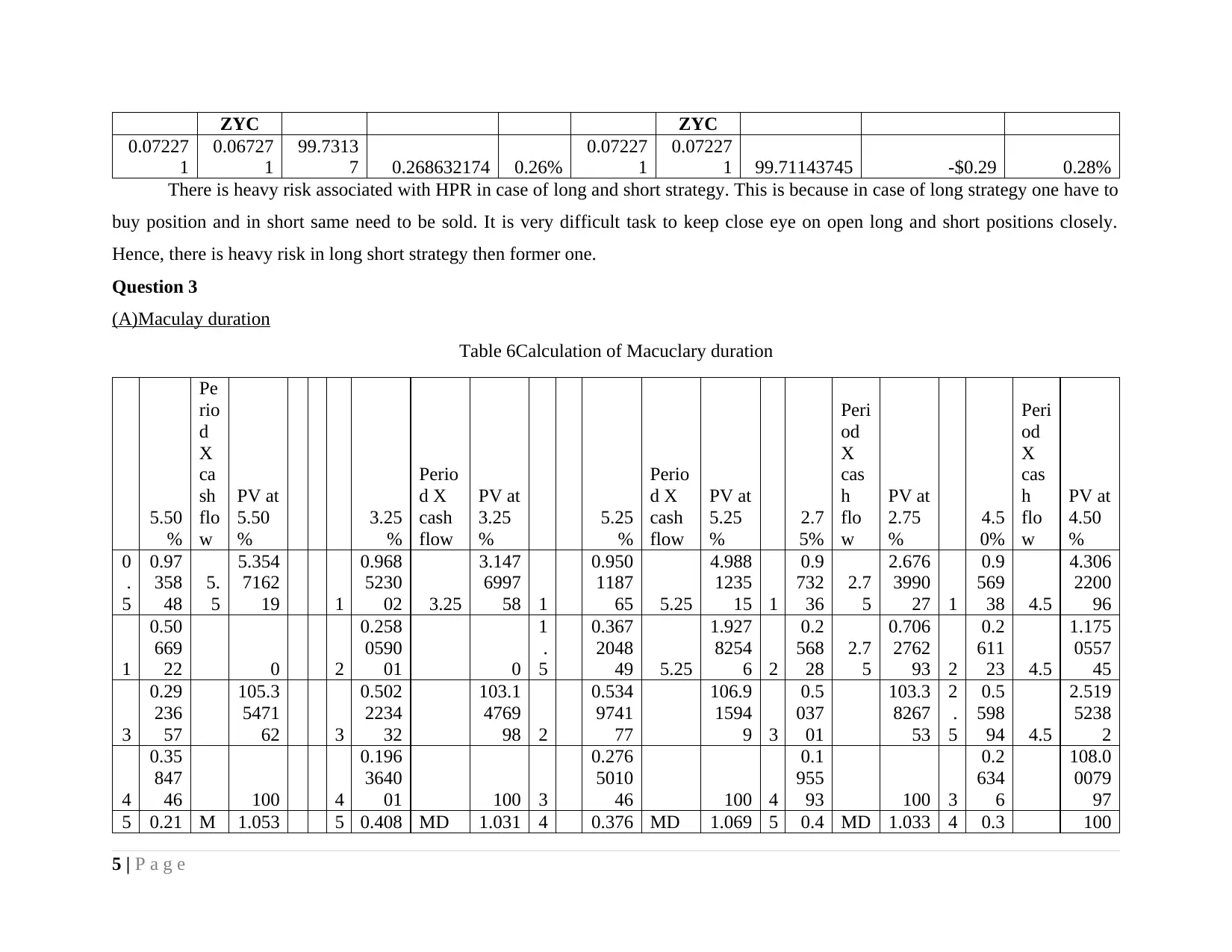

(A)Maculay duration

Table 6Calculation of Macuclary duration

5.50

%

Pe

rio

d

X

ca

sh

flo

w

PV at

5.50

%

3.25

%

Perio

d X

cash

flow

PV at

3.25

%

5.25

%

Perio

d X

cash

flow

PV at

5.25

%

2.7

5%

Peri

od

X

cas

h

flo

w

PV at

2.75

%

4.5

0%

Peri

od

X

cas

h

flo

w

PV at

4.50

%

0

.

5

0.97

358

48

5.

5

5.354

7162

19 1

0.968

5230

02 3.25

3.147

6997

58 1

0.950

1187

65 5.25

4.988

1235

15 1

0.9

732

36

2.7

5

2.676

3990

27 1

0.9

569

38 4.5

4.306

2200

96

1

0.50

669

22 0 2

0.258

0590

01 0

1

.

5

0.367

2048

49 5.25

1.927

8254

6 2

0.2

568

28

2.7

5

0.706

2762

93 2

0.2

611

23 4.5

1.175

0557

45

3

0.29

236

57

105.3

5471

62 3

0.502

2234

32

103.1

4769

98 2

0.534

9741

77

106.9

1594

9 3

0.5

037

01

103.3

8267

53

2

.

5

0.5

598

94 4.5

2.519

5238

2

4

0.35

847

46 100 4

0.196

3640

01 100 3

0.276

5010

46 100 4

0.1

955

93 100 3

0.2

634

6

108.0

0079

97

5 0.21 M 1.053 5 0.408 MD 1.031 4 0.376 MD 1.069 5 0.4 MD 1.033 4 0.3 100

5 | P a g e

0.07227

1

0.06727

1

99.7313

7 0.268632174 0.26%

0.07227

1

0.07227

1 99.71143745 -$0.29 0.28%

There is heavy risk associated with HPR in case of long and short strategy. This is because in case of long strategy one have to

buy position and in short same need to be sold. It is very difficult task to keep close eye on open long and short positions closely.

Hence, there is heavy risk in long short strategy then former one.

Question 3

(A)Maculay duration

Table 6Calculation of Macuclary duration

5.50

%

Pe

rio

d

X

ca

sh

flo

w

PV at

5.50

%

3.25

%

Perio

d X

cash

flow

PV at

3.25

%

5.25

%

Perio

d X

cash

flow

PV at

5.25

%

2.7

5%

Peri

od

X

cas

h

flo

w

PV at

2.75

%

4.5

0%

Peri

od

X

cas

h

flo

w

PV at

4.50

%

0

.

5

0.97

358

48

5.

5

5.354

7162

19 1

0.968

5230

02 3.25

3.147

6997

58 1

0.950

1187

65 5.25

4.988

1235

15 1

0.9

732

36

2.7

5

2.676

3990

27 1

0.9

569

38 4.5

4.306

2200

96

1

0.50

669

22 0 2

0.258

0590

01 0

1

.

5

0.367

2048

49 5.25

1.927

8254

6 2

0.2

568

28

2.7

5

0.706

2762

93 2

0.2

611

23 4.5

1.175

0557

45

3

0.29

236

57

105.3

5471

62 3

0.502

2234

32

103.1

4769

98 2

0.534

9741

77

106.9

1594

9 3

0.5

037

01

103.3

8267

53

2

.

5

0.5

598

94 4.5

2.519

5238

2

4

0.35

847

46 100 4

0.196

3640

01 100 3

0.276

5010

46 100 4

0.1

955

93 100 3

0.2

634

6

108.0

0079

97

5 0.21 M 1.053 5 0.408 MD 1.031 4 0.376 MD 1.069 5 0.4 MD 1.033 4 0.3 100

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

614

36 D

5471

62

0217

54

4769

98

6303

38

1594

9

093

38

8267

53

924

23

6

0.30

909

41 6

0.128

3346

15 5

0.202

2615

44 6

0.1

276

17 5

0.1

910

49 MD

1.080

0079

97

7

0.15

177

63 7

0.429

4717

66 6

0.331

1358

98 7

0.4

313

89 6

0.3

502

86

8

0.32

289

03 8

0.057

3581

78 7

0.135

0340

31 8

0.0

567

46 7

0.1

221

86

9

0.08

059

08 9

0.605

3420

51 8

0.363

0186

51 9

0.6

085

03 8

0.3

976

33

1

0

0.46

066

73

1

0

0.008

7967

89 9

0.061

5862

57

1

0

0.0

086

25 9

0.0

491

43

3.67

227

96

3.562

4945

89

0.744

0939

15

3.598

4655

57

0.766

4167

32

3.5

715

77

0.7

440

94

3.5

441

34

0.7

664

17

Maculay duration is 7.4 which means that in order to earn return one have to make investment for 7 years and 4 month.

(B) Assessing investment amount

Investment of 100 need to be made to make purchase of both securities which is GSBU20 and GSB121. Maculay duration is

2.13 which means that investment can be covered in 2 year and 13 month.

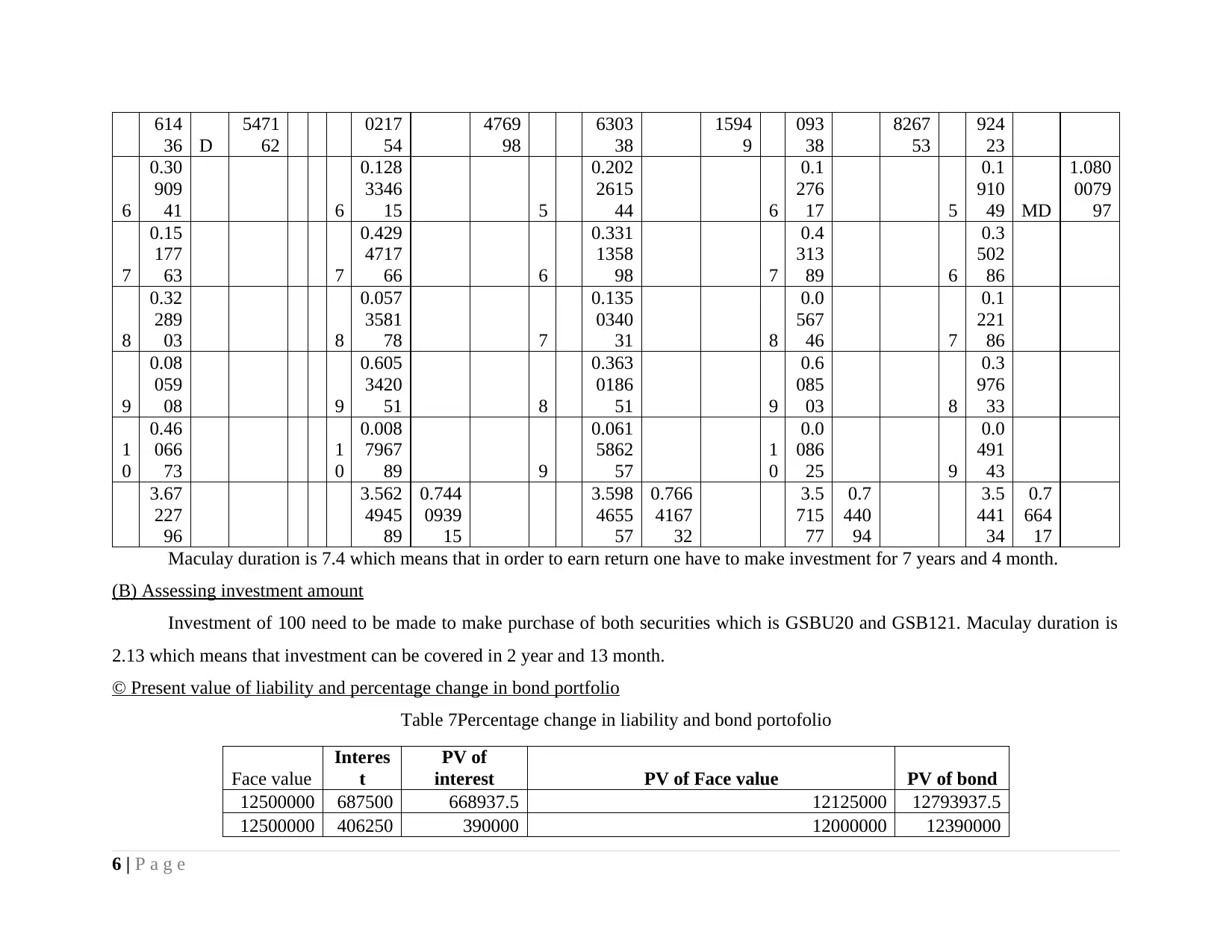

© Present value of liability and percentage change in bond portfolio

Table 7Percentage change in liability and bond portofolio

Face value

Interes

t

PV of

interest PV of Face value PV of bond

12500000 687500 668937.5 12125000 12793937.5

12500000 406250 390000 12000000 12390000

6 | P a g e

36 D

5471

62

0217

54

4769

98

6303

38

1594

9

093

38

8267

53

924

23

6

0.30

909

41 6

0.128

3346

15 5

0.202

2615

44 6

0.1

276

17 5

0.1

910

49 MD

1.080

0079

97

7

0.15

177

63 7

0.429

4717

66 6

0.331

1358

98 7

0.4

313

89 6

0.3

502

86

8

0.32

289

03 8

0.057

3581

78 7

0.135

0340

31 8

0.0

567

46 7

0.1

221

86

9

0.08

059

08 9

0.605

3420

51 8

0.363

0186

51 9

0.6

085

03 8

0.3

976

33

1

0

0.46

066

73

1

0

0.008

7967

89 9

0.061

5862

57

1

0

0.0

086

25 9

0.0

491

43

3.67

227

96

3.562

4945

89

0.744

0939

15

3.598

4655

57

0.766

4167

32

3.5

715

77

0.7

440

94

3.5

441

34

0.7

664

17

Maculay duration is 7.4 which means that in order to earn return one have to make investment for 7 years and 4 month.

(B) Assessing investment amount

Investment of 100 need to be made to make purchase of both securities which is GSBU20 and GSB121. Maculay duration is

2.13 which means that investment can be covered in 2 year and 13 month.

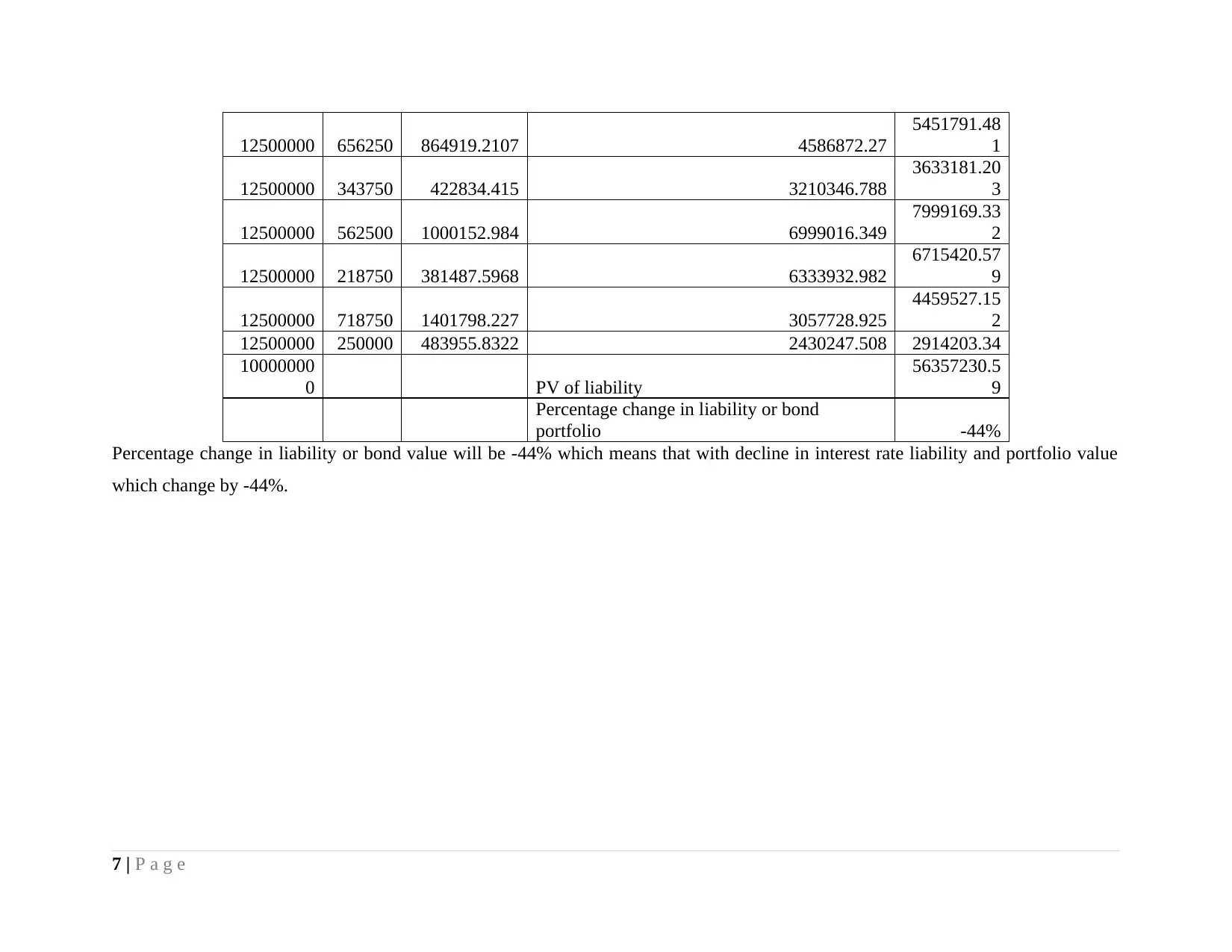

© Present value of liability and percentage change in bond portfolio

Table 7Percentage change in liability and bond portofolio

Face value

Interes

t

PV of

interest PV of Face value PV of bond

12500000 687500 668937.5 12125000 12793937.5

12500000 406250 390000 12000000 12390000

6 | P a g e

12500000 656250 864919.2107 4586872.27

5451791.48

1

12500000 343750 422834.415 3210346.788

3633181.20

3

12500000 562500 1000152.984 6999016.349

7999169.33

2

12500000 218750 381487.5968 6333932.982

6715420.57

9

12500000 718750 1401798.227 3057728.925

4459527.15

2

12500000 250000 483955.8322 2430247.508 2914203.34

10000000

0 PV of liability

56357230.5

9

Percentage change in liability or bond

portfolio -44%

Percentage change in liability or bond value will be -44% which means that with decline in interest rate liability and portfolio value

which change by -44%.

7 | P a g e

5451791.48

1

12500000 343750 422834.415 3210346.788

3633181.20

3

12500000 562500 1000152.984 6999016.349

7999169.33

2

12500000 218750 381487.5968 6333932.982

6715420.57

9

12500000 718750 1401798.227 3057728.925

4459527.15

2

12500000 250000 483955.8322 2430247.508 2914203.34

10000000

0 PV of liability

56357230.5

9

Percentage change in liability or bond

portfolio -44%

Percentage change in liability or bond value will be -44% which means that with decline in interest rate liability and portfolio value

which change by -44%.

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.