Investment Management Homework - Finance Course, Semester 1

VerifiedAdded on 2020/03/16

|8

|1317

|49

Homework Assignment

AI Summary

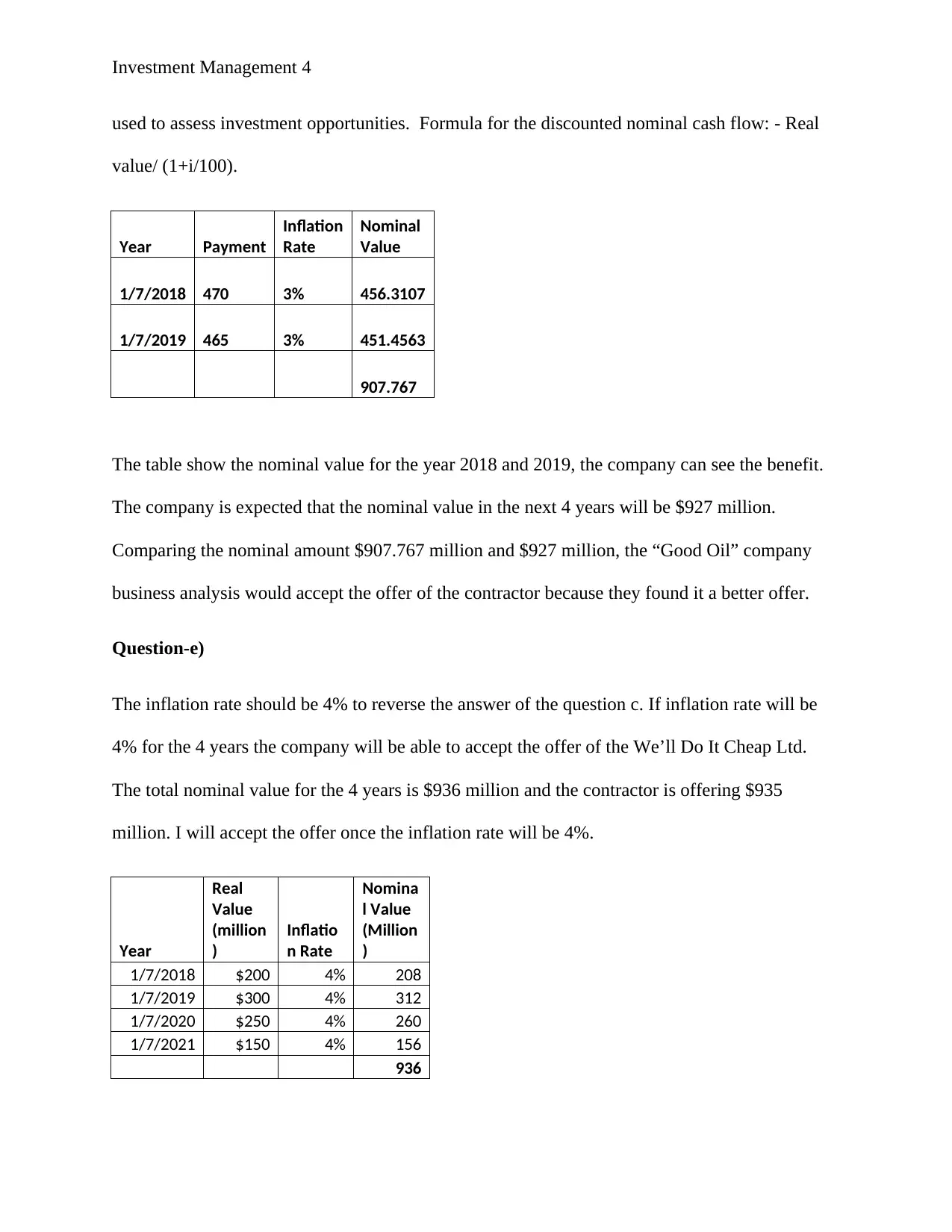

This assignment delves into key concepts of investment management, beginning with the time value of money and nominal cash flow calculations. The solution demonstrates the impact of inflation on expenditures and evaluates different payment offers from contractors. Furthermore, the assignment explores taxation concepts, specifically the purpose and impact of tax depreciation in after-tax discounted cash flow. It contrasts straight-line depreciation with the units of production depreciation method, highlighting the merits of each approach. The analysis includes detailed calculations and explanations, providing a comprehensive understanding of the financial principles involved. The assignment emphasizes the importance of considering both nominal and discounted cash flows in making informed investment decisions. References from academic journals and books are provided to support the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.