Investment Management: Bond Portfolio Strategy and Yield Analysis

VerifiedAdded on 2023/06/11

|14

|1715

|249

Homework Assignment

AI Summary

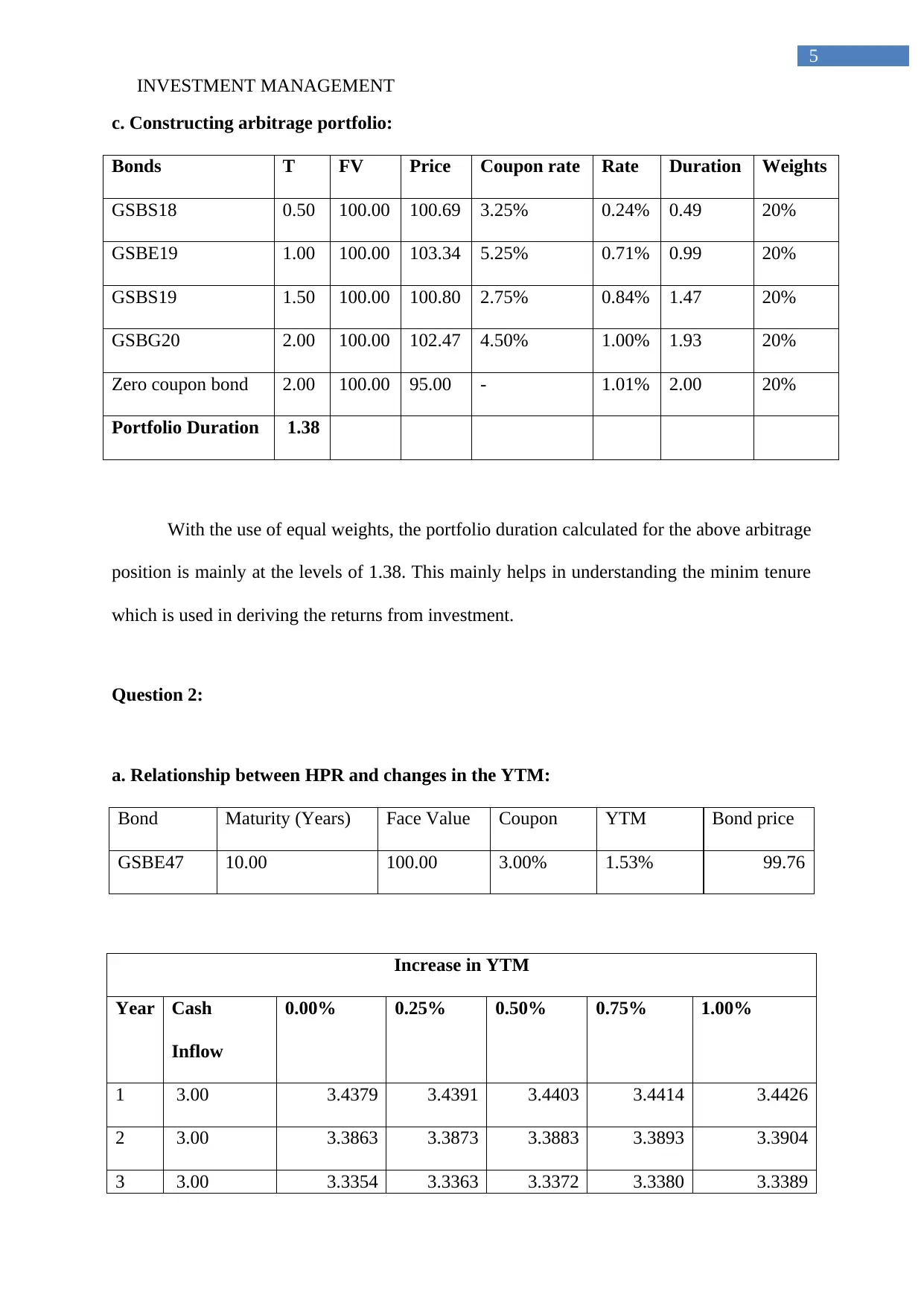

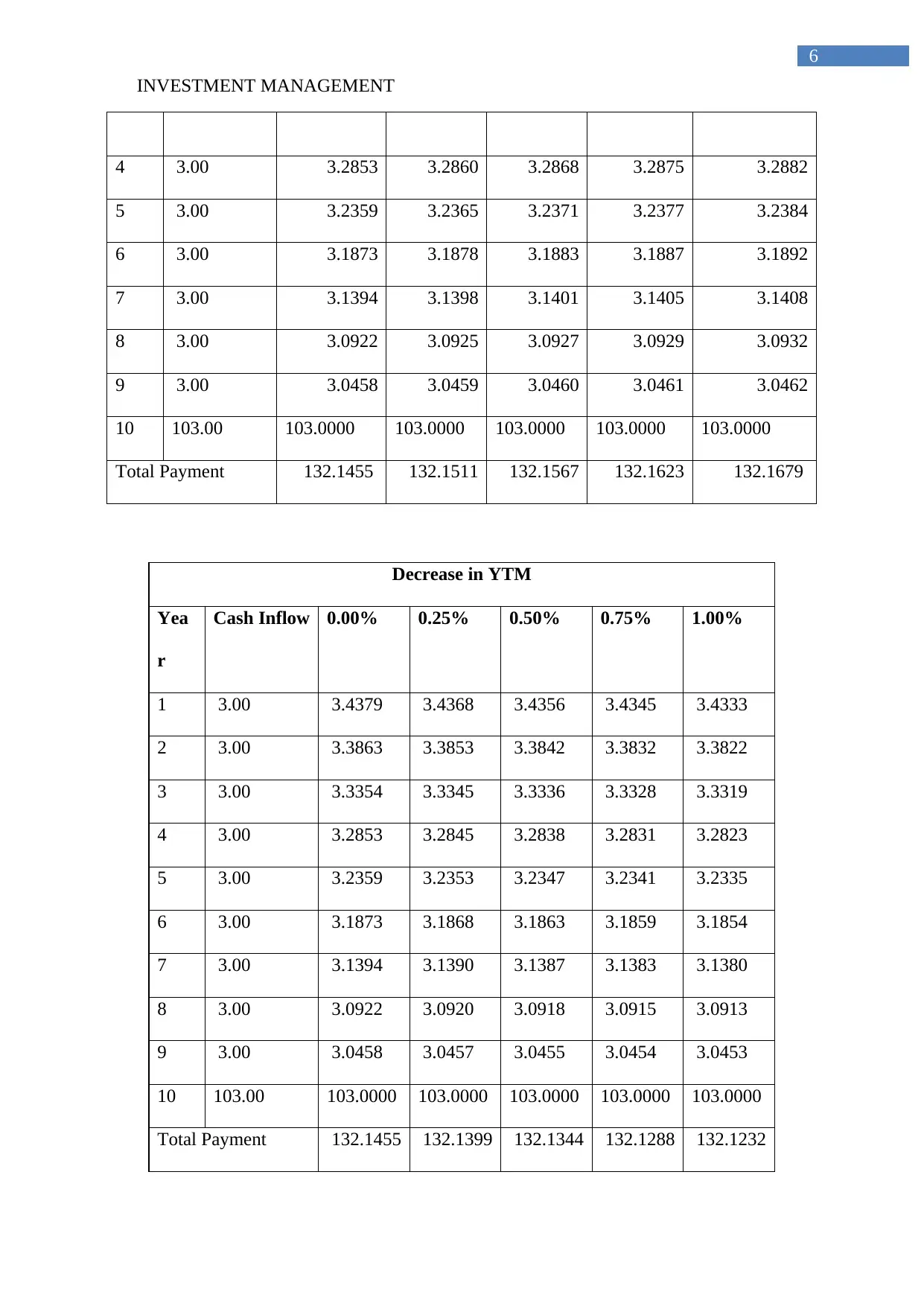

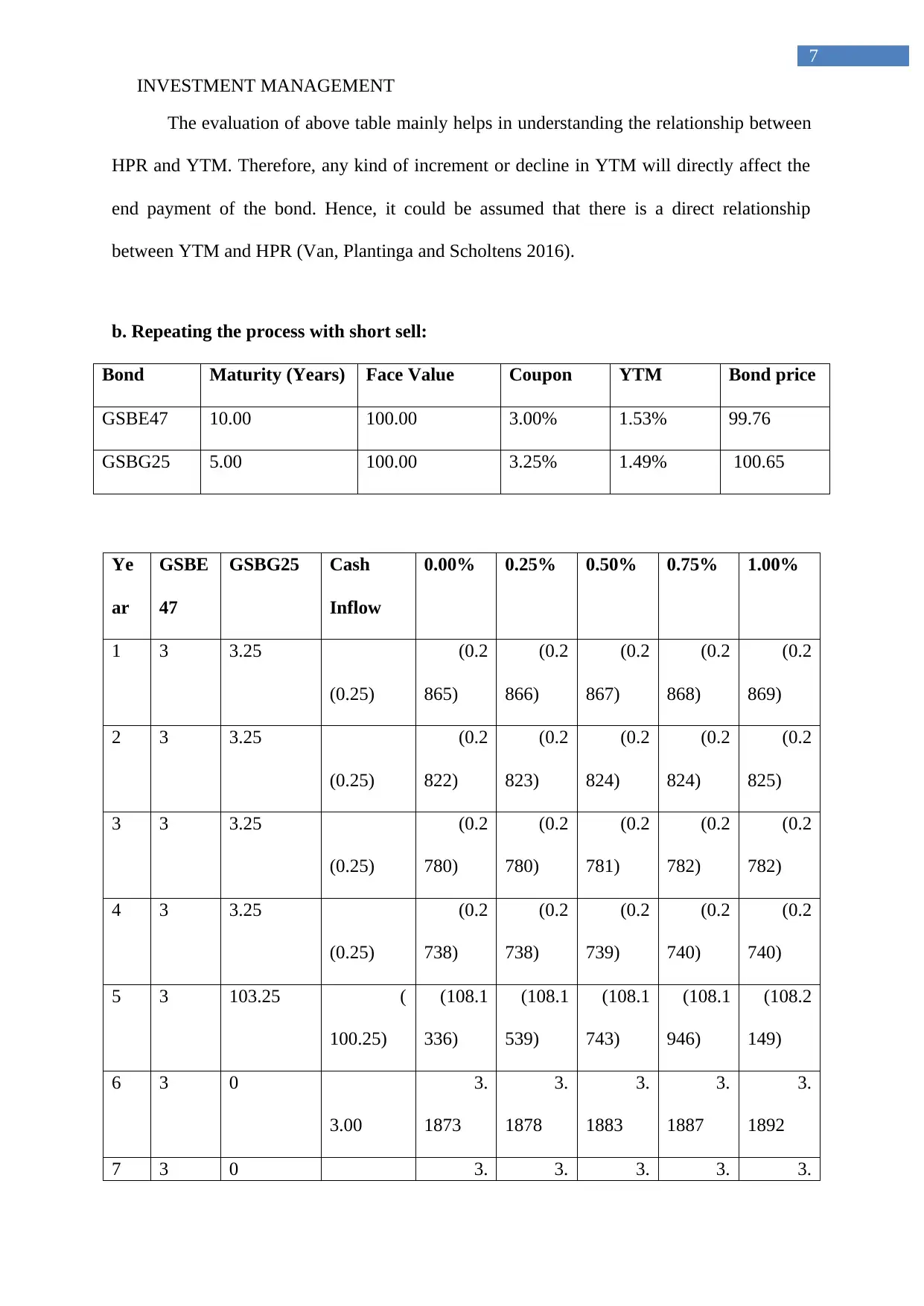

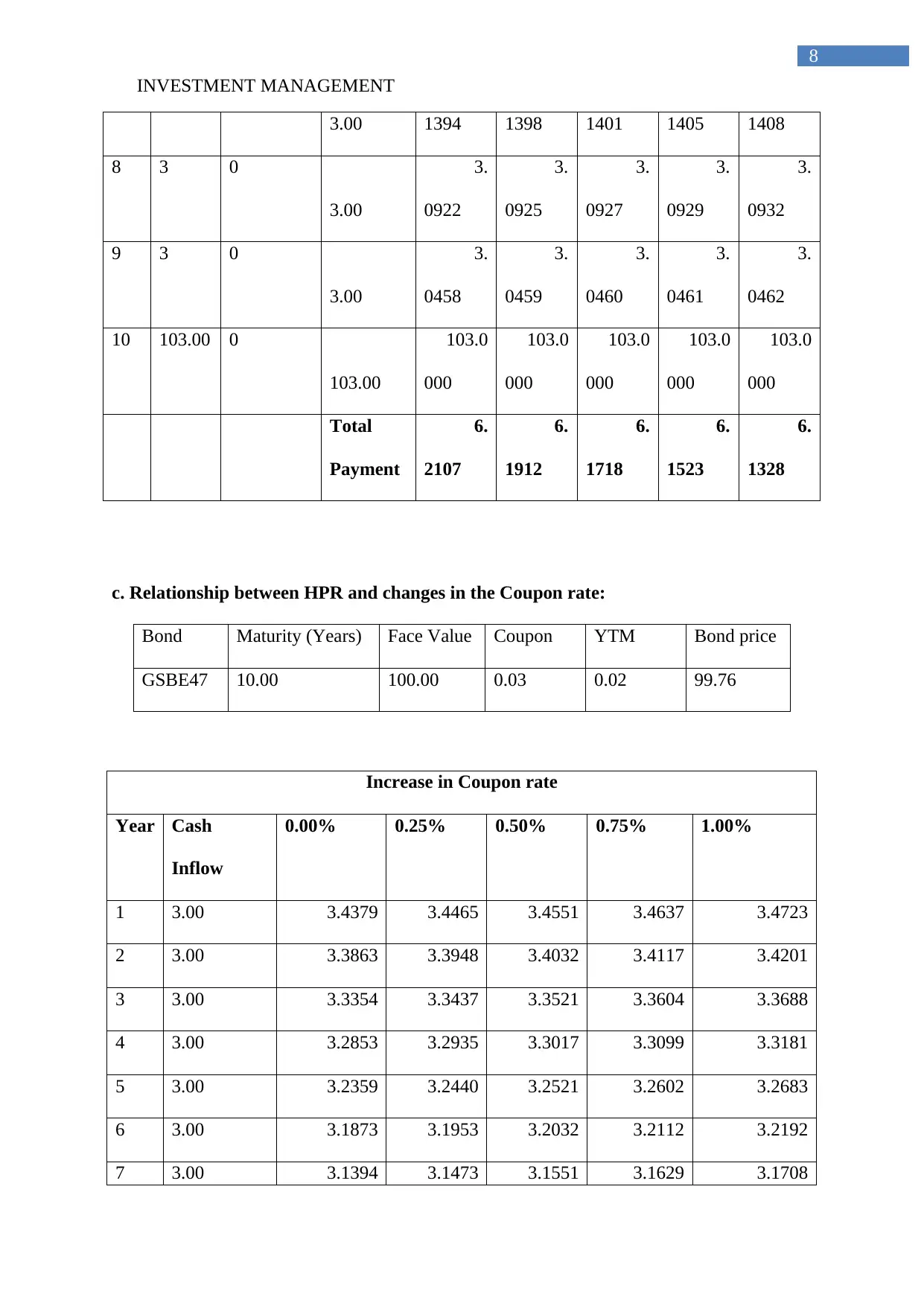

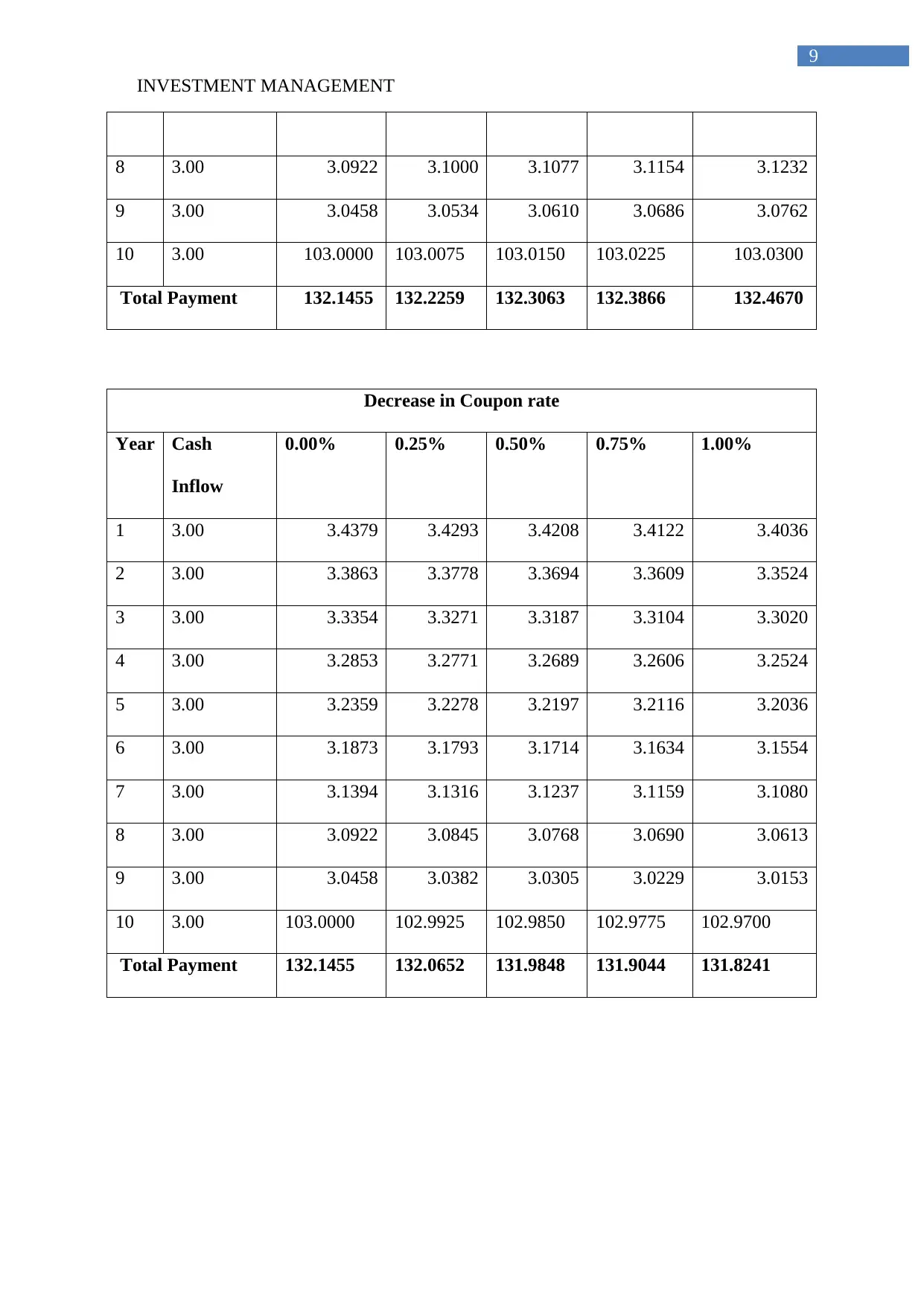

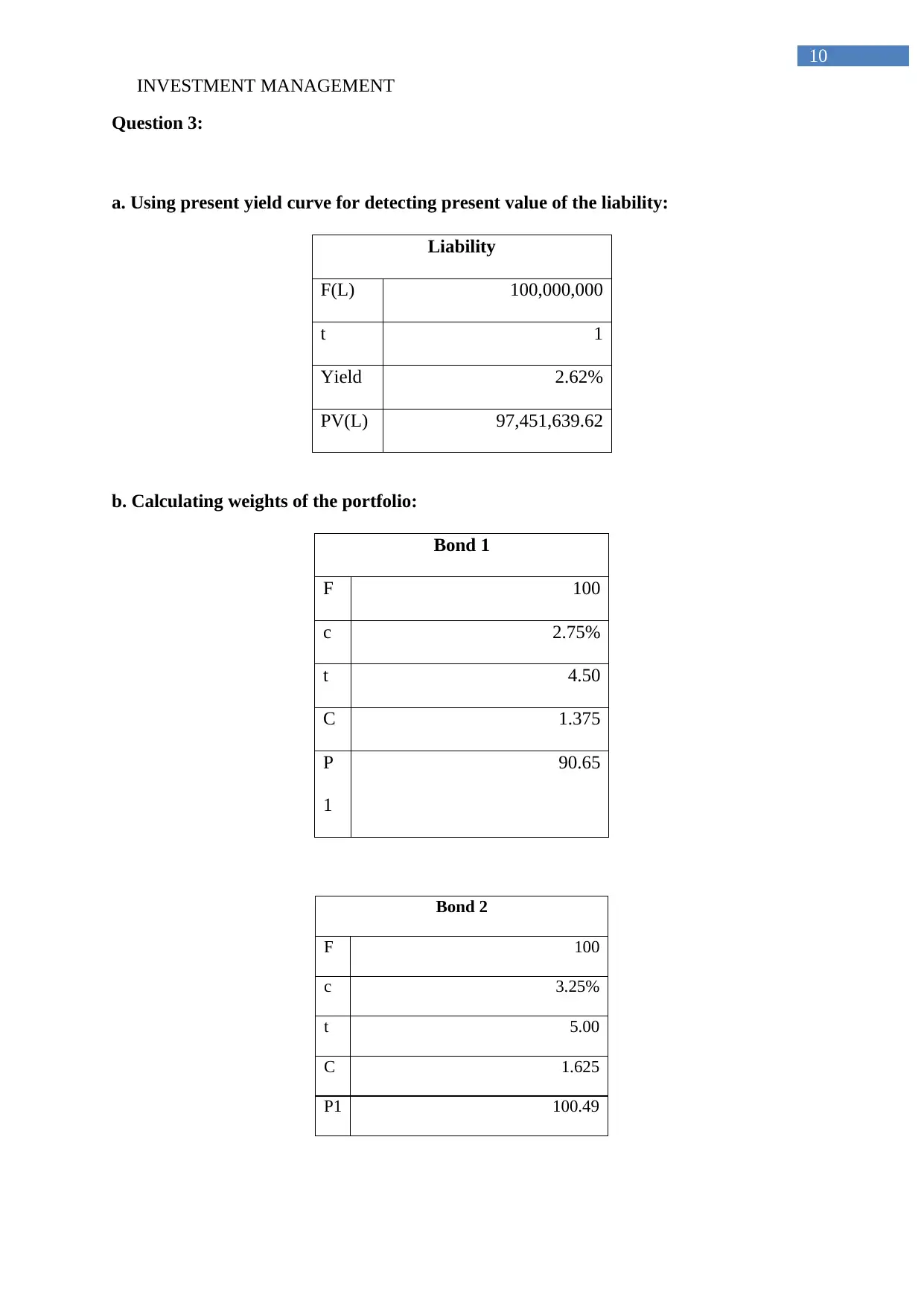

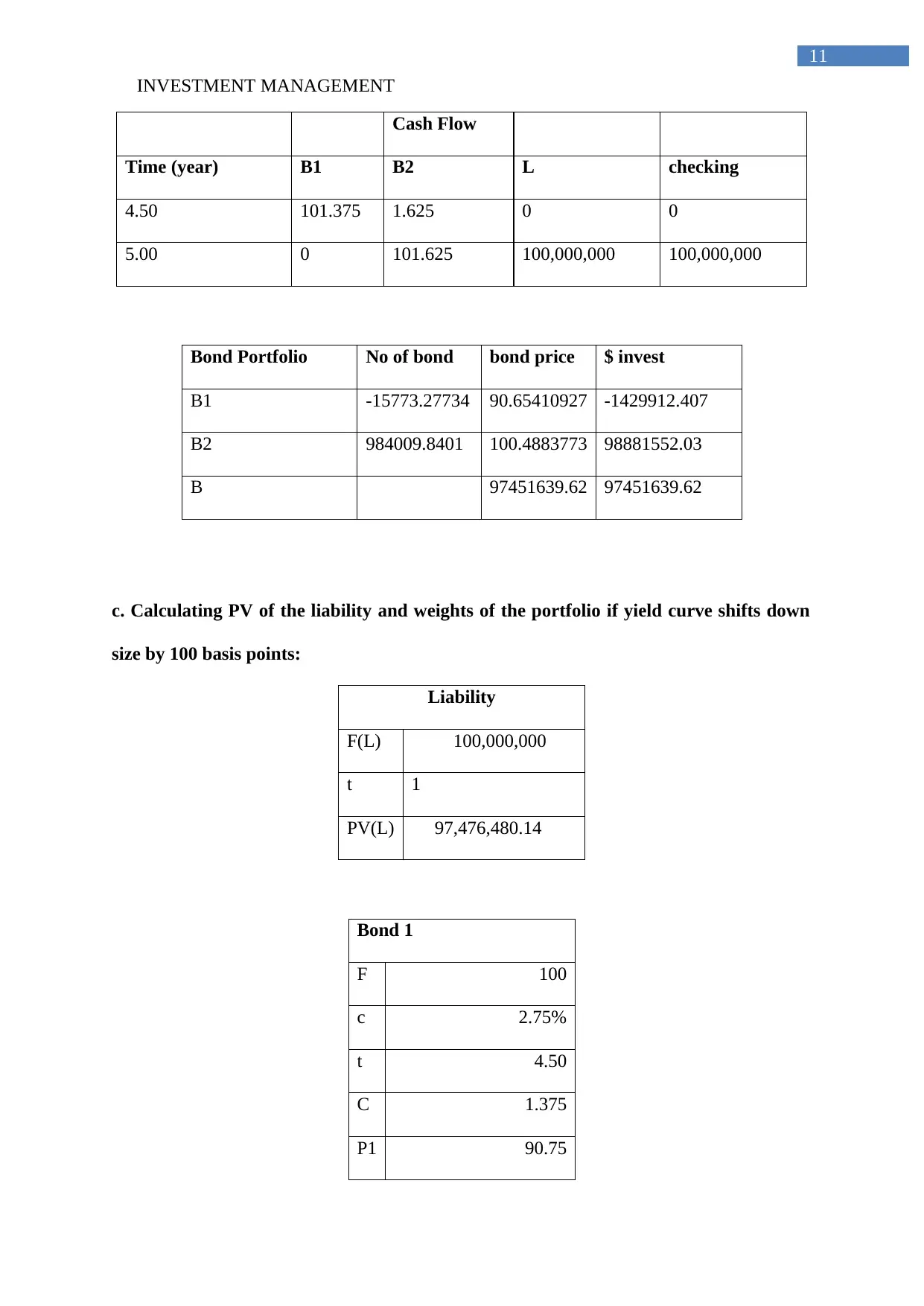

This assignment focuses on investment management principles, specifically addressing bond portfolio hedging, yield curve analysis, and yield to maturity (YTM) calculations. It begins by calculating bond prices and depicting the yield curve, followed by determining the YTM for various maturities. The assignment then constructs an arbitrage portfolio and examines the relationship between Holding Period Return (HPR) and changes in YTM, including scenarios involving short selling. Further analysis explores the impact of coupon rate changes on HPR. Finally, the assignment delves into cash flow matching, calculating the present value of liabilities and determining portfolio weights to immunize against interest rate risk, including scenarios where the yield curve shifts. The study uses hedging measures to minimize investment risk and maximize profitability.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.