Investment Management: Analyzing Yield Curves & Bond Portfolios 2018

VerifiedAdded on 2023/06/04

|10

|1679

|308

Report

AI Summary

This Investment Management report provides a detailed analysis of treasury bonds and yield curves. It includes calculations of zero-coupon yields, YTM, and portfolio construction strategies. The report explores arbitrage opportunities, assesses the impact of yield curve shifts on bond prices, and calcul...

Running head: Investment Management

Investment Management

Name of the Student:

Name of the University:

Author’s Note:

Investment Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INVESTMENT MANAGEMENT

Table of Contents

In Response to Question 1..........................................................................................................2

In Response Question 2..............................................................................................................3

In Response to Question 3..........................................................................................................5

Table of Contents

In Response to Question 1..........................................................................................................2

In Response Question 2..............................................................................................................3

In Response to Question 3..........................................................................................................5

2INVESTMENT MANAGEMENT

In Response to Question 1

Treasury Bonds

Code Coupon PMT PMT Amt Maturity (years) N Face value

GSBE19 5.25% 2.63% 2.63 0.50 1.00 100

GSBS19 2.75% 1.38% 1.38 1.00 2.00 100

GSBG20 4.50% 2.25% 2.25 1.50 3.00 100

GSBU20 1.75% 0.88% 0.88 2.00 4.00 100

GSBI21 5.75% 2.88% 2.88 2.50 5.00 100

GSBW21 2.00% 1.00% 1.00 3.00 6.00 100

GSBM22 5.75% 2.88% 2.88 3.50 7.00 100

GSBU22 2.25% 1.13% 1.13 4.00 8.00 100

GSBG23 5.50% 2.75% 2.75 4.50 9.00 100

GSBG24 2.75% 1.38% 1.38 5.00 10.00 100

GSBG25 3.25% 1.63% 1.63 5.50 11.00 100

GSBG26 4.25% 2.13% 2.13 6.00 12.00 100

GSBG27 4.75% 2.38% 2.38 6.50 13.00 100

GSBU27 2.75% 1.38% 1.38 7.00 14.00 100

GSBI28 2.25% 1.13% 1.13 7.50 15.00 100

GSBG29 3.25% 1.63% 1.63 8.00 16.00 100

GSBU29 2.75% 1.38% 1.38 8.50 17.00 100

GSBG33 4.50% 2.25% 2.25 9.00 18.00 100

GSBK35 2.75% 1.38% 1.38 9.50 19.00 100

GSBK39 3.25% 1.63% 1.63 10.00 20.00 100

Term-structure of Interest Rates

Maturity (years) Zero-Coupon Yields I/Y Price YTM

0.50 1.470% 0.7350% -101.88 1.47%

1.00 1.540% 0.7700% -101.20 1.54%

1.50 1.650% 0.8250% -104.21 1.65%

2.00 1.760% 0.8800% -99.98 1.76%

2.50 1.880% 0.9400% -109.41 1.88%

3.00 1.980% 0.9900% -100.06 1.98%

3.50 2.060% 1.0300% -112.40 2.06%

4.00 2.130% 1.0650% -100.46 2.13%

4.50 2.190% 1.0950% -114.11 2.19%

5.00 2.230% 1.1150% -102.45 2.23%

5.50 2.270% 1.1350% -105.04 2.27%

6.00 2.300% 1.1500% -110.87 2.30%

6.50 2.330% 1.1650% -114.52 2.33%

7.00 2.360% 1.1800% -102.50 2.36%

7.50 2.390% 1.1950% -99.04 2.39%

8.00 2.410% 1.2050% -106.08 2.41%

8.50 2.440% 1.2200% -102.37 2.44%

In Response to Question 1

Treasury Bonds

Code Coupon PMT PMT Amt Maturity (years) N Face value

GSBE19 5.25% 2.63% 2.63 0.50 1.00 100

GSBS19 2.75% 1.38% 1.38 1.00 2.00 100

GSBG20 4.50% 2.25% 2.25 1.50 3.00 100

GSBU20 1.75% 0.88% 0.88 2.00 4.00 100

GSBI21 5.75% 2.88% 2.88 2.50 5.00 100

GSBW21 2.00% 1.00% 1.00 3.00 6.00 100

GSBM22 5.75% 2.88% 2.88 3.50 7.00 100

GSBU22 2.25% 1.13% 1.13 4.00 8.00 100

GSBG23 5.50% 2.75% 2.75 4.50 9.00 100

GSBG24 2.75% 1.38% 1.38 5.00 10.00 100

GSBG25 3.25% 1.63% 1.63 5.50 11.00 100

GSBG26 4.25% 2.13% 2.13 6.00 12.00 100

GSBG27 4.75% 2.38% 2.38 6.50 13.00 100

GSBU27 2.75% 1.38% 1.38 7.00 14.00 100

GSBI28 2.25% 1.13% 1.13 7.50 15.00 100

GSBG29 3.25% 1.63% 1.63 8.00 16.00 100

GSBU29 2.75% 1.38% 1.38 8.50 17.00 100

GSBG33 4.50% 2.25% 2.25 9.00 18.00 100

GSBK35 2.75% 1.38% 1.38 9.50 19.00 100

GSBK39 3.25% 1.63% 1.63 10.00 20.00 100

Term-structure of Interest Rates

Maturity (years) Zero-Coupon Yields I/Y Price YTM

0.50 1.470% 0.7350% -101.88 1.47%

1.00 1.540% 0.7700% -101.20 1.54%

1.50 1.650% 0.8250% -104.21 1.65%

2.00 1.760% 0.8800% -99.98 1.76%

2.50 1.880% 0.9400% -109.41 1.88%

3.00 1.980% 0.9900% -100.06 1.98%

3.50 2.060% 1.0300% -112.40 2.06%

4.00 2.130% 1.0650% -100.46 2.13%

4.50 2.190% 1.0950% -114.11 2.19%

5.00 2.230% 1.1150% -102.45 2.23%

5.50 2.270% 1.1350% -105.04 2.27%

6.00 2.300% 1.1500% -110.87 2.30%

6.50 2.330% 1.1650% -114.52 2.33%

7.00 2.360% 1.1800% -102.50 2.36%

7.50 2.390% 1.1950% -99.04 2.39%

8.00 2.410% 1.2050% -106.08 2.41%

8.50 2.440% 1.2200% -102.37 2.44%

You're viewing a preview

Unlock full access by subscribing today!

3INVESTMENT MANAGEMENT

9.00 2.460% 1.2300% -116.38 2.46%

9.50 2.480% 1.2400% -102.27 2.48%

10.00 2.510% 1.2550% -106.51 2.51%

B) Plot the Curves

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

8.50

9.00

9.50

10.00

0.000%

1.000%

2.000%

3.000%

4.000%

5.000%

6.000%

Graphical Analysis

Zero-Coupon Yields YTM

C)

Particulars

Portfoli

o 5

2 Year ZCB

Time Period 2 Years

Face Value 100

Present Value 98

Required Rate 1.76%

PMT 0

Price -96.57

Portfolio will be formed by the allocation of each will be based on

20% weightage to per bond

The arbitrage portfolio will be considered after reconsidering the pricing and the yield

generated by the bond. The arbitrage portfolio will be created by the help of the bonds where

9.00 2.460% 1.2300% -116.38 2.46%

9.50 2.480% 1.2400% -102.27 2.48%

10.00 2.510% 1.2550% -106.51 2.51%

B) Plot the Curves

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

8.50

9.00

9.50

10.00

0.000%

1.000%

2.000%

3.000%

4.000%

5.000%

6.000%

Graphical Analysis

Zero-Coupon Yields YTM

C)

Particulars

Portfoli

o 5

2 Year ZCB

Time Period 2 Years

Face Value 100

Present Value 98

Required Rate 1.76%

PMT 0

Price -96.57

Portfolio will be formed by the allocation of each will be based on

20% weightage to per bond

The arbitrage portfolio will be considered after reconsidering the pricing and the yield

generated by the bond. The arbitrage portfolio will be created by the help of the bonds where

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INVESTMENT MANAGEMENT

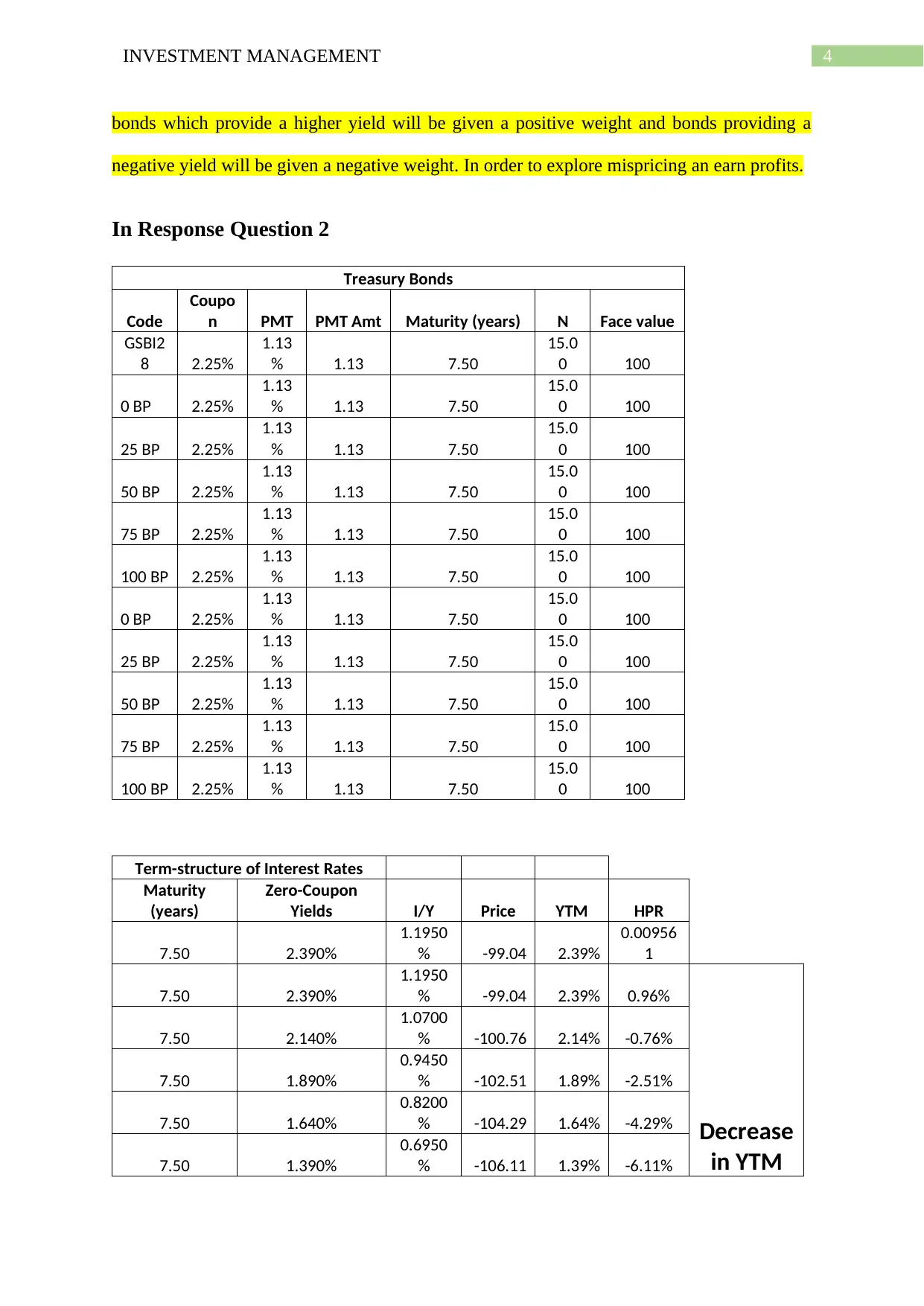

bonds which provide a higher yield will be given a positive weight and bonds providing a

negative yield will be given a negative weight. In order to explore mispricing an earn profits.

In Response Question 2

Treasury Bonds

Code

Coupo

n PMT PMT Amt Maturity (years) N Face value

GSBI2

8 2.25%

1.13

% 1.13 7.50

15.0

0 100

0 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

25 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

50 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

75 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

100 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

0 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

25 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

50 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

75 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

100 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

Term-structure of Interest Rates

Maturity

(years)

Zero-Coupon

Yields I/Y Price YTM HPR

7.50 2.390%

1.1950

% -99.04 2.39%

0.00956

1

7.50 2.390%

1.1950

% -99.04 2.39% 0.96%

Decrease

in YTM

7.50 2.140%

1.0700

% -100.76 2.14% -0.76%

7.50 1.890%

0.9450

% -102.51 1.89% -2.51%

7.50 1.640%

0.8200

% -104.29 1.64% -4.29%

7.50 1.390%

0.6950

% -106.11 1.39% -6.11%

bonds which provide a higher yield will be given a positive weight and bonds providing a

negative yield will be given a negative weight. In order to explore mispricing an earn profits.

In Response Question 2

Treasury Bonds

Code

Coupo

n PMT PMT Amt Maturity (years) N Face value

GSBI2

8 2.25%

1.13

% 1.13 7.50

15.0

0 100

0 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

25 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

50 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

75 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

100 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

0 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

25 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

50 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

75 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

100 BP 2.25%

1.13

% 1.13 7.50

15.0

0 100

Term-structure of Interest Rates

Maturity

(years)

Zero-Coupon

Yields I/Y Price YTM HPR

7.50 2.390%

1.1950

% -99.04 2.39%

0.00956

1

7.50 2.390%

1.1950

% -99.04 2.39% 0.96%

Decrease

in YTM

7.50 2.140%

1.0700

% -100.76 2.14% -0.76%

7.50 1.890%

0.9450

% -102.51 1.89% -2.51%

7.50 1.640%

0.8200

% -104.29 1.64% -4.29%

7.50 1.390%

0.6950

% -106.11 1.39% -6.11%

5INVESTMENT MANAGEMENT

7.50 2.390%

1.1950

% -99.04 2.39% 0.96%

Increase

in YTM

7.50 2.640%

1.3200

% -97.36 2.64% 2.64%

7.50 2.890%

1.4450

% -95.71 2.89% 4.29%

7.50 3.140%

1.5700

% -94.09 3.14% 5.91%

7.50 3.390%

1.6950

% -92.51 3.39% 7.49%

0 BP 25 BP 50 BP 75 BP 100 BP

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

Decrease in YTM

1 2 3 4 5 6 7 8 9 10 11

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

YTM AND ZCB

YTM HPR

7.50 2.390%

1.1950

% -99.04 2.39% 0.96%

Increase

in YTM

7.50 2.640%

1.3200

% -97.36 2.64% 2.64%

7.50 2.890%

1.4450

% -95.71 2.89% 4.29%

7.50 3.140%

1.5700

% -94.09 3.14% 5.91%

7.50 3.390%

1.6950

% -92.51 3.39% 7.49%

0 BP 25 BP 50 BP 75 BP 100 BP

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

Decrease in YTM

1 2 3 4 5 6 7 8 9 10 11

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

YTM AND ZCB

YTM HPR

You're viewing a preview

Unlock full access by subscribing today!

6INVESTMENT MANAGEMENT

In Response to Question 3

a) Summarize the Present value of the Fund

Particulars 1 2 3 4 5 6 7 8 9 10

Liabilility

Amt 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000

Yeld Curve 0.7350% 0.7700% 0.8250% 0.8800% 0.9400% 0.9900% 1.0300% 1.0650% 1.0950% 1.1150%

Present

VALUE 248175.9 248089.7 247954.4 247819.2 247671.9 247549.3 247451.3 247365.6 247292.2 247243.2

Sum Total 3465170

b) The calculation of the Modified Duration was done after calculating he duration of

each of the Treasury Bond Taken below :

The treasury bond taken was one was of 3 Years which a coupon rate of 9%

payable semi-annually and the price for the same is trading at 96.2$. The

YTM calculated for the Bond was around 5.25%.

The second bond had a face value of 100 with a coupon rate of 10% payable,

3year semi-annually and the price for the same was trading at 98.79. The

YTM calculated for the bond was around 5.25%.

Calculation of D (Duration)

Bond 1

Present Value 96.2

Modified

Duration Duration/(1+ Periodic R)

PMT (Coupon) 4.5

YTM

(Calculated) 5.25%

Face Value 100

Annual

Duration

2.68810

1

Period (Semi Annually) 12

Modified

Duration

2.55401

5

Period In 6 months

Cash

Flow

P.V @

5.25% Weights

Weights*Perio

d

1 4.5

4.27553444

2

0.04443

3 0.044433381

2 4.5

4.06226550

3

0.04221

7 0.084433978

3 4.5

3.85963468

2

0.04011

1 0.12033346

In Response to Question 3

a) Summarize the Present value of the Fund

Particulars 1 2 3 4 5 6 7 8 9 10

Liabilility

Amt 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000 2,50,000

Yeld Curve 0.7350% 0.7700% 0.8250% 0.8800% 0.9400% 0.9900% 1.0300% 1.0650% 1.0950% 1.1150%

Present

VALUE 248175.9 248089.7 247954.4 247819.2 247671.9 247549.3 247451.3 247365.6 247292.2 247243.2

Sum Total 3465170

b) The calculation of the Modified Duration was done after calculating he duration of

each of the Treasury Bond Taken below :

The treasury bond taken was one was of 3 Years which a coupon rate of 9%

payable semi-annually and the price for the same is trading at 96.2$. The

YTM calculated for the Bond was around 5.25%.

The second bond had a face value of 100 with a coupon rate of 10% payable,

3year semi-annually and the price for the same was trading at 98.79. The

YTM calculated for the bond was around 5.25%.

Calculation of D (Duration)

Bond 1

Present Value 96.2

Modified

Duration Duration/(1+ Periodic R)

PMT (Coupon) 4.5

YTM

(Calculated) 5.25%

Face Value 100

Annual

Duration

2.68810

1

Period (Semi Annually) 12

Modified

Duration

2.55401

5

Period In 6 months

Cash

Flow

P.V @

5.25% Weights

Weights*Perio

d

1 4.5

4.27553444

2

0.04443

3 0.044433381

2 4.5

4.06226550

3

0.04221

7 0.084433978

3 4.5

3.85963468

2

0.04011

1 0.12033346

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INVESTMENT MANAGEMENT

4 4.5

3.66711133

7 0.03811 0.152441438

5 4.5

3.48419129

4

0.03620

9 0.181046839

6

104.

5

76.8747406

1

0.79891

9 4.793512497

Total Price

96.2234778

7

Duratio

n 5.376201593

Calculation of D (Duration)

Bond 2

Present Value

98.7

9

Modified

Duration Duration/(1+ Periodic R)

PMT (Coupon) 5

YTM

(Calculated) 5.25%

Face Value 100

Annual

Duration 2.73194

Period (Semi Annually) 12

Modified

Duration

2.59566

8

Period In 6 months

Cash

Flow

P.V @

5.25% Weights

Weights*Perio

d

1 5

4.75059382

4 0.04937 0.049370423

2 5

4.51362833

7

0.04690

8 0.093815531

3 5 4.28848298

0.04456

8 0.133703845

4 5

4.07456815

2

0.04234

5 0.169379376

5 5 3.87132366

0.04023

3 0.201163154

6 105

77.2425623

4

0.80274

1 4.816447963

Total Price

98.7411592

9 Duration 5.463880292

4 4.5

3.66711133

7 0.03811 0.152441438

5 4.5

3.48419129

4

0.03620

9 0.181046839

6

104.

5

76.8747406

1

0.79891

9 4.793512497

Total Price

96.2234778

7

Duratio

n 5.376201593

Calculation of D (Duration)

Bond 2

Present Value

98.7

9

Modified

Duration Duration/(1+ Periodic R)

PMT (Coupon) 5

YTM

(Calculated) 5.25%

Face Value 100

Annual

Duration 2.73194

Period (Semi Annually) 12

Modified

Duration

2.59566

8

Period In 6 months

Cash

Flow

P.V @

5.25% Weights

Weights*Perio

d

1 5

4.75059382

4 0.04937 0.049370423

2 5

4.51362833

7

0.04690

8 0.093815531

3 5 4.28848298

0.04456

8 0.133703845

4 5

4.07456815

2

0.04234

5 0.169379376

5 5 3.87132366

0.04023

3 0.201163154

6 105

77.2425623

4

0.80274

1 4.816447963

Total Price

98.7411592

9 Duration 5.463880292

8INVESTMENT MANAGEMENT

Modified Duration: Duration in Year/ (1+ Periodic r)

Modified Duration for the portfolio calculated was done by taking the weight in each of the

bond as 50% and the annual duration of the bond was calculated for bond 1 and 2

respectively.

The modified duration for the portfolio was calculated as 2.71%, which implies that if the

YTM of the Bond that is 10.5% changes by 1% the value of the portfolio is expected to

change by 2.71% in the opposite direction ignoring convexity.

The reason for selecting the Treasury bond was the liquidity factor present in this bond.

c) After setting up the hedge, if the entire yield curve shifts down by 25 basis points then

the recalculation of the Modified duration will be done by using the approx. formula

taking a 25 basis point shock in the YTM.

Modified Duration Approx.: P2-P1(2P0*YTM)

Calculation of P2

So new YTM = 10.5-0.25 = 10.25 annually.

i.e., YTM semi-annually = 5.125% for 6 months.

The new price of the bond 1 will be:

4.5PMT (Coupon Payment)

12 N=Time period

100 Face Value.

5.125% I/Y

Equals: Present Value: $96.22856

Calculation of P2

So new YTM = 10.5-0.25 = 10.25 annually.

Modified Duration: Duration in Year/ (1+ Periodic r)

Modified Duration for the portfolio calculated was done by taking the weight in each of the

bond as 50% and the annual duration of the bond was calculated for bond 1 and 2

respectively.

The modified duration for the portfolio was calculated as 2.71%, which implies that if the

YTM of the Bond that is 10.5% changes by 1% the value of the portfolio is expected to

change by 2.71% in the opposite direction ignoring convexity.

The reason for selecting the Treasury bond was the liquidity factor present in this bond.

c) After setting up the hedge, if the entire yield curve shifts down by 25 basis points then

the recalculation of the Modified duration will be done by using the approx. formula

taking a 25 basis point shock in the YTM.

Modified Duration Approx.: P2-P1(2P0*YTM)

Calculation of P2

So new YTM = 10.5-0.25 = 10.25 annually.

i.e., YTM semi-annually = 5.125% for 6 months.

The new price of the bond 1 will be:

4.5PMT (Coupon Payment)

12 N=Time period

100 Face Value.

5.125% I/Y

Equals: Present Value: $96.22856

Calculation of P2

So new YTM = 10.5-0.25 = 10.25 annually.

You're viewing a preview

Unlock full access by subscribing today!

9INVESTMENT MANAGEMENT

i.e., YTM semi-annually = 5.125% for 6 months.

The new price of the bond 2 will be:

5 PMT (Coupon Payment)

12 N=Time period

100 Face Value.

5.125% I/Y

Equals: Present Value: $98.74680803

Yes the bond portfolio is a perfectly hedged portfolio as the interest rate charged by

negative 25 basis point and the value of the bond portfolio increased.

i.e., YTM semi-annually = 5.125% for 6 months.

The new price of the bond 2 will be:

5 PMT (Coupon Payment)

12 N=Time period

100 Face Value.

5.125% I/Y

Equals: Present Value: $98.74680803

Yes the bond portfolio is a perfectly hedged portfolio as the interest rate charged by

negative 25 basis point and the value of the bond portfolio increased.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.