Investment Opportunities for ALLCURE INC. - Feasibility Study

VerifiedAdded on 2023/06/03

|17

|3607

|210

AI Summary

The report analyses two revenue earning opportunities i.e. T-REC and P-REC based on quantitative and qualitative parameters. The quantitative analysis has been carried out on four parameters - Discounted Payback period, Net Present Value, Internal Rate of Return, and Profitability Index. The qualitative analysis of the two projects has been carried out based on litigation, penalty & moral impact of the project on the future prospect of the company. The report recommends T-REC as a better alternative based on critical aspects of the sector and the impact on human body.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Analysis of

Investment

opportunities for

ALLCURE INC.

Investment

opportunities for

ALLCURE INC.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

In the said report, there has been analysis of investment proposal at the disposal of

ALLCURE Inc. The two proposals has been analysed based on quantitative and

qualitative parameter to understand the feasibility of project on financial, social and

other areas. The quantitative parameter of analysing the project has been highlighted

here in below:

(a) Net Present Value;

(b) Profitability Index;

(c) Internal Rate of Return;

(d) Discounted Payback Period

Further, the parameters for analysing qualitative aspect of the project includes

litigation, penalty & moral impact of the project on the future prospect of the

company.

On the basis of above analysis, it has been understood that P-REC is feasible on

quantitative front while T-REC is feasible on qualitative front and hence a

conservative view has been taken to safeguard the future interest of the company by

choosing proposal T-REC and further testing P-REC before official launch.

In the said report, there has been analysis of investment proposal at the disposal of

ALLCURE Inc. The two proposals has been analysed based on quantitative and

qualitative parameter to understand the feasibility of project on financial, social and

other areas. The quantitative parameter of analysing the project has been highlighted

here in below:

(a) Net Present Value;

(b) Profitability Index;

(c) Internal Rate of Return;

(d) Discounted Payback Period

Further, the parameters for analysing qualitative aspect of the project includes

litigation, penalty & moral impact of the project on the future prospect of the

company.

On the basis of above analysis, it has been understood that P-REC is feasible on

quantitative front while T-REC is feasible on qualitative front and hence a

conservative view has been taken to safeguard the future interest of the company by

choosing proposal T-REC and further testing P-REC before official launch.

Table Of Contents:

Executive Summary...........................................................................2

Introduction.......................................................................................4

Findings.............................................................................................4

4.1 Quantitative Findings on the basis (P-REC & T-REC)..............4

Discounted Payback period:........................................................5

Net Present Value:.......................................................................5

Internal Rate of Return:...............................................................5

Profitability Index.........................................................................5

4.2 Qualitative Findings................................................................7

Recommendation and Justifications.................................................7

Detail Comparison and Further Recommendation...........................7

Conclusion.........................................................................................8

References.........................................................................................8

Appendix-1........................................................................................9

Executive Summary...........................................................................2

Introduction.......................................................................................4

Findings.............................................................................................4

4.1 Quantitative Findings on the basis (P-REC & T-REC)..............4

Discounted Payback period:........................................................5

Net Present Value:.......................................................................5

Internal Rate of Return:...............................................................5

Profitability Index.........................................................................5

4.2 Qualitative Findings................................................................7

Recommendation and Justifications.................................................7

Detail Comparison and Further Recommendation...........................7

Conclusion.........................................................................................8

References.........................................................................................8

Appendix-1........................................................................................9

Introduction

ALL Cure Inc. has incurred expenditure on Research and development of medicine for

years and is now proposing to explore two revenue earning opportunities i.e. T-REC

and P-REC. The analysis in this report deals with feasibility study of the aforesaid

project based on quantitative and qualitative parameters. Further, P- REC has side

impact and shall result in long term disease while T –REC is much more stable>

Findings

4.1 Quantitative Findings on the basis (P-REC & T-REC)

The assumptions that have been undertaken for carrying out the analysis presented in

the Appendix of the report have been highlighted here in under:

(a) Expenses incurred in training human resource has been treated as capital

expenditure which is non –depreciable and no tax deduction shall be available on

the same;

(b) The life of both the proposal is 8 years and the assets are assumed to be disposed

at the end of eight years;

(c) The cost incurred towards renovation is treated as Capital Expenditure and the

same is tax depreciable for analysis purpose.

(d) Any loss or gain on disposal of asset after completion of 8 years has been taken

into consideration for analysis;

(e) Realisation of Working capital on completion of project;

(f) Expenditure incurred on Research and Development has been considered as sunk

cost and not tax deductible.

The quantitative analysis has been carried on four parameters. The parameter chosen

for analysis has been enumerated here-in-under:

Discounted Payback period:

This capital budgeting tool analyse the time period to breakeven the investment made

initially while recognising the concept of time value of money. Further, in layman

terms it means that time period which shall be required by the company to recollect

the initial outlay made by discounting the cash flows to present value. (Anon., 2018)

Net Present Value:

It is a significant methods under capital budgeting under it the discounted cash flow

computed is reduced by initial outlay to understand the feasibility of the project. If the

said computation is positive, the project is feasible and if negative, the project shall

ALL Cure Inc. has incurred expenditure on Research and development of medicine for

years and is now proposing to explore two revenue earning opportunities i.e. T-REC

and P-REC. The analysis in this report deals with feasibility study of the aforesaid

project based on quantitative and qualitative parameters. Further, P- REC has side

impact and shall result in long term disease while T –REC is much more stable>

Findings

4.1 Quantitative Findings on the basis (P-REC & T-REC)

The assumptions that have been undertaken for carrying out the analysis presented in

the Appendix of the report have been highlighted here in under:

(a) Expenses incurred in training human resource has been treated as capital

expenditure which is non –depreciable and no tax deduction shall be available on

the same;

(b) The life of both the proposal is 8 years and the assets are assumed to be disposed

at the end of eight years;

(c) The cost incurred towards renovation is treated as Capital Expenditure and the

same is tax depreciable for analysis purpose.

(d) Any loss or gain on disposal of asset after completion of 8 years has been taken

into consideration for analysis;

(e) Realisation of Working capital on completion of project;

(f) Expenditure incurred on Research and Development has been considered as sunk

cost and not tax deductible.

The quantitative analysis has been carried on four parameters. The parameter chosen

for analysis has been enumerated here-in-under:

Discounted Payback period:

This capital budgeting tool analyse the time period to breakeven the investment made

initially while recognising the concept of time value of money. Further, in layman

terms it means that time period which shall be required by the company to recollect

the initial outlay made by discounting the cash flows to present value. (Anon., 2018)

Net Present Value:

It is a significant methods under capital budgeting under it the discounted cash flow

computed is reduced by initial outlay to understand the feasibility of the project. If the

said computation is positive, the project is feasible and if negative, the project shall

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

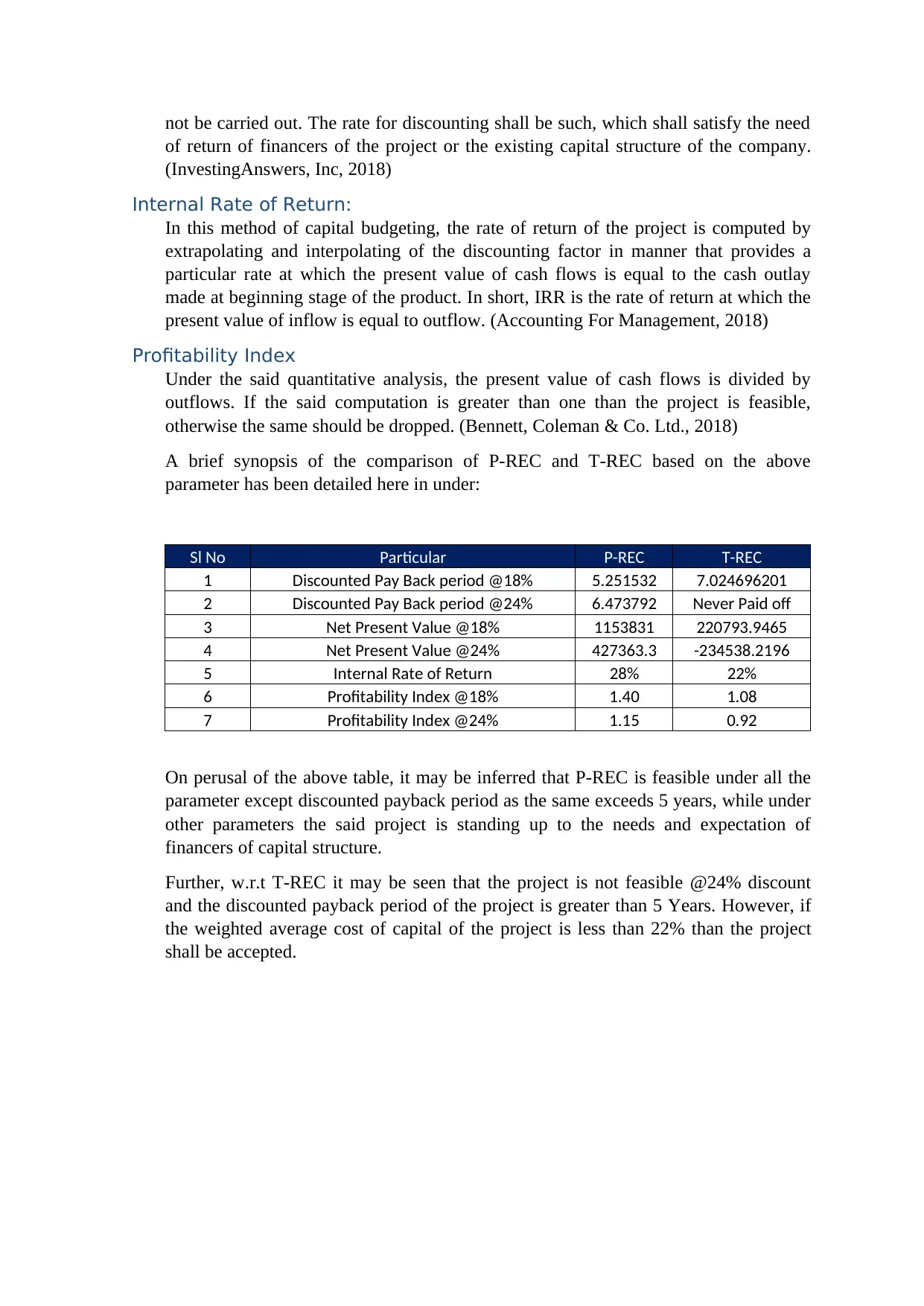

not be carried out. The rate for discounting shall be such, which shall satisfy the need

of return of financers of the project or the existing capital structure of the company.

(InvestingAnswers, Inc, 2018)

Internal Rate of Return:

In this method of capital budgeting, the rate of return of the project is computed by

extrapolating and interpolating of the discounting factor in manner that provides a

particular rate at which the present value of cash flows is equal to the cash outlay

made at beginning stage of the product. In short, IRR is the rate of return at which the

present value of inflow is equal to outflow. (Accounting For Management, 2018)

Profitability Index

Under the said quantitative analysis, the present value of cash flows is divided by

outflows. If the said computation is greater than one than the project is feasible,

otherwise the same should be dropped. (Bennett, Coleman & Co. Ltd., 2018)

A brief synopsis of the comparison of P-REC and T-REC based on the above

parameter has been detailed here in under:

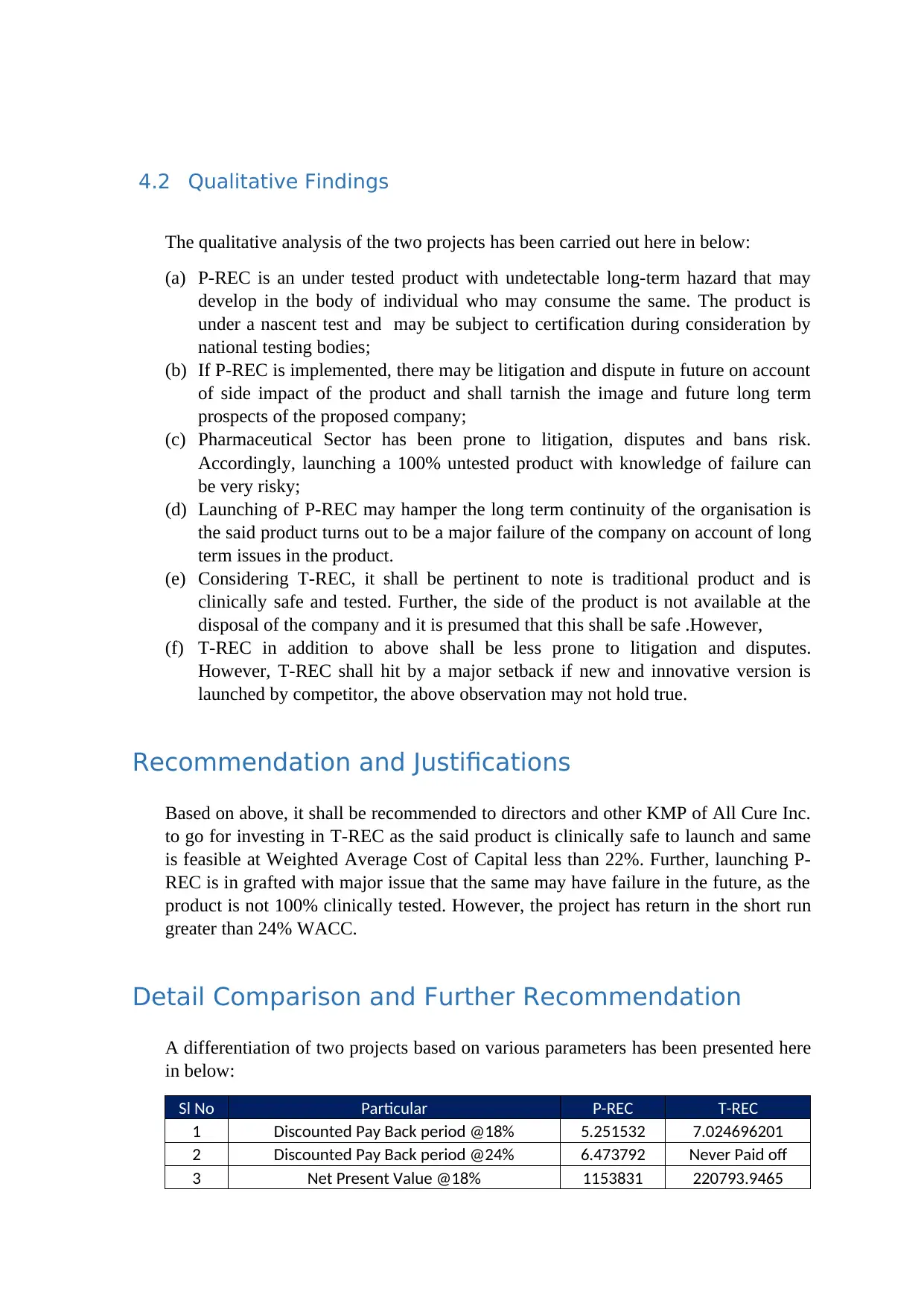

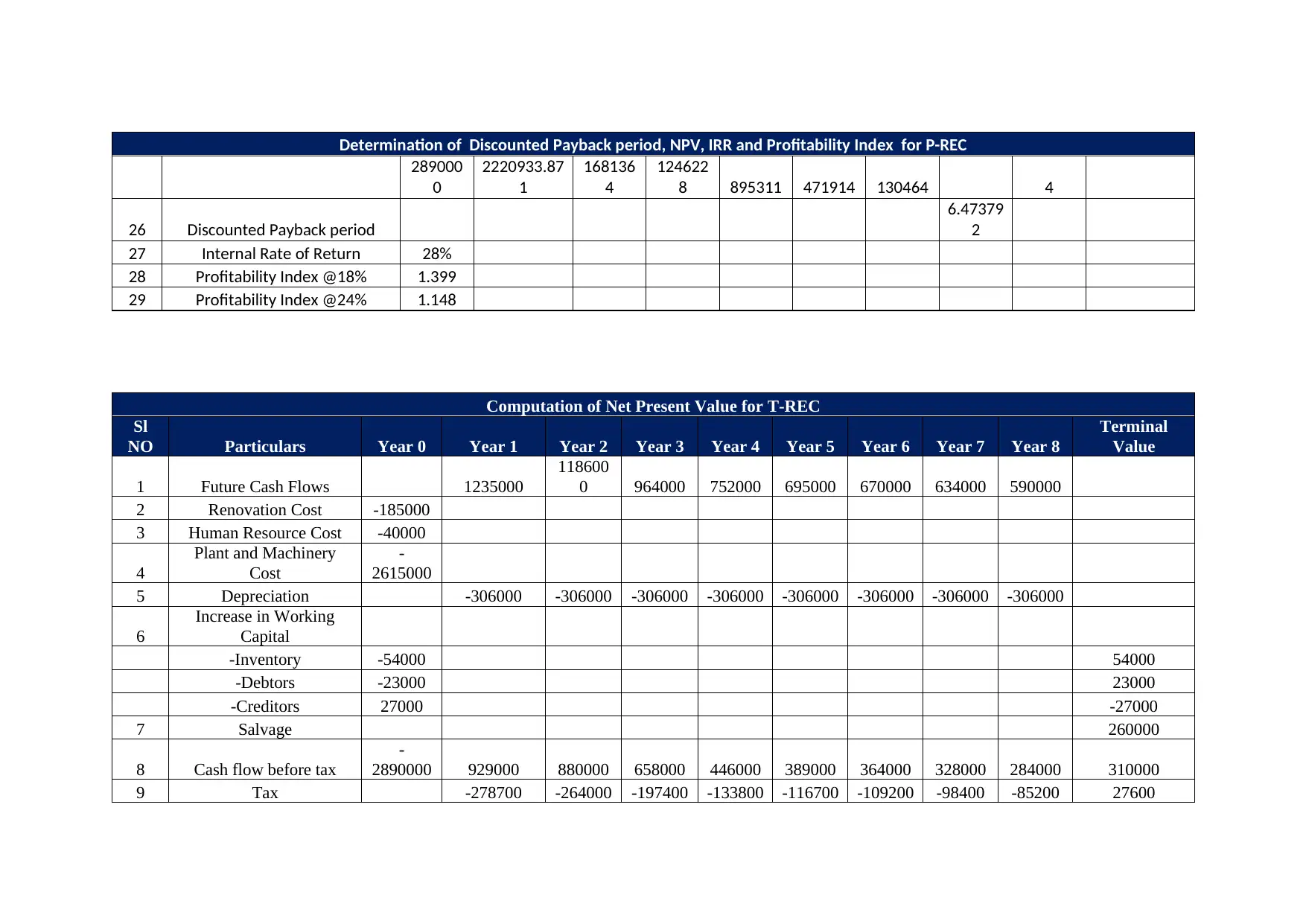

Sl No Particular P-REC T-REC

1 Discounted Pay Back period @18% 5.251532 7.024696201

2 Discounted Pay Back period @24% 6.473792 Never Paid off

3 Net Present Value @18% 1153831 220793.9465

4 Net Present Value @24% 427363.3 -234538.2196

5 Internal Rate of Return 28% 22%

6 Profitability Index @18% 1.40 1.08

7 Profitability Index @24% 1.15 0.92

On perusal of the above table, it may be inferred that P-REC is feasible under all the

parameter except discounted payback period as the same exceeds 5 years, while under

other parameters the said project is standing up to the needs and expectation of

financers of capital structure.

Further, w.r.t T-REC it may be seen that the project is not feasible @24% discount

and the discounted payback period of the project is greater than 5 Years. However, if

the weighted average cost of capital of the project is less than 22% than the project

shall be accepted.

of return of financers of the project or the existing capital structure of the company.

(InvestingAnswers, Inc, 2018)

Internal Rate of Return:

In this method of capital budgeting, the rate of return of the project is computed by

extrapolating and interpolating of the discounting factor in manner that provides a

particular rate at which the present value of cash flows is equal to the cash outlay

made at beginning stage of the product. In short, IRR is the rate of return at which the

present value of inflow is equal to outflow. (Accounting For Management, 2018)

Profitability Index

Under the said quantitative analysis, the present value of cash flows is divided by

outflows. If the said computation is greater than one than the project is feasible,

otherwise the same should be dropped. (Bennett, Coleman & Co. Ltd., 2018)

A brief synopsis of the comparison of P-REC and T-REC based on the above

parameter has been detailed here in under:

Sl No Particular P-REC T-REC

1 Discounted Pay Back period @18% 5.251532 7.024696201

2 Discounted Pay Back period @24% 6.473792 Never Paid off

3 Net Present Value @18% 1153831 220793.9465

4 Net Present Value @24% 427363.3 -234538.2196

5 Internal Rate of Return 28% 22%

6 Profitability Index @18% 1.40 1.08

7 Profitability Index @24% 1.15 0.92

On perusal of the above table, it may be inferred that P-REC is feasible under all the

parameter except discounted payback period as the same exceeds 5 years, while under

other parameters the said project is standing up to the needs and expectation of

financers of capital structure.

Further, w.r.t T-REC it may be seen that the project is not feasible @24% discount

and the discounted payback period of the project is greater than 5 Years. However, if

the weighted average cost of capital of the project is less than 22% than the project

shall be accepted.

4.2 Qualitative Findings

The qualitative analysis of the two projects has been carried out here in below:

(a) P-REC is an under tested product with undetectable long-term hazard that may

develop in the body of individual who may consume the same. The product is

under a nascent test and may be subject to certification during consideration by

national testing bodies;

(b) If P-REC is implemented, there may be litigation and dispute in future on account

of side impact of the product and shall tarnish the image and future long term

prospects of the proposed company;

(c) Pharmaceutical Sector has been prone to litigation, disputes and bans risk.

Accordingly, launching a 100% untested product with knowledge of failure can

be very risky;

(d) Launching of P-REC may hamper the long term continuity of the organisation is

the said product turns out to be a major failure of the company on account of long

term issues in the product.

(e) Considering T-REC, it shall be pertinent to note is traditional product and is

clinically safe and tested. Further, the side of the product is not available at the

disposal of the company and it is presumed that this shall be safe .However,

(f) T-REC in addition to above shall be less prone to litigation and disputes.

However, T-REC shall hit by a major setback if new and innovative version is

launched by competitor, the above observation may not hold true.

Recommendation and Justifications

Based on above, it shall be recommended to directors and other KMP of All Cure Inc.

to go for investing in T-REC as the said product is clinically safe to launch and same

is feasible at Weighted Average Cost of Capital less than 22%. Further, launching P-

REC is in grafted with major issue that the same may have failure in the future, as the

product is not 100% clinically tested. However, the project has return in the short run

greater than 24% WACC.

Detail Comparison and Further Recommendation

A differentiation of two projects based on various parameters has been presented here

in below:

Sl No Particular P-REC T-REC

1 Discounted Pay Back period @18% 5.251532 7.024696201

2 Discounted Pay Back period @24% 6.473792 Never Paid off

3 Net Present Value @18% 1153831 220793.9465

The qualitative analysis of the two projects has been carried out here in below:

(a) P-REC is an under tested product with undetectable long-term hazard that may

develop in the body of individual who may consume the same. The product is

under a nascent test and may be subject to certification during consideration by

national testing bodies;

(b) If P-REC is implemented, there may be litigation and dispute in future on account

of side impact of the product and shall tarnish the image and future long term

prospects of the proposed company;

(c) Pharmaceutical Sector has been prone to litigation, disputes and bans risk.

Accordingly, launching a 100% untested product with knowledge of failure can

be very risky;

(d) Launching of P-REC may hamper the long term continuity of the organisation is

the said product turns out to be a major failure of the company on account of long

term issues in the product.

(e) Considering T-REC, it shall be pertinent to note is traditional product and is

clinically safe and tested. Further, the side of the product is not available at the

disposal of the company and it is presumed that this shall be safe .However,

(f) T-REC in addition to above shall be less prone to litigation and disputes.

However, T-REC shall hit by a major setback if new and innovative version is

launched by competitor, the above observation may not hold true.

Recommendation and Justifications

Based on above, it shall be recommended to directors and other KMP of All Cure Inc.

to go for investing in T-REC as the said product is clinically safe to launch and same

is feasible at Weighted Average Cost of Capital less than 22%. Further, launching P-

REC is in grafted with major issue that the same may have failure in the future, as the

product is not 100% clinically tested. However, the project has return in the short run

greater than 24% WACC.

Detail Comparison and Further Recommendation

A differentiation of two projects based on various parameters has been presented here

in below:

Sl No Particular P-REC T-REC

1 Discounted Pay Back period @18% 5.251532 7.024696201

2 Discounted Pay Back period @24% 6.473792 Never Paid off

3 Net Present Value @18% 1153831 220793.9465

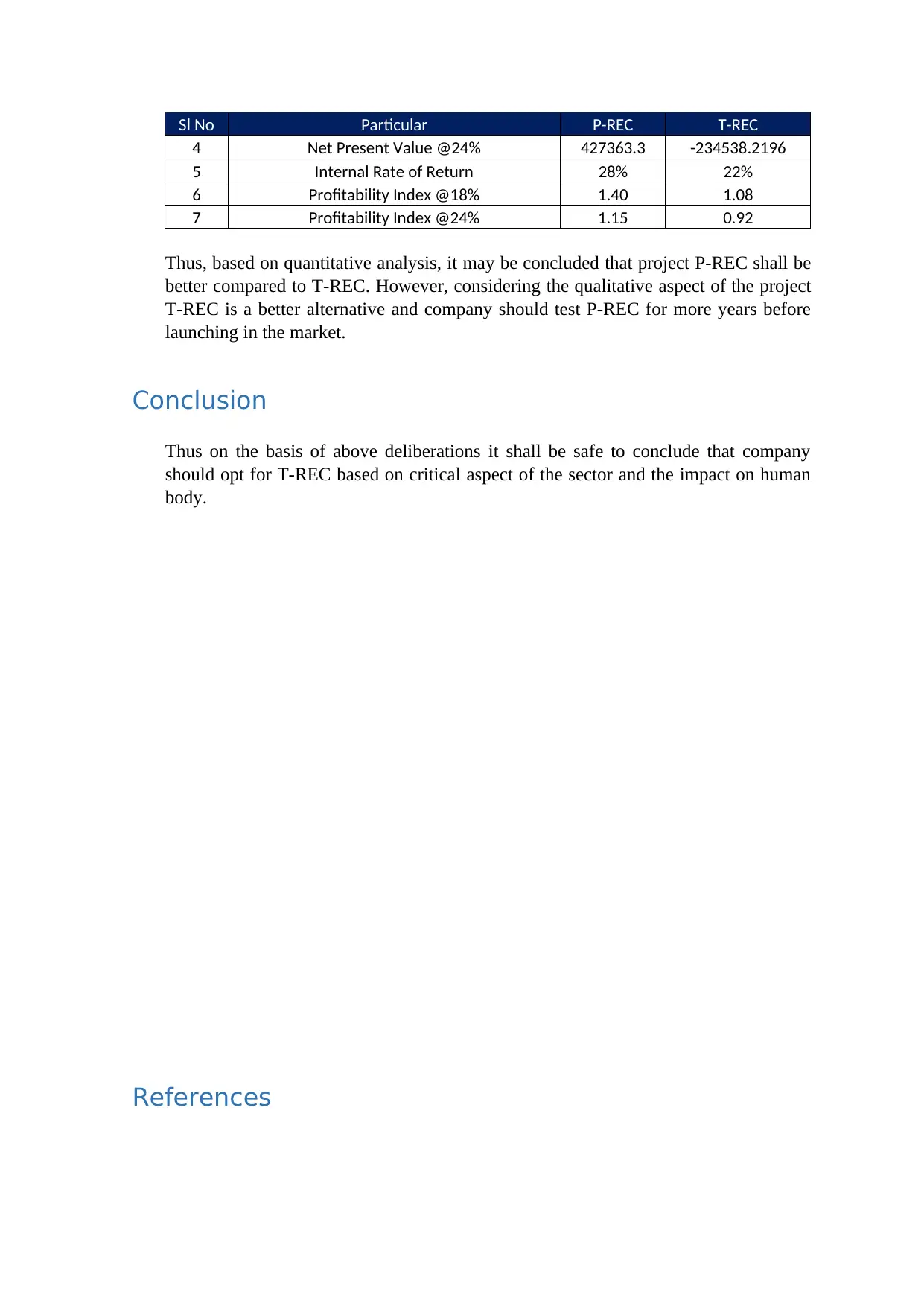

Sl No Particular P-REC T-REC

4 Net Present Value @24% 427363.3 -234538.2196

5 Internal Rate of Return 28% 22%

6 Profitability Index @18% 1.40 1.08

7 Profitability Index @24% 1.15 0.92

Thus, based on quantitative analysis, it may be concluded that project P-REC shall be

better compared to T-REC. However, considering the qualitative aspect of the project

T-REC is a better alternative and company should test P-REC for more years before

launching in the market.

Conclusion

Thus on the basis of above deliberations it shall be safe to conclude that company

should opt for T-REC based on critical aspect of the sector and the impact on human

body.

References

4 Net Present Value @24% 427363.3 -234538.2196

5 Internal Rate of Return 28% 22%

6 Profitability Index @18% 1.40 1.08

7 Profitability Index @24% 1.15 0.92

Thus, based on quantitative analysis, it may be concluded that project P-REC shall be

better compared to T-REC. However, considering the qualitative aspect of the project

T-REC is a better alternative and company should test P-REC for more years before

launching in the market.

Conclusion

Thus on the basis of above deliberations it shall be safe to conclude that company

should opt for T-REC based on critical aspect of the sector and the impact on human

body.

References

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting For Management, 2018. Internal rate of return method. [Online]

Available at: https://www.accountingformanagement.org/internal-rate-of-return-method/

[Accessed 5 October 2018].

Anon., 2018. Payback Period & Discounted Payback Period | Formula | Example. [Online]

Available at: https://www.wallstreetmojo.com/payback-period-discounted-payback-period/

[Accessed 5 October 2018].

Bennett, Coleman & Co. Ltd., 2018. Definition of 'Profitability Index'. [Online]

Available at: https://economictimes.indiatimes.com/definition/profitability-index

[Accessed 5 October 2018].

InvestingAnswers, Inc, 2018. Net Present Value (NPV). [Online]

Available at: https://investinganswers.com/financial-dictionary/technical-analysis/net-present-

value-npv-2995

[Accessed 5 October 2018].

Available at: https://www.accountingformanagement.org/internal-rate-of-return-method/

[Accessed 5 October 2018].

Anon., 2018. Payback Period & Discounted Payback Period | Formula | Example. [Online]

Available at: https://www.wallstreetmojo.com/payback-period-discounted-payback-period/

[Accessed 5 October 2018].

Bennett, Coleman & Co. Ltd., 2018. Definition of 'Profitability Index'. [Online]

Available at: https://economictimes.indiatimes.com/definition/profitability-index

[Accessed 5 October 2018].

InvestingAnswers, Inc, 2018. Net Present Value (NPV). [Online]

Available at: https://investinganswers.com/financial-dictionary/technical-analysis/net-present-

value-npv-2995

[Accessed 5 October 2018].

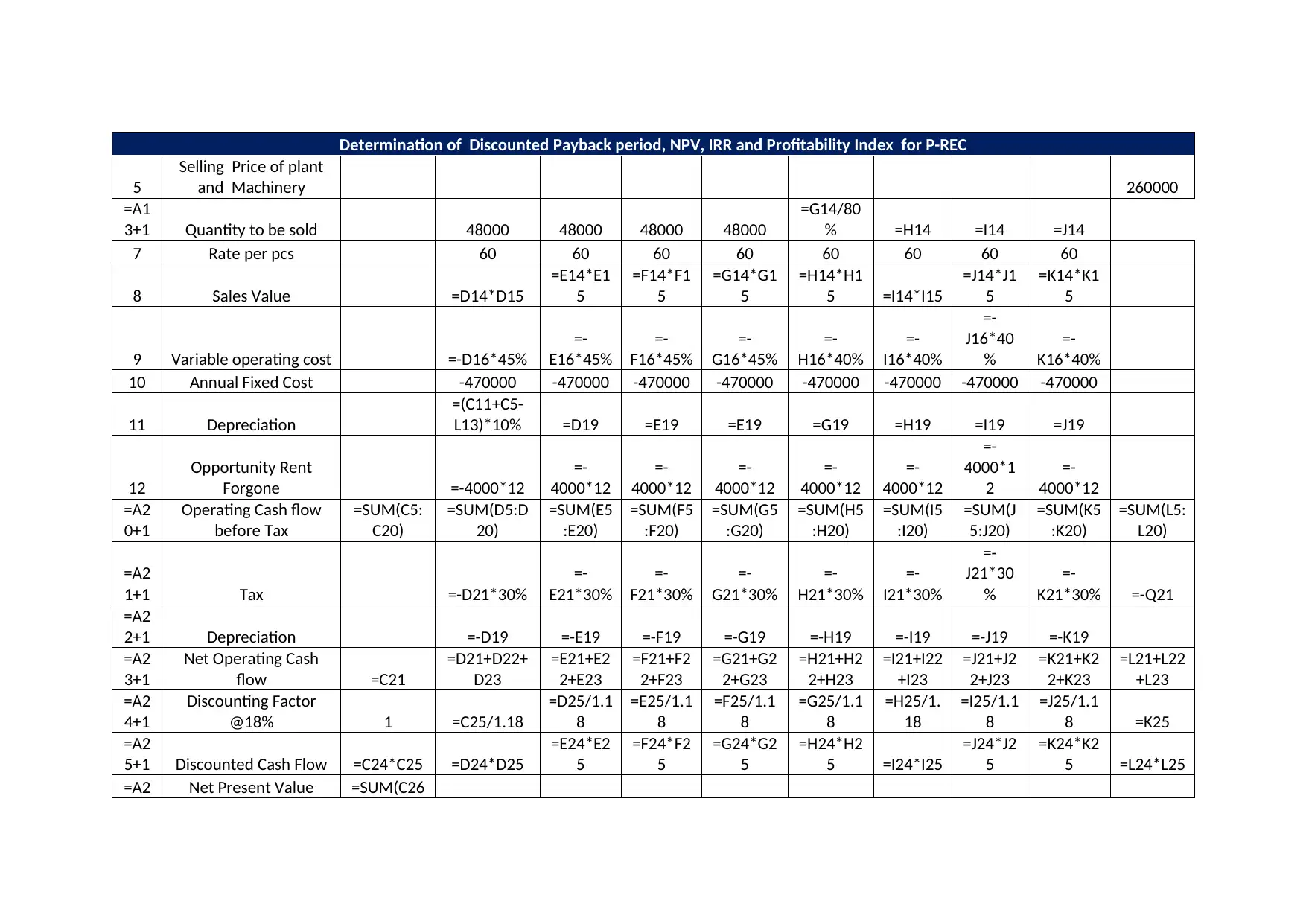

Appendix-1

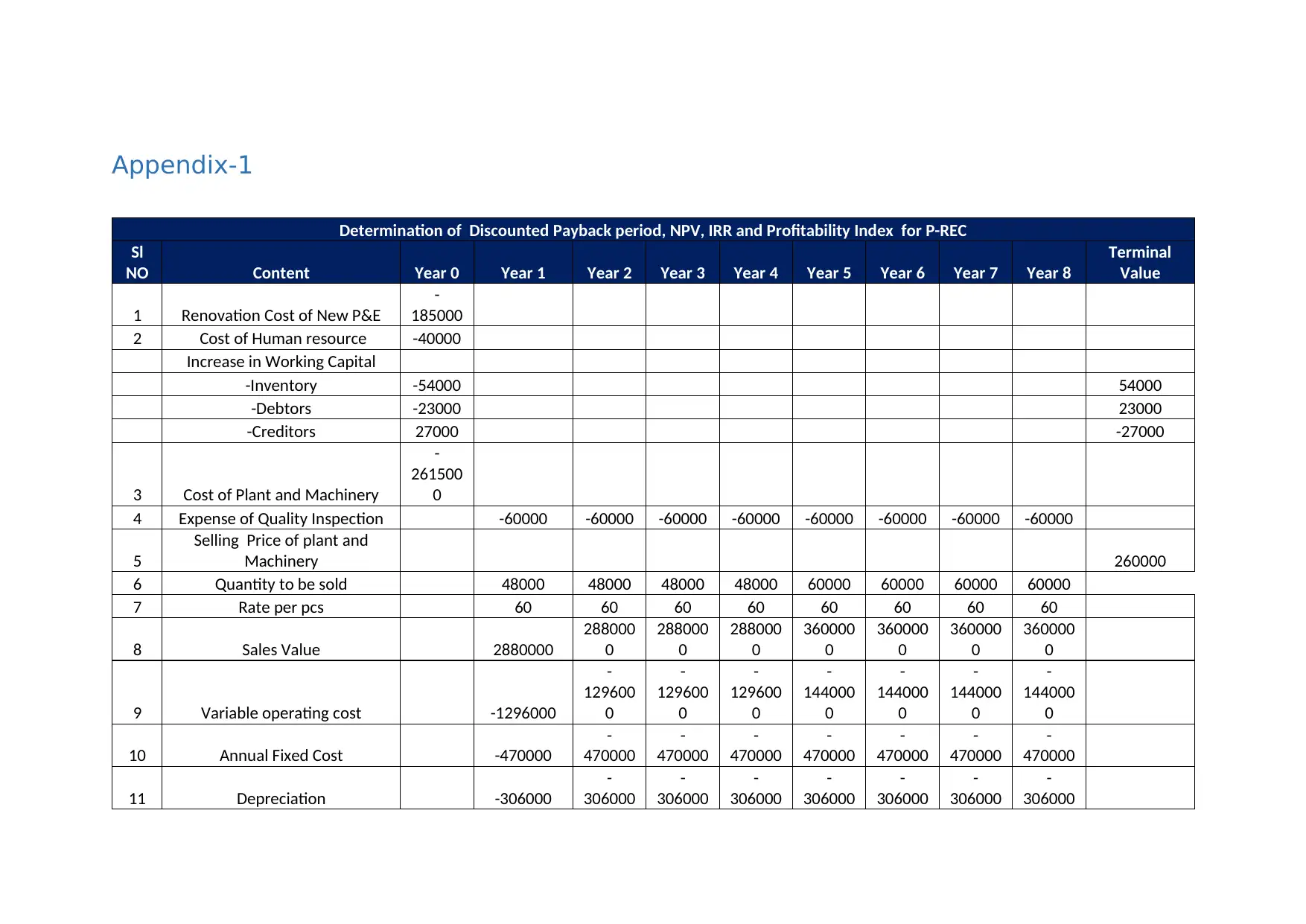

Determination of Discounted Payback period, NPV, IRR and Profitability Index for P-REC

Sl

NO Content Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

Terminal

Value

1 Renovation Cost of New P&E

-

185000

2 Cost of Human resource -40000

Increase in Working Capital

-Inventory -54000 54000

-Debtors -23000 23000

-Creditors 27000 -27000

3 Cost of Plant and Machinery

-

261500

0

4 Expense of Quality Inspection -60000 -60000 -60000 -60000 -60000 -60000 -60000 -60000

5

Selling Price of plant and

Machinery 260000

6 Quantity to be sold 48000 48000 48000 48000 60000 60000 60000 60000

7 Rate per pcs 60 60 60 60 60 60 60 60

8 Sales Value 2880000

288000

0

288000

0

288000

0

360000

0

360000

0

360000

0

360000

0

9 Variable operating cost -1296000

-

129600

0

-

129600

0

-

129600

0

-

144000

0

-

144000

0

-

144000

0

-

144000

0

10 Annual Fixed Cost -470000

-

470000

-

470000

-

470000

-

470000

-

470000

-

470000

-

470000

11 Depreciation -306000

-

306000

-

306000

-

306000

-

306000

-

306000

-

306000

-

306000

Determination of Discounted Payback period, NPV, IRR and Profitability Index for P-REC

Sl

NO Content Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

Terminal

Value

1 Renovation Cost of New P&E

-

185000

2 Cost of Human resource -40000

Increase in Working Capital

-Inventory -54000 54000

-Debtors -23000 23000

-Creditors 27000 -27000

3 Cost of Plant and Machinery

-

261500

0

4 Expense of Quality Inspection -60000 -60000 -60000 -60000 -60000 -60000 -60000 -60000

5

Selling Price of plant and

Machinery 260000

6 Quantity to be sold 48000 48000 48000 48000 60000 60000 60000 60000

7 Rate per pcs 60 60 60 60 60 60 60 60

8 Sales Value 2880000

288000

0

288000

0

288000

0

360000

0

360000

0

360000

0

360000

0

9 Variable operating cost -1296000

-

129600

0

-

129600

0

-

129600

0

-

144000

0

-

144000

0

-

144000

0

-

144000

0

10 Annual Fixed Cost -470000

-

470000

-

470000

-

470000

-

470000

-

470000

-

470000

-

470000

11 Depreciation -306000

-

306000

-

306000

-

306000

-

306000

-

306000

-

306000

-

306000

Determination of Discounted Payback period, NPV, IRR and Profitability Index for P-REC

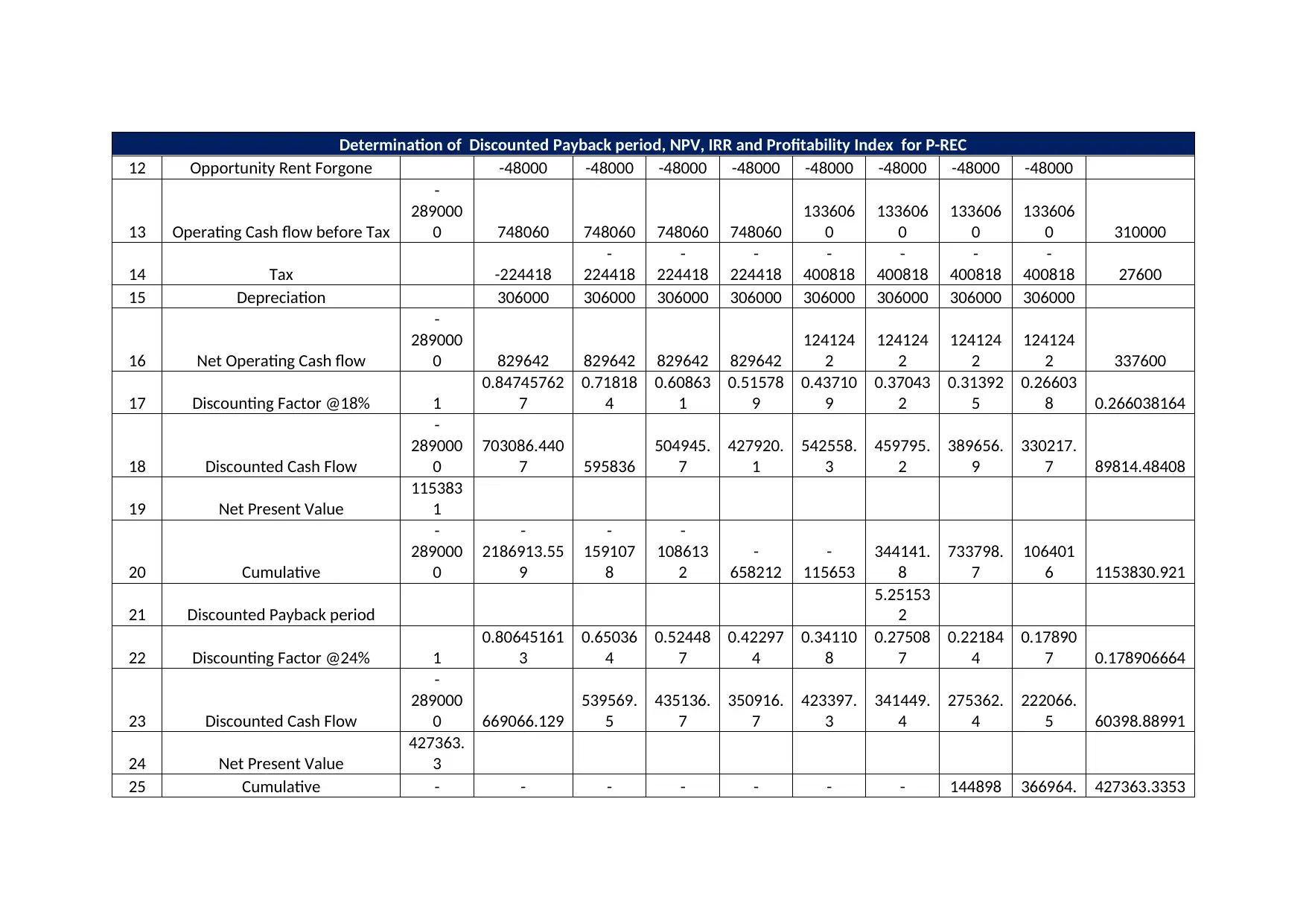

12 Opportunity Rent Forgone -48000 -48000 -48000 -48000 -48000 -48000 -48000 -48000

13 Operating Cash flow before Tax

-

289000

0 748060 748060 748060 748060

133606

0

133606

0

133606

0

133606

0 310000

14 Tax -224418

-

224418

-

224418

-

224418

-

400818

-

400818

-

400818

-

400818 27600

15 Depreciation 306000 306000 306000 306000 306000 306000 306000 306000

16 Net Operating Cash flow

-

289000

0 829642 829642 829642 829642

124124

2

124124

2

124124

2

124124

2 337600

17 Discounting Factor @18% 1

0.84745762

7

0.71818

4

0.60863

1

0.51578

9

0.43710

9

0.37043

2

0.31392

5

0.26603

8 0.266038164

18 Discounted Cash Flow

-

289000

0

703086.440

7 595836

504945.

7

427920.

1

542558.

3

459795.

2

389656.

9

330217.

7 89814.48408

19 Net Present Value

115383

1

20 Cumulative

-

289000

0

-

2186913.55

9

-

159107

8

-

108613

2

-

658212

-

115653

344141.

8

733798.

7

106401

6 1153830.921

21 Discounted Payback period

5.25153

2

22 Discounting Factor @24% 1

0.80645161

3

0.65036

4

0.52448

7

0.42297

4

0.34110

8

0.27508

7

0.22184

4

0.17890

7 0.178906664

23 Discounted Cash Flow

-

289000

0 669066.129

539569.

5

435136.

7

350916.

7

423397.

3

341449.

4

275362.

4

222066.

5 60398.88991

24 Net Present Value

427363.

3

25 Cumulative - - - - - - - 144898 366964. 427363.3353

12 Opportunity Rent Forgone -48000 -48000 -48000 -48000 -48000 -48000 -48000 -48000

13 Operating Cash flow before Tax

-

289000

0 748060 748060 748060 748060

133606

0

133606

0

133606

0

133606

0 310000

14 Tax -224418

-

224418

-

224418

-

224418

-

400818

-

400818

-

400818

-

400818 27600

15 Depreciation 306000 306000 306000 306000 306000 306000 306000 306000

16 Net Operating Cash flow

-

289000

0 829642 829642 829642 829642

124124

2

124124

2

124124

2

124124

2 337600

17 Discounting Factor @18% 1

0.84745762

7

0.71818

4

0.60863

1

0.51578

9

0.43710

9

0.37043

2

0.31392

5

0.26603

8 0.266038164

18 Discounted Cash Flow

-

289000

0

703086.440

7 595836

504945.

7

427920.

1

542558.

3

459795.

2

389656.

9

330217.

7 89814.48408

19 Net Present Value

115383

1

20 Cumulative

-

289000

0

-

2186913.55

9

-

159107

8

-

108613

2

-

658212

-

115653

344141.

8

733798.

7

106401

6 1153830.921

21 Discounted Payback period

5.25153

2

22 Discounting Factor @24% 1

0.80645161

3

0.65036

4

0.52448

7

0.42297

4

0.34110

8

0.27508

7

0.22184

4

0.17890

7 0.178906664

23 Discounted Cash Flow

-

289000

0 669066.129

539569.

5

435136.

7

350916.

7

423397.

3

341449.

4

275362.

4

222066.

5 60398.88991

24 Net Present Value

427363.

3

25 Cumulative - - - - - - - 144898 366964. 427363.3353

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Determination of Discounted Payback period, NPV, IRR and Profitability Index for P-REC

289000

0

2220933.87

1

168136

4

124622

8 895311 471914 130464 4

26 Discounted Payback period

6.47379

2

27 Internal Rate of Return 28%

28 Profitability Index @18% 1.399

29 Profitability Index @24% 1.148

Computation of Net Present Value for T-REC

Sl

NO Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

Terminal

Value

1 Future Cash Flows 1235000

118600

0 964000 752000 695000 670000 634000 590000

2 Renovation Cost -185000

3 Human Resource Cost -40000

4

Plant and Machinery

Cost

-

2615000

5 Depreciation -306000 -306000 -306000 -306000 -306000 -306000 -306000 -306000

6

Increase in Working

Capital

-Inventory -54000 54000

-Debtors -23000 23000

-Creditors 27000 -27000

7 Salvage 260000

8 Cash flow before tax

-

2890000 929000 880000 658000 446000 389000 364000 328000 284000 310000

9 Tax -278700 -264000 -197400 -133800 -116700 -109200 -98400 -85200 27600

289000

0

2220933.87

1

168136

4

124622

8 895311 471914 130464 4

26 Discounted Payback period

6.47379

2

27 Internal Rate of Return 28%

28 Profitability Index @18% 1.399

29 Profitability Index @24% 1.148

Computation of Net Present Value for T-REC

Sl

NO Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

Terminal

Value

1 Future Cash Flows 1235000

118600

0 964000 752000 695000 670000 634000 590000

2 Renovation Cost -185000

3 Human Resource Cost -40000

4

Plant and Machinery

Cost

-

2615000

5 Depreciation -306000 -306000 -306000 -306000 -306000 -306000 -306000 -306000

6

Increase in Working

Capital

-Inventory -54000 54000

-Debtors -23000 23000

-Creditors 27000 -27000

7 Salvage 260000

8 Cash flow before tax

-

2890000 929000 880000 658000 446000 389000 364000 328000 284000 310000

9 Tax -278700 -264000 -197400 -133800 -116700 -109200 -98400 -85200 27600

Computation of Net Present Value for T-REC

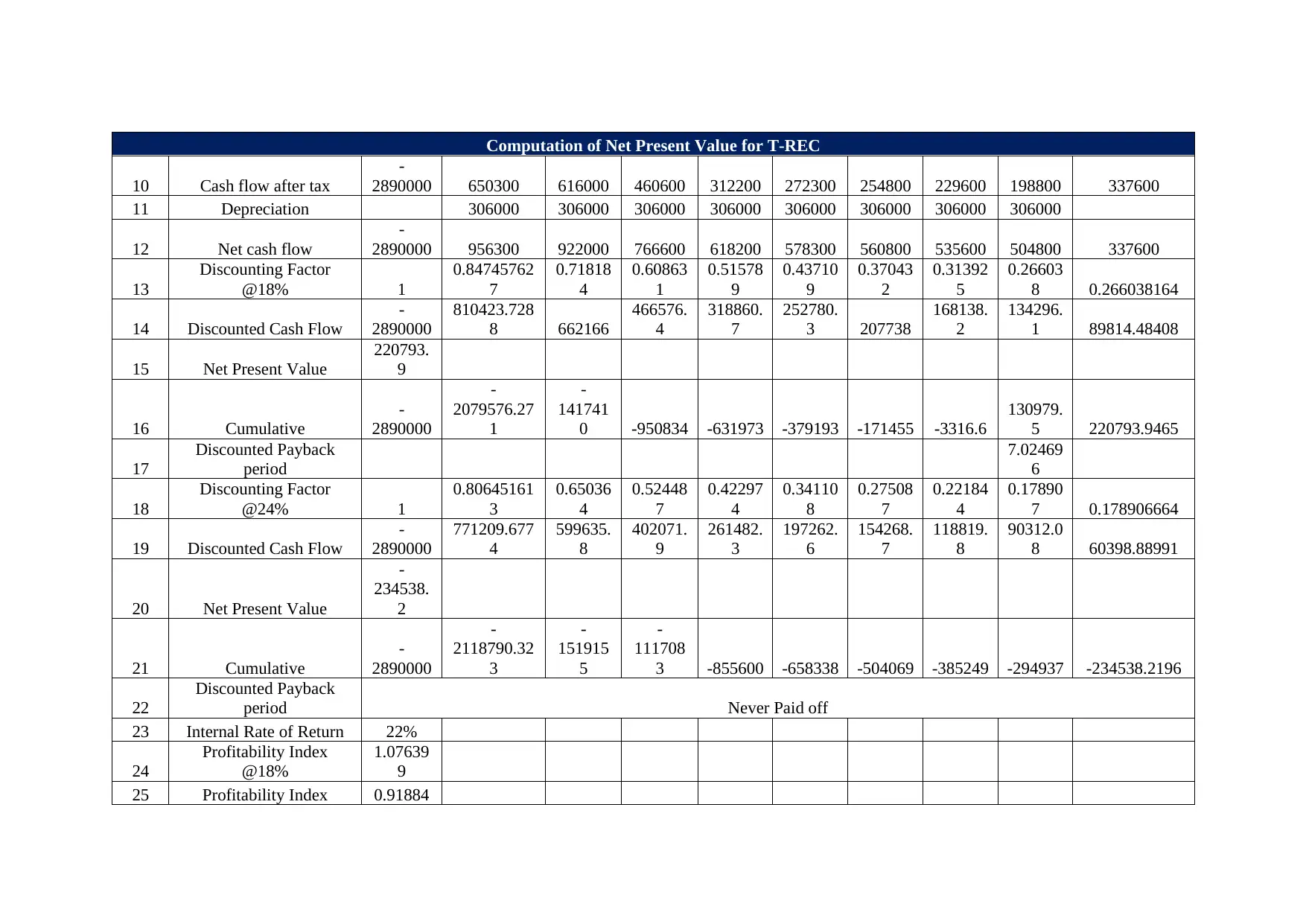

10 Cash flow after tax

-

2890000 650300 616000 460600 312200 272300 254800 229600 198800 337600

11 Depreciation 306000 306000 306000 306000 306000 306000 306000 306000

12 Net cash flow

-

2890000 956300 922000 766600 618200 578300 560800 535600 504800 337600

13

Discounting Factor

@18% 1

0.84745762

7

0.71818

4

0.60863

1

0.51578

9

0.43710

9

0.37043

2

0.31392

5

0.26603

8 0.266038164

14 Discounted Cash Flow

-

2890000

810423.728

8 662166

466576.

4

318860.

7

252780.

3 207738

168138.

2

134296.

1 89814.48408

15 Net Present Value

220793.

9

16 Cumulative

-

2890000

-

2079576.27

1

-

141741

0 -950834 -631973 -379193 -171455 -3316.6

130979.

5 220793.9465

17

Discounted Payback

period

7.02469

6

18

Discounting Factor

@24% 1

0.80645161

3

0.65036

4

0.52448

7

0.42297

4

0.34110

8

0.27508

7

0.22184

4

0.17890

7 0.178906664

19 Discounted Cash Flow

-

2890000

771209.677

4

599635.

8

402071.

9

261482.

3

197262.

6

154268.

7

118819.

8

90312.0

8 60398.88991

20 Net Present Value

-

234538.

2

21 Cumulative

-

2890000

-

2118790.32

3

-

151915

5

-

111708

3 -855600 -658338 -504069 -385249 -294937 -234538.2196

22

Discounted Payback

period Never Paid off

23 Internal Rate of Return 22%

24

Profitability Index

@18%

1.07639

9

25 Profitability Index 0.91884

10 Cash flow after tax

-

2890000 650300 616000 460600 312200 272300 254800 229600 198800 337600

11 Depreciation 306000 306000 306000 306000 306000 306000 306000 306000

12 Net cash flow

-

2890000 956300 922000 766600 618200 578300 560800 535600 504800 337600

13

Discounting Factor

@18% 1

0.84745762

7

0.71818

4

0.60863

1

0.51578

9

0.43710

9

0.37043

2

0.31392

5

0.26603

8 0.266038164

14 Discounted Cash Flow

-

2890000

810423.728

8 662166

466576.

4

318860.

7

252780.

3 207738

168138.

2

134296.

1 89814.48408

15 Net Present Value

220793.

9

16 Cumulative

-

2890000

-

2079576.27

1

-

141741

0 -950834 -631973 -379193 -171455 -3316.6

130979.

5 220793.9465

17

Discounted Payback

period

7.02469

6

18

Discounting Factor

@24% 1

0.80645161

3

0.65036

4

0.52448

7

0.42297

4

0.34110

8

0.27508

7

0.22184

4

0.17890

7 0.178906664

19 Discounted Cash Flow

-

2890000

771209.677

4

599635.

8

402071.

9

261482.

3

197262.

6

154268.

7

118819.

8

90312.0

8 60398.88991

20 Net Present Value

-

234538.

2

21 Cumulative

-

2890000

-

2118790.32

3

-

151915

5

-

111708

3 -855600 -658338 -504069 -385249 -294937 -234538.2196

22

Discounted Payback

period Never Paid off

23 Internal Rate of Return 22%

24

Profitability Index

@18%

1.07639

9

25 Profitability Index 0.91884

Computation of Net Present Value for T-REC

@18% 5

Appendix -2

Determination of Discounted Payback period, NPV, IRR and Profitability Index for P-REC

Sl

NO Content Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

Terminal

Value

1

Renovation Cost of

New P&E -185000

2

Cost of Human

resource -40000

Increase in Working

Capital

-Inventory -54000 =-C8

-Debtors -23000 =-C9

-Creditors 27000 =-C10

3

Cost of Plant and

Machinery

=-

2550000-

65000

4

Expense of Quality

Inspection =-5000*12

=-

5000*12

=-

5000*12

=-

5000*12

=-

5000*12

=-

5000*12

=-

5000*1

2

=-

5000*12

@18% 5

Appendix -2

Determination of Discounted Payback period, NPV, IRR and Profitability Index for P-REC

Sl

NO Content Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

Terminal

Value

1

Renovation Cost of

New P&E -185000

2

Cost of Human

resource -40000

Increase in Working

Capital

-Inventory -54000 =-C8

-Debtors -23000 =-C9

-Creditors 27000 =-C10

3

Cost of Plant and

Machinery

=-

2550000-

65000

4

Expense of Quality

Inspection =-5000*12

=-

5000*12

=-

5000*12

=-

5000*12

=-

5000*12

=-

5000*12

=-

5000*1

2

=-

5000*12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Determination of Discounted Payback period, NPV, IRR and Profitability Index for P-REC

5

Selling Price of plant

and Machinery 260000

=A1

3+1 Quantity to be sold 48000 48000 48000 48000

=G14/80

% =H14 =I14 =J14

7 Rate per pcs 60 60 60 60 60 60 60 60

8 Sales Value =D14*D15

=E14*E1

5

=F14*F1

5

=G14*G1

5

=H14*H1

5 =I14*I15

=J14*J1

5

=K14*K1

5

9 Variable operating cost =-D16*45%

=-

E16*45%

=-

F16*45%

=-

G16*45%

=-

H16*40%

=-

I16*40%

=-

J16*40

%

=-

K16*40%

10 Annual Fixed Cost -470000 -470000 -470000 -470000 -470000 -470000 -470000 -470000

11 Depreciation

=(C11+C5-

L13)*10% =D19 =E19 =E19 =G19 =H19 =I19 =J19

12

Opportunity Rent

Forgone =-4000*12

=-

4000*12

=-

4000*12

=-

4000*12

=-

4000*12

=-

4000*12

=-

4000*1

2

=-

4000*12

=A2

0+1

Operating Cash flow

before Tax

=SUM(C5:

C20)

=SUM(D5:D

20)

=SUM(E5

:E20)

=SUM(F5

:F20)

=SUM(G5

:G20)

=SUM(H5

:H20)

=SUM(I5

:I20)

=SUM(J

5:J20)

=SUM(K5

:K20)

=SUM(L5:

L20)

=A2

1+1 Tax =-D21*30%

=-

E21*30%

=-

F21*30%

=-

G21*30%

=-

H21*30%

=-

I21*30%

=-

J21*30

%

=-

K21*30% =-Q21

=A2

2+1 Depreciation =-D19 =-E19 =-F19 =-G19 =-H19 =-I19 =-J19 =-K19

=A2

3+1

Net Operating Cash

flow =C21

=D21+D22+

D23

=E21+E2

2+E23

=F21+F2

2+F23

=G21+G2

2+G23

=H21+H2

2+H23

=I21+I22

+I23

=J21+J2

2+J23

=K21+K2

2+K23

=L21+L22

+L23

=A2

4+1

Discounting Factor

@18% 1 =C25/1.18

=D25/1.1

8

=E25/1.1

8

=F25/1.1

8

=G25/1.1

8

=H25/1.

18

=I25/1.1

8

=J25/1.1

8 =K25

=A2

5+1 Discounted Cash Flow =C24*C25 =D24*D25

=E24*E2

5

=F24*F2

5

=G24*G2

5

=H24*H2

5 =I24*I25

=J24*J2

5

=K24*K2

5 =L24*L25

=A2 Net Present Value =SUM(C26

5

Selling Price of plant

and Machinery 260000

=A1

3+1 Quantity to be sold 48000 48000 48000 48000

=G14/80

% =H14 =I14 =J14

7 Rate per pcs 60 60 60 60 60 60 60 60

8 Sales Value =D14*D15

=E14*E1

5

=F14*F1

5

=G14*G1

5

=H14*H1

5 =I14*I15

=J14*J1

5

=K14*K1

5

9 Variable operating cost =-D16*45%

=-

E16*45%

=-

F16*45%

=-

G16*45%

=-

H16*40%

=-

I16*40%

=-

J16*40

%

=-

K16*40%

10 Annual Fixed Cost -470000 -470000 -470000 -470000 -470000 -470000 -470000 -470000

11 Depreciation

=(C11+C5-

L13)*10% =D19 =E19 =E19 =G19 =H19 =I19 =J19

12

Opportunity Rent

Forgone =-4000*12

=-

4000*12

=-

4000*12

=-

4000*12

=-

4000*12

=-

4000*12

=-

4000*1

2

=-

4000*12

=A2

0+1

Operating Cash flow

before Tax

=SUM(C5:

C20)

=SUM(D5:D

20)

=SUM(E5

:E20)

=SUM(F5

:F20)

=SUM(G5

:G20)

=SUM(H5

:H20)

=SUM(I5

:I20)

=SUM(J

5:J20)

=SUM(K5

:K20)

=SUM(L5:

L20)

=A2

1+1 Tax =-D21*30%

=-

E21*30%

=-

F21*30%

=-

G21*30%

=-

H21*30%

=-

I21*30%

=-

J21*30

%

=-

K21*30% =-Q21

=A2

2+1 Depreciation =-D19 =-E19 =-F19 =-G19 =-H19 =-I19 =-J19 =-K19

=A2

3+1

Net Operating Cash

flow =C21

=D21+D22+

D23

=E21+E2

2+E23

=F21+F2

2+F23

=G21+G2

2+G23

=H21+H2

2+H23

=I21+I22

+I23

=J21+J2

2+J23

=K21+K2

2+K23

=L21+L22

+L23

=A2

4+1

Discounting Factor

@18% 1 =C25/1.18

=D25/1.1

8

=E25/1.1

8

=F25/1.1

8

=G25/1.1

8

=H25/1.

18

=I25/1.1

8

=J25/1.1

8 =K25

=A2

5+1 Discounted Cash Flow =C24*C25 =D24*D25

=E24*E2

5

=F24*F2

5

=G24*G2

5

=H24*H2

5 =I24*I25

=J24*J2

5

=K24*K2

5 =L24*L25

=A2 Net Present Value =SUM(C26

Determination of Discounted Payback period, NPV, IRR and Profitability Index for P-REC

6+1 :L26)

=A2

7+1 Cumulative =C26 =C26+D26

=D28+E2

6

=E28+F2

6

=F28+G2

6

=G28+H2

6

=H28+I2

6

=I28+J2

6

=J28+K2

6 =K28+L26

=A2

8+1

Discounted Payback

period

=5+(-

H28/I26)

=A2

9+1

Discounting Factor

@24% 1 =C30/1.24

=D30/1.2

4

=E30/1.2

4

=F30/1.2

4

=G30/1.2

4

=H30/1.

24

=I30/1.2

4

=J30/1.2

4 =K30

=A3

0+1 Discounted Cash Flow =C30*C24 =D30*D24

=E30*E2

4

=F30*F2

4

=G30*G2

4

=H30*H2

4 =I30*I24

=J30*J2

4

=K30*K2

4 =L30*L24

=A3

1+1 Net Present Value

=SUM(C31

:L31)

=A3

2+1 Cumulative =C31 =C33+D31

=D33+E3

1

=E33+F3

1

=F33+G3

1

=G33+H3

1

=H33+I3

1

=I33+J3

1

=J33+K3

1 =K33+L31

=A3

3+1

Discounted Payback

period

=6+(-

I33/J31)

=A3

4+1 Internal Rate of Return

=IRR(N35:

N45)

=A3

5+1

Profitability Index

@18%

=1+L28/-

C28

=A3

6+1

Profitability Index

@24%

=1+L33/-

C33

Computation of Net Present Value for T-REC

Sl

NO Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

Terminal

Value

1 Future Cash Flows 1235000 1186000 964000 752000 695000 670000 634000 590000

2 =B5 =C5

6+1 :L26)

=A2

7+1 Cumulative =C26 =C26+D26

=D28+E2

6

=E28+F2

6

=F28+G2

6

=G28+H2

6

=H28+I2

6

=I28+J2

6

=J28+K2

6 =K28+L26

=A2

8+1

Discounted Payback

period

=5+(-

H28/I26)

=A2

9+1

Discounting Factor

@24% 1 =C30/1.24

=D30/1.2

4

=E30/1.2

4

=F30/1.2

4

=G30/1.2

4

=H30/1.

24

=I30/1.2

4

=J30/1.2

4 =K30

=A3

0+1 Discounted Cash Flow =C30*C24 =D30*D24

=E30*E2

4

=F30*F2

4

=G30*G2

4

=H30*H2

4 =I30*I24

=J30*J2

4

=K30*K2

4 =L30*L24

=A3

1+1 Net Present Value

=SUM(C31

:L31)

=A3

2+1 Cumulative =C31 =C33+D31

=D33+E3

1

=E33+F3

1

=F33+G3

1

=G33+H3

1

=H33+I3

1

=I33+J3

1

=J33+K3

1 =K33+L31

=A3

3+1

Discounted Payback

period

=6+(-

I33/J31)

=A3

4+1 Internal Rate of Return

=IRR(N35:

N45)

=A3

5+1

Profitability Index

@18%

=1+L28/-

C28

=A3

6+1

Profitability Index

@24%

=1+L33/-

C33

Computation of Net Present Value for T-REC

Sl

NO Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

Terminal

Value

1 Future Cash Flows 1235000 1186000 964000 752000 695000 670000 634000 590000

2 =B5 =C5

Computation of Net Present Value for T-REC

3 =B6 =C6

4 =B8 =C8

5 Depreciation =D13 =E13 =F13 =G13 =H13 =I13 =J13 =K13

6

Increase in

Working Capital

-Inventory =C18 =L18

-Debtors =C19 =L19

-Creditors =C20 =L20

7 Salvage =L9

8

Cash flow before

tax

=SUM(C4

3:C51)

=SUM(D43

:D51)

=SUM(E4

3:E51)

=SUM(F4

3:F51)

=SUM(G43

:G51)

=SUM(H43

:H51)

=SUM(I4

3:I51)

=SUM(J4

3:J51)

=SUM(K4

3:K51)

=SUM(L4

3:L52)

9 Tax

=-

D53*30%

=-

E53*30%

=-

F53*30%

=-

G53*30%

=-

H53*30%

=-

I53*30%

=-

J53*30%

=-

K53*30% =-Q15

10

Cash flow after

tax =C53+C54 =D53+D54 =E53+E54 =F53+F54 =G53+G54 =H53+H54 =I53+I54 =J53+J54 =K53+K54 =L53+L54

11 Depreciation =-D47 =-E47 =-F47 =-G47 =-H47 =-I47 =-J47 =-K47

12 Net cash flow =C55+C56 =D55+D56 =E55+E56 =F55+F56 =G55+G56 =H55+H56 =I55+I56 =J55+J56 =K55+K56 =L55+L56

13

Discounting

Factor @18% =C25 =D25 =E25 =F25 =G25 =H25 =I25 =J25 =K25 =L25

=A5

8+1

Discounted Cash

Flow =C57*C58 =D57*D58 =E57*E58 =F57*F58 =G57*G58 =H57*H58 =I57*I58 =J57*J58 =K57*K58 =L57*L58

=A5

9+1 Net Present Value

=SUM(C5

9:L59)

=A6

0+1 Cumulative =C59 =C59+D59 =D61+E59 =E61+F59 =F61+G59 =G61+H59 =H61+I59 =I61+J59 =J61+K59 =K61+L59

=A6

1+1

Discounted

Payback period

=7+(-

J61/K59)

=A6

2+1

Discounting

Factor @24% 1 =C63/1.24

=D63/1.2

4 =E63/1.24 =F63/1.24 =G63/1.24

=H63/1.2

4 =I63/1.24 =J63/1.24 =K63

3 =B6 =C6

4 =B8 =C8

5 Depreciation =D13 =E13 =F13 =G13 =H13 =I13 =J13 =K13

6

Increase in

Working Capital

-Inventory =C18 =L18

-Debtors =C19 =L19

-Creditors =C20 =L20

7 Salvage =L9

8

Cash flow before

tax

=SUM(C4

3:C51)

=SUM(D43

:D51)

=SUM(E4

3:E51)

=SUM(F4

3:F51)

=SUM(G43

:G51)

=SUM(H43

:H51)

=SUM(I4

3:I51)

=SUM(J4

3:J51)

=SUM(K4

3:K51)

=SUM(L4

3:L52)

9 Tax

=-

D53*30%

=-

E53*30%

=-

F53*30%

=-

G53*30%

=-

H53*30%

=-

I53*30%

=-

J53*30%

=-

K53*30% =-Q15

10

Cash flow after

tax =C53+C54 =D53+D54 =E53+E54 =F53+F54 =G53+G54 =H53+H54 =I53+I54 =J53+J54 =K53+K54 =L53+L54

11 Depreciation =-D47 =-E47 =-F47 =-G47 =-H47 =-I47 =-J47 =-K47

12 Net cash flow =C55+C56 =D55+D56 =E55+E56 =F55+F56 =G55+G56 =H55+H56 =I55+I56 =J55+J56 =K55+K56 =L55+L56

13

Discounting

Factor @18% =C25 =D25 =E25 =F25 =G25 =H25 =I25 =J25 =K25 =L25

=A5

8+1

Discounted Cash

Flow =C57*C58 =D57*D58 =E57*E58 =F57*F58 =G57*G58 =H57*H58 =I57*I58 =J57*J58 =K57*K58 =L57*L58

=A5

9+1 Net Present Value

=SUM(C5

9:L59)

=A6

0+1 Cumulative =C59 =C59+D59 =D61+E59 =E61+F59 =F61+G59 =G61+H59 =H61+I59 =I61+J59 =J61+K59 =K61+L59

=A6

1+1

Discounted

Payback period

=7+(-

J61/K59)

=A6

2+1

Discounting

Factor @24% 1 =C63/1.24

=D63/1.2

4 =E63/1.24 =F63/1.24 =G63/1.24

=H63/1.2

4 =I63/1.24 =J63/1.24 =K63

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Computation of Net Present Value for T-REC

=A6

3+1

Discounted Cash

Flow =C63*C57 =D63*D57 =E63*E57 =F63*F57 =G63*G57 =H63*H57 =I63*I57 =J63*J57 =K63*K57 =L63*L57

=A6

4+1 Net Present Value

=SUM(C6

4:L64)

=A6

5+1 Cumulative =C64 =C66+D64 =D66+E64 =E66+F64 =F66+G64 =G66+H64 =H66+I64 =I66+J64 =J66+K64 =K66+L64

=A6

6+1

Discounted

Payback period Never Paid off

=A6

7+1

Internal Rate of

Return

=IRR(N62:

N71)

=A6

8+1

Profitability Index

@18%

=1+(L61/-

C61)

25

Profitability Index

@18%

=1+L66/-

C66

=A6

3+1

Discounted Cash

Flow =C63*C57 =D63*D57 =E63*E57 =F63*F57 =G63*G57 =H63*H57 =I63*I57 =J63*J57 =K63*K57 =L63*L57

=A6

4+1 Net Present Value

=SUM(C6

4:L64)

=A6

5+1 Cumulative =C64 =C66+D64 =D66+E64 =E66+F64 =F66+G64 =G66+H64 =H66+I64 =I66+J64 =J66+K64 =K66+L64

=A6

6+1

Discounted

Payback period Never Paid off

=A6

7+1

Internal Rate of

Return

=IRR(N62:

N71)

=A6

8+1

Profitability Index

@18%

=1+(L61/-

C61)

25

Profitability Index

@18%

=1+L66/-

C66

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.