Analysis and Construction of an all-Australian shares equity portfolio

VerifiedAdded on 2022/08/23

|16

|3411

|22

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: INVESTMENT POLICY

Investment Policy

Name of the Student:

Name of the University:

Author Note:

Investment Policy

Name of the Student:

Name of the University:

Author Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1INVESTMENT POLICY

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Risk and Return Profile of the client:.....................................................................................2

Portfolio monitoring and Feedback:.......................................................................................3

Assumptions in the portfolio construction:............................................................................4

Risk due to the assumptions:..................................................................................................4

Constituents of the Portfolio and their characteristics:..........................................................5

Portfolio Construction:...........................................................................................................6

Caveats in the rise in value which should be considered:......................................................7

Measurement of performance metrics:...................................................................................8

Portfolio Comparison with index:........................................................................................10

Recommendation:....................................................................................................................11

Conclusion:..............................................................................................................................11

References:...............................................................................................................................13

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Risk and Return Profile of the client:.....................................................................................2

Portfolio monitoring and Feedback:.......................................................................................3

Assumptions in the portfolio construction:............................................................................4

Risk due to the assumptions:..................................................................................................4

Constituents of the Portfolio and their characteristics:..........................................................5

Portfolio Construction:...........................................................................................................6

Caveats in the rise in value which should be considered:......................................................7

Measurement of performance metrics:...................................................................................8

Portfolio Comparison with index:........................................................................................10

Recommendation:....................................................................................................................11

Conclusion:..............................................................................................................................11

References:...............................................................................................................................13

2INVESTMENT POLICY

Introduction:

The following report contains the analysis and the construction of an all Australian

shares equity portfolio. The portfolio management process involves the consideration of the

risk and the return of the client for whom the portfolio is constructed. The report contains the

stocks which are being considered for the construction of the portfolio, along with the risk

associated with the stocks (Arena and Krause 2019).

In the first part of the report an analysis of the risk profile of the client is represented

based upon which the asset allocation of the stocks is being considered. It highlights the

tolerance of risk level of the client and the required return which is desired by the client. The

assumptions which are undertaken in the construction of the portfolio is presented in the first

part of the report.

In the second part of the report the construction of the portfolio which is suitable for

the client along with the measurement of performance of the client’s portfolio is presented.

The analysis of the portfolio is taken for a period of ten years beginning in the year 2010 and

till the year 2019. The performance of the portfolio is measured using various statistics and

compared with the individual stock returns and the index. A recommendation and conclusion

is provided at the end of the report which consists of the brief analysis of the report.

Discussion:

Risk and Return Profile of the client:

The risk profile of the client along with the return requirements from the portfolio is

highlighted in this point. The client has an average risk tolerance level which is highlighted

by the client in the meeting which was conducted with the client. The client has provided

Introduction:

The following report contains the analysis and the construction of an all Australian

shares equity portfolio. The portfolio management process involves the consideration of the

risk and the return of the client for whom the portfolio is constructed. The report contains the

stocks which are being considered for the construction of the portfolio, along with the risk

associated with the stocks (Arena and Krause 2019).

In the first part of the report an analysis of the risk profile of the client is represented

based upon which the asset allocation of the stocks is being considered. It highlights the

tolerance of risk level of the client and the required return which is desired by the client. The

assumptions which are undertaken in the construction of the portfolio is presented in the first

part of the report.

In the second part of the report the construction of the portfolio which is suitable for

the client along with the measurement of performance of the client’s portfolio is presented.

The analysis of the portfolio is taken for a period of ten years beginning in the year 2010 and

till the year 2019. The performance of the portfolio is measured using various statistics and

compared with the individual stock returns and the index. A recommendation and conclusion

is provided at the end of the report which consists of the brief analysis of the report.

Discussion:

Risk and Return Profile of the client:

The risk profile of the client along with the return requirements from the portfolio is

highlighted in this point. The client has an average risk tolerance level which is highlighted

by the client in the meeting which was conducted with the client. The client has provided

3INVESTMENT POLICY

$900000 to be invested in stocks which are trading in the Australian stock exchange. The

client wants the stocks to be invested in stocks which are established companies and each

stock belong to different industry. The client as is involved in the mining industry has advised

to choose a mining stock, along with a consumer discretionary stock. The third industry has

been left at the discretion of the portfolio manager. The client has stated to not having any

liquidity requirement in the short term and the long term. The returns from the portfolio will

be used to fund the retirement of the client which is after 35 years from the initiation of the

portfolio. The client has no other requirements and the client is expected to receive a lump-

sum amount from a deceased relative which would increase the clients risk tolerance level

(Dolan, Stevens and Zucker 2017).

The return requirement of the client is to fund the retirement of the client and no other

requirement by the client has been highlighted. However, the client is willing to invest in the

only equity asset class, as the client believes equity asset class over a long time horizon

provides abnormal returns. All other asset classes are to be avoided as per the client’s

requirement (Kinuthia 2018).

Thus the client has a risk tolerance level which is above average due to no liquidity

requirement and a long time horizon. The ability of the client to take a high level of risk is

due to the amount which is due to be received from the deceased relative. Thus the risk and

return profile of the client is above average with high returns (Minh and Tam 2017).

Portfolio monitoring and Feedback:

The portfolio of the client will be reviewed annually and rebalancing to the portfolio

will be done on a dynamic basis. The dividends which would be received would be reinvested

to purchase the stocks for the client portfolio. Thus any changes in the investment policy

statement if needed would be done on an annual basis.

$900000 to be invested in stocks which are trading in the Australian stock exchange. The

client wants the stocks to be invested in stocks which are established companies and each

stock belong to different industry. The client as is involved in the mining industry has advised

to choose a mining stock, along with a consumer discretionary stock. The third industry has

been left at the discretion of the portfolio manager. The client has stated to not having any

liquidity requirement in the short term and the long term. The returns from the portfolio will

be used to fund the retirement of the client which is after 35 years from the initiation of the

portfolio. The client has no other requirements and the client is expected to receive a lump-

sum amount from a deceased relative which would increase the clients risk tolerance level

(Dolan, Stevens and Zucker 2017).

The return requirement of the client is to fund the retirement of the client and no other

requirement by the client has been highlighted. However, the client is willing to invest in the

only equity asset class, as the client believes equity asset class over a long time horizon

provides abnormal returns. All other asset classes are to be avoided as per the client’s

requirement (Kinuthia 2018).

Thus the client has a risk tolerance level which is above average due to no liquidity

requirement and a long time horizon. The ability of the client to take a high level of risk is

due to the amount which is due to be received from the deceased relative. Thus the risk and

return profile of the client is above average with high returns (Minh and Tam 2017).

Portfolio monitoring and Feedback:

The portfolio of the client will be reviewed annually and rebalancing to the portfolio

will be done on a dynamic basis. The dividends which would be received would be reinvested

to purchase the stocks for the client portfolio. Thus any changes in the investment policy

statement if needed would be done on an annual basis.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4INVESTMENT POLICY

Assumptions in the portfolio construction:

The following assumptions will be undertaken when constructing the portfolio of the

client which is highlighted in the following points.

The portfolio will be equally weighted initially and the change in weights due to the

change in the stock price will not be altered.

The stocks from the Mining industry, consumer discretionary industry and the

banking industry will be taken in the construction of the portfolio.

All dividend which would be received will be reinvested in the stocks of the company

at the end of the year.

The selection of the stocks will be made on a strategic basis and no tactical asset

allocation will be made to the portfolio.

The stocks from the Australian stock exchange will be taken for the construction of

the portfolio and all other asset class will be avoided.

The portfolio will be measured using the arithmetic mean, standard deviation and the

geometric mean of the stocks and the portfolio.

The covariance of the stock and the portfolio will be measured along with the

correlation of the stocks.

Risk due to the assumptions:

The following risk which is highlighted in the following points will be present when

undertaking the following assumptions,

The assumption of equally weighted portfolio is prevalent only at the initiation of the

portfolio since the weights of the stocks will change with the change in the stock

price.

Assumptions in the portfolio construction:

The following assumptions will be undertaken when constructing the portfolio of the

client which is highlighted in the following points.

The portfolio will be equally weighted initially and the change in weights due to the

change in the stock price will not be altered.

The stocks from the Mining industry, consumer discretionary industry and the

banking industry will be taken in the construction of the portfolio.

All dividend which would be received will be reinvested in the stocks of the company

at the end of the year.

The selection of the stocks will be made on a strategic basis and no tactical asset

allocation will be made to the portfolio.

The stocks from the Australian stock exchange will be taken for the construction of

the portfolio and all other asset class will be avoided.

The portfolio will be measured using the arithmetic mean, standard deviation and the

geometric mean of the stocks and the portfolio.

The covariance of the stock and the portfolio will be measured along with the

correlation of the stocks.

Risk due to the assumptions:

The following risk which is highlighted in the following points will be present when

undertaking the following assumptions,

The assumption of equally weighted portfolio is prevalent only at the initiation of the

portfolio since the weights of the stocks will change with the change in the stock

price.

5INVESTMENT POLICY

If the portfolio is left to be dynamically rebalanced it will lead to concentration of

stocks in the portfolio, whose price will increase exponentially.

The constraint of using only equity leads to the foregoing of the benefits of

diversification, since equity as an asset class along with other asset class provides

benefits of diversification due to low correlation.

The constraint of not using tactical asset allocation leads to a limitation to the

portfolio manager who cannot use short term strategies to benefit from the economic

conditions.

Since the stock are only from the Australian stock exchange the benefits of

incorporating an international stock in the portfolio is foregone.

Constituents of the Portfolio and their characteristics:

The portfolio is constructed by taking stocks from the industry highlighted in the

above points. The stock from the mining industry is BHP Billiton which is a mining company

located in Australia and is involved in providing mining infrastructure in Australian and

Africa. The company is also involved in exploration of probable mining sites which consist

of valuable minerals. It also devises strategies and methods for the efficient mining at

existing locations in Australia and other countries (Nathanson, Craig, Geoghegan and Lee

2018).

The second company is taken from the consumer discretionary industry and the stock

of the company Woolworths is taken in the portfolio. The company owns a chain of

supermarkets across Australia and New Zealand and is the second largest company in

Australia (Davies, Kat and Lu 2016).

The third company which is taken from the financial sector and from the banking

industry is the stock of commonwealth bank of Australia. This stock is one of the leading

If the portfolio is left to be dynamically rebalanced it will lead to concentration of

stocks in the portfolio, whose price will increase exponentially.

The constraint of using only equity leads to the foregoing of the benefits of

diversification, since equity as an asset class along with other asset class provides

benefits of diversification due to low correlation.

The constraint of not using tactical asset allocation leads to a limitation to the

portfolio manager who cannot use short term strategies to benefit from the economic

conditions.

Since the stock are only from the Australian stock exchange the benefits of

incorporating an international stock in the portfolio is foregone.

Constituents of the Portfolio and their characteristics:

The portfolio is constructed by taking stocks from the industry highlighted in the

above points. The stock from the mining industry is BHP Billiton which is a mining company

located in Australia and is involved in providing mining infrastructure in Australian and

Africa. The company is also involved in exploration of probable mining sites which consist

of valuable minerals. It also devises strategies and methods for the efficient mining at

existing locations in Australia and other countries (Nathanson, Craig, Geoghegan and Lee

2018).

The second company is taken from the consumer discretionary industry and the stock

of the company Woolworths is taken in the portfolio. The company owns a chain of

supermarkets across Australia and New Zealand and is the second largest company in

Australia (Davies, Kat and Lu 2016).

The third company which is taken from the financial sector and from the banking

industry is the stock of commonwealth bank of Australia. This stock is one of the leading

6INVESTMENT POLICY

banks of Australia which has its operations all over Australia, New Zealand and the United

states (Saborido, Ruiz, Bermúdez, Vercher and Luque 2016).

Portfolio Construction:

The construction of the portfolio takes place in the beginning of the year 2010 and the

stocks of the three companies is purchased and a portfolio is constructed taking equal weights

in the stocks.

banks of Australia which has its operations all over Australia, New Zealand and the United

states (Saborido, Ruiz, Bermúdez, Vercher and Luque 2016).

Portfolio Construction:

The construction of the portfolio takes place in the beginning of the year 2010 and the

stocks of the three companies is purchased and a portfolio is constructed taking equal weights

in the stocks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INVESTMENT POLICY

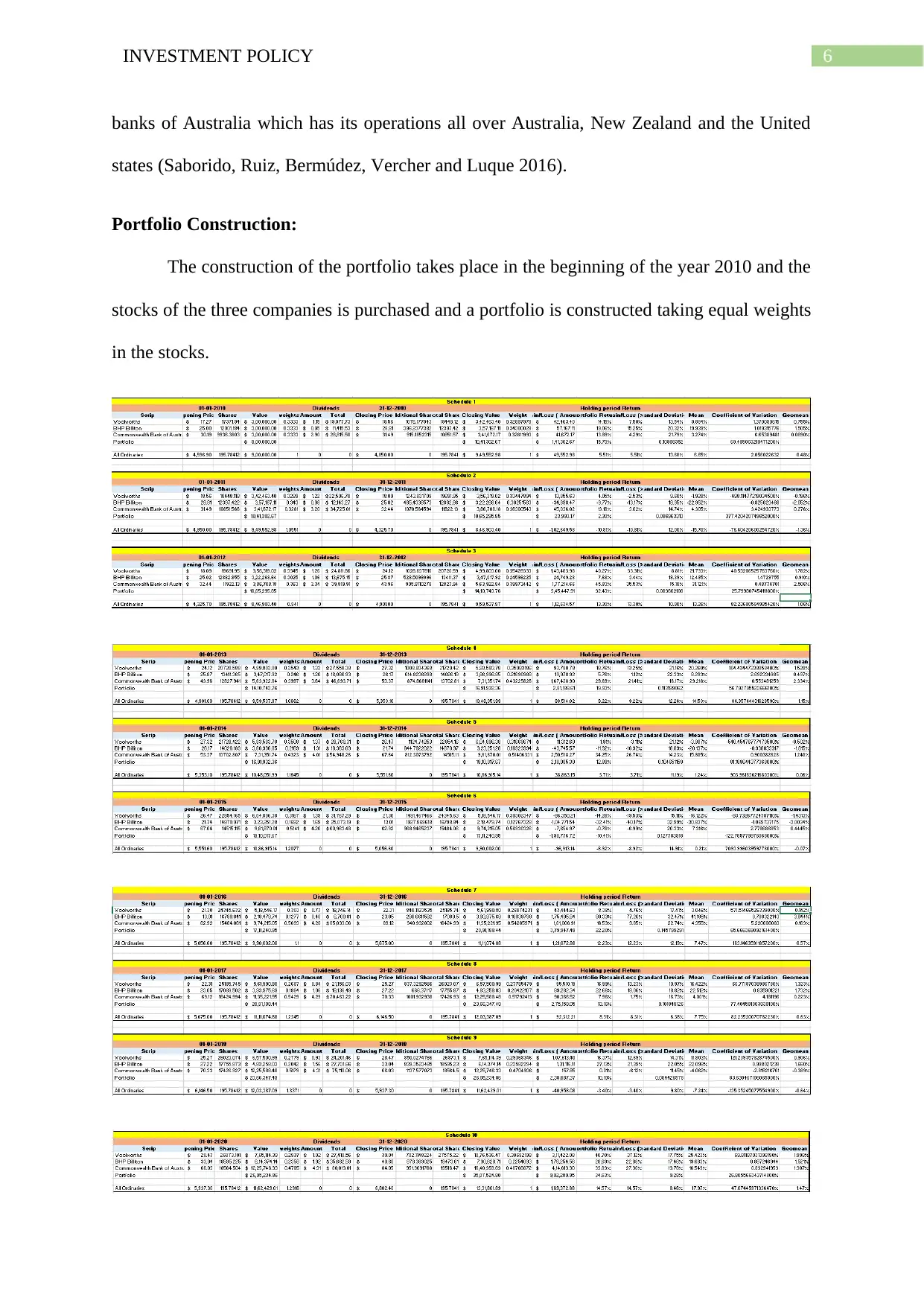

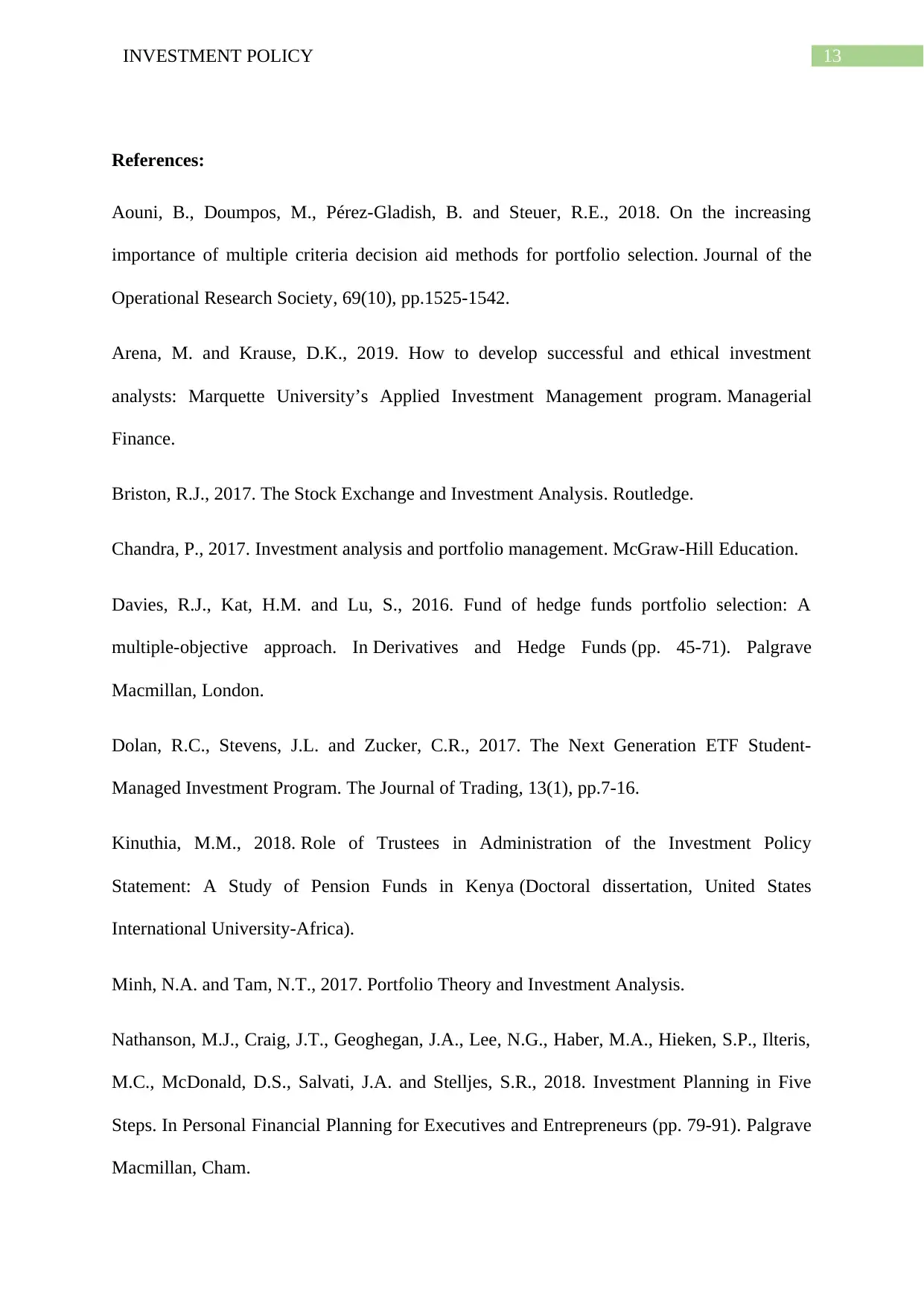

Figure 1: Schedule of Portfolio over Investment Horizon

Source: By the Author

At the portfolio initiation date on 01/01/2010, the stocks which were purchased using

the opening price of each stock and the initial amount which is invested in each stock which

is of $300000. Thus the value of the portfolio at the initiation is $900000, while at the end of

the year 2010 the value of the portfolio is $1041302. The value of the same amount when

invested in the index at the end of the year is $949552 (Pedersen and Peskir 2017).

As per schedule 2, the initiation value of the portfolio is the stock price at the end of

the year 2010, while the closing price is taken for the year 2011. The initial value of the

portfolio is $1041302, while the closing value of the portfolio is $1065295. The index value

has fallen and the value of the amount which is invested in the index is $846903.

As per schedule 3, the initial value of the portfolio is $1065295, while the closing

value of the portfolio is $1410743. The index also have increased and the value of the amount

invested in the index is $959537.

As per schedule 4, the value of the index have increased to $1048051, while the

portfolio value have increased to $1691932. Thus the value of the portfolio at the end of 10

years is $3507524, while that of index is $1331801.89. Thus the portfolio has increased by

almost 400% in the past 10 years while the amount which was invested in the index have

increased by around 50% (Aouni, Doumpos, Pérez-Gladish and Steuer 2018).

Caveats in the rise in value which should be considered:

The rise in value of the stock over the 10 years period is due to the rise in the holding

of the stock due to dividend reinvestment assumption. This is not done in the value of the

index, which represent the holding which had been present at the initiation of the portfolio.

Figure 1: Schedule of Portfolio over Investment Horizon

Source: By the Author

At the portfolio initiation date on 01/01/2010, the stocks which were purchased using

the opening price of each stock and the initial amount which is invested in each stock which

is of $300000. Thus the value of the portfolio at the initiation is $900000, while at the end of

the year 2010 the value of the portfolio is $1041302. The value of the same amount when

invested in the index at the end of the year is $949552 (Pedersen and Peskir 2017).

As per schedule 2, the initiation value of the portfolio is the stock price at the end of

the year 2010, while the closing price is taken for the year 2011. The initial value of the

portfolio is $1041302, while the closing value of the portfolio is $1065295. The index value

has fallen and the value of the amount which is invested in the index is $846903.

As per schedule 3, the initial value of the portfolio is $1065295, while the closing

value of the portfolio is $1410743. The index also have increased and the value of the amount

invested in the index is $959537.

As per schedule 4, the value of the index have increased to $1048051, while the

portfolio value have increased to $1691932. Thus the value of the portfolio at the end of 10

years is $3507524, while that of index is $1331801.89. Thus the portfolio has increased by

almost 400% in the past 10 years while the amount which was invested in the index have

increased by around 50% (Aouni, Doumpos, Pérez-Gladish and Steuer 2018).

Caveats in the rise in value which should be considered:

The rise in value of the stock over the 10 years period is due to the rise in the holding

of the stock due to dividend reinvestment assumption. This is not done in the value of the

index, which represent the holding which had been present at the initiation of the portfolio.

8INVESTMENT POLICY

The holdings of the stock had increased due to the reinvestment of dividend which led to the

rise in the value of the portfolio to such an extent (Chandra, 2017).

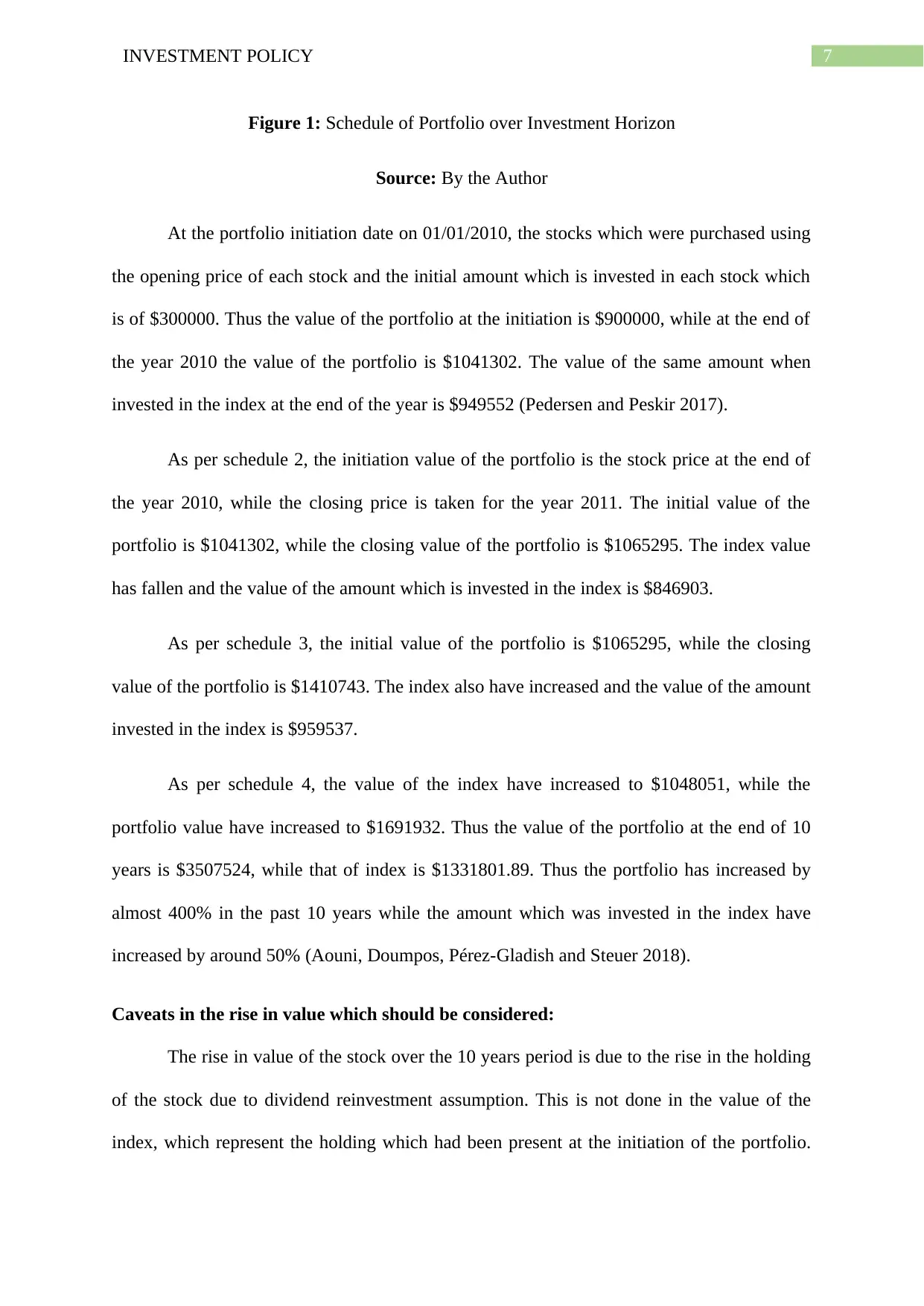

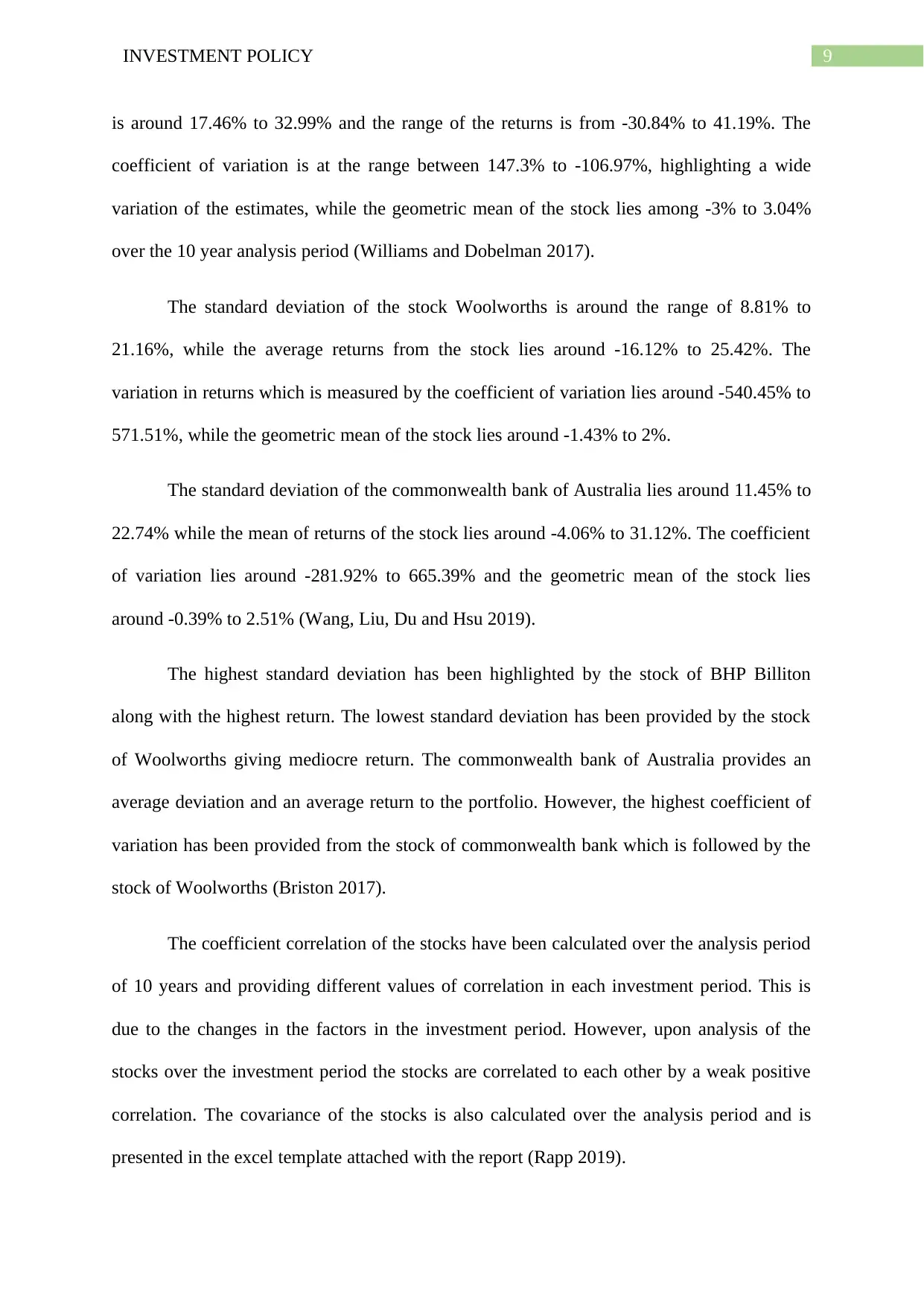

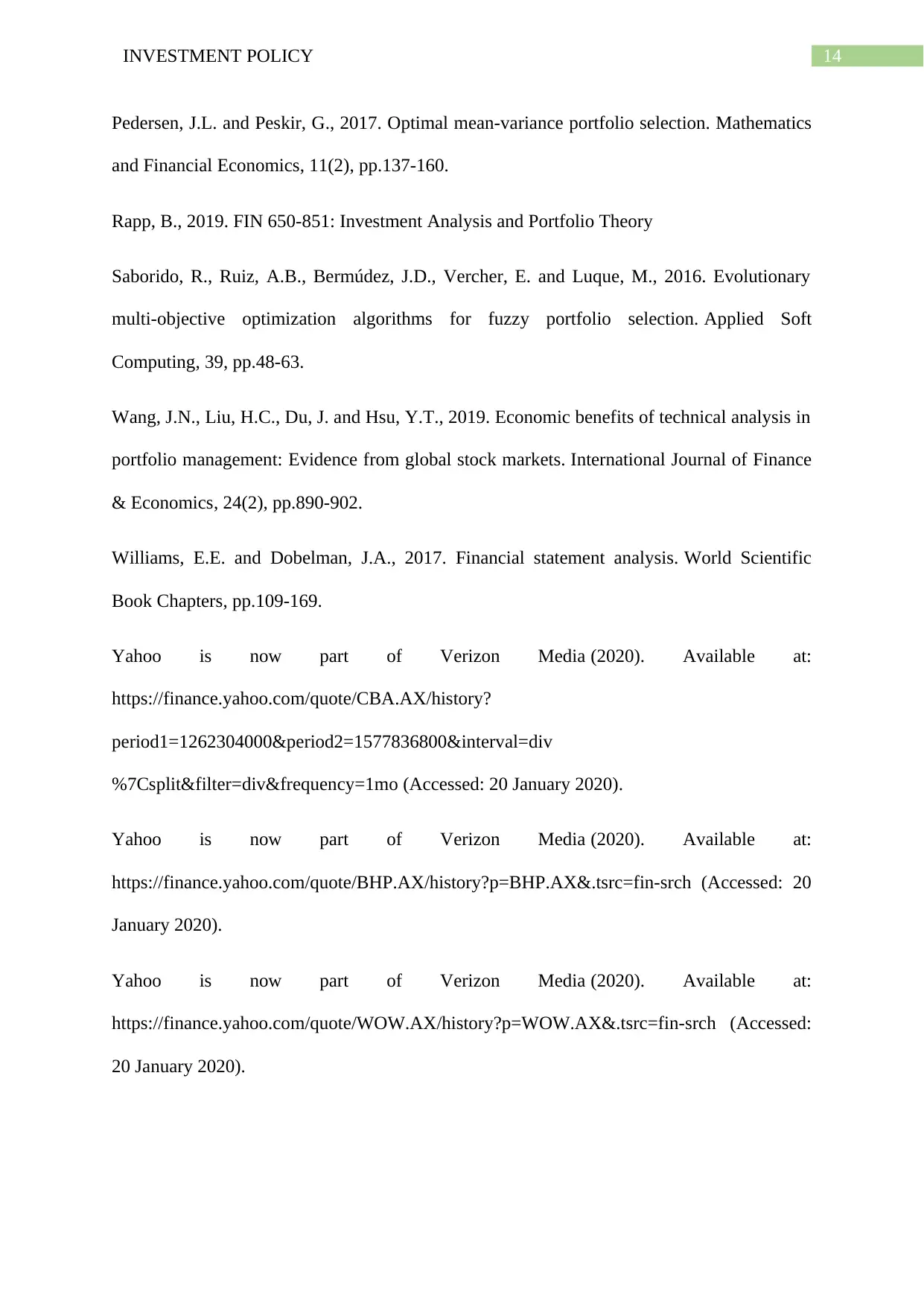

Measurement of performance metrics:

The performance of the stocks on an individual basis is calculated in the following

table with the calculation of standard deviation, mean, coefficient of variation and the

geometric mean of the stocks. The following figures highlight the calculation,

Figure 2: Stock Performance Return

Source: By the Author

The standard deviation for the company BHP Billiton has been the highest in the year

6 at 32.99% and the mean return in that year for the stock excluding dividend reinvestment is

-30.84%. The lowest standard deviation for the company is in the year 10 with at 17.46%,

while the mean of the returns is at 19.68%. The range of the standard deviation over the years

The holdings of the stock had increased due to the reinvestment of dividend which led to the

rise in the value of the portfolio to such an extent (Chandra, 2017).

Measurement of performance metrics:

The performance of the stocks on an individual basis is calculated in the following

table with the calculation of standard deviation, mean, coefficient of variation and the

geometric mean of the stocks. The following figures highlight the calculation,

Figure 2: Stock Performance Return

Source: By the Author

The standard deviation for the company BHP Billiton has been the highest in the year

6 at 32.99% and the mean return in that year for the stock excluding dividend reinvestment is

-30.84%. The lowest standard deviation for the company is in the year 10 with at 17.46%,

while the mean of the returns is at 19.68%. The range of the standard deviation over the years

9INVESTMENT POLICY

is around 17.46% to 32.99% and the range of the returns is from -30.84% to 41.19%. The

coefficient of variation is at the range between 147.3% to -106.97%, highlighting a wide

variation of the estimates, while the geometric mean of the stock lies among -3% to 3.04%

over the 10 year analysis period (Williams and Dobelman 2017).

The standard deviation of the stock Woolworths is around the range of 8.81% to

21.16%, while the average returns from the stock lies around -16.12% to 25.42%. The

variation in returns which is measured by the coefficient of variation lies around -540.45% to

571.51%, while the geometric mean of the stock lies around -1.43% to 2%.

The standard deviation of the commonwealth bank of Australia lies around 11.45% to

22.74% while the mean of returns of the stock lies around -4.06% to 31.12%. The coefficient

of variation lies around -281.92% to 665.39% and the geometric mean of the stock lies

around -0.39% to 2.51% (Wang, Liu, Du and Hsu 2019).

The highest standard deviation has been highlighted by the stock of BHP Billiton

along with the highest return. The lowest standard deviation has been provided by the stock

of Woolworths giving mediocre return. The commonwealth bank of Australia provides an

average deviation and an average return to the portfolio. However, the highest coefficient of

variation has been provided from the stock of commonwealth bank which is followed by the

stock of Woolworths (Briston 2017).

The coefficient correlation of the stocks have been calculated over the analysis period

of 10 years and providing different values of correlation in each investment period. This is

due to the changes in the factors in the investment period. However, upon analysis of the

stocks over the investment period the stocks are correlated to each other by a weak positive

correlation. The covariance of the stocks is also calculated over the analysis period and is

presented in the excel template attached with the report (Rapp 2019).

is around 17.46% to 32.99% and the range of the returns is from -30.84% to 41.19%. The

coefficient of variation is at the range between 147.3% to -106.97%, highlighting a wide

variation of the estimates, while the geometric mean of the stock lies among -3% to 3.04%

over the 10 year analysis period (Williams and Dobelman 2017).

The standard deviation of the stock Woolworths is around the range of 8.81% to

21.16%, while the average returns from the stock lies around -16.12% to 25.42%. The

variation in returns which is measured by the coefficient of variation lies around -540.45% to

571.51%, while the geometric mean of the stock lies around -1.43% to 2%.

The standard deviation of the commonwealth bank of Australia lies around 11.45% to

22.74% while the mean of returns of the stock lies around -4.06% to 31.12%. The coefficient

of variation lies around -281.92% to 665.39% and the geometric mean of the stock lies

around -0.39% to 2.51% (Wang, Liu, Du and Hsu 2019).

The highest standard deviation has been highlighted by the stock of BHP Billiton

along with the highest return. The lowest standard deviation has been provided by the stock

of Woolworths giving mediocre return. The commonwealth bank of Australia provides an

average deviation and an average return to the portfolio. However, the highest coefficient of

variation has been provided from the stock of commonwealth bank which is followed by the

stock of Woolworths (Briston 2017).

The coefficient correlation of the stocks have been calculated over the analysis period

of 10 years and providing different values of correlation in each investment period. This is

due to the changes in the factors in the investment period. However, upon analysis of the

stocks over the investment period the stocks are correlated to each other by a weak positive

correlation. The covariance of the stocks is also calculated over the analysis period and is

presented in the excel template attached with the report (Rapp 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10INVESTMENT POLICY

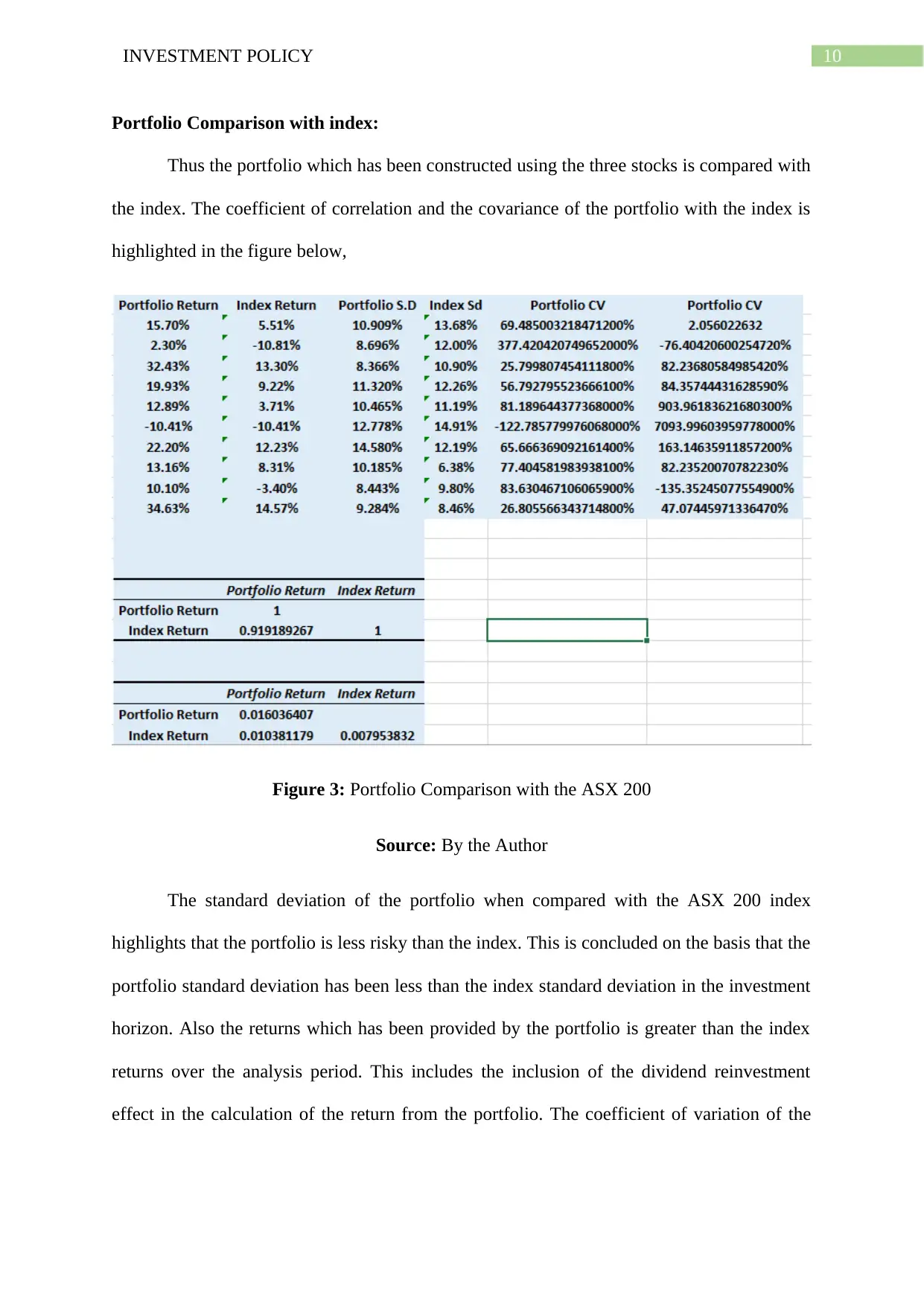

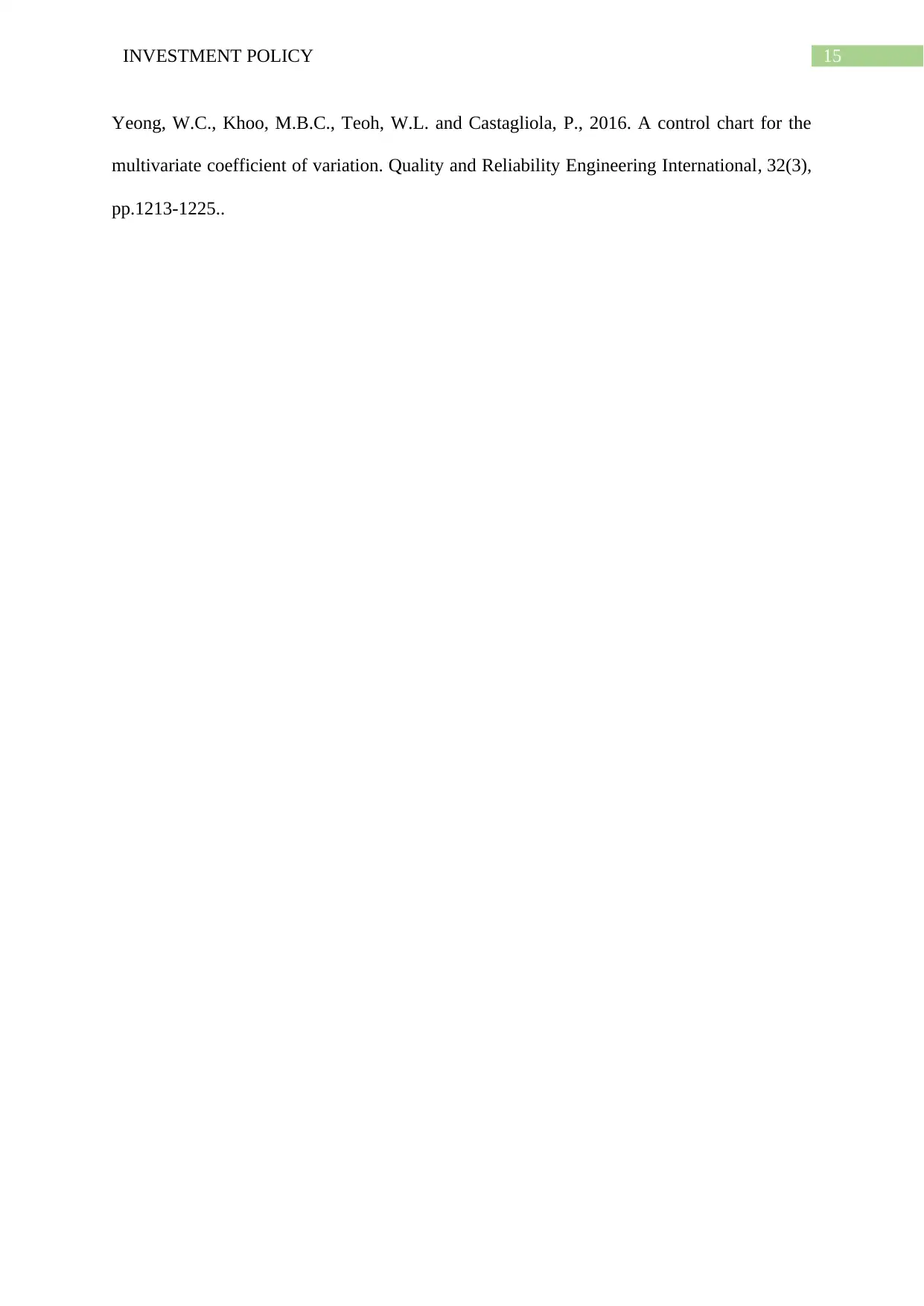

Portfolio Comparison with index:

Thus the portfolio which has been constructed using the three stocks is compared with

the index. The coefficient of correlation and the covariance of the portfolio with the index is

highlighted in the figure below,

Figure 3: Portfolio Comparison with the ASX 200

Source: By the Author

The standard deviation of the portfolio when compared with the ASX 200 index

highlights that the portfolio is less risky than the index. This is concluded on the basis that the

portfolio standard deviation has been less than the index standard deviation in the investment

horizon. Also the returns which has been provided by the portfolio is greater than the index

returns over the analysis period. This includes the inclusion of the dividend reinvestment

effect in the calculation of the return from the portfolio. The coefficient of variation of the

Portfolio Comparison with index:

Thus the portfolio which has been constructed using the three stocks is compared with

the index. The coefficient of correlation and the covariance of the portfolio with the index is

highlighted in the figure below,

Figure 3: Portfolio Comparison with the ASX 200

Source: By the Author

The standard deviation of the portfolio when compared with the ASX 200 index

highlights that the portfolio is less risky than the index. This is concluded on the basis that the

portfolio standard deviation has been less than the index standard deviation in the investment

horizon. Also the returns which has been provided by the portfolio is greater than the index

returns over the analysis period. This includes the inclusion of the dividend reinvestment

effect in the calculation of the return from the portfolio. The coefficient of variation of the

11INVESTMENT POLICY

portfolio is greater than the index coefficient of variation which is highlighted in the figure

above.

The correlation of the portfolio with the index is close to 0, thus highlighting that the

portfolio is less affected by the changes in the index over the 10 year analysis period (Yeong,

Khoo, Teoh and Castagliola 2016).

Recommendation:

The following recommendation would be useful in managing the portfolio in a more

efficient manner,

The portfolio weights have not been interfered with and if the portfolio manager could

alter the weight of the portfolio, it would have led to further reduction in risk and

maximization of returns.

The portfolio should be reviewed quarterly, such that any short term opportunities

could had been exploited by the portfolio manager.

The inclusion of other asset classes should be taken in the portfolio to provide the

benefits of diversification to the portfolio.

The measurement metrics of the portfolio should be increased to also measure the

portfolio performance using Sharpe ratio, tracking error, Jensen alpha ratio and other

metrics.

Conclusion:

Thus in this report it is concluded that the selection of stocks according to the clients

risk and return profile has been efficient and provided the client with higher returns compared

to the market. The risk of the stock BHP Billiton is high which should be reduced by the

portfolio manager, and other asset classes should be included in the portfolio to reduce the

portfolio is greater than the index coefficient of variation which is highlighted in the figure

above.

The correlation of the portfolio with the index is close to 0, thus highlighting that the

portfolio is less affected by the changes in the index over the 10 year analysis period (Yeong,

Khoo, Teoh and Castagliola 2016).

Recommendation:

The following recommendation would be useful in managing the portfolio in a more

efficient manner,

The portfolio weights have not been interfered with and if the portfolio manager could

alter the weight of the portfolio, it would have led to further reduction in risk and

maximization of returns.

The portfolio should be reviewed quarterly, such that any short term opportunities

could had been exploited by the portfolio manager.

The inclusion of other asset classes should be taken in the portfolio to provide the

benefits of diversification to the portfolio.

The measurement metrics of the portfolio should be increased to also measure the

portfolio performance using Sharpe ratio, tracking error, Jensen alpha ratio and other

metrics.

Conclusion:

Thus in this report it is concluded that the selection of stocks according to the clients

risk and return profile has been efficient and provided the client with higher returns compared

to the market. The risk of the stock BHP Billiton is high which should be reduced by the

portfolio manager, and other asset classes should be included in the portfolio to reduce the

12INVESTMENT POLICY

risk of the portfolio. Although the risk of the portfolio is less than the index a further

reduction is possible by using other asset class such as bond or alternate investment. The

shareholding of the investor have increased over the years and the portfolio provided positive

returns even during when the markets were falling down.

Thus the performance of the portfolio has been good when compared to the index and

the risk of the portfolio is less than the stocks when compared on a standalone basis.

risk of the portfolio. Although the risk of the portfolio is less than the index a further

reduction is possible by using other asset class such as bond or alternate investment. The

shareholding of the investor have increased over the years and the portfolio provided positive

returns even during when the markets were falling down.

Thus the performance of the portfolio has been good when compared to the index and

the risk of the portfolio is less than the stocks when compared on a standalone basis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13INVESTMENT POLICY

References:

Aouni, B., Doumpos, M., Pérez-Gladish, B. and Steuer, R.E., 2018. On the increasing

importance of multiple criteria decision aid methods for portfolio selection. Journal of the

Operational Research Society, 69(10), pp.1525-1542.

Arena, M. and Krause, D.K., 2019. How to develop successful and ethical investment

analysts: Marquette University’s Applied Investment Management program. Managerial

Finance.

Briston, R.J., 2017. The Stock Exchange and Investment Analysis. Routledge.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Davies, R.J., Kat, H.M. and Lu, S., 2016. Fund of hedge funds portfolio selection: A

multiple-objective approach. In Derivatives and Hedge Funds (pp. 45-71). Palgrave

Macmillan, London.

Dolan, R.C., Stevens, J.L. and Zucker, C.R., 2017. The Next Generation ETF Student-

Managed Investment Program. The Journal of Trading, 13(1), pp.7-16.

Kinuthia, M.M., 2018. Role of Trustees in Administration of the Investment Policy

Statement: A Study of Pension Funds in Kenya (Doctoral dissertation, United States

International University-Africa).

Minh, N.A. and Tam, N.T., 2017. Portfolio Theory and Investment Analysis.

Nathanson, M.J., Craig, J.T., Geoghegan, J.A., Lee, N.G., Haber, M.A., Hieken, S.P., Ilteris,

M.C., McDonald, D.S., Salvati, J.A. and Stelljes, S.R., 2018. Investment Planning in Five

Steps. In Personal Financial Planning for Executives and Entrepreneurs (pp. 79-91). Palgrave

Macmillan, Cham.

References:

Aouni, B., Doumpos, M., Pérez-Gladish, B. and Steuer, R.E., 2018. On the increasing

importance of multiple criteria decision aid methods for portfolio selection. Journal of the

Operational Research Society, 69(10), pp.1525-1542.

Arena, M. and Krause, D.K., 2019. How to develop successful and ethical investment

analysts: Marquette University’s Applied Investment Management program. Managerial

Finance.

Briston, R.J., 2017. The Stock Exchange and Investment Analysis. Routledge.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Davies, R.J., Kat, H.M. and Lu, S., 2016. Fund of hedge funds portfolio selection: A

multiple-objective approach. In Derivatives and Hedge Funds (pp. 45-71). Palgrave

Macmillan, London.

Dolan, R.C., Stevens, J.L. and Zucker, C.R., 2017. The Next Generation ETF Student-

Managed Investment Program. The Journal of Trading, 13(1), pp.7-16.

Kinuthia, M.M., 2018. Role of Trustees in Administration of the Investment Policy

Statement: A Study of Pension Funds in Kenya (Doctoral dissertation, United States

International University-Africa).

Minh, N.A. and Tam, N.T., 2017. Portfolio Theory and Investment Analysis.

Nathanson, M.J., Craig, J.T., Geoghegan, J.A., Lee, N.G., Haber, M.A., Hieken, S.P., Ilteris,

M.C., McDonald, D.S., Salvati, J.A. and Stelljes, S.R., 2018. Investment Planning in Five

Steps. In Personal Financial Planning for Executives and Entrepreneurs (pp. 79-91). Palgrave

Macmillan, Cham.

14INVESTMENT POLICY

Pedersen, J.L. and Peskir, G., 2017. Optimal mean-variance portfolio selection. Mathematics

and Financial Economics, 11(2), pp.137-160.

Rapp, B., 2019. FIN 650-851: Investment Analysis and Portfolio Theory

Saborido, R., Ruiz, A.B., Bermúdez, J.D., Vercher, E. and Luque, M., 2016. Evolutionary

multi-objective optimization algorithms for fuzzy portfolio selection. Applied Soft

Computing, 39, pp.48-63.

Wang, J.N., Liu, H.C., Du, J. and Hsu, Y.T., 2019. Economic benefits of technical analysis in

portfolio management: Evidence from global stock markets. International Journal of Finance

& Economics, 24(2), pp.890-902.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific

Book Chapters, pp.109-169.

Yahoo is now part of Verizon Media (2020). Available at:

https://finance.yahoo.com/quote/CBA.AX/history?

period1=1262304000&period2=1577836800&interval=div

%7Csplit&filter=div&frequency=1mo (Accessed: 20 January 2020).

Yahoo is now part of Verizon Media (2020). Available at:

https://finance.yahoo.com/quote/BHP.AX/history?p=BHP.AX&.tsrc=fin-srch (Accessed: 20

January 2020).

Yahoo is now part of Verizon Media (2020). Available at:

https://finance.yahoo.com/quote/WOW.AX/history?p=WOW.AX&.tsrc=fin-srch (Accessed:

20 January 2020).

Pedersen, J.L. and Peskir, G., 2017. Optimal mean-variance portfolio selection. Mathematics

and Financial Economics, 11(2), pp.137-160.

Rapp, B., 2019. FIN 650-851: Investment Analysis and Portfolio Theory

Saborido, R., Ruiz, A.B., Bermúdez, J.D., Vercher, E. and Luque, M., 2016. Evolutionary

multi-objective optimization algorithms for fuzzy portfolio selection. Applied Soft

Computing, 39, pp.48-63.

Wang, J.N., Liu, H.C., Du, J. and Hsu, Y.T., 2019. Economic benefits of technical analysis in

portfolio management: Evidence from global stock markets. International Journal of Finance

& Economics, 24(2), pp.890-902.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific

Book Chapters, pp.109-169.

Yahoo is now part of Verizon Media (2020). Available at:

https://finance.yahoo.com/quote/CBA.AX/history?

period1=1262304000&period2=1577836800&interval=div

%7Csplit&filter=div&frequency=1mo (Accessed: 20 January 2020).

Yahoo is now part of Verizon Media (2020). Available at:

https://finance.yahoo.com/quote/BHP.AX/history?p=BHP.AX&.tsrc=fin-srch (Accessed: 20

January 2020).

Yahoo is now part of Verizon Media (2020). Available at:

https://finance.yahoo.com/quote/WOW.AX/history?p=WOW.AX&.tsrc=fin-srch (Accessed:

20 January 2020).

15INVESTMENT POLICY

Yeong, W.C., Khoo, M.B.C., Teoh, W.L. and Castagliola, P., 2016. A control chart for the

multivariate coefficient of variation. Quality and Reliability Engineering International, 32(3),

pp.1213-1225..

Yeong, W.C., Khoo, M.B.C., Teoh, W.L. and Castagliola, P., 2016. A control chart for the

multivariate coefficient of variation. Quality and Reliability Engineering International, 32(3),

pp.1213-1225..

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.