Investment Project Analysis: Dividend and Free Cash Flow Models

VerifiedAdded on 2019/11/14

|11

|1814

|162

Project

AI Summary

This investment project analyzes the financial valuation of a company using two primary models: the Dividend Discount Model (DDM) and the Free Cash Flow to Equity (FCFE) model. The project begins by explaining the theoretical underpinnings of the DDM, including historical and forecasted growth rates, and calculates the intrinsic value of the stock. It then conducts a sensitivity analysis to assess how changes in key variables impact the valuation. The FCFE model is then applied, following a similar structure to the DDM, including historical and forecasted growth rates, intrinsic value calculation, and sensitivity analysis. The project compares the intrinsic values derived from both models with the current market price to determine if the stock is overvalued or undervalued, providing recommendations based on the analysis. The analysis includes the calculations for the Sembcorp company, and uses the provided data to demonstrate the application of the models.

Running head: INVESTMENT PROJECT

Investment Project

Name of the Student:

Name of the University:

Author’s Note:

Investment Project

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INVESTMENT PROJECT

Table of Contents

Question 2..................................................................................................................................2

2.1 Dividend Valuation Model (DDM)......................................................................................2

2.1.1 Historical Growth..............................................................................................................2

2.1.2 Forecasted Growth............................................................................................................4

2.1.3 Intrinsic Value...................................................................................................................4

2.1.4 Sensitivity Analysis (Constant Growth)............................................................................5

2.2 Free Cash Flow to Equity Model (FCFE)............................................................................6

2.2.1 Historical growth rate for FCFE.......................................................................................6

2.2.2 Forecasted growth rate for FCFE......................................................................................7

2.2.3 Intrinsic Value...................................................................................................................9

2.2.4 Sensitivity Analysis for FCFE........................................................................................10

Reference and Bibliography:....................................................................................................11

Table of Contents

Question 2..................................................................................................................................2

2.1 Dividend Valuation Model (DDM)......................................................................................2

2.1.1 Historical Growth..............................................................................................................2

2.1.2 Forecasted Growth............................................................................................................4

2.1.3 Intrinsic Value...................................................................................................................4

2.1.4 Sensitivity Analysis (Constant Growth)............................................................................5

2.2 Free Cash Flow to Equity Model (FCFE)............................................................................6

2.2.1 Historical growth rate for FCFE.......................................................................................6

2.2.2 Forecasted growth rate for FCFE......................................................................................7

2.2.3 Intrinsic Value...................................................................................................................9

2.2.4 Sensitivity Analysis for FCFE........................................................................................10

Reference and Bibliography:....................................................................................................11

2INVESTMENT PROJECT

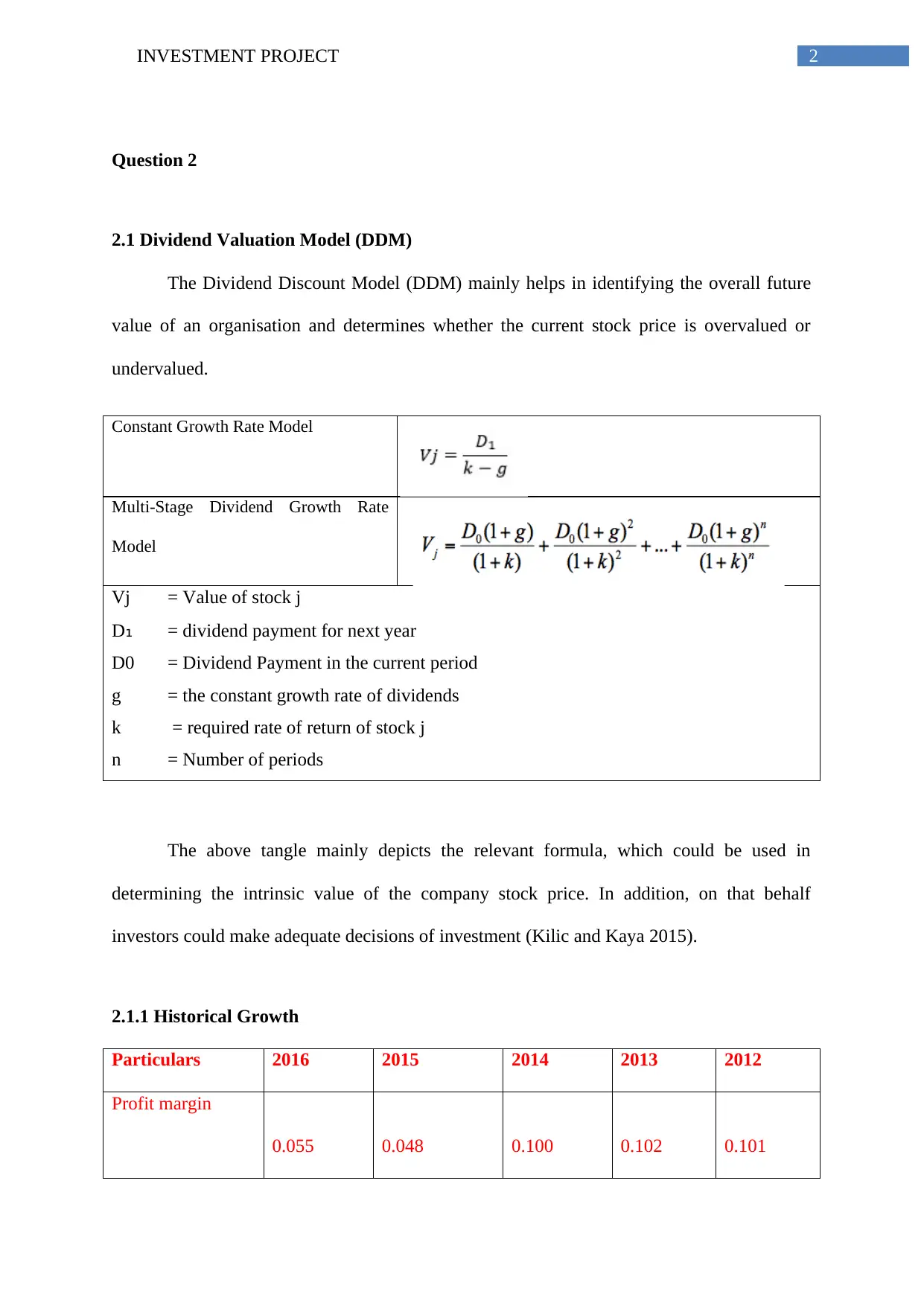

Question 2

2.1 Dividend Valuation Model (DDM)

The Dividend Discount Model (DDM) mainly helps in identifying the overall future

value of an organisation and determines whether the current stock price is overvalued or

undervalued.

Constant Growth Rate Model

Multi-Stage Dividend Growth Rate

Model

Vj = Value of stock j

D₁ = dividend payment for next year

D0 = Dividend Payment in the current period

g = the constant growth rate of dividends

k = required rate of return of stock j

n = Number of periods

The above tangle mainly depicts the relevant formula, which could be used in

determining the intrinsic value of the company stock price. In addition, on that behalf

investors could make adequate decisions of investment (Kilic and Kaya 2015).

2.1.1 Historical Growth

Particulars 2016 2015 2014 2013 2012

Profit margin

0.055 0.048 0.100 0.102 0.101

Question 2

2.1 Dividend Valuation Model (DDM)

The Dividend Discount Model (DDM) mainly helps in identifying the overall future

value of an organisation and determines whether the current stock price is overvalued or

undervalued.

Constant Growth Rate Model

Multi-Stage Dividend Growth Rate

Model

Vj = Value of stock j

D₁ = dividend payment for next year

D0 = Dividend Payment in the current period

g = the constant growth rate of dividends

k = required rate of return of stock j

n = Number of periods

The above tangle mainly depicts the relevant formula, which could be used in

determining the intrinsic value of the company stock price. In addition, on that behalf

investors could make adequate decisions of investment (Kilic and Kaya 2015).

2.1.1 Historical Growth

Particulars 2016 2015 2014 2013 2012

Profit margin

0.055 0.048 0.100 0.102 0.101

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INVESTMENT PROJECT

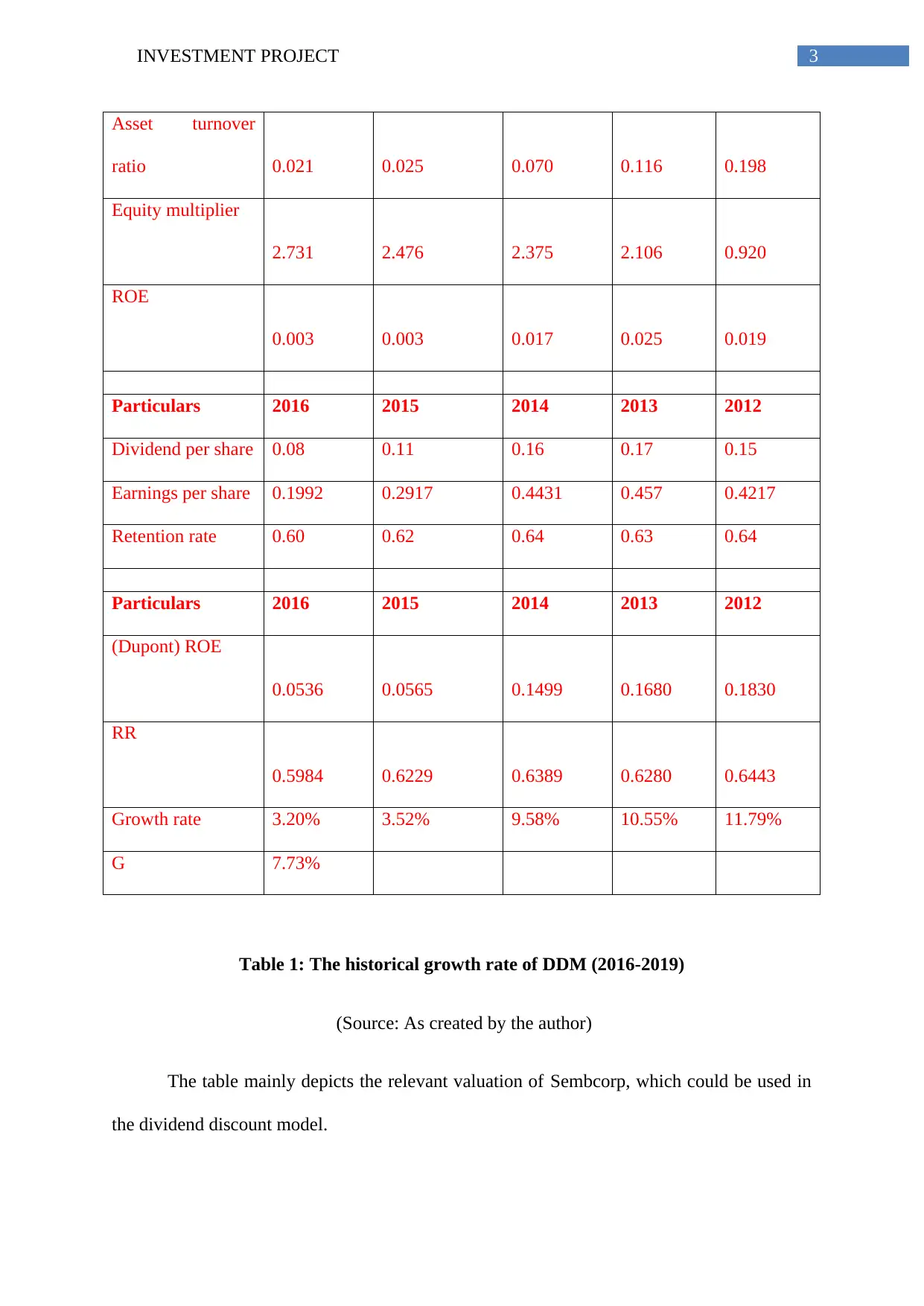

Asset turnover

ratio 0.021 0.025 0.070 0.116 0.198

Equity multiplier

2.731 2.476 2.375 2.106 0.920

ROE

0.003 0.003 0.017 0.025 0.019

Particulars 2016 2015 2014 2013 2012

Dividend per share 0.08 0.11 0.16 0.17 0.15

Earnings per share 0.1992 0.2917 0.4431 0.457 0.4217

Retention rate 0.60 0.62 0.64 0.63 0.64

Particulars 2016 2015 2014 2013 2012

(Dupont) ROE

0.0536 0.0565 0.1499 0.1680 0.1830

RR

0.5984 0.6229 0.6389 0.6280 0.6443

Growth rate 3.20% 3.52% 9.58% 10.55% 11.79%

G 7.73%

Table 1: The historical growth rate of DDM (2016-2019)

(Source: As created by the author)

The table mainly depicts the relevant valuation of Sembcorp, which could be used in

the dividend discount model.

Asset turnover

ratio 0.021 0.025 0.070 0.116 0.198

Equity multiplier

2.731 2.476 2.375 2.106 0.920

ROE

0.003 0.003 0.017 0.025 0.019

Particulars 2016 2015 2014 2013 2012

Dividend per share 0.08 0.11 0.16 0.17 0.15

Earnings per share 0.1992 0.2917 0.4431 0.457 0.4217

Retention rate 0.60 0.62 0.64 0.63 0.64

Particulars 2016 2015 2014 2013 2012

(Dupont) ROE

0.0536 0.0565 0.1499 0.1680 0.1830

RR

0.5984 0.6229 0.6389 0.6280 0.6443

Growth rate 3.20% 3.52% 9.58% 10.55% 11.79%

G 7.73%

Table 1: The historical growth rate of DDM (2016-2019)

(Source: As created by the author)

The table mainly depicts the relevant valuation of Sembcorp, which could be used in

the dividend discount model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INVESTMENT PROJECT

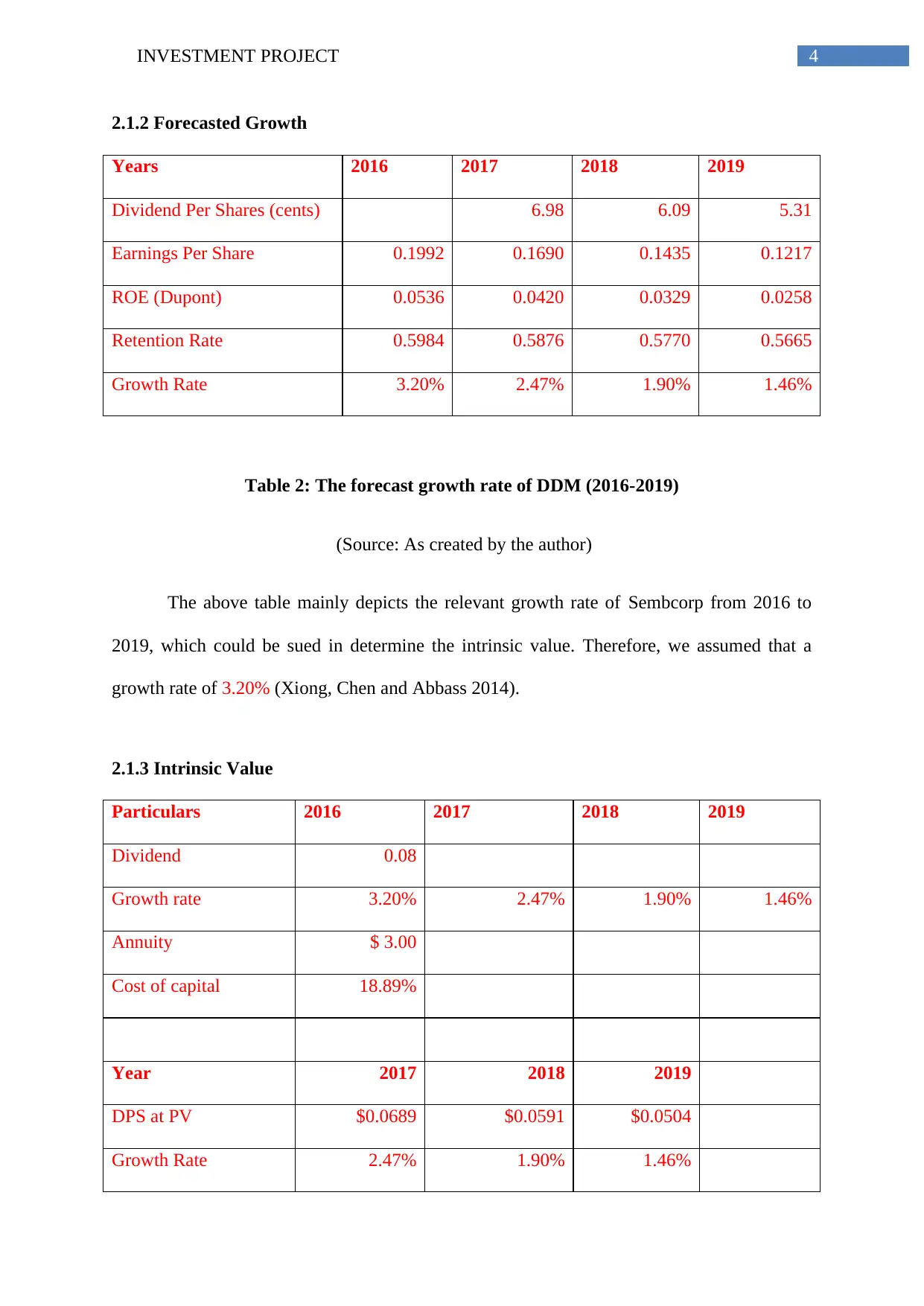

2.1.2 Forecasted Growth

Years 2016 2017 2018 2019

Dividend Per Shares (cents) 6.98 6.09 5.31

Earnings Per Share 0.1992 0.1690 0.1435 0.1217

ROE (Dupont) 0.0536 0.0420 0.0329 0.0258

Retention Rate 0.5984 0.5876 0.5770 0.5665

Growth Rate 3.20% 2.47% 1.90% 1.46%

Table 2: The forecast growth rate of DDM (2016-2019)

(Source: As created by the author)

The above table mainly depicts the relevant growth rate of Sembcorp from 2016 to

2019, which could be sued in determine the intrinsic value. Therefore, we assumed that a

growth rate of 3.20% (Xiong, Chen and Abbass 2014).

2.1.3 Intrinsic Value

Particulars 2016 2017 2018 2019

Dividend 0.08

Growth rate 3.20% 2.47% 1.90% 1.46%

Annuity $ 3.00

Cost of capital 18.89%

Year 2017 2018 2019

DPS at PV $0.0689 $0.0591 $0.0504

Growth Rate 2.47% 1.90% 1.46%

2.1.2 Forecasted Growth

Years 2016 2017 2018 2019

Dividend Per Shares (cents) 6.98 6.09 5.31

Earnings Per Share 0.1992 0.1690 0.1435 0.1217

ROE (Dupont) 0.0536 0.0420 0.0329 0.0258

Retention Rate 0.5984 0.5876 0.5770 0.5665

Growth Rate 3.20% 2.47% 1.90% 1.46%

Table 2: The forecast growth rate of DDM (2016-2019)

(Source: As created by the author)

The above table mainly depicts the relevant growth rate of Sembcorp from 2016 to

2019, which could be sued in determine the intrinsic value. Therefore, we assumed that a

growth rate of 3.20% (Xiong, Chen and Abbass 2014).

2.1.3 Intrinsic Value

Particulars 2016 2017 2018 2019

Dividend 0.08

Growth rate 3.20% 2.47% 1.90% 1.46%

Annuity $ 3.00

Cost of capital 18.89%

Year 2017 2018 2019

DPS at PV $0.0689 $0.0591 $0.0504

Growth Rate 2.47% 1.90% 1.46%

5INVESTMENT PROJECT

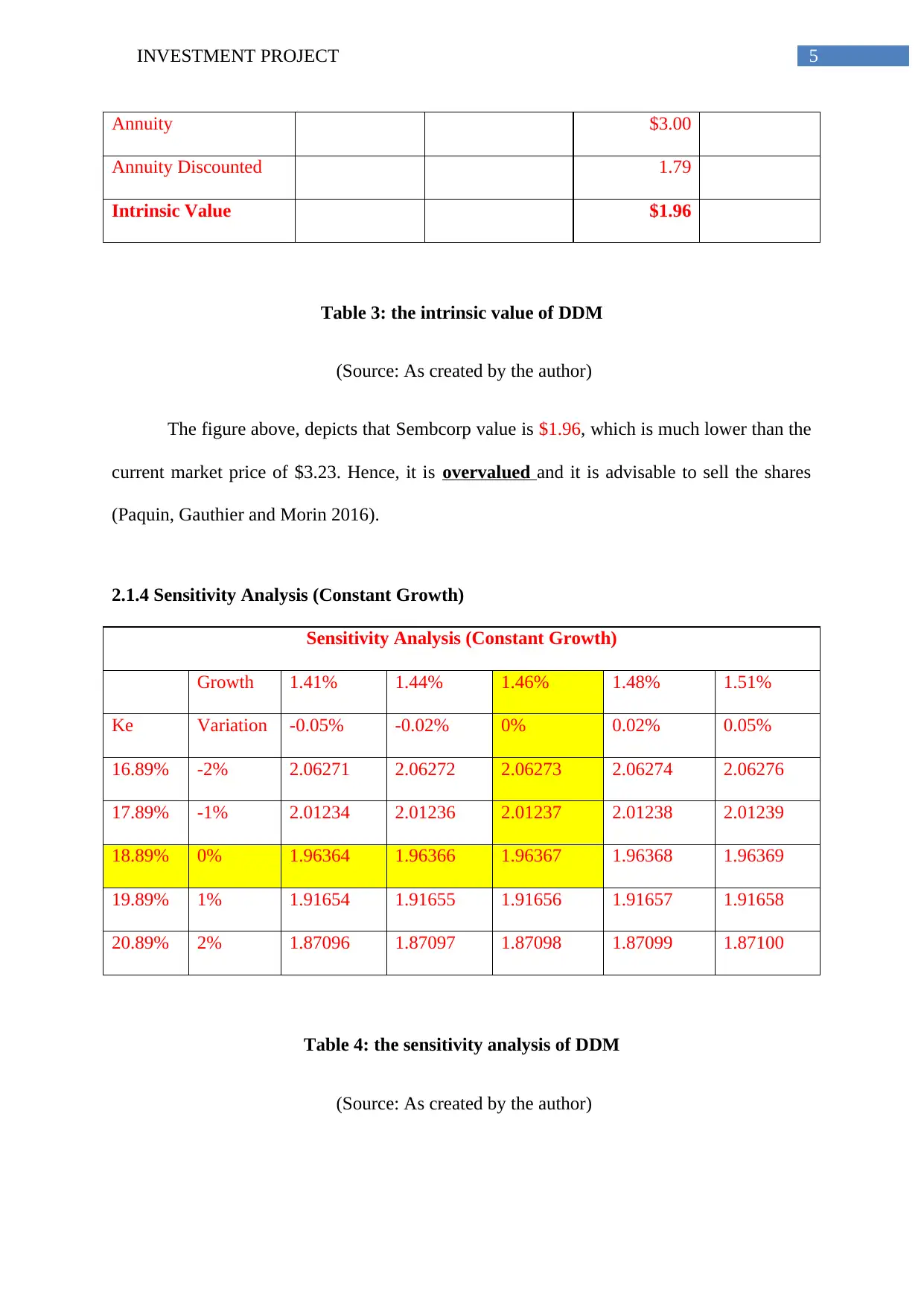

Annuity $3.00

Annuity Discounted 1.79

Intrinsic Value $1.96

Table 3: the intrinsic value of DDM

(Source: As created by the author)

The figure above, depicts that Sembcorp value is $1.96, which is much lower than the

current market price of $3.23. Hence, it is overvalued and it is advisable to sell the shares

(Paquin, Gauthier and Morin 2016).

2.1.4 Sensitivity Analysis (Constant Growth)

Sensitivity Analysis (Constant Growth)

Growth 1.41% 1.44% 1.46% 1.48% 1.51%

Ke Variation -0.05% -0.02% 0% 0.02% 0.05%

16.89% -2% 2.06271 2.06272 2.06273 2.06274 2.06276

17.89% -1% 2.01234 2.01236 2.01237 2.01238 2.01239

18.89% 0% 1.96364 1.96366 1.96367 1.96368 1.96369

19.89% 1% 1.91654 1.91655 1.91656 1.91657 1.91658

20.89% 2% 1.87096 1.87097 1.87098 1.87099 1.87100

Table 4: the sensitivity analysis of DDM

(Source: As created by the author)

Annuity $3.00

Annuity Discounted 1.79

Intrinsic Value $1.96

Table 3: the intrinsic value of DDM

(Source: As created by the author)

The figure above, depicts that Sembcorp value is $1.96, which is much lower than the

current market price of $3.23. Hence, it is overvalued and it is advisable to sell the shares

(Paquin, Gauthier and Morin 2016).

2.1.4 Sensitivity Analysis (Constant Growth)

Sensitivity Analysis (Constant Growth)

Growth 1.41% 1.44% 1.46% 1.48% 1.51%

Ke Variation -0.05% -0.02% 0% 0.02% 0.05%

16.89% -2% 2.06271 2.06272 2.06273 2.06274 2.06276

17.89% -1% 2.01234 2.01236 2.01237 2.01238 2.01239

18.89% 0% 1.96364 1.96366 1.96367 1.96368 1.96369

19.89% 1% 1.91654 1.91655 1.91656 1.91657 1.91658

20.89% 2% 1.87096 1.87097 1.87098 1.87099 1.87100

Table 4: the sensitivity analysis of DDM

(Source: As created by the author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INVESTMENT PROJECT

The use of sensitivity analysis mainly helps in identifying the overall intrinsic value

of the Sembcorp, if the valuation is changed (Vajarothai, Al-Jibouri and Halman 2015).

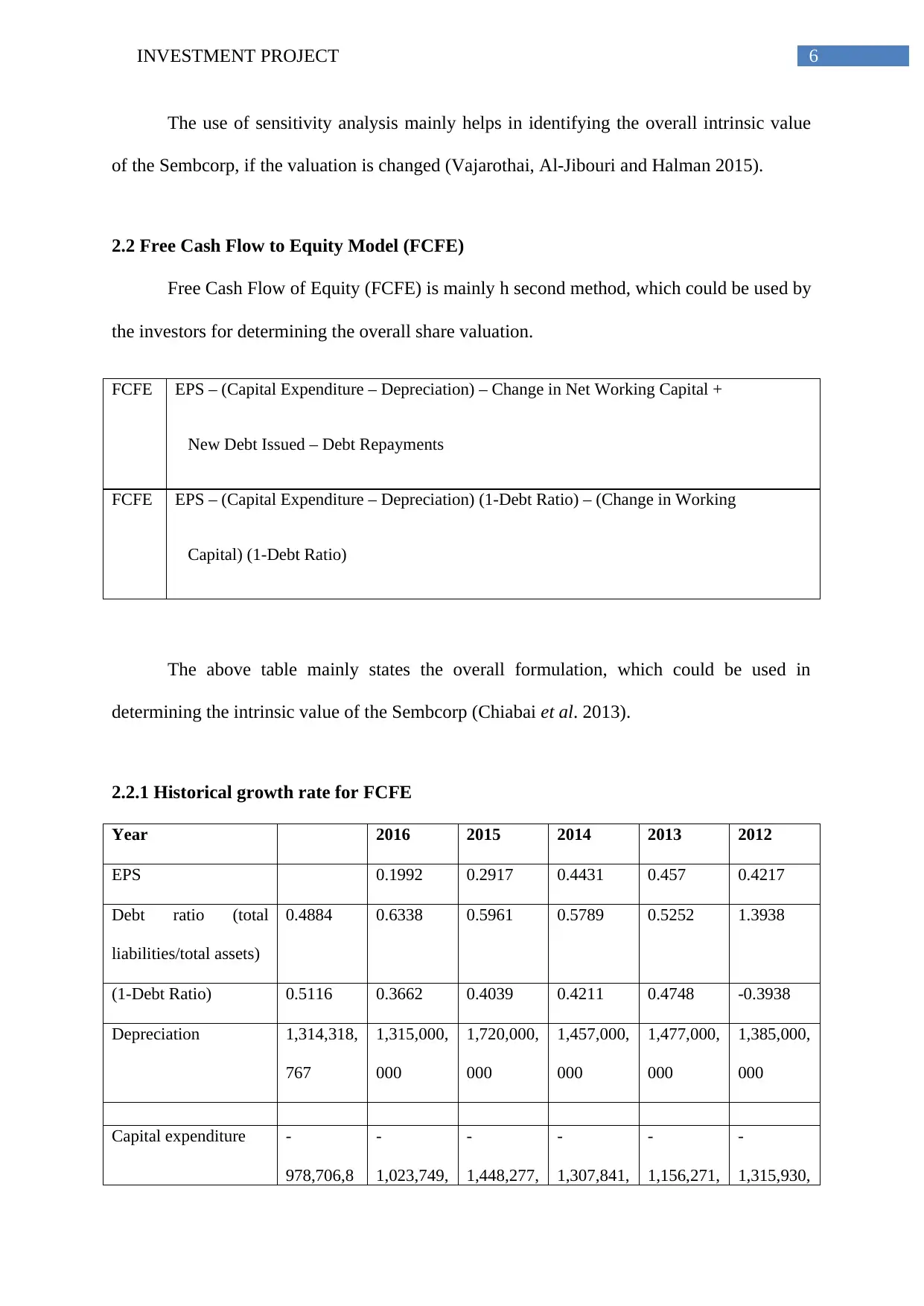

2.2 Free Cash Flow to Equity Model (FCFE)

Free Cash Flow of Equity (FCFE) is mainly h second method, which could be used by

the investors for determining the overall share valuation.

FCFE EPS – (Capital Expenditure – Depreciation) – Change in Net Working Capital +

New Debt Issued – Debt Repayments

FCFE EPS – (Capital Expenditure – Depreciation) (1-Debt Ratio) – (Change in Working

Capital) (1-Debt Ratio)

The above table mainly states the overall formulation, which could be used in

determining the intrinsic value of the Sembcorp (Chiabai et al. 2013).

2.2.1 Historical growth rate for FCFE

Year 2016 2015 2014 2013 2012

EPS 0.1992 0.2917 0.4431 0.457 0.4217

Debt ratio (total

liabilities/total assets)

0.4884 0.6338 0.5961 0.5789 0.5252 1.3938

(1-Debt Ratio) 0.5116 0.3662 0.4039 0.4211 0.4748 -0.3938

Depreciation 1,314,318,

767

1,315,000,

000

1,720,000,

000

1,457,000,

000

1,477,000,

000

1,385,000,

000

Capital expenditure -

978,706,8

-

1,023,749,

-

1,448,277,

-

1,307,841,

-

1,156,271,

-

1,315,930,

The use of sensitivity analysis mainly helps in identifying the overall intrinsic value

of the Sembcorp, if the valuation is changed (Vajarothai, Al-Jibouri and Halman 2015).

2.2 Free Cash Flow to Equity Model (FCFE)

Free Cash Flow of Equity (FCFE) is mainly h second method, which could be used by

the investors for determining the overall share valuation.

FCFE EPS – (Capital Expenditure – Depreciation) – Change in Net Working Capital +

New Debt Issued – Debt Repayments

FCFE EPS – (Capital Expenditure – Depreciation) (1-Debt Ratio) – (Change in Working

Capital) (1-Debt Ratio)

The above table mainly states the overall formulation, which could be used in

determining the intrinsic value of the Sembcorp (Chiabai et al. 2013).

2.2.1 Historical growth rate for FCFE

Year 2016 2015 2014 2013 2012

EPS 0.1992 0.2917 0.4431 0.457 0.4217

Debt ratio (total

liabilities/total assets)

0.4884 0.6338 0.5961 0.5789 0.5252 1.3938

(1-Debt Ratio) 0.5116 0.3662 0.4039 0.4211 0.4748 -0.3938

Depreciation 1,314,318,

767

1,315,000,

000

1,720,000,

000

1,457,000,

000

1,477,000,

000

1,385,000,

000

Capital expenditure -

978,706,8

-

1,023,749,

-

1,448,277,

-

1,307,841,

-

1,156,271,

-

1,315,930,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

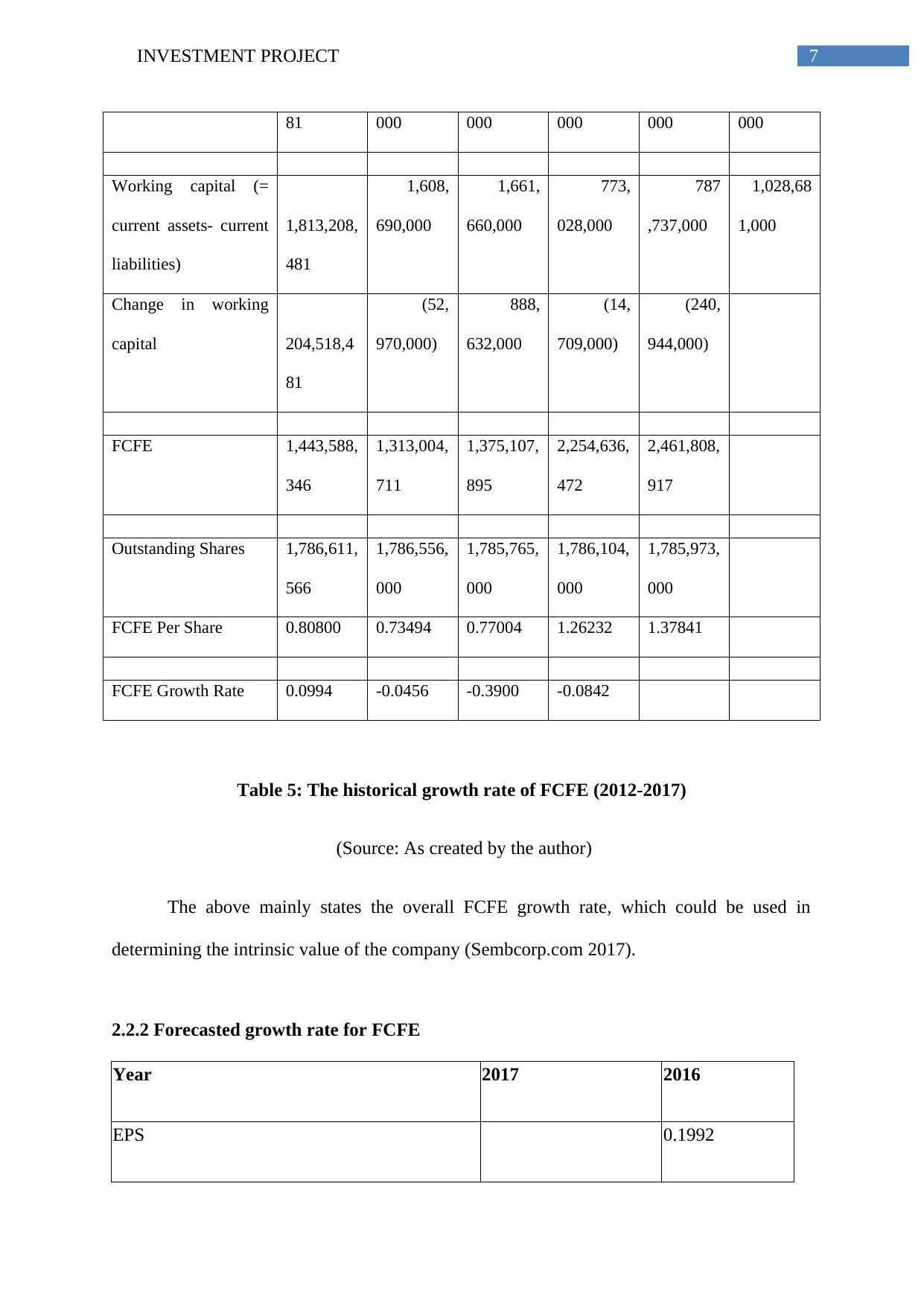

7INVESTMENT PROJECT

81 000 000 000 000 000

Working capital (=

current assets- current

liabilities)

1,813,208,

481

1,608,

690,000

1,661,

660,000

773,

028,000

787

,737,000

1,028,68

1,000

Change in working

capital 204,518,4

81

(52,

970,000)

888,

632,000

(14,

709,000)

(240,

944,000)

FCFE 1,443,588,

346

1,313,004,

711

1,375,107,

895

2,254,636,

472

2,461,808,

917

Outstanding Shares 1,786,611,

566

1,786,556,

000

1,785,765,

000

1,786,104,

000

1,785,973,

000

FCFE Per Share 0.80800 0.73494 0.77004 1.26232 1.37841

FCFE Growth Rate 0.0994 -0.0456 -0.3900 -0.0842

Table 5: The historical growth rate of FCFE (2012-2017)

(Source: As created by the author)

The above mainly states the overall FCFE growth rate, which could be used in

determining the intrinsic value of the company (Sembcorp.com 2017).

2.2.2 Forecasted growth rate for FCFE

Year 2017 2016

EPS 0.1992

81 000 000 000 000 000

Working capital (=

current assets- current

liabilities)

1,813,208,

481

1,608,

690,000

1,661,

660,000

773,

028,000

787

,737,000

1,028,68

1,000

Change in working

capital 204,518,4

81

(52,

970,000)

888,

632,000

(14,

709,000)

(240,

944,000)

FCFE 1,443,588,

346

1,313,004,

711

1,375,107,

895

2,254,636,

472

2,461,808,

917

Outstanding Shares 1,786,611,

566

1,786,556,

000

1,785,765,

000

1,786,104,

000

1,785,973,

000

FCFE Per Share 0.80800 0.73494 0.77004 1.26232 1.37841

FCFE Growth Rate 0.0994 -0.0456 -0.3900 -0.0842

Table 5: The historical growth rate of FCFE (2012-2017)

(Source: As created by the author)

The above mainly states the overall FCFE growth rate, which could be used in

determining the intrinsic value of the company (Sembcorp.com 2017).

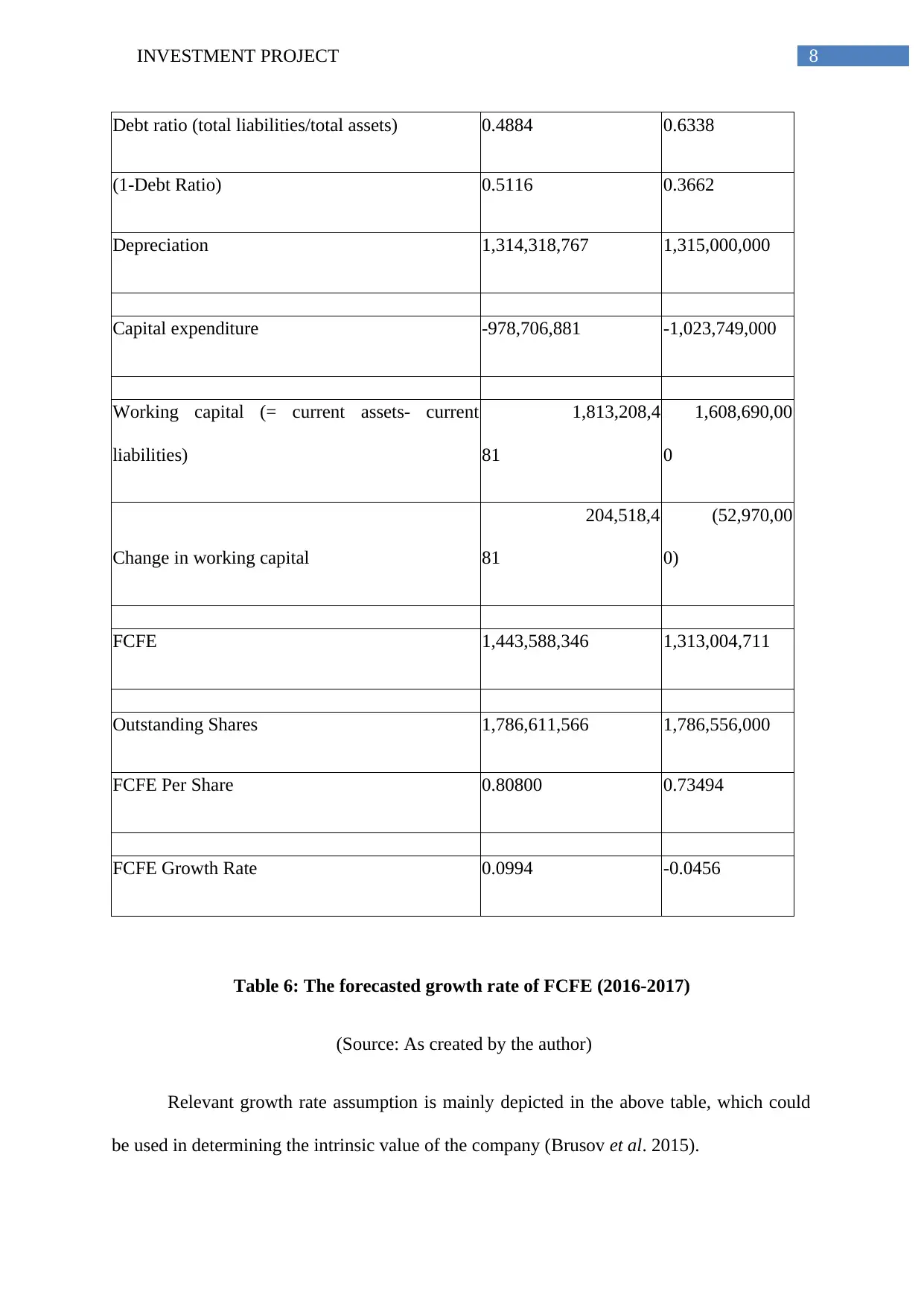

2.2.2 Forecasted growth rate for FCFE

Year 2017 2016

EPS 0.1992

8INVESTMENT PROJECT

Debt ratio (total liabilities/total assets) 0.4884 0.6338

(1-Debt Ratio) 0.5116 0.3662

Depreciation 1,314,318,767 1,315,000,000

Capital expenditure -978,706,881 -1,023,749,000

Working capital (= current assets- current

liabilities)

1,813,208,4

81

1,608,690,00

0

Change in working capital

204,518,4

81

(52,970,00

0)

FCFE 1,443,588,346 1,313,004,711

Outstanding Shares 1,786,611,566 1,786,556,000

FCFE Per Share 0.80800 0.73494

FCFE Growth Rate 0.0994 -0.0456

Table 6: The forecasted growth rate of FCFE (2016-2017)

(Source: As created by the author)

Relevant growth rate assumption is mainly depicted in the above table, which could

be used in determining the intrinsic value of the company (Brusov et al. 2015).

Debt ratio (total liabilities/total assets) 0.4884 0.6338

(1-Debt Ratio) 0.5116 0.3662

Depreciation 1,314,318,767 1,315,000,000

Capital expenditure -978,706,881 -1,023,749,000

Working capital (= current assets- current

liabilities)

1,813,208,4

81

1,608,690,00

0

Change in working capital

204,518,4

81

(52,970,00

0)

FCFE 1,443,588,346 1,313,004,711

Outstanding Shares 1,786,611,566 1,786,556,000

FCFE Per Share 0.80800 0.73494

FCFE Growth Rate 0.0994 -0.0456

Table 6: The forecasted growth rate of FCFE (2016-2017)

(Source: As created by the author)

Relevant growth rate assumption is mainly depicted in the above table, which could

be used in determining the intrinsic value of the company (Brusov et al. 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INVESTMENT PROJECT

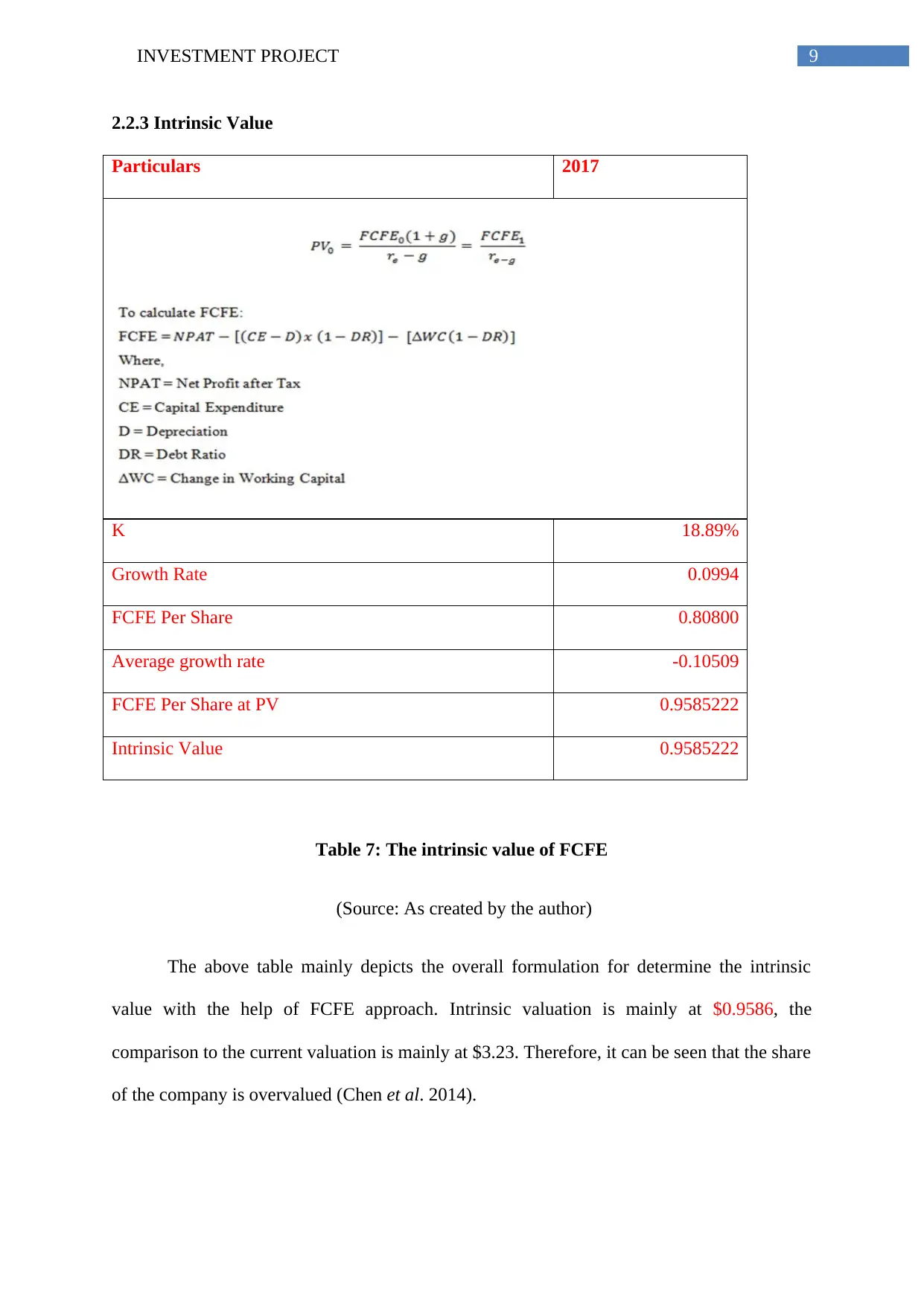

2.2.3 Intrinsic Value

Particulars 2017

K 18.89%

Growth Rate 0.0994

FCFE Per Share 0.80800

Average growth rate -0.10509

FCFE Per Share at PV 0.9585222

Intrinsic Value 0.9585222

Table 7: The intrinsic value of FCFE

(Source: As created by the author)

The above table mainly depicts the overall formulation for determine the intrinsic

value with the help of FCFE approach. Intrinsic valuation is mainly at $0.9586, the

comparison to the current valuation is mainly at $3.23. Therefore, it can be seen that the share

of the company is overvalued (Chen et al. 2014).

2.2.3 Intrinsic Value

Particulars 2017

K 18.89%

Growth Rate 0.0994

FCFE Per Share 0.80800

Average growth rate -0.10509

FCFE Per Share at PV 0.9585222

Intrinsic Value 0.9585222

Table 7: The intrinsic value of FCFE

(Source: As created by the author)

The above table mainly depicts the overall formulation for determine the intrinsic

value with the help of FCFE approach. Intrinsic valuation is mainly at $0.9586, the

comparison to the current valuation is mainly at $3.23. Therefore, it can be seen that the share

of the company is overvalued (Chen et al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INVESTMENT PROJECT

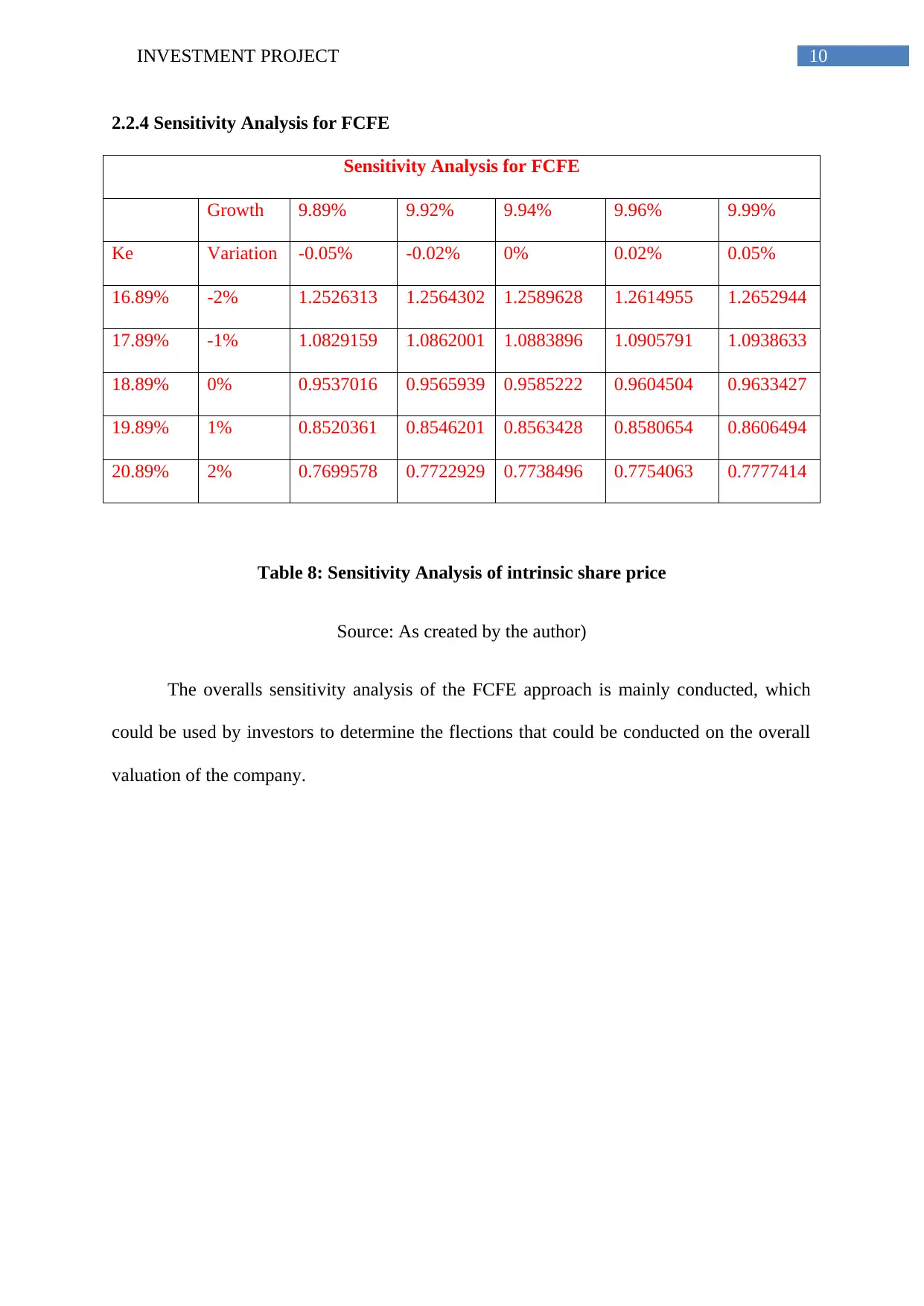

2.2.4 Sensitivity Analysis for FCFE

Sensitivity Analysis for FCFE

Growth 9.89% 9.92% 9.94% 9.96% 9.99%

Ke Variation -0.05% -0.02% 0% 0.02% 0.05%

16.89% -2% 1.2526313 1.2564302 1.2589628 1.2614955 1.2652944

17.89% -1% 1.0829159 1.0862001 1.0883896 1.0905791 1.0938633

18.89% 0% 0.9537016 0.9565939 0.9585222 0.9604504 0.9633427

19.89% 1% 0.8520361 0.8546201 0.8563428 0.8580654 0.8606494

20.89% 2% 0.7699578 0.7722929 0.7738496 0.7754063 0.7777414

Table 8: Sensitivity Analysis of intrinsic share price

Source: As created by the author)

The overalls sensitivity analysis of the FCFE approach is mainly conducted, which

could be used by investors to determine the flections that could be conducted on the overall

valuation of the company.

2.2.4 Sensitivity Analysis for FCFE

Sensitivity Analysis for FCFE

Growth 9.89% 9.92% 9.94% 9.96% 9.99%

Ke Variation -0.05% -0.02% 0% 0.02% 0.05%

16.89% -2% 1.2526313 1.2564302 1.2589628 1.2614955 1.2652944

17.89% -1% 1.0829159 1.0862001 1.0883896 1.0905791 1.0938633

18.89% 0% 0.9537016 0.9565939 0.9585222 0.9604504 0.9633427

19.89% 1% 0.8520361 0.8546201 0.8563428 0.8580654 0.8606494

20.89% 2% 0.7699578 0.7722929 0.7738496 0.7754063 0.7777414

Table 8: Sensitivity Analysis of intrinsic share price

Source: As created by the author)

The overalls sensitivity analysis of the FCFE approach is mainly conducted, which

could be used by investors to determine the flections that could be conducted on the overall

valuation of the company.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.