Data Analysis Assignment: Data Analysis and Interpretation Report

VerifiedAdded on 2020/02/24

|17

|1904

|40

Homework Assignment

AI Summary

This data analysis assignment encompasses a comprehensive analysis of various datasets, including financial data, employing statistical methods to derive meaningful insights. The assignment begins with descriptive statistics, including stem and leaf plots, histograms, and box plots, to visualize and summarize data distributions. It proceeds to compare investment recommendations between two companies, Crown Resorts Limited and Tabcorp Holdings Limited, based on financial performance. Further analysis involves hypothesis testing using t-tests to assess differences between groups based on ratios like Net Profit/Total Assets, Total Liabilities/Total Assets, and Working Capital/Total Assets. The assignment also explores probability concepts related to rainfall and student ATAR scores, providing a well-rounded approach to data analysis and interpretation.

Running head: DATA ANALYSIS ASSIGNMENT

Data Analysis Assignment

Name

Course Number

Date

Faculty Name

Data Analysis Assignment

Name

Course Number

Date

Faculty Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA ANALYSIS ASSIGNMENT 2

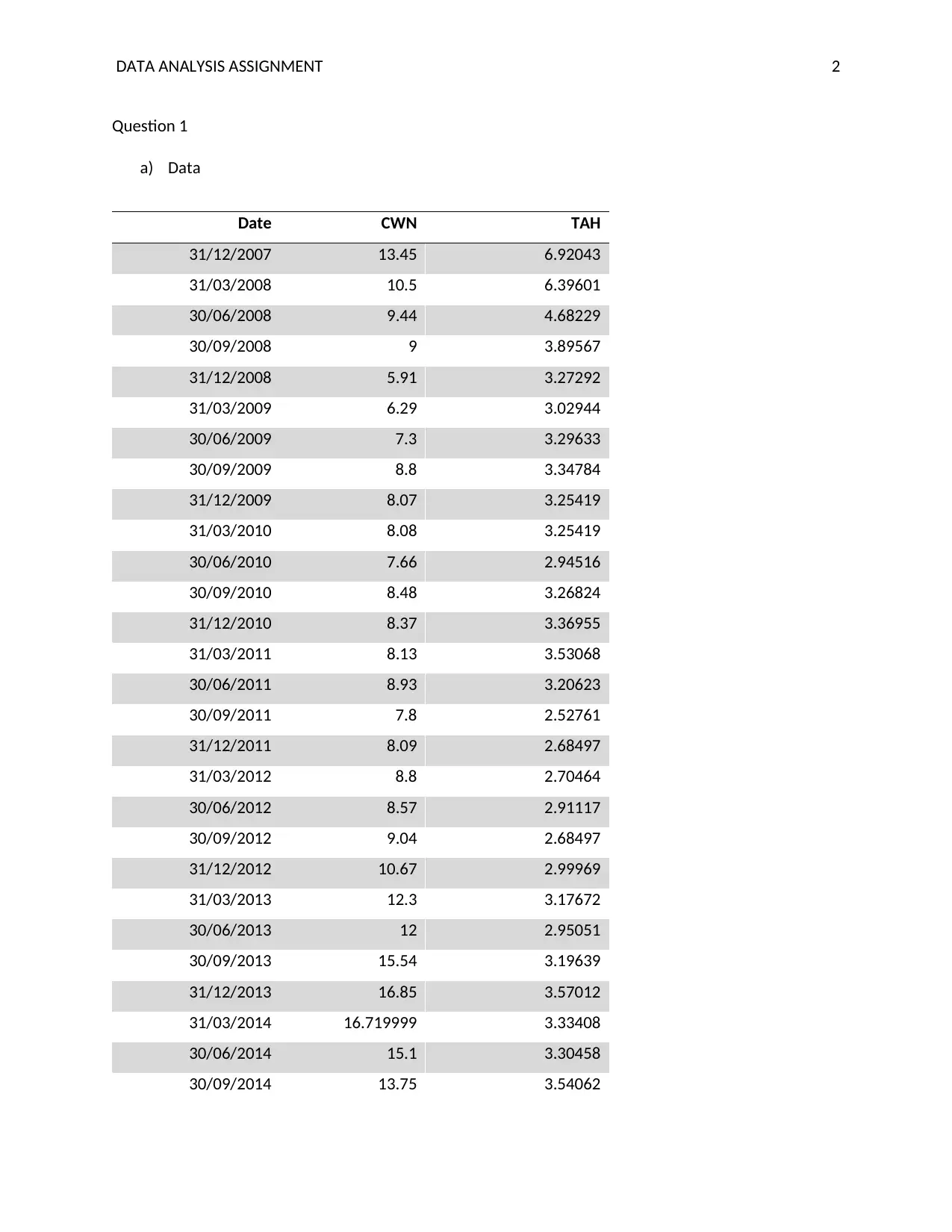

Question 1

a) Data

Date CWN TAH

31/12/2007 13.45 6.92043

31/03/2008 10.5 6.39601

30/06/2008 9.44 4.68229

30/09/2008 9 3.89567

31/12/2008 5.91 3.27292

31/03/2009 6.29 3.02944

30/06/2009 7.3 3.29633

30/09/2009 8.8 3.34784

31/12/2009 8.07 3.25419

31/03/2010 8.08 3.25419

30/06/2010 7.66 2.94516

30/09/2010 8.48 3.26824

31/12/2010 8.37 3.36955

31/03/2011 8.13 3.53068

30/06/2011 8.93 3.20623

30/09/2011 7.8 2.52761

31/12/2011 8.09 2.68497

31/03/2012 8.8 2.70464

30/06/2012 8.57 2.91117

30/09/2012 9.04 2.68497

31/12/2012 10.67 2.99969

31/03/2013 12.3 3.17672

30/06/2013 12 2.95051

30/09/2013 15.54 3.19639

31/12/2013 16.85 3.57012

31/03/2014 16.719999 3.33408

30/06/2014 15.1 3.30458

30/09/2014 13.75 3.54062

Question 1

a) Data

Date CWN TAH

31/12/2007 13.45 6.92043

31/03/2008 10.5 6.39601

30/06/2008 9.44 4.68229

30/09/2008 9 3.89567

31/12/2008 5.91 3.27292

31/03/2009 6.29 3.02944

30/06/2009 7.3 3.29633

30/09/2009 8.8 3.34784

31/12/2009 8.07 3.25419

31/03/2010 8.08 3.25419

30/06/2010 7.66 2.94516

30/09/2010 8.48 3.26824

31/12/2010 8.37 3.36955

31/03/2011 8.13 3.53068

30/06/2011 8.93 3.20623

30/09/2011 7.8 2.52761

31/12/2011 8.09 2.68497

31/03/2012 8.8 2.70464

30/06/2012 8.57 2.91117

30/09/2012 9.04 2.68497

31/12/2012 10.67 2.99969

31/03/2013 12.3 3.17672

30/06/2013 12 2.95051

30/09/2013 15.54 3.19639

31/12/2013 16.85 3.57012

31/03/2014 16.719999 3.33408

30/06/2014 15.1 3.30458

30/09/2014 13.75 3.54062

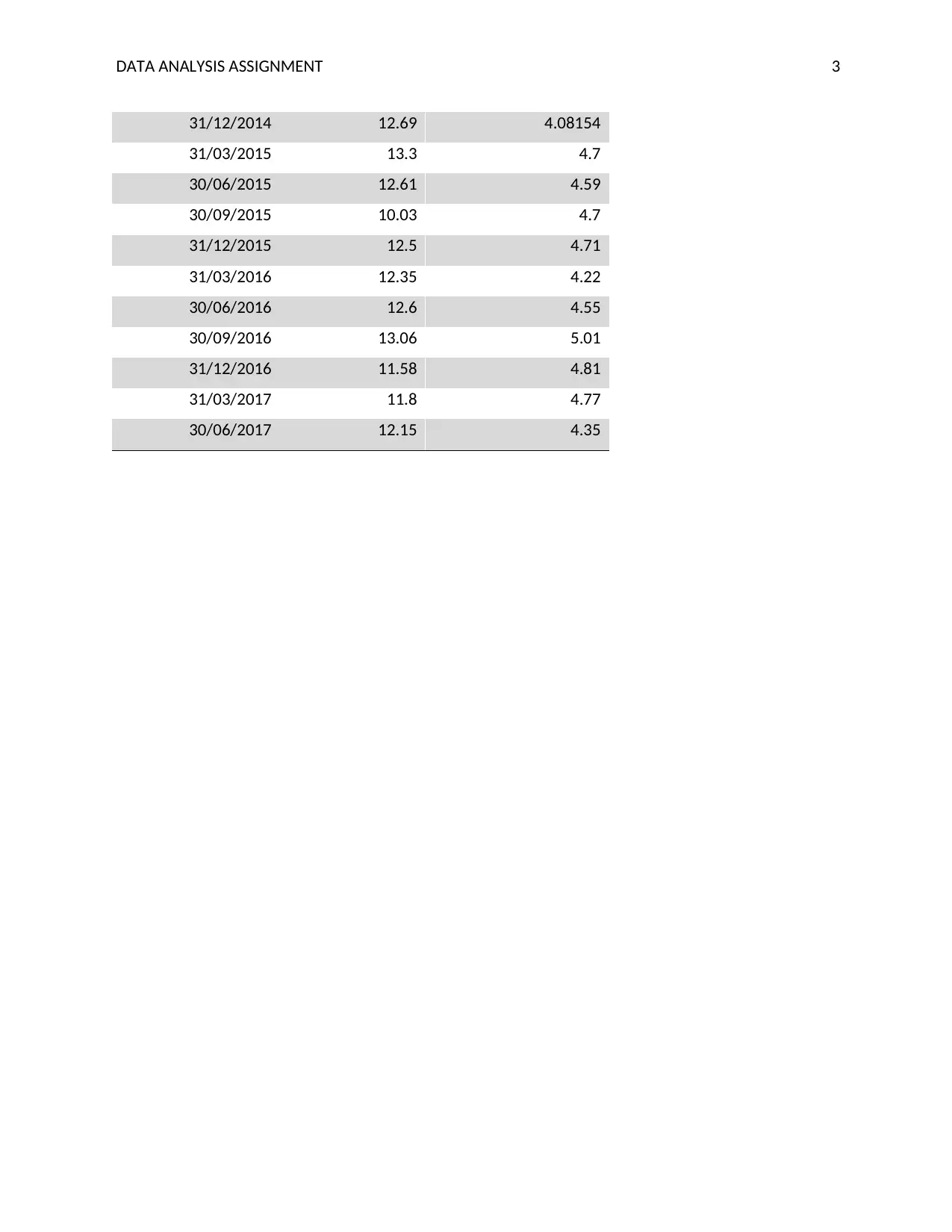

DATA ANALYSIS ASSIGNMENT 3

31/12/2014 12.69 4.08154

31/03/2015 13.3 4.7

30/06/2015 12.61 4.59

30/09/2015 10.03 4.7

31/12/2015 12.5 4.71

31/03/2016 12.35 4.22

30/06/2016 12.6 4.55

30/09/2016 13.06 5.01

31/12/2016 11.58 4.81

31/03/2017 11.8 4.77

30/06/2017 12.15 4.35

31/12/2014 12.69 4.08154

31/03/2015 13.3 4.7

30/06/2015 12.61 4.59

30/09/2015 10.03 4.7

31/12/2015 12.5 4.71

31/03/2016 12.35 4.22

30/06/2016 12.6 4.55

30/09/2016 13.06 5.01

31/12/2016 11.58 4.81

31/03/2017 11.8 4.77

30/06/2017 12.15 4.35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DATA ANALYSIS ASSIGNMENT 4

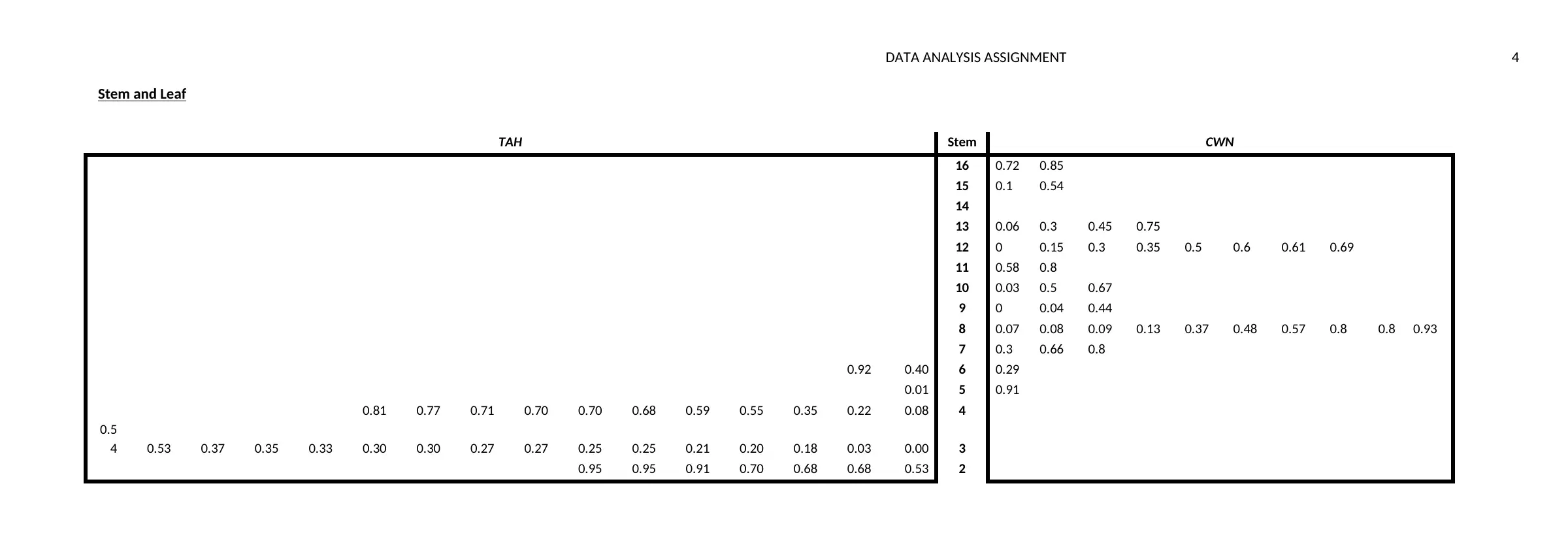

Stem and Leaf

TAH Stem CWN

16 0.72 0.85

15 0.1 0.54

14

13 0.06 0.3 0.45 0.75

12 0 0.15 0.3 0.35 0.5 0.6 0.61 0.69

11 0.58 0.8

10 0.03 0.5 0.67

9 0 0.04 0.44

8 0.07 0.08 0.09 0.13 0.37 0.48 0.57 0.8 0.8 0.93

7 0.3 0.66 0.8

0.92 0.40 6 0.29

0.01 5 0.91

0.81 0.77 0.71 0.70 0.70 0.68 0.59 0.55 0.35 0.22 0.08 4

0.5

4 0.53 0.37 0.35 0.33 0.30 0.30 0.27 0.27 0.25 0.25 0.21 0.20 0.18 0.03 0.00 3

0.95 0.95 0.91 0.70 0.68 0.68 0.53 2

Stem and Leaf

TAH Stem CWN

16 0.72 0.85

15 0.1 0.54

14

13 0.06 0.3 0.45 0.75

12 0 0.15 0.3 0.35 0.5 0.6 0.61 0.69

11 0.58 0.8

10 0.03 0.5 0.67

9 0 0.04 0.44

8 0.07 0.08 0.09 0.13 0.37 0.48 0.57 0.8 0.8 0.93

7 0.3 0.66 0.8

0.92 0.40 6 0.29

0.01 5 0.91

0.81 0.77 0.71 0.70 0.70 0.68 0.59 0.55 0.35 0.22 0.08 4

0.5

4 0.53 0.37 0.35 0.33 0.30 0.30 0.27 0.27 0.25 0.25 0.21 0.20 0.18 0.03 0.00 3

0.95 0.95 0.91 0.70 0.68 0.68 0.53 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA ANALYSIS ASSIGNMENT 5

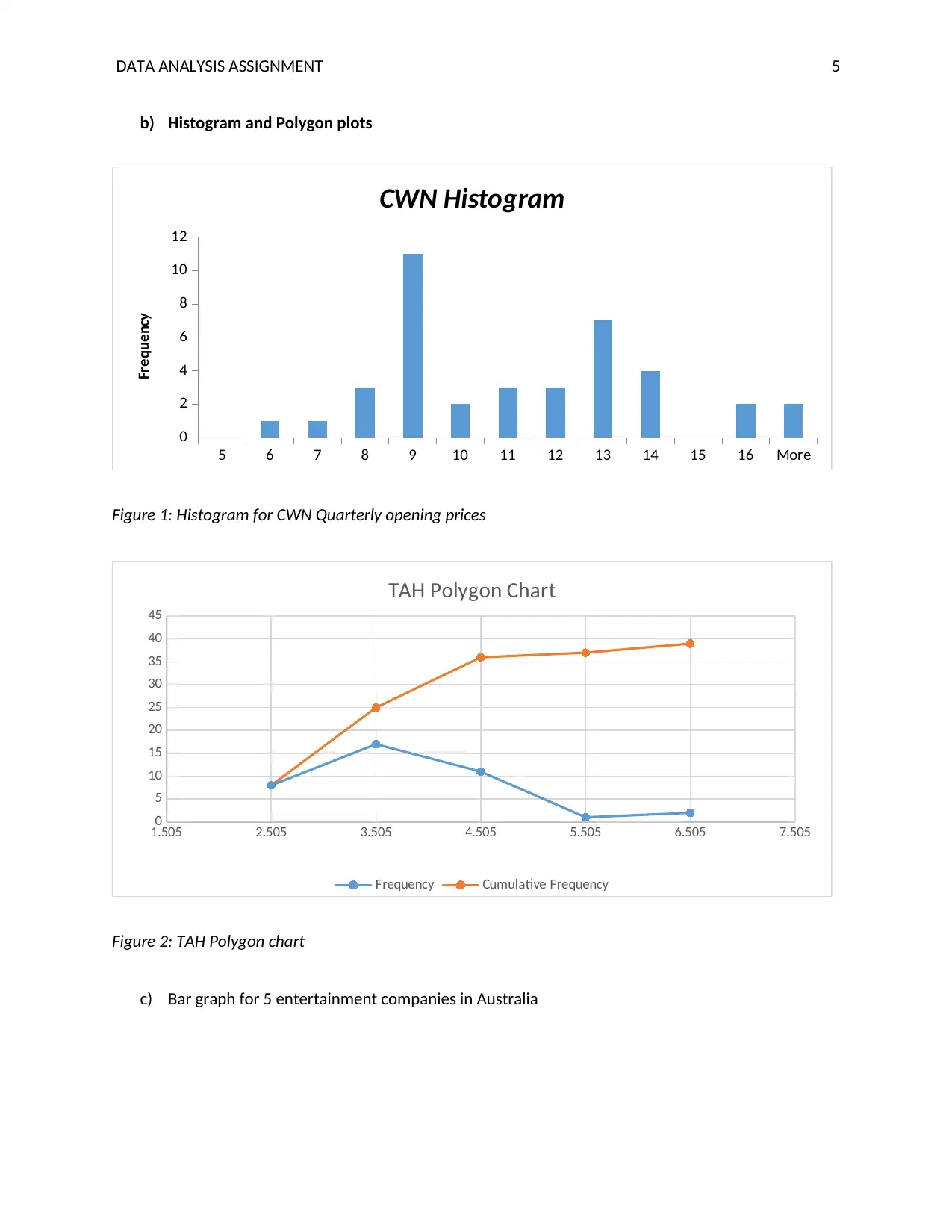

b) Histogram and Polygon plots

5 6 7 8 9 10 11 12 13 14 15 16 More

0

2

4

6

8

10

12

CWN Histogram

Frequency

Figure 1: Histogram for CWN Quarterly opening prices

1.505 2.505 3.505 4.505 5.505 6.505 7.505

0

5

10

15

20

25

30

35

40

45

TAH Polygon Chart

Frequency Cumulative Frequency

Figure 2: TAH Polygon chart

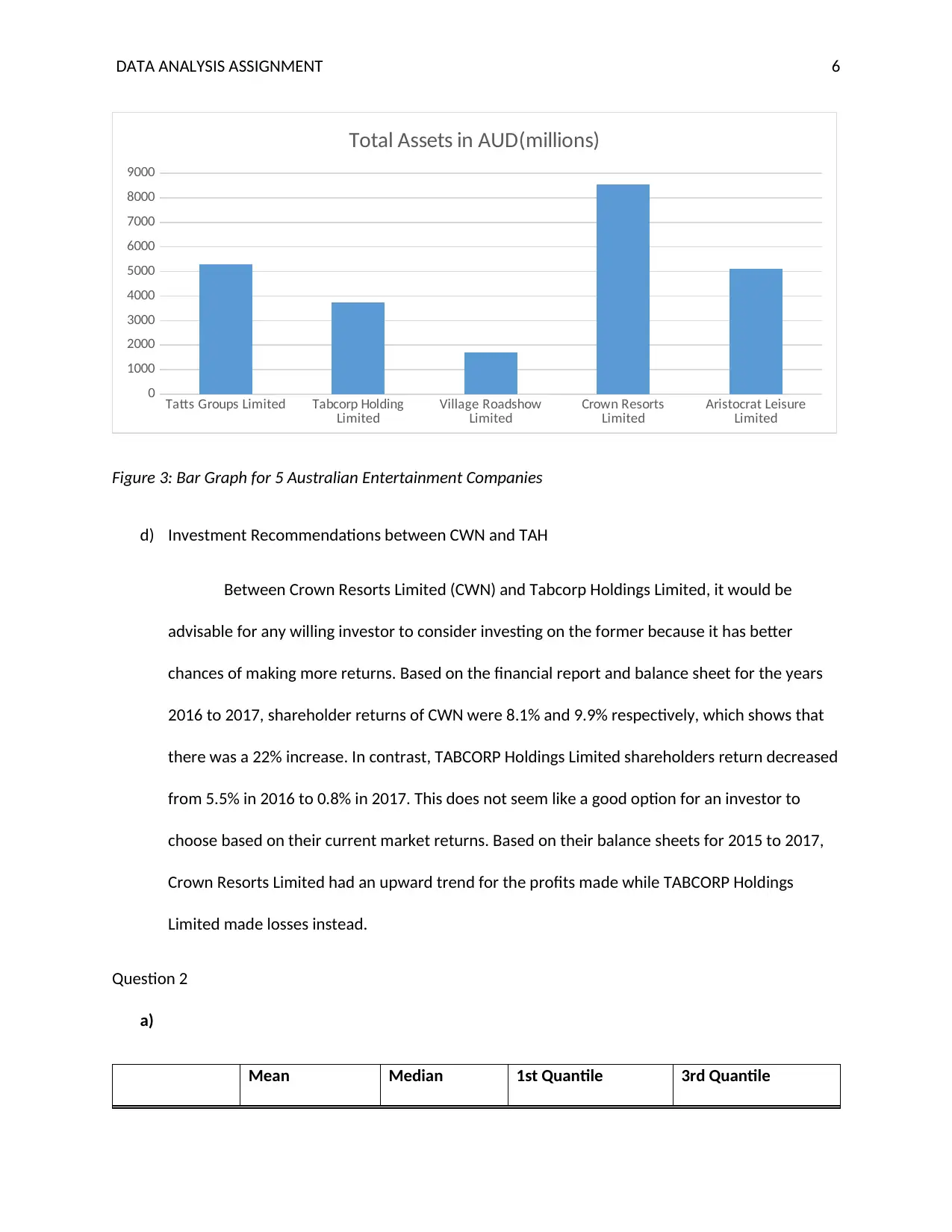

c) Bar graph for 5 entertainment companies in Australia

b) Histogram and Polygon plots

5 6 7 8 9 10 11 12 13 14 15 16 More

0

2

4

6

8

10

12

CWN Histogram

Frequency

Figure 1: Histogram for CWN Quarterly opening prices

1.505 2.505 3.505 4.505 5.505 6.505 7.505

0

5

10

15

20

25

30

35

40

45

TAH Polygon Chart

Frequency Cumulative Frequency

Figure 2: TAH Polygon chart

c) Bar graph for 5 entertainment companies in Australia

DATA ANALYSIS ASSIGNMENT 6

Tatts Groups Limited Tabcorp Holding

Limited Village Roadshow

Limited Crown Resorts

Limited Aristocrat Leisure

Limited

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Total Assets in AUD(millions)

Figure 3: Bar Graph for 5 Australian Entertainment Companies

d) Investment Recommendations between CWN and TAH

Between Crown Resorts Limited (CWN) and Tabcorp Holdings Limited, it would be

advisable for any willing investor to consider investing on the former because it has better

chances of making more returns. Based on the financial report and balance sheet for the years

2016 to 2017, shareholder returns of CWN were 8.1% and 9.9% respectively, which shows that

there was a 22% increase. In contrast, TABCORP Holdings Limited shareholders return decreased

from 5.5% in 2016 to 0.8% in 2017. This does not seem like a good option for an investor to

choose based on their current market returns. Based on their balance sheets for 2015 to 2017,

Crown Resorts Limited had an upward trend for the profits made while TABCORP Holdings

Limited made losses instead.

Question 2

a)

Mean Median 1st Quantile 3rd Quantile

Tatts Groups Limited Tabcorp Holding

Limited Village Roadshow

Limited Crown Resorts

Limited Aristocrat Leisure

Limited

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Total Assets in AUD(millions)

Figure 3: Bar Graph for 5 Australian Entertainment Companies

d) Investment Recommendations between CWN and TAH

Between Crown Resorts Limited (CWN) and Tabcorp Holdings Limited, it would be

advisable for any willing investor to consider investing on the former because it has better

chances of making more returns. Based on the financial report and balance sheet for the years

2016 to 2017, shareholder returns of CWN were 8.1% and 9.9% respectively, which shows that

there was a 22% increase. In contrast, TABCORP Holdings Limited shareholders return decreased

from 5.5% in 2016 to 0.8% in 2017. This does not seem like a good option for an investor to

choose based on their current market returns. Based on their balance sheets for 2015 to 2017,

Crown Resorts Limited had an upward trend for the profits made while TABCORP Holdings

Limited made losses instead.

Question 2

a)

Mean Median 1st Quantile 3rd Quantile

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DATA ANALYSIS ASSIGNMENT 7

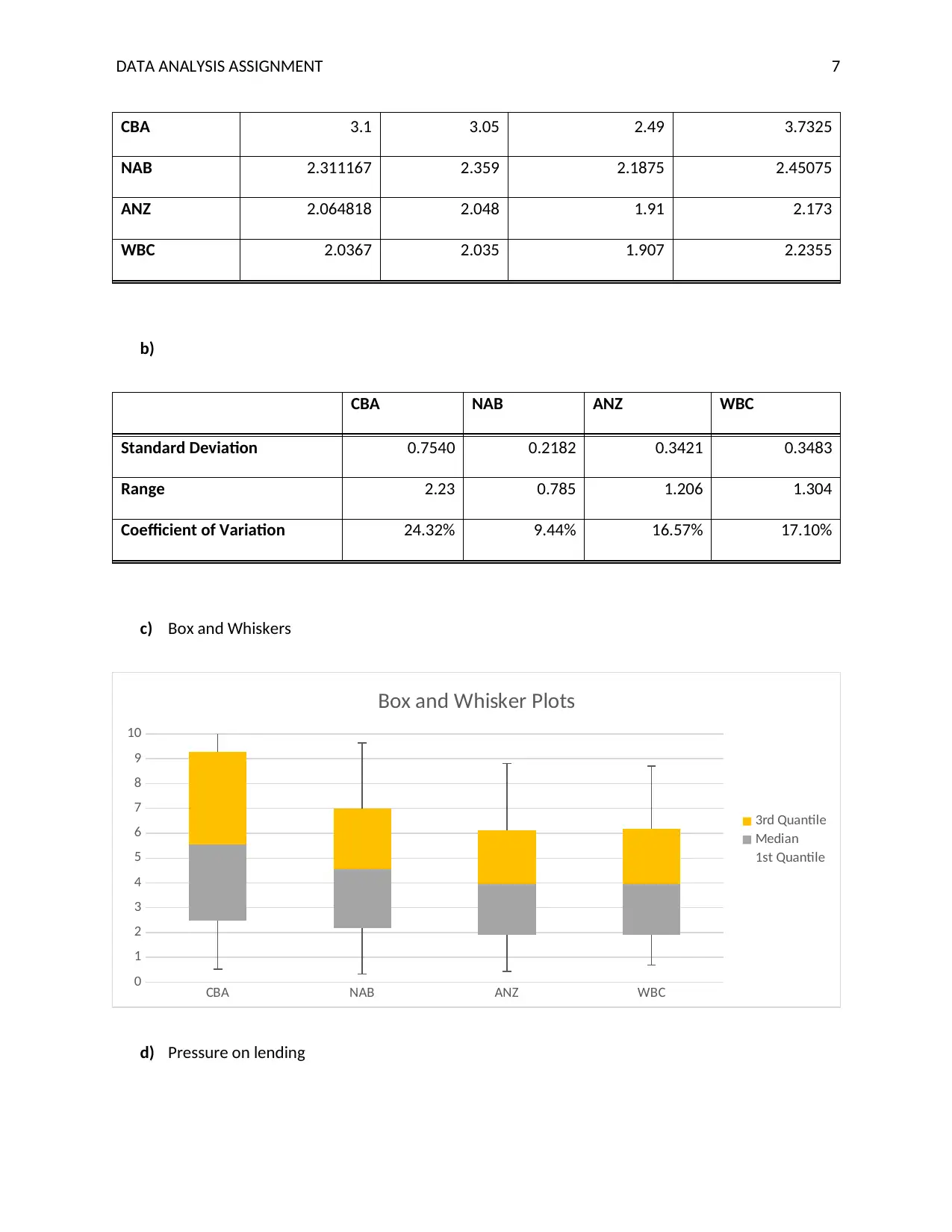

CBA 3.1 3.05 2.49 3.7325

NAB 2.311167 2.359 2.1875 2.45075

ANZ 2.064818 2.048 1.91 2.173

WBC 2.0367 2.035 1.907 2.2355

b)

CBA NAB ANZ WBC

Standard Deviation 0.7540 0.2182 0.3421 0.3483

Range 2.23 0.785 1.206 1.304

Coefficient of Variation 24.32% 9.44% 16.57% 17.10%

c) Box and Whiskers

CBA NAB ANZ WBC

0

1

2

3

4

5

6

7

8

9

10

Box and Whisker Plots

3rd Quantile

Median

1st Quantile

d) Pressure on lending

CBA 3.1 3.05 2.49 3.7325

NAB 2.311167 2.359 2.1875 2.45075

ANZ 2.064818 2.048 1.91 2.173

WBC 2.0367 2.035 1.907 2.2355

b)

CBA NAB ANZ WBC

Standard Deviation 0.7540 0.2182 0.3421 0.3483

Range 2.23 0.785 1.206 1.304

Coefficient of Variation 24.32% 9.44% 16.57% 17.10%

c) Box and Whiskers

CBA NAB ANZ WBC

0

1

2

3

4

5

6

7

8

9

10

Box and Whisker Plots

3rd Quantile

Median

1st Quantile

d) Pressure on lending

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA ANALYSIS ASSIGNMENT 8

The pressure on lending generally affects the annual dividends differently on the banks.

For instance, CBA seems to be performing better than the other three based on the average

dividends per share and the range statistics. NAB, ANZ, and WBC are performing poorly as

compared to CBA. However, CBA has the highest variation of 24.32% in relation to 9.44%,

16.57% and 17.1% of NAB, ANZ, and WBC respectively. The lending pressure is aimed at

ensuring that the poorly performing banks can improve because of a base on CBA’s

performance, there is a good market for the banking sector.

Question 3

a) Society and culture are the most popular discipline for the best-performing students. With a

proportion of 8,180 /221,060 ¿ 3.7 %

b) The number students studying society and culture and are on ATAR score of less than 80 would

be2814+2807+3906+5030=14,557. Therefore, the probability of selecting a student with

ATAR score less than 80 who is studying society and culture would be 14,557

221,060 =0.0658 .

c) Society and culture discipline has the highest proportion of students with the lowest ATAR

grades. The proportion of students studying society and culture and having ATAR score of less

than 50 is 2,814

221,060 =0.0127.

d) Health discipline has the highest proportion of students with the highest proportion of students

in the category of No ATAR/Non-Yr 12.

This is because students wishing to undertake any course in health discipline can be rated

based on their prerequisite studies.

Also, those who are of No ATAR category can be accepted in the health discipline through

mature entry option and be engaged on special tertiary examinations.

The pressure on lending generally affects the annual dividends differently on the banks.

For instance, CBA seems to be performing better than the other three based on the average

dividends per share and the range statistics. NAB, ANZ, and WBC are performing poorly as

compared to CBA. However, CBA has the highest variation of 24.32% in relation to 9.44%,

16.57% and 17.1% of NAB, ANZ, and WBC respectively. The lending pressure is aimed at

ensuring that the poorly performing banks can improve because of a base on CBA’s

performance, there is a good market for the banking sector.

Question 3

a) Society and culture are the most popular discipline for the best-performing students. With a

proportion of 8,180 /221,060 ¿ 3.7 %

b) The number students studying society and culture and are on ATAR score of less than 80 would

be2814+2807+3906+5030=14,557. Therefore, the probability of selecting a student with

ATAR score less than 80 who is studying society and culture would be 14,557

221,060 =0.0658 .

c) Society and culture discipline has the highest proportion of students with the lowest ATAR

grades. The proportion of students studying society and culture and having ATAR score of less

than 50 is 2,814

221,060 =0.0127.

d) Health discipline has the highest proportion of students with the highest proportion of students

in the category of No ATAR/Non-Yr 12.

This is because students wishing to undertake any course in health discipline can be rated

based on their prerequisite studies.

Also, those who are of No ATAR category can be accepted in the health discipline through

mature entry option and be engaged on special tertiary examinations.

DATA ANALYSIS ASSIGNMENT 9

Question 4

a) Probability of rain

i) Probability of no rain on any given week

λwk=0.007093

P ( 0 )= λwk

0

0 ! ∗e− λwk =e−λwk

¿ e−0.007093

¿ 0.9929

ii) The probability of having rain in two or more days of a week

¿ 1−P(0)−P(1)

¿ 1− ( 0.9929 )−(0.007093∗e−0.007093 )

¿ 1−0.9929−0.00704

¿ 0.00006

b) The 2016 annual rainfall for station number 23034 had a mean of 12.48 and a standard

deviation of 7.244.

i) The probability of having rain between 8mm and 16mm in a week.

P(between 8 mm∧16 mm)=P>8−P>16

Z( 8)=( 8−12.48

7.244 )=Z (−0.618)

P>8=1−0.2676=0.7324

Z ( 16 ) =16−12.48

7.244 =Z ( 0.4859 )

P>16=0.6844

Question 4

a) Probability of rain

i) Probability of no rain on any given week

λwk=0.007093

P ( 0 )= λwk

0

0 ! ∗e− λwk =e−λwk

¿ e−0.007093

¿ 0.9929

ii) The probability of having rain in two or more days of a week

¿ 1−P(0)−P(1)

¿ 1− ( 0.9929 )−(0.007093∗e−0.007093 )

¿ 1−0.9929−0.00704

¿ 0.00006

b) The 2016 annual rainfall for station number 23034 had a mean of 12.48 and a standard

deviation of 7.244.

i) The probability of having rain between 8mm and 16mm in a week.

P(between 8 mm∧16 mm)=P>8−P>16

Z( 8)=( 8−12.48

7.244 )=Z (−0.618)

P>8=1−0.2676=0.7324

Z ( 16 ) =16−12.48

7.244 =Z ( 0.4859 )

P>16=0.6844

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DATA ANALYSIS ASSIGNMENT 10

P ( of rainbetween 8 mm∧16 mm ) =0.7324−0.6844=0.048

ii)

Count of days Percent

Rain between 8mm and 16mm 21 12%

Rain >0 but <= 8 108 61.71%

Rain greater or equal to 16 7 4%

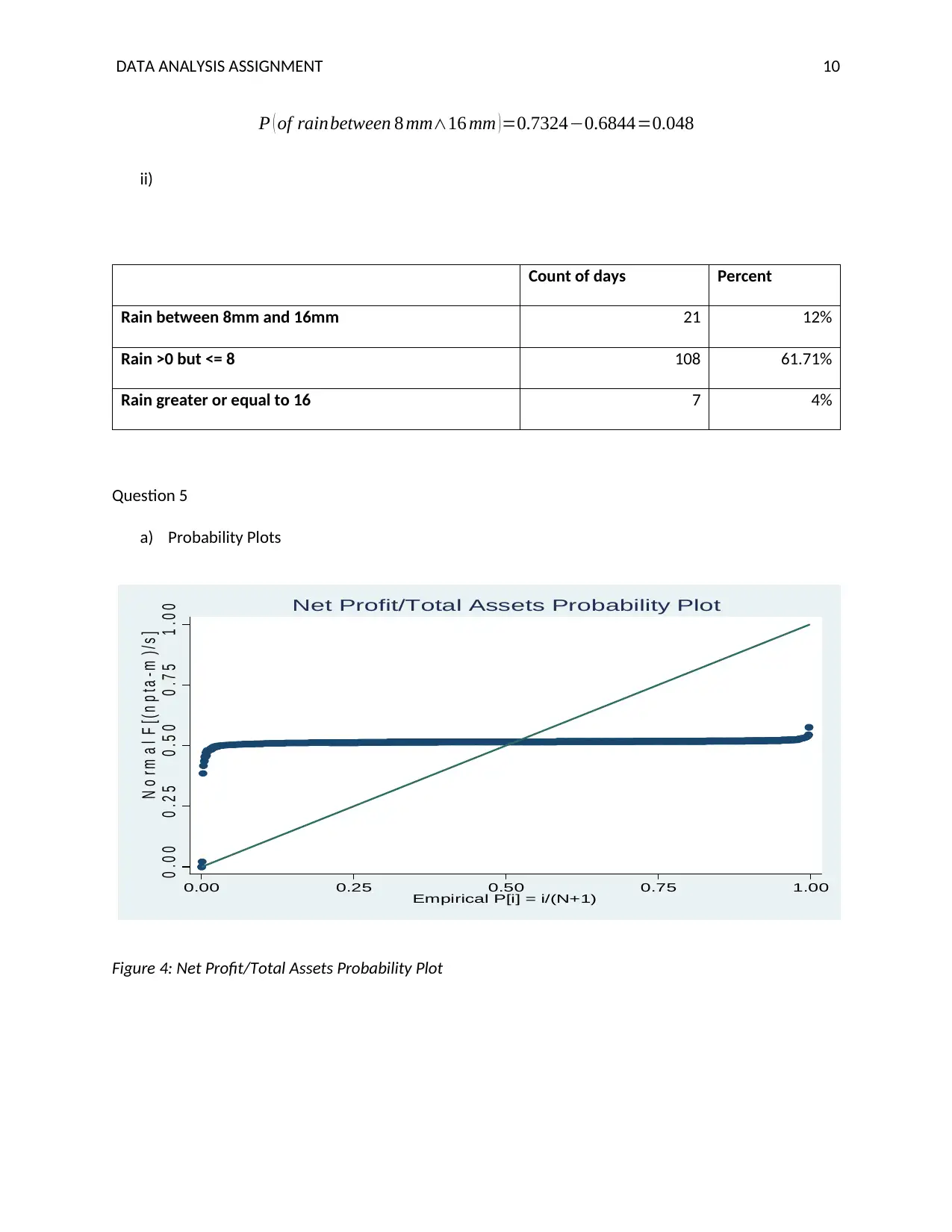

Question 5

a) Probability Plots

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( n p t a - m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Net Profit/Total Assets Probability Plot

Figure 4: Net Profit/Total Assets Probability Plot

P ( of rainbetween 8 mm∧16 mm ) =0.7324−0.6844=0.048

ii)

Count of days Percent

Rain between 8mm and 16mm 21 12%

Rain >0 but <= 8 108 61.71%

Rain greater or equal to 16 7 4%

Question 5

a) Probability Plots

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( n p t a - m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Net Profit/Total Assets Probability Plot

Figure 4: Net Profit/Total Assets Probability Plot

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

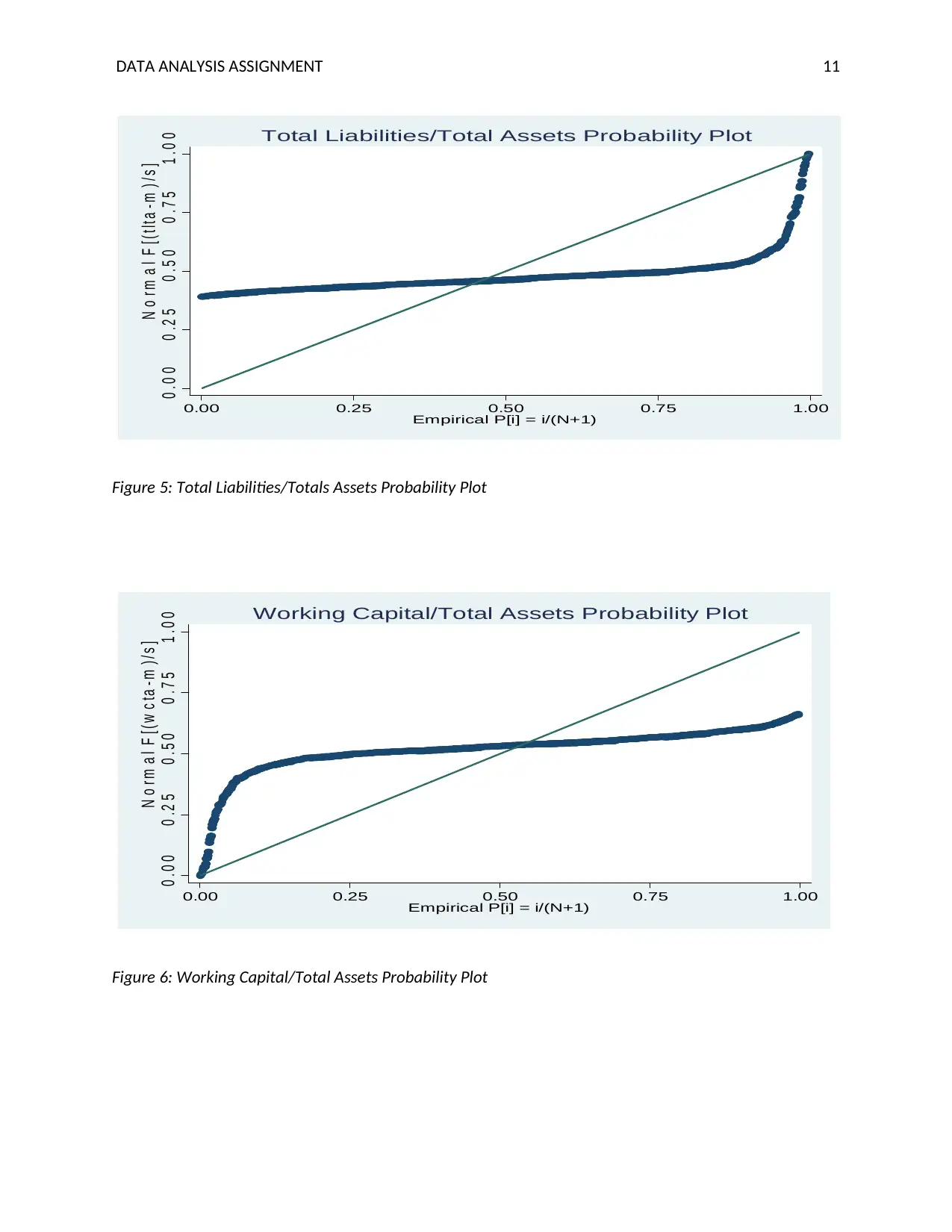

DATA ANALYSIS ASSIGNMENT 11

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( t l t a - m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Total Liabilities/Total Assets Probability Plot

Figure 5: Total Liabilities/Totals Assets Probability Plot

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( w c t a - m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Working Capital/Total Assets Probability Plot

Figure 6: Working Capital/Total Assets Probability Plot

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( t l t a - m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Total Liabilities/Total Assets Probability Plot

Figure 5: Total Liabilities/Totals Assets Probability Plot

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( w c t a - m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Working Capital/Total Assets Probability Plot

Figure 6: Working Capital/Total Assets Probability Plot

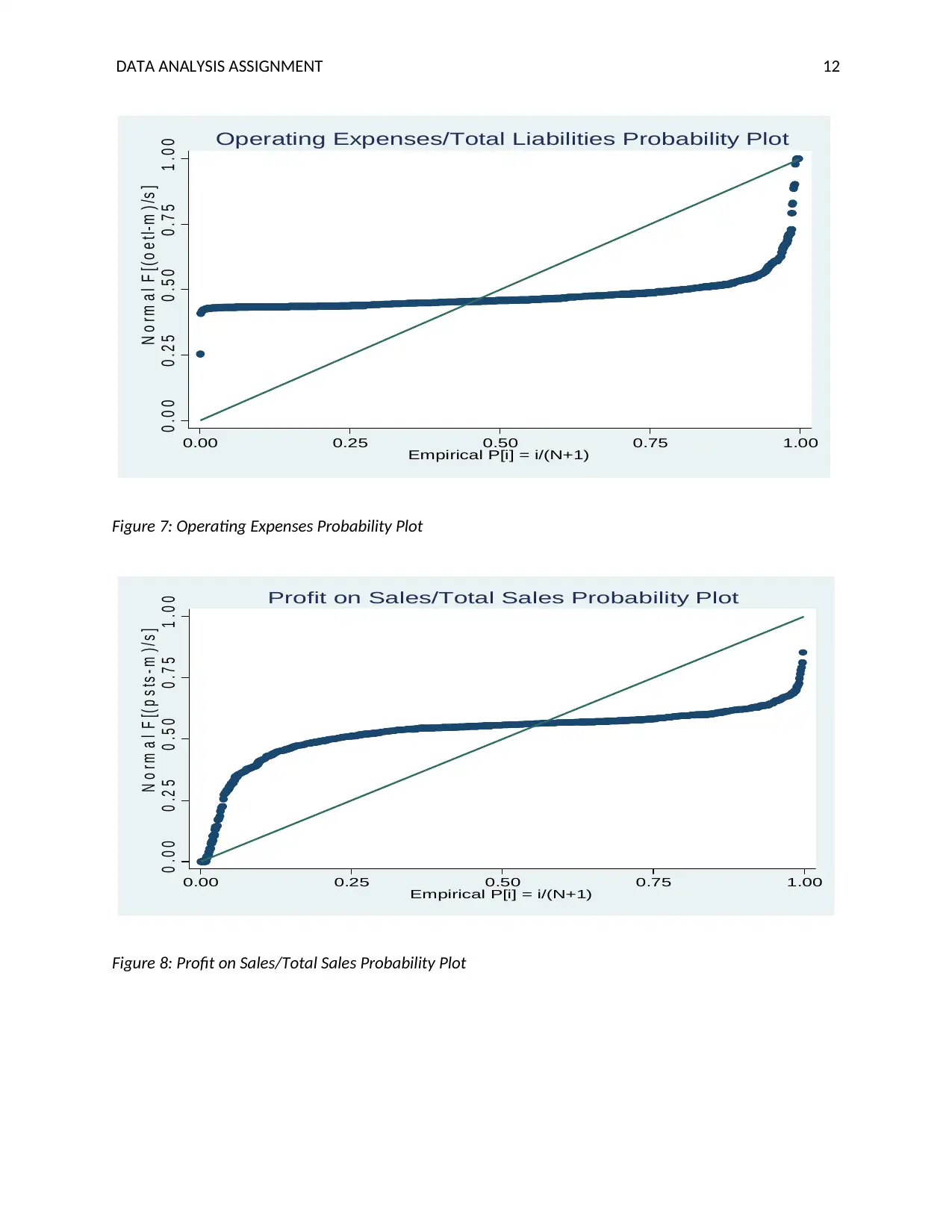

DATA ANALYSIS ASSIGNMENT 12

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( o e t l- m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Operating Expenses/Total Liabilities Probability Plot

Figure 7: Operating Expenses Probability Plot

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( p s t s - m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Profit on Sales/Total Sales Probability Plot

Figure 8: Profit on Sales/Total Sales Probability Plot

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( o e t l- m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Operating Expenses/Total Liabilities Probability Plot

Figure 7: Operating Expenses Probability Plot

0 . 0 0 0 . 2 5 0 . 5 0 0 . 7 5 1 . 0 0

N o r m a l F [ ( p s t s - m ) / s ]

0.00 0.25 0.50 0.75 1.00

Empirical P[i] = i/(N+1)

Profit on Sales/Total Sales Probability Plot

Figure 8: Profit on Sales/Total Sales Probability Plot

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17