Investment Strategies Project - Finance Module, Semester 1

VerifiedAdded on 2023/01/17

|12

|2831

|55

Project

AI Summary

This project comprehensively analyzes various investment strategies. It begins by calculating annualised interest rates for zero-coupon bonds and T-bills using semi-annual interest payments and roll-over strategies, considering changes in interest rates. The project then delves into technical analysis, explaining its application in trading currencies, managing foreign currency risk, and using historical data to predict price movements. The principles and application of carry trades are explored, including calculations based on New Zealand dollar and Japanese yen exchange rates. Furthermore, the project covers forward exchange rates, their calculation, and factors influencing them, along with the evaluation of premiums and discounts. The project concludes by comparing and contrasting option and forward rate strategies, using a case study involving an AUD/EUR currency pair and a hypothetical bid scenario. Finally, the project reflects on a group activity, outlining individual roles and collaborative efforts.

INVESTMENT STRATEGIES

INVESTMENT STRATEGIES

NAME OF STUDENT

NAME OF UNIVERSITY

INVESTMENT STRATEGIES

NAME OF STUDENT

NAME OF UNIVERSITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INVESTMENT STRATEGIES

Question 1.Annualised interest rate for zero coupon bonds and t-

bills

We will first calculate the intest payable by first calculating the

cuurent value of the bond. Interest is payable semi annually on bonds

and bills

Solution steps.

Step 1. How to find the current price of the bond

(Budgeting.thenest.com, 2019).

P = M / (1+r)n

where:

P = Current price of the bond

M = maturity value (We will use 100 for this case) .

r = investor's required annual yield / 2 (adjusted for semi annual

interest payments)

n = number of years until maturity x 2

a) Zero coupon rate

Interest on a one year zero coupon bond at a rate of 4,2%. Interest rate

will not change and interest earned in the first six months will not be

reinvested. Interest is payable over two times per year.

Calculation of interest on the face value.

Interest rate /100 x face value

4,2/100 *100= 4,2

Interest for the whole year is 4,2 ,divided by 2 to get the semi annual

rate is 2,1.

Annualised interest will be the compounded interest of the two

periods.

= ((1+0,021) X(1+0,021)) -1 = 0,021 or 2,1% per period or 4,2% per

year.

b) 6 month rolling strategy for the t-bill.

Using the 6 month roll over strategy at an interest rate of 4%.

Calculation of interest on the face value.

Interest rate /100 x face value

4/100 *100= 4

Interest for the whole year is 4 ,divided by 2 to get the semi annual

rate is 2.

The second six months the interest rate will be 5 ,divided by 2 =2,5%.

Annualised interest will be the compounded interest of the two

periods.

= ((1+0,02) X(1+0,025)) -1 = 0,0455 or 4,6% per year.

INVESTMENT STRATEGIES

Question 1.Annualised interest rate for zero coupon bonds and t-

bills

We will first calculate the intest payable by first calculating the

cuurent value of the bond. Interest is payable semi annually on bonds

and bills

Solution steps.

Step 1. How to find the current price of the bond

(Budgeting.thenest.com, 2019).

P = M / (1+r)n

where:

P = Current price of the bond

M = maturity value (We will use 100 for this case) .

r = investor's required annual yield / 2 (adjusted for semi annual

interest payments)

n = number of years until maturity x 2

a) Zero coupon rate

Interest on a one year zero coupon bond at a rate of 4,2%. Interest rate

will not change and interest earned in the first six months will not be

reinvested. Interest is payable over two times per year.

Calculation of interest on the face value.

Interest rate /100 x face value

4,2/100 *100= 4,2

Interest for the whole year is 4,2 ,divided by 2 to get the semi annual

rate is 2,1.

Annualised interest will be the compounded interest of the two

periods.

= ((1+0,021) X(1+0,021)) -1 = 0,021 or 2,1% per period or 4,2% per

year.

b) 6 month rolling strategy for the t-bill.

Using the 6 month roll over strategy at an interest rate of 4%.

Calculation of interest on the face value.

Interest rate /100 x face value

4/100 *100= 4

Interest for the whole year is 4 ,divided by 2 to get the semi annual

rate is 2.

The second six months the interest rate will be 5 ,divided by 2 =2,5%.

Annualised interest will be the compounded interest of the two

periods.

= ((1+0,02) X(1+0,025)) -1 = 0,0455 or 4,6% per year.

3

INVESTMENT STRATEGIES

c) If interest changes by a reduction of 1%.

Interest recievable if we reduce the rates by 1%

When interest rates reduce by 1% ,the only impact will be on the

rollover stategy for the last six month period. The new interest rate

will be (4-1)=3%

The interst eared on zero cuopun bond will not be affected by changes

in intret rates.

The second six months the interest rate will be

3 ,divided by 2 =1,5%.

Annualised interest will be the compounded

interest of the two periods.

= ((1+0,02) X(1+0,015)) -1 = 0,0353 or 3,5%

per year.

Rate of interest returns summarised

At 4,2% and 4% interest rates Annualised rate of return.

Zero coupon bond 4,2%

Rollover strategy and an increase of

1 % in the second half of the year. 4,6%

With a 1% reduction on interest rate

Zero coupon bond 4,2%

Rollover strategy 3,5%

The rollover strategy is very responsive to the changes in interest rate.

Question 2

a. Technical analysis application.

Technical analysis is a concept in investments and trading whose

basis is that past price activity trends like volumes and prices can be

used to predict current and future price movements of a stock or

commodity. The key data required for any conclusion of a trading

price is historical data.

Trading currencies is purely exchange of one currency for

another .The aim of this exchange is to make a profit from the change

in price of a currency pair. The traders will take a position on a

currency whose price is expected to change favourably. Once the

price of the currency has changed, the trader can then exchange the

currency with another currency whose price is favourable .The

exchange results in gains or losses.

Foreign currency risk arises when the exchange rate changes

adversely for transactions denominated in a foreign curreny . This risk

requires an enhaced level of management by an investor. The change

in foreign exchange can be frequent and unpredictable.

INVESTMENT STRATEGIES

c) If interest changes by a reduction of 1%.

Interest recievable if we reduce the rates by 1%

When interest rates reduce by 1% ,the only impact will be on the

rollover stategy for the last six month period. The new interest rate

will be (4-1)=3%

The interst eared on zero cuopun bond will not be affected by changes

in intret rates.

The second six months the interest rate will be

3 ,divided by 2 =1,5%.

Annualised interest will be the compounded

interest of the two periods.

= ((1+0,02) X(1+0,015)) -1 = 0,0353 or 3,5%

per year.

Rate of interest returns summarised

At 4,2% and 4% interest rates Annualised rate of return.

Zero coupon bond 4,2%

Rollover strategy and an increase of

1 % in the second half of the year. 4,6%

With a 1% reduction on interest rate

Zero coupon bond 4,2%

Rollover strategy 3,5%

The rollover strategy is very responsive to the changes in interest rate.

Question 2

a. Technical analysis application.

Technical analysis is a concept in investments and trading whose

basis is that past price activity trends like volumes and prices can be

used to predict current and future price movements of a stock or

commodity. The key data required for any conclusion of a trading

price is historical data.

Trading currencies is purely exchange of one currency for

another .The aim of this exchange is to make a profit from the change

in price of a currency pair. The traders will take a position on a

currency whose price is expected to change favourably. Once the

price of the currency has changed, the trader can then exchange the

currency with another currency whose price is favourable .The

exchange results in gains or losses.

Foreign currency risk arises when the exchange rate changes

adversely for transactions denominated in a foreign curreny . This risk

requires an enhaced level of management by an investor. The change

in foreign exchange can be frequent and unpredictable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

INVESTMENT STRATEGIES

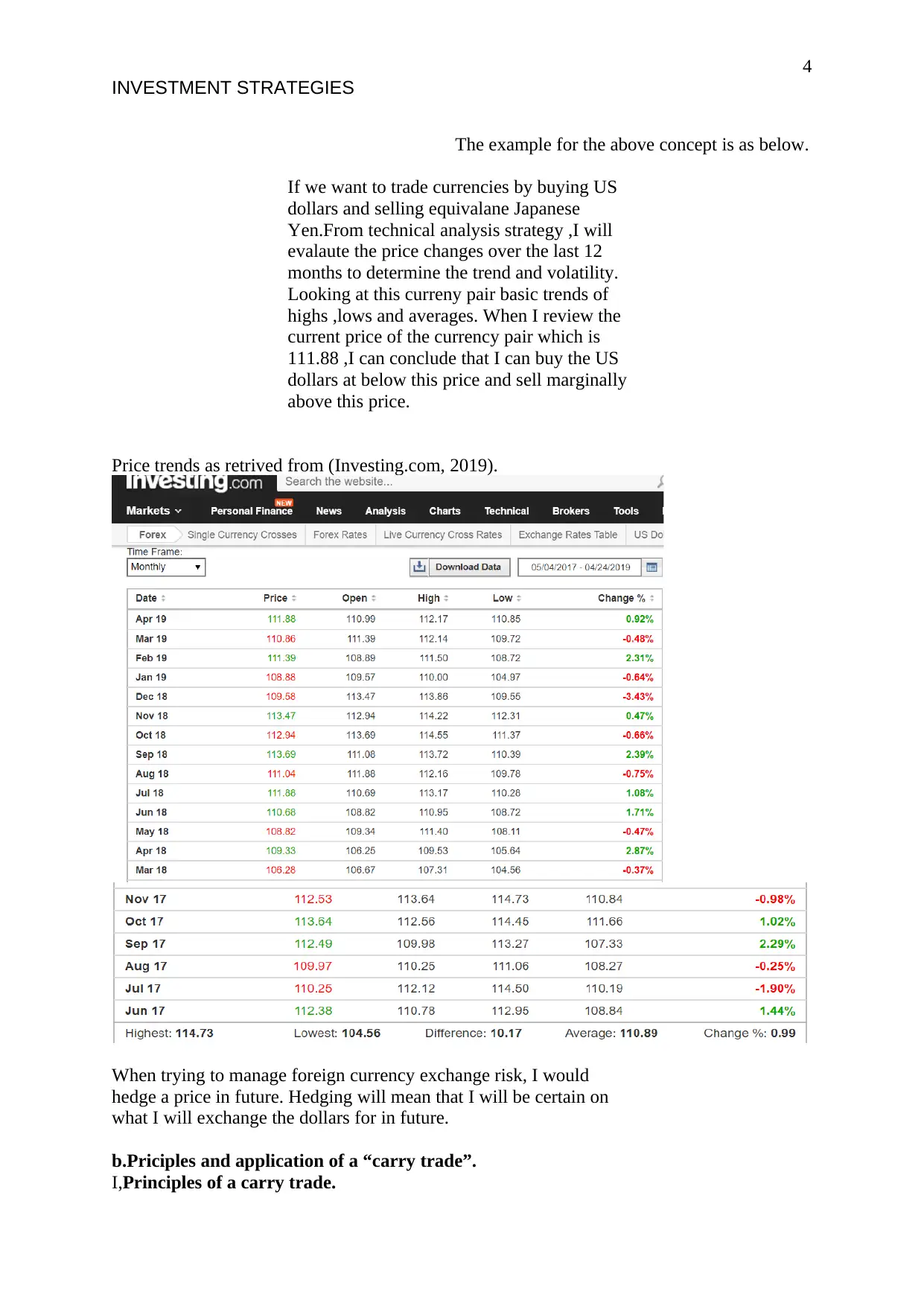

The example for the above concept is as below.

If we want to trade currencies by buying US

dollars and selling equivalane Japanese

Yen.From technical analysis strategy ,I will

evalaute the price changes over the last 12

months to determine the trend and volatility.

Looking at this curreny pair basic trends of

highs ,lows and averages. When I review the

current price of the currency pair which is

111.88 ,I can conclude that I can buy the US

dollars at below this price and sell marginally

above this price.

Price trends as retrived from (Investing.com, 2019).

When trying to manage foreign currency exchange risk, I would

hedge a price in future. Hedging will mean that I will be certain on

what I will exchange the dollars for in future.

b.Priciples and application of a “carry trade”.

I,Principles of a carry trade.

INVESTMENT STRATEGIES

The example for the above concept is as below.

If we want to trade currencies by buying US

dollars and selling equivalane Japanese

Yen.From technical analysis strategy ,I will

evalaute the price changes over the last 12

months to determine the trend and volatility.

Looking at this curreny pair basic trends of

highs ,lows and averages. When I review the

current price of the currency pair which is

111.88 ,I can conclude that I can buy the US

dollars at below this price and sell marginally

above this price.

Price trends as retrived from (Investing.com, 2019).

When trying to manage foreign currency exchange risk, I would

hedge a price in future. Hedging will mean that I will be certain on

what I will exchange the dollars for in future.

b.Priciples and application of a “carry trade”.

I,Principles of a carry trade.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

INVESTMENT STRATEGIES

Principles of a carry trade are ;

a) Buy a currency with a high interest rate by selling one with a

low interest rate.

This means the currency to be bought will have a high interest rate,

while the currency to fund this trade will have a low or lower

comparative interest rate.

b) The exchange rates between the currencies should be stable for the

expected profit to be made. If the exchange rate for the lower yielding

currency strengthens, the trader will book less profit or even book a

loss.

c) It is also expected that the interest rate spread for the two currencies

will be stable. If the interest rate spread shrinks, then the trader my

book a lesser margin or loss.

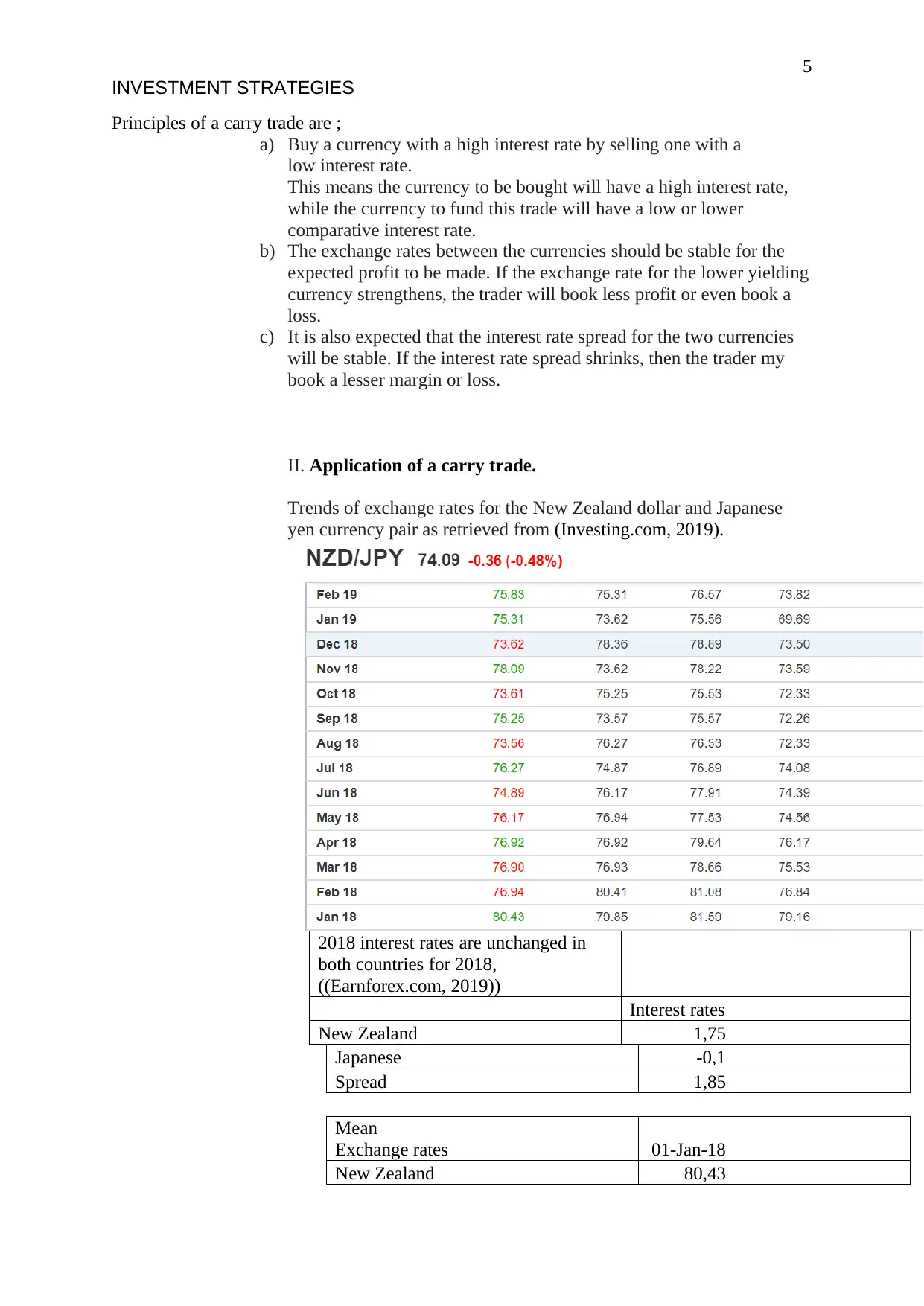

II. Application of a carry trade.

Trends of exchange rates for the New Zealand dollar and Japanese

yen currency pair as retrieved from (Investing.com, 2019).

2018 interest rates are unchanged in

both countries for 2018,

((Earnforex.com, 2019))

Interest rates

New Zealand 1,75

Japanese -0,1

Spread 1,85

Mean

Exchange rates 01-Jan-18

New Zealand 80,43

INVESTMENT STRATEGIES

Principles of a carry trade are ;

a) Buy a currency with a high interest rate by selling one with a

low interest rate.

This means the currency to be bought will have a high interest rate,

while the currency to fund this trade will have a low or lower

comparative interest rate.

b) The exchange rates between the currencies should be stable for the

expected profit to be made. If the exchange rate for the lower yielding

currency strengthens, the trader will book less profit or even book a

loss.

c) It is also expected that the interest rate spread for the two currencies

will be stable. If the interest rate spread shrinks, then the trader my

book a lesser margin or loss.

II. Application of a carry trade.

Trends of exchange rates for the New Zealand dollar and Japanese

yen currency pair as retrieved from (Investing.com, 2019).

2018 interest rates are unchanged in

both countries for 2018,

((Earnforex.com, 2019))

Interest rates

New Zealand 1,75

Japanese -0,1

Spread 1,85

Mean

Exchange rates 01-Jan-18

New Zealand 80,43

6

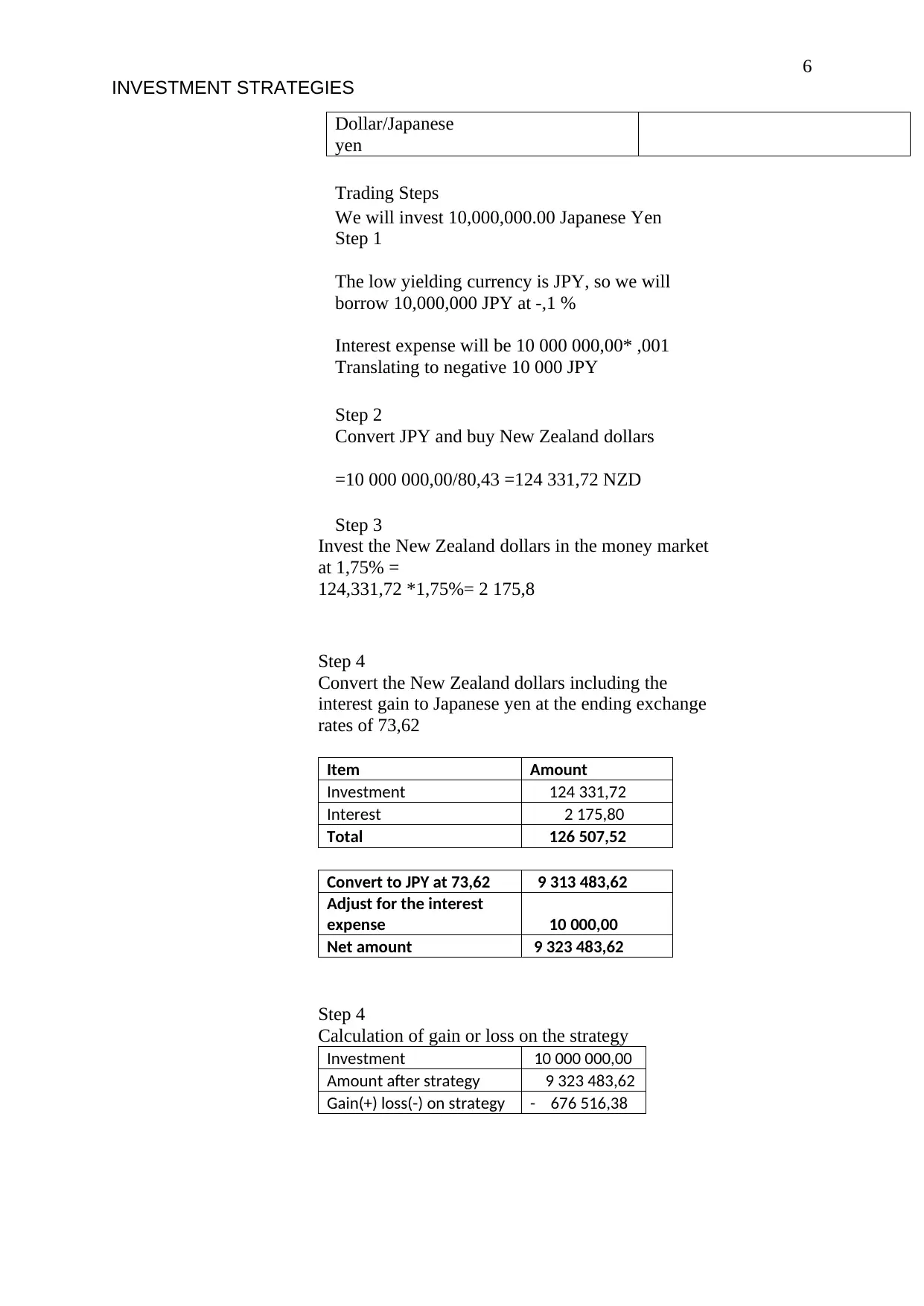

INVESTMENT STRATEGIES

Dollar/Japanese

yen

Trading Steps

We will invest 10,000,000.00 Japanese Yen

Step 1

The low yielding currency is JPY, so we will

borrow 10,000,000 JPY at -,1 %

Interest expense will be 10 000 000,00* ,001

Translating to negative 10 000 JPY

Step 2

Convert JPY and buy New Zealand dollars

=10 000 000,00/80,43 =124 331,72 NZD

Step 3

Invest the New Zealand dollars in the money market

at 1,75% =

124,331,72 *1,75%= 2 175,8

Step 4

Convert the New Zealand dollars including the

interest gain to Japanese yen at the ending exchange

rates of 73,62

Item Amount

Investment 124 331,72

Interest 2 175,80

Total 126 507,52

Convert to JPY at 73,62 9 313 483,62

Adjust for the interest

expense 10 000,00

Net amount 9 323 483,62

Step 4

Calculation of gain or loss on the strategy

Investment 10 000 000,00

Amount after strategy 9 323 483,62

Gain(+) loss(-) on strategy - 676 516,38

INVESTMENT STRATEGIES

Dollar/Japanese

yen

Trading Steps

We will invest 10,000,000.00 Japanese Yen

Step 1

The low yielding currency is JPY, so we will

borrow 10,000,000 JPY at -,1 %

Interest expense will be 10 000 000,00* ,001

Translating to negative 10 000 JPY

Step 2

Convert JPY and buy New Zealand dollars

=10 000 000,00/80,43 =124 331,72 NZD

Step 3

Invest the New Zealand dollars in the money market

at 1,75% =

124,331,72 *1,75%= 2 175,8

Step 4

Convert the New Zealand dollars including the

interest gain to Japanese yen at the ending exchange

rates of 73,62

Item Amount

Investment 124 331,72

Interest 2 175,80

Total 126 507,52

Convert to JPY at 73,62 9 313 483,62

Adjust for the interest

expense 10 000,00

Net amount 9 323 483,62

Step 4

Calculation of gain or loss on the strategy

Investment 10 000 000,00

Amount after strategy 9 323 483,62

Gain(+) loss(-) on strategy - 676 516,38

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

INVESTMENT STRATEGIES

The result is a loss as the Japanese Yen has strenghted agaist the New

Zeland dollar over the period.

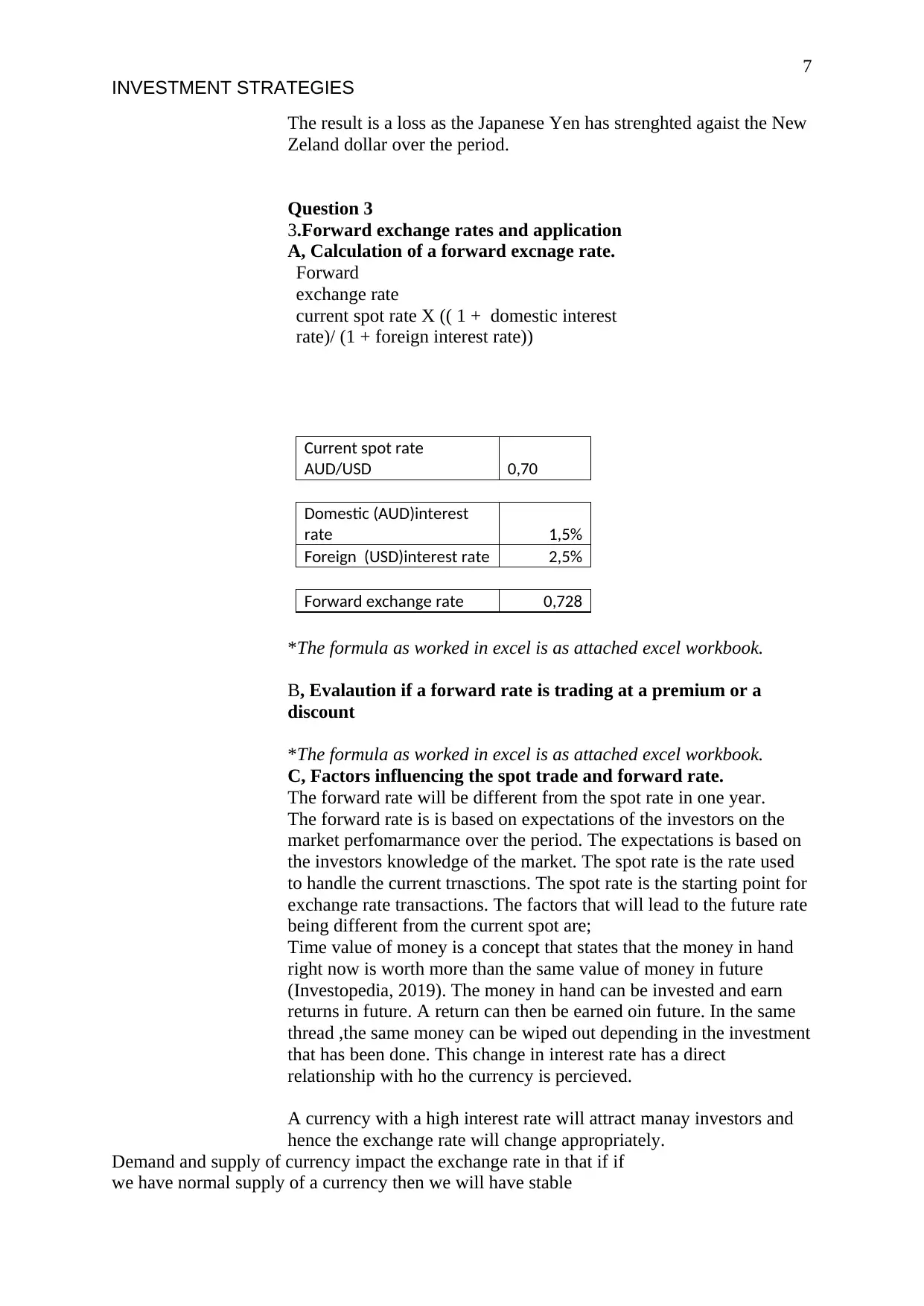

Question 3

3.Forward exchange rates and application

A, Calculation of a forward excnage rate.

Forward

exchange rate

current spot rate X (( 1 + domestic interest

rate)/ (1 + foreign interest rate))

Current spot rate

AUD/USD 0,70

Domestic (AUD)interest

rate 1,5%

Foreign (USD)interest rate 2,5%

Forward exchange rate 0,728

*The formula as worked in excel is as attached excel workbook.

B, Evalaution if a forward rate is trading at a premium or a

discount

*The formula as worked in excel is as attached excel workbook.

C, Factors influencing the spot trade and forward rate.

The forward rate will be different from the spot rate in one year.

The forward rate is is based on expectations of the investors on the

market perfomarmance over the period. The expectations is based on

the investors knowledge of the market. The spot rate is the rate used

to handle the current trnasctions. The spot rate is the starting point for

exchange rate transactions. The factors that will lead to the future rate

being different from the current spot are;

Time value of money is a concept that states that the money in hand

right now is worth more than the same value of money in future

(Investopedia, 2019). The money in hand can be invested and earn

returns in future. A return can then be earned oin future. In the same

thread ,the same money can be wiped out depending in the investment

that has been done. This change in interest rate has a direct

relationship with ho the currency is percieved.

A currency with a high interest rate will attract manay investors and

hence the exchange rate will change appropriately.

Demand and supply of currency impact the exchange rate in that if if

we have normal supply of a currency then we will have stable

INVESTMENT STRATEGIES

The result is a loss as the Japanese Yen has strenghted agaist the New

Zeland dollar over the period.

Question 3

3.Forward exchange rates and application

A, Calculation of a forward excnage rate.

Forward

exchange rate

current spot rate X (( 1 + domestic interest

rate)/ (1 + foreign interest rate))

Current spot rate

AUD/USD 0,70

Domestic (AUD)interest

rate 1,5%

Foreign (USD)interest rate 2,5%

Forward exchange rate 0,728

*The formula as worked in excel is as attached excel workbook.

B, Evalaution if a forward rate is trading at a premium or a

discount

*The formula as worked in excel is as attached excel workbook.

C, Factors influencing the spot trade and forward rate.

The forward rate will be different from the spot rate in one year.

The forward rate is is based on expectations of the investors on the

market perfomarmance over the period. The expectations is based on

the investors knowledge of the market. The spot rate is the rate used

to handle the current trnasctions. The spot rate is the starting point for

exchange rate transactions. The factors that will lead to the future rate

being different from the current spot are;

Time value of money is a concept that states that the money in hand

right now is worth more than the same value of money in future

(Investopedia, 2019). The money in hand can be invested and earn

returns in future. A return can then be earned oin future. In the same

thread ,the same money can be wiped out depending in the investment

that has been done. This change in interest rate has a direct

relationship with ho the currency is percieved.

A currency with a high interest rate will attract manay investors and

hence the exchange rate will change appropriately.

Demand and supply of currency impact the exchange rate in that if if

we have normal supply of a currency then we will have stable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

INVESTMENT STRATEGIES

exchange rate. If a currency is not readily available,then the cuency is

deemed scarce and will command a premuim to acquire.

Presence of speculators also leads to changes in exchange rates.

Exchange rates are driven by the volumes and treds of buying and

selling currencies. Speculators who have expectations of a chnge in

rate may take position in the market that will distort the prices. If a

speculator buys large quantiies fo a currency ,the market may respond

by buying the same currency and create a shortage and subsequnt rise

in the priceof such a currency.

Terms of trade wil affect the exchange rate .If a country is a net

exporter in referenceot a trading partner, then the that country,s

currency may be stronger than than the trading partner. Any changes

in the balance of trade will have an impact on bothe countries

exchange rates.

Political stability of ac ountry has a direct impact on the stability of

exchange rates .If a country is not stable politically its currency take a

hit in that it is weakens against other currencies.

D.Factors influencing changes in excnage rate.

Factors that lead to strengthening of the AUD USD exchange rate.

Interest rate apprecaion in Australia will lead strengthening of the

spot rate .In our exampe if the interest rate increase to 6% the

exchange rate can strengthen to .76. Alternatively if the US exchange

rate was to reduce to ,05% ,the exchange rate can weaken to ,71.

If the balance of payments between australia and US shifts

adversely ,then exchange rates will respond appropriately.

Question 4

4. Application of a suitable strategy between an option and

forward rate.

The Euro was introduced in 1999 and now has a membership of 17

European countries who have adoped it as their currency. AUD was

floated the dollar in 1983 to reflect the balance of payments and other

drivers f the market that affect the exchange rate.

The historical exchange rates for the AUD/EUR currency pair for the

last one year sho that the exchange rate was ,6327 as at April 2018

and is trading at ,6240 as at April 2019 (Investing.com, 2019). This

represents an appreciation of the EUR of (,6240-,6327)/,6327 = 1,4%.

This bid is made in Euros and this presents an exchange currency risk

in that there can be exposure in delivery of the project should the

exchange rates move be unfavourable. The risk is even more

enhanced given the payments are spread over three months intervals if

the bid is scucessful.

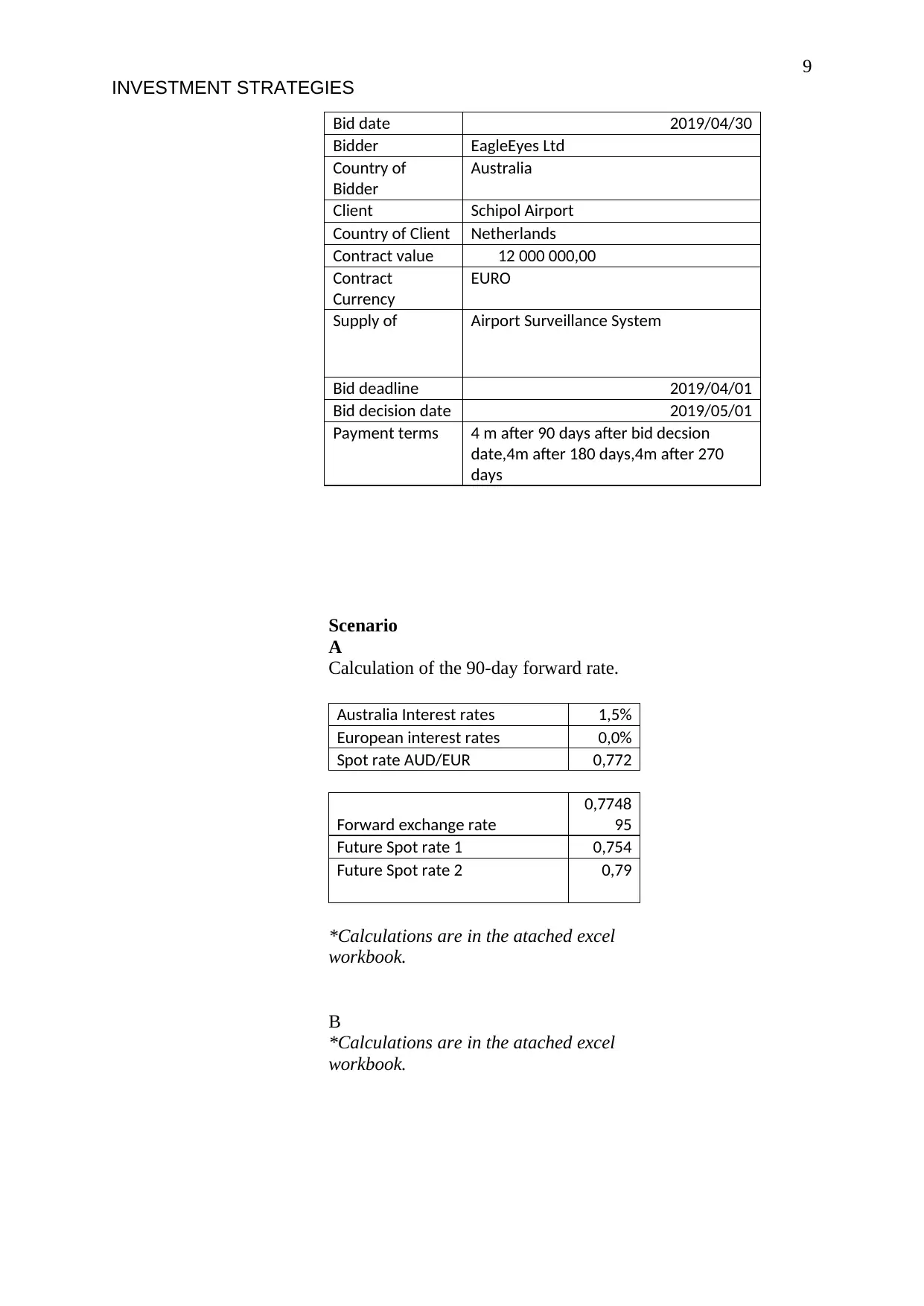

The bid

INVESTMENT STRATEGIES

exchange rate. If a currency is not readily available,then the cuency is

deemed scarce and will command a premuim to acquire.

Presence of speculators also leads to changes in exchange rates.

Exchange rates are driven by the volumes and treds of buying and

selling currencies. Speculators who have expectations of a chnge in

rate may take position in the market that will distort the prices. If a

speculator buys large quantiies fo a currency ,the market may respond

by buying the same currency and create a shortage and subsequnt rise

in the priceof such a currency.

Terms of trade wil affect the exchange rate .If a country is a net

exporter in referenceot a trading partner, then the that country,s

currency may be stronger than than the trading partner. Any changes

in the balance of trade will have an impact on bothe countries

exchange rates.

Political stability of ac ountry has a direct impact on the stability of

exchange rates .If a country is not stable politically its currency take a

hit in that it is weakens against other currencies.

D.Factors influencing changes in excnage rate.

Factors that lead to strengthening of the AUD USD exchange rate.

Interest rate apprecaion in Australia will lead strengthening of the

spot rate .In our exampe if the interest rate increase to 6% the

exchange rate can strengthen to .76. Alternatively if the US exchange

rate was to reduce to ,05% ,the exchange rate can weaken to ,71.

If the balance of payments between australia and US shifts

adversely ,then exchange rates will respond appropriately.

Question 4

4. Application of a suitable strategy between an option and

forward rate.

The Euro was introduced in 1999 and now has a membership of 17

European countries who have adoped it as their currency. AUD was

floated the dollar in 1983 to reflect the balance of payments and other

drivers f the market that affect the exchange rate.

The historical exchange rates for the AUD/EUR currency pair for the

last one year sho that the exchange rate was ,6327 as at April 2018

and is trading at ,6240 as at April 2019 (Investing.com, 2019). This

represents an appreciation of the EUR of (,6240-,6327)/,6327 = 1,4%.

This bid is made in Euros and this presents an exchange currency risk

in that there can be exposure in delivery of the project should the

exchange rates move be unfavourable. The risk is even more

enhanced given the payments are spread over three months intervals if

the bid is scucessful.

The bid

9

INVESTMENT STRATEGIES

Bid date 2019/04/30

Bidder EagleEyes Ltd

Country of

Bidder

Australia

Client Schipol Airport

Country of Client Netherlands

Contract value 12 000 000,00

Contract

Currency

EURO

Supply of Airport Surveillance System

Bid deadline 2019/04/01

Bid decision date 2019/05/01

Payment terms 4 m after 90 days after bid decsion

date,4m after 180 days,4m after 270

days

Scenario

A

Calculation of the 90-day forward rate.

Australia Interest rates 1,5%

European interest rates 0,0%

Spot rate AUD/EUR 0,772

Forward exchange rate

0,7748

95

Future Spot rate 1 0,754

Future Spot rate 2 0,79

*Calculations are in the atached excel

workbook.

B

*Calculations are in the atached excel

workbook.

INVESTMENT STRATEGIES

Bid date 2019/04/30

Bidder EagleEyes Ltd

Country of

Bidder

Australia

Client Schipol Airport

Country of Client Netherlands

Contract value 12 000 000,00

Contract

Currency

EURO

Supply of Airport Surveillance System

Bid deadline 2019/04/01

Bid decision date 2019/05/01

Payment terms 4 m after 90 days after bid decsion

date,4m after 180 days,4m after 270

days

Scenario

A

Calculation of the 90-day forward rate.

Australia Interest rates 1,5%

European interest rates 0,0%

Spot rate AUD/EUR 0,772

Forward exchange rate

0,7748

95

Future Spot rate 1 0,754

Future Spot rate 2 0,79

*Calculations are in the atached excel

workbook.

B

*Calculations are in the atached excel

workbook.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

INVESTMENT STRATEGIES

Question 5.

5.Reflections from the group activity.

My group had five members and each was assigned one question

while one member was tasked with being a secretary and enforcer.

The secretary was also tasked with conflict resolution .The primary

resposibilty of the secretary was to make sure we delivered the

assignment in time and in the prescribed manner. The questions were

allocated on the strength of each member depending on the question.

However ,when a question did not have a taker ,the group reassigned

the question in an amicable way. Every one then took his favourite

topic.

We agreed on the rules ,including timelines of reporting on

milestones. On a weekly basis ,each member was to update the group

on where thay had reached. The group was also meeting on weekly

basis on Tuesday afternoon for one hour . You had to attend and if not

in a position to attend you were to give a days notice and hand in your

progress report. The consequencies of not abiding were that you

would not be welcome in that group or individuals in future.

The weekly meetings were to review the progress of each member.

Each member would present their workings including references.

Each member had to use illustrations for ease of understanding. The

member had to clarify any query from another member ,till the

member who had queried was satisfied.

The main problem we encountered was on

having simple illustrations that would make

understanding these concepts easier. However

we spent a lot of time on going through a

number of illustrations ,including real life case

studies. The other problem was on time

keeping where many members were not

sticking to the stipulated timelines. We

resolved this by rejecting the submissions of

such members. The affected members simply

pulled up their socks and were not late in

subsequent submissions.

INVESTMENT STRATEGIES

Question 5.

5.Reflections from the group activity.

My group had five members and each was assigned one question

while one member was tasked with being a secretary and enforcer.

The secretary was also tasked with conflict resolution .The primary

resposibilty of the secretary was to make sure we delivered the

assignment in time and in the prescribed manner. The questions were

allocated on the strength of each member depending on the question.

However ,when a question did not have a taker ,the group reassigned

the question in an amicable way. Every one then took his favourite

topic.

We agreed on the rules ,including timelines of reporting on

milestones. On a weekly basis ,each member was to update the group

on where thay had reached. The group was also meeting on weekly

basis on Tuesday afternoon for one hour . You had to attend and if not

in a position to attend you were to give a days notice and hand in your

progress report. The consequencies of not abiding were that you

would not be welcome in that group or individuals in future.

The weekly meetings were to review the progress of each member.

Each member would present their workings including references.

Each member had to use illustrations for ease of understanding. The

member had to clarify any query from another member ,till the

member who had queried was satisfied.

The main problem we encountered was on

having simple illustrations that would make

understanding these concepts easier. However

we spent a lot of time on going through a

number of illustrations ,including real life case

studies. The other problem was on time

keeping where many members were not

sticking to the stipulated timelines. We

resolved this by rejecting the submissions of

such members. The affected members simply

pulled up their socks and were not late in

subsequent submissions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

INVESTMENT STRATEGIES

Our strategy worked in that despite the slow start ,we were able to

achieve much in the second week . We even had time to do reflections

during our last meeting.

My take from this group exercise is on the resourcefulnes of a group.

We were able to have many opinions on the understanding of varous

concepts. The sum of these opinions was very insightful. We were

able to meet the deadlines through use of a penalty which is very

punitive. No member would have wished to be blacklisted as the

consequencies were to be carried over from this unit.

The real life applications of this group assignment is in the power of

collective responsibilty .We can achieve so much if we work together

as a group. I also leant on the role of having guidleines to guide on

behavoiur .Thse are used to measure progress and evaluate

acountability.

INVESTMENT STRATEGIES

Our strategy worked in that despite the slow start ,we were able to

achieve much in the second week . We even had time to do reflections

during our last meeting.

My take from this group exercise is on the resourcefulnes of a group.

We were able to have many opinions on the understanding of varous

concepts. The sum of these opinions was very insightful. We were

able to meet the deadlines through use of a penalty which is very

punitive. No member would have wished to be blacklisted as the

consequencies were to be carried over from this unit.

The real life applications of this group assignment is in the power of

collective responsibilty .We can achieve so much if we work together

as a group. I also leant on the role of having guidleines to guide on

behavoiur .Thse are used to measure progress and evaluate

acountability.

12

INVESTMENT STRATEGIES

References.

Budgeting.thenest.com. (2019). How to Find the Interest Rate on a Bond. [online] Available

at: https://budgeting.thenest.com/interest-rate-bond-3654.html [Accessed 29 Apr. 2019].

Earnforex.com. (2019). Interest Rates Table. [online] Available at:

https://www.earnforex.com/interest-rates-table/ [Accessed 29 Apr. 2019].

Investing.com. (2019). USD JPY Historical Data - Investing.com. [online] Available at:

https://www.investing.com/currencies/usd-jpy-historical-data [Accessed 29 Apr. 2019].

Investopedia. (2019). Currency Appreciation Definition. [online] Available at:

https://www.investopedia.com/terms/c/currency-appreciation.asp [Accessed 29 Apr. 2019].

INVESTMENT STRATEGIES

References.

Budgeting.thenest.com. (2019). How to Find the Interest Rate on a Bond. [online] Available

at: https://budgeting.thenest.com/interest-rate-bond-3654.html [Accessed 29 Apr. 2019].

Earnforex.com. (2019). Interest Rates Table. [online] Available at:

https://www.earnforex.com/interest-rates-table/ [Accessed 29 Apr. 2019].

Investing.com. (2019). USD JPY Historical Data - Investing.com. [online] Available at:

https://www.investing.com/currencies/usd-jpy-historical-data [Accessed 29 Apr. 2019].

Investopedia. (2019). Currency Appreciation Definition. [online] Available at:

https://www.investopedia.com/terms/c/currency-appreciation.asp [Accessed 29 Apr. 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.