Determinants of ISO 9000 Adoption & Impact on Firm Performance

VerifiedAdded on 2023/06/11

|32

|7643

|483

Report

AI Summary

This report investigates the operational significance of ISO 9000 and its impact on firm performance, using a speculative model to analyze benefits related to quality management. It explores the determinants of ISO 9000 adoption, considering factors like quality improvement, cost reduction, and innovation, while also addressing the nuances of compliance and the varying adoption patterns across different countries. The study uses statistical and regression analysis on Chinese firms to determine how ISO certification and ownership structure affect firm performance, finding that the positive impact of ISO certification diminishes in firms with ownership issues. Furthermore, the research differentiates the determinants of ISO 9000 certification between manufacturing and service sectors, highlighting the varying importance of factors like quality change, cost reduction, and advancement in these sectors. Ultimately, the findings aim to inform policymakers in effectively applying controls that impact the business success of firms in both manufacturing and service industries.

1

Impact of ISO 9000 on

Performance of Firms

Impact of ISO 9000 on

Performance of Firms

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

1.0 Executive Summary

The inspiration driving this paper was to develop the operational significance of ISO 9000, a

speculative model which will investigate the benefits in analyze on quality organization. A

course of action of specific components and sub-factors for tasks of the ISO 9000 compliance

were proposed. Not executing the consistency and getting a charge out of the offices of the

standards rather was an unquestionably essential point, as in past works found in the writing

in various countries, the conclusion was drawn that affiliations don't grasp ISO 9000

homogeneously. The conclusions may be of interest both for insightful and capable circles of

development. Initially, the key parts of a substantive choice of ISO 9000 were included. For

scholastics, certain specific request segments were proposed for a critical form so that these

may be used as a piece of coming works. ISO accreditation has transformed into an inevitable

instrument got by firms to improve their operational execution. In this paper, we take a

gander at the operational and legitimate factors that enhance the likelihood of getting ISO

confirmation and the impact that ISO affirmation and proprietorship structure have upon firm

execution. Regardless, the results demonstrate that the beneficial outcome of ISO

confirmation on execution diminishes in firms where ownership was an issue. One of a kind

survey data on Chinese firms was inspected, regardless of whether there was a qualification

in the determinants of International Organization for Standardization 9000 confirmation

between the vital elements for development and organization portions. Using an exploratory

approach, revelations reveal out that the elements of ISO 9000 affirmation in a general sense

differ among worker and organization elements of the organizations, especially for quality

change, cost diminishment and advancement of these associations. The outcomes of this

examination could enable policy makers to better detail and sufficiently apply controls

impacting the business achievement of firms in both the collecting and organization portions.

Table of Contents

1.0 Executive Summary

The inspiration driving this paper was to develop the operational significance of ISO 9000, a

speculative model which will investigate the benefits in analyze on quality organization. A

course of action of specific components and sub-factors for tasks of the ISO 9000 compliance

were proposed. Not executing the consistency and getting a charge out of the offices of the

standards rather was an unquestionably essential point, as in past works found in the writing

in various countries, the conclusion was drawn that affiliations don't grasp ISO 9000

homogeneously. The conclusions may be of interest both for insightful and capable circles of

development. Initially, the key parts of a substantive choice of ISO 9000 were included. For

scholastics, certain specific request segments were proposed for a critical form so that these

may be used as a piece of coming works. ISO accreditation has transformed into an inevitable

instrument got by firms to improve their operational execution. In this paper, we take a

gander at the operational and legitimate factors that enhance the likelihood of getting ISO

confirmation and the impact that ISO affirmation and proprietorship structure have upon firm

execution. Regardless, the results demonstrate that the beneficial outcome of ISO

confirmation on execution diminishes in firms where ownership was an issue. One of a kind

survey data on Chinese firms was inspected, regardless of whether there was a qualification

in the determinants of International Organization for Standardization 9000 confirmation

between the vital elements for development and organization portions. Using an exploratory

approach, revelations reveal out that the elements of ISO 9000 affirmation in a general sense

differ among worker and organization elements of the organizations, especially for quality

change, cost diminishment and advancement of these associations. The outcomes of this

examination could enable policy makers to better detail and sufficiently apply controls

impacting the business achievement of firms in both the collecting and organization portions.

Table of Contents

3

1.0 Executive Summary................................................................................................................................. 2

2.0 Introduction................................................................................................................................................ 3

3.0 Literature Review..................................................................................................................................... 5

4.0 Methodology............................................................................................................................................... 8

5.0 Data Analysis.............................................................................................................................................. 9

5.1 Data............................................................................................................................................................ 9

5.2 Variables.................................................................................................................................................. 9

5.3 Descriptive Analysis......................................................................................................................... 10

5.4 Statistical Analysis............................................................................................................................ 14

5.5 Regression Model.............................................................................................................................. 16

6.0 Discussion and Recommendations................................................................................................. 18

7.0 Limitation and Future scope............................................................................................................. 20

8.0 References................................................................................................................................................ 22

9.0 Appendix A............................................................................................................................................... 27

9.1 Appendix B............................................................................................................................................... 28

9.2 Appendix C: Regression Model (Sales).......................................................................................... 31

9.3 Appendix: Regression Model (Profits).......................................................................................... 32

1.0 Executive Summary................................................................................................................................. 2

2.0 Introduction................................................................................................................................................ 3

3.0 Literature Review..................................................................................................................................... 5

4.0 Methodology............................................................................................................................................... 8

5.0 Data Analysis.............................................................................................................................................. 9

5.1 Data............................................................................................................................................................ 9

5.2 Variables.................................................................................................................................................. 9

5.3 Descriptive Analysis......................................................................................................................... 10

5.4 Statistical Analysis............................................................................................................................ 14

5.5 Regression Model.............................................................................................................................. 16

6.0 Discussion and Recommendations................................................................................................. 18

7.0 Limitation and Future scope............................................................................................................. 20

8.0 References................................................................................................................................................ 22

9.0 Appendix A............................................................................................................................................... 27

9.1 Appendix B............................................................................................................................................... 28

9.2 Appendix C: Regression Model (Sales).......................................................................................... 31

9.3 Appendix: Regression Model (Profits).......................................................................................... 32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

2.0 Introduction

Firms don't act self-rousingly in light of the way that they depend upon the legitimacy

constrained by institutional circumstances. In this way, they were constrained to solidify

fundamental segments, practices, techniques, and frameworks that were considered as a target

means to recognize various levelled goals. A segment of these requirements could be expert

by the gathering of money related structures, the hugeness of which has turned out to be

gigantically imperative in the latest decade. An affirmation of money related systems has

been credited in exceptional part to the furthest reaches of those structures, to advance the

presence of the foundation of an overwhelmingly engaged circumstance. The International

Organization for Standardization arranged the ISO 9000 accreditation that decides necessities

for a quality organization structure to demonstrate that a firm agrees to the customer and

regulatory requirements. ISO Survey of Certifications 2013 affirms around 1,129,000 firms

which have been affirmed worldwide to ISO 9000 benchmarks in 189 nations. In this manner,

the essential issue of enthusiasm for the institutional money related work has been the

legitimacy and adequacy control, for instance, ISO 9000 affirmation. Regardless of that, a

number of observational examinations have gone over to make sense of the variables of the

ISO 9000 confirmation (Lo et al., 2013). Studies of such degree were compulsory and basic

in light of the way that hypothetically stranded observational investigation centre into the

variables of ISO 9000. Insistence can contribute important bits of information into firms'

legitimate guide by illuminating why certain sorts of firms search for ISO 9000 attestation

while others don't. Firms were embracing for ISO 9000 accreditation even with less number

of clients. Despite the fact that there was insufficient centrality for each industry area, still,

ISO 9000 certification encourages to develop the business from numerous edges.

Universal authentic gauges have been proposed as an administration instrument for corporate

conduct where government direction was probably not going to be powerful. Norms of the

ISO 14000 natural administration framework standard and the SA 8000 social responsibility

standard can add to firm self-control by indicating necessities that go past the government

directions. These guidelines were not created and authorized by governments, but rather by

non-administrative partner bunch, including the International Organization for

Standardization (ISO) and banking associations. Firms can get standard affirmation by

autonomous outsider inspectors who check a company's consistency with standard

2.0 Introduction

Firms don't act self-rousingly in light of the way that they depend upon the legitimacy

constrained by institutional circumstances. In this way, they were constrained to solidify

fundamental segments, practices, techniques, and frameworks that were considered as a target

means to recognize various levelled goals. A segment of these requirements could be expert

by the gathering of money related structures, the hugeness of which has turned out to be

gigantically imperative in the latest decade. An affirmation of money related systems has

been credited in exceptional part to the furthest reaches of those structures, to advance the

presence of the foundation of an overwhelmingly engaged circumstance. The International

Organization for Standardization arranged the ISO 9000 accreditation that decides necessities

for a quality organization structure to demonstrate that a firm agrees to the customer and

regulatory requirements. ISO Survey of Certifications 2013 affirms around 1,129,000 firms

which have been affirmed worldwide to ISO 9000 benchmarks in 189 nations. In this manner,

the essential issue of enthusiasm for the institutional money related work has been the

legitimacy and adequacy control, for instance, ISO 9000 affirmation. Regardless of that, a

number of observational examinations have gone over to make sense of the variables of the

ISO 9000 confirmation (Lo et al., 2013). Studies of such degree were compulsory and basic

in light of the way that hypothetically stranded observational investigation centre into the

variables of ISO 9000. Insistence can contribute important bits of information into firms'

legitimate guide by illuminating why certain sorts of firms search for ISO 9000 attestation

while others don't. Firms were embracing for ISO 9000 accreditation even with less number

of clients. Despite the fact that there was insufficient centrality for each industry area, still,

ISO 9000 certification encourages to develop the business from numerous edges.

Universal authentic gauges have been proposed as an administration instrument for corporate

conduct where government direction was probably not going to be powerful. Norms of the

ISO 14000 natural administration framework standard and the SA 8000 social responsibility

standard can add to firm self-control by indicating necessities that go past the government

directions. These guidelines were not created and authorized by governments, but rather by

non-administrative partner bunch, including the International Organization for

Standardization (ISO) and banking associations. Firms can get standard affirmation by

autonomous outsider inspectors who check a company's consistency with standard

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

prerequisites. Firms can utilize affirmations in promoting their items. Accordingly, this

administration component depends on the suspicion that organizations will wilfully embrace

these benchmarks since it was useful for business, on the grounds that clients want to buy

items from affirmed providers (Gabriel & Lang, 2015).

For authentic norms to be a compelling administration system for firm self-control, ISO

regulated firms need to agree to the standard's necessities. Most exact research on authentic

models regards confirmation as a double factor estimating the appropriation of the practices

determined by the ISO standard (Drori, Höllerer & Walgenbach, 2014). This accepts that the

demonstration of affirmation was identified with the real execution of the predefined

practises. Inquiries regarding inspector capability, reviewer freedom and the intermittent idea

of reviews raise worries about the adequacy of outsider affirmations (Aravind & Christmann,

2011). It was conceivable that organizations could acquire standard affirmation to show their

responsibility to capable natural direct and working conditions while decoupling accreditation

from genuine practices (Shi Congmei, 2010). Late research has demonstrated that numerous

organizations that do that don't conform to a standard's necessities on a progressing premise

can at present pass occasional reviews for proceeded with confirmation (Boiral & Paillé,

2012). These discoveries question the quality of the connection amongst confirmation and the

execution of the ensured rehearses and the viability of authentic measures as an

administration system.

3.0 Literature Review

Theoretical structure, composing a review and research question point out that disguise of the

ISO 9000 standard includes a dynamic use of concealed practices to change direct and

fundamental initiative (Abe, Bassett & Dempsey, 2012). One of the theoretical structures that

have been progressed in this written work was to look at the interrelationships between ISO

9000 and progress data of the organization. They keep up that organization system. Those

disguised the QM structures (QMS) of ISO 9001 rules; contain unequivocal and undeniable

sorts of embedded data (Martínez-Costa et al., 2009). Information advances toward getting to

be realized when it was deciphered by individuals, given a particular situation, and moored

into the feelings and obligations of individuals (Beitsch, Yeager and Moran, 2015). Cross

sectional analysis of firm’s data was an objective and adjusted learning that addressed the

prerequisites. Firms can utilize affirmations in promoting their items. Accordingly, this

administration component depends on the suspicion that organizations will wilfully embrace

these benchmarks since it was useful for business, on the grounds that clients want to buy

items from affirmed providers (Gabriel & Lang, 2015).

For authentic norms to be a compelling administration system for firm self-control, ISO

regulated firms need to agree to the standard's necessities. Most exact research on authentic

models regards confirmation as a double factor estimating the appropriation of the practices

determined by the ISO standard (Drori, Höllerer & Walgenbach, 2014). This accepts that the

demonstration of affirmation was identified with the real execution of the predefined

practises. Inquiries regarding inspector capability, reviewer freedom and the intermittent idea

of reviews raise worries about the adequacy of outsider affirmations (Aravind & Christmann,

2011). It was conceivable that organizations could acquire standard affirmation to show their

responsibility to capable natural direct and working conditions while decoupling accreditation

from genuine practices (Shi Congmei, 2010). Late research has demonstrated that numerous

organizations that do that don't conform to a standard's necessities on a progressing premise

can at present pass occasional reviews for proceeded with confirmation (Boiral & Paillé,

2012). These discoveries question the quality of the connection amongst confirmation and the

execution of the ensured rehearses and the viability of authentic measures as an

administration system.

3.0 Literature Review

Theoretical structure, composing a review and research question point out that disguise of the

ISO 9000 standard includes a dynamic use of concealed practices to change direct and

fundamental initiative (Abe, Bassett & Dempsey, 2012). One of the theoretical structures that

have been progressed in this written work was to look at the interrelationships between ISO

9000 and progress data of the organization. They keep up that organization system. Those

disguised the QM structures (QMS) of ISO 9001 rules; contain unequivocal and undeniable

sorts of embedded data (Martínez-Costa et al., 2009). Information advances toward getting to

be realized when it was deciphered by individuals, given a particular situation, and moored

into the feelings and obligations of individuals (Beitsch, Yeager and Moran, 2015). Cross

sectional analysis of firm’s data was an objective and adjusted learning that addressed the

6

systematized interpretation of the information that can be secured and transmitted

(Rafiquzzaman et al., 2017). The creativeness and institutional effect of ISO 9000 was

evident from the adoption by the small and medium firms in China (Du, Yin and Zhang,

2016). As it was particularly critical to the examination of ISO 9000 benchmarks as it

addressed the route toward holding both understood and unequivocal information into the

affiliation and making an understanding of it into statistical process control data (Dahlgaard,

Khanji and Kristensen, 2008). As underlined, QMS proposed by ISO 9001 can be seen as one

kind of encoded data and can urge figuring out how to store, data trade, in conclusion,

learning application (Ahmed, 2017). Also, as underlined, ISO 9000 engages information

sharing as a key to vanquish the correspondence checks existing in the ISO affiliations (Lin

and Jang, 2008). Among these works, specification was made of a research paper that was

taken as a sort of a point of view in the work which adds to theory and practice by driving the

perception of the elaboration of ISO 9000 standards, in perspective of extensively referenced

past works in Brazilian context(Helena, Monteiro and Lee 2008). In addition, there similarly

exist distinctive works that may in like manner be of interest, in spite of the way that they

may be established on fairly uncommon frameworks and thoughts (Foley et al, 2008). The

African point of view of the inward approaches for ISO consistency was examined and a

positive relationship with ISO confirmation (Fikru, 2016). In Ethiopian situation the same

kind of results was obvious; the beneficial outcome of ISO 9001, 14001 and worker size of

the organizations was usefully connected with the development of the organizations (Fikru,

2014a). In the late twentieth century, Japanese firms understood the positive part of ISO

consistency and began to adjust the standards for their organizations (Nakamura, Takahashi

and Vertinsky, 2001). In any case, it should attempt to content underneath, from the review of

observational composition impacted it to can be resolved that subjective test explore was

required remembering the ultimate objective to develop the operational importance of the

possibility of ISO 9000 compliance.

Privatisation of firms was largely due to the probable dissatisfaction of the labourers on

government controls in a globalizing economy (Christmann, 2004). Several members of the

General Conference of the United Nations held in the city of Rio de Janeiro in 1992, agreed

upon the fact, which contains essentials for companies to move towards privatization. The

world guidelines invoked then by the executive authority to the nature of their business nature

and in favor of privatisation (Pautz, 2009).

systematized interpretation of the information that can be secured and transmitted

(Rafiquzzaman et al., 2017). The creativeness and institutional effect of ISO 9000 was

evident from the adoption by the small and medium firms in China (Du, Yin and Zhang,

2016). As it was particularly critical to the examination of ISO 9000 benchmarks as it

addressed the route toward holding both understood and unequivocal information into the

affiliation and making an understanding of it into statistical process control data (Dahlgaard,

Khanji and Kristensen, 2008). As underlined, QMS proposed by ISO 9001 can be seen as one

kind of encoded data and can urge figuring out how to store, data trade, in conclusion,

learning application (Ahmed, 2017). Also, as underlined, ISO 9000 engages information

sharing as a key to vanquish the correspondence checks existing in the ISO affiliations (Lin

and Jang, 2008). Among these works, specification was made of a research paper that was

taken as a sort of a point of view in the work which adds to theory and practice by driving the

perception of the elaboration of ISO 9000 standards, in perspective of extensively referenced

past works in Brazilian context(Helena, Monteiro and Lee 2008). In addition, there similarly

exist distinctive works that may in like manner be of interest, in spite of the way that they

may be established on fairly uncommon frameworks and thoughts (Foley et al, 2008). The

African point of view of the inward approaches for ISO consistency was examined and a

positive relationship with ISO confirmation (Fikru, 2016). In Ethiopian situation the same

kind of results was obvious; the beneficial outcome of ISO 9001, 14001 and worker size of

the organizations was usefully connected with the development of the organizations (Fikru,

2014a). In the late twentieth century, Japanese firms understood the positive part of ISO

consistency and began to adjust the standards for their organizations (Nakamura, Takahashi

and Vertinsky, 2001). In any case, it should attempt to content underneath, from the review of

observational composition impacted it to can be resolved that subjective test explore was

required remembering the ultimate objective to develop the operational importance of the

possibility of ISO 9000 compliance.

Privatisation of firms was largely due to the probable dissatisfaction of the labourers on

government controls in a globalizing economy (Christmann, 2004). Several members of the

General Conference of the United Nations held in the city of Rio de Janeiro in 1992, agreed

upon the fact, which contains essentials for companies to move towards privatization. The

world guidelines invoked then by the executive authority to the nature of their business nature

and in favor of privatisation (Pautz, 2009).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Clients were interested in social obligation and responsibility, encouraging the management

to think of their clients and control the entire managerial decisions (Freeman, 2010). The

previous studies showed that firms correctly determined the standing claims of the clients,

while the tendency of the customer was to buy guaranteed products from reputed companies

(Albuquerque, Bronnenberg & Corbett, 2007). Some multinational brands like General

Motors or Ford had mandated ISO Certification. By this, they had that everyone must obtain

the certification of ISO to supply and purchase products from them

Taiwanese companies have a significant customer base in Europe, North America and Japan.

They have a significant responsibility in the supply chain in the world. For the customers of

these companies, a high priority on ecological security was levied Pressure of the

multinational giants, such as IBM, Hewlett Packard, and Ford on the stakeholders to end non

ISO compliance, builds pressure on Taiwanese companies (Yin & Schmeidler, 2009). All of

the above production companies were very stringent about their standards, and to be a

subsidiary firm or parts supplier it was essential to be ISO 14001 certificated. Consequently,

ISO 14001certification became the primary priority for Taiwanese firms. This kind of

certification also represented a passageway for business with the Europe and North American

companies. In absence of such certification, loss in imperative business opportunities was

unavoidable and unbearable (Charles Jr, Schmidheiny & Watts, 2017).

A few researchers recommend that contemporary Japanese firms might be just responding to

the greening pattern in a portion of their fare markets while North American and European

firms were following proactive green methodologies. Japanese firms' essential enthusiasm for

getting ISO 14001 confirmation was to enter the European Union's ŽEU (Montobbio &

Solito, 2018).

Recounted proves were there that some of the Japanese firms had put ordinary workers’

assertion high in their requirements. For example, Sony set up their corporate Environmental

Council in 1976 which was chaired by the C.E.O., and effectively looked to enhance its

corporate usual functioning all around the globe. Sony obtained its first ISO14001

certification in May 1995 and after that the quantity of Sony plants and backups surpassed

expected production figures by February 1997 and were even higher by September 1998. An

area executive in the Environment section of Sony trusted that ISO certification has

effectively standardized its enterprise procedure in environment within its business

Clients were interested in social obligation and responsibility, encouraging the management

to think of their clients and control the entire managerial decisions (Freeman, 2010). The

previous studies showed that firms correctly determined the standing claims of the clients,

while the tendency of the customer was to buy guaranteed products from reputed companies

(Albuquerque, Bronnenberg & Corbett, 2007). Some multinational brands like General

Motors or Ford had mandated ISO Certification. By this, they had that everyone must obtain

the certification of ISO to supply and purchase products from them

Taiwanese companies have a significant customer base in Europe, North America and Japan.

They have a significant responsibility in the supply chain in the world. For the customers of

these companies, a high priority on ecological security was levied Pressure of the

multinational giants, such as IBM, Hewlett Packard, and Ford on the stakeholders to end non

ISO compliance, builds pressure on Taiwanese companies (Yin & Schmeidler, 2009). All of

the above production companies were very stringent about their standards, and to be a

subsidiary firm or parts supplier it was essential to be ISO 14001 certificated. Consequently,

ISO 14001certification became the primary priority for Taiwanese firms. This kind of

certification also represented a passageway for business with the Europe and North American

companies. In absence of such certification, loss in imperative business opportunities was

unavoidable and unbearable (Charles Jr, Schmidheiny & Watts, 2017).

A few researchers recommend that contemporary Japanese firms might be just responding to

the greening pattern in a portion of their fare markets while North American and European

firms were following proactive green methodologies. Japanese firms' essential enthusiasm for

getting ISO 14001 confirmation was to enter the European Union's ŽEU (Montobbio &

Solito, 2018).

Recounted proves were there that some of the Japanese firms had put ordinary workers’

assertion high in their requirements. For example, Sony set up their corporate Environmental

Council in 1976 which was chaired by the C.E.O., and effectively looked to enhance its

corporate usual functioning all around the globe. Sony obtained its first ISO14001

certification in May 1995 and after that the quantity of Sony plants and backups surpassed

expected production figures by February 1997 and were even higher by September 1998. An

area executive in the Environment section of Sony trusted that ISO certification has

effectively standardized its enterprise procedure in environment within its business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

organizing framework and thus that Sony's ecological exercises were manageable. Several

other Japanese firms were seeking ISO 14001 confirmations after that.

4.0 Methodology

The present paper was made in four overlays. An observational technique has been used to

limit the disadvantages in the composition by investigating the likelihood of firms grasping

ISO 9000 certification. Moreover, this paper gives imperative bits of learning into how the

collecting and organization divisions see and attract with ISO 9000 confirmation. Thirdly, we

take conflict, recommending that it was indispensable to explore the components that clear up

the determination of an overall standard at its starting circumstances since they may differ

from the segments that illuminate its later gathering. Thusly, investigations have improved

the situation to separate between the adopters and defaulters (Cao and Prakash, 2011). A

special Chinese database from National Bureau of Statistics has permitted investigating the

degree of the elements of ISO 9000 affirmation. In the accompanying portion, a theoretical

motivation to the ISO 9000 affirmation and detail speculations has been portrayed. Four

theories were tried in the inferential examination.

Firstly, it was hypothesized that,

H10: Sales and profit of companies were independent of ISO 9000 complaint factor.

Secondly,

H20: Return on assets and return on sales were hypothesized to be indifferent to ISO certified

and a non-certified case, this study was separately done based on FDI status.

In the third hypothesis,

H30: Capital from state and overseas for both ISO statuses was compared considering them

to be same.

H40: There was no relation between the employee education levels and growth of the firms

for both the groups.

organizing framework and thus that Sony's ecological exercises were manageable. Several

other Japanese firms were seeking ISO 14001 confirmations after that.

4.0 Methodology

The present paper was made in four overlays. An observational technique has been used to

limit the disadvantages in the composition by investigating the likelihood of firms grasping

ISO 9000 certification. Moreover, this paper gives imperative bits of learning into how the

collecting and organization divisions see and attract with ISO 9000 confirmation. Thirdly, we

take conflict, recommending that it was indispensable to explore the components that clear up

the determination of an overall standard at its starting circumstances since they may differ

from the segments that illuminate its later gathering. Thusly, investigations have improved

the situation to separate between the adopters and defaulters (Cao and Prakash, 2011). A

special Chinese database from National Bureau of Statistics has permitted investigating the

degree of the elements of ISO 9000 affirmation. In the accompanying portion, a theoretical

motivation to the ISO 9000 affirmation and detail speculations has been portrayed. Four

theories were tried in the inferential examination.

Firstly, it was hypothesized that,

H10: Sales and profit of companies were independent of ISO 9000 complaint factor.

Secondly,

H20: Return on assets and return on sales were hypothesized to be indifferent to ISO certified

and a non-certified case, this study was separately done based on FDI status.

In the third hypothesis,

H30: Capital from state and overseas for both ISO statuses was compared considering them

to be same.

H40: There was no relation between the employee education levels and growth of the firms

for both the groups.

9

5.0 Data Analysis

5.1 Data

The information utilized as a part of the experimental examination of the paper was acquired

from a review of business foundations directed by National Bureau of Statistics of China in

2008. The objective range for the study included every one of the foundations from the

different cities of China. The example was stratified by size and area. Foundations with a

lower number of representatives were rejected in light of the fact that they, as a rule, indicate

more factor and less formal examples of work association, which makes it harder to get

dependable reactions in connection to the manner by which this work was sorted out.

The survey was sent by post to the general administrator of the foundation. It was replied by

phone, fax or email, by the general administrator of the foundation or another chief assigned

by him/her as a result of the last's recognition with the issues managed in the survey. The

explanation behind offering firms these three methods of the reaction was to encourage

investment in the overview by enabling the respondent to pick the system most appropriate to

him. The reaction rate was high because of both the scope of reaction modes and to the way

that the overview was directed by the Regional Government and interest was obligatory

under the danger of a fine. The high reaction rate ensures the representativeness of the

example and guarantees there was no noteworthy predisposition accordingly and non-reaction

designs. This prompted an underlying example of 5717 foundations.

5.2 Variables

Dependent Variables: The adaptable work hones considered in the exact examination were

illustrative of the practices that normally show up in the writing correlated to this exploration

field. Revenue earned and Profit obtained share the standard for being instruments through

which the firm empowers representative contribution and data sharing either through

upwards, downwards or sidelong correspondence and basic leadership.

Independent Variables: Various other factors were utilized to quantify the appropriation of

value frameworks or models. FDI status was a parallel variable that demonstrates regardless

of whether the firm has an ensured quality framework as per the ISO 9000 standard. The

others were additionally scale factors those demonstrate regardless of whether the firm was

5.0 Data Analysis

5.1 Data

The information utilized as a part of the experimental examination of the paper was acquired

from a review of business foundations directed by National Bureau of Statistics of China in

2008. The objective range for the study included every one of the foundations from the

different cities of China. The example was stratified by size and area. Foundations with a

lower number of representatives were rejected in light of the fact that they, as a rule, indicate

more factor and less formal examples of work association, which makes it harder to get

dependable reactions in connection to the manner by which this work was sorted out.

The survey was sent by post to the general administrator of the foundation. It was replied by

phone, fax or email, by the general administrator of the foundation or another chief assigned

by him/her as a result of the last's recognition with the issues managed in the survey. The

explanation behind offering firms these three methods of the reaction was to encourage

investment in the overview by enabling the respondent to pick the system most appropriate to

him. The reaction rate was high because of both the scope of reaction modes and to the way

that the overview was directed by the Regional Government and interest was obligatory

under the danger of a fine. The high reaction rate ensures the representativeness of the

example and guarantees there was no noteworthy predisposition accordingly and non-reaction

designs. This prompted an underlying example of 5717 foundations.

5.2 Variables

Dependent Variables: The adaptable work hones considered in the exact examination were

illustrative of the practices that normally show up in the writing correlated to this exploration

field. Revenue earned and Profit obtained share the standard for being instruments through

which the firm empowers representative contribution and data sharing either through

upwards, downwards or sidelong correspondence and basic leadership.

Independent Variables: Various other factors were utilized to quantify the appropriation of

value frameworks or models. FDI status was a parallel variable that demonstrates regardless

of whether the firm has an ensured quality framework as per the ISO 9000 standard. The

others were additionally scale factors those demonstrate regardless of whether the firm was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

engaged with the assessment procedure as indicated by the EFQM demonstrate, as an

approach to guarantee that the firm was successfully working in such a structure.

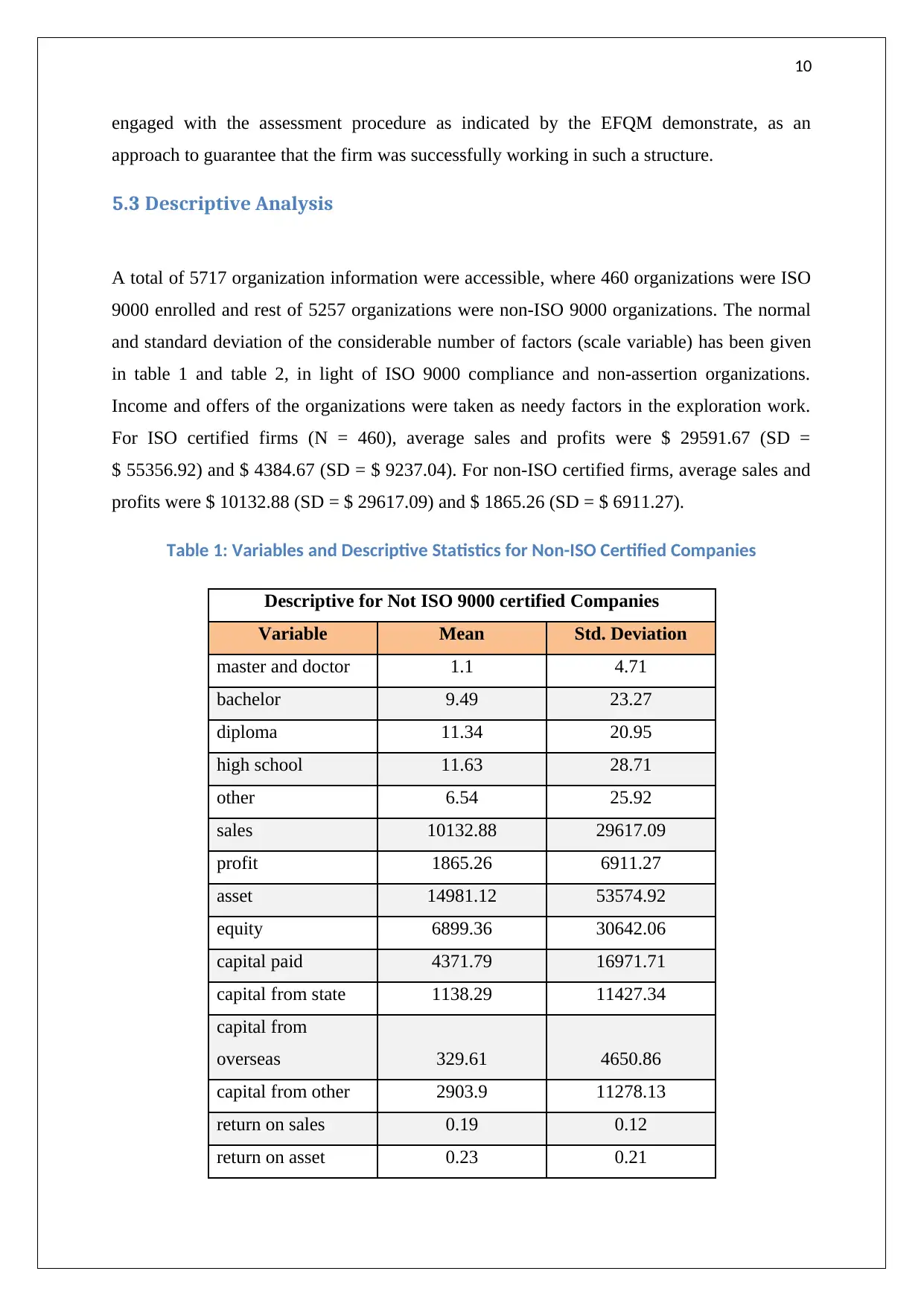

5.3 Descriptive Analysis

A total of 5717 organization information were accessible, where 460 organizations were ISO

9000 enrolled and rest of 5257 organizations were non-ISO 9000 organizations. The normal

and standard deviation of the considerable number of factors (scale variable) has been given

in table 1 and table 2, in light of ISO 9000 compliance and non-assertion organizations.

Income and offers of the organizations were taken as needy factors in the exploration work.

For ISO certified firms (N = 460), average sales and profits were $ 29591.67 (SD =

$ 55356.92) and $ 4384.67 (SD = $ 9237.04). For non-ISO certified firms, average sales and

profits were $ 10132.88 (SD = $ 29617.09) and $ 1865.26 (SD = $ 6911.27).

Table 1: Variables and Descriptive Statistics for Non-ISO Certified Companies

Descriptive for Not ISO 9000 certified Companies

Variable Mean Std. Deviation

master and doctor 1.1 4.71

bachelor 9.49 23.27

diploma 11.34 20.95

high school 11.63 28.71

other 6.54 25.92

sales 10132.88 29617.09

profit 1865.26 6911.27

asset 14981.12 53574.92

equity 6899.36 30642.06

capital paid 4371.79 16971.71

capital from state 1138.29 11427.34

capital from

overseas 329.61 4650.86

capital from other 2903.9 11278.13

return on sales 0.19 0.12

return on asset 0.23 0.21

engaged with the assessment procedure as indicated by the EFQM demonstrate, as an

approach to guarantee that the firm was successfully working in such a structure.

5.3 Descriptive Analysis

A total of 5717 organization information were accessible, where 460 organizations were ISO

9000 enrolled and rest of 5257 organizations were non-ISO 9000 organizations. The normal

and standard deviation of the considerable number of factors (scale variable) has been given

in table 1 and table 2, in light of ISO 9000 compliance and non-assertion organizations.

Income and offers of the organizations were taken as needy factors in the exploration work.

For ISO certified firms (N = 460), average sales and profits were $ 29591.67 (SD =

$ 55356.92) and $ 4384.67 (SD = $ 9237.04). For non-ISO certified firms, average sales and

profits were $ 10132.88 (SD = $ 29617.09) and $ 1865.26 (SD = $ 6911.27).

Table 1: Variables and Descriptive Statistics for Non-ISO Certified Companies

Descriptive for Not ISO 9000 certified Companies

Variable Mean Std. Deviation

master and doctor 1.1 4.71

bachelor 9.49 23.27

diploma 11.34 20.95

high school 11.63 28.71

other 6.54 25.92

sales 10132.88 29617.09

profit 1865.26 6911.27

asset 14981.12 53574.92

equity 6899.36 30642.06

capital paid 4371.79 16971.71

capital from state 1138.29 11427.34

capital from

overseas 329.61 4650.86

capital from other 2903.9 11278.13

return on sales 0.19 0.12

return on asset 0.23 0.21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

percentage of FDI 0.02 0.15

FDI dummy 0.03 0.17

age of company in

years 7.39 6.82

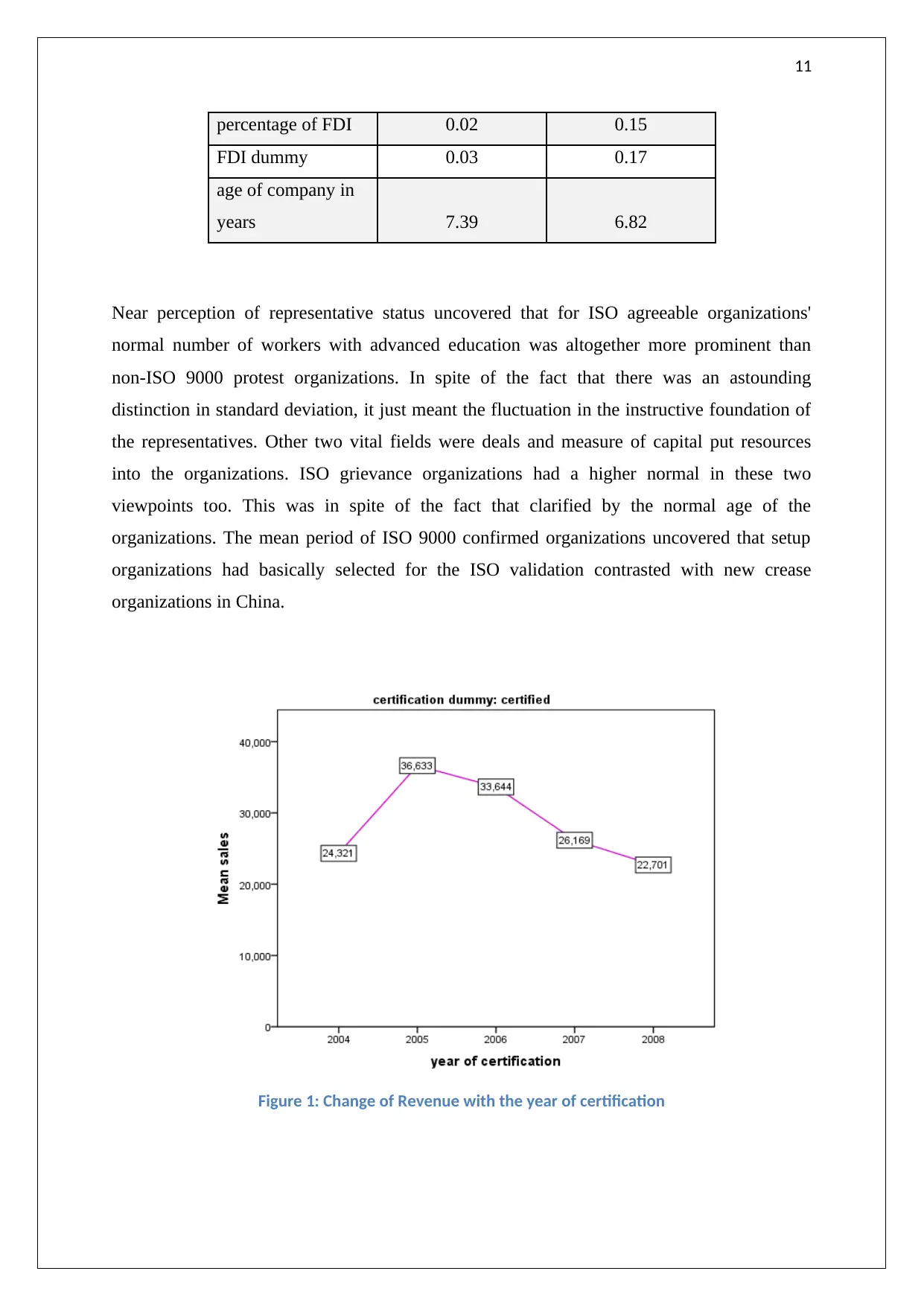

Near perception of representative status uncovered that for ISO agreeable organizations'

normal number of workers with advanced education was altogether more prominent than

non-ISO 9000 protest organizations. In spite of the fact that there was an astounding

distinction in standard deviation, it just meant the fluctuation in the instructive foundation of

the representatives. Other two vital fields were deals and measure of capital put resources

into the organizations. ISO grievance organizations had a higher normal in these two

viewpoints too. This was in spite of the fact that clarified by the normal age of the

organizations. The mean period of ISO 9000 confirmed organizations uncovered that setup

organizations had basically selected for the ISO validation contrasted with new crease

organizations in China.

Figure 1: Change of Revenue with the year of certification

percentage of FDI 0.02 0.15

FDI dummy 0.03 0.17

age of company in

years 7.39 6.82

Near perception of representative status uncovered that for ISO agreeable organizations'

normal number of workers with advanced education was altogether more prominent than

non-ISO 9000 protest organizations. In spite of the fact that there was an astounding

distinction in standard deviation, it just meant the fluctuation in the instructive foundation of

the representatives. Other two vital fields were deals and measure of capital put resources

into the organizations. ISO grievance organizations had a higher normal in these two

viewpoints too. This was in spite of the fact that clarified by the normal age of the

organizations. The mean period of ISO 9000 confirmed organizations uncovered that setup

organizations had basically selected for the ISO validation contrasted with new crease

organizations in China.

Figure 1: Change of Revenue with the year of certification

12

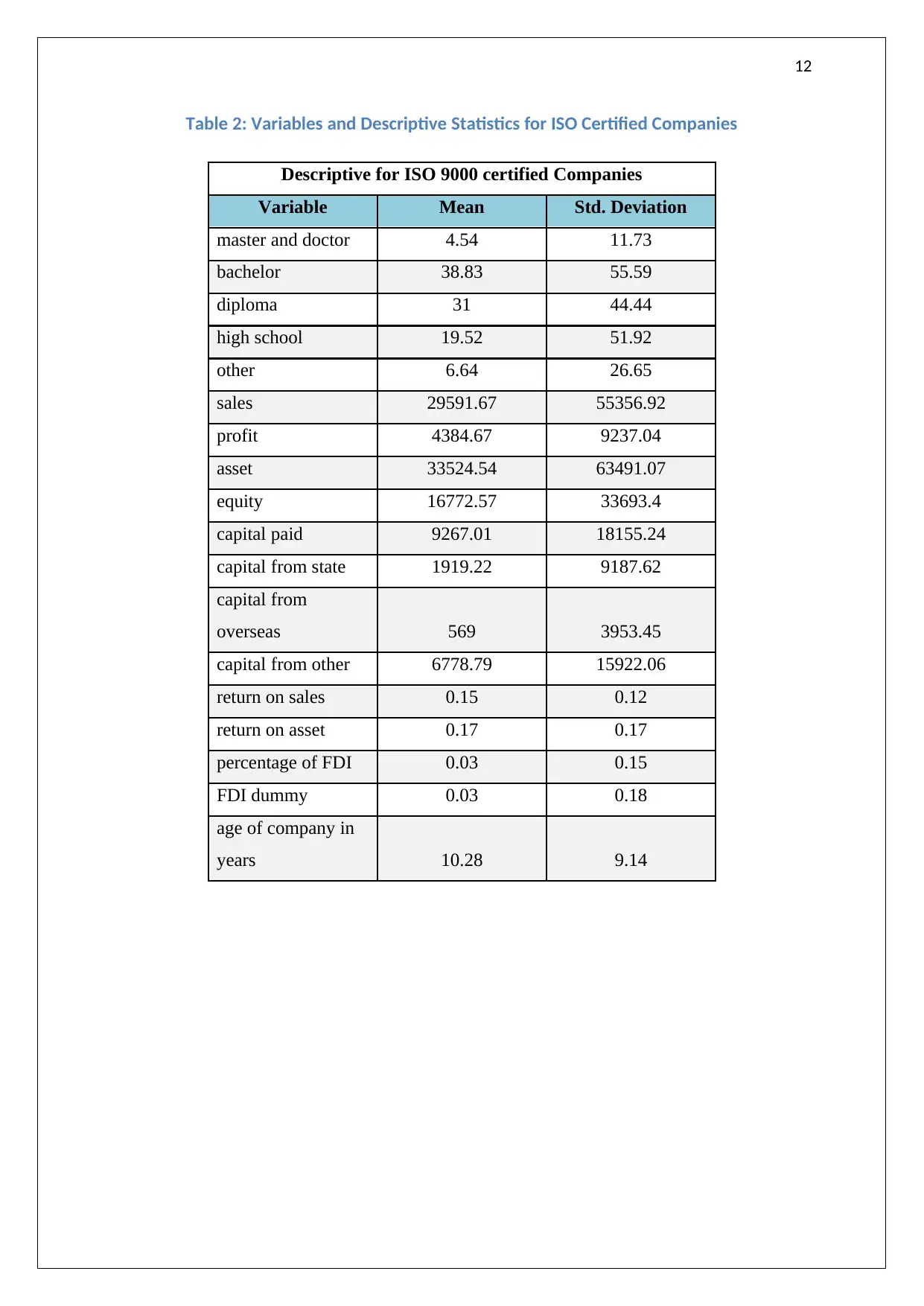

Table 2: Variables and Descriptive Statistics for ISO Certified Companies

Descriptive for ISO 9000 certified Companies

Variable Mean Std. Deviation

master and doctor 4.54 11.73

bachelor 38.83 55.59

diploma 31 44.44

high school 19.52 51.92

other 6.64 26.65

sales 29591.67 55356.92

profit 4384.67 9237.04

asset 33524.54 63491.07

equity 16772.57 33693.4

capital paid 9267.01 18155.24

capital from state 1919.22 9187.62

capital from

overseas 569 3953.45

capital from other 6778.79 15922.06

return on sales 0.15 0.12

return on asset 0.17 0.17

percentage of FDI 0.03 0.15

FDI dummy 0.03 0.18

age of company in

years 10.28 9.14

Table 2: Variables and Descriptive Statistics for ISO Certified Companies

Descriptive for ISO 9000 certified Companies

Variable Mean Std. Deviation

master and doctor 4.54 11.73

bachelor 38.83 55.59

diploma 31 44.44

high school 19.52 51.92

other 6.64 26.65

sales 29591.67 55356.92

profit 4384.67 9237.04

asset 33524.54 63491.07

equity 16772.57 33693.4

capital paid 9267.01 18155.24

capital from state 1919.22 9187.62

capital from

overseas 569 3953.45

capital from other 6778.79 15922.06

return on sales 0.15 0.12

return on asset 0.17 0.17

percentage of FDI 0.03 0.15

FDI dummy 0.03 0.18

age of company in

years 10.28 9.14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 32

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.