ACC621 Audit Practice: Materiality & Audit Procedures for Chamoisee

VerifiedAdded on 2023/06/03

|13

|2512

|324

Report

AI Summary

This report identifies material items from the trial balance and income statement of Chamoisee Enterprise, establishing a materiality level for the entity and determining the assertions associated with the identified items. It suggests specific audit procedures for material items like sales, cost of sales, repairs and maintenance, and wages. The report highlights the importance of analytical review in identifying risk areas and the need for appropriate materiality assessment, suggesting a lower materiality level than initially proposed by the audit partner. Ultimately, the report concludes that several accounts require verification for material misstatement, emphasizing the auditor's responsibility to detect misstatements due to fraud, even when management is perceived as honest.

Running head: ISSUES IN AUDIT PRACTICE

Issues in audit practice

Name of the student

Name of the university

Author note

Issues in audit practice

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ISSUES IN AUDIT PRACTICE

Executive summary

The purpose of the report is to highlight on the material items those will be identified from

the trial balance and income statement of Chamoisee Enterprise. The report will focus on

establishing the materiality level for the entity. Based on the materiality level and identified

material items the report will determine the assertion associated with the items. Further, for

each identified material items particular audit procedure will be suggested.

Executive summary

The purpose of the report is to highlight on the material items those will be identified from

the trial balance and income statement of Chamoisee Enterprise. The report will focus on

establishing the materiality level for the entity. Based on the materiality level and identified

material items the report will determine the assertion associated with the items. Further, for

each identified material items particular audit procedure will be suggested.

2ISSUES IN AUDIT PRACTICE

Table of Contents

1.0 Introduction.....................................................................................................................3

1.1 Analytical review.............................................................................................................3

1.2 Preliminary judgement for the purpose of materiality.....................................................4

2.0 Trend analysis.................................................................................................................5

3.0 Accounts considered for material misstatement..................................................................5

3.1.1 First account selected – Sales........................................................................................5

3.1.2 Rational for selection....................................................................................................5

3.1.3 Assertion and explanation.............................................................................................5

3.2 Second account selected – Cost of sales......................................................................6

3.2.1 Rational for selection...............................................................................................6

3.2.2 Assertion and explanation........................................................................................6

3.3 Third account selected – Repairs and maintenance.........................................................7

3.3.1 Rational for selection....................................................................................................7

3.3.2 Assertion and explanation.............................................................................................7

3.4 Fourth account selected – Wages.....................................................................................7

3.4.1 Rational for selection....................................................................................................7

3.4.2 Assertion and explanation.............................................................................................7

4.0 Audit procedure....................................................................................................................8

4.1 Sales.................................................................................................................................8

4.2 Cost of sales.....................................................................................................................8

Table of Contents

1.0 Introduction.....................................................................................................................3

1.1 Analytical review.............................................................................................................3

1.2 Preliminary judgement for the purpose of materiality.....................................................4

2.0 Trend analysis.................................................................................................................5

3.0 Accounts considered for material misstatement..................................................................5

3.1.1 First account selected – Sales........................................................................................5

3.1.2 Rational for selection....................................................................................................5

3.1.3 Assertion and explanation.............................................................................................5

3.2 Second account selected – Cost of sales......................................................................6

3.2.1 Rational for selection...............................................................................................6

3.2.2 Assertion and explanation........................................................................................6

3.3 Third account selected – Repairs and maintenance.........................................................7

3.3.1 Rational for selection....................................................................................................7

3.3.2 Assertion and explanation.............................................................................................7

3.4 Fourth account selected – Wages.....................................................................................7

3.4.1 Rational for selection....................................................................................................7

3.4.2 Assertion and explanation.............................................................................................7

4.0 Audit procedure....................................................................................................................8

4.1 Sales.................................................................................................................................8

4.2 Cost of sales.....................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ISSUES IN AUDIT PRACTICE

4.3 Repairs and maintenance..................................................................................................8

4.4 Wages...............................................................................................................................8

5.0 Conclusions..........................................................................................................................9

Reference..................................................................................................................................10

4.3 Repairs and maintenance..................................................................................................8

4.4 Wages...............................................................................................................................8

5.0 Conclusions..........................................................................................................................9

Reference..................................................................................................................................10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ISSUES IN AUDIT PRACTICE

1.0 Introduction

Auditor’s main objective is to develop a plan for audit so that the audit can be

performed in efficient manner. Audit plan highlights the risk areas and based on the findings

audit procedures are carried out for the risk – prone areas. 3 major components of successful

audit are – (i) Timing – it is the continuous procedure that starts with the ending of previous

audit and finishes after completion of audit (ii) assessment of risk – risk is assessed on the

basis of the client’s external, internal and regulatory factors that may have impact on audit

(iii) audit team – it considers the professional experience of the auditors included in the team.

It shall assure that right people have been included under the audit team (Leung et al. 2014).

1.1 Analytical review

It is the crucial part of the audit procedure that includes the analysis of the financial

data provided in the financial reports of the company. It starts from the simple comparison

and can be extended to complex models that involves various relationships and data elements.

It involves the comparison of the reported amounts or financial ratios to expectations of the

entity or with the industry standards or with the entity’s data for previous year (Louwers et al.

2015). The auditor uses the analytical procedures for the following purposes –

It is used as the substantive test for obtaining the evidential matter regarding

particular assertion involved with the account balance or the transactions

Supporting the auditors with regard to plan the extent, timing and nature of the audit

procedure

As the overall review for the financial data identified under the audit review stage

(Titera 2013).

1.0 Introduction

Auditor’s main objective is to develop a plan for audit so that the audit can be

performed in efficient manner. Audit plan highlights the risk areas and based on the findings

audit procedures are carried out for the risk – prone areas. 3 major components of successful

audit are – (i) Timing – it is the continuous procedure that starts with the ending of previous

audit and finishes after completion of audit (ii) assessment of risk – risk is assessed on the

basis of the client’s external, internal and regulatory factors that may have impact on audit

(iii) audit team – it considers the professional experience of the auditors included in the team.

It shall assure that right people have been included under the audit team (Leung et al. 2014).

1.1 Analytical review

It is the crucial part of the audit procedure that includes the analysis of the financial

data provided in the financial reports of the company. It starts from the simple comparison

and can be extended to complex models that involves various relationships and data elements.

It involves the comparison of the reported amounts or financial ratios to expectations of the

entity or with the industry standards or with the entity’s data for previous year (Louwers et al.

2015). The auditor uses the analytical procedures for the following purposes –

It is used as the substantive test for obtaining the evidential matter regarding

particular assertion involved with the account balance or the transactions

Supporting the auditors with regard to plan the extent, timing and nature of the audit

procedure

As the overall review for the financial data identified under the audit review stage

(Titera 2013).

5ISSUES IN AUDIT PRACTICE

1.2 Preliminary judgement for the purpose of materiality

Professional standard stated insufficient guidance regarding assessment of materiality

on reasonable basis. AASB 108 stated material misstatement as the omission that can have

impact on the user’s financial decision making individually or in aggregate with any other

item. However, for establishing the materiality level various factors like the nature and type

of the industry in which the company operates shall be taken into consideration as per the

requirement of ISA 320. Thouse the sufficient bases have not been provided to the

practitioners as per AICPA and FASB, there must have some base for evaluation of

materiality (Eilifsen and Messier 2014). It is assumed that is the materiality is established on

the basis of sales revenue the amount will be 1% to 5% of sales revenue. Hence, for

Chamoisee Enterprise materiality will be ($ 189,000 * 1%) = $ 1,890 to ($ 189,000 * 5%) = $

9,450. However, the tolerable misstatement may be set at lower limit as compared to overall

materiality as it is unlikely that all the accounts are not misstated with full amount.

Therefore, materiality can be established at around $ 8,000 (Legoria, Melendrez and

Reynolds 2013). Hence, the estimated materiality of the audit partner that is $ 15,000 is not

appropriate for Chamoisee Enterprise and shall be reduced to $ 8,000.

The audit budget is the number of items required to be selected for the purpose of

carrying out the audit procedure based on materiality level. If the materiality level increases

the auditor will be required to select less number of items and vice versa. Therefore, as the

materiality level shall be reduced from $ 15,000 to $ 8,000 the audit budget will be increased

and the auditor will be required to select more items for the purpose of assessing material

misstatement (Glover and Prawitt 2014).

1.2 Preliminary judgement for the purpose of materiality

Professional standard stated insufficient guidance regarding assessment of materiality

on reasonable basis. AASB 108 stated material misstatement as the omission that can have

impact on the user’s financial decision making individually or in aggregate with any other

item. However, for establishing the materiality level various factors like the nature and type

of the industry in which the company operates shall be taken into consideration as per the

requirement of ISA 320. Thouse the sufficient bases have not been provided to the

practitioners as per AICPA and FASB, there must have some base for evaluation of

materiality (Eilifsen and Messier 2014). It is assumed that is the materiality is established on

the basis of sales revenue the amount will be 1% to 5% of sales revenue. Hence, for

Chamoisee Enterprise materiality will be ($ 189,000 * 1%) = $ 1,890 to ($ 189,000 * 5%) = $

9,450. However, the tolerable misstatement may be set at lower limit as compared to overall

materiality as it is unlikely that all the accounts are not misstated with full amount.

Therefore, materiality can be established at around $ 8,000 (Legoria, Melendrez and

Reynolds 2013). Hence, the estimated materiality of the audit partner that is $ 15,000 is not

appropriate for Chamoisee Enterprise and shall be reduced to $ 8,000.

The audit budget is the number of items required to be selected for the purpose of

carrying out the audit procedure based on materiality level. If the materiality level increases

the auditor will be required to select less number of items and vice versa. Therefore, as the

materiality level shall be reduced from $ 15,000 to $ 8,000 the audit budget will be increased

and the auditor will be required to select more items for the purpose of assessing material

misstatement (Glover and Prawitt 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ISSUES IN AUDIT PRACTICE

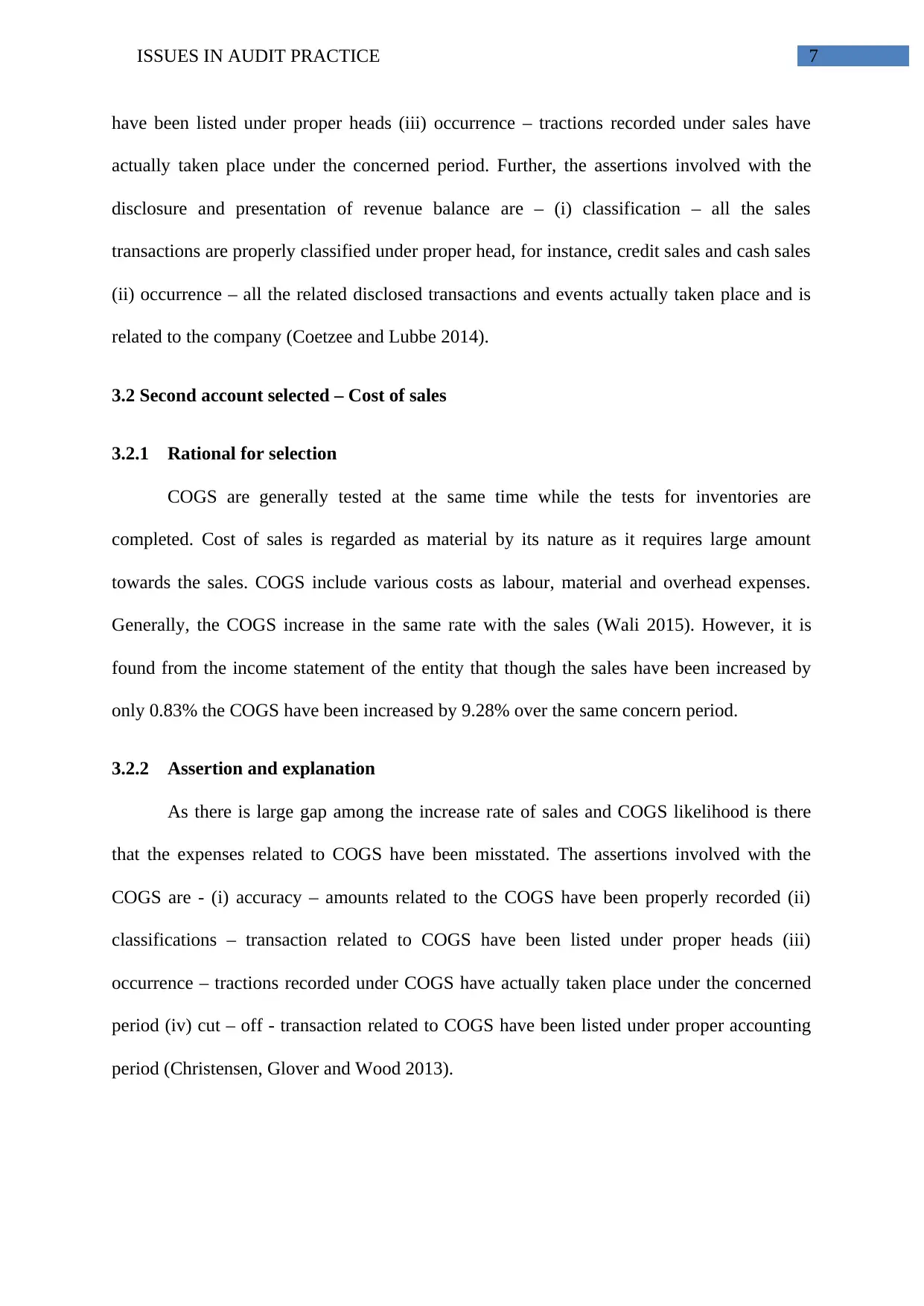

2.0 Trend analysis

3.0 Accounts considered for material misstatement

3.1.1 First account selected – Sales

3.1.2 Rational for selection

Sales and the collection procedure under any business operation is the set of

procedure that starts with the sales of services or goods and completes with the receipt of

payment. It is found from the income statement of the entity that the sales have been

increased only by 0.83%. However, sales transaction shall be verified to assure that internal

control on sales transaction is sufficient and the revenues are not misstated materially

(Ruhnke, Pronobis and Michel 2014).

3.1.3 Assertion and explanation

Audit assertion related to sales transaction are – (i) accuracy – amounts related to the

sales transactions have been properly recorded (ii) classifications – transaction related to sales

2.0 Trend analysis

3.0 Accounts considered for material misstatement

3.1.1 First account selected – Sales

3.1.2 Rational for selection

Sales and the collection procedure under any business operation is the set of

procedure that starts with the sales of services or goods and completes with the receipt of

payment. It is found from the income statement of the entity that the sales have been

increased only by 0.83%. However, sales transaction shall be verified to assure that internal

control on sales transaction is sufficient and the revenues are not misstated materially

(Ruhnke, Pronobis and Michel 2014).

3.1.3 Assertion and explanation

Audit assertion related to sales transaction are – (i) accuracy – amounts related to the

sales transactions have been properly recorded (ii) classifications – transaction related to sales

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ISSUES IN AUDIT PRACTICE

have been listed under proper heads (iii) occurrence – tractions recorded under sales have

actually taken place under the concerned period. Further, the assertions involved with the

disclosure and presentation of revenue balance are – (i) classification – all the sales

transactions are properly classified under proper head, for instance, credit sales and cash sales

(ii) occurrence – all the related disclosed transactions and events actually taken place and is

related to the company (Coetzee and Lubbe 2014).

3.2 Second account selected – Cost of sales

3.2.1 Rational for selection

COGS are generally tested at the same time while the tests for inventories are

completed. Cost of sales is regarded as material by its nature as it requires large amount

towards the sales. COGS include various costs as labour, material and overhead expenses.

Generally, the COGS increase in the same rate with the sales (Wali 2015). However, it is

found from the income statement of the entity that though the sales have been increased by

only 0.83% the COGS have been increased by 9.28% over the same concern period.

3.2.2 Assertion and explanation

As there is large gap among the increase rate of sales and COGS likelihood is there

that the expenses related to COGS have been misstated. The assertions involved with the

COGS are - (i) accuracy – amounts related to the COGS have been properly recorded (ii)

classifications – transaction related to COGS have been listed under proper heads (iii)

occurrence – tractions recorded under COGS have actually taken place under the concerned

period (iv) cut – off - transaction related to COGS have been listed under proper accounting

period (Christensen, Glover and Wood 2013).

have been listed under proper heads (iii) occurrence – tractions recorded under sales have

actually taken place under the concerned period. Further, the assertions involved with the

disclosure and presentation of revenue balance are – (i) classification – all the sales

transactions are properly classified under proper head, for instance, credit sales and cash sales

(ii) occurrence – all the related disclosed transactions and events actually taken place and is

related to the company (Coetzee and Lubbe 2014).

3.2 Second account selected – Cost of sales

3.2.1 Rational for selection

COGS are generally tested at the same time while the tests for inventories are

completed. Cost of sales is regarded as material by its nature as it requires large amount

towards the sales. COGS include various costs as labour, material and overhead expenses.

Generally, the COGS increase in the same rate with the sales (Wali 2015). However, it is

found from the income statement of the entity that though the sales have been increased by

only 0.83% the COGS have been increased by 9.28% over the same concern period.

3.2.2 Assertion and explanation

As there is large gap among the increase rate of sales and COGS likelihood is there

that the expenses related to COGS have been misstated. The assertions involved with the

COGS are - (i) accuracy – amounts related to the COGS have been properly recorded (ii)

classifications – transaction related to COGS have been listed under proper heads (iii)

occurrence – tractions recorded under COGS have actually taken place under the concerned

period (iv) cut – off - transaction related to COGS have been listed under proper accounting

period (Christensen, Glover and Wood 2013).

8ISSUES IN AUDIT PRACTICE

3.3 Third account selected – Repairs and maintenance

3.3.1 Rational for selection

It can be seen from the income statement of the company that the expenses towards

repairs and maintenance was one of the biggest expenses during the previous year. However,

the expenses under same head have been reduced by 71.49% during the current period.

3.3.2 Assertion and explanation

Various assertion involved with repairs and maintenance expenses are – (i)

occurrence – all the related transactions and events actually taken place and is related to the

company (ii) cut – off - transaction related to repairs and maintenance have been listed under

proper accounting period (iii) classifications – transaction related to COGS have been listed

under proper heads (Kharisova and Kozlova 2014).

3.4 Fourth account selected – Wages

3.4.1 Rational for selection

Payment of wages or payroll processing is considered as an important part of day to

day business operations. Further as large amount is involved with the wage payment wage

payment shall be considered as a material item that requires analysis and evaluation. It is

found from the income statement of the entity that though the wages expenses have been

reduced by only 9.43% over the concern period.

3.4.2 Assertion and explanation

As it involves payment to large number of employees it leaves a scope to the

management for misstating the account balance. Various assertions involved with wage

payment are – (i) cut – off - transaction related to wage payments have been listed under

proper accounting period (ii) occurrence – tractions recorded under wage payment have

3.3 Third account selected – Repairs and maintenance

3.3.1 Rational for selection

It can be seen from the income statement of the company that the expenses towards

repairs and maintenance was one of the biggest expenses during the previous year. However,

the expenses under same head have been reduced by 71.49% during the current period.

3.3.2 Assertion and explanation

Various assertion involved with repairs and maintenance expenses are – (i)

occurrence – all the related transactions and events actually taken place and is related to the

company (ii) cut – off - transaction related to repairs and maintenance have been listed under

proper accounting period (iii) classifications – transaction related to COGS have been listed

under proper heads (Kharisova and Kozlova 2014).

3.4 Fourth account selected – Wages

3.4.1 Rational for selection

Payment of wages or payroll processing is considered as an important part of day to

day business operations. Further as large amount is involved with the wage payment wage

payment shall be considered as a material item that requires analysis and evaluation. It is

found from the income statement of the entity that though the wages expenses have been

reduced by only 9.43% over the concern period.

3.4.2 Assertion and explanation

As it involves payment to large number of employees it leaves a scope to the

management for misstating the account balance. Various assertions involved with wage

payment are – (i) cut – off - transaction related to wage payments have been listed under

proper accounting period (ii) occurrence – tractions recorded under wage payment have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ISSUES IN AUDIT PRACTICE

actually taken place under the concerned period. In other words, payments made to those

employees who are actually engaged with the entity during the concern period.

4.0 Audit procedure

4.1 Sales

Sales transaction shall be matched with the unit price listed in the authorised price list

of the company. Further, the auditor shall verify that the sales revenue has been recorded only

after the risk and rewards associated with the services or goods transferred to the purchaser

(Byrnes et al. 2015). Further, the sales register shall be verified to confirm that the recorded

amount matched with the amount for which bill raised.

4.2 Cost of sales

Cost of sales shall be verified with the expenses under particular head of material

expenses, labour expenses and overhead expenses. Further, in case of any mismatch or doubt

the amount shall be confirmed from the 3rd party. For instance, amount of purchases can be

confirmed from the creditors or suppliers.

4.3 Repairs and maintenance

Amount spent for repairs and maintenance shall be verified with the payment

transaction and vouchers for evaluation the items those were repaired. Further, where large

amount has been paid towards repair or maintenance authorization for the same shall be

verified (Arens et al. 2016).

4.4 Wages

Wages shall be verified with the employee register to confirm that the payments made

only to those who were in engagement with the company during the period taken under

actually taken place under the concerned period. In other words, payments made to those

employees who are actually engaged with the entity during the concern period.

4.0 Audit procedure

4.1 Sales

Sales transaction shall be matched with the unit price listed in the authorised price list

of the company. Further, the auditor shall verify that the sales revenue has been recorded only

after the risk and rewards associated with the services or goods transferred to the purchaser

(Byrnes et al. 2015). Further, the sales register shall be verified to confirm that the recorded

amount matched with the amount for which bill raised.

4.2 Cost of sales

Cost of sales shall be verified with the expenses under particular head of material

expenses, labour expenses and overhead expenses. Further, in case of any mismatch or doubt

the amount shall be confirmed from the 3rd party. For instance, amount of purchases can be

confirmed from the creditors or suppliers.

4.3 Repairs and maintenance

Amount spent for repairs and maintenance shall be verified with the payment

transaction and vouchers for evaluation the items those were repaired. Further, where large

amount has been paid towards repair or maintenance authorization for the same shall be

verified (Arens et al. 2016).

4.4 Wages

Wages shall be verified with the employee register to confirm that the payments made

only to those who were in engagement with the company during the period taken under

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ISSUES IN AUDIT PRACTICE

consideration. In case of new engagement their contract shall be verified to confirm that they

are getting the same amount that is mentioned in the engagement contract letter.

5.0 Conclusions

It can be concluded from the above that some of the accounts of the company that is

sales, wages, repairs and maintenance and COGS shall be verified for material misstatement.

However, in fraud aspect the auditor is responsible for carrying out the audit to detect the

misstatement due to fraud. It is assumed that the employees or management involved in fraud

if they get chance. Therefore, even if the audit partner is in the view that the employees are

honest they shall be carried out the audit for detecting the fraud misstatement.

consideration. In case of new engagement their contract shall be verified to confirm that they

are getting the same amount that is mentioned in the engagement contract letter.

5.0 Conclusions

It can be concluded from the above that some of the accounts of the company that is

sales, wages, repairs and maintenance and COGS shall be verified for material misstatement.

However, in fraud aspect the auditor is responsible for carrying out the audit to detect the

misstatement due to fraud. It is assumed that the employees or management involved in fraud

if they get chance. Therefore, even if the audit partner is in the view that the employees are

honest they shall be carried out the audit for detecting the fraud misstatement.

11ISSUES IN AUDIT PRACTICE

Reference

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D.

and Vasarhelyi, M., 2015. Evolution of auditing: From the traditional approach to the future

audit. Audit Analytics, 71.

Christensen, B.E., Glover, S.M. and Wood, D.A., 2013. Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Coetzee, P. and Lubbe, D., 2014. Improving the efficiency and effectiveness of risk‐based

internal audit engagements. International Journal of Auditing, 18(2), pp.115-125.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Glover, S.M. and Prawitt, D.F., 2014. Enhancing auditor professional skepticism: The

professional skepticism continuum. Current Issues in Auditing, 8(2), pp.P1-P10.

Kharisova, F.I. and Kozlova, N.N., 2014. Applying the category of «Assertions (or

preconditions)» In audit of financial statement. Mediterranean Journal of Social

Sciences, 5(24), p.180.

Legoria, J., Melendrez, K.D. and Reynolds, J.K., 2013. Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), pp.414-442.

Leung, P., Coram, P., Cooper, B.J. and Richardson, P., 2014. Modern Auditing and

Assurance Services 6e. Wiley.

Reference

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D.

and Vasarhelyi, M., 2015. Evolution of auditing: From the traditional approach to the future

audit. Audit Analytics, 71.

Christensen, B.E., Glover, S.M. and Wood, D.A., 2013. Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Coetzee, P. and Lubbe, D., 2014. Improving the efficiency and effectiveness of risk‐based

internal audit engagements. International Journal of Auditing, 18(2), pp.115-125.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Glover, S.M. and Prawitt, D.F., 2014. Enhancing auditor professional skepticism: The

professional skepticism continuum. Current Issues in Auditing, 8(2), pp.P1-P10.

Kharisova, F.I. and Kozlova, N.N., 2014. Applying the category of «Assertions (or

preconditions)» In audit of financial statement. Mediterranean Journal of Social

Sciences, 5(24), p.180.

Legoria, J., Melendrez, K.D. and Reynolds, J.K., 2013. Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), pp.414-442.

Leung, P., Coram, P., Cooper, B.J. and Richardson, P., 2014. Modern Auditing and

Assurance Services 6e. Wiley.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.