HI5020 Group Assignment: Analysis of Issues in Cash Flow Statements

VerifiedAdded on 2023/03/31

|13

|3779

|462

Report

AI Summary

This report analyzes the cash flow statements of BHP Billiton, Santos Limited, and Funtastic Limited to evaluate various cash flow aspects. The report explores the components of cash flow statements, including operating, financing, and investing activities. It highlights that Santos Limited demonstrates a strong ability to generate cash flows from financing activities, which supports its business operations and repayment of borrowings. In contrast, BHP Billiton and Funtastic Limited do not exhibit the same financial strength in their cash flow statements. The report also examines the impact of cash flows on dividend payments, capital expenditures, and working capital, and it identifies common trends, such as negative cash flows from investing activities. The analysis provides insights into the financial health of the companies and their ability to manage cash effectively, making it a valuable resource for understanding corporate accounting and financial decision-making.

Running head: ISSUES IN CASH FLOW STATEMENT

Issues in Cash Flow Statement

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Issues in Cash Flow Statement

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ISSUES IN CASH FLOW STATEMENT

Abstract:

The fundamental objective of the report is to include the evaluation of various cash flow

aspects in three organisations, which include BHP Billiton, Santos Limited and Funtastic

Limited. The report is effective to develop an insight on the various components of the

cash flow statement. It has been analysed that that Santos Limited is able to generate

considerable amount of cash flows from financing activities, which is considerable

beneficial for the business operations of the entity. However, for BHP Billiton and

Funtastic Limited, these aspects are not evident from their cash flow statements. Thus,

Santos Limited out of the three organisations only possesses the capability of

repayment of borrowings within the stipulated time. Therefore, for lending purpose,

Santos Limitred is evaluated to be the most appropriate entity out of the three

organisations.

Abstract:

The fundamental objective of the report is to include the evaluation of various cash flow

aspects in three organisations, which include BHP Billiton, Santos Limited and Funtastic

Limited. The report is effective to develop an insight on the various components of the

cash flow statement. It has been analysed that that Santos Limited is able to generate

considerable amount of cash flows from financing activities, which is considerable

beneficial for the business operations of the entity. However, for BHP Billiton and

Funtastic Limited, these aspects are not evident from their cash flow statements. Thus,

Santos Limited out of the three organisations only possesses the capability of

repayment of borrowings within the stipulated time. Therefore, for lending purpose,

Santos Limitred is evaluated to be the most appropriate entity out of the three

organisations.

2ISSUES IN CASH FLOW STATEMENT

Table of Contents

Introduction:.......................................................................................................................3

Part A:................................................................................................................................3

Part B:................................................................................................................................4

Requirement 1:...............................................................................................................4

Question a:.................................................................................................................4

Question b:.................................................................................................................4

Question c:.................................................................................................................5

Question d:.................................................................................................................5

Question e:.................................................................................................................5

Question f:..................................................................................................................5

Question g:.................................................................................................................6

Question h:.................................................................................................................6

Question i:..................................................................................................................7

Question j:..................................................................................................................7

Question k:.................................................................................................................7

Question l:..................................................................................................................8

Requirement 2:...............................................................................................................8

Requirement 3:...............................................................................................................9

Conclusion:........................................................................................................................9

References:......................................................................................................................10

Table of Contents

Introduction:.......................................................................................................................3

Part A:................................................................................................................................3

Part B:................................................................................................................................4

Requirement 1:...............................................................................................................4

Question a:.................................................................................................................4

Question b:.................................................................................................................4

Question c:.................................................................................................................5

Question d:.................................................................................................................5

Question e:.................................................................................................................5

Question f:..................................................................................................................5

Question g:.................................................................................................................6

Question h:.................................................................................................................6

Question i:..................................................................................................................7

Question j:..................................................................................................................7

Question k:.................................................................................................................7

Question l:..................................................................................................................8

Requirement 2:...............................................................................................................8

Requirement 3:...............................................................................................................9

Conclusion:........................................................................................................................9

References:......................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ISSUES IN CASH FLOW STATEMENT

Introduction:

Cash flow statement is deemed to be one of the important financial statements

for the organisations that show the effect of the modifications of the income statement

and balance sheet statement accounts on the cash and cash equivalents and such

statement divides the analysis into three activities that comprise of operating, financing

and investing activities (Afrifa 2016). The sound overview regarding the various aspects

of cash flows is required for the management of the entities to make sound business

decisions. The fundamental objective of the report is to include the evaluation of various

cash flow aspects in three organisations, which include BHP Billiton, Santos Limited and

Funtastic Limited. The report is effective to develop an insight on the various

components of the cash flow statement.

Part A:

The cash flow statement as well as the income statement is of immense use for

the investors and the reasons are provided as follows:

Cash flow statement:

This statement is adjudged as one of the vital financial statements for the

investors, as it provides crucial information regarding the cash availability of any

business organisation. In order to ensure organisational success, there should be

sufficient amount of cash in the business so that it could settle its expenses, taxes, bank

loans and payment for buying new assets (Atanasov and Black 2016). By analysing the

cash flow statement, an investor could find out the cash availability for the following

purposes. The income statements do not provide any kind of information about the

principal business payments; however, the cash flow statement provides information to

the investors about those areas where principal payments are made by the entity, From

the cash flow statement, the cash indicator could be observed in different circumstances

such as rise in inventory, credit extension to the customers, buying capital equipment

and others, which could not be reported in the consolidated income statement (Ball et

al. 2016). In compliance with the cash flow statement, it is possible for the investors to

obtain an understanding of whether the firm is lacking money despite having adequate

amount of profit in hand. In addition to this, the owners could have an understanding of

whether they are withdrawing too much capital out of the business. By combining all

these aspects, the investors could be able to undertake sound investment decisions

after critical evaluation of the cash flow statement (Bilinski 2014).

Income statement:

One of the critical financial reports is the income statement, which is beneficial to

the investors having the requirement to obtain necessary information before they

undertake investment decisions. The statement provides all the necessary information

to the investors like sales, operational efficacy and profit to various other non-operating

aspects. Such information helps the investors to obtain concise and clear picture of the

existing business performance as well as the future expectations. As a result, income

statement is considered as a reliable measure in order to evaluate the business

conditions (Chang et al. 2014).

Introduction:

Cash flow statement is deemed to be one of the important financial statements

for the organisations that show the effect of the modifications of the income statement

and balance sheet statement accounts on the cash and cash equivalents and such

statement divides the analysis into three activities that comprise of operating, financing

and investing activities (Afrifa 2016). The sound overview regarding the various aspects

of cash flows is required for the management of the entities to make sound business

decisions. The fundamental objective of the report is to include the evaluation of various

cash flow aspects in three organisations, which include BHP Billiton, Santos Limited and

Funtastic Limited. The report is effective to develop an insight on the various

components of the cash flow statement.

Part A:

The cash flow statement as well as the income statement is of immense use for

the investors and the reasons are provided as follows:

Cash flow statement:

This statement is adjudged as one of the vital financial statements for the

investors, as it provides crucial information regarding the cash availability of any

business organisation. In order to ensure organisational success, there should be

sufficient amount of cash in the business so that it could settle its expenses, taxes, bank

loans and payment for buying new assets (Atanasov and Black 2016). By analysing the

cash flow statement, an investor could find out the cash availability for the following

purposes. The income statements do not provide any kind of information about the

principal business payments; however, the cash flow statement provides information to

the investors about those areas where principal payments are made by the entity, From

the cash flow statement, the cash indicator could be observed in different circumstances

such as rise in inventory, credit extension to the customers, buying capital equipment

and others, which could not be reported in the consolidated income statement (Ball et

al. 2016). In compliance with the cash flow statement, it is possible for the investors to

obtain an understanding of whether the firm is lacking money despite having adequate

amount of profit in hand. In addition to this, the owners could have an understanding of

whether they are withdrawing too much capital out of the business. By combining all

these aspects, the investors could be able to undertake sound investment decisions

after critical evaluation of the cash flow statement (Bilinski 2014).

Income statement:

One of the critical financial reports is the income statement, which is beneficial to

the investors having the requirement to obtain necessary information before they

undertake investment decisions. The statement provides all the necessary information

to the investors like sales, operational efficacy and profit to various other non-operating

aspects. Such information helps the investors to obtain concise and clear picture of the

existing business performance as well as the future expectations. As a result, income

statement is considered as a reliable measure in order to evaluate the business

conditions (Chang et al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ISSUES IN CASH FLOW STATEMENT

The income statement is vital for the investors, since it provides clear indication

about the profit generating ability of the firm. The total revenue and expenses are

recorded in the income statement and by deducting the latter from the former, profit or

loss is calculated appropriately (Collins, Hribar and Tian 2014). This information could

be found only by the investors in the consolidated income statement. Moreover, the

operations are updated timely in the income statement, since update could be made

more rapidly in comparison to the other financial statements. Owing to the fact that clear

and concise overview of the current profitability of the firm is provided in the income

statement, the business managers and the investors analyse the income statement

continuously for obtaining the updated information on business operation. The investors

obtain the categorisation of various revenues and expenses of the firm from the income

statements (Cui 2017). This implies the usefulness of the income statement to the

investors, as they could have the needed information in order to make investment

decisions.

Therefore, it could be stated that the investors are benefitted by analysing the

cash flow statement as well as the income statement.

Part B:

Requirement 1:

Question a:

Funtastic Limited:

For this organisation, cash is received mainly from the sales made to the

customers, amount received from loans provided and issuance of shares. On the other

hand, cash is incurred for clearing the payments of the employees and the suppliers,

business operations, finance cost and other expenses, plant and equipment, intangible

assets and share issuance cost (DeFusco et al. 2015).

BHP Billiton:

BHP Billiton is observed to receive cash mainly from trade and other receivables,

amount received from interest-bearing loans, receipt of interest from loan provided and

dividend from shares in other firms. On the contrary, it has incurred cash mainly for

depreciation and amortisation, trade and other payables, impairment, net finance

expense, payment of interest, royalty tax, income tax, exploration expense, purchase of

property, plant and equipment, repaying interest-bearing loans and payment of dividend

to the shareholders (Donovan et al. 2014).

Santos Limited:

Santos Limited receives cash mainly from credit sales made to the customers,

interest on borrowings provided, pipeline tariffs and others. However, it incurs cash

mainly for settling the payments of its staffs and suppliers, interest on loan taken, oil and

gas assets, repayment of borrowings and oil and gas assets (Douglas, Huang and

Vetzal 2016).

Question b:

In terms of cash flow from continuing operations, Santos Limited and BHP Billiton

are observed to follow similar pattern, since they have produced positive cash flows

The income statement is vital for the investors, since it provides clear indication

about the profit generating ability of the firm. The total revenue and expenses are

recorded in the income statement and by deducting the latter from the former, profit or

loss is calculated appropriately (Collins, Hribar and Tian 2014). This information could

be found only by the investors in the consolidated income statement. Moreover, the

operations are updated timely in the income statement, since update could be made

more rapidly in comparison to the other financial statements. Owing to the fact that clear

and concise overview of the current profitability of the firm is provided in the income

statement, the business managers and the investors analyse the income statement

continuously for obtaining the updated information on business operation. The investors

obtain the categorisation of various revenues and expenses of the firm from the income

statements (Cui 2017). This implies the usefulness of the income statement to the

investors, as they could have the needed information in order to make investment

decisions.

Therefore, it could be stated that the investors are benefitted by analysing the

cash flow statement as well as the income statement.

Part B:

Requirement 1:

Question a:

Funtastic Limited:

For this organisation, cash is received mainly from the sales made to the

customers, amount received from loans provided and issuance of shares. On the other

hand, cash is incurred for clearing the payments of the employees and the suppliers,

business operations, finance cost and other expenses, plant and equipment, intangible

assets and share issuance cost (DeFusco et al. 2015).

BHP Billiton:

BHP Billiton is observed to receive cash mainly from trade and other receivables,

amount received from interest-bearing loans, receipt of interest from loan provided and

dividend from shares in other firms. On the contrary, it has incurred cash mainly for

depreciation and amortisation, trade and other payables, impairment, net finance

expense, payment of interest, royalty tax, income tax, exploration expense, purchase of

property, plant and equipment, repaying interest-bearing loans and payment of dividend

to the shareholders (Donovan et al. 2014).

Santos Limited:

Santos Limited receives cash mainly from credit sales made to the customers,

interest on borrowings provided, pipeline tariffs and others. However, it incurs cash

mainly for settling the payments of its staffs and suppliers, interest on loan taken, oil and

gas assets, repayment of borrowings and oil and gas assets (Douglas, Huang and

Vetzal 2016).

Question b:

In terms of cash flow from continuing operations, Santos Limited and BHP Billiton

are observed to follow similar pattern, since they have produced positive cash flows

5ISSUES IN CASH FLOW STATEMENT

from their business operations. However, in case of Funtastic Limited, the cash flows

from continuing operations are found to be negative (Drobetz, Haller and Meier 2016).

Question c:

For BHP Billiton, the net income is observed to be more when contrasted with the

cash flow from operations. One of the crucial profitability measures is net income and

cash flows from operations reveal the relevant adjustments made to the net income;

thereby, creating the difference (Henderson et al. 2015). There are some items that are

not treated in a similar manner in the cash flow statement and the income statement.

There is no consideration of non-cash expenses in the income statement that constitute

of share-based payments, amortisation and depreciation. However, such costs do not

minimise the cash amount, which an entity generates in a specific year. Therefore,

addition is made to the cash flow statement, which leads to the difference (Hoskin,

Fizzell and Cherry 2014).

Question d:

Funtastic Limited:

The cash flows from operations are observed to be negative for Funtastic

Limited, which is not sufficient in order to pay capital expenditures that constitute of

plant and equipment payment as well as payment for other intangible assets.

BHP Billiton:

The cash flows from operations of BHP Billiton are positive and they are

sufficient when it comes to settling the capital expenditures comprising of property, plant

and equipment as well as exploration expenditure.

Santos Limited:

Like BHP Billiton, the cash flows from operations are found to be positive for BHP

Billiton as well. However, it is not sufficient for the firm to settle its capital expenditures

including exploration and evaluation assets, land, building, oil and gas assets,

settlement of cost of borrowings, subsidiary acquisition and plant and equipment (Kraft

and Schwartz 2015).

Question e:

No dividend payment is made by Funtastic Limited; however, dividend payment

is made by both BHP Billiton and Santos Limited. It could be observed that BHP Billiton

has adequate cash flows from operations that cover both capital expenditure and

payment of dividend, as higher operating cash flows could be observed compared to the

combination of dividend payment and capital expenditure. On the other hand, inability

could be observed in Santos Limited in settling its dividend payment from operating

cash flows, as it is not sufficient to settle capital expenditure (Lee 2014).

Question f:

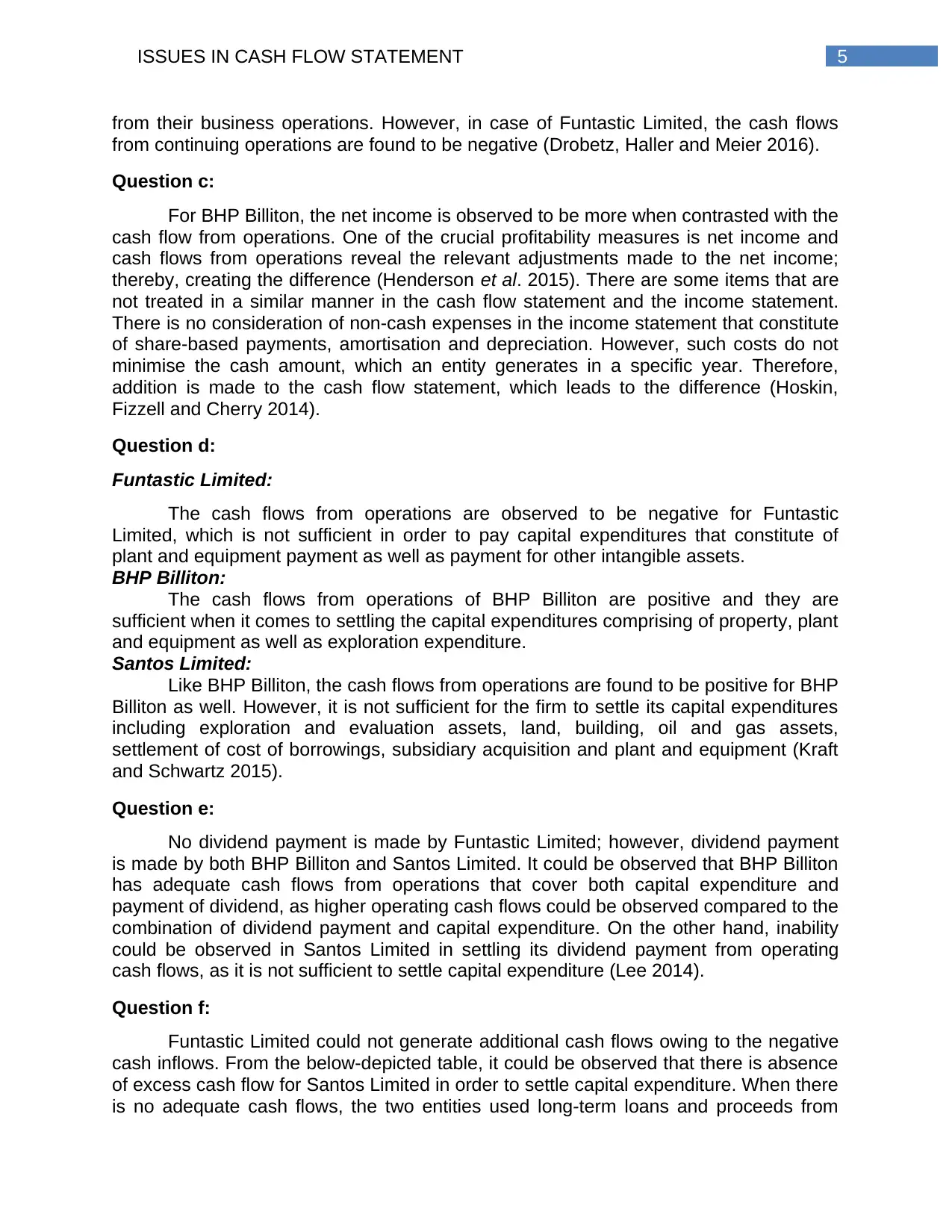

Funtastic Limited could not generate additional cash flows owing to the negative

cash inflows. From the below-depicted table, it could be observed that there is absence

of excess cash flow for Santos Limited in order to settle capital expenditure. When there

is no adequate cash flows, the two entities used long-term loans and proceeds from

from their business operations. However, in case of Funtastic Limited, the cash flows

from continuing operations are found to be negative (Drobetz, Haller and Meier 2016).

Question c:

For BHP Billiton, the net income is observed to be more when contrasted with the

cash flow from operations. One of the crucial profitability measures is net income and

cash flows from operations reveal the relevant adjustments made to the net income;

thereby, creating the difference (Henderson et al. 2015). There are some items that are

not treated in a similar manner in the cash flow statement and the income statement.

There is no consideration of non-cash expenses in the income statement that constitute

of share-based payments, amortisation and depreciation. However, such costs do not

minimise the cash amount, which an entity generates in a specific year. Therefore,

addition is made to the cash flow statement, which leads to the difference (Hoskin,

Fizzell and Cherry 2014).

Question d:

Funtastic Limited:

The cash flows from operations are observed to be negative for Funtastic

Limited, which is not sufficient in order to pay capital expenditures that constitute of

plant and equipment payment as well as payment for other intangible assets.

BHP Billiton:

The cash flows from operations of BHP Billiton are positive and they are

sufficient when it comes to settling the capital expenditures comprising of property, plant

and equipment as well as exploration expenditure.

Santos Limited:

Like BHP Billiton, the cash flows from operations are found to be positive for BHP

Billiton as well. However, it is not sufficient for the firm to settle its capital expenditures

including exploration and evaluation assets, land, building, oil and gas assets,

settlement of cost of borrowings, subsidiary acquisition and plant and equipment (Kraft

and Schwartz 2015).

Question e:

No dividend payment is made by Funtastic Limited; however, dividend payment

is made by both BHP Billiton and Santos Limited. It could be observed that BHP Billiton

has adequate cash flows from operations that cover both capital expenditure and

payment of dividend, as higher operating cash flows could be observed compared to the

combination of dividend payment and capital expenditure. On the other hand, inability

could be observed in Santos Limited in settling its dividend payment from operating

cash flows, as it is not sufficient to settle capital expenditure (Lee 2014).

Question f:

Funtastic Limited could not generate additional cash flows owing to the negative

cash inflows. From the below-depicted table, it could be observed that there is absence

of excess cash flow for Santos Limited in order to settle capital expenditure. When there

is no adequate cash flows, the two entities used long-term loans and proceeds from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ISSUES IN CASH FLOW STATEMENT

other aspects such as selling portions of their fixed assets in order to generate cash for

paying the capital expenditure (Lewellen and Lewellen 2016).

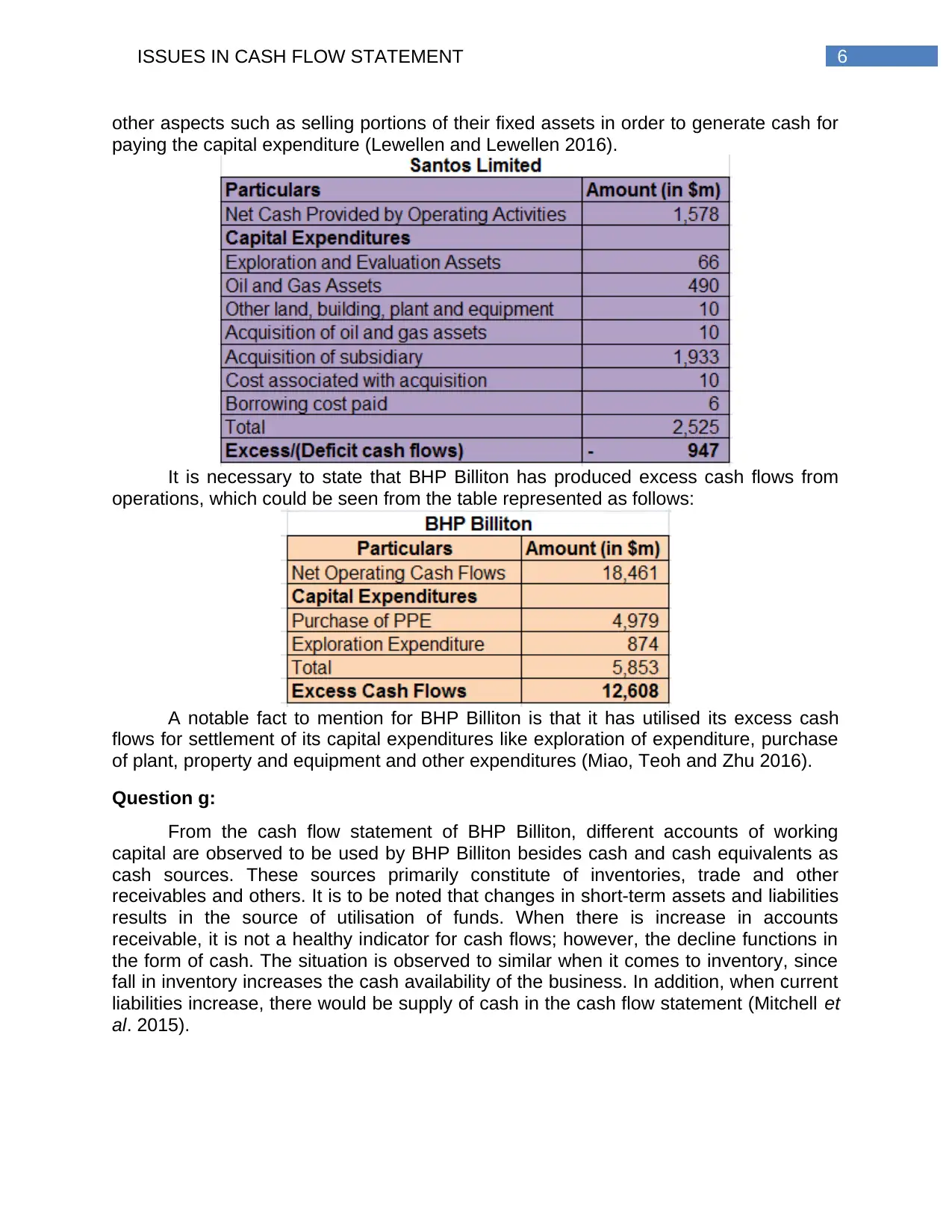

It is necessary to state that BHP Billiton has produced excess cash flows from

operations, which could be seen from the table represented as follows:

A notable fact to mention for BHP Billiton is that it has utilised its excess cash

flows for settlement of its capital expenditures like exploration of expenditure, purchase

of plant, property and equipment and other expenditures (Miao, Teoh and Zhu 2016).

Question g:

From the cash flow statement of BHP Billiton, different accounts of working

capital are observed to be used by BHP Billiton besides cash and cash equivalents as

cash sources. These sources primarily constitute of inventories, trade and other

receivables and others. It is to be noted that changes in short-term assets and liabilities

results in the source of utilisation of funds. When there is increase in accounts

receivable, it is not a healthy indicator for cash flows; however, the decline functions in

the form of cash. The situation is observed to similar when it comes to inventory, since

fall in inventory increases the cash availability of the business. In addition, when current

liabilities increase, there would be supply of cash in the cash flow statement (Mitchell et

al. 2015).

other aspects such as selling portions of their fixed assets in order to generate cash for

paying the capital expenditure (Lewellen and Lewellen 2016).

It is necessary to state that BHP Billiton has produced excess cash flows from

operations, which could be seen from the table represented as follows:

A notable fact to mention for BHP Billiton is that it has utilised its excess cash

flows for settlement of its capital expenditures like exploration of expenditure, purchase

of plant, property and equipment and other expenditures (Miao, Teoh and Zhu 2016).

Question g:

From the cash flow statement of BHP Billiton, different accounts of working

capital are observed to be used by BHP Billiton besides cash and cash equivalents as

cash sources. These sources primarily constitute of inventories, trade and other

receivables and others. It is to be noted that changes in short-term assets and liabilities

results in the source of utilisation of funds. When there is increase in accounts

receivable, it is not a healthy indicator for cash flows; however, the decline functions in

the form of cash. The situation is observed to similar when it comes to inventory, since

fall in inventory increases the cash availability of the business. In addition, when current

liabilities increase, there would be supply of cash in the cash flow statement (Mitchell et

al. 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ISSUES IN CASH FLOW STATEMENT

Question h:

Cash flows are affected by a number of items and one such item could be

identified as the tax payments. If the firms do not preserve considerable cash amount,

they are needed to incur heavy tax payments having effect on the cash flows. Another

influential dynamic includes the repayment of long-term borrowings. It could be

observed that the entities have to utilise significant cash amount so that they could

repay long-term loans and this is observed to have adverse influence on their cash

flows (Nekhili et al. 2016).

Question i:

One common trend is similar among all the firms and they include the presence

of negative cash flows from investing activities. In other words, it could be stated that

these organisations have lower capital income in contrast to their capital expenditures.

Moreover, another similar trend in capital expenditure for the firms includes the

settlement of the payment for non-current assets like plant, property and equipment. For

BHP Billiton and Funtastic Limited, fluctuations could be seen in capital expenditures of

these entities between 2016 and 2018. However, for Santos Limited, capital

expenditures have increased steadily in the same period, which is a necessary aspect

for consideration (Palea 2014).

Question j:

Based on the cash flow statement of Funtastic Limited, it could be observed that

there is absence of any dividend for the firm between 2016 and 2018. BHP Billiton is

observed to incur normal dividend as well as non-controlling interest dividend and

based on the trend; the firm has raised the payment of dividend in the existing year.

Even though Santos Limited is observed to receive dividend, the trend is found to be

declining in the current period. In addition, dividend is incurred in 2018 when no

dividend is provided in the past period (Robinson et al. 2015).

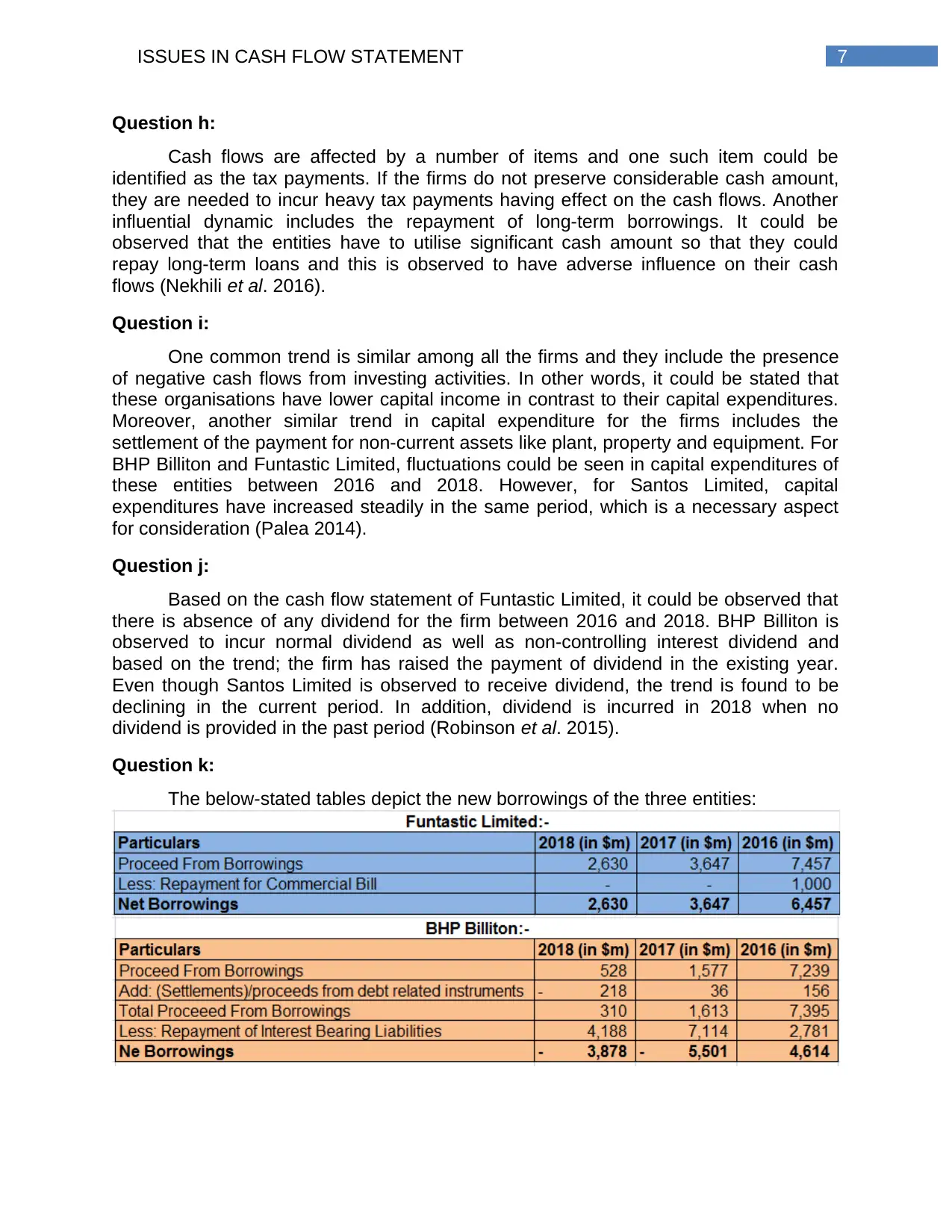

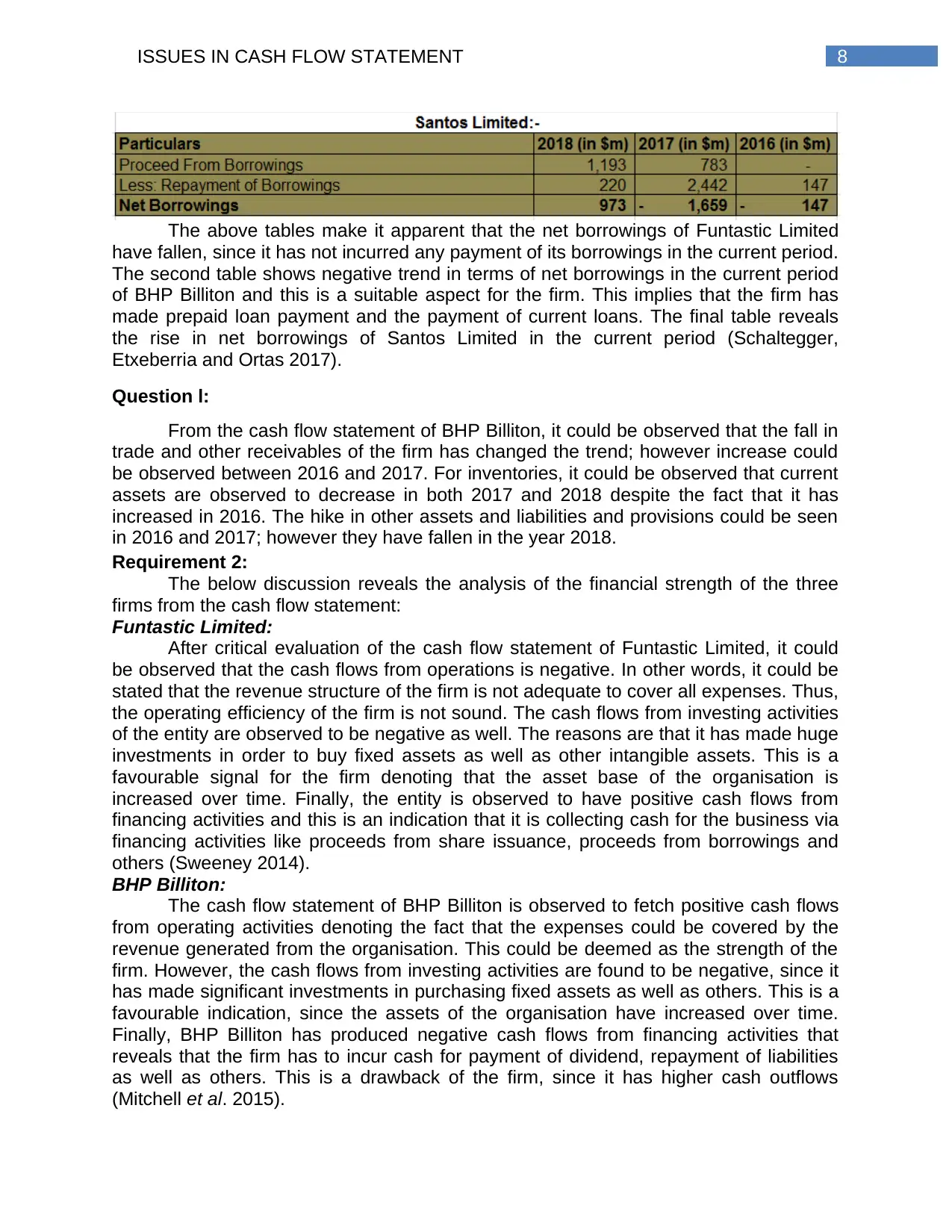

Question k:

The below-stated tables depict the new borrowings of the three entities:

Question h:

Cash flows are affected by a number of items and one such item could be

identified as the tax payments. If the firms do not preserve considerable cash amount,

they are needed to incur heavy tax payments having effect on the cash flows. Another

influential dynamic includes the repayment of long-term borrowings. It could be

observed that the entities have to utilise significant cash amount so that they could

repay long-term loans and this is observed to have adverse influence on their cash

flows (Nekhili et al. 2016).

Question i:

One common trend is similar among all the firms and they include the presence

of negative cash flows from investing activities. In other words, it could be stated that

these organisations have lower capital income in contrast to their capital expenditures.

Moreover, another similar trend in capital expenditure for the firms includes the

settlement of the payment for non-current assets like plant, property and equipment. For

BHP Billiton and Funtastic Limited, fluctuations could be seen in capital expenditures of

these entities between 2016 and 2018. However, for Santos Limited, capital

expenditures have increased steadily in the same period, which is a necessary aspect

for consideration (Palea 2014).

Question j:

Based on the cash flow statement of Funtastic Limited, it could be observed that

there is absence of any dividend for the firm between 2016 and 2018. BHP Billiton is

observed to incur normal dividend as well as non-controlling interest dividend and

based on the trend; the firm has raised the payment of dividend in the existing year.

Even though Santos Limited is observed to receive dividend, the trend is found to be

declining in the current period. In addition, dividend is incurred in 2018 when no

dividend is provided in the past period (Robinson et al. 2015).

Question k:

The below-stated tables depict the new borrowings of the three entities:

8ISSUES IN CASH FLOW STATEMENT

The above tables make it apparent that the net borrowings of Funtastic Limited

have fallen, since it has not incurred any payment of its borrowings in the current period.

The second table shows negative trend in terms of net borrowings in the current period

of BHP Billiton and this is a suitable aspect for the firm. This implies that the firm has

made prepaid loan payment and the payment of current loans. The final table reveals

the rise in net borrowings of Santos Limited in the current period (Schaltegger,

Etxeberria and Ortas 2017).

Question l:

From the cash flow statement of BHP Billiton, it could be observed that the fall in

trade and other receivables of the firm has changed the trend; however increase could

be observed between 2016 and 2017. For inventories, it could be observed that current

assets are observed to decrease in both 2017 and 2018 despite the fact that it has

increased in 2016. The hike in other assets and liabilities and provisions could be seen

in 2016 and 2017; however they have fallen in the year 2018.

Requirement 2:

The below discussion reveals the analysis of the financial strength of the three

firms from the cash flow statement:

Funtastic Limited:

After critical evaluation of the cash flow statement of Funtastic Limited, it could

be observed that the cash flows from operations is negative. In other words, it could be

stated that the revenue structure of the firm is not adequate to cover all expenses. Thus,

the operating efficiency of the firm is not sound. The cash flows from investing activities

of the entity are observed to be negative as well. The reasons are that it has made huge

investments in order to buy fixed assets as well as other intangible assets. This is a

favourable signal for the firm denoting that the asset base of the organisation is

increased over time. Finally, the entity is observed to have positive cash flows from

financing activities and this is an indication that it is collecting cash for the business via

financing activities like proceeds from share issuance, proceeds from borrowings and

others (Sweeney 2014).

BHP Billiton:

The cash flow statement of BHP Billiton is observed to fetch positive cash flows

from operating activities denoting the fact that the expenses could be covered by the

revenue generated from the organisation. This could be deemed as the strength of the

firm. However, the cash flows from investing activities are found to be negative, since it

has made significant investments in purchasing fixed assets as well as others. This is a

favourable indication, since the assets of the organisation have increased over time.

Finally, BHP Billiton has produced negative cash flows from financing activities that

reveals that the firm has to incur cash for payment of dividend, repayment of liabilities

as well as others. This is a drawback of the firm, since it has higher cash outflows

(Mitchell et al. 2015).

The above tables make it apparent that the net borrowings of Funtastic Limited

have fallen, since it has not incurred any payment of its borrowings in the current period.

The second table shows negative trend in terms of net borrowings in the current period

of BHP Billiton and this is a suitable aspect for the firm. This implies that the firm has

made prepaid loan payment and the payment of current loans. The final table reveals

the rise in net borrowings of Santos Limited in the current period (Schaltegger,

Etxeberria and Ortas 2017).

Question l:

From the cash flow statement of BHP Billiton, it could be observed that the fall in

trade and other receivables of the firm has changed the trend; however increase could

be observed between 2016 and 2017. For inventories, it could be observed that current

assets are observed to decrease in both 2017 and 2018 despite the fact that it has

increased in 2016. The hike in other assets and liabilities and provisions could be seen

in 2016 and 2017; however they have fallen in the year 2018.

Requirement 2:

The below discussion reveals the analysis of the financial strength of the three

firms from the cash flow statement:

Funtastic Limited:

After critical evaluation of the cash flow statement of Funtastic Limited, it could

be observed that the cash flows from operations is negative. In other words, it could be

stated that the revenue structure of the firm is not adequate to cover all expenses. Thus,

the operating efficiency of the firm is not sound. The cash flows from investing activities

of the entity are observed to be negative as well. The reasons are that it has made huge

investments in order to buy fixed assets as well as other intangible assets. This is a

favourable signal for the firm denoting that the asset base of the organisation is

increased over time. Finally, the entity is observed to have positive cash flows from

financing activities and this is an indication that it is collecting cash for the business via

financing activities like proceeds from share issuance, proceeds from borrowings and

others (Sweeney 2014).

BHP Billiton:

The cash flow statement of BHP Billiton is observed to fetch positive cash flows

from operating activities denoting the fact that the expenses could be covered by the

revenue generated from the organisation. This could be deemed as the strength of the

firm. However, the cash flows from investing activities are found to be negative, since it

has made significant investments in purchasing fixed assets as well as others. This is a

favourable indication, since the assets of the organisation have increased over time.

Finally, BHP Billiton has produced negative cash flows from financing activities that

reveals that the firm has to incur cash for payment of dividend, repayment of liabilities

as well as others. This is a drawback of the firm, since it has higher cash outflows

(Mitchell et al. 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ISSUES IN CASH FLOW STATEMENT

Santos Limited:

The cash flow statement of Santos Limited makes it apparent that the cash flows

from operating activities of the entity are found to be positive. This is a sound prospect

for the entity since, it denotes the ability of the entity in producing cash flows from

operating activities. Along with this, it could be observed that the cash flows from

investing activities of the organisation are found to be negative because it has

purchased different fixed assets along with acquisition of other businesses. This is a

sound aspect from the business perspective of Santos Limited. The cash flows from

investing activities are found to be positive for Santos Limited as well because of

earnings made from the provided loans. This represents that the entity is producing

cash from the investing activities. These aspects reveal sound financial condition of the

firm necessary to ensure business success (Henderson et al. 2015).

Requirement 3:

According to the cash flow statement of Santos Limited, it is evident that the

organisation has produced positive cash flows from operating activities over three-year

period. The values are $1,578 million, $1,248 million and $840 million respectively in

2016, 2017 and 2018. In addition, it has received the maximum money owing to its

customers amounting to $3,740 million. This implies that the entity has provided

maximum fees from its core operations of the business. Besides, it has been identified

that the entity has made heavy investment in order to purchase fixed assets such as oil

and gas assets, exploration assets, building, land, plant, new business acquisition as

well as others (Kraft and Schwartz 2015). These aspects indicate that the firm is

planning to expand its business operations and activities, which is a favourable signal.

Finally, it could be observed that Santos Limited is able to generate considerable

amount of cash flows from financing activities, which is considerable beneficial for the

business operations of the entity. Hence, these factors state that Santos Limited has

managed to increase its business strength considerably over the years. However, for

BHP Billiton and Funtastic Limited, these aspects are not evident from their cash flow

statements. Thus, Santos Limited out of the three organisations only possesses the

capability of repayment of borrowings within the stipulated time. Therefore, for lending

purpose, Santos Limitred is evaluated to be the most appropriate entity out of the three

organisations.

Conclusion:

Based on the above discussion, it could be stated that one of the critical financial

reports is the income statement, which is beneficial to the investors having the

requirement to obtain necessary information before they undertake investment

decisions. The statement provides all the necessary information to the investors like

sales, operational efficacy and profit to various other non-operating aspects. On the

other hand, the cash flow statement is adjudged as one of the vital financial statements

for the investors, as it provides crucial information regarding the cash availability of any

business organisation. In order to ensure organisational success, there should be

sufficient amount of cash in the business so that it could settle its expenses, taxes, bank

loans and payment for buying new assets.

It has been analysed that that Santos Limited is able to generate considerable

amount of cash flows from financing activities, which is considerable beneficial for the

Santos Limited:

The cash flow statement of Santos Limited makes it apparent that the cash flows

from operating activities of the entity are found to be positive. This is a sound prospect

for the entity since, it denotes the ability of the entity in producing cash flows from

operating activities. Along with this, it could be observed that the cash flows from

investing activities of the organisation are found to be negative because it has

purchased different fixed assets along with acquisition of other businesses. This is a

sound aspect from the business perspective of Santos Limited. The cash flows from

investing activities are found to be positive for Santos Limited as well because of

earnings made from the provided loans. This represents that the entity is producing

cash from the investing activities. These aspects reveal sound financial condition of the

firm necessary to ensure business success (Henderson et al. 2015).

Requirement 3:

According to the cash flow statement of Santos Limited, it is evident that the

organisation has produced positive cash flows from operating activities over three-year

period. The values are $1,578 million, $1,248 million and $840 million respectively in

2016, 2017 and 2018. In addition, it has received the maximum money owing to its

customers amounting to $3,740 million. This implies that the entity has provided

maximum fees from its core operations of the business. Besides, it has been identified

that the entity has made heavy investment in order to purchase fixed assets such as oil

and gas assets, exploration assets, building, land, plant, new business acquisition as

well as others (Kraft and Schwartz 2015). These aspects indicate that the firm is

planning to expand its business operations and activities, which is a favourable signal.

Finally, it could be observed that Santos Limited is able to generate considerable

amount of cash flows from financing activities, which is considerable beneficial for the

business operations of the entity. Hence, these factors state that Santos Limited has

managed to increase its business strength considerably over the years. However, for

BHP Billiton and Funtastic Limited, these aspects are not evident from their cash flow

statements. Thus, Santos Limited out of the three organisations only possesses the

capability of repayment of borrowings within the stipulated time. Therefore, for lending

purpose, Santos Limitred is evaluated to be the most appropriate entity out of the three

organisations.

Conclusion:

Based on the above discussion, it could be stated that one of the critical financial

reports is the income statement, which is beneficial to the investors having the

requirement to obtain necessary information before they undertake investment

decisions. The statement provides all the necessary information to the investors like

sales, operational efficacy and profit to various other non-operating aspects. On the

other hand, the cash flow statement is adjudged as one of the vital financial statements

for the investors, as it provides crucial information regarding the cash availability of any

business organisation. In order to ensure organisational success, there should be

sufficient amount of cash in the business so that it could settle its expenses, taxes, bank

loans and payment for buying new assets.

It has been analysed that that Santos Limited is able to generate considerable

amount of cash flows from financing activities, which is considerable beneficial for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ISSUES IN CASH FLOW STATEMENT

business operations of the entity. However, for BHP Billiton and Funtastic Limited, these

aspects are not evident from their cash flow statements. Thus, Santos Limited out of the

three organisations only possesses the capability of repayment of borrowings within the

stipulated time. Therefore, for lending purpose, Santos Limitred is evaluated to be the

most appropriate entity out of the three organisations.

business operations of the entity. However, for BHP Billiton and Funtastic Limited, these

aspects are not evident from their cash flow statements. Thus, Santos Limited out of the

three organisations only possesses the capability of repayment of borrowings within the

stipulated time. Therefore, for lending purpose, Santos Limitred is evaluated to be the

most appropriate entity out of the three organisations.

11ISSUES IN CASH FLOW STATEMENT

References:

Afrifa, G.A., 2016. Net working capital, cash flow and performance of UK SMEs. Review

of Accounting and Finance, 15(1), pp.21-44.

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Ball, R., Gerakos, J., Linnainmaa, J.T. and Nikolaev, V., 2016. Accruals, cash flows,

and operating profitability in the cross section of stock returns. Journal of Financial

Economics, 121(1), pp.28-45.

Bilinski, P., 2014. Do analysts disclose cash flow forecasts with earnings estimates

when earnings quality is low?. Journal of Business Finance & Accounting, 41(3-4),

pp.401-434.

Chang, X., Dasgupta, S., Wong, G. and Yao, J., 2014. Cash-flow sensitivities and the

allocation of internal cash flow. The Review of Financial Studies, 27(12), pp.3628-3657.

Collins, D.W., Hribar, P. and Tian, X.S., 2014. Cash flow asymmetry: Causes and

implications for conditional conservatism research. Journal of Accounting and

Economics, 58(2-3), pp.173-200.

Cui, W., 2017. Destination-based cash-flow taxation: A critical appraisal. University of

Toronto Law Journal, 67(3), pp.301-347.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

Donovan, J., Frankel, R., Lee, J., Martin, X. and Seo, H., 2014. Issues raised by

studying DeFond and Zhang: What should audit researchers do?. Journal of Accounting

and Economics, 58(2-3), pp.327-338.

Douglas, A.V., Huang, A.G. and Vetzal, K.R., 2016. Cash flow volatility and corporate

bond yield spreads. Review of Quantitative Finance and Accounting, 46(2), pp.417-458.

Drobetz, W., Haller, R. and Meier, I., 2016. Cash flow sensitivities during normal and

crisis times: Evidence from shipping. Transportation Research Part A: Policy and

Practice, 90, pp.26-49.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user

perspective. Wiley Global Education.

Kraft, H. and Schwartz, E., 2015. Cash flow multipliers and optimal investment

decisions. European Financial Management, 21(3), pp.399-429.

Lee, T.A., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an

Accounting Practice. Routledge.

Lewellen, J. and Lewellen, K., 2016. Investment and cash flow: New evidence. Journal

of Financial and Quantitative Analysis, 51(4), pp.1135-1164.

Miao, B., Teoh, S.H. and Zhu, Z., 2016. Limited attention, statement of cash flow

disclosure, and the valuation of accruals. Review of Accounting Studies, 21(2), pp.473-

515.

Mitchell, R.K., Van Buren III, H.J., Greenwood, M. and Freeman, R.E., 2015.

Stakeholder inclusion and accounting for stakeholders. Journal of Management

Studies, 52(7), pp.851-877.

References:

Afrifa, G.A., 2016. Net working capital, cash flow and performance of UK SMEs. Review

of Accounting and Finance, 15(1), pp.21-44.

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Ball, R., Gerakos, J., Linnainmaa, J.T. and Nikolaev, V., 2016. Accruals, cash flows,

and operating profitability in the cross section of stock returns. Journal of Financial

Economics, 121(1), pp.28-45.

Bilinski, P., 2014. Do analysts disclose cash flow forecasts with earnings estimates

when earnings quality is low?. Journal of Business Finance & Accounting, 41(3-4),

pp.401-434.

Chang, X., Dasgupta, S., Wong, G. and Yao, J., 2014. Cash-flow sensitivities and the

allocation of internal cash flow. The Review of Financial Studies, 27(12), pp.3628-3657.

Collins, D.W., Hribar, P. and Tian, X.S., 2014. Cash flow asymmetry: Causes and

implications for conditional conservatism research. Journal of Accounting and

Economics, 58(2-3), pp.173-200.

Cui, W., 2017. Destination-based cash-flow taxation: A critical appraisal. University of

Toronto Law Journal, 67(3), pp.301-347.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

Donovan, J., Frankel, R., Lee, J., Martin, X. and Seo, H., 2014. Issues raised by

studying DeFond and Zhang: What should audit researchers do?. Journal of Accounting

and Economics, 58(2-3), pp.327-338.

Douglas, A.V., Huang, A.G. and Vetzal, K.R., 2016. Cash flow volatility and corporate

bond yield spreads. Review of Quantitative Finance and Accounting, 46(2), pp.417-458.

Drobetz, W., Haller, R. and Meier, I., 2016. Cash flow sensitivities during normal and

crisis times: Evidence from shipping. Transportation Research Part A: Policy and

Practice, 90, pp.26-49.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user

perspective. Wiley Global Education.

Kraft, H. and Schwartz, E., 2015. Cash flow multipliers and optimal investment

decisions. European Financial Management, 21(3), pp.399-429.

Lee, T.A., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an

Accounting Practice. Routledge.

Lewellen, J. and Lewellen, K., 2016. Investment and cash flow: New evidence. Journal

of Financial and Quantitative Analysis, 51(4), pp.1135-1164.

Miao, B., Teoh, S.H. and Zhu, Z., 2016. Limited attention, statement of cash flow

disclosure, and the valuation of accruals. Review of Accounting Studies, 21(2), pp.473-

515.

Mitchell, R.K., Van Buren III, H.J., Greenwood, M. and Freeman, R.E., 2015.

Stakeholder inclusion and accounting for stakeholders. Journal of Management

Studies, 52(7), pp.851-877.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.