Issues in Cash Flow Statement

VerifiedAdded on 2023/04/03

|11

|3493

|100

AI Summary

This report assesses the various aspects of cash flows related to three organizations, BHP Billiton, Santos Limited, and Funtastic Limited. It provides insight into the cash flow components and their significance to investors and financial reports users. The analysis identifies the main sources and utilization of cash for each organization. Recommendations are made based on the cash flow positions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ISSUES IN CASH FLOW STATEMENT

Issues in Cash Flow Statement

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Issues in Cash Flow Statement

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ISSUES IN CASH FLOW STATEMENT

Abstract:

The objective of this report is to assess the various aspects of cash flows related to

three organisations, which include BHP Billiton, Santos Limited and Funtastic Limited.

The report is considered to be useful in developing insight on the various cash flow

components. It has been evaluated that the income statement and the cash flow

statement provide the investors with significant crucial information when it comes to

undertaking investment decisions and the two statements have significance to the users

of the financial reports. Moreover, from the above discussion, it could be seen that the

cash flow statement plays a pivotal role in order to ascertain the financial position and

financial strength of an organisation. The above analysis has assisted in the

identification of the main sources of cash along with their utilisation by Funtastic Limited,

BHP Billiton and Santos Limited. Santos Limited is observed to have sound cash flow

position, as positive cash flows have been generated by the organisation from its

financing and operating activities in order to settle its obligations. By considering all

these aspects, it is recommended to the creditors to lend to Santos Limited, since it

possesses the ability of settling its borrowings within the scheduled time.

Abstract:

The objective of this report is to assess the various aspects of cash flows related to

three organisations, which include BHP Billiton, Santos Limited and Funtastic Limited.

The report is considered to be useful in developing insight on the various cash flow

components. It has been evaluated that the income statement and the cash flow

statement provide the investors with significant crucial information when it comes to

undertaking investment decisions and the two statements have significance to the users

of the financial reports. Moreover, from the above discussion, it could be seen that the

cash flow statement plays a pivotal role in order to ascertain the financial position and

financial strength of an organisation. The above analysis has assisted in the

identification of the main sources of cash along with their utilisation by Funtastic Limited,

BHP Billiton and Santos Limited. Santos Limited is observed to have sound cash flow

position, as positive cash flows have been generated by the organisation from its

financing and operating activities in order to settle its obligations. By considering all

these aspects, it is recommended to the creditors to lend to Santos Limited, since it

possesses the ability of settling its borrowings within the scheduled time.

2ISSUES IN CASH FLOW STATEMENT

Table of Contents

Introduction:.......................................................................................................................3

Part A:................................................................................................................................3

Part B:................................................................................................................................4

Requirement 1:...............................................................................................................4

Requirement 2:...............................................................................................................7

Requirement 3:...............................................................................................................8

Conclusion:........................................................................................................................8

References;......................................................................................................................10

Table of Contents

Introduction:.......................................................................................................................3

Part A:................................................................................................................................3

Part B:................................................................................................................................4

Requirement 1:...............................................................................................................4

Requirement 2:...............................................................................................................7

Requirement 3:...............................................................................................................8

Conclusion:........................................................................................................................8

References;......................................................................................................................10

3ISSUES IN CASH FLOW STATEMENT

Introduction:

One of the significant financial statements is the cash flow statement for the

organisations that depicts the impact of the alterations in income and balance sheet

statements on the cash and cash equivalents. The statement separates the analysis

into operating, financing and investing activities (Atanasov and Black 2016). The

management needs to have a clear insight of the various cash flow aspects for

undertaking sound business decisions. The objective of this report is to assess the

various aspects of cash flows related to three organisations, which include BHP Billiton,

Santos Limited and Funtastic Limited. The report is considered to be useful in

developing insight on the various cash flow components.

Part A:

The income statement and the cash flow statement are considered to be highly

beneficial for the investors owing to the following reasons:

Income statement:

This is a useful financial report for the investors, as they require detailed

information before investing in an organisation. With the help of this statement, the

investors are provided with all information like revenue, profit and operating efficiency to

various other non-operational aspects. By using this information, the investors could

have a clear overview of the existing business performance as well as the future

expectations (Baños-Caballero, García-Teruel and Martínez-Solano 2014). Owing to

this reason, the income statement could be adjudged as a trustworthy source in order to

judge the condition of the organisations.

In other words, the income statement is crucial for the investors, since it provides

a concise picture of the profitability position of an organisation. The statement is

involved in recording overall business revenue and expenses and profit or loss is

computed by deducting total expenses from total revenue (Bedford and Ziegler 2016).

This information could be found only by the investors in the income statement.

Moreover, the income statement depicts timely update of the business operations, as it

is updated more often than the other financial statements. Owing to the fact that the

income statement provides concise and clear picture of the existing profitability of an

organisation, the business managers and the investors are involved in continual review

of the income statement to find the updated information on the business operations. The

investors obtain the classification of various expenses and revenue of the organisations

from the income statements (Dang, Li and Yang 2018). In the presence of all these

aspects, it could be stated that the income statement is valuable for the investors, as

they are provided with necessary information for undertaking investment decisions.

Cash flow statement:

Cash flow statement is deemed to be another significant financial statement for

the investors, as it provides information regarding the cash position of the organisation.

In order to ensure business success, adequate cash flows need to be present for

repayment of expenses (Ehrhardt and Brigham 2016). Thus, with the help of cash flow

statement, it becomes possible to ascertain whether an organisation has significant

cash for fulfilling the above purposes. The income statements do not provide any

Introduction:

One of the significant financial statements is the cash flow statement for the

organisations that depicts the impact of the alterations in income and balance sheet

statements on the cash and cash equivalents. The statement separates the analysis

into operating, financing and investing activities (Atanasov and Black 2016). The

management needs to have a clear insight of the various cash flow aspects for

undertaking sound business decisions. The objective of this report is to assess the

various aspects of cash flows related to three organisations, which include BHP Billiton,

Santos Limited and Funtastic Limited. The report is considered to be useful in

developing insight on the various cash flow components.

Part A:

The income statement and the cash flow statement are considered to be highly

beneficial for the investors owing to the following reasons:

Income statement:

This is a useful financial report for the investors, as they require detailed

information before investing in an organisation. With the help of this statement, the

investors are provided with all information like revenue, profit and operating efficiency to

various other non-operational aspects. By using this information, the investors could

have a clear overview of the existing business performance as well as the future

expectations (Baños-Caballero, García-Teruel and Martínez-Solano 2014). Owing to

this reason, the income statement could be adjudged as a trustworthy source in order to

judge the condition of the organisations.

In other words, the income statement is crucial for the investors, since it provides

a concise picture of the profitability position of an organisation. The statement is

involved in recording overall business revenue and expenses and profit or loss is

computed by deducting total expenses from total revenue (Bedford and Ziegler 2016).

This information could be found only by the investors in the income statement.

Moreover, the income statement depicts timely update of the business operations, as it

is updated more often than the other financial statements. Owing to the fact that the

income statement provides concise and clear picture of the existing profitability of an

organisation, the business managers and the investors are involved in continual review

of the income statement to find the updated information on the business operations. The

investors obtain the classification of various expenses and revenue of the organisations

from the income statements (Dang, Li and Yang 2018). In the presence of all these

aspects, it could be stated that the income statement is valuable for the investors, as

they are provided with necessary information for undertaking investment decisions.

Cash flow statement:

Cash flow statement is deemed to be another significant financial statement for

the investors, as it provides information regarding the cash position of the organisation.

In order to ensure business success, adequate cash flows need to be present for

repayment of expenses (Ehrhardt and Brigham 2016). Thus, with the help of cash flow

statement, it becomes possible to ascertain whether an organisation has significant

cash for fulfilling the above purposes. The income statements do not provide any

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ISSUES IN CASH FLOW STATEMENT

information regarding the principal business payments. However, the cash flow

statements inform the investors regarding the areas of the organisation, in which

principal payments are made. In accordance with the cash flow statement, the indication

of utilising cash could be observed in a variety of situations such as extending credit

terms of the customers, rise in inventory, buying capital equipment and others that could

not be represented in the income statement (Ferran and Ho 2014). By analysing the

cash flow statement, the investors could obtain an in-depth overview of whether an

organisation is suffering from cash shortage despite having sound profitability position.

Along with this, the owners could know if they are drawing too much money from the

business funds. When all such information is available, it becomes easy for the

investors to undertake sound investment decisions (Fourie et al. 2015). By combining all

the aspects, it could be stated that the income statement and the cash flow statement

are deemed to be valuable for the investors.

Part B:

Requirement 1:

a) In case of Funtastic Limited, the significant sources of cash include customer

receipts, proceeds from borrowings and issuance of shares and the significant uses for

cash include supplier and staff payments, cash used from operations, interest and other

expenses, plant and equipment payment along with intangible assets and share issue

cost (Fracassi 2016).

In case of BHP Billiton, the significant cash sources include trade and other

receivables, interest and dividend received, proceeds from interest bearing liabilities.

Cash is used for net finance cost, amortisation and depreciation, trade and other

payables, impairment, payment of interest, payment of royalty-related taxation, income

tax, exploration expense, purchase of plant and equipment, repaying interest payment

liabilities and payment of dividend (Frino, Hill and Chen 2015).

In case of Santos Limited, cash is received from customer receipts, amount

received from borrowings, pipeline tariffs. On the other hand, cash is incurred on

supplier and staff payments, borrowing cost payment, oil and gas assets’ payments,

subsidiary acquisition and borrowing repayment (Gippel, Smith and Zhu 2015).

b) Both BHP Billiton and Santos Limited are observed to follow similar trend owing to

the fact that they have generated positive cash flows from their business operations.

However, for Funtastic Limited, the trend is observed to be negative due to generation

of negative cash flows (Gitman, Juchau and Flanagan 2015).

c) The net income of BHP Billiton is lower compared to its cash flows. Net profit is a

significant profitability measure, while the operating cash flows depicts the crucial

adjustments made to net profit and this is the significant reason behind the difference

(Gullifer and Payne 2015). The treatment is different for certain items in the cash flow

statement in contrast to the income statement. The income statement needs to include

non-cash expenses like amortisation, depreciation and share-based payments;

however, these expenses do not minimise the cash amount generated by an

organisation in a specific period. As a result, these items are added to the cash flow

statement as well and thus, difference could be seen (Haas 2014).

information regarding the principal business payments. However, the cash flow

statements inform the investors regarding the areas of the organisation, in which

principal payments are made. In accordance with the cash flow statement, the indication

of utilising cash could be observed in a variety of situations such as extending credit

terms of the customers, rise in inventory, buying capital equipment and others that could

not be represented in the income statement (Ferran and Ho 2014). By analysing the

cash flow statement, the investors could obtain an in-depth overview of whether an

organisation is suffering from cash shortage despite having sound profitability position.

Along with this, the owners could know if they are drawing too much money from the

business funds. When all such information is available, it becomes easy for the

investors to undertake sound investment decisions (Fourie et al. 2015). By combining all

the aspects, it could be stated that the income statement and the cash flow statement

are deemed to be valuable for the investors.

Part B:

Requirement 1:

a) In case of Funtastic Limited, the significant sources of cash include customer

receipts, proceeds from borrowings and issuance of shares and the significant uses for

cash include supplier and staff payments, cash used from operations, interest and other

expenses, plant and equipment payment along with intangible assets and share issue

cost (Fracassi 2016).

In case of BHP Billiton, the significant cash sources include trade and other

receivables, interest and dividend received, proceeds from interest bearing liabilities.

Cash is used for net finance cost, amortisation and depreciation, trade and other

payables, impairment, payment of interest, payment of royalty-related taxation, income

tax, exploration expense, purchase of plant and equipment, repaying interest payment

liabilities and payment of dividend (Frino, Hill and Chen 2015).

In case of Santos Limited, cash is received from customer receipts, amount

received from borrowings, pipeline tariffs. On the other hand, cash is incurred on

supplier and staff payments, borrowing cost payment, oil and gas assets’ payments,

subsidiary acquisition and borrowing repayment (Gippel, Smith and Zhu 2015).

b) Both BHP Billiton and Santos Limited are observed to follow similar trend owing to

the fact that they have generated positive cash flows from their business operations.

However, for Funtastic Limited, the trend is observed to be negative due to generation

of negative cash flows (Gitman, Juchau and Flanagan 2015).

c) The net income of BHP Billiton is lower compared to its cash flows. Net profit is a

significant profitability measure, while the operating cash flows depicts the crucial

adjustments made to net profit and this is the significant reason behind the difference

(Gullifer and Payne 2015). The treatment is different for certain items in the cash flow

statement in contrast to the income statement. The income statement needs to include

non-cash expenses like amortisation, depreciation and share-based payments;

however, these expenses do not minimise the cash amount generated by an

organisation in a specific period. As a result, these items are added to the cash flow

statement as well and thus, difference could be seen (Haas 2014).

5ISSUES IN CASH FLOW STATEMENT

d) Funtastic Limited has negative operating cash flows, which is not sufficient for

payment of capital expenses, which include intangible asset payment and purchase of

plant and equipment.

For BHP Billiton, operating cash flows are found to be positive in order to pay for

capital expenses including exploration expense and purchase of plant and equipment.

Although Santos Limited has positive operating cash flows, they are not sufficient

to cover the capital expenses, which include evaluation and exploration of assets, land

and building, oil and gas assets, subsidiary acquisition, acquisition costs and borrowing

cost payment (Hillier et al. 2014).

e) Funtastic Limited has not paid any dividend, while Santos Limited and BHP Billiton

have paid dividend to the shareholders. It could be observed that the operating cash

flows of BHP Billiton are sufficient to cover dividend payment as well as capital

expenditure, as the operating cash flows are more compared to the combination of

dividend payment and capital expenses. Santos Limited has been unable to pay

dividend from its operating cash flows, since capital expense could not be settled with

the generated operating cash flows (Johnson, McLaughlin and Haueter 2015).

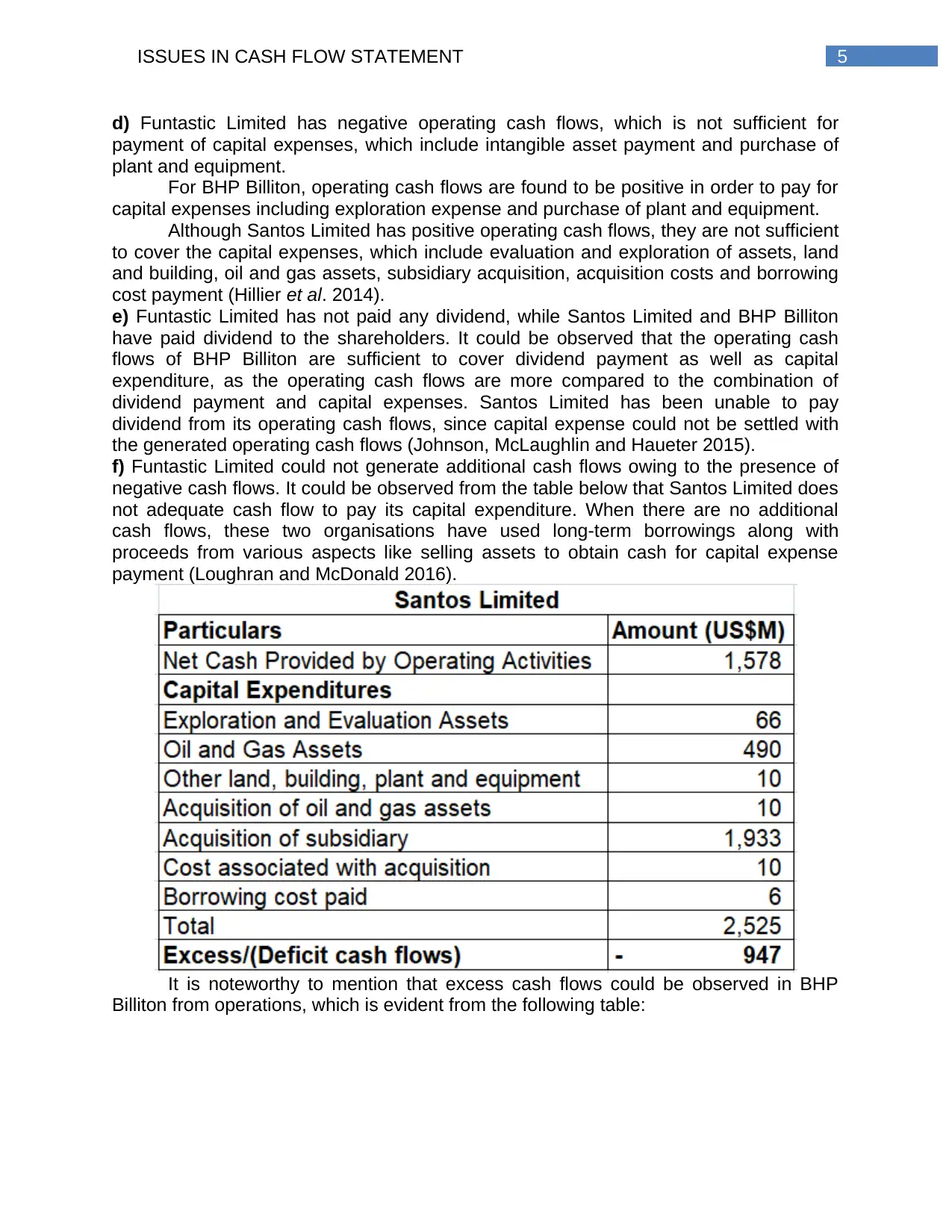

f) Funtastic Limited could not generate additional cash flows owing to the presence of

negative cash flows. It could be observed from the table below that Santos Limited does

not adequate cash flow to pay its capital expenditure. When there are no additional

cash flows, these two organisations have used long-term borrowings along with

proceeds from various aspects like selling assets to obtain cash for capital expense

payment (Loughran and McDonald 2016).

It is noteworthy to mention that excess cash flows could be observed in BHP

Billiton from operations, which is evident from the following table:

d) Funtastic Limited has negative operating cash flows, which is not sufficient for

payment of capital expenses, which include intangible asset payment and purchase of

plant and equipment.

For BHP Billiton, operating cash flows are found to be positive in order to pay for

capital expenses including exploration expense and purchase of plant and equipment.

Although Santos Limited has positive operating cash flows, they are not sufficient

to cover the capital expenses, which include evaluation and exploration of assets, land

and building, oil and gas assets, subsidiary acquisition, acquisition costs and borrowing

cost payment (Hillier et al. 2014).

e) Funtastic Limited has not paid any dividend, while Santos Limited and BHP Billiton

have paid dividend to the shareholders. It could be observed that the operating cash

flows of BHP Billiton are sufficient to cover dividend payment as well as capital

expenditure, as the operating cash flows are more compared to the combination of

dividend payment and capital expenses. Santos Limited has been unable to pay

dividend from its operating cash flows, since capital expense could not be settled with

the generated operating cash flows (Johnson, McLaughlin and Haueter 2015).

f) Funtastic Limited could not generate additional cash flows owing to the presence of

negative cash flows. It could be observed from the table below that Santos Limited does

not adequate cash flow to pay its capital expenditure. When there are no additional

cash flows, these two organisations have used long-term borrowings along with

proceeds from various aspects like selling assets to obtain cash for capital expense

payment (Loughran and McDonald 2016).

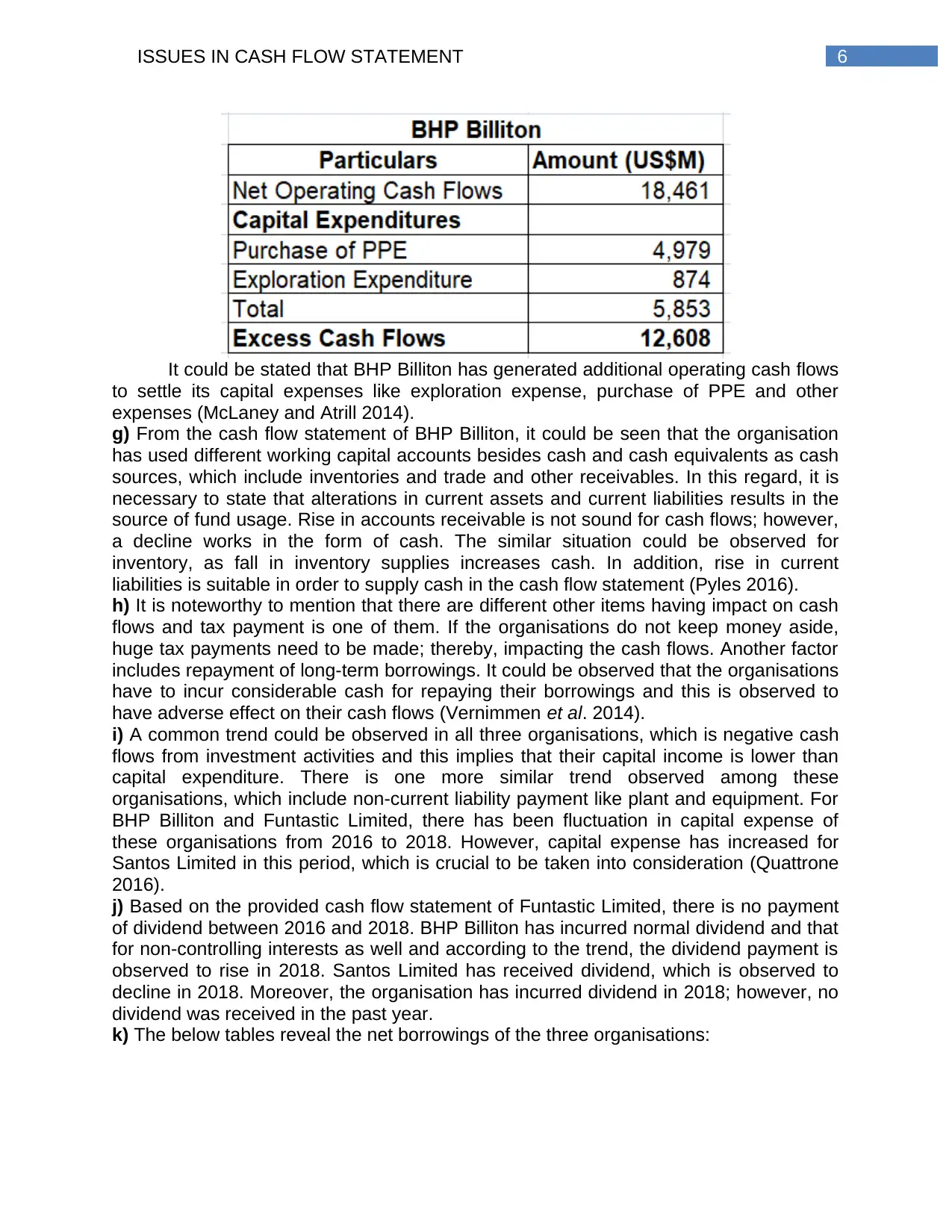

It is noteworthy to mention that excess cash flows could be observed in BHP

Billiton from operations, which is evident from the following table:

6ISSUES IN CASH FLOW STATEMENT

It could be stated that BHP Billiton has generated additional operating cash flows

to settle its capital expenses like exploration expense, purchase of PPE and other

expenses (McLaney and Atrill 2014).

g) From the cash flow statement of BHP Billiton, it could be seen that the organisation

has used different working capital accounts besides cash and cash equivalents as cash

sources, which include inventories and trade and other receivables. In this regard, it is

necessary to state that alterations in current assets and current liabilities results in the

source of fund usage. Rise in accounts receivable is not sound for cash flows; however,

a decline works in the form of cash. The similar situation could be observed for

inventory, as fall in inventory supplies increases cash. In addition, rise in current

liabilities is suitable in order to supply cash in the cash flow statement (Pyles 2016).

h) It is noteworthy to mention that there are different other items having impact on cash

flows and tax payment is one of them. If the organisations do not keep money aside,

huge tax payments need to be made; thereby, impacting the cash flows. Another factor

includes repayment of long-term borrowings. It could be observed that the organisations

have to incur considerable cash for repaying their borrowings and this is observed to

have adverse effect on their cash flows (Vernimmen et al. 2014).

i) A common trend could be observed in all three organisations, which is negative cash

flows from investment activities and this implies that their capital income is lower than

capital expenditure. There is one more similar trend observed among these

organisations, which include non-current liability payment like plant and equipment. For

BHP Billiton and Funtastic Limited, there has been fluctuation in capital expense of

these organisations from 2016 to 2018. However, capital expense has increased for

Santos Limited in this period, which is crucial to be taken into consideration (Quattrone

2016).

j) Based on the provided cash flow statement of Funtastic Limited, there is no payment

of dividend between 2016 and 2018. BHP Billiton has incurred normal dividend and that

for non-controlling interests as well and according to the trend, the dividend payment is

observed to rise in 2018. Santos Limited has received dividend, which is observed to

decline in 2018. Moreover, the organisation has incurred dividend in 2018; however, no

dividend was received in the past year.

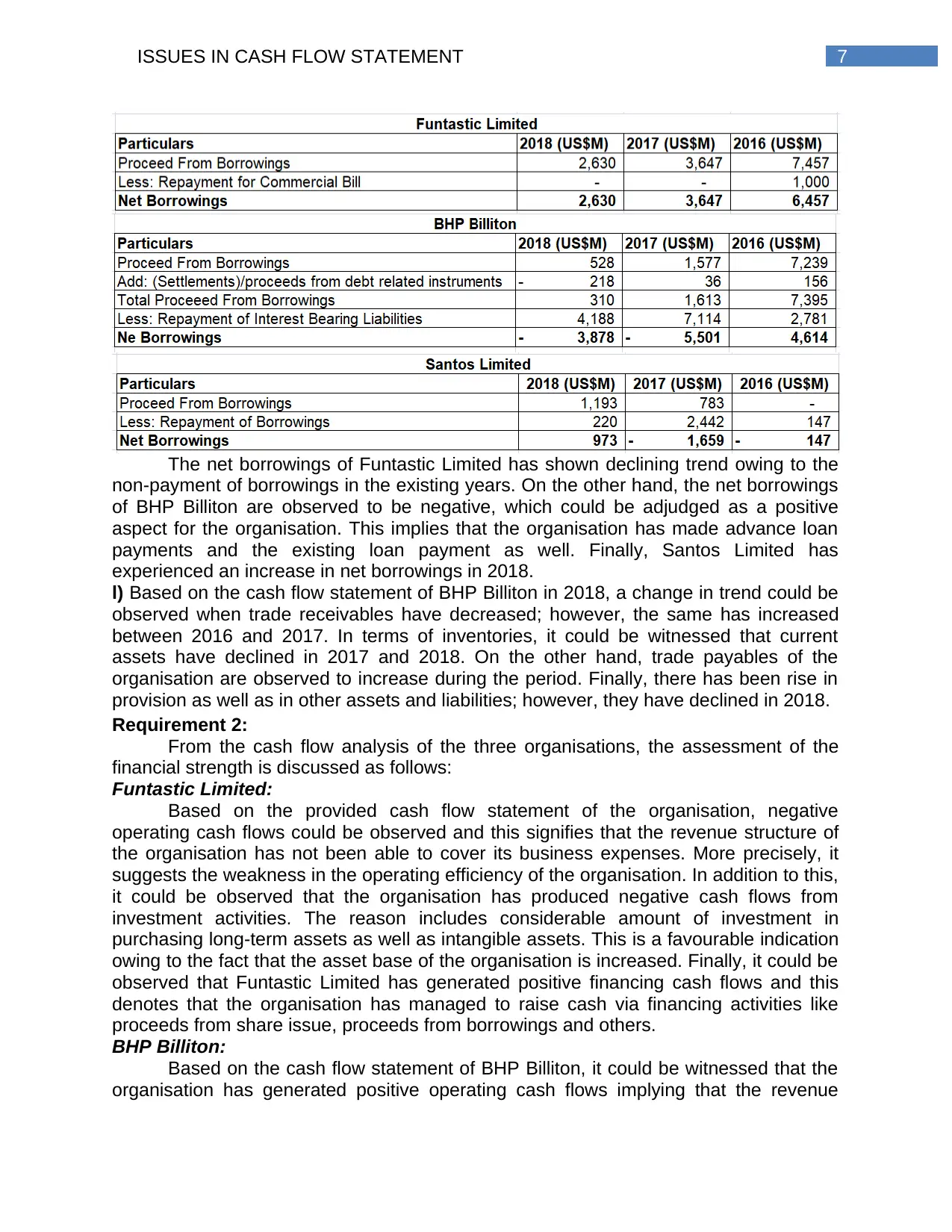

k) The below tables reveal the net borrowings of the three organisations:

It could be stated that BHP Billiton has generated additional operating cash flows

to settle its capital expenses like exploration expense, purchase of PPE and other

expenses (McLaney and Atrill 2014).

g) From the cash flow statement of BHP Billiton, it could be seen that the organisation

has used different working capital accounts besides cash and cash equivalents as cash

sources, which include inventories and trade and other receivables. In this regard, it is

necessary to state that alterations in current assets and current liabilities results in the

source of fund usage. Rise in accounts receivable is not sound for cash flows; however,

a decline works in the form of cash. The similar situation could be observed for

inventory, as fall in inventory supplies increases cash. In addition, rise in current

liabilities is suitable in order to supply cash in the cash flow statement (Pyles 2016).

h) It is noteworthy to mention that there are different other items having impact on cash

flows and tax payment is one of them. If the organisations do not keep money aside,

huge tax payments need to be made; thereby, impacting the cash flows. Another factor

includes repayment of long-term borrowings. It could be observed that the organisations

have to incur considerable cash for repaying their borrowings and this is observed to

have adverse effect on their cash flows (Vernimmen et al. 2014).

i) A common trend could be observed in all three organisations, which is negative cash

flows from investment activities and this implies that their capital income is lower than

capital expenditure. There is one more similar trend observed among these

organisations, which include non-current liability payment like plant and equipment. For

BHP Billiton and Funtastic Limited, there has been fluctuation in capital expense of

these organisations from 2016 to 2018. However, capital expense has increased for

Santos Limited in this period, which is crucial to be taken into consideration (Quattrone

2016).

j) Based on the provided cash flow statement of Funtastic Limited, there is no payment

of dividend between 2016 and 2018. BHP Billiton has incurred normal dividend and that

for non-controlling interests as well and according to the trend, the dividend payment is

observed to rise in 2018. Santos Limited has received dividend, which is observed to

decline in 2018. Moreover, the organisation has incurred dividend in 2018; however, no

dividend was received in the past year.

k) The below tables reveal the net borrowings of the three organisations:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ISSUES IN CASH FLOW STATEMENT

The net borrowings of Funtastic Limited has shown declining trend owing to the

non-payment of borrowings in the existing years. On the other hand, the net borrowings

of BHP Billiton are observed to be negative, which could be adjudged as a positive

aspect for the organisation. This implies that the organisation has made advance loan

payments and the existing loan payment as well. Finally, Santos Limited has

experienced an increase in net borrowings in 2018.

l) Based on the cash flow statement of BHP Billiton in 2018, a change in trend could be

observed when trade receivables have decreased; however, the same has increased

between 2016 and 2017. In terms of inventories, it could be witnessed that current

assets have declined in 2017 and 2018. On the other hand, trade payables of the

organisation are observed to increase during the period. Finally, there has been rise in

provision as well as in other assets and liabilities; however, they have declined in 2018.

Requirement 2:

From the cash flow analysis of the three organisations, the assessment of the

financial strength is discussed as follows:

Funtastic Limited:

Based on the provided cash flow statement of the organisation, negative

operating cash flows could be observed and this signifies that the revenue structure of

the organisation has not been able to cover its business expenses. More precisely, it

suggests the weakness in the operating efficiency of the organisation. In addition to this,

it could be observed that the organisation has produced negative cash flows from

investment activities. The reason includes considerable amount of investment in

purchasing long-term assets as well as intangible assets. This is a favourable indication

owing to the fact that the asset base of the organisation is increased. Finally, it could be

observed that Funtastic Limited has generated positive financing cash flows and this

denotes that the organisation has managed to raise cash via financing activities like

proceeds from share issue, proceeds from borrowings and others.

BHP Billiton:

Based on the cash flow statement of BHP Billiton, it could be witnessed that the

organisation has generated positive operating cash flows implying that the revenue

The net borrowings of Funtastic Limited has shown declining trend owing to the

non-payment of borrowings in the existing years. On the other hand, the net borrowings

of BHP Billiton are observed to be negative, which could be adjudged as a positive

aspect for the organisation. This implies that the organisation has made advance loan

payments and the existing loan payment as well. Finally, Santos Limited has

experienced an increase in net borrowings in 2018.

l) Based on the cash flow statement of BHP Billiton in 2018, a change in trend could be

observed when trade receivables have decreased; however, the same has increased

between 2016 and 2017. In terms of inventories, it could be witnessed that current

assets have declined in 2017 and 2018. On the other hand, trade payables of the

organisation are observed to increase during the period. Finally, there has been rise in

provision as well as in other assets and liabilities; however, they have declined in 2018.

Requirement 2:

From the cash flow analysis of the three organisations, the assessment of the

financial strength is discussed as follows:

Funtastic Limited:

Based on the provided cash flow statement of the organisation, negative

operating cash flows could be observed and this signifies that the revenue structure of

the organisation has not been able to cover its business expenses. More precisely, it

suggests the weakness in the operating efficiency of the organisation. In addition to this,

it could be observed that the organisation has produced negative cash flows from

investment activities. The reason includes considerable amount of investment in

purchasing long-term assets as well as intangible assets. This is a favourable indication

owing to the fact that the asset base of the organisation is increased. Finally, it could be

observed that Funtastic Limited has generated positive financing cash flows and this

denotes that the organisation has managed to raise cash via financing activities like

proceeds from share issue, proceeds from borrowings and others.

BHP Billiton:

Based on the cash flow statement of BHP Billiton, it could be witnessed that the

organisation has generated positive operating cash flows implying that the revenue

8ISSUES IN CASH FLOW STATEMENT

structure of the organisation has covered all expenses, which could be adjudged as

strength of the organisation. However, BHP Billiton has provided negative investing

cash flows in order to purchase non-current assets and other investments. This is

deemed to be a favourable aspect for the organisation, which denotes rise in its asset

base. Finally, the financing cash flows of BHP Billiton are observed to be negative,

which reveals that it has to incur cash for making dividend payments, liability

repayments and others. This could be considered as a weakness for the organisation

because of significant cash outflows (Warren and Jones 2018).

Santos Limited:

As per the cash flow statement of Santos Limited, the organisation has earned

positive operating cash flows and this is a sound aspect when it comes to judging the

ability of a firm in operating cash flows. Moreover, it could be observed that the

organisation has generated negative investing cash flows because of purchasing

various classes of fixed assets and business acquisition. This could be adjudged as the

crucial positive aspect from the business perspective of Santos Limited. Along with this,

investing cash flows are observed to be positive for Santos Limited owing to the

drawdown of borrowings. This signifies the ability of the organisation in generating cash

from its investing activities. By combining all these aspects, it could be said that Santos

Limited has sound financial strength deemed to be crucial for ensuring business

success (Watson 2015).

Requirement 3:

It is apparent from the cash flow statement of Santos Limited that the

organisation has managed to earn positive operating cash flows between 2016 and

2018, the values of which are $1,578 million, $1,248 million and $840 million in 2016,

2017 and 2018 respectively. Moreover, it could be witnessed that Santos Limited has

obtained the maximum amount of receipts from customers valuing $3,740 million. This

clearly indicates the fact that majority of the fees are generated by the organisation from

its primary business operations. Besides this, it is clearly visible that the organisation

has made huge amount of investment in order to buy assets like oil and gas assets,

exploration assets, plant, building, land, new business acquisition as well as others.

These measures could be considered as the measures of business diversification

undertaken by the organisation so that it could increase its profitability further in future.

Finally, it could be observed that Santos Limited has been successful in generating

positive cash flows from financing activities, which is considerably useful from the

business viewpoint of the organisation. By combining all these aspects, it could be

stated that Santos Limited has increased its business strength over the years.

However, the above-stated aspects are deemed to be missing for BHP Billiton

and Funtastic Limited. When all these aspects are taken into consideration, it could be

said that Santos Limited possesses the ability of repaying its borrowings within the

stipulated timeframe. Hence, for lending purpose, Santos Limited would be the first

choice for the creditors.

Conclusion:

It has been evaluated from the above discussion that the income statement and

the cash flow statement provide the investors with significant crucial information when it

comes to undertaking investment decisions and the two statements have significance to

structure of the organisation has covered all expenses, which could be adjudged as

strength of the organisation. However, BHP Billiton has provided negative investing

cash flows in order to purchase non-current assets and other investments. This is

deemed to be a favourable aspect for the organisation, which denotes rise in its asset

base. Finally, the financing cash flows of BHP Billiton are observed to be negative,

which reveals that it has to incur cash for making dividend payments, liability

repayments and others. This could be considered as a weakness for the organisation

because of significant cash outflows (Warren and Jones 2018).

Santos Limited:

As per the cash flow statement of Santos Limited, the organisation has earned

positive operating cash flows and this is a sound aspect when it comes to judging the

ability of a firm in operating cash flows. Moreover, it could be observed that the

organisation has generated negative investing cash flows because of purchasing

various classes of fixed assets and business acquisition. This could be adjudged as the

crucial positive aspect from the business perspective of Santos Limited. Along with this,

investing cash flows are observed to be positive for Santos Limited owing to the

drawdown of borrowings. This signifies the ability of the organisation in generating cash

from its investing activities. By combining all these aspects, it could be said that Santos

Limited has sound financial strength deemed to be crucial for ensuring business

success (Watson 2015).

Requirement 3:

It is apparent from the cash flow statement of Santos Limited that the

organisation has managed to earn positive operating cash flows between 2016 and

2018, the values of which are $1,578 million, $1,248 million and $840 million in 2016,

2017 and 2018 respectively. Moreover, it could be witnessed that Santos Limited has

obtained the maximum amount of receipts from customers valuing $3,740 million. This

clearly indicates the fact that majority of the fees are generated by the organisation from

its primary business operations. Besides this, it is clearly visible that the organisation

has made huge amount of investment in order to buy assets like oil and gas assets,

exploration assets, plant, building, land, new business acquisition as well as others.

These measures could be considered as the measures of business diversification

undertaken by the organisation so that it could increase its profitability further in future.

Finally, it could be observed that Santos Limited has been successful in generating

positive cash flows from financing activities, which is considerably useful from the

business viewpoint of the organisation. By combining all these aspects, it could be

stated that Santos Limited has increased its business strength over the years.

However, the above-stated aspects are deemed to be missing for BHP Billiton

and Funtastic Limited. When all these aspects are taken into consideration, it could be

said that Santos Limited possesses the ability of repaying its borrowings within the

stipulated timeframe. Hence, for lending purpose, Santos Limited would be the first

choice for the creditors.

Conclusion:

It has been evaluated from the above discussion that the income statement and

the cash flow statement provide the investors with significant crucial information when it

comes to undertaking investment decisions and the two statements have significance to

9ISSUES IN CASH FLOW STATEMENT

the users of the financial reports. Moreover, from the above discussion, it could be seen

that the cash flow statement plays a pivotal role in order to ascertain the financial

position and financial strength of an organisation. The above analysis has assisted in

the identification of the main sources of cash along with their utilisation by Funtastic

Limited, BHP Billiton and Santos Limited.

As per the cash flow statement of Santos Limited, the organisation has earned

positive operating cash flows and this is a sound aspect when it comes to judging the

ability of a firm in operating cash flows. Moreover, it could be observed that the

organisation has generated negative investing cash flows because of purchasing

various classes of fixed assets and business acquisition. This could be adjudged as the

crucial positive aspect from the business perspective of Santos Limited. Along with this,

investing cash flows are observed to be positive for Santos Limited owing to the

drawdown of borrowings. This signifies the ability of the organisation in generating cash

from its investing activities. Santos Limited is observed to have sound cash flow

position, as positive cash flows have been generated by the organisation from its

financing and operating activities in order to settle its obligations. By considering all

these aspects, it is recommended to the creditors to lend to Santos Limited, since it

possesses the ability of settling its borrowings within the scheduled time.

the users of the financial reports. Moreover, from the above discussion, it could be seen

that the cash flow statement plays a pivotal role in order to ascertain the financial

position and financial strength of an organisation. The above analysis has assisted in

the identification of the main sources of cash along with their utilisation by Funtastic

Limited, BHP Billiton and Santos Limited.

As per the cash flow statement of Santos Limited, the organisation has earned

positive operating cash flows and this is a sound aspect when it comes to judging the

ability of a firm in operating cash flows. Moreover, it could be observed that the

organisation has generated negative investing cash flows because of purchasing

various classes of fixed assets and business acquisition. This could be adjudged as the

crucial positive aspect from the business perspective of Santos Limited. Along with this,

investing cash flows are observed to be positive for Santos Limited owing to the

drawdown of borrowings. This signifies the ability of the organisation in generating cash

from its investing activities. Santos Limited is observed to have sound cash flow

position, as positive cash flows have been generated by the organisation from its

financing and operating activities in order to settle its obligations. By considering all

these aspects, it is recommended to the creditors to lend to Santos Limited, since it

possesses the ability of settling its borrowings within the scheduled time.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ISSUES IN CASH FLOW STATEMENT

References;

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working

capital management, corporate performance, and financial constraints. Journal of

Business Research, 67(3), pp.332-338.

Bedford, N.M. and Ziegler, R.E., 2016. The contributions of AC Littleton to accounting

thought and practice. Memorial Articles for 20th Century American Accounting

Leaders, 49, p.219.

Dang, C., Li, Z.F. and Yang, C., 2018. Measuring firm size in empirical corporate

finance. Journal of Banking & Finance, 86, pp.159-176.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach.

Cengage learning.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University

Press.

Fourie, M.L., Opperman, L., Scott, D. and Kumar, K., 2015. Municipal finance and

accounting. Van Schaik Publishers.

Fracassi, C., 2016. Corporate finance policies and social networks. Management

Science, 63(8), pp.2420-2438.

Frino, A., Hill, A. and Chen, Z., 2015. Introduction to corporate finance. Pearson Higher

Education AU.

Gippel, J., Smith, T. and Zhu, Y., 2015. Endogeneity in accounting and finance

research: natural experiments as a state‐of‐the‐art solution. Abacus, 51(2), pp.143-168.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

Gullifer, L. and Payne, J., 2015. Corporate finance law: principles and policy.

Bloomsbury Publishing.

Haas, J.J., 2014. Corporate finance. West Academic.

Hillier, D., Clacher, I., Ross, S., Westerfield, R. and Jordan, B., 2014. Fundamentals of

corporate finance (No. 2nd Eu). McGraw Hill.

Johnson, C.J., McLaughlin, J. and Haueter, E.S., 2015. Corporate finance and the

securities laws. Wolters Kluwer Law & Business.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

McLaney, E.J. and Atrill, P., 2014. Accounting and finance: an introduction. New York:

Pearson.

Pyles, M., 2016. Applied Corporate Finance. Springer-Verlag New York.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

References;

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working

capital management, corporate performance, and financial constraints. Journal of

Business Research, 67(3), pp.332-338.

Bedford, N.M. and Ziegler, R.E., 2016. The contributions of AC Littleton to accounting

thought and practice. Memorial Articles for 20th Century American Accounting

Leaders, 49, p.219.

Dang, C., Li, Z.F. and Yang, C., 2018. Measuring firm size in empirical corporate

finance. Journal of Banking & Finance, 86, pp.159-176.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach.

Cengage learning.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University

Press.

Fourie, M.L., Opperman, L., Scott, D. and Kumar, K., 2015. Municipal finance and

accounting. Van Schaik Publishers.

Fracassi, C., 2016. Corporate finance policies and social networks. Management

Science, 63(8), pp.2420-2438.

Frino, A., Hill, A. and Chen, Z., 2015. Introduction to corporate finance. Pearson Higher

Education AU.

Gippel, J., Smith, T. and Zhu, Y., 2015. Endogeneity in accounting and finance

research: natural experiments as a state‐of‐the‐art solution. Abacus, 51(2), pp.143-168.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

Gullifer, L. and Payne, J., 2015. Corporate finance law: principles and policy.

Bloomsbury Publishing.

Haas, J.J., 2014. Corporate finance. West Academic.

Hillier, D., Clacher, I., Ross, S., Westerfield, R. and Jordan, B., 2014. Fundamentals of

corporate finance (No. 2nd Eu). McGraw Hill.

Johnson, C.J., McLaughlin, J. and Haueter, E.S., 2015. Corporate finance and the

securities laws. Wolters Kluwer Law & Business.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

McLaney, E.J. and Atrill, P., 2014. Accounting and finance: an introduction. New York:

Pearson.

Pyles, M., 2016. Applied Corporate Finance. Springer-Verlag New York.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.