Accounting Report Evaluation: REA Group Limited

VerifiedAdded on 2019/10/18

|11

|2234

|496

Essay

AI Summary

The assignment content discusses the preparation of accounting statements for REA Group Limited according to international accounting standards and best practices. The management has reported similar classes of items separately if material, provided clear and meaningful disclosures, and prepared the statements based on accrual accounting. Each statement has facilitated the provision of required information with a high degree of comparability. The report meets the objectives of general-purpose accounting reports. The target audience, including shareholders, stakeholders, creditors, debtors, and other third-party investors, can effectively utilize the report for decision-making. Additionally, the report demonstrates the enhancement of fundamental qualitative characteristics such as relevance, faithful representation, and verifiability.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Issues in Contemporary Accounting Theory

Name of the Student:

Name of the University:

Author Note

Issues in Contemporary Accounting Theory

Name of the Student:

Name of the University:

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Table of Contents

Introduction......................................................................................................................................3

Objectives of the general purpose accounting report......................................................................3

Have the target audience adequately used the report?.....................................................................5

Recognition criteria for the elements of the accounting statements................................................6

Fundamental qualitative characteristics of accounting report.........................................................6

Enhancing qualitative characteristic of the firm..............................................................................7

Conclusion.......................................................................................................................................7

References and Bibliography...........................................................................................................8

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Table of Contents

Introduction......................................................................................................................................3

Objectives of the general purpose accounting report......................................................................3

Have the target audience adequately used the report?.....................................................................5

Recognition criteria for the elements of the accounting statements................................................6

Fundamental qualitative characteristics of accounting report.........................................................6

Enhancing qualitative characteristic of the firm..............................................................................7

Conclusion.......................................................................................................................................7

References and Bibliography...........................................................................................................8

2

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Executive Summary

This particular study focuses upon the Australian corporate entity, REA Group Limited.

The annual report of this particular entity for the accounting year of 2017 has been evaluated in

order to find out the fact that whether accounting statements satisfy the required objectives of

accounting report, whether the company has satisfied the recognition criteria for the elements of

the accounting statements and other associated factors.

It has been found out that the management of the company has prepared the accounting

statements of the companies in regards to the issued standards of the regulatory bodies like the

Australian Accounting Standards Board.

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Executive Summary

This particular study focuses upon the Australian corporate entity, REA Group Limited.

The annual report of this particular entity for the accounting year of 2017 has been evaluated in

order to find out the fact that whether accounting statements satisfy the required objectives of

accounting report, whether the company has satisfied the recognition criteria for the elements of

the accounting statements and other associated factors.

It has been found out that the management of the company has prepared the accounting

statements of the companies in regards to the issued standards of the regulatory bodies like the

Australian Accounting Standards Board.

3

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Introduction

The issue that has been presented in the question is that the annual report of a listed

organization has been analyzed in order to examine the objectivity the regulatory standards that

have been applied for the objective behind the preparation of the accounting statements. It must

be noted here that the Australian Accounting Standards Board has essentially established the

particular accounting standards that are applied for the preparation of the accounting statements

of an organization in Australia.

This particular study focuses upon the Australian corporate entity, REA Group Limited.

The annual report of this particular entity for the accounting year of 2017 has been evaluated in

order to find out the fact that whether accounting statements satisfy the required objectives of

accounting report, whether the company has satisfied the criteria of recognition for the elements

of the accounting statements and other associated factors.

Objectives of the accounting report

The objectives of the accounting report have been as follows:

The objective of the general purpose accounting report is primarily regulated around the

providence of accounting information in regards to the accounting entity that can be

useful to the third party investors, lenders and creditors for making the investment

decisions.

Decisions in regards to the potential and existing potential investors for dealing in the

debt instruments are also facilitated by analyzing the accounting statements.

It must be noted here that the general purpose accounting reports cannot provide all the

accounting information that is required by the investors in order to make the required

accounting decisions (Ali, Akbar & Ormrod, 2016)

The accounting statements of REA Group Limited reflect the fact that the accounting

reports have been prepared in accordance to the financial accounting standards as prescribed by

AASB. This means that the accounting statements satisfy the requirements of the accounting

report sufficiently. This can be further evidenced from the fact that the Australian Accounting

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Introduction

The issue that has been presented in the question is that the annual report of a listed

organization has been analyzed in order to examine the objectivity the regulatory standards that

have been applied for the objective behind the preparation of the accounting statements. It must

be noted here that the Australian Accounting Standards Board has essentially established the

particular accounting standards that are applied for the preparation of the accounting statements

of an organization in Australia.

This particular study focuses upon the Australian corporate entity, REA Group Limited.

The annual report of this particular entity for the accounting year of 2017 has been evaluated in

order to find out the fact that whether accounting statements satisfy the required objectives of

accounting report, whether the company has satisfied the criteria of recognition for the elements

of the accounting statements and other associated factors.

Objectives of the accounting report

The objectives of the accounting report have been as follows:

The objective of the general purpose accounting report is primarily regulated around the

providence of accounting information in regards to the accounting entity that can be

useful to the third party investors, lenders and creditors for making the investment

decisions.

Decisions in regards to the potential and existing potential investors for dealing in the

debt instruments are also facilitated by analyzing the accounting statements.

It must be noted here that the general purpose accounting reports cannot provide all the

accounting information that is required by the investors in order to make the required

accounting decisions (Ali, Akbar & Ormrod, 2016)

The accounting statements of REA Group Limited reflect the fact that the accounting

reports have been prepared in accordance to the financial accounting standards as prescribed by

AASB. This means that the accounting statements satisfy the requirements of the accounting

report sufficiently. This can be further evidenced from the fact that the Australian Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Standards Board (AASB 101) reports that the basis for the preparation of the accounting

statements have been that the degree of comparability of the accounting statements of the

corporate entity for the previous periods and the accounting statements of other entities is high

(Ali, Akbar & Ormrod, 2016). It must be mentioned here that a sufficiently qualified accounting

statements will consist of the elements like:

Assets

Liabilities

Equity statement

Income and expenses

Cash flows

Moreover, it must be mentioned here that a complete set of accounting statements

essentially consist of the essential elements as follows:

accounting position statement that has been prepared at the end of the period

Comprehensive income statement in regards to the stipulated period

Equity statement for the stipulated period

Statement of cash flow for the stipulated period

Accounting disclosures

The accounting report of the company has adhered to all these standards. This means that

the financial report of the business entity has included all the above mentioned accounting

statements. These statements are the consolidated income statement, consolidated statement of

comprehensive income, consolidated of accounting position, consolidated statement of changes

in equity and consolidated statement of cash flows. The company has also provided the required

accounting disclosures. Furthermore, the general features of the annual reports of REA Group

Limited have been in accordance to the accounting report standards (Ali, Akbar & Ormrod,

2016). This can be evidenced from the fact that are as follows:

The accounting statements have been prepared on the basis of the International

Accounting report Standards

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Standards Board (AASB 101) reports that the basis for the preparation of the accounting

statements have been that the degree of comparability of the accounting statements of the

corporate entity for the previous periods and the accounting statements of other entities is high

(Ali, Akbar & Ormrod, 2016). It must be mentioned here that a sufficiently qualified accounting

statements will consist of the elements like:

Assets

Liabilities

Equity statement

Income and expenses

Cash flows

Moreover, it must be mentioned here that a complete set of accounting statements

essentially consist of the essential elements as follows:

accounting position statement that has been prepared at the end of the period

Comprehensive income statement in regards to the stipulated period

Equity statement for the stipulated period

Statement of cash flow for the stipulated period

Accounting disclosures

The accounting report of the company has adhered to all these standards. This means that

the financial report of the business entity has included all the above mentioned accounting

statements. These statements are the consolidated income statement, consolidated statement of

comprehensive income, consolidated of accounting position, consolidated statement of changes

in equity and consolidated statement of cash flows. The company has also provided the required

accounting disclosures. Furthermore, the general features of the annual reports of REA Group

Limited have been in accordance to the accounting report standards (Ali, Akbar & Ormrod,

2016). This can be evidenced from the fact that are as follows:

The accounting statements have been prepared on the basis of the International

Accounting report Standards

5

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

The management of the firm has properly asserted the fact that the corporate entity is a

going concern and has resulted in the execution of the preparation of the accounting

statements accordingly

Furthermore, the management of the firm has prepared the accounting statements in such

a way that the similar classes of items have been reported separately if material

The accounting disclosures that have been provided by the companies have been reported

separately and the accounting information revealed by the particular disclosures have

been clear and meaningful

It must be noted here that the accounting statements of the company has been prepared on

the basis of accrual accounting

The administration of the firm has been such that it has facilitated in the providence of

the required information in regards to the offset of the assets and the liabilities of the firm

Each of the statements that have been included in the financial report of the company has

facilitated the providence of the required information that has been featured by a high

degree of comparability

Therefore, it can be deduced that the company has met the objectives of the general

purpose accounting report (Balsmeier & Vanhaverbeke, 2018).

Have the target audience adequately used the report?

The target audience that are the shareholders, stakeholders, creditors, debtors and the

other third party investors of the firm have been able to utilize the accounting report for the

purpose of taking the accounting decisions effectively. This can be evidenced from the fact that

the accounting report prepared by the management of REA Group Limited has been providing

enough information into the accounting condition of the company. The accounting disclosures

provide enough overview in to the past performance of the company. The investors of the

company and the other potential stakeholders get enough overview into the operations of the

company on the basis of the information that has been provided in the accounting statements of

the companies. Moreover, it has been provided in the accounting report of the company that the

shareholders have received enough remuneration thus ensuring welfare of the shareholders of the

firm (Balsmeier & Vanhaverbeke, 2018).

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

The management of the firm has properly asserted the fact that the corporate entity is a

going concern and has resulted in the execution of the preparation of the accounting

statements accordingly

Furthermore, the management of the firm has prepared the accounting statements in such

a way that the similar classes of items have been reported separately if material

The accounting disclosures that have been provided by the companies have been reported

separately and the accounting information revealed by the particular disclosures have

been clear and meaningful

It must be noted here that the accounting statements of the company has been prepared on

the basis of accrual accounting

The administration of the firm has been such that it has facilitated in the providence of

the required information in regards to the offset of the assets and the liabilities of the firm

Each of the statements that have been included in the financial report of the company has

facilitated the providence of the required information that has been featured by a high

degree of comparability

Therefore, it can be deduced that the company has met the objectives of the general

purpose accounting report (Balsmeier & Vanhaverbeke, 2018).

Have the target audience adequately used the report?

The target audience that are the shareholders, stakeholders, creditors, debtors and the

other third party investors of the firm have been able to utilize the accounting report for the

purpose of taking the accounting decisions effectively. This can be evidenced from the fact that

the accounting report prepared by the management of REA Group Limited has been providing

enough information into the accounting condition of the company. The accounting disclosures

provide enough overview in to the past performance of the company. The investors of the

company and the other potential stakeholders get enough overview into the operations of the

company on the basis of the information that has been provided in the accounting statements of

the companies. Moreover, it has been provided in the accounting report of the company that the

shareholders have received enough remuneration thus ensuring welfare of the shareholders of the

firm (Balsmeier & Vanhaverbeke, 2018).

6

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

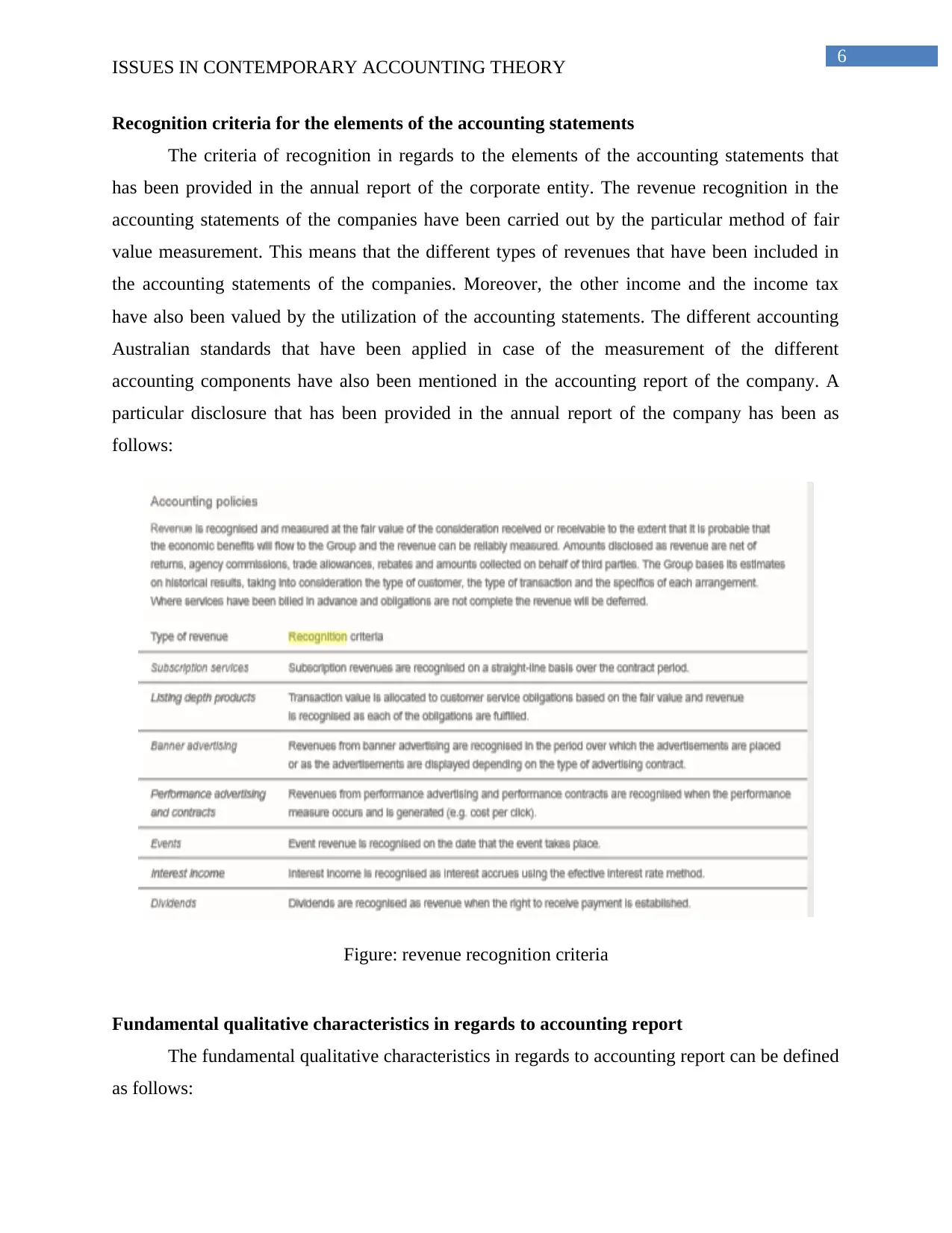

Recognition criteria for the elements of the accounting statements

The criteria of recognition in regards to the elements of the accounting statements that

has been provided in the annual report of the corporate entity. The revenue recognition in the

accounting statements of the companies have been carried out by the particular method of fair

value measurement. This means that the different types of revenues that have been included in

the accounting statements of the companies. Moreover, the other income and the income tax

have also been valued by the utilization of the accounting statements. The different accounting

Australian standards that have been applied in case of the measurement of the different

accounting components have also been mentioned in the accounting report of the company. A

particular disclosure that has been provided in the annual report of the company has been as

follows:

Figure: revenue recognition criteria

Fundamental qualitative characteristics in regards to accounting report

The fundamental qualitative characteristics in regards to accounting report can be defined

as follows:

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Recognition criteria for the elements of the accounting statements

The criteria of recognition in regards to the elements of the accounting statements that

has been provided in the annual report of the corporate entity. The revenue recognition in the

accounting statements of the companies have been carried out by the particular method of fair

value measurement. This means that the different types of revenues that have been included in

the accounting statements of the companies. Moreover, the other income and the income tax

have also been valued by the utilization of the accounting statements. The different accounting

Australian standards that have been applied in case of the measurement of the different

accounting components have also been mentioned in the accounting report of the company. A

particular disclosure that has been provided in the annual report of the company has been as

follows:

Figure: revenue recognition criteria

Fundamental qualitative characteristics in regards to accounting report

The fundamental qualitative characteristics in regards to accounting report can be defined

as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Relevance – the relevance of the accounting statements have sufficiently satisfied the

fundamental quality standards of the company

Faithful representation – it can be certainly deduced that the conveyed accounting

information reflect a true and fair image of the accounting position of the company.

It can be evidently stated that the accounting statements of the REA Group has been

prepared on the basis of the fundamental qualitative features of accounting report. This means

that the accounting report provides enough information in regards to the different accounting

components. This can be further evidenced by the auditor’s report that has stated the fact that the

accounting statements of REA Group has adhered to the qualitative features satisfactorily.

Moreover, the information that has been conveyed by the accounting statements reflect the fact

that the accounting statement represent a true and fair image of the corporate entity.

Enhancing qualitative characteristic of the firm

The enhancing characteristic of accounting report can be defined as follows:

Comparability – the degree of the comparability of the accounting statement of the

company have been high.

Clarity – the clarity of the information that has been obtained from the accounting

statements of the companies has been of a high degree

Conciseness – the provided information in the accounting report of the company has been

concise which has facilitated the economic decision making by the stakeholders and the

shareholders of the firm

Verifiability – the verifiability of the information that has been disclosed in the

accounting report of the company has been of a high degree. This has increased the trust

between the management and the stakeholders of the firm (Balsmeier & Vanhaverbeke,

2018).

The degree of comparability of the accounting statements have been high. This is

because the accounting statements of REA Group have been prepared on the basis of the

Australian Accounting Standards Board. The clarity of the information conveyed by the

accounting report has also been high resulting in the reflection of the accounting

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Relevance – the relevance of the accounting statements have sufficiently satisfied the

fundamental quality standards of the company

Faithful representation – it can be certainly deduced that the conveyed accounting

information reflect a true and fair image of the accounting position of the company.

It can be evidently stated that the accounting statements of the REA Group has been

prepared on the basis of the fundamental qualitative features of accounting report. This means

that the accounting report provides enough information in regards to the different accounting

components. This can be further evidenced by the auditor’s report that has stated the fact that the

accounting statements of REA Group has adhered to the qualitative features satisfactorily.

Moreover, the information that has been conveyed by the accounting statements reflect the fact

that the accounting statement represent a true and fair image of the corporate entity.

Enhancing qualitative characteristic of the firm

The enhancing characteristic of accounting report can be defined as follows:

Comparability – the degree of the comparability of the accounting statement of the

company have been high.

Clarity – the clarity of the information that has been obtained from the accounting

statements of the companies has been of a high degree

Conciseness – the provided information in the accounting report of the company has been

concise which has facilitated the economic decision making by the stakeholders and the

shareholders of the firm

Verifiability – the verifiability of the information that has been disclosed in the

accounting report of the company has been of a high degree. This has increased the trust

between the management and the stakeholders of the firm (Balsmeier & Vanhaverbeke,

2018).

The degree of comparability of the accounting statements have been high. This is

because the accounting statements of REA Group have been prepared on the basis of the

Australian Accounting Standards Board. The clarity of the information conveyed by the

accounting report has also been high resulting in the reflection of the accounting

8

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

statements of the particular corporate entity with an optimum degree of verifiability. This

fact has also been confirmed by the auditor of the company.

Conclusion

The particular conclusion that can be arrived at is that the accounting statements of REA

Group Limited for the accounting year of 2017 have been prepared in accordance to the

regulatory standards as conveyed by the Australian Accounting Standards Board. Therefore, no

such recommendation is required for the management of the corporate entity. However, a

particular fact that should be noted is that the adoption of the new accounting policies should be

properly revealed in the financial report in a proper way.

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

statements of the particular corporate entity with an optimum degree of verifiability. This

fact has also been confirmed by the auditor of the company.

Conclusion

The particular conclusion that can be arrived at is that the accounting statements of REA

Group Limited for the accounting year of 2017 have been prepared in accordance to the

regulatory standards as conveyed by the Australian Accounting Standards Board. Therefore, no

such recommendation is required for the management of the corporate entity. However, a

particular fact that should be noted is that the adoption of the new accounting policies should be

properly revealed in the financial report in a proper way.

9

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

References and Bibliography

Ali, A., Akbar, S., & Ormrod, P. (2016, March). Impact of international accounting report

standards on the profit and equity of AIM listed companies in the UK. In Accounting

Forum (Vol. 40, No. 1, pp. 45-62). Elsevier.

Balsmeier, B., & Vanhaverbeke, S. (2018). International accounting report standards and private

firms’ access to bank loans. European Accounting Review, 27(1), 75-104.

Dye, R., Glover, J., & Sunder, S. (2014). How Can Accounting report Standards Resist

Accounting-Motivated Accounting Engineering?.

Graham, A., Nandialath, A. M., Skaradzinski, D., & Rustambekov, E. (2017). Macroeconomic

Determinants of International Accounting report Standards (IFRS) Adoption: Evidence

from the Middle East North Africa (MENA) Region.

Jibril, M. A., & Abubakar, M. (2016, October). Effect Of International Accounting report

Standards (Ifrs) On Corporate Financing In Nigerian Banking Industry. In Proceedings of

Economics and Finance Conferences (No. 4206880). International Institute of Social and

Economic Sciences.

Kim, J. B., Shi, H., & Zhou, J. (2014). International Accounting report Standards, institutional

infrastructures, and implied cost of equity capital around the world. Review of

Quantitative Finance and Accounting, 42(3), 469-507.

Lestari, D. (2015). The Effect OF Implementation OF Convergence International Accounting

report Standards (ifrs), Good Corporate Governance, And Disclosure OF Corporate

Social Responsibility (csr) ON Investor Reactions (in Manufacturing Companies Listed

ON Indonesia Stock Exchange Period 2011-2013).

Perkins, J. D. (2016). Discussion of “Security Returns and Volume Responses around

International Accounting report Standards (IFRS) Earnings Announcements”. The

International Journal of Accounting, 51(2), 266-270.

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

References and Bibliography

Ali, A., Akbar, S., & Ormrod, P. (2016, March). Impact of international accounting report

standards on the profit and equity of AIM listed companies in the UK. In Accounting

Forum (Vol. 40, No. 1, pp. 45-62). Elsevier.

Balsmeier, B., & Vanhaverbeke, S. (2018). International accounting report standards and private

firms’ access to bank loans. European Accounting Review, 27(1), 75-104.

Dye, R., Glover, J., & Sunder, S. (2014). How Can Accounting report Standards Resist

Accounting-Motivated Accounting Engineering?.

Graham, A., Nandialath, A. M., Skaradzinski, D., & Rustambekov, E. (2017). Macroeconomic

Determinants of International Accounting report Standards (IFRS) Adoption: Evidence

from the Middle East North Africa (MENA) Region.

Jibril, M. A., & Abubakar, M. (2016, October). Effect Of International Accounting report

Standards (Ifrs) On Corporate Financing In Nigerian Banking Industry. In Proceedings of

Economics and Finance Conferences (No. 4206880). International Institute of Social and

Economic Sciences.

Kim, J. B., Shi, H., & Zhou, J. (2014). International Accounting report Standards, institutional

infrastructures, and implied cost of equity capital around the world. Review of

Quantitative Finance and Accounting, 42(3), 469-507.

Lestari, D. (2015). The Effect OF Implementation OF Convergence International Accounting

report Standards (ifrs), Good Corporate Governance, And Disclosure OF Corporate

Social Responsibility (csr) ON Investor Reactions (in Manufacturing Companies Listed

ON Indonesia Stock Exchange Period 2011-2013).

Perkins, J. D. (2016). Discussion of “Security Returns and Volume Responses around

International Accounting report Standards (IFRS) Earnings Announcements”. The

International Journal of Accounting, 51(2), 266-270.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Sunder, S. (2016). Rethinking accounting report: standards, norms and institutions. Foundations

and Trends® in Accounting, 11(1–2), 1-118.

Tsunogaya, N. (2016). Issues affecting decisions on mandatory adoption of International

Accounting report Standards (IFRS) in Japan. Accounting, Auditing & Accountability

Journal, 29(5), 828-860.

ISSUES IN CONTEMPORARY ACCOUNTING THEORY

Sunder, S. (2016). Rethinking accounting report: standards, norms and institutions. Foundations

and Trends® in Accounting, 11(1–2), 1-118.

Tsunogaya, N. (2016). Issues affecting decisions on mandatory adoption of International

Accounting report Standards (IFRS) in Japan. Accounting, Auditing & Accountability

Journal, 29(5), 828-860.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.