Management Accounting: Techniques and Planning Tools Report

VerifiedAdded on 2021/06/30

|15

|4292

|39

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on the application of various techniques and tools within an organizational context. It begins by demonstrating an understanding of management accounting systems and explaining the essential requirements of different types of these systems. The report then delves into the methods used for management accounting reporting, including budget reports, account receivable aging reports, cost reports, and performance reports. A significant portion of the report is dedicated to applying a range of management accounting techniques, such as calculating costs using marginal and absorption costing methods, preparing income statements, and conducting reconciliation statements. Additionally, the report examines the use of planning tools like traditional, activity-based, zero-based, and rolling budgets, analyzing their advantages and disadvantages. The analysis extends to how organizations can use management accounting to respond to financial problems and achieve sustainable success through financial governance, key performance indicators, and benchmark systems. The report concludes by summarizing the key findings and insights gained from the analysis, emphasizing the importance of management accounting in financial decision-making and organizational growth. This report is a valuable resource for students seeking to understand and apply management accounting principles.

(J-A 2021) RQFBM-MA0602053 03.2021

Submission Front Sheet

Programme BTEC Higher National Diploma (HND) in Business (RQF)

Unit Title and Number: Management Accounting (Unit 5)

Assignment title Management Accounting Assignment Brief

Unit RQF level/Code Level 4

H/508/0489

Module Tutor Name

/Email

Dr Ayodele Aluko

a.aluko@mrcollege.ac.u

k

Credit Value 15

Assignment Brief Code (J-A 2021) RQFBM-

MA0602053

Cohort Name Sept 20B Assignment Date Set 5th Jan 2021

Student’s Name

Bianca

AndreeaPresicare

anu

Student’sRegistration

Number

25467

Submission Date

04.03.2021

Distribution Date 18/01/21

Is this a first

submission

Is this a referral

submission

Word Count

3338

Learner’s statement of authenticity

I certify that the work submitted for this assignment is my own. Where the work of others has

been used to support my work then credit has been acknowledged.I have identified and

acknowledged all sources used in this assignment and have referenced according to the

Harvard referencing system. I have read and understood the Plagiarism and Collusion section

provided with the assignment brief and understood the consequences of plagiarising.

Student’s Signature

Presicareanu Date 04.03.2021

1

Presicareanu 25467

Submission Front Sheet

Programme BTEC Higher National Diploma (HND) in Business (RQF)

Unit Title and Number: Management Accounting (Unit 5)

Assignment title Management Accounting Assignment Brief

Unit RQF level/Code Level 4

H/508/0489

Module Tutor Name

Dr Ayodele Aluko

a.aluko@mrcollege.ac.u

k

Credit Value 15

Assignment Brief Code (J-A 2021) RQFBM-

MA0602053

Cohort Name Sept 20B Assignment Date Set 5th Jan 2021

Student’s Name

Bianca

AndreeaPresicare

anu

Student’sRegistration

Number

25467

Submission Date

04.03.2021

Distribution Date 18/01/21

Is this a first

submission

Is this a referral

submission

Word Count

3338

Learner’s statement of authenticity

I certify that the work submitted for this assignment is my own. Where the work of others has

been used to support my work then credit has been acknowledged.I have identified and

acknowledged all sources used in this assignment and have referenced according to the

Harvard referencing system. I have read and understood the Plagiarism and Collusion section

provided with the assignment brief and understood the consequences of plagiarising.

Student’s Signature

Presicareanu Date 04.03.2021

1

Presicareanu 25467

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(J-A 2021) RQFBM-MA0602053 03.2021

Table of Contents

Introduction..............................................................................................................................4

Demonstrate an understanding of management accounting systems.................................4

Explain management accounting and give the essential requirements of different types of

management accounting systems...........................................................................................4

Explain different methods used for management accounting reporting...............................5

Evaluate the benefits of management accounting systems and their application within an

organisational context............................................................................................................5

Apply a range of management accounting techniques........................................................6

Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................6

Marginal costing technique................................................................................................6

Absorption costing technique.............................................................................................6

Reconciliation statement....................................................................................................7

Interpretation of the income statements.............................................................................8

Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents................................................................................................8

Marginal costing method....................................................................................................8

Absorption costing method................................................................................................8

Explain the use of planning tools used in management accounting....................................9

Explain the advantages and disadvantages of different types of planning tools used for

budgetary control...................................................................................................................9

Traditional budget..............................................................................................................9

Activity based budget.........................................................................................................9

Zero based budget............................................................................................................10

Rolling budget..................................................................................................................10

2

Presicareanu 25467

Table of Contents

Introduction..............................................................................................................................4

Demonstrate an understanding of management accounting systems.................................4

Explain management accounting and give the essential requirements of different types of

management accounting systems...........................................................................................4

Explain different methods used for management accounting reporting...............................5

Evaluate the benefits of management accounting systems and their application within an

organisational context............................................................................................................5

Apply a range of management accounting techniques........................................................6

Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................6

Marginal costing technique................................................................................................6

Absorption costing technique.............................................................................................6

Reconciliation statement....................................................................................................7

Interpretation of the income statements.............................................................................8

Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents................................................................................................8

Marginal costing method....................................................................................................8

Absorption costing method................................................................................................8

Explain the use of planning tools used in management accounting....................................9

Explain the advantages and disadvantages of different types of planning tools used for

budgetary control...................................................................................................................9

Traditional budget..............................................................................................................9

Activity based budget.........................................................................................................9

Zero based budget............................................................................................................10

Rolling budget..................................................................................................................10

2

Presicareanu 25467

(J-A 2021) RQFBM-MA0602053 03.2021

Analyse the use of different planning tools and their application for preparing and

forecasting budgets...............................................................................................................10

Compare ways in which organisations could use management accounting to respond to

financial problems..................................................................................................................10

Compare how organisations are adapting management accounting systems to respond to

financial problems................................................................................................................10

Cost accounting................................................................................................................11

Pricing strategy.................................................................................................................11

Budgetary control.............................................................................................................11

Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success.....................................................................................11

Financial governance.......................................................................................................12

Key performance indicator...............................................................................................12

Benchmark system...........................................................................................................12

Conclusion................................................................................................................................13

Reference..................................................................................................................................14

3

Presicareanu 25467

Analyse the use of different planning tools and their application for preparing and

forecasting budgets...............................................................................................................10

Compare ways in which organisations could use management accounting to respond to

financial problems..................................................................................................................10

Compare how organisations are adapting management accounting systems to respond to

financial problems................................................................................................................10

Cost accounting................................................................................................................11

Pricing strategy.................................................................................................................11

Budgetary control.............................................................................................................11

Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success.....................................................................................11

Financial governance.......................................................................................................12

Key performance indicator...............................................................................................12

Benchmark system...........................................................................................................12

Conclusion................................................................................................................................13

Reference..................................................................................................................................14

3

Presicareanu 25467

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(J-A 2021) RQFBM-MA0602053 03.2021

Introduction

In the business organisation, making play a significant role as to contribute in the growth and

development planning of the business. For the business organisation the use of different tools

and techniques for preparation of the different strategies to execute in the market is a

significant part as the wrong choice of tools and technique can create significant impact on

the decision making of the business. As a result, the growth and development of the business

organisation will also be hampered. For the financial decision making, the financial manager

and the management of the business organisation uses financial management. This is why,

along with the financial management the use of management accounting is important for the

business organisation to maintain the confidentiality of the preparation of strategies and

planning as well as to improve the efficiency level of the decision making system of the

business. In this report, the discussion regarding the management accounting has been

conducted to evaluate the integration of the management accounting system with

organisational processes. Also how the business organisation response to solve differing

financial problems of the business by the tools and techniques of management accounting and

achieve the sustainable success has been mentioned in the report.

Demonstrate an understanding of management accounting systems

Management accounting system (MAS) is engaged with the process of collection, analysis

and interpretation of both financial and non-financial data which are instrumental for the

managers to undertake important strategic decisions. A manufacturing company uses MAS to

evaluate the profitable cost of production as well as to fix the prices of its products and

services by analysing the performance of the company in the past along with the performance

of its competitors in the market. MAS prepares reports in accordance with the needs of the

management

4

Presicareanu 25467

Introduction

In the business organisation, making play a significant role as to contribute in the growth and

development planning of the business. For the business organisation the use of different tools

and techniques for preparation of the different strategies to execute in the market is a

significant part as the wrong choice of tools and technique can create significant impact on

the decision making of the business. As a result, the growth and development of the business

organisation will also be hampered. For the financial decision making, the financial manager

and the management of the business organisation uses financial management. This is why,

along with the financial management the use of management accounting is important for the

business organisation to maintain the confidentiality of the preparation of strategies and

planning as well as to improve the efficiency level of the decision making system of the

business. In this report, the discussion regarding the management accounting has been

conducted to evaluate the integration of the management accounting system with

organisational processes. Also how the business organisation response to solve differing

financial problems of the business by the tools and techniques of management accounting and

achieve the sustainable success has been mentioned in the report.

Demonstrate an understanding of management accounting systems

Management accounting system (MAS) is engaged with the process of collection, analysis

and interpretation of both financial and non-financial data which are instrumental for the

managers to undertake important strategic decisions. A manufacturing company uses MAS to

evaluate the profitable cost of production as well as to fix the prices of its products and

services by analysing the performance of the company in the past along with the performance

of its competitors in the market. MAS prepares reports in accordance with the needs of the

management

4

Presicareanu 25467

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(J-A 2021) RQFBM-MA0602053 03.2021

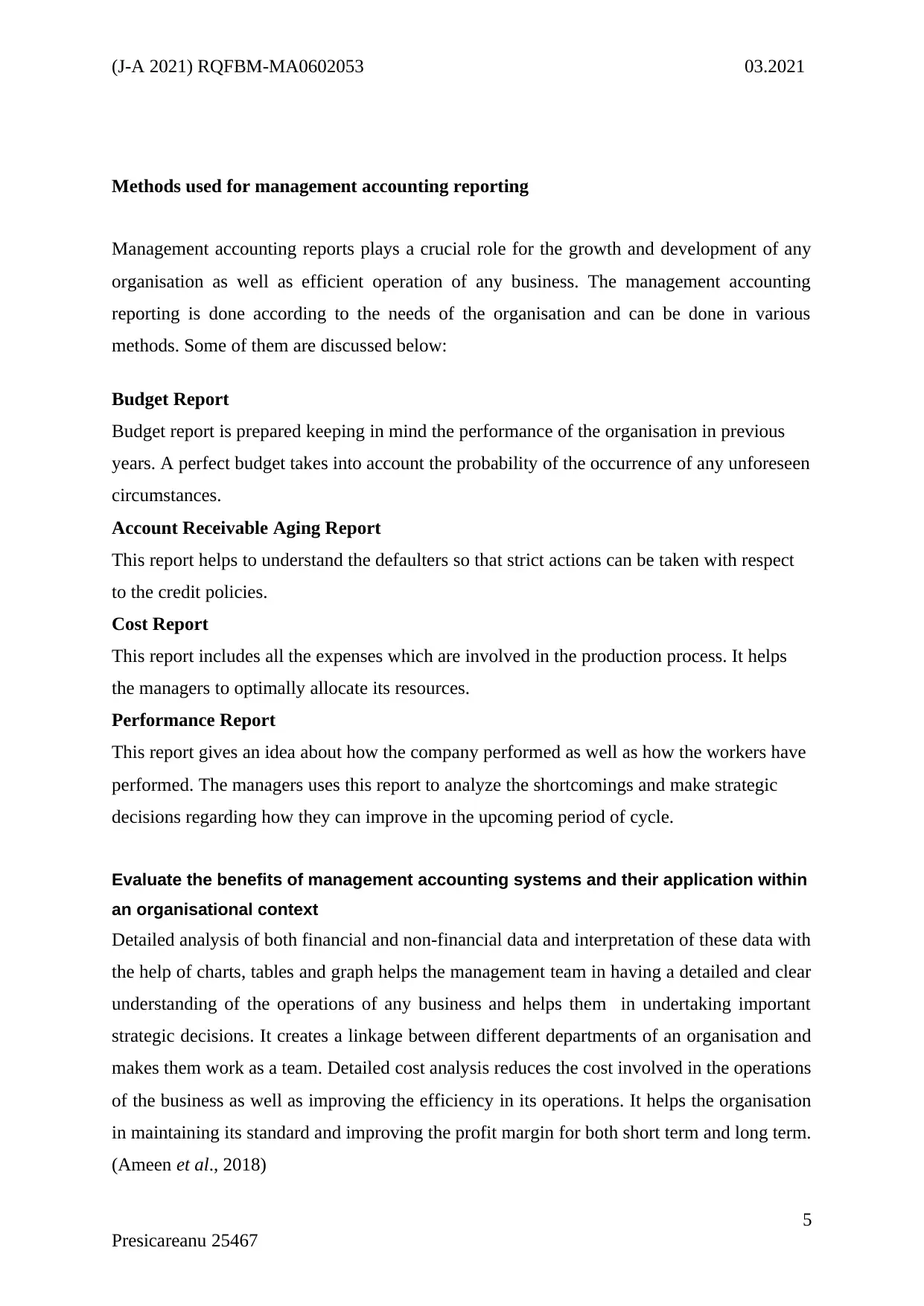

Methods used for management accounting reporting

Management accounting reports plays a crucial role for the growth and development of any

organisation as well as efficient operation of any business. The management accounting

reporting is done according to the needs of the organisation and can be done in various

methods. Some of them are discussed below:

Budget Report

Budget report is prepared keeping in mind the performance of the organisation in previous

years. A perfect budget takes into account the probability of the occurrence of any unforeseen

circumstances.

Account Receivable Aging Report

This report helps to understand the defaulters so that strict actions can be taken with respect

to the credit policies.

Cost Report

This report includes all the expenses which are involved in the production process. It helps

the managers to optimally allocate its resources.

Performance Report

This report gives an idea about how the company performed as well as how the workers have

performed. The managers uses this report to analyze the shortcomings and make strategic

decisions regarding how they can improve in the upcoming period of cycle.

Evaluate the benefits of management accounting systems and their application within

an organisational context

Detailed analysis of both financial and non-financial data and interpretation of these data with

the help of charts, tables and graph helps the management team in having a detailed and clear

understanding of the operations of any business and helps them in undertaking important

strategic decisions. It creates a linkage between different departments of an organisation and

makes them work as a team. Detailed cost analysis reduces the cost involved in the operations

of the business as well as improving the efficiency in its operations. It helps the organisation

in maintaining its standard and improving the profit margin for both short term and long term.

(Ameen et al., 2018)

5

Presicareanu 25467

Methods used for management accounting reporting

Management accounting reports plays a crucial role for the growth and development of any

organisation as well as efficient operation of any business. The management accounting

reporting is done according to the needs of the organisation and can be done in various

methods. Some of them are discussed below:

Budget Report

Budget report is prepared keeping in mind the performance of the organisation in previous

years. A perfect budget takes into account the probability of the occurrence of any unforeseen

circumstances.

Account Receivable Aging Report

This report helps to understand the defaulters so that strict actions can be taken with respect

to the credit policies.

Cost Report

This report includes all the expenses which are involved in the production process. It helps

the managers to optimally allocate its resources.

Performance Report

This report gives an idea about how the company performed as well as how the workers have

performed. The managers uses this report to analyze the shortcomings and make strategic

decisions regarding how they can improve in the upcoming period of cycle.

Evaluate the benefits of management accounting systems and their application within

an organisational context

Detailed analysis of both financial and non-financial data and interpretation of these data with

the help of charts, tables and graph helps the management team in having a detailed and clear

understanding of the operations of any business and helps them in undertaking important

strategic decisions. It creates a linkage between different departments of an organisation and

makes them work as a team. Detailed cost analysis reduces the cost involved in the operations

of the business as well as improving the efficiency in its operations. It helps the organisation

in maintaining its standard and improving the profit margin for both short term and long term.

(Ameen et al., 2018)

5

Presicareanu 25467

(J-A 2021) RQFBM-MA0602053 03.2021

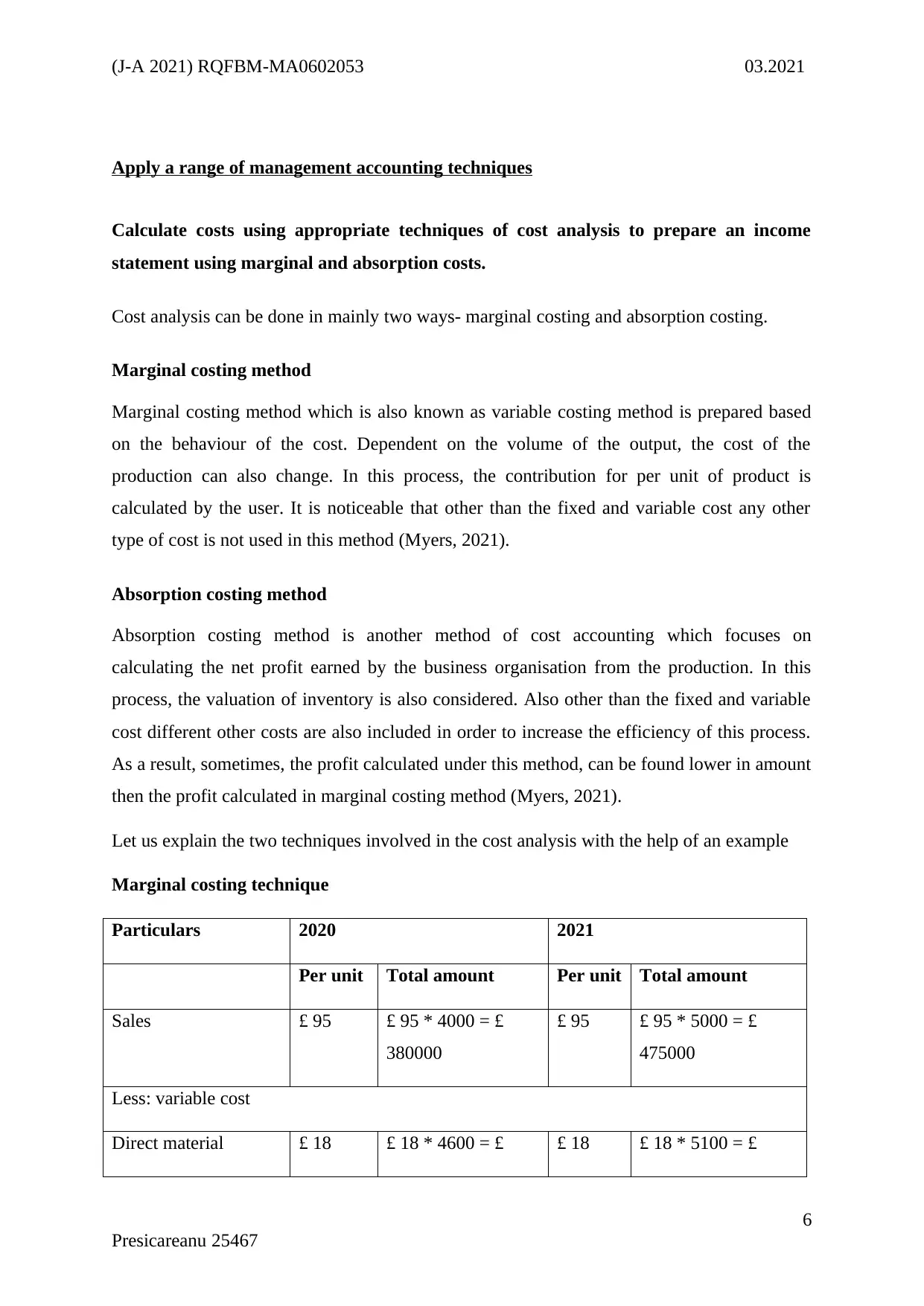

Apply a range of management accounting techniques

Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Cost analysis can be done in mainly two ways- marginal costing and absorption costing.

Marginal costing method

Marginal costing method which is also known as variable costing method is prepared based

on the behaviour of the cost. Dependent on the volume of the output, the cost of the

production can also change. In this process, the contribution for per unit of product is

calculated by the user. It is noticeable that other than the fixed and variable cost any other

type of cost is not used in this method (Myers, 2021).

Absorption costing method

Absorption costing method is another method of cost accounting which focuses on

calculating the net profit earned by the business organisation from the production. In this

process, the valuation of inventory is also considered. Also other than the fixed and variable

cost different other costs are also included in order to increase the efficiency of this process.

As a result, sometimes, the profit calculated under this method, can be found lower in amount

then the profit calculated in marginal costing method (Myers, 2021).

Let us explain the two techniques involved in the cost analysis with the help of an example

Marginal costing technique

Particulars 2020 2021

Per unit Total amount Per unit Total amount

Sales £ 95 £ 95 * 4000 = £

380000

£ 95 £ 95 * 5000 = £

475000

Less: variable cost

Direct material £ 18 £ 18 * 4600 = £ £ 18 £ 18 * 5100 = £

6

Presicareanu 25467

Apply a range of management accounting techniques

Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Cost analysis can be done in mainly two ways- marginal costing and absorption costing.

Marginal costing method

Marginal costing method which is also known as variable costing method is prepared based

on the behaviour of the cost. Dependent on the volume of the output, the cost of the

production can also change. In this process, the contribution for per unit of product is

calculated by the user. It is noticeable that other than the fixed and variable cost any other

type of cost is not used in this method (Myers, 2021).

Absorption costing method

Absorption costing method is another method of cost accounting which focuses on

calculating the net profit earned by the business organisation from the production. In this

process, the valuation of inventory is also considered. Also other than the fixed and variable

cost different other costs are also included in order to increase the efficiency of this process.

As a result, sometimes, the profit calculated under this method, can be found lower in amount

then the profit calculated in marginal costing method (Myers, 2021).

Let us explain the two techniques involved in the cost analysis with the help of an example

Marginal costing technique

Particulars 2020 2021

Per unit Total amount Per unit Total amount

Sales £ 95 £ 95 * 4000 = £

380000

£ 95 £ 95 * 5000 = £

475000

Less: variable cost

Direct material £ 18 £ 18 * 4600 = £ £ 18 £ 18 * 5100 = £

6

Presicareanu 25467

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(J-A 2021) RQFBM-MA0602053 03.2021

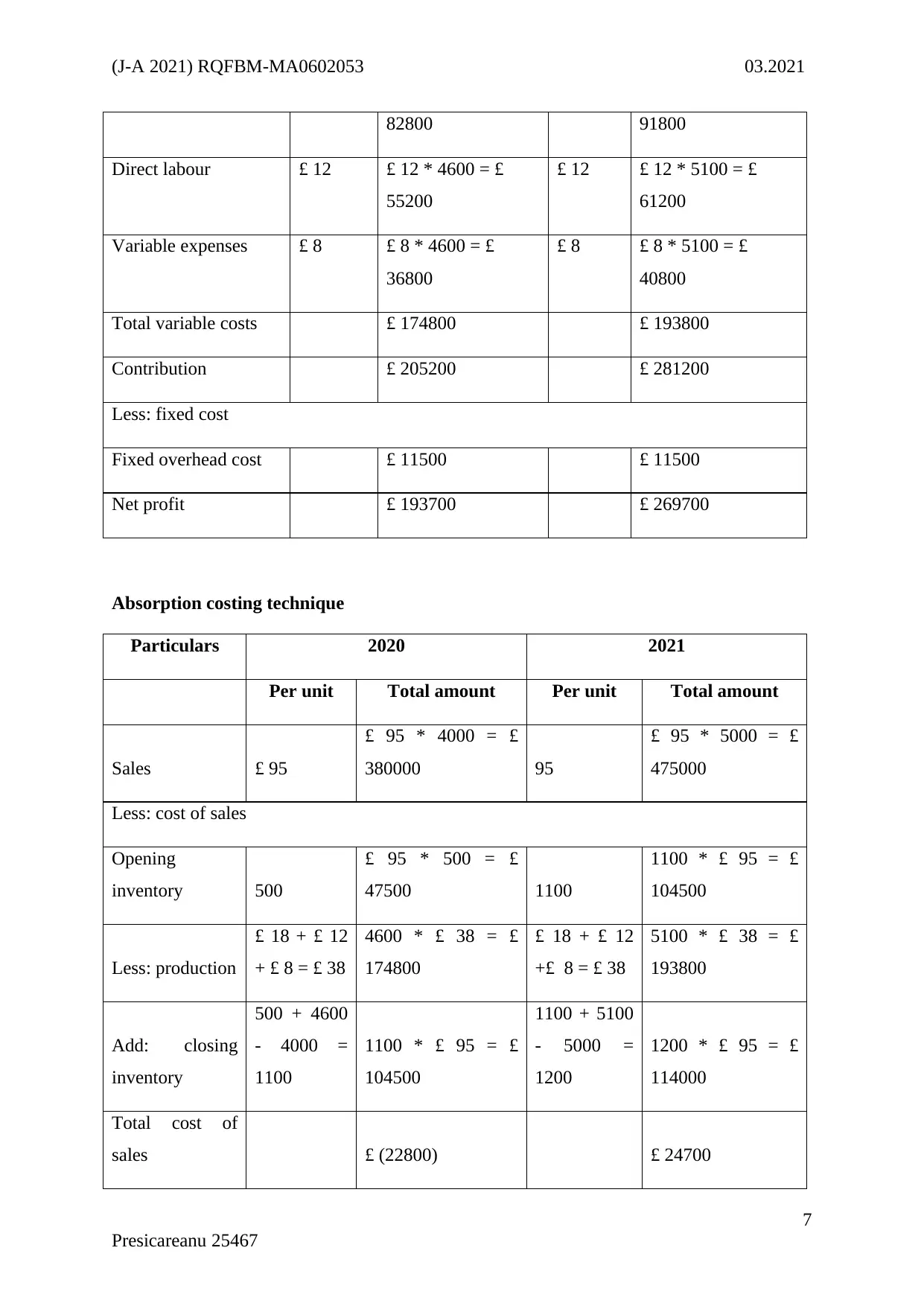

82800 91800

Direct labour £ 12 £ 12 * 4600 = £

55200

£ 12 £ 12 * 5100 = £

61200

Variable expenses £ 8 £ 8 * 4600 = £

36800

£ 8 £ 8 * 5100 = £

40800

Total variable costs £ 174800 £ 193800

Contribution £ 205200 £ 281200

Less: fixed cost

Fixed overhead cost £ 11500 £ 11500

Net profit £ 193700 £ 269700

Absorption costing technique

Particulars 2020 2021

Per unit Total amount Per unit Total amount

Sales £ 95

£ 95 * 4000 = £

380000 95

£ 95 * 5000 = £

475000

Less: cost of sales

Opening

inventory 500

£ 95 * 500 = £

47500 1100

1100 * £ 95 = £

104500

Less: production

£ 18 + £ 12

+ £ 8 = £ 38

4600 * £ 38 = £

174800

£ 18 + £ 12

+£ 8 = £ 38

5100 * £ 38 = £

193800

Add: closing

inventory

500 + 4600

- 4000 =

1100

1100 * £ 95 = £

104500

1100 + 5100

- 5000 =

1200

1200 * £ 95 = £

114000

Total cost of

sales £ (22800) £ 24700

7

Presicareanu 25467

82800 91800

Direct labour £ 12 £ 12 * 4600 = £

55200

£ 12 £ 12 * 5100 = £

61200

Variable expenses £ 8 £ 8 * 4600 = £

36800

£ 8 £ 8 * 5100 = £

40800

Total variable costs £ 174800 £ 193800

Contribution £ 205200 £ 281200

Less: fixed cost

Fixed overhead cost £ 11500 £ 11500

Net profit £ 193700 £ 269700

Absorption costing technique

Particulars 2020 2021

Per unit Total amount Per unit Total amount

Sales £ 95

£ 95 * 4000 = £

380000 95

£ 95 * 5000 = £

475000

Less: cost of sales

Opening

inventory 500

£ 95 * 500 = £

47500 1100

1100 * £ 95 = £

104500

Less: production

£ 18 + £ 12

+ £ 8 = £ 38

4600 * £ 38 = £

174800

£ 18 + £ 12

+£ 8 = £ 38

5100 * £ 38 = £

193800

Add: closing

inventory

500 + 4600

- 4000 =

1100

1100 * £ 95 = £

104500

1100 + 5100

- 5000 =

1200

1200 * £ 95 = £

114000

Total cost of

sales £ (22800) £ 24700

7

Presicareanu 25467

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(J-A 2021) RQFBM-MA0602053 03.2021

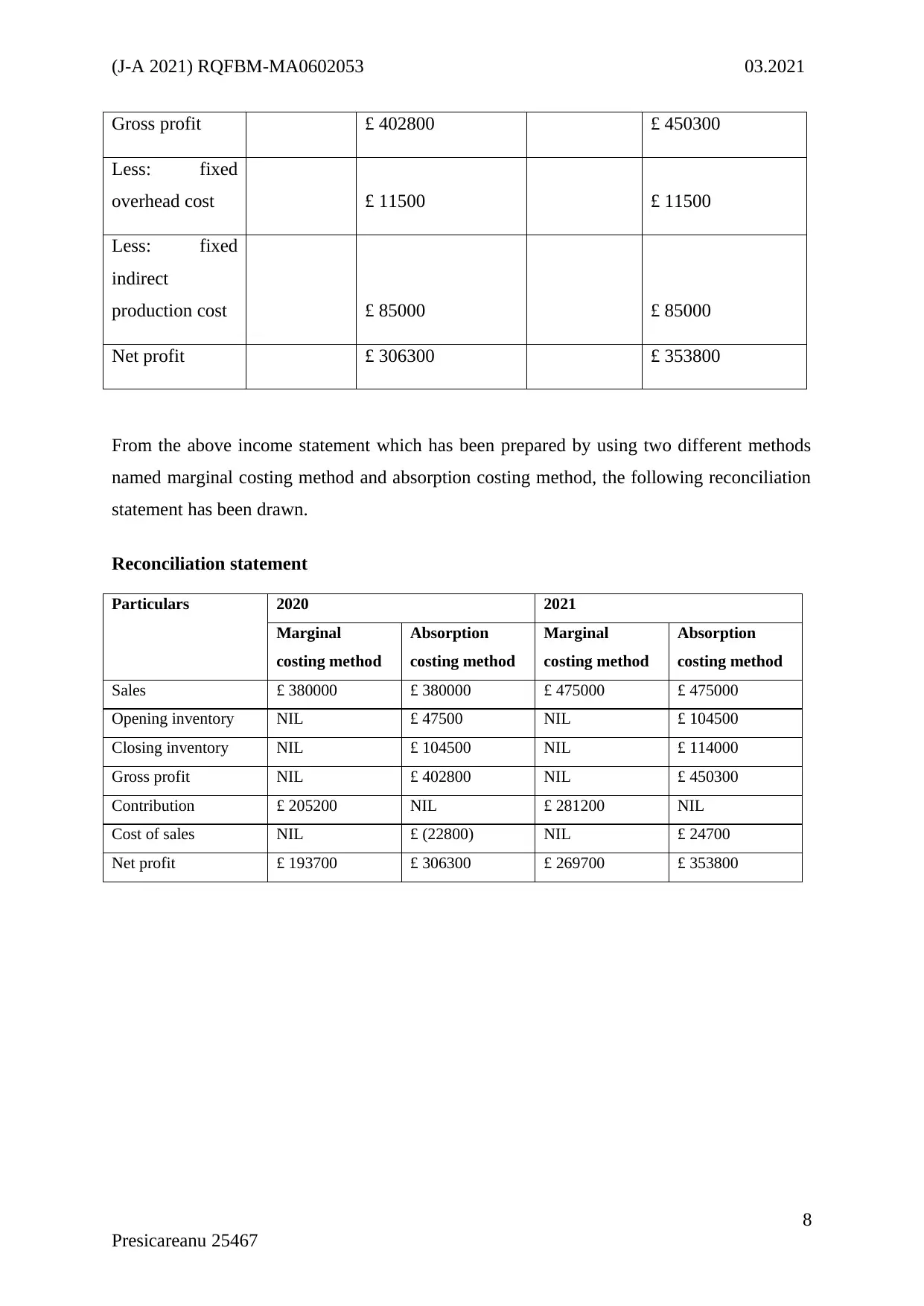

Gross profit £ 402800 £ 450300

Less: fixed

overhead cost £ 11500 £ 11500

Less: fixed

indirect

production cost £ 85000 £ 85000

Net profit £ 306300 £ 353800

From the above income statement which has been prepared by using two different methods

named marginal costing method and absorption costing method, the following reconciliation

statement has been drawn.

Reconciliation statement

Particulars 2020 2021

Marginal

costing method

Absorption

costing method

Marginal

costing method

Absorption

costing method

Sales £ 380000 £ 380000 £ 475000 £ 475000

Opening inventory NIL £ 47500 NIL £ 104500

Closing inventory NIL £ 104500 NIL £ 114000

Gross profit NIL £ 402800 NIL £ 450300

Contribution £ 205200 NIL £ 281200 NIL

Cost of sales NIL £ (22800) NIL £ 24700

Net profit £ 193700 £ 306300 £ 269700 £ 353800

8

Presicareanu 25467

Gross profit £ 402800 £ 450300

Less: fixed

overhead cost £ 11500 £ 11500

Less: fixed

indirect

production cost £ 85000 £ 85000

Net profit £ 306300 £ 353800

From the above income statement which has been prepared by using two different methods

named marginal costing method and absorption costing method, the following reconciliation

statement has been drawn.

Reconciliation statement

Particulars 2020 2021

Marginal

costing method

Absorption

costing method

Marginal

costing method

Absorption

costing method

Sales £ 380000 £ 380000 £ 475000 £ 475000

Opening inventory NIL £ 47500 NIL £ 104500

Closing inventory NIL £ 104500 NIL £ 114000

Gross profit NIL £ 402800 NIL £ 450300

Contribution £ 205200 NIL £ 281200 NIL

Cost of sales NIL £ (22800) NIL £ 24700

Net profit £ 193700 £ 306300 £ 269700 £ 353800

8

Presicareanu 25467

(J-A 2021) RQFBM-MA0602053 03.2021

Interpretation of the income statements

From the above reconciliation statement, we can understand that the amount of sales is same

in both the methods. But as per as net profit is concerned, it is evident that because of the

inclusion of different types of fixed cost, as well as the inventory calculation, the amount of

profit in both of techniques are showing different results.

Explain the use of planning tools used in management accounting

Among the different kinds of planning tools used by the business organisation, budgetary

control is one of them. For the preparation of budgetary control different kinds of budget are

used by the business organisation. From the perspective of the method the budgets can be

differentiated in two different categories which are traditional budget and alternative budget.

Under the alternative budgeting method, the activity based budgeting, the zero based

budgeting the rolling budget et cetera are the most popular tools (Gunawan et al., 2020). The

discussion on advantages and disadvantages of these tools for preparing budgetary control

has been conducted below.

Traditional budget

Here, budget of the current year is prepared by taking budget of the previous year as the base

year. The traditional budget can provide a readymade format and framework to the workers

and employees of the business organisation. But on the other hand it is also important

remember that because of the rigid nature of the traditional budget any kinds of innovation

and creativity is not motivated. Here, budget of the current year is prepared by taking budget

of the previous year as the base year (Kholod et al., 2019).

Activity based budget

Here, budget is prepared based on the cost involved in the operation of any business. Activity

based budget can provide significant guidance to the business organisation regarding

eliminating the unnecessary work to reduce the time and cost and increased efficiency. But

for the preparation of this budget, significant amount of cost and time is needed along with

the expert knowledge and skill. Here, budget is prepared based on the cost involved in the

operation of any business (Zheng and Abu, 2019).

9

Presicareanu 25467

Interpretation of the income statements

From the above reconciliation statement, we can understand that the amount of sales is same

in both the methods. But as per as net profit is concerned, it is evident that because of the

inclusion of different types of fixed cost, as well as the inventory calculation, the amount of

profit in both of techniques are showing different results.

Explain the use of planning tools used in management accounting

Among the different kinds of planning tools used by the business organisation, budgetary

control is one of them. For the preparation of budgetary control different kinds of budget are

used by the business organisation. From the perspective of the method the budgets can be

differentiated in two different categories which are traditional budget and alternative budget.

Under the alternative budgeting method, the activity based budgeting, the zero based

budgeting the rolling budget et cetera are the most popular tools (Gunawan et al., 2020). The

discussion on advantages and disadvantages of these tools for preparing budgetary control

has been conducted below.

Traditional budget

Here, budget of the current year is prepared by taking budget of the previous year as the base

year. The traditional budget can provide a readymade format and framework to the workers

and employees of the business organisation. But on the other hand it is also important

remember that because of the rigid nature of the traditional budget any kinds of innovation

and creativity is not motivated. Here, budget of the current year is prepared by taking budget

of the previous year as the base year (Kholod et al., 2019).

Activity based budget

Here, budget is prepared based on the cost involved in the operation of any business. Activity

based budget can provide significant guidance to the business organisation regarding

eliminating the unnecessary work to reduce the time and cost and increased efficiency. But

for the preparation of this budget, significant amount of cost and time is needed along with

the expert knowledge and skill. Here, budget is prepared based on the cost involved in the

operation of any business (Zheng and Abu, 2019).

9

Presicareanu 25467

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(J-A 2021) RQFBM-MA0602053 03.2021

Zero based budget

Under this category, the budget for the next budget cycle for the organisation starts from zero

level instead of increasing the current expenditure. The zero based budget can you help the

business organisation by analysing each and every activity to prioritise the same. But for this

purpose a high amount of labour, time, and cost is needed. (Erasmus, 2020).

Rolling budget

Here, new budgets are updated continuously as soon as the most recent budget period is

completed. The rolling budget can help the business organisation in keep up with the

continuous change in the business environment. But without the continuous updation in the

rolling budget, the efficiency of the same will be lost (Bhimani et al., 2018).

Analyse the use of different planning tools and their application for preparing and

forecasting budgets.

Planning is essential for creating the blueprint of what the organisation expects in the

upcoming years and on which financial direction it is currently heading. Companies generally

prepare their budgets at the beginning of a fiscal year with certain adjustments with the

growth or decline of revenue. Planning varies on a monthly basis in accordance with the

performance in the market as well as other unforeseen circumstances. Estimates of revenue

and expenses along with the inflow and outflow of cash help the management team to plan

their operations. Pricing pattern followed by the organisation is planned as per the cost

expenses as well as the prices followed by its competitors.

Compare how organisations are adapting management accounting systems to respond

to financial problems.

From the above discussion in the report it is clearly understandable that there are various kind

of tools techniques and methods can be available under the field of management accounting.

In order to adopt the management accounting system in the business organisation there are

various kind of tools and techniques which can be used by the business organisation for

different purpose to achieve the objective and success.

10

Presicareanu 25467

Zero based budget

Under this category, the budget for the next budget cycle for the organisation starts from zero

level instead of increasing the current expenditure. The zero based budget can you help the

business organisation by analysing each and every activity to prioritise the same. But for this

purpose a high amount of labour, time, and cost is needed. (Erasmus, 2020).

Rolling budget

Here, new budgets are updated continuously as soon as the most recent budget period is

completed. The rolling budget can help the business organisation in keep up with the

continuous change in the business environment. But without the continuous updation in the

rolling budget, the efficiency of the same will be lost (Bhimani et al., 2018).

Analyse the use of different planning tools and their application for preparing and

forecasting budgets.

Planning is essential for creating the blueprint of what the organisation expects in the

upcoming years and on which financial direction it is currently heading. Companies generally

prepare their budgets at the beginning of a fiscal year with certain adjustments with the

growth or decline of revenue. Planning varies on a monthly basis in accordance with the

performance in the market as well as other unforeseen circumstances. Estimates of revenue

and expenses along with the inflow and outflow of cash help the management team to plan

their operations. Pricing pattern followed by the organisation is planned as per the cost

expenses as well as the prices followed by its competitors.

Compare how organisations are adapting management accounting systems to respond

to financial problems.

From the above discussion in the report it is clearly understandable that there are various kind

of tools techniques and methods can be available under the field of management accounting.

In order to adopt the management accounting system in the business organisation there are

various kind of tools and techniques which can be used by the business organisation for

different purpose to achieve the objective and success.

10

Presicareanu 25467

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(J-A 2021) RQFBM-MA0602053 03.2021

Cost accounting Pricing strategy Budgetary control

Cost accounting help

the organisation in

solving the issues

related to cost

problems (Hilorme et

al., 2019).

To help the business

organisation in

increasing the price

margin of the

organisation to

maximize the profit.

Reduction of the cost

(both operational and

production) (Marota

et al., 2017).

To help the

organisation in

ensuring the

maximum utilisation

of the resources to

optimise the benefit

from the

same(Marota et al.,

2017).

In order to maintain

the coordination and

cooperation in the

organisation.

The pricing strategy

of the organisation

determines the price

of the product and

services (Kung and

Zhong, 2017).

In order to maximize

the profit of the

organisation.

To maintain the

customer base while

maximize the price

of the product (Kung

and Zhong, 2017).

To help the

organisation in

attracting different

customers from

different segments of

the market.

To help the in

providing the chance

to balance the profit

maximization in the

market without

losing any customer

(Kung and Zhong,

2017).

Budgetary control is

conducted in order to

predict and forecast

the revenue and

expenditure of the

organisation for the

future period of time.

To predict and

forecast the revenue

and expenditure of

the organisation for

the future period of

time.

For the purpose of

allocation of

resources among the

different departments

of the organisation.

(Henttu-Aho, 2018).

To help the

organisation in

maintaining the

cooperation and

coordination

between different

departments

individuals and

teams.

In order to reduce the

cost and unnecessary

activities of the

organisation (Henttu-

11

Presicareanu 25467

Cost accounting Pricing strategy Budgetary control

Cost accounting help

the organisation in

solving the issues

related to cost

problems (Hilorme et

al., 2019).

To help the business

organisation in

increasing the price

margin of the

organisation to

maximize the profit.

Reduction of the cost

(both operational and

production) (Marota

et al., 2017).

To help the

organisation in

ensuring the

maximum utilisation

of the resources to

optimise the benefit

from the

same(Marota et al.,

2017).

In order to maintain

the coordination and

cooperation in the

organisation.

The pricing strategy

of the organisation

determines the price

of the product and

services (Kung and

Zhong, 2017).

In order to maximize

the profit of the

organisation.

To maintain the

customer base while

maximize the price

of the product (Kung

and Zhong, 2017).

To help the

organisation in

attracting different

customers from

different segments of

the market.

To help the in

providing the chance

to balance the profit

maximization in the

market without

losing any customer

(Kung and Zhong,

2017).

Budgetary control is

conducted in order to

predict and forecast

the revenue and

expenditure of the

organisation for the

future period of time.

To predict and

forecast the revenue

and expenditure of

the organisation for

the future period of

time.

For the purpose of

allocation of

resources among the

different departments

of the organisation.

(Henttu-Aho, 2018).

To help the

organisation in

maintaining the

cooperation and

coordination

between different

departments

individuals and

teams.

In order to reduce the

cost and unnecessary

activities of the

organisation (Henttu-

11

Presicareanu 25467

(J-A 2021) RQFBM-MA0602053 03.2021

Aho, 2018).

From the above discussion in the report it is clearly understandable that there are various kind

of tools techniques and methods can be available under the field of management accounting.

In order to adopt the management accounting system in the business organisation there are

various kind of tools and techniques which can be used by the business organisation for

different purpose to achieve the objective and success.

Cost accounting

Cost accounting can be considered one of the most important part of management accounting

who is used by the business organisation for the purpose of solving the issues regarding the

cost. The management of cost in the business play a significant role in maintaining the profit

margin as well as improving the same(Hilorme et al., 2019). Through the different tools of

cost accounting, the efficiency of managing the cost in the business can be improved.

Pricing strategy

The use of pricing strategy can be conducted by the management of the business organisation

to increase the profit margin in the business. Also it is important to remember that the

appropriate use a pricing strategy can also help the business organisation in attracting more

customer from different segments of the market to increase the customer base as well as the

revenue and profit of the business(Kienzler and Kowalkowski, 2017).

Budgetary control

Budgetary control is another most important and common method of management accounting

which is used by the business organisation to understand and focus the future income and

expenditure of the business organisation. The forecasting regarding the future activities and

transaction of the business organisation will help the business organisation in better allocation

of the capital resources which can provide the competitive edge to the business

organisation(Henttu-Aho, 2018).

12

Presicareanu 25467

Aho, 2018).

From the above discussion in the report it is clearly understandable that there are various kind

of tools techniques and methods can be available under the field of management accounting.

In order to adopt the management accounting system in the business organisation there are

various kind of tools and techniques which can be used by the business organisation for

different purpose to achieve the objective and success.

Cost accounting

Cost accounting can be considered one of the most important part of management accounting

who is used by the business organisation for the purpose of solving the issues regarding the

cost. The management of cost in the business play a significant role in maintaining the profit

margin as well as improving the same(Hilorme et al., 2019). Through the different tools of

cost accounting, the efficiency of managing the cost in the business can be improved.

Pricing strategy

The use of pricing strategy can be conducted by the management of the business organisation

to increase the profit margin in the business. Also it is important to remember that the

appropriate use a pricing strategy can also help the business organisation in attracting more

customer from different segments of the market to increase the customer base as well as the

revenue and profit of the business(Kienzler and Kowalkowski, 2017).

Budgetary control

Budgetary control is another most important and common method of management accounting

which is used by the business organisation to understand and focus the future income and

expenditure of the business organisation. The forecasting regarding the future activities and

transaction of the business organisation will help the business organisation in better allocation

of the capital resources which can provide the competitive edge to the business

organisation(Henttu-Aho, 2018).

12

Presicareanu 25467

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.