Corporate Reporting: Analysis of JB HI-FI's Cash Flow Statement, Other Comprehensive Income and Tax Flow

VerifiedAdded on 2023/06/11

|10

|2561

|368

AI Summary

This report provides an analysis of JB HI-FI's cash flow statement, other comprehensive income and tax flow. It includes a brief description of the items recorded in the cash flow statement, other comprehensive income statement and accounting for corporate income tax. The report also highlights the main reasons for the non-inclusion of certain items in the P&L statement.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CORPORATE REPORTING

Assignment

Student Name/ Id

[Pick the date]

Assignment

Student Name/ Id

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

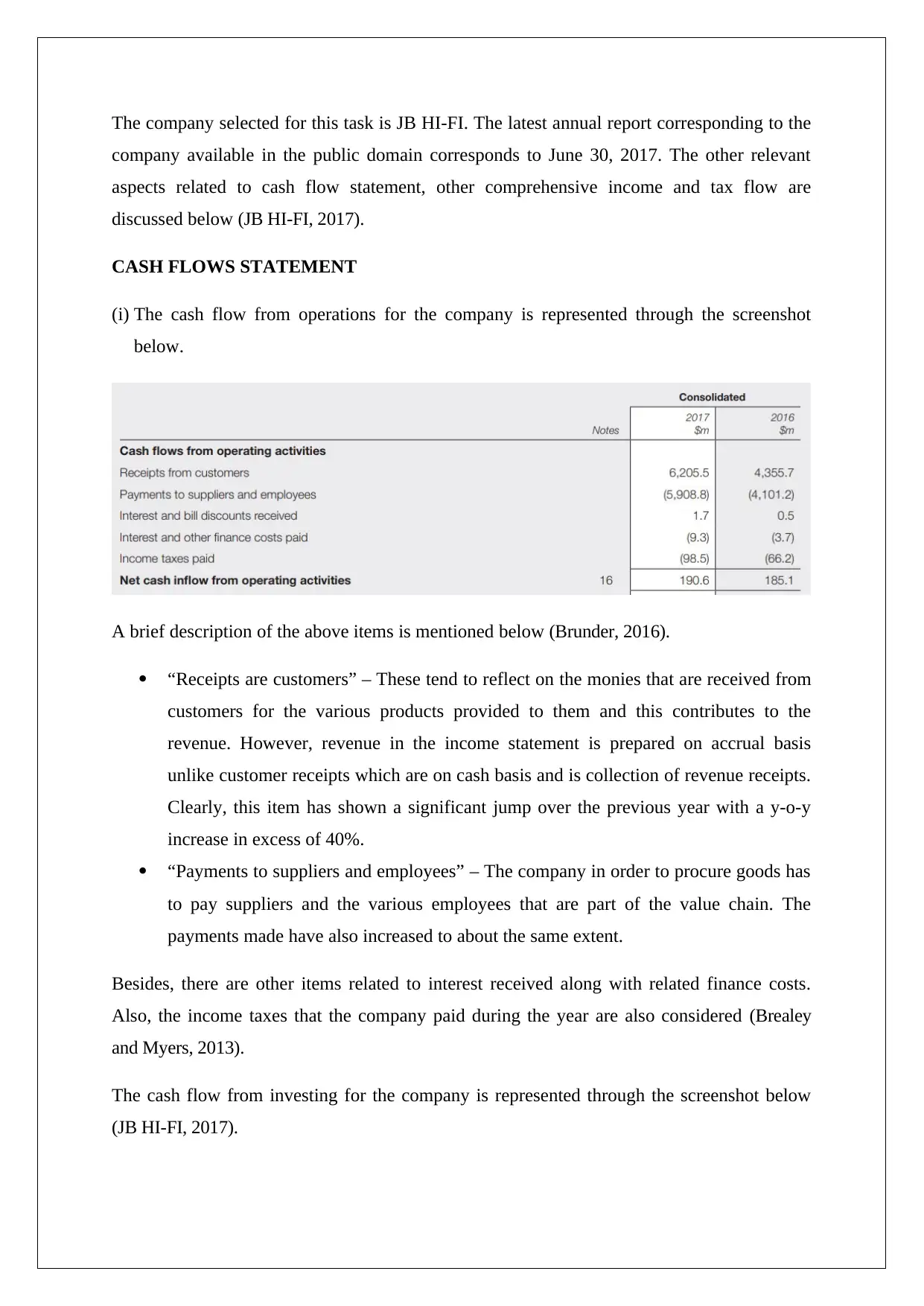

The company selected for this task is JB HI-FI. The latest annual report corresponding to the

company available in the public domain corresponds to June 30, 2017. The other relevant

aspects related to cash flow statement, other comprehensive income and tax flow are

discussed below (JB HI-FI, 2017).

CASH FLOWS STATEMENT

(i) The cash flow from operations for the company is represented through the screenshot

below.

A brief description of the above items is mentioned below (Brunder, 2016).

“Receipts are customers” – These tend to reflect on the monies that are received from

customers for the various products provided to them and this contributes to the

revenue. However, revenue in the income statement is prepared on accrual basis

unlike customer receipts which are on cash basis and is collection of revenue receipts.

Clearly, this item has shown a significant jump over the previous year with a y-o-y

increase in excess of 40%.

“Payments to suppliers and employees” – The company in order to procure goods has

to pay suppliers and the various employees that are part of the value chain. The

payments made have also increased to about the same extent.

Besides, there are other items related to interest received along with related finance costs.

Also, the income taxes that the company paid during the year are also considered (Brealey

and Myers, 2013).

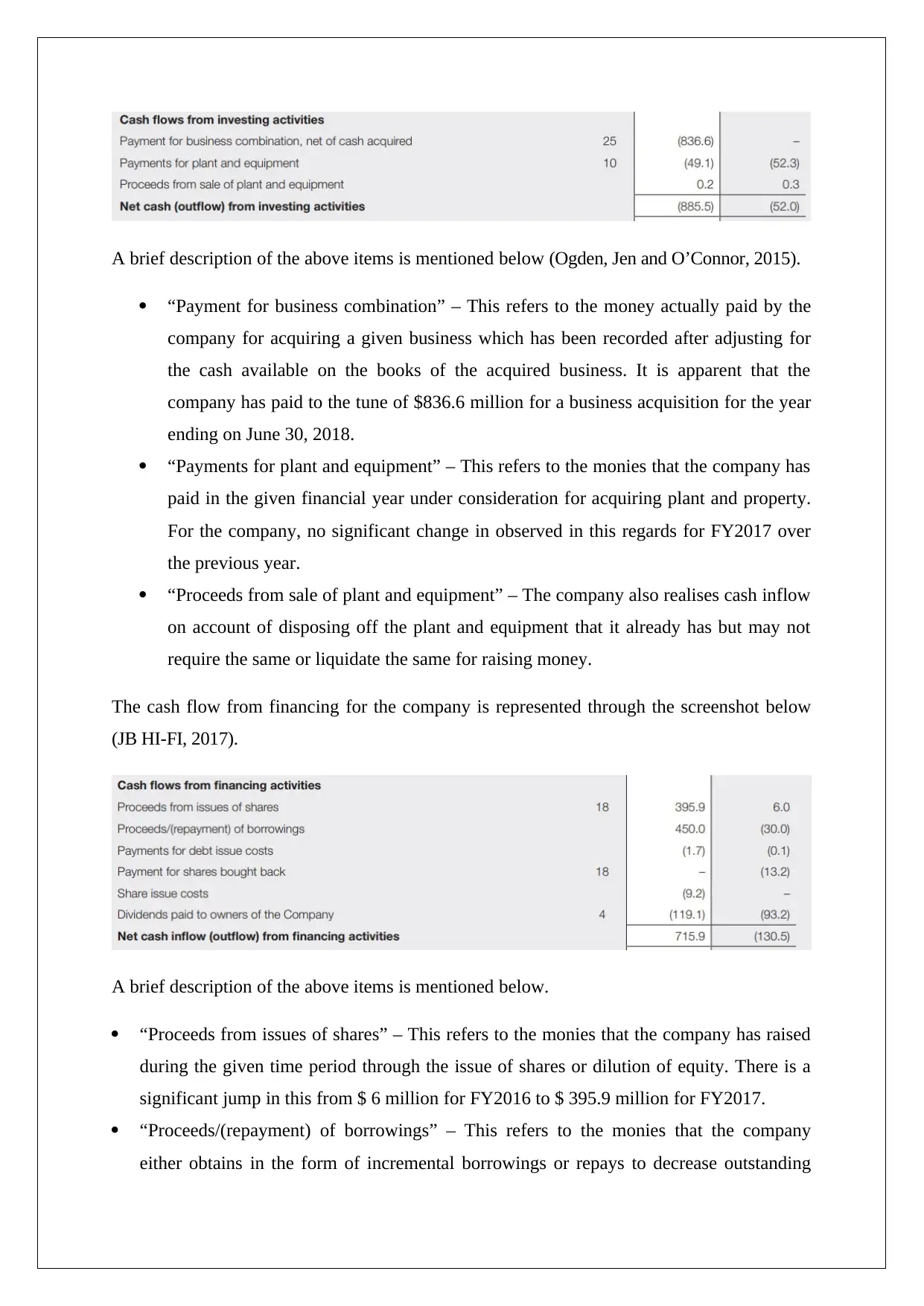

The cash flow from investing for the company is represented through the screenshot below

(JB HI-FI, 2017).

company available in the public domain corresponds to June 30, 2017. The other relevant

aspects related to cash flow statement, other comprehensive income and tax flow are

discussed below (JB HI-FI, 2017).

CASH FLOWS STATEMENT

(i) The cash flow from operations for the company is represented through the screenshot

below.

A brief description of the above items is mentioned below (Brunder, 2016).

“Receipts are customers” – These tend to reflect on the monies that are received from

customers for the various products provided to them and this contributes to the

revenue. However, revenue in the income statement is prepared on accrual basis

unlike customer receipts which are on cash basis and is collection of revenue receipts.

Clearly, this item has shown a significant jump over the previous year with a y-o-y

increase in excess of 40%.

“Payments to suppliers and employees” – The company in order to procure goods has

to pay suppliers and the various employees that are part of the value chain. The

payments made have also increased to about the same extent.

Besides, there are other items related to interest received along with related finance costs.

Also, the income taxes that the company paid during the year are also considered (Brealey

and Myers, 2013).

The cash flow from investing for the company is represented through the screenshot below

(JB HI-FI, 2017).

A brief description of the above items is mentioned below (Ogden, Jen and O’Connor, 2015).

“Payment for business combination” – This refers to the money actually paid by the

company for acquiring a given business which has been recorded after adjusting for

the cash available on the books of the acquired business. It is apparent that the

company has paid to the tune of $836.6 million for a business acquisition for the year

ending on June 30, 2018.

“Payments for plant and equipment” – This refers to the monies that the company has

paid in the given financial year under consideration for acquiring plant and property.

For the company, no significant change in observed in this regards for FY2017 over

the previous year.

“Proceeds from sale of plant and equipment” – The company also realises cash inflow

on account of disposing off the plant and equipment that it already has but may not

require the same or liquidate the same for raising money.

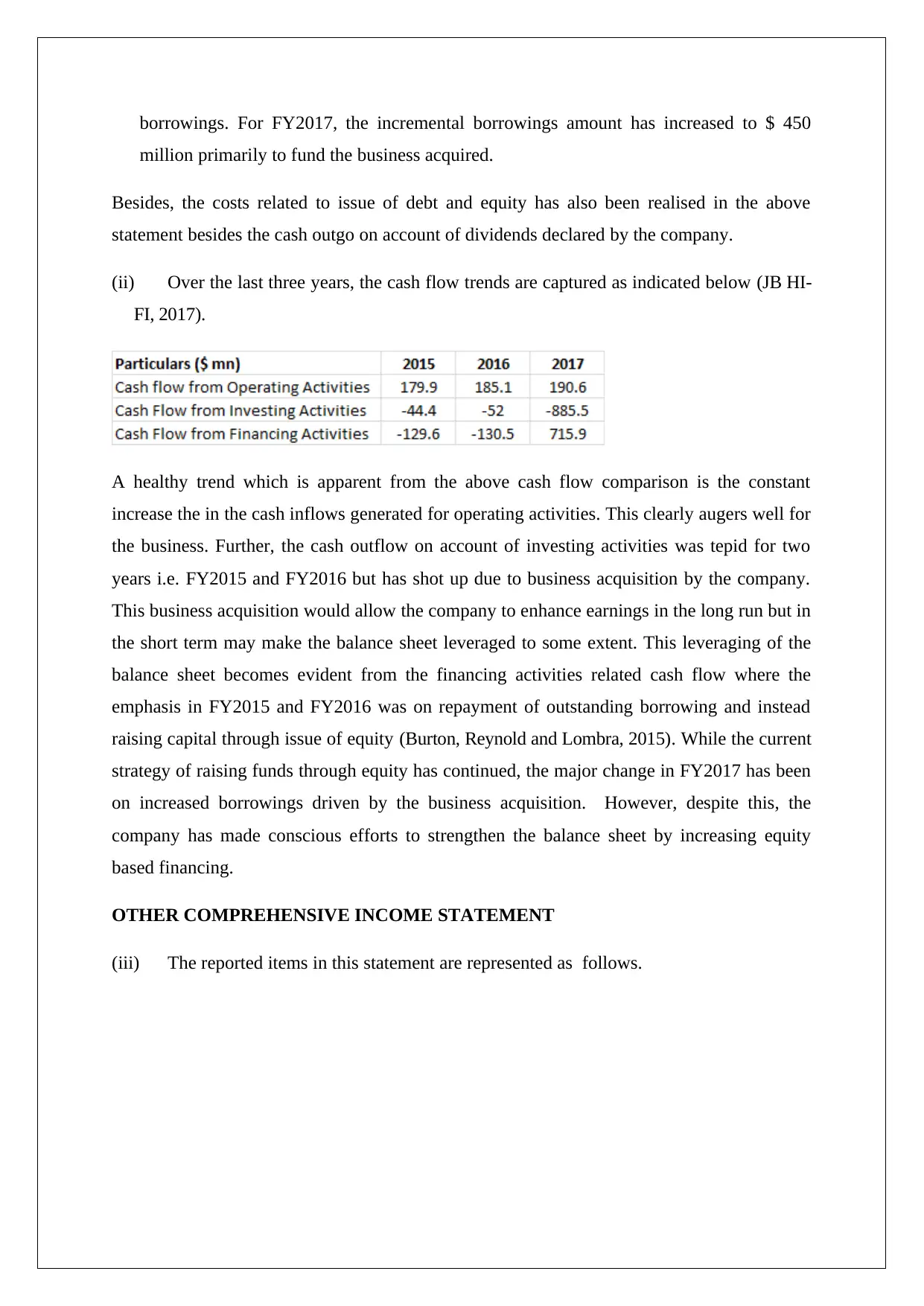

The cash flow from financing for the company is represented through the screenshot below

(JB HI-FI, 2017).

A brief description of the above items is mentioned below.

“Proceeds from issues of shares” – This refers to the monies that the company has raised

during the given time period through the issue of shares or dilution of equity. There is a

significant jump in this from $ 6 million for FY2016 to $ 395.9 million for FY2017.

“Proceeds/(repayment) of borrowings” – This refers to the monies that the company

either obtains in the form of incremental borrowings or repays to decrease outstanding

“Payment for business combination” – This refers to the money actually paid by the

company for acquiring a given business which has been recorded after adjusting for

the cash available on the books of the acquired business. It is apparent that the

company has paid to the tune of $836.6 million for a business acquisition for the year

ending on June 30, 2018.

“Payments for plant and equipment” – This refers to the monies that the company has

paid in the given financial year under consideration for acquiring plant and property.

For the company, no significant change in observed in this regards for FY2017 over

the previous year.

“Proceeds from sale of plant and equipment” – The company also realises cash inflow

on account of disposing off the plant and equipment that it already has but may not

require the same or liquidate the same for raising money.

The cash flow from financing for the company is represented through the screenshot below

(JB HI-FI, 2017).

A brief description of the above items is mentioned below.

“Proceeds from issues of shares” – This refers to the monies that the company has raised

during the given time period through the issue of shares or dilution of equity. There is a

significant jump in this from $ 6 million for FY2016 to $ 395.9 million for FY2017.

“Proceeds/(repayment) of borrowings” – This refers to the monies that the company

either obtains in the form of incremental borrowings or repays to decrease outstanding

borrowings. For FY2017, the incremental borrowings amount has increased to $ 450

million primarily to fund the business acquired.

Besides, the costs related to issue of debt and equity has also been realised in the above

statement besides the cash outgo on account of dividends declared by the company.

(ii) Over the last three years, the cash flow trends are captured as indicated below (JB HI-

FI, 2017).

A healthy trend which is apparent from the above cash flow comparison is the constant

increase the in the cash inflows generated for operating activities. This clearly augers well for

the business. Further, the cash outflow on account of investing activities was tepid for two

years i.e. FY2015 and FY2016 but has shot up due to business acquisition by the company.

This business acquisition would allow the company to enhance earnings in the long run but in

the short term may make the balance sheet leveraged to some extent. This leveraging of the

balance sheet becomes evident from the financing activities related cash flow where the

emphasis in FY2015 and FY2016 was on repayment of outstanding borrowing and instead

raising capital through issue of equity (Burton, Reynold and Lombra, 2015). While the current

strategy of raising funds through equity has continued, the major change in FY2017 has been

on increased borrowings driven by the business acquisition. However, despite this, the

company has made conscious efforts to strengthen the balance sheet by increasing equity

based financing.

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) The reported items in this statement are represented as follows.

million primarily to fund the business acquired.

Besides, the costs related to issue of debt and equity has also been realised in the above

statement besides the cash outgo on account of dividends declared by the company.

(ii) Over the last three years, the cash flow trends are captured as indicated below (JB HI-

FI, 2017).

A healthy trend which is apparent from the above cash flow comparison is the constant

increase the in the cash inflows generated for operating activities. This clearly augers well for

the business. Further, the cash outflow on account of investing activities was tepid for two

years i.e. FY2015 and FY2016 but has shot up due to business acquisition by the company.

This business acquisition would allow the company to enhance earnings in the long run but in

the short term may make the balance sheet leveraged to some extent. This leveraging of the

balance sheet becomes evident from the financing activities related cash flow where the

emphasis in FY2015 and FY2016 was on repayment of outstanding borrowing and instead

raising capital through issue of equity (Burton, Reynold and Lombra, 2015). While the current

strategy of raising funds through equity has continued, the major change in FY2017 has been

on increased borrowings driven by the business acquisition. However, despite this, the

company has made conscious efforts to strengthen the balance sheet by increasing equity

based financing.

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) The reported items in this statement are represented as follows.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

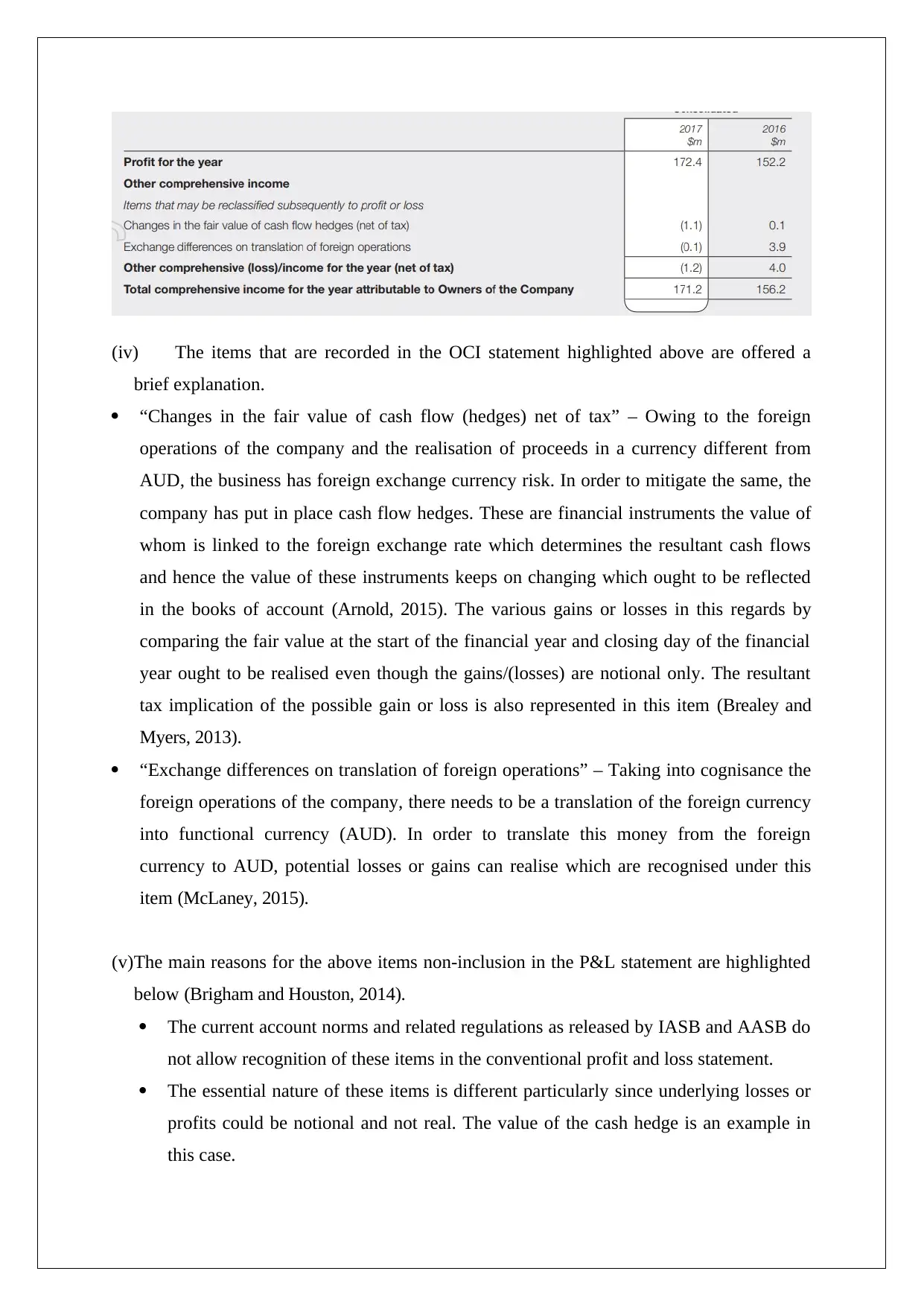

(iv) The items that are recorded in the OCI statement highlighted above are offered a

brief explanation.

“Changes in the fair value of cash flow (hedges) net of tax” – Owing to the foreign

operations of the company and the realisation of proceeds in a currency different from

AUD, the business has foreign exchange currency risk. In order to mitigate the same, the

company has put in place cash flow hedges. These are financial instruments the value of

whom is linked to the foreign exchange rate which determines the resultant cash flows

and hence the value of these instruments keeps on changing which ought to be reflected

in the books of account (Arnold, 2015). The various gains or losses in this regards by

comparing the fair value at the start of the financial year and closing day of the financial

year ought to be realised even though the gains/(losses) are notional only. The resultant

tax implication of the possible gain or loss is also represented in this item (Brealey and

Myers, 2013).

“Exchange differences on translation of foreign operations” – Taking into cognisance the

foreign operations of the company, there needs to be a translation of the foreign currency

into functional currency (AUD). In order to translate this money from the foreign

currency to AUD, potential losses or gains can realise which are recognised under this

item (McLaney, 2015).

(v)The main reasons for the above items non-inclusion in the P&L statement are highlighted

below (Brigham and Houston, 2014).

The current account norms and related regulations as released by IASB and AASB do

not allow recognition of these items in the conventional profit and loss statement.

The essential nature of these items is different particularly since underlying losses or

profits could be notional and not real. The value of the cash hedge is an example in

this case.

brief explanation.

“Changes in the fair value of cash flow (hedges) net of tax” – Owing to the foreign

operations of the company and the realisation of proceeds in a currency different from

AUD, the business has foreign exchange currency risk. In order to mitigate the same, the

company has put in place cash flow hedges. These are financial instruments the value of

whom is linked to the foreign exchange rate which determines the resultant cash flows

and hence the value of these instruments keeps on changing which ought to be reflected

in the books of account (Arnold, 2015). The various gains or losses in this regards by

comparing the fair value at the start of the financial year and closing day of the financial

year ought to be realised even though the gains/(losses) are notional only. The resultant

tax implication of the possible gain or loss is also represented in this item (Brealey and

Myers, 2013).

“Exchange differences on translation of foreign operations” – Taking into cognisance the

foreign operations of the company, there needs to be a translation of the foreign currency

into functional currency (AUD). In order to translate this money from the foreign

currency to AUD, potential losses or gains can realise which are recognised under this

item (McLaney, 2015).

(v)The main reasons for the above items non-inclusion in the P&L statement are highlighted

below (Brigham and Houston, 2014).

The current account norms and related regulations as released by IASB and AASB do

not allow recognition of these items in the conventional profit and loss statement.

The essential nature of these items is different particularly since underlying losses or

profits could be notional and not real. The value of the cash hedge is an example in

this case.

Also, this loss or gain usually is not the direct or intended consequence of the

operating activity. However, it does not imply that items listed in the OCI statement

lack significance.

ACCOUNTING FOR CORPORATE INCOME TAX

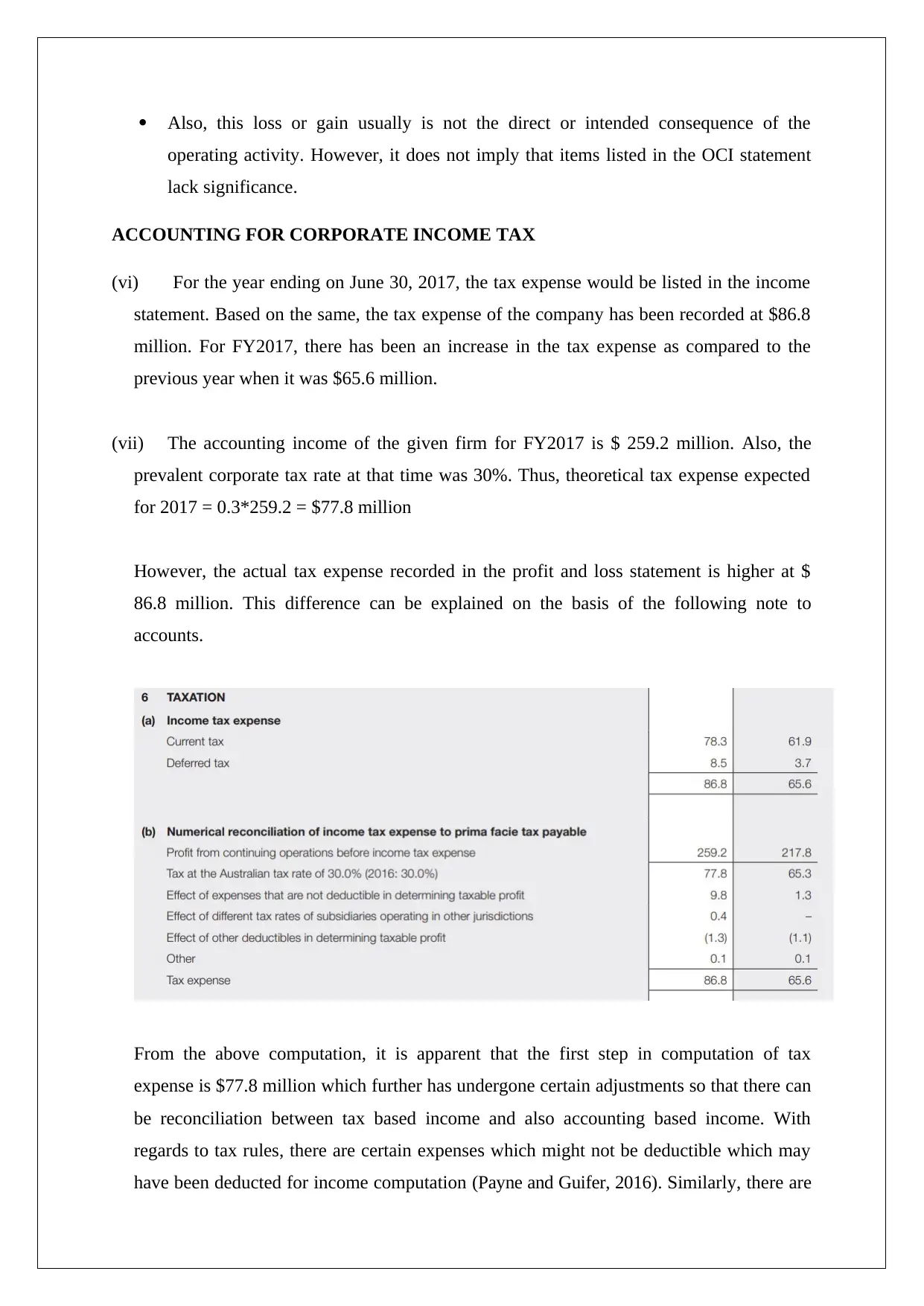

(vi) For the year ending on June 30, 2017, the tax expense would be listed in the income

statement. Based on the same, the tax expense of the company has been recorded at $86.8

million. For FY2017, there has been an increase in the tax expense as compared to the

previous year when it was $65.6 million.

(vii) The accounting income of the given firm for FY2017 is $ 259.2 million. Also, the

prevalent corporate tax rate at that time was 30%. Thus, theoretical tax expense expected

for 2017 = 0.3*259.2 = $77.8 million

However, the actual tax expense recorded in the profit and loss statement is higher at $

86.8 million. This difference can be explained on the basis of the following note to

accounts.

From the above computation, it is apparent that the first step in computation of tax

expense is $77.8 million which further has undergone certain adjustments so that there can

be reconciliation between tax based income and also accounting based income. With

regards to tax rules, there are certain expenses which might not be deductible which may

have been deducted for income computation (Payne and Guifer, 2016). Similarly, there are

operating activity. However, it does not imply that items listed in the OCI statement

lack significance.

ACCOUNTING FOR CORPORATE INCOME TAX

(vi) For the year ending on June 30, 2017, the tax expense would be listed in the income

statement. Based on the same, the tax expense of the company has been recorded at $86.8

million. For FY2017, there has been an increase in the tax expense as compared to the

previous year when it was $65.6 million.

(vii) The accounting income of the given firm for FY2017 is $ 259.2 million. Also, the

prevalent corporate tax rate at that time was 30%. Thus, theoretical tax expense expected

for 2017 = 0.3*259.2 = $77.8 million

However, the actual tax expense recorded in the profit and loss statement is higher at $

86.8 million. This difference can be explained on the basis of the following note to

accounts.

From the above computation, it is apparent that the first step in computation of tax

expense is $77.8 million which further has undergone certain adjustments so that there can

be reconciliation between tax based income and also accounting based income. With

regards to tax rules, there are certain expenses which might not be deductible which may

have been deducted for income computation (Payne and Guifer, 2016). Similarly, there are

other deductions that would be valid under tax norms but not so under accounting.

Therefore, in order to obtain the tax payable various adjustments are carried out as shown

below.

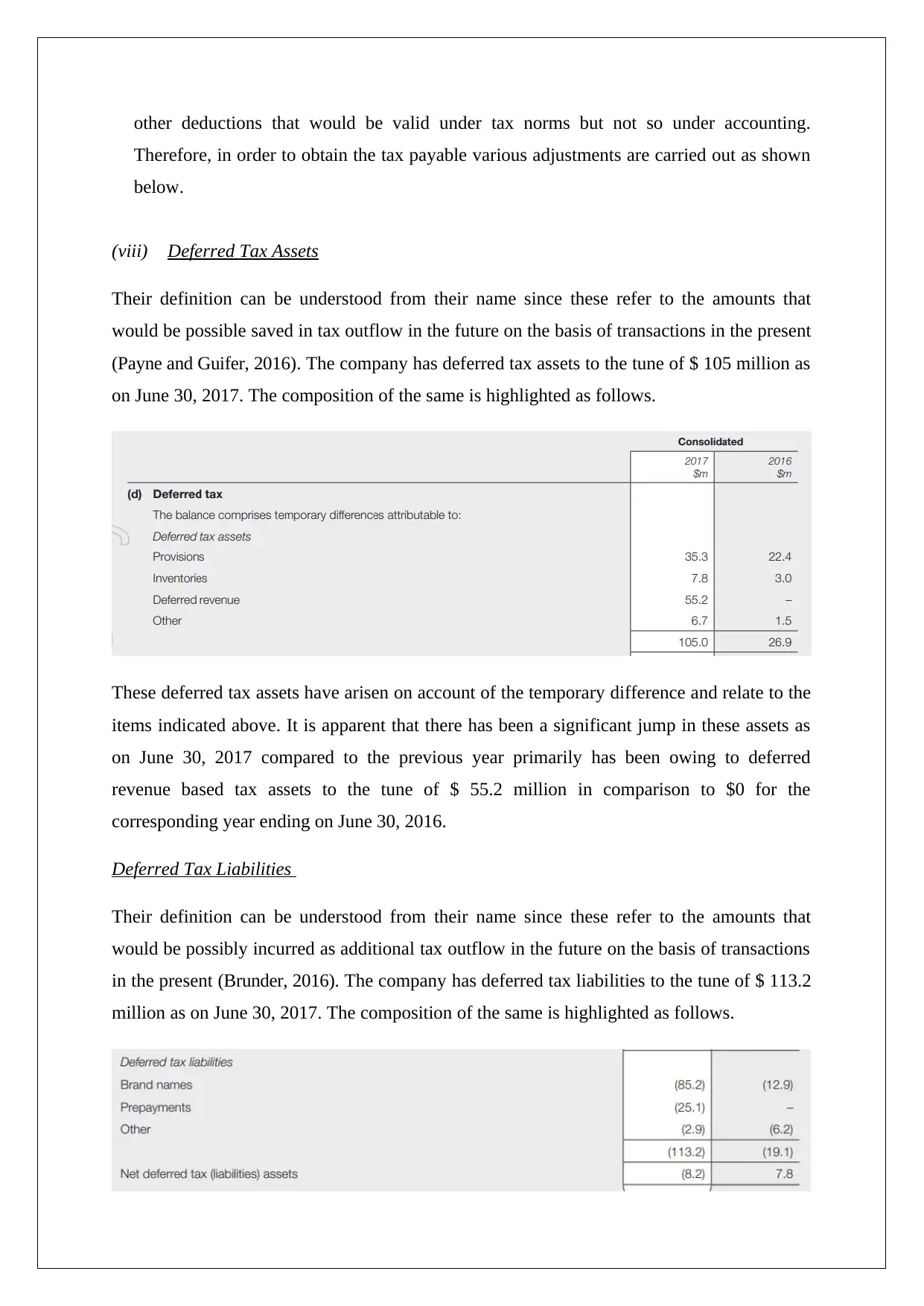

(viii) Deferred Tax Assets

Their definition can be understood from their name since these refer to the amounts that

would be possible saved in tax outflow in the future on the basis of transactions in the present

(Payne and Guifer, 2016). The company has deferred tax assets to the tune of $ 105 million as

on June 30, 2017. The composition of the same is highlighted as follows.

These deferred tax assets have arisen on account of the temporary difference and relate to the

items indicated above. It is apparent that there has been a significant jump in these assets as

on June 30, 2017 compared to the previous year primarily has been owing to deferred

revenue based tax assets to the tune of $ 55.2 million in comparison to $0 for the

corresponding year ending on June 30, 2016.

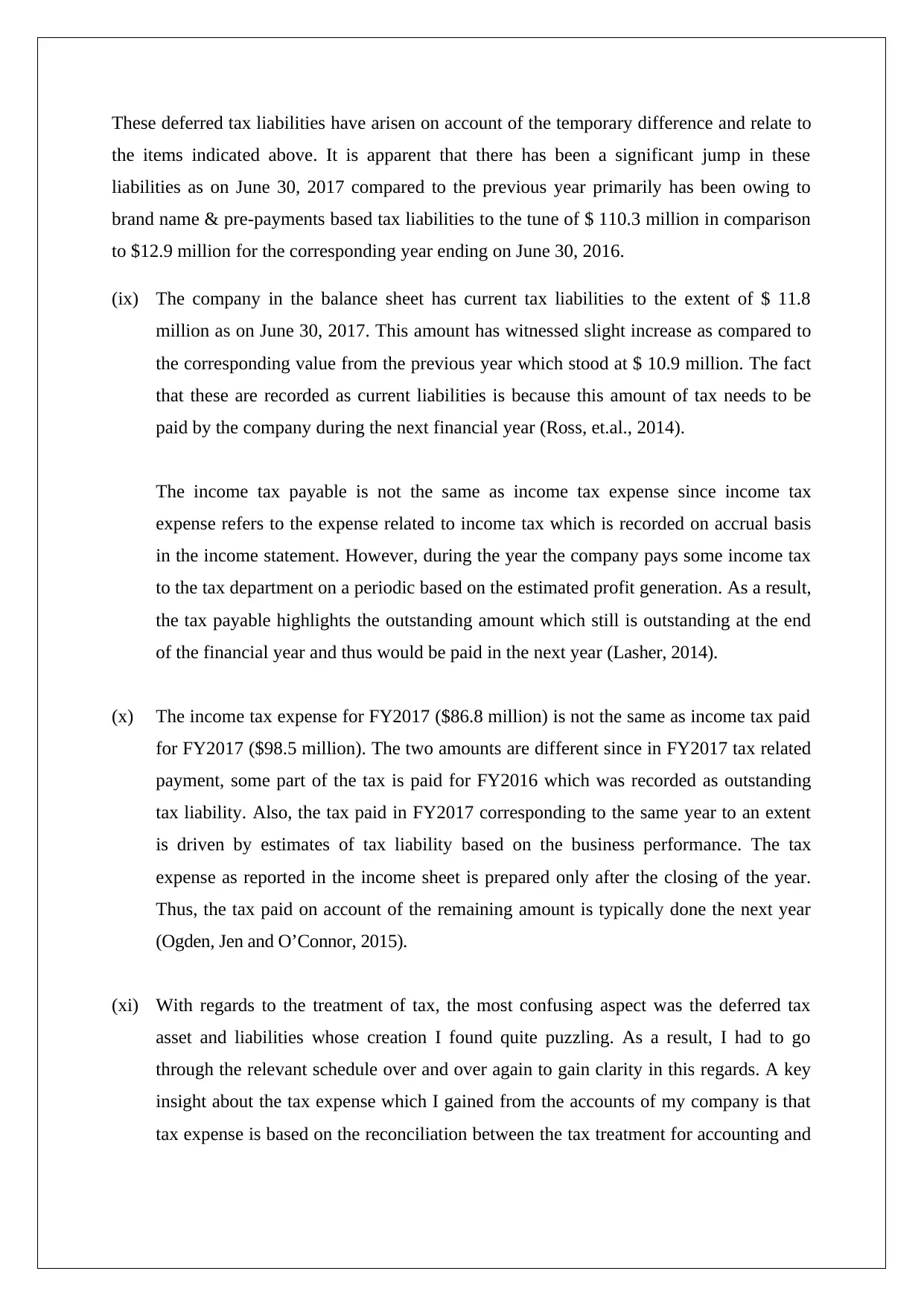

Deferred Tax Liabilities

Their definition can be understood from their name since these refer to the amounts that

would be possibly incurred as additional tax outflow in the future on the basis of transactions

in the present (Brunder, 2016). The company has deferred tax liabilities to the tune of $ 113.2

million as on June 30, 2017. The composition of the same is highlighted as follows.

Therefore, in order to obtain the tax payable various adjustments are carried out as shown

below.

(viii) Deferred Tax Assets

Their definition can be understood from their name since these refer to the amounts that

would be possible saved in tax outflow in the future on the basis of transactions in the present

(Payne and Guifer, 2016). The company has deferred tax assets to the tune of $ 105 million as

on June 30, 2017. The composition of the same is highlighted as follows.

These deferred tax assets have arisen on account of the temporary difference and relate to the

items indicated above. It is apparent that there has been a significant jump in these assets as

on June 30, 2017 compared to the previous year primarily has been owing to deferred

revenue based tax assets to the tune of $ 55.2 million in comparison to $0 for the

corresponding year ending on June 30, 2016.

Deferred Tax Liabilities

Their definition can be understood from their name since these refer to the amounts that

would be possibly incurred as additional tax outflow in the future on the basis of transactions

in the present (Brunder, 2016). The company has deferred tax liabilities to the tune of $ 113.2

million as on June 30, 2017. The composition of the same is highlighted as follows.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These deferred tax liabilities have arisen on account of the temporary difference and relate to

the items indicated above. It is apparent that there has been a significant jump in these

liabilities as on June 30, 2017 compared to the previous year primarily has been owing to

brand name & pre-payments based tax liabilities to the tune of $ 110.3 million in comparison

to $12.9 million for the corresponding year ending on June 30, 2016.

(ix) The company in the balance sheet has current tax liabilities to the extent of $ 11.8

million as on June 30, 2017. This amount has witnessed slight increase as compared to

the corresponding value from the previous year which stood at $ 10.9 million. The fact

that these are recorded as current liabilities is because this amount of tax needs to be

paid by the company during the next financial year (Ross, et.al., 2014).

The income tax payable is not the same as income tax expense since income tax

expense refers to the expense related to income tax which is recorded on accrual basis

in the income statement. However, during the year the company pays some income tax

to the tax department on a periodic based on the estimated profit generation. As a result,

the tax payable highlights the outstanding amount which still is outstanding at the end

of the financial year and thus would be paid in the next year (Lasher, 2014).

(x) The income tax expense for FY2017 ($86.8 million) is not the same as income tax paid

for FY2017 ($98.5 million). The two amounts are different since in FY2017 tax related

payment, some part of the tax is paid for FY2016 which was recorded as outstanding

tax liability. Also, the tax paid in FY2017 corresponding to the same year to an extent

is driven by estimates of tax liability based on the business performance. The tax

expense as reported in the income sheet is prepared only after the closing of the year.

Thus, the tax paid on account of the remaining amount is typically done the next year

(Ogden, Jen and O’Connor, 2015).

(xi) With regards to the treatment of tax, the most confusing aspect was the deferred tax

asset and liabilities whose creation I found quite puzzling. As a result, I had to go

through the relevant schedule over and over again to gain clarity in this regards. A key

insight about the tax expense which I gained from the accounts of my company is that

tax expense is based on the reconciliation between the tax treatment for accounting and

the items indicated above. It is apparent that there has been a significant jump in these

liabilities as on June 30, 2017 compared to the previous year primarily has been owing to

brand name & pre-payments based tax liabilities to the tune of $ 110.3 million in comparison

to $12.9 million for the corresponding year ending on June 30, 2016.

(ix) The company in the balance sheet has current tax liabilities to the extent of $ 11.8

million as on June 30, 2017. This amount has witnessed slight increase as compared to

the corresponding value from the previous year which stood at $ 10.9 million. The fact

that these are recorded as current liabilities is because this amount of tax needs to be

paid by the company during the next financial year (Ross, et.al., 2014).

The income tax payable is not the same as income tax expense since income tax

expense refers to the expense related to income tax which is recorded on accrual basis

in the income statement. However, during the year the company pays some income tax

to the tax department on a periodic based on the estimated profit generation. As a result,

the tax payable highlights the outstanding amount which still is outstanding at the end

of the financial year and thus would be paid in the next year (Lasher, 2014).

(x) The income tax expense for FY2017 ($86.8 million) is not the same as income tax paid

for FY2017 ($98.5 million). The two amounts are different since in FY2017 tax related

payment, some part of the tax is paid for FY2016 which was recorded as outstanding

tax liability. Also, the tax paid in FY2017 corresponding to the same year to an extent

is driven by estimates of tax liability based on the business performance. The tax

expense as reported in the income sheet is prepared only after the closing of the year.

Thus, the tax paid on account of the remaining amount is typically done the next year

(Ogden, Jen and O’Connor, 2015).

(xi) With regards to the treatment of tax, the most confusing aspect was the deferred tax

asset and liabilities whose creation I found quite puzzling. As a result, I had to go

through the relevant schedule over and over again to gain clarity in this regards. A key

insight about the tax expense which I gained from the accounts of my company is that

tax expense is based on the reconciliation between the tax treatment for accounting and

income tax purposes. As a result, it deviates from the theoretical value so as to make

relevant adjustments (Brigham and Houston, 2014).

References

relevant adjustments (Brigham and Houston, 2014).

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Brealey, R. and Myers, S., (2013) Principles of Corporate Finance. 9th ed. New York City:

McGraw –Hill.

Brigham, E. F. and Houston, J. F., (2014) Fundamentals of Financial Management. 14th ed.

Boston: Cengage Learning.

Bruner, R. F. (2016) Case Studies in Finance. 7th ed. New York City: McGraw-Hill Education.

Burton, M., Reynold, N. and Lombra, R. (2015) An Introduction to Financial Markets and

Institutions. 2nd ed. New York City: Routheldge.

JB HI-FI (2017) Annual Report 2017. Available at:

https://www.jbhifi.com.au/Documents/2017%20Annual%20Report.pdf (Accessed: 23 May

2018).

Lasher, W. R. (2014) Practical Financial Management. 5th ed. London: South- Western

College Publisher.

McLaney, E.J. (2015) Business Finance – Theory and Practice. 8th ed. New Jersey: Prentice

Hall.

Ogden, J., Jen, F. C. and O’Connor, P. F. (2015) Advanced Corporate Finance. 3rd ed.

London: Pearson Publisher.

Payne, J. and Gullifer, L. (2016) Corporate finance law: Principles and policy. 4th ed.

Oxford: Hart Publishing.

Ross, S.A., Trayler, R., Bird, R. and al, et (2014) Essentials of corporate finance. Sydney,

Australia: McGraw-Hill Australia.

Management.

Brealey, R. and Myers, S., (2013) Principles of Corporate Finance. 9th ed. New York City:

McGraw –Hill.

Brigham, E. F. and Houston, J. F., (2014) Fundamentals of Financial Management. 14th ed.

Boston: Cengage Learning.

Bruner, R. F. (2016) Case Studies in Finance. 7th ed. New York City: McGraw-Hill Education.

Burton, M., Reynold, N. and Lombra, R. (2015) An Introduction to Financial Markets and

Institutions. 2nd ed. New York City: Routheldge.

JB HI-FI (2017) Annual Report 2017. Available at:

https://www.jbhifi.com.au/Documents/2017%20Annual%20Report.pdf (Accessed: 23 May

2018).

Lasher, W. R. (2014) Practical Financial Management. 5th ed. London: South- Western

College Publisher.

McLaney, E.J. (2015) Business Finance – Theory and Practice. 8th ed. New Jersey: Prentice

Hall.

Ogden, J., Jen, F. C. and O’Connor, P. F. (2015) Advanced Corporate Finance. 3rd ed.

London: Pearson Publisher.

Payne, J. and Gullifer, L. (2016) Corporate finance law: Principles and policy. 4th ed.

Oxford: Hart Publishing.

Ross, S.A., Trayler, R., Bird, R. and al, et (2014) Essentials of corporate finance. Sydney,

Australia: McGraw-Hill Australia.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.