HI5020 Corporate Accounting: Detailed Analysis of JB HI-FI Financials

VerifiedAdded on 2023/06/11

|8

|1813

|242

Report

AI Summary

This report provides a detailed analysis of JB HI-FI's financial statements, focusing on the cash flow statement, other comprehensive income (OCI) statement, and accounting for corporate income tax. The analysis of the cash flow statement includes a breakdown of receipts from customers, payments t...

CORPORATE ACCOUNTING

[Type the document subtitle]

STUDENT ID:

[Pick the date]

[Type the document subtitle]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The firm listed on ASX which has been selected for this activity is JB HI-FI.

CASH FLOWS STATEMENT

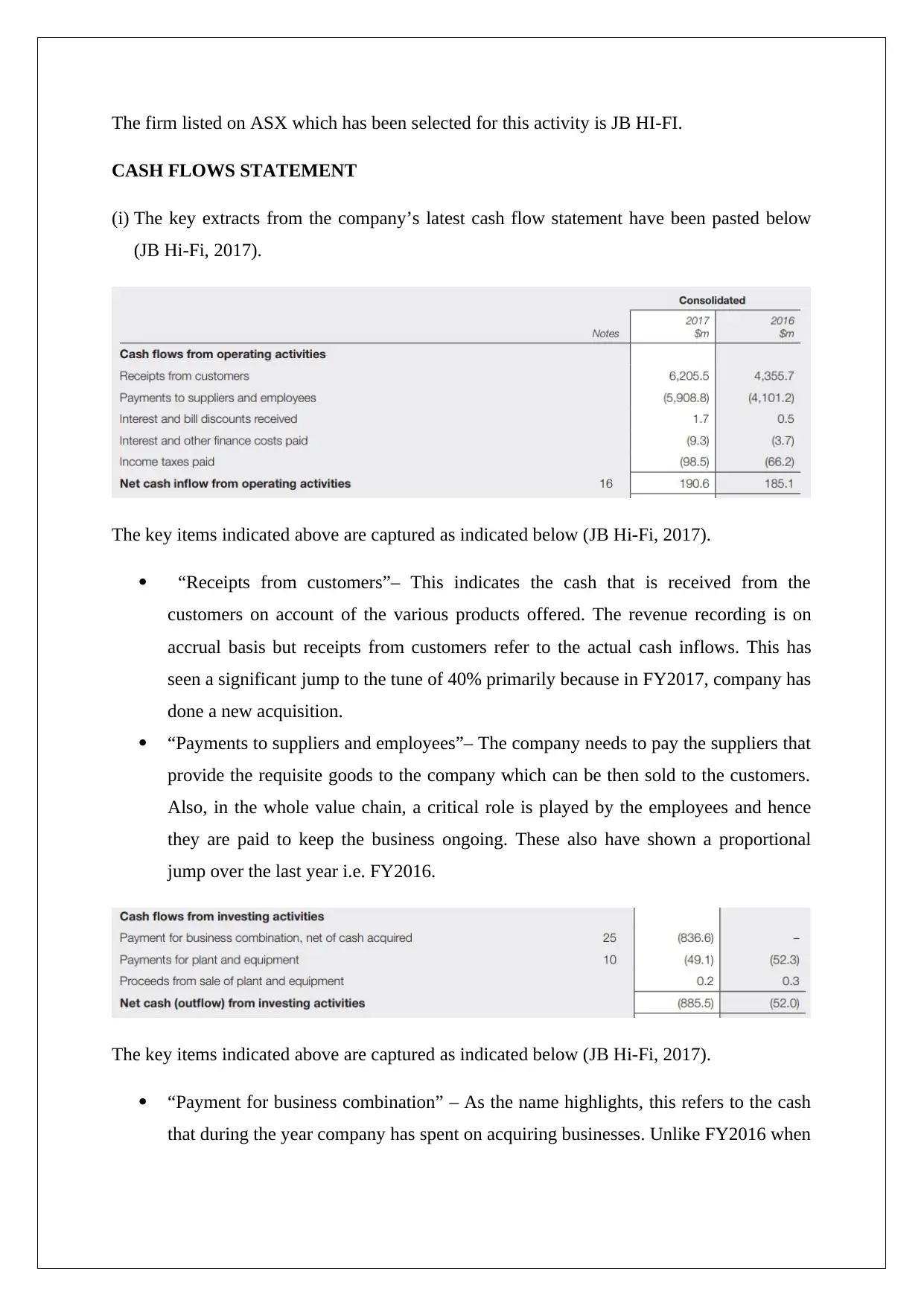

(i) The key extracts from the company’s latest cash flow statement have been pasted below

(JB Hi-Fi, 2017).

The key items indicated above are captured as indicated below (JB Hi-Fi, 2017).

“Receipts from customers”– This indicates the cash that is received from the

customers on account of the various products offered. The revenue recording is on

accrual basis but receipts from customers refer to the actual cash inflows. This has

seen a significant jump to the tune of 40% primarily because in FY2017, company has

done a new acquisition.

“Payments to suppliers and employees”– The company needs to pay the suppliers that

provide the requisite goods to the company which can be then sold to the customers.

Also, in the whole value chain, a critical role is played by the employees and hence

they are paid to keep the business ongoing. These also have shown a proportional

jump over the last year i.e. FY2016.

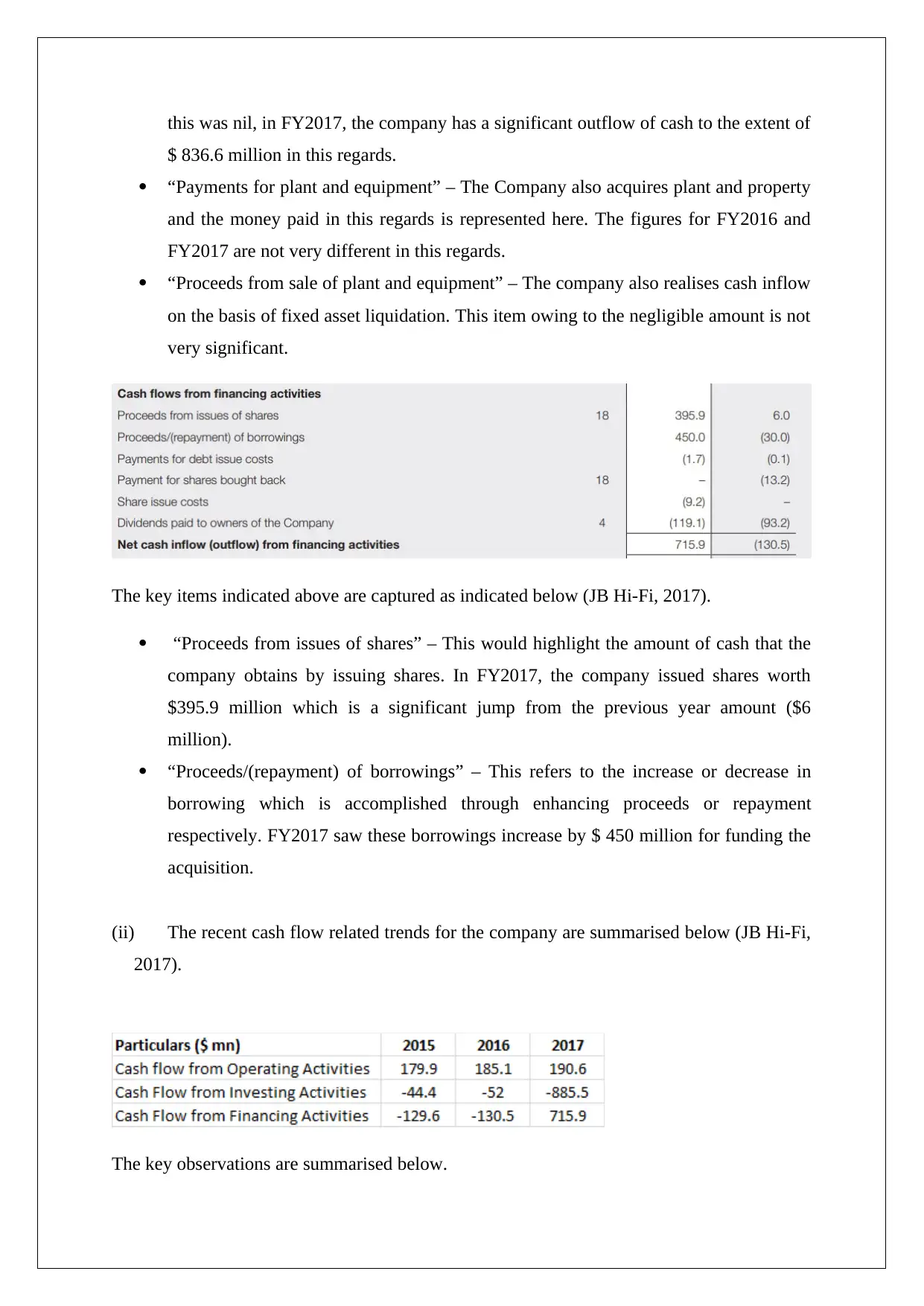

The key items indicated above are captured as indicated below (JB Hi-Fi, 2017).

“Payment for business combination” – As the name highlights, this refers to the cash

that during the year company has spent on acquiring businesses. Unlike FY2016 when

CASH FLOWS STATEMENT

(i) The key extracts from the company’s latest cash flow statement have been pasted below

(JB Hi-Fi, 2017).

The key items indicated above are captured as indicated below (JB Hi-Fi, 2017).

“Receipts from customers”– This indicates the cash that is received from the

customers on account of the various products offered. The revenue recording is on

accrual basis but receipts from customers refer to the actual cash inflows. This has

seen a significant jump to the tune of 40% primarily because in FY2017, company has

done a new acquisition.

“Payments to suppliers and employees”– The company needs to pay the suppliers that

provide the requisite goods to the company which can be then sold to the customers.

Also, in the whole value chain, a critical role is played by the employees and hence

they are paid to keep the business ongoing. These also have shown a proportional

jump over the last year i.e. FY2016.

The key items indicated above are captured as indicated below (JB Hi-Fi, 2017).

“Payment for business combination” – As the name highlights, this refers to the cash

that during the year company has spent on acquiring businesses. Unlike FY2016 when

this was nil, in FY2017, the company has a significant outflow of cash to the extent of

$ 836.6 million in this regards.

“Payments for plant and equipment” – The Company also acquires plant and property

and the money paid in this regards is represented here. The figures for FY2016 and

FY2017 are not very different in this regards.

“Proceeds from sale of plant and equipment” – The company also realises cash inflow

on the basis of fixed asset liquidation. This item owing to the negligible amount is not

very significant.

The key items indicated above are captured as indicated below (JB Hi-Fi, 2017).

“Proceeds from issues of shares” – This would highlight the amount of cash that the

company obtains by issuing shares. In FY2017, the company issued shares worth

$395.9 million which is a significant jump from the previous year amount ($6

million).

“Proceeds/(repayment) of borrowings” – This refers to the increase or decrease in

borrowing which is accomplished through enhancing proceeds or repayment

respectively. FY2017 saw these borrowings increase by $ 450 million for funding the

acquisition.

(ii) The recent cash flow related trends for the company are summarised below (JB Hi-Fi,

2017).

The key observations are summarised below.

$ 836.6 million in this regards.

“Payments for plant and equipment” – The Company also acquires plant and property

and the money paid in this regards is represented here. The figures for FY2016 and

FY2017 are not very different in this regards.

“Proceeds from sale of plant and equipment” – The company also realises cash inflow

on the basis of fixed asset liquidation. This item owing to the negligible amount is not

very significant.

The key items indicated above are captured as indicated below (JB Hi-Fi, 2017).

“Proceeds from issues of shares” – This would highlight the amount of cash that the

company obtains by issuing shares. In FY2017, the company issued shares worth

$395.9 million which is a significant jump from the previous year amount ($6

million).

“Proceeds/(repayment) of borrowings” – This refers to the increase or decrease in

borrowing which is accomplished through enhancing proceeds or repayment

respectively. FY2017 saw these borrowings increase by $ 450 million for funding the

acquisition.

(ii) The recent cash flow related trends for the company are summarised below (JB Hi-Fi,

2017).

The key observations are summarised below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operational cashflows are showing steady improvement on a y-o-y basis which

highlights that the business is stable.

Investing cashflows saw a significant jump in FY2017 owing to the acquisition.

The company had been focusing on deleveraging the balance sheet but had to raise

incremental debt in FY2017 owing to the acquisition. However, positive aspect is the

amount of equity raised by the company in FY2017.

OTHER COMPREHENSIVE INCOME STATEMENT

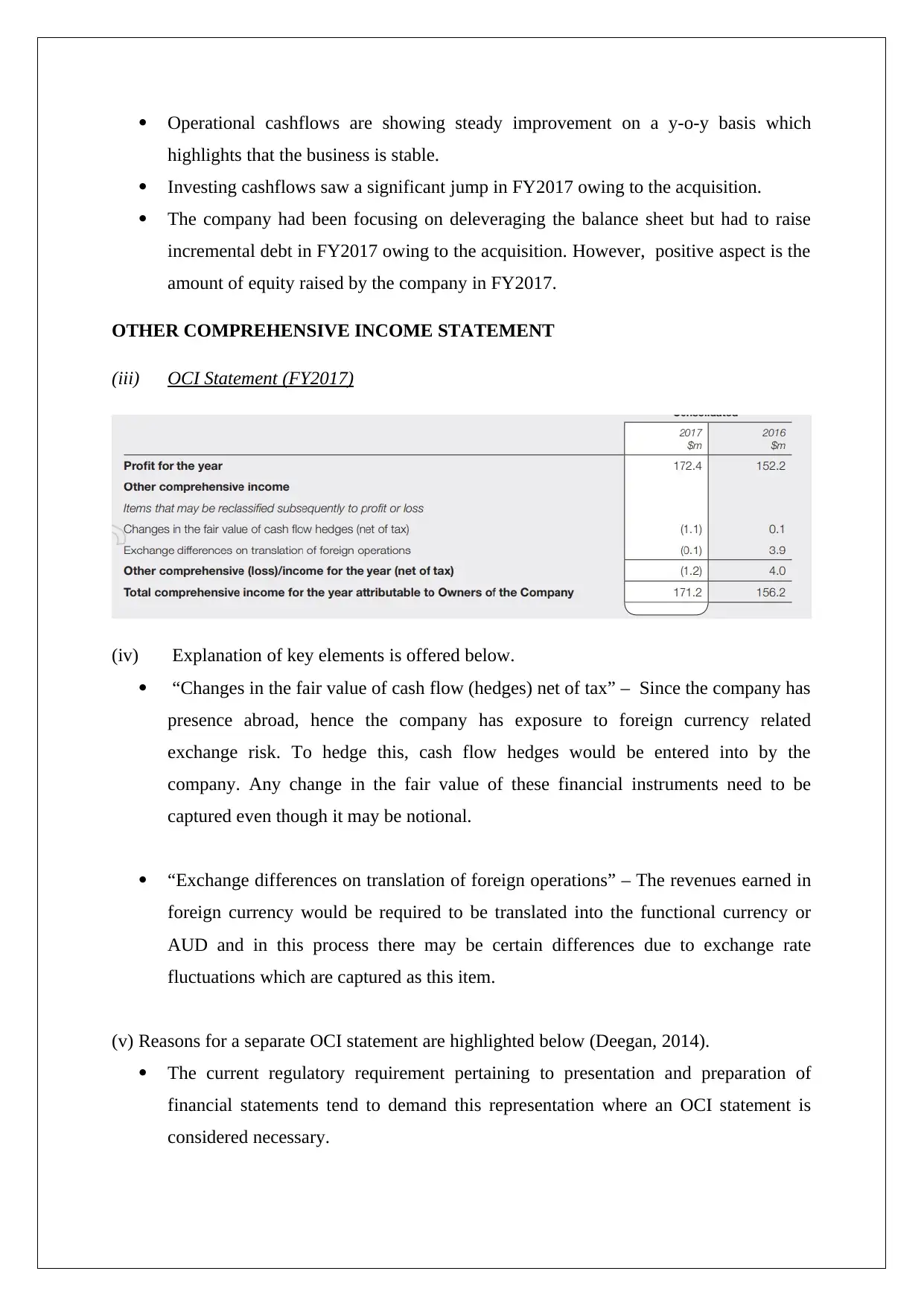

(iii) OCI Statement (FY2017)

(iv) Explanation of key elements is offered below.

“Changes in the fair value of cash flow (hedges) net of tax” – Since the company has

presence abroad, hence the company has exposure to foreign currency related

exchange risk. To hedge this, cash flow hedges would be entered into by the

company. Any change in the fair value of these financial instruments need to be

captured even though it may be notional.

“Exchange differences on translation of foreign operations” – The revenues earned in

foreign currency would be required to be translated into the functional currency or

AUD and in this process there may be certain differences due to exchange rate

fluctuations which are captured as this item.

(v) Reasons for a separate OCI statement are highlighted below (Deegan, 2014).

The current regulatory requirement pertaining to presentation and preparation of

financial statements tend to demand this representation where an OCI statement is

considered necessary.

highlights that the business is stable.

Investing cashflows saw a significant jump in FY2017 owing to the acquisition.

The company had been focusing on deleveraging the balance sheet but had to raise

incremental debt in FY2017 owing to the acquisition. However, positive aspect is the

amount of equity raised by the company in FY2017.

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) OCI Statement (FY2017)

(iv) Explanation of key elements is offered below.

“Changes in the fair value of cash flow (hedges) net of tax” – Since the company has

presence abroad, hence the company has exposure to foreign currency related

exchange risk. To hedge this, cash flow hedges would be entered into by the

company. Any change in the fair value of these financial instruments need to be

captured even though it may be notional.

“Exchange differences on translation of foreign operations” – The revenues earned in

foreign currency would be required to be translated into the functional currency or

AUD and in this process there may be certain differences due to exchange rate

fluctuations which are captured as this item.

(v) Reasons for a separate OCI statement are highlighted below (Deegan, 2014).

The current regulatory requirement pertaining to presentation and preparation of

financial statements tend to demand this representation where an OCI statement is

considered necessary.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There may be some items on financial instruments such as hedging related cash flow

whose value changes in real time and this gives rise to notional profits and losses

which may not be actually realised.

The items represented here are not meant for producing income but are rather

consequences of the normal business operations.

ACCOUNTING FOR CORPORATE INCOME TAX

(vi) The company has recorded a tax expense of $ 86.8 million for the latest year i.e.

FY2017 which is about 30% higher than the corresponding figure in FY2016 (JB Hi-Fi,

2017).

(vii) Expected tax expense = Pre-tax income * Corporate tax rate = 259.2 *(30/100) =

$77.8 million

It would be expected that the above would be the value of tax expense but the actual value

has been recorded higher at $ 86.8 million. The difference between the two is explained

with the help of the following schedule (JB Hi-Fi, 2017).

There are adjustments made to the theoretical tax expense which tend to arise on the basis

of reconciliation of accounting tax expense in order to determine the tax payable. The need

for reconciliation between the two arises on account of difference between the rules

prescribed be relevant tax statutes and accounting principles (Barkoczy, 2017).

whose value changes in real time and this gives rise to notional profits and losses

which may not be actually realised.

The items represented here are not meant for producing income but are rather

consequences of the normal business operations.

ACCOUNTING FOR CORPORATE INCOME TAX

(vi) The company has recorded a tax expense of $ 86.8 million for the latest year i.e.

FY2017 which is about 30% higher than the corresponding figure in FY2016 (JB Hi-Fi,

2017).

(vii) Expected tax expense = Pre-tax income * Corporate tax rate = 259.2 *(30/100) =

$77.8 million

It would be expected that the above would be the value of tax expense but the actual value

has been recorded higher at $ 86.8 million. The difference between the two is explained

with the help of the following schedule (JB Hi-Fi, 2017).

There are adjustments made to the theoretical tax expense which tend to arise on the basis

of reconciliation of accounting tax expense in order to determine the tax payable. The need

for reconciliation between the two arises on account of difference between the rules

prescribed be relevant tax statutes and accounting principles (Barkoczy, 2017).

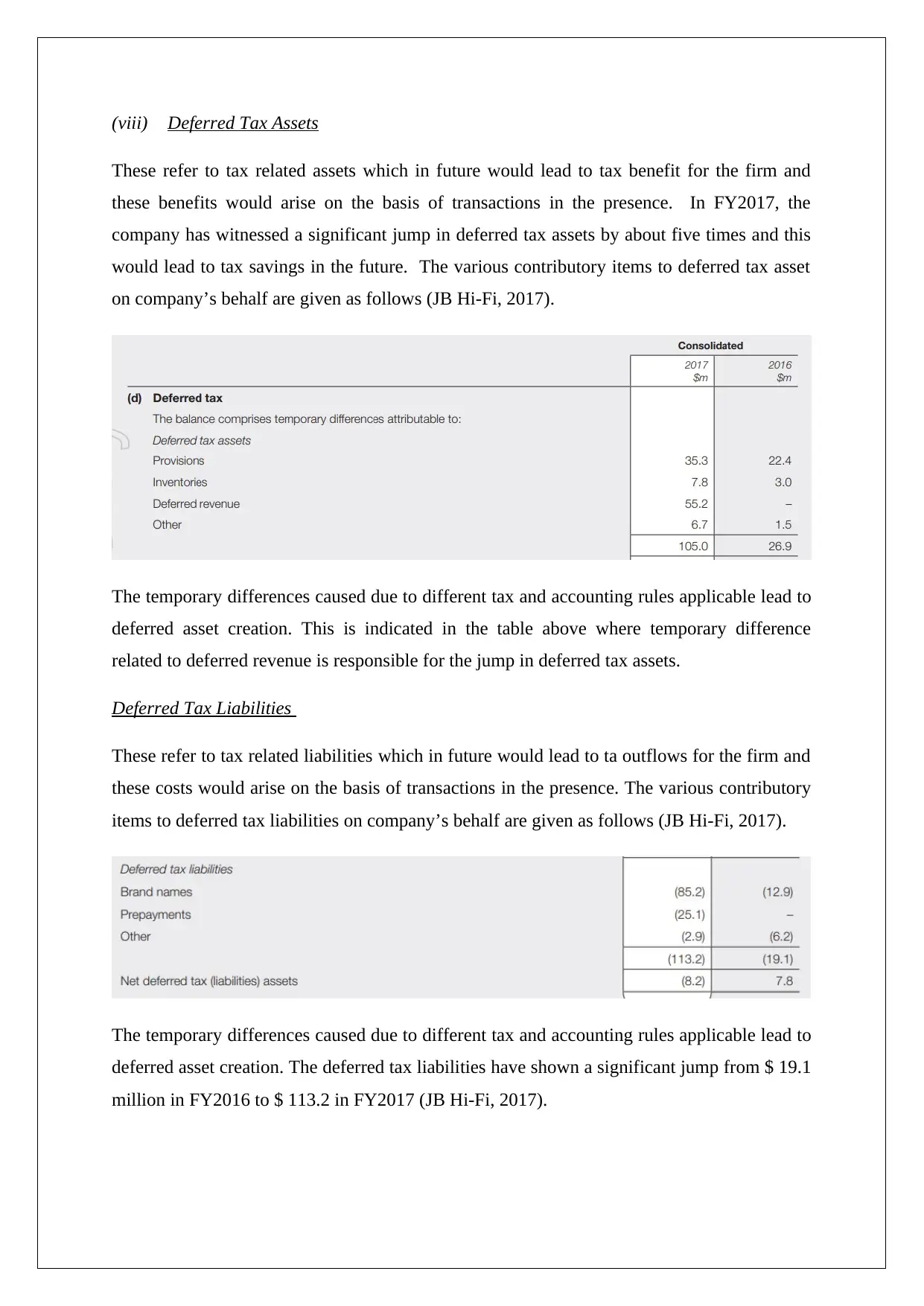

(viii) Deferred Tax Assets

These refer to tax related assets which in future would lead to tax benefit for the firm and

these benefits would arise on the basis of transactions in the presence. In FY2017, the

company has witnessed a significant jump in deferred tax assets by about five times and this

would lead to tax savings in the future. The various contributory items to deferred tax asset

on company’s behalf are given as follows (JB Hi-Fi, 2017).

The temporary differences caused due to different tax and accounting rules applicable lead to

deferred asset creation. This is indicated in the table above where temporary difference

related to deferred revenue is responsible for the jump in deferred tax assets.

Deferred Tax Liabilities

These refer to tax related liabilities which in future would lead to ta outflows for the firm and

these costs would arise on the basis of transactions in the presence. The various contributory

items to deferred tax liabilities on company’s behalf are given as follows (JB Hi-Fi, 2017).

The temporary differences caused due to different tax and accounting rules applicable lead to

deferred asset creation. The deferred tax liabilities have shown a significant jump from $ 19.1

million in FY2016 to $ 113.2 in FY2017 (JB Hi-Fi, 2017).

These refer to tax related assets which in future would lead to tax benefit for the firm and

these benefits would arise on the basis of transactions in the presence. In FY2017, the

company has witnessed a significant jump in deferred tax assets by about five times and this

would lead to tax savings in the future. The various contributory items to deferred tax asset

on company’s behalf are given as follows (JB Hi-Fi, 2017).

The temporary differences caused due to different tax and accounting rules applicable lead to

deferred asset creation. This is indicated in the table above where temporary difference

related to deferred revenue is responsible for the jump in deferred tax assets.

Deferred Tax Liabilities

These refer to tax related liabilities which in future would lead to ta outflows for the firm and

these costs would arise on the basis of transactions in the presence. The various contributory

items to deferred tax liabilities on company’s behalf are given as follows (JB Hi-Fi, 2017).

The temporary differences caused due to different tax and accounting rules applicable lead to

deferred asset creation. The deferred tax liabilities have shown a significant jump from $ 19.1

million in FY2016 to $ 113.2 in FY2017 (JB Hi-Fi, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(ix) In accordance with the balance sheet of the company for FY2017, the current tax

liabilities stand at $ 11.8 million. In comparison to the corresponding current tax

liabilities for FY2016 were marginally lower at $ 10.9 million. The tax outflow on

account of these would occur during the 12 months of the next financial year in which

they are recorded.

The income tax expense and income tax payable do not show convergence. The

concept of income tax expense captures the tax amount that the company would be

expected to pay for the financial year under consideration. But, only after the financial

year is over is the tax expense amount can be computed. However, on an ongoing basis,

the company keeps on paying some tax to the relevant tax authorities. Thus, based on

the amount of money which has actually been paid, the tax payable may be positive or

negative. A positive tax payable leads to creation of current tax liability. However, a

negative tax payable leads to creation of current tax asset (Petty et. al., 2015)

(x) There is no convergence between the figures corresponding to income tax expense and

the tax paid. This is because the tax expense computation is completed after the closing

of the financial year. As a result, since the tax expense is not known during the given

year with certainty, hence tax paid is driven by estimates which would tend to deviate

positively or negatively. As a result, tax paid for a given year may be more or less than

the tax expense. Further, the tax paid in a given year may have some share of the

pending tax payable for the previous year which puts off the tax paid from the tax

expense (Gilders et. al., 2016).

(xi) With regards to the tax treatment, without doubt the most confusing aspect related to

the temporary differences in carrying value of various items which then brought into

picture the deferred tax assets/liabilities which had potential future implications and it

is this intermingling which complicated the whole computations. A key insight related

to the tax expense recorded in the income statement and the underlying computation

particularly related to the reconciliation of accounting income to arrive at the taxable

income and tax payable.

liabilities stand at $ 11.8 million. In comparison to the corresponding current tax

liabilities for FY2016 were marginally lower at $ 10.9 million. The tax outflow on

account of these would occur during the 12 months of the next financial year in which

they are recorded.

The income tax expense and income tax payable do not show convergence. The

concept of income tax expense captures the tax amount that the company would be

expected to pay for the financial year under consideration. But, only after the financial

year is over is the tax expense amount can be computed. However, on an ongoing basis,

the company keeps on paying some tax to the relevant tax authorities. Thus, based on

the amount of money which has actually been paid, the tax payable may be positive or

negative. A positive tax payable leads to creation of current tax liability. However, a

negative tax payable leads to creation of current tax asset (Petty et. al., 2015)

(x) There is no convergence between the figures corresponding to income tax expense and

the tax paid. This is because the tax expense computation is completed after the closing

of the financial year. As a result, since the tax expense is not known during the given

year with certainty, hence tax paid is driven by estimates which would tend to deviate

positively or negatively. As a result, tax paid for a given year may be more or less than

the tax expense. Further, the tax paid in a given year may have some share of the

pending tax payable for the previous year which puts off the tax paid from the tax

expense (Gilders et. al., 2016).

(xi) With regards to the tax treatment, without doubt the most confusing aspect related to

the temporary differences in carrying value of various items which then brought into

picture the deferred tax assets/liabilities which had potential future implications and it

is this intermingling which complicated the whole computations. A key insight related

to the tax expense recorded in the income statement and the underlying computation

particularly related to the reconciliation of accounting income to arrive at the taxable

income and tax payable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University

Press.

Deegan, C. (2014). Financial Accounting Theory, 4th ed. Sydney: McGraw-Hill

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016, 9th ed. Sydney: LexisNexis/Butterworths.

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th ed. NSW: Pearson Education, French

Forest Australia.

JB HI-FI (2017) Annual Report 2017 [online] Available at

https://www.jbhifi.com.au/Documents/2017%20Annual%20Report.pdf (Accessed on May 25,

2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University

Press.

Deegan, C. (2014). Financial Accounting Theory, 4th ed. Sydney: McGraw-Hill

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016, 9th ed. Sydney: LexisNexis/Butterworths.

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th ed. NSW: Pearson Education, French

Forest Australia.

JB HI-FI (2017) Annual Report 2017 [online] Available at

https://www.jbhifi.com.au/Documents/2017%20Annual%20Report.pdf (Accessed on May 25,

2018)

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.