HI5020 Corporate Accounting: JB HI-FI Financial Statement Analysis

VerifiedAdded on 2023/06/12

|9

|2298

|253

Report

AI Summary

This report provides a comprehensive analysis of JB HI-FI's financial statements, focusing on the cash flow statement, other comprehensive income (OCI) statement, and accounting for corporate income tax. It examines the operational, investing, and financing cash flows, explaining key items such as receipts from customers, payments to suppliers and employees, and proceeds from share issues. The analysis also covers the elements of the OCI statement, including changes in the fair value of cash flow hedges and exchange differences on translation of foreign operations. Furthermore, the report delves into the company's tax expenses, deferred tax assets, and deferred tax liabilities, highlighting the differences between accounting and tax treatments. The report references the 2017 annual report of JB HI-FI and various corporate finance principles.

CORPORATE ACCOUNTING

[Type the document subtitle]

STUDENT ID:

[Pick the date]

[Type the document subtitle]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The selected firm is a consumer goods retailor named JB HI-FI. The company’s 2017 annual

report is the latest and hence the financial statements used for this task would correspond to

June 30, 2017 position. The key analysis of the requisite items is carried out below.

CASH FLOWS STATEMENT

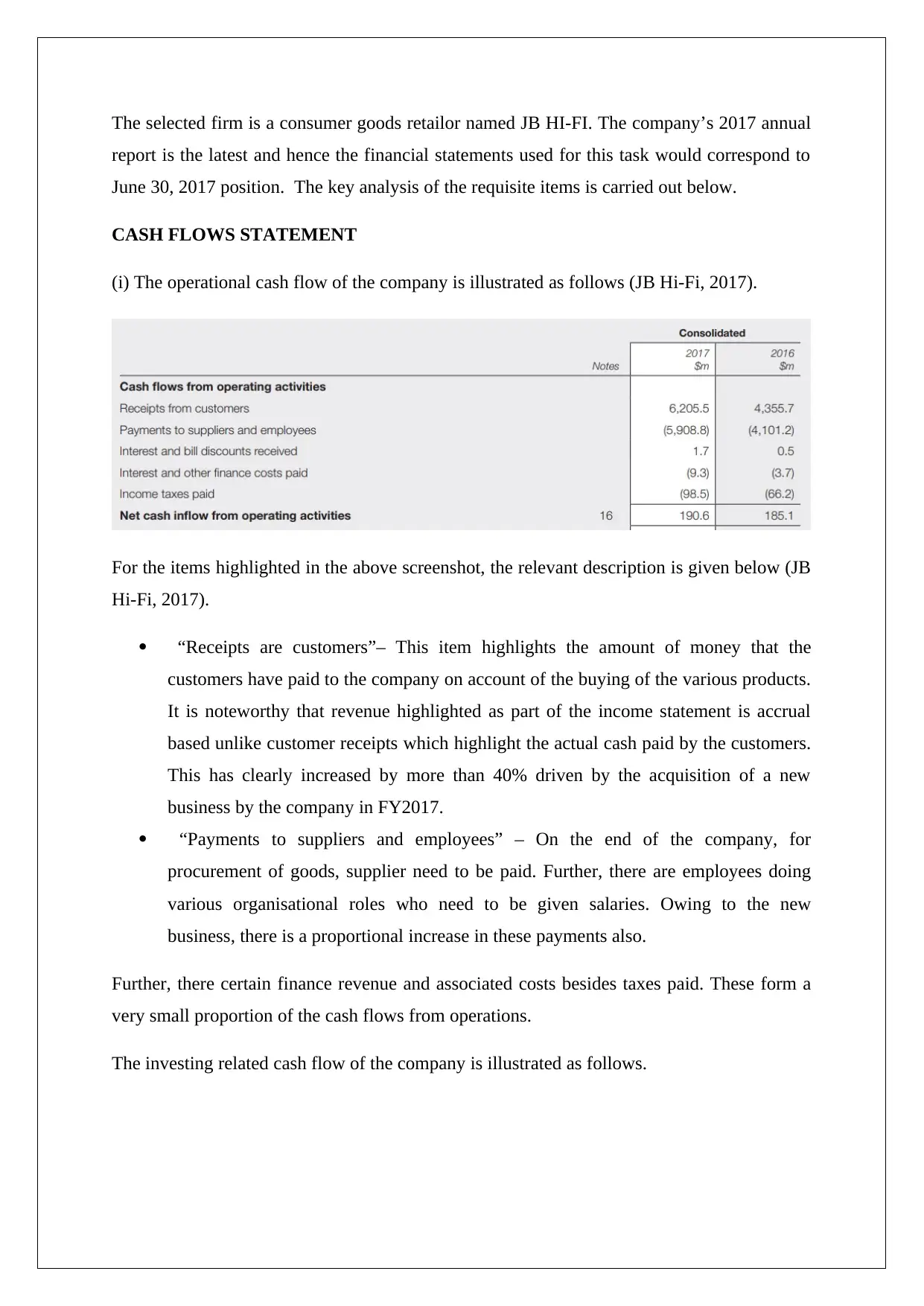

(i) The operational cash flow of the company is illustrated as follows (JB Hi-Fi, 2017).

For the items highlighted in the above screenshot, the relevant description is given below (JB

Hi-Fi, 2017).

“Receipts are customers”– This item highlights the amount of money that the

customers have paid to the company on account of the buying of the various products.

It is noteworthy that revenue highlighted as part of the income statement is accrual

based unlike customer receipts which highlight the actual cash paid by the customers.

This has clearly increased by more than 40% driven by the acquisition of a new

business by the company in FY2017.

“Payments to suppliers and employees” – On the end of the company, for

procurement of goods, supplier need to be paid. Further, there are employees doing

various organisational roles who need to be given salaries. Owing to the new

business, there is a proportional increase in these payments also.

Further, there certain finance revenue and associated costs besides taxes paid. These form a

very small proportion of the cash flows from operations.

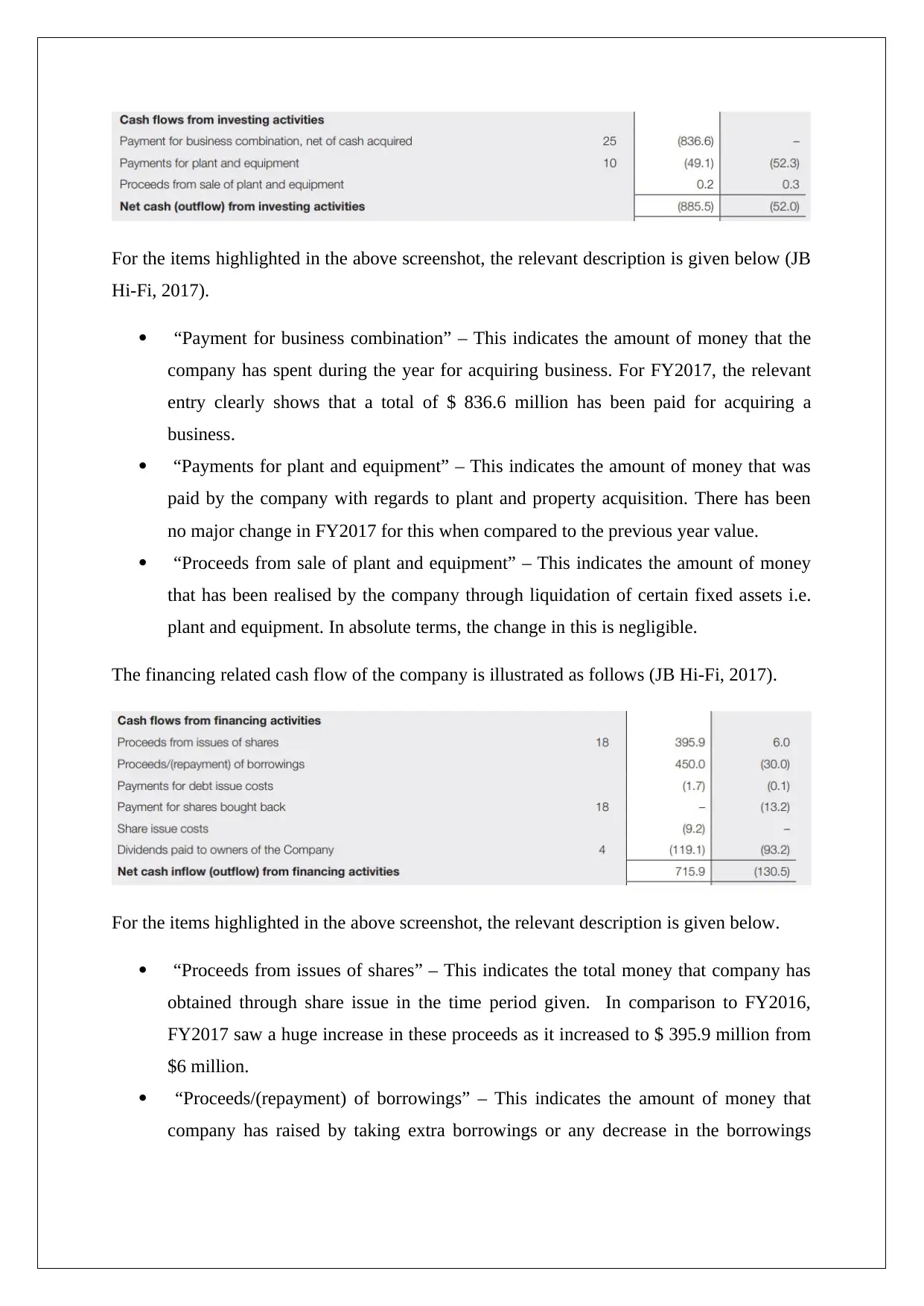

The investing related cash flow of the company is illustrated as follows.

report is the latest and hence the financial statements used for this task would correspond to

June 30, 2017 position. The key analysis of the requisite items is carried out below.

CASH FLOWS STATEMENT

(i) The operational cash flow of the company is illustrated as follows (JB Hi-Fi, 2017).

For the items highlighted in the above screenshot, the relevant description is given below (JB

Hi-Fi, 2017).

“Receipts are customers”– This item highlights the amount of money that the

customers have paid to the company on account of the buying of the various products.

It is noteworthy that revenue highlighted as part of the income statement is accrual

based unlike customer receipts which highlight the actual cash paid by the customers.

This has clearly increased by more than 40% driven by the acquisition of a new

business by the company in FY2017.

“Payments to suppliers and employees” – On the end of the company, for

procurement of goods, supplier need to be paid. Further, there are employees doing

various organisational roles who need to be given salaries. Owing to the new

business, there is a proportional increase in these payments also.

Further, there certain finance revenue and associated costs besides taxes paid. These form a

very small proportion of the cash flows from operations.

The investing related cash flow of the company is illustrated as follows.

For the items highlighted in the above screenshot, the relevant description is given below (JB

Hi-Fi, 2017).

“Payment for business combination” – This indicates the amount of money that the

company has spent during the year for acquiring business. For FY2017, the relevant

entry clearly shows that a total of $ 836.6 million has been paid for acquiring a

business.

“Payments for plant and equipment” – This indicates the amount of money that was

paid by the company with regards to plant and property acquisition. There has been

no major change in FY2017 for this when compared to the previous year value.

“Proceeds from sale of plant and equipment” – This indicates the amount of money

that has been realised by the company through liquidation of certain fixed assets i.e.

plant and equipment. In absolute terms, the change in this is negligible.

The financing related cash flow of the company is illustrated as follows (JB Hi-Fi, 2017).

For the items highlighted in the above screenshot, the relevant description is given below.

“Proceeds from issues of shares” – This indicates the total money that company has

obtained through share issue in the time period given. In comparison to FY2016,

FY2017 saw a huge increase in these proceeds as it increased to $ 395.9 million from

$6 million.

“Proceeds/(repayment) of borrowings” – This indicates the amount of money that

company has raised by taking extra borrowings or any decrease in the borrowings

Hi-Fi, 2017).

“Payment for business combination” – This indicates the amount of money that the

company has spent during the year for acquiring business. For FY2017, the relevant

entry clearly shows that a total of $ 836.6 million has been paid for acquiring a

business.

“Payments for plant and equipment” – This indicates the amount of money that was

paid by the company with regards to plant and property acquisition. There has been

no major change in FY2017 for this when compared to the previous year value.

“Proceeds from sale of plant and equipment” – This indicates the amount of money

that has been realised by the company through liquidation of certain fixed assets i.e.

plant and equipment. In absolute terms, the change in this is negligible.

The financing related cash flow of the company is illustrated as follows (JB Hi-Fi, 2017).

For the items highlighted in the above screenshot, the relevant description is given below.

“Proceeds from issues of shares” – This indicates the total money that company has

obtained through share issue in the time period given. In comparison to FY2016,

FY2017 saw a huge increase in these proceeds as it increased to $ 395.9 million from

$6 million.

“Proceeds/(repayment) of borrowings” – This indicates the amount of money that

company has raised by taking extra borrowings or any decrease in the borrowings

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

level through repayment. There is an increase in borrowings by $ 450 million that has

occurred in FY2017.

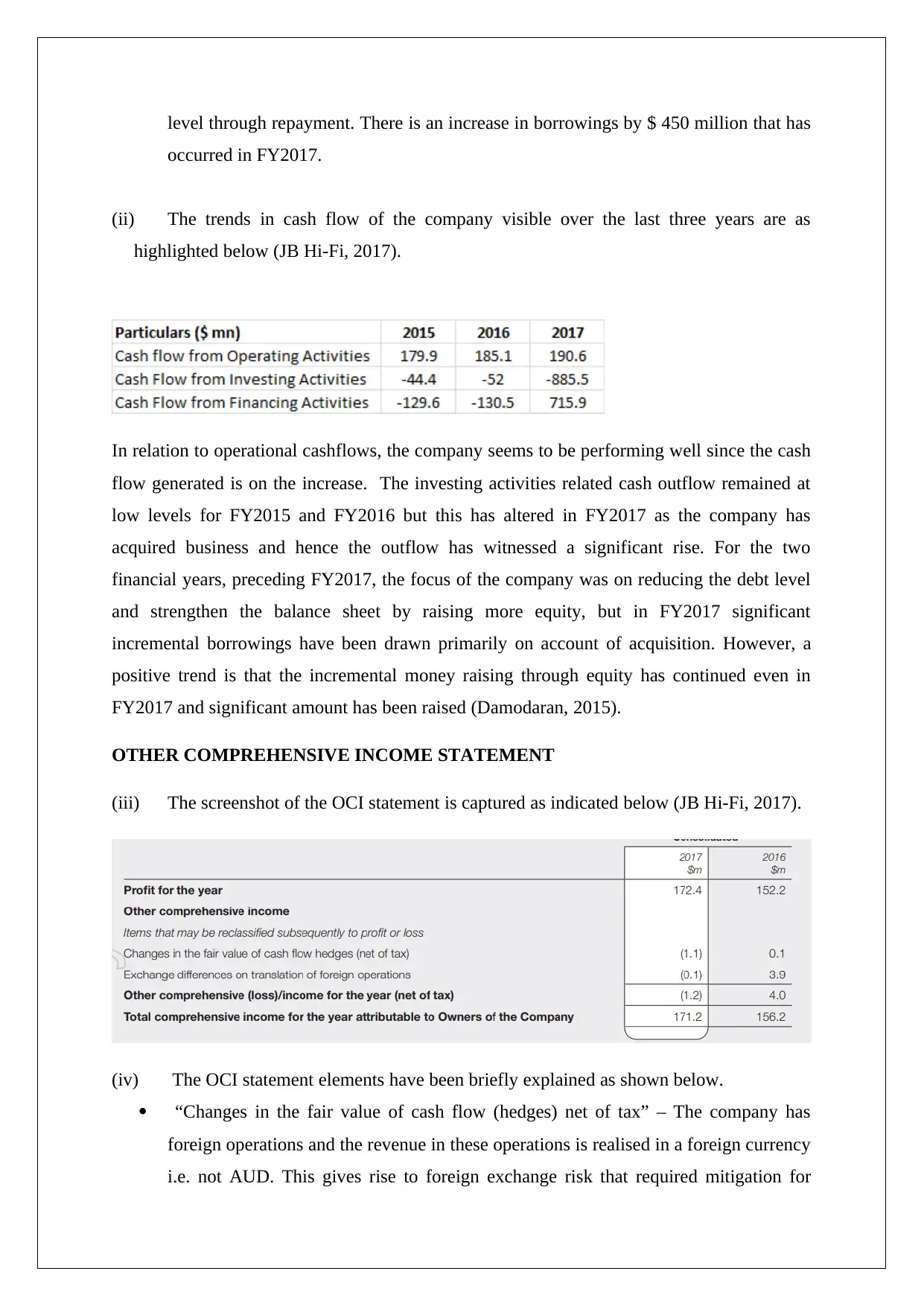

(ii) The trends in cash flow of the company visible over the last three years are as

highlighted below (JB Hi-Fi, 2017).

In relation to operational cashflows, the company seems to be performing well since the cash

flow generated is on the increase. The investing activities related cash outflow remained at

low levels for FY2015 and FY2016 but this has altered in FY2017 as the company has

acquired business and hence the outflow has witnessed a significant rise. For the two

financial years, preceding FY2017, the focus of the company was on reducing the debt level

and strengthen the balance sheet by raising more equity, but in FY2017 significant

incremental borrowings have been drawn primarily on account of acquisition. However, a

positive trend is that the incremental money raising through equity has continued even in

FY2017 and significant amount has been raised (Damodaran, 2015).

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) The screenshot of the OCI statement is captured as indicated below (JB Hi-Fi, 2017).

(iv) The OCI statement elements have been briefly explained as shown below.

“Changes in the fair value of cash flow (hedges) net of tax” – The company has

foreign operations and the revenue in these operations is realised in a foreign currency

i.e. not AUD. This gives rise to foreign exchange risk that required mitigation for

occurred in FY2017.

(ii) The trends in cash flow of the company visible over the last three years are as

highlighted below (JB Hi-Fi, 2017).

In relation to operational cashflows, the company seems to be performing well since the cash

flow generated is on the increase. The investing activities related cash outflow remained at

low levels for FY2015 and FY2016 but this has altered in FY2017 as the company has

acquired business and hence the outflow has witnessed a significant rise. For the two

financial years, preceding FY2017, the focus of the company was on reducing the debt level

and strengthen the balance sheet by raising more equity, but in FY2017 significant

incremental borrowings have been drawn primarily on account of acquisition. However, a

positive trend is that the incremental money raising through equity has continued even in

FY2017 and significant amount has been raised (Damodaran, 2015).

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) The screenshot of the OCI statement is captured as indicated below (JB Hi-Fi, 2017).

(iv) The OCI statement elements have been briefly explained as shown below.

“Changes in the fair value of cash flow (hedges) net of tax” – The company has

foreign operations and the revenue in these operations is realised in a foreign currency

i.e. not AUD. This gives rise to foreign exchange risk that required mitigation for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which cash flow hedges have been procured by the company. These refer to financial

instruments whose underlying value is determined based on the rate of foreign

exchange. Since the exchange rate tends to fluctuate in real time, hence the value of

cash flow hedge also alters. It is therefore required that any notional gain/(loss)

derived should be captured in the financial statements for which the value of these

instruments at the opening day of the financial year and closing day of the financial

year is compared (Arnold, 2015).

“Exchange differences on translation of foreign operations” – Considering the fact

that the company has foreign operations, the foreign currency would have to be

translated into AUD which acts as the functional currency. This translation process

may lead to possible gains or losses owing to the translation not proceeding at the

same moment when foreign currency revenue is obtained (Petty et. al., 2015).

(v) The key reasons why the items enlisted are listed as part of the separate OCI statement are

listed as follows (Brealey, Myers and Allen, 2014).

It is requirement as per the existing accounting regulations along with presentation of

financial statements guidelines offered by bodies such as IASB.

For certain items such as cash hedge, the loss or gain booked may be notional only

and not realised. It is possible that over the next year this notional gain or loss is

erased owing to opposite movement.

These items are usually not intended towards earning income even though they serve

an important function. Also, listing of certain items as part of the OCI statement does

not imply that they lack importance.

ACCOUNTING FOR CORPORATE INCOME TAX

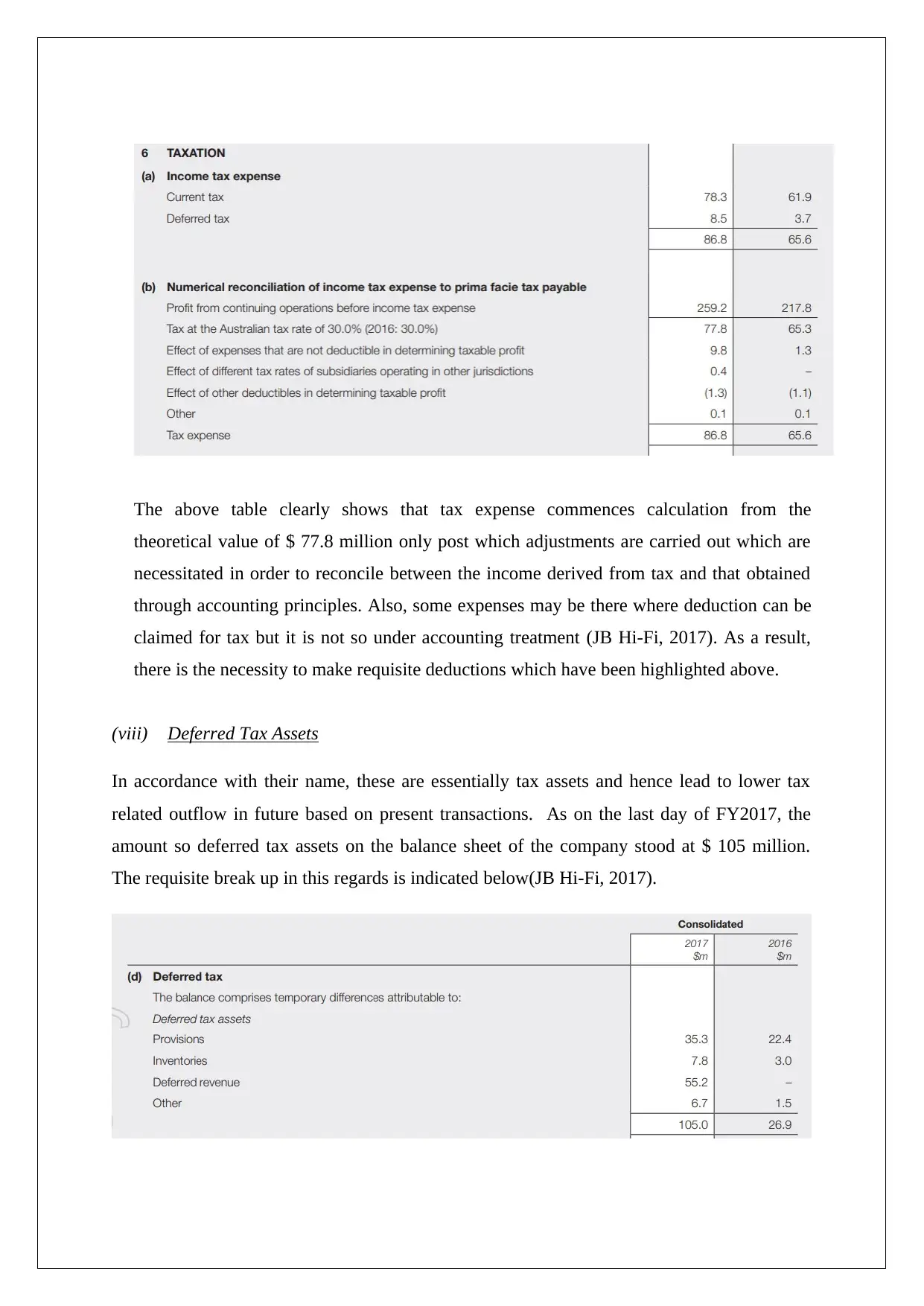

(vi) The tax expense for JB Hi Fi for FY2017 is $ 86.8 million which is highlighted in the

income statement. Also, compared to the previous year i.e. FY2016, the tax expense has

seen a jump of around 30% (JB Hi-Fi, 2017).

(vii) For JB Hi Fi, the pre-tax accounting income for FY2017 has come out as $ 259.2

million. Besides, a 30% corporate tax rate is prevalent. Hence, the expected tax expense

would be (30/100)*259.2 or $ 77.8 million. It can be seen from the income statement that

the actual tax expense is much higher at about $ 86.8 million. The income tax related

schedule can help in understanding the differences (JB Hi-Fi, 2017).

instruments whose underlying value is determined based on the rate of foreign

exchange. Since the exchange rate tends to fluctuate in real time, hence the value of

cash flow hedge also alters. It is therefore required that any notional gain/(loss)

derived should be captured in the financial statements for which the value of these

instruments at the opening day of the financial year and closing day of the financial

year is compared (Arnold, 2015).

“Exchange differences on translation of foreign operations” – Considering the fact

that the company has foreign operations, the foreign currency would have to be

translated into AUD which acts as the functional currency. This translation process

may lead to possible gains or losses owing to the translation not proceeding at the

same moment when foreign currency revenue is obtained (Petty et. al., 2015).

(v) The key reasons why the items enlisted are listed as part of the separate OCI statement are

listed as follows (Brealey, Myers and Allen, 2014).

It is requirement as per the existing accounting regulations along with presentation of

financial statements guidelines offered by bodies such as IASB.

For certain items such as cash hedge, the loss or gain booked may be notional only

and not realised. It is possible that over the next year this notional gain or loss is

erased owing to opposite movement.

These items are usually not intended towards earning income even though they serve

an important function. Also, listing of certain items as part of the OCI statement does

not imply that they lack importance.

ACCOUNTING FOR CORPORATE INCOME TAX

(vi) The tax expense for JB Hi Fi for FY2017 is $ 86.8 million which is highlighted in the

income statement. Also, compared to the previous year i.e. FY2016, the tax expense has

seen a jump of around 30% (JB Hi-Fi, 2017).

(vii) For JB Hi Fi, the pre-tax accounting income for FY2017 has come out as $ 259.2

million. Besides, a 30% corporate tax rate is prevalent. Hence, the expected tax expense

would be (30/100)*259.2 or $ 77.8 million. It can be seen from the income statement that

the actual tax expense is much higher at about $ 86.8 million. The income tax related

schedule can help in understanding the differences (JB Hi-Fi, 2017).

The above table clearly shows that tax expense commences calculation from the

theoretical value of $ 77.8 million only post which adjustments are carried out which are

necessitated in order to reconcile between the income derived from tax and that obtained

through accounting principles. Also, some expenses may be there where deduction can be

claimed for tax but it is not so under accounting treatment (JB Hi-Fi, 2017). As a result,

there is the necessity to make requisite deductions which have been highlighted above.

(viii) Deferred Tax Assets

In accordance with their name, these are essentially tax assets and hence lead to lower tax

related outflow in future based on present transactions. As on the last day of FY2017, the

amount so deferred tax assets on the balance sheet of the company stood at $ 105 million.

The requisite break up in this regards is indicated below(JB Hi-Fi, 2017).

theoretical value of $ 77.8 million only post which adjustments are carried out which are

necessitated in order to reconcile between the income derived from tax and that obtained

through accounting principles. Also, some expenses may be there where deduction can be

claimed for tax but it is not so under accounting treatment (JB Hi-Fi, 2017). As a result,

there is the necessity to make requisite deductions which have been highlighted above.

(viii) Deferred Tax Assets

In accordance with their name, these are essentially tax assets and hence lead to lower tax

related outflow in future based on present transactions. As on the last day of FY2017, the

amount so deferred tax assets on the balance sheet of the company stood at $ 105 million.

The requisite break up in this regards is indicated below(JB Hi-Fi, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The origin or creation of these assets is attributed to the carrying value related temporary

differences that tend to arise due to differential treatment of tax and accounting rules. For the

year ending on June 30, 2017, the deferred tax assets have shown a significant rise which is

related to deferred revenue based temporary revenue which in the future would result in

lower tax outflow by the company to the tune of $ 55.2 million.

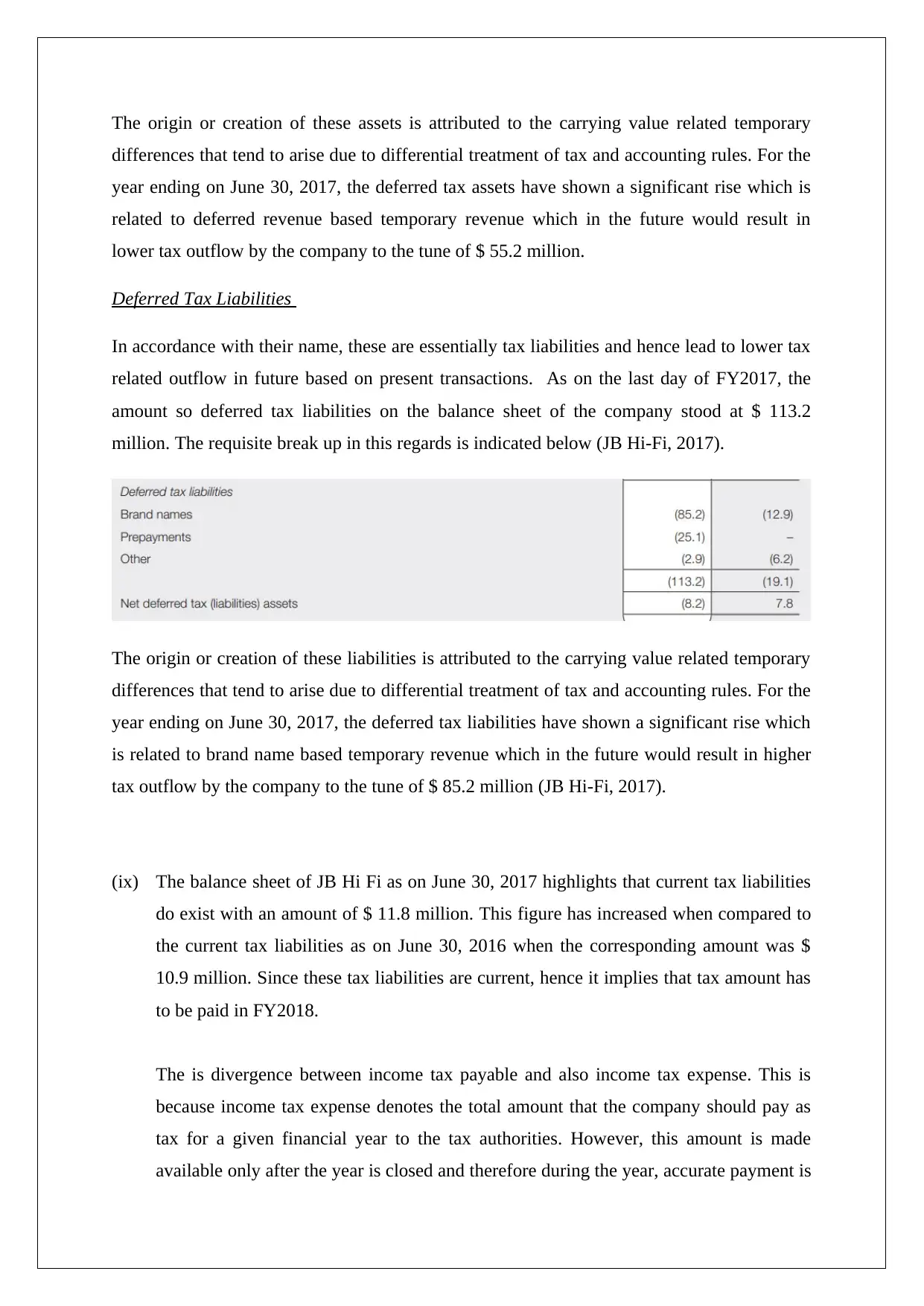

Deferred Tax Liabilities

In accordance with their name, these are essentially tax liabilities and hence lead to lower tax

related outflow in future based on present transactions. As on the last day of FY2017, the

amount so deferred tax liabilities on the balance sheet of the company stood at $ 113.2

million. The requisite break up in this regards is indicated below (JB Hi-Fi, 2017).

The origin or creation of these liabilities is attributed to the carrying value related temporary

differences that tend to arise due to differential treatment of tax and accounting rules. For the

year ending on June 30, 2017, the deferred tax liabilities have shown a significant rise which

is related to brand name based temporary revenue which in the future would result in higher

tax outflow by the company to the tune of $ 85.2 million (JB Hi-Fi, 2017).

(ix) The balance sheet of JB Hi Fi as on June 30, 2017 highlights that current tax liabilities

do exist with an amount of $ 11.8 million. This figure has increased when compared to

the current tax liabilities as on June 30, 2016 when the corresponding amount was $

10.9 million. Since these tax liabilities are current, hence it implies that tax amount has

to be paid in FY2018.

The is divergence between income tax payable and also income tax expense. This is

because income tax expense denotes the total amount that the company should pay as

tax for a given financial year to the tax authorities. However, this amount is made

available only after the year is closed and therefore during the year, accurate payment is

differences that tend to arise due to differential treatment of tax and accounting rules. For the

year ending on June 30, 2017, the deferred tax assets have shown a significant rise which is

related to deferred revenue based temporary revenue which in the future would result in

lower tax outflow by the company to the tune of $ 55.2 million.

Deferred Tax Liabilities

In accordance with their name, these are essentially tax liabilities and hence lead to lower tax

related outflow in future based on present transactions. As on the last day of FY2017, the

amount so deferred tax liabilities on the balance sheet of the company stood at $ 113.2

million. The requisite break up in this regards is indicated below (JB Hi-Fi, 2017).

The origin or creation of these liabilities is attributed to the carrying value related temporary

differences that tend to arise due to differential treatment of tax and accounting rules. For the

year ending on June 30, 2017, the deferred tax liabilities have shown a significant rise which

is related to brand name based temporary revenue which in the future would result in higher

tax outflow by the company to the tune of $ 85.2 million (JB Hi-Fi, 2017).

(ix) The balance sheet of JB Hi Fi as on June 30, 2017 highlights that current tax liabilities

do exist with an amount of $ 11.8 million. This figure has increased when compared to

the current tax liabilities as on June 30, 2016 when the corresponding amount was $

10.9 million. Since these tax liabilities are current, hence it implies that tax amount has

to be paid in FY2018.

The is divergence between income tax payable and also income tax expense. This is

because income tax expense denotes the total amount that the company should pay as

tax for a given financial year to the tax authorities. However, this amount is made

available only after the year is closed and therefore during the year, accurate payment is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not possible and hence only approximate money is paid as tax. As a result, there is

some pending amount of tax payable in a given year identified as current tax liabilities

which is paid the next year. Further, the amount of tax paid in a year comprises of the

outstanding tax liability of the previous year along with tax for the current year based

on estimates of profits (Parrino and Kidwell, 2014).

(x) It is evident by comparing the two figures that income tax expense and income tax paid

in the latest financial statement does not match. The difference in the amounts arises

because it is quite possible that a portion of the tax outstanding for FY2016 would be

reported as current tax liability. In FY2017, the current liability for the previous year

would be paid besides the tax for the current year which would be based on estimates.

This way a part of the tax is usually paid in the next financial year (Damodaran, 2015).

(xi) In context of tax treatment, the most interesting aspect would be the treatment of

deferred tax assets/liabilities which at times was quite complex. This however enabled

higher clarity in tax related concepts as the various concepts covered in class were

being applied here. In relation to the tax expense, the aspect that gained by attention as

the reconciliation and the related adjustment which ought to be made so as to ensure

that tax expense is as per the tax norms applicable for the company.

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Brealey, R. A., Myers, S. C., & Allen, F. (2014) Principles of corporate finance, 2nd ed. New

York: McGraw-Hill Inc.

some pending amount of tax payable in a given year identified as current tax liabilities

which is paid the next year. Further, the amount of tax paid in a year comprises of the

outstanding tax liability of the previous year along with tax for the current year based

on estimates of profits (Parrino and Kidwell, 2014).

(x) It is evident by comparing the two figures that income tax expense and income tax paid

in the latest financial statement does not match. The difference in the amounts arises

because it is quite possible that a portion of the tax outstanding for FY2016 would be

reported as current tax liability. In FY2017, the current liability for the previous year

would be paid besides the tax for the current year which would be based on estimates.

This way a part of the tax is usually paid in the next financial year (Damodaran, 2015).

(xi) In context of tax treatment, the most interesting aspect would be the treatment of

deferred tax assets/liabilities which at times was quite complex. This however enabled

higher clarity in tax related concepts as the various concepts covered in class were

being applied here. In relation to the tax expense, the aspect that gained by attention as

the reconciliation and the related adjustment which ought to be made so as to ensure

that tax expense is as per the tax norms applicable for the company.

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Brealey, R. A., Myers, S. C., & Allen, F. (2014) Principles of corporate finance, 2nd ed. New

York: McGraw-Hill Inc.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

JB HI-FI (2017) Annual Report 2017. Retrieved from

https://www.jbhifi.com.au/Documents/2017%20Annual%20Report.pdf

Parrino, R. and Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publications

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., & Nguyen, H. (2015).

Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education,

French Forest Australia.

Wiley, John & Sons.

JB HI-FI (2017) Annual Report 2017. Retrieved from

https://www.jbhifi.com.au/Documents/2017%20Annual%20Report.pdf

Parrino, R. and Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publications

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., & Nguyen, H. (2015).

Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education,

French Forest Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.