Using Classical Political Economy Theory and Managerial Branch of Stakeholder Theory to Explain JB Hi-Fi's Reporting Decisions

VerifiedAdded on 2023/06/11

|16

|6087

|63

AI Summary

This article discusses how JB Hi-Fi's reporting decisions can be explained using Classical Political Economy Theory and Managerial Branch of Stakeholder Theory. It also explores the extent to which current share prices anticipate future earnings announcements. The article provides evidence from the case study to support the observations made.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCT20074 Final Assignment

Term 1, 2018

Student ID:………………………………. Student name……………………………………………………..

Marker’s overall comments: The markers may include any

final comments here.

Overall Mark (Total) out of 50:

0

Term 1, 2018

Student ID:………………………………. Student name……………………………………………………..

Marker’s overall comments: The markers may include any

final comments here.

Overall Mark (Total) out of 50:

0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1: Use Classical Political Economy Theory to explain JB Hi-Fi’s decision to release its profit downgrade

in the way it did. Make sure you explain what Institutional Theory is, and support your observations with evidence

from the case study.

Answer: The classical theory of Economics is mainly the overall Foundation that was laid for the modern economics, which was

essential to promote growth, free trade and competition without the interference of government regulations. classical theory of

Economics directly indicated the use of self-regulating methods which could effectively allow the economy to improve without the

intervention of the government. classical economist mainly evaluated the growth of a country with GDP output level and not by the

detecting the wealth of the king or government. This will help in laying the foundation for modern economics, while promoting trades

conducted without government intervention. The classical theory of Economics can be evaluated on the decision made by JB hi fi in

disclosing the downgrade in their profits during the fiscal year. From the evaluation point of you the decision made by JB Hi-Fi was

directly considered as an independent move where the organisation effectively complied with all the relevant regulations laid down

before conducting the announcement. Hence, the intervention of ASX was not needed as the overall profit downgrade was relatively

under the material disclosure limit. Therefore, it could be understood that under the measures of classical theory of Economics

organisation adequately portrayed free competition without the intervention of government regulations. Therefore, under the classical

political economy theory the decision made by JB Hi-Fi regarding the disclosure of the profit downgrade was adequate. the company

is able to disclose all the relevant information regarding their operations regardless of the intervention from governments, as it

complied with all the relevant regulations laid down by ASX. In this context, Onions & Schefold (2017) stated that with adequate

disclosure measure the organisation is able to minimise any kind of rumours that might hamper its share price and have impact on their

capital reserves.

The institutional theory directly indicates that organisation needs to follow the regulations structures and establishment that is

portrayed by regulator for depicting their social behaviour. the social behaviour of the organisation is essential as it delivers all the

relevant information to the stakeholders in accordance to the changes in its operations. according to the institutional theory company

has effectively portrayed all the relevant information to the ASX and investors where is no manipulation is being conducted by the

company. JB hi fi has relatively portrait the information in an adequate way, where no additional information was required as the

material impact was below 3%, as stated in the ASX regulations. Major compliance with all the relevant information directly indicates

the usefulness of institutional theory in detecting the major problems faced by the company. hence, it could be identified that under the

institutional theory measure JB hi fi has adequately complied with all the regulations laid down by ASX regarding the disclosure

measure of their profit downgrade (Willmott, 2018). Before after evaluating all the relevant evidence from the case study it will be

identified that JB hi fi has effectively followed all the relevant regulations before conducting the announcement. This relevantly

in the way it did. Make sure you explain what Institutional Theory is, and support your observations with evidence

from the case study.

Answer: The classical theory of Economics is mainly the overall Foundation that was laid for the modern economics, which was

essential to promote growth, free trade and competition without the interference of government regulations. classical theory of

Economics directly indicated the use of self-regulating methods which could effectively allow the economy to improve without the

intervention of the government. classical economist mainly evaluated the growth of a country with GDP output level and not by the

detecting the wealth of the king or government. This will help in laying the foundation for modern economics, while promoting trades

conducted without government intervention. The classical theory of Economics can be evaluated on the decision made by JB hi fi in

disclosing the downgrade in their profits during the fiscal year. From the evaluation point of you the decision made by JB Hi-Fi was

directly considered as an independent move where the organisation effectively complied with all the relevant regulations laid down

before conducting the announcement. Hence, the intervention of ASX was not needed as the overall profit downgrade was relatively

under the material disclosure limit. Therefore, it could be understood that under the measures of classical theory of Economics

organisation adequately portrayed free competition without the intervention of government regulations. Therefore, under the classical

political economy theory the decision made by JB Hi-Fi regarding the disclosure of the profit downgrade was adequate. the company

is able to disclose all the relevant information regarding their operations regardless of the intervention from governments, as it

complied with all the relevant regulations laid down by ASX. In this context, Onions & Schefold (2017) stated that with adequate

disclosure measure the organisation is able to minimise any kind of rumours that might hamper its share price and have impact on their

capital reserves.

The institutional theory directly indicates that organisation needs to follow the regulations structures and establishment that is

portrayed by regulator for depicting their social behaviour. the social behaviour of the organisation is essential as it delivers all the

relevant information to the stakeholders in accordance to the changes in its operations. according to the institutional theory company

has effectively portrayed all the relevant information to the ASX and investors where is no manipulation is being conducted by the

company. JB hi fi has relatively portrait the information in an adequate way, where no additional information was required as the

material impact was below 3%, as stated in the ASX regulations. Major compliance with all the relevant information directly indicates

the usefulness of institutional theory in detecting the major problems faced by the company. hence, it could be identified that under the

institutional theory measure JB hi fi has adequately complied with all the regulations laid down by ASX regarding the disclosure

measure of their profit downgrade (Willmott, 2018). Before after evaluating all the relevant evidence from the case study it will be

identified that JB hi fi has effectively followed all the relevant regulations before conducting the announcement. This relevantly

supports the measures drafted by institutional theory and indicates that the organisation has complied with all the regulations of ASX.

References:

Insert your references here, for example:

Onions, C. T., & Schefold, B. (2017). Essays on Piero Sraffa: Critical perspectives on the revival of classical theory.

Routledge.

Johnson, H. G. (2017). Macroeconomics and monetary theory. Routledge.

Greenwood, R., Oliver, C., Lawrence, T. B., & Meyer, R. E. (Eds.). (2017). The Sage handbook of organizational

institutionalism. Sage.

Willmott, H. (2018). Can It? On Expanding Institutional Theory by Disarming Critique. Journal of Management Inquiry,

1056492617744893.

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high

standard. Paragraphs are

coherently connected to each

other. Correct grammar, spelling

and punctuation.

Quality of writing is of a high

standard. Paragraphs are mostly

well structured. Few grammar,

spelling and punctuation mistakes.

Quality of writing is of a good

standard. Few grammar, spelling

and punctuation mistakes.

Some problems with sentence

structure and presentation

Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

Quality of writing is at a very poor

standard so barely

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

References:

Insert your references here, for example:

Onions, C. T., & Schefold, B. (2017). Essays on Piero Sraffa: Critical perspectives on the revival of classical theory.

Routledge.

Johnson, H. G. (2017). Macroeconomics and monetary theory. Routledge.

Greenwood, R., Oliver, C., Lawrence, T. B., & Meyer, R. E. (Eds.). (2017). The Sage handbook of organizational

institutionalism. Sage.

Willmott, H. (2018). Can It? On Expanding Institutional Theory by Disarming Critique. Journal of Management Inquiry,

1056492617744893.

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high

standard. Paragraphs are

coherently connected to each

other. Correct grammar, spelling

and punctuation.

Quality of writing is of a high

standard. Paragraphs are mostly

well structured. Few grammar,

spelling and punctuation mistakes.

Quality of writing is of a good

standard. Few grammar, spelling

and punctuation mistakes.

Some problems with sentence

structure and presentation

Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

Quality of writing is at a very poor

standard so barely

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 2: Use the Managerial branch of Stakeholder Theory to explain JB Hi-Fi’s reporting decisions. Make sure

you support your observations with evidence from the case study.

Answer: From the evaluation of managerial branch of stakeholder theory it could be identified that are relevant information needs to be

provided to stakeholders who can help the organization achieve their goals. The overall managerial branch of stakeholder theory

indicates the adequate information that needs to be provided to different level of stakeholders of the company depicting their progress.

Moreover, the theory effectively helps the organisation to manage specific stakeholder groups within the society for effectively

detecting the impact of disclosure policies on the market. Directly indicates that the organisation does not have to respond to all the

stakeholders equally instead which should segregate the stakeholders to identify the most powerful ones. this would eventually help

the organisation to understand the level of control over resources that is required by the organisation. Furthermore, it will be identified

that assessing the significance of stakeholder demand is a strategic move made by the organisation to fulfil its firm objective.

Additionally, the decision made by JB Hi-Fi regarding the profit downgrade announcement is relatively considered to be under the

managerial branch of stakeholder theory. the company has effectively disclosed all the relevant information to these specific

stakeholders during the conference by addressing the relevant problems faced by the organisation. This information is relatively

supporting the stakeholders such as to take adequate steps in valuing the company’s share price. The drastic decline in share price of

the company is also result of adequate announcements conducted by the company regarding the current financial position to the

adequate stakeholders (Poulton, Barnes & Clarke, 2017).

After while reading the case study it will be identified that the relevant information regarding the downgrade of Profits by 3% was

directly announced to the shareholders of the company. This information transfer was essential by the organisation for depicting

Problems related to future profit that will incur in the fiscal year. Furthermore, the information that is provided by the organisation was

adequate, while ASX indicated that a separate announcement needs to be conducted by the organisation to highlight the decline in

future profit. However, the mandate that was provided by ASX mainly instigated that if the overall material changes is higher than 5%

then adequate information needs to be delivered in a different announcement. moreover, if the impact is less than 5% then the

organisation is not viable to provide separate information or announcement to the shareholders and stakeholders of the organisation.

Hence, under the evaluation of stakeholder theory the decision made by JB hi fi for reporting the annual decline and profit was

adequate. The company adequately followed all the relevant information needed by the Stakeholders who are supporting the

organisation to achieve its goal (Kent & Zunker, 2017). Therefore, under managerial branch of stakeholder theory JB hi fi have

adequately provided all the relevant information to the stakeholders, who can help the organisation to achieve higher growth in future.

Investment executive such as Smith directly supported the operations of JB hi fi, which directly indicates that the information depicted

you support your observations with evidence from the case study.

Answer: From the evaluation of managerial branch of stakeholder theory it could be identified that are relevant information needs to be

provided to stakeholders who can help the organization achieve their goals. The overall managerial branch of stakeholder theory

indicates the adequate information that needs to be provided to different level of stakeholders of the company depicting their progress.

Moreover, the theory effectively helps the organisation to manage specific stakeholder groups within the society for effectively

detecting the impact of disclosure policies on the market. Directly indicates that the organisation does not have to respond to all the

stakeholders equally instead which should segregate the stakeholders to identify the most powerful ones. this would eventually help

the organisation to understand the level of control over resources that is required by the organisation. Furthermore, it will be identified

that assessing the significance of stakeholder demand is a strategic move made by the organisation to fulfil its firm objective.

Additionally, the decision made by JB Hi-Fi regarding the profit downgrade announcement is relatively considered to be under the

managerial branch of stakeholder theory. the company has effectively disclosed all the relevant information to these specific

stakeholders during the conference by addressing the relevant problems faced by the organisation. This information is relatively

supporting the stakeholders such as to take adequate steps in valuing the company’s share price. The drastic decline in share price of

the company is also result of adequate announcements conducted by the company regarding the current financial position to the

adequate stakeholders (Poulton, Barnes & Clarke, 2017).

After while reading the case study it will be identified that the relevant information regarding the downgrade of Profits by 3% was

directly announced to the shareholders of the company. This information transfer was essential by the organisation for depicting

Problems related to future profit that will incur in the fiscal year. Furthermore, the information that is provided by the organisation was

adequate, while ASX indicated that a separate announcement needs to be conducted by the organisation to highlight the decline in

future profit. However, the mandate that was provided by ASX mainly instigated that if the overall material changes is higher than 5%

then adequate information needs to be delivered in a different announcement. moreover, if the impact is less than 5% then the

organisation is not viable to provide separate information or announcement to the shareholders and stakeholders of the organisation.

Hence, under the evaluation of stakeholder theory the decision made by JB hi fi for reporting the annual decline and profit was

adequate. The company adequately followed all the relevant information needed by the Stakeholders who are supporting the

organisation to achieve its goal (Kent & Zunker, 2017). Therefore, under managerial branch of stakeholder theory JB hi fi have

adequately provided all the relevant information to the stakeholders, who can help the organisation to achieve higher growth in future.

Investment executive such as Smith directly supported the operations of JB hi fi, which directly indicates that the information depicted

by the organisation was adequately supported by the investors.

References:

Insert your references here, for example:

Kent, P., & Zunker, T. (2017). A stakeholder analysis of employee disclosures in annual reports. Accounting & Finance,

57(2), 533-563.

Poulton, E., Barnes, L., & Clarke, F. (2017). Disclosure and Reporting of Governance Practices by Australian Residential

Aged Care Providers: Accountability to Stakeholders.

Pérez, A., López, C., & García-De los Salmones, M. D. M. (2017). An empirical exploration of the link between reporting to

stakeholders and corporate social responsibility reputation in the Spanish context. Accounting, Auditing & Accountability

Journal, 30(3), 668-698.

Hussain, N., Rigoni, U., & Orij, R. P. (2018). Corporate governance and sustainability performance: Analysis of triple

bottom line performance. Journal of Business Ethics, 149(2), 411-432.

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high

standard. Paragraphs are

Quality of writing is of a high

standard. Paragraphs are mostly

Quality of writing is of a good

standard. Few grammar, spelling

Some problems with sentence

structure and presentation

Quality of writing is at a very poor

standard so barely

References:

Insert your references here, for example:

Kent, P., & Zunker, T. (2017). A stakeholder analysis of employee disclosures in annual reports. Accounting & Finance,

57(2), 533-563.

Poulton, E., Barnes, L., & Clarke, F. (2017). Disclosure and Reporting of Governance Practices by Australian Residential

Aged Care Providers: Accountability to Stakeholders.

Pérez, A., López, C., & García-De los Salmones, M. D. M. (2017). An empirical exploration of the link between reporting to

stakeholders and corporate social responsibility reputation in the Spanish context. Accounting, Auditing & Accountability

Journal, 30(3), 668-698.

Hussain, N., Rigoni, U., & Orij, R. P. (2018). Corporate governance and sustainability performance: Analysis of triple

bottom line performance. Journal of Business Ethics, 149(2), 411-432.

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high

standard. Paragraphs are

Quality of writing is of a high

standard. Paragraphs are mostly

Quality of writing is of a good

standard. Few grammar, spelling

Some problems with sentence

structure and presentation

Quality of writing is at a very poor

standard so barely

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

coherently connected to each

other. Correct grammar, spelling

and punctuation.

well structured. Few grammar,

spelling and punctuation mistakes.

and punctuation mistakes. Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

coherently connected to each

other. Correct grammar, spelling

and punctuation.

well structured. Few grammar,

spelling and punctuation mistakes.

and punctuation mistakes. Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3: To what extent do current share prices anticipate future earnings announcements? Use the case

study to support your answer.

Answer: The share price of the organisation relatively declined after the announcement of the profit downgrade, which was not

activated by JB hi fi. JB Hi-Fi directly indicated that the decline and share price was not anticipated by the organisation due to the low

impact of materiality on its profits. The organisation directly indicated that only 3% decline in its overall profit will income during the

fiscal year, which led to the mass panic among investors, who dumped all the relevant shares of the organisation to minimise the

negative impact on their investment capital. The continuation of the relevant decline and share price was mainly a signal from the

investors regarding the current evaluation of the organisation. Moreover, the share price of the company directly instigated the

relevant decline and its future learning that has been declared in the article. According to the case study, the share price of the

organisation fell up to 10% on a single day after the announcement was made by JB hi fi. This significant move was previously

conducted in 2011, where the organisations future was not certain. Therefore, the mass panic conducted by the investors directly

indicating the current financial position and share price valuation of the organisation. Moreover, from the evaluation of the share price

movement from the announcement date to the lowest point of the share it could be identified that the company share has been declined

from 25.7 per share to 22.05 per share. The anticipation of the investors regarding the future earnings announcement of the

organisation is effectively depicted with the help of current share price. Investors relatively use share price valuation to determine the

actual value of the organisation. Moreover, the decisions made by the organisation in the announcement relatively depicted the actual

valuation of the company, which was delivered by the change in its share price. In this context, Xu & Beck (2017) stated that

fundamental analysis uses financial report of the organisation to evaluate its future growth. On the other hand, Lee & Tong (2018)

argued that due to the limitations of fundamental analysis investors are not able to understand the level of changes in short term that

will is conducted in share price of the organisation.

Therefore, the current share price of JB hi fi is relatively putting the anticipated future earnings announcement of the organisation. The

company will eventually have a decline in its profits during the fiscal year, which will result in declining valuation of the organisation.

hence, the current decline in share price of the company relatively defected the future valuation of the organisation and the anticipation

of a declining profit. Thus, the change in share price is mainly estimated from the future progress and growth of the organisation, as

investor use different valuation models to detect the level of share price that is for the company. The decline in share price after the

announcement was mainly aggressive, which instigated wide spread panic among the investors. This is the main reason behind the

drastic fall in share price of JB Hi-Fi.

study to support your answer.

Answer: The share price of the organisation relatively declined after the announcement of the profit downgrade, which was not

activated by JB hi fi. JB Hi-Fi directly indicated that the decline and share price was not anticipated by the organisation due to the low

impact of materiality on its profits. The organisation directly indicated that only 3% decline in its overall profit will income during the

fiscal year, which led to the mass panic among investors, who dumped all the relevant shares of the organisation to minimise the

negative impact on their investment capital. The continuation of the relevant decline and share price was mainly a signal from the

investors regarding the current evaluation of the organisation. Moreover, the share price of the company directly instigated the

relevant decline and its future learning that has been declared in the article. According to the case study, the share price of the

organisation fell up to 10% on a single day after the announcement was made by JB hi fi. This significant move was previously

conducted in 2011, where the organisations future was not certain. Therefore, the mass panic conducted by the investors directly

indicating the current financial position and share price valuation of the organisation. Moreover, from the evaluation of the share price

movement from the announcement date to the lowest point of the share it could be identified that the company share has been declined

from 25.7 per share to 22.05 per share. The anticipation of the investors regarding the future earnings announcement of the

organisation is effectively depicted with the help of current share price. Investors relatively use share price valuation to determine the

actual value of the organisation. Moreover, the decisions made by the organisation in the announcement relatively depicted the actual

valuation of the company, which was delivered by the change in its share price. In this context, Xu & Beck (2017) stated that

fundamental analysis uses financial report of the organisation to evaluate its future growth. On the other hand, Lee & Tong (2018)

argued that due to the limitations of fundamental analysis investors are not able to understand the level of changes in short term that

will is conducted in share price of the organisation.

Therefore, the current share price of JB hi fi is relatively putting the anticipated future earnings announcement of the organisation. The

company will eventually have a decline in its profits during the fiscal year, which will result in declining valuation of the organisation.

hence, the current decline in share price of the company relatively defected the future valuation of the organisation and the anticipation

of a declining profit. Thus, the change in share price is mainly estimated from the future progress and growth of the organisation, as

investor use different valuation models to detect the level of share price that is for the company. The decline in share price after the

announcement was mainly aggressive, which instigated wide spread panic among the investors. This is the main reason behind the

drastic fall in share price of JB Hi-Fi.

References:

Insert your references here, for example:

Asx.com.au. (2018). Asx.com.au. Retrieved 30 May 2018, from

https://www.asx.com.au/asx/share-price-research/company/JBH

Lee, Y. T., & Tong, W. H. (2018). The impact of reporting frequency on the information quality of share price: evidence

from Chinese state-owned enterprises. Frontiers of Business Research in China, 12(1), 9.

Xu, D., & Beck, C. (2017). Symbolic dynamics techniques for complex systems: Application to share price dynamics. EPL

(Europhysics Letters), 118(3), 30001.

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high

standard. Paragraphs are

coherently connected to each

other. Correct grammar, spelling

and punctuation.

Quality of writing is of a high

standard. Paragraphs are mostly

well structured. Few grammar,

spelling and punctuation mistakes.

Quality of writing is of a good

standard. Few grammar, spelling

and punctuation mistakes.

Some problems with sentence

structure and presentation

Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

Quality of writing is at a very poor

standard so barely

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

Insert your references here, for example:

Asx.com.au. (2018). Asx.com.au. Retrieved 30 May 2018, from

https://www.asx.com.au/asx/share-price-research/company/JBH

Lee, Y. T., & Tong, W. H. (2018). The impact of reporting frequency on the information quality of share price: evidence

from Chinese state-owned enterprises. Frontiers of Business Research in China, 12(1), 9.

Xu, D., & Beck, C. (2017). Symbolic dynamics techniques for complex systems: Application to share price dynamics. EPL

(Europhysics Letters), 118(3), 30001.

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high

standard. Paragraphs are

coherently connected to each

other. Correct grammar, spelling

and punctuation.

Quality of writing is of a high

standard. Paragraphs are mostly

well structured. Few grammar,

spelling and punctuation mistakes.

Quality of writing is of a good

standard. Few grammar, spelling

and punctuation mistakes.

Some problems with sentence

structure and presentation

Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

Quality of writing is at a very poor

standard so barely

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

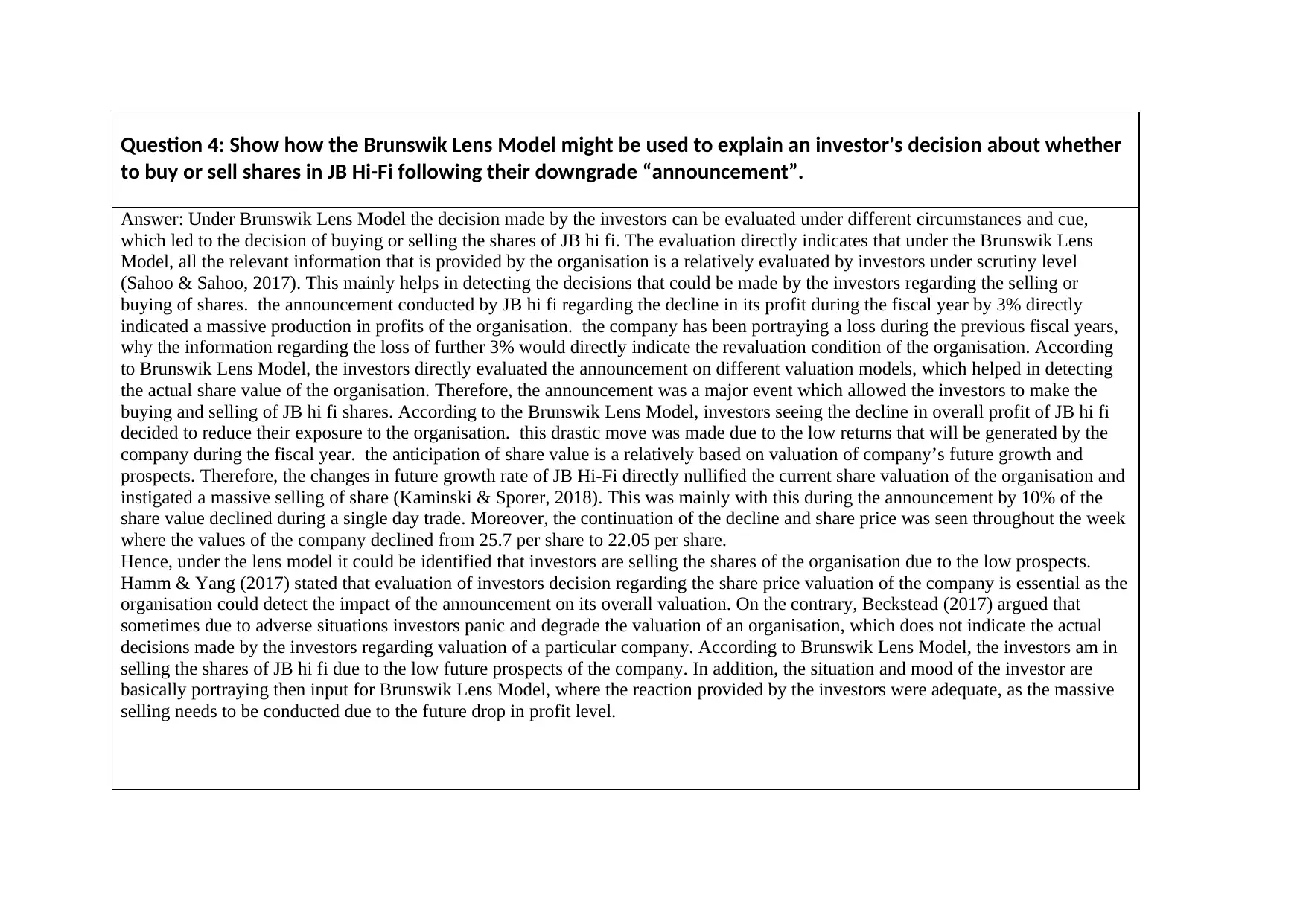

Question 4: Show how the Brunswik Lens Model might be used to explain an investor's decision about whether

to buy or sell shares in JB Hi-Fi following their downgrade “announcement”.

Answer: Under Brunswik Lens Model the decision made by the investors can be evaluated under different circumstances and cue,

which led to the decision of buying or selling the shares of JB hi fi. The evaluation directly indicates that under the Brunswik Lens

Model, all the relevant information that is provided by the organisation is a relatively evaluated by investors under scrutiny level

(Sahoo & Sahoo, 2017). This mainly helps in detecting the decisions that could be made by the investors regarding the selling or

buying of shares. the announcement conducted by JB hi fi regarding the decline in its profit during the fiscal year by 3% directly

indicated a massive production in profits of the organisation. the company has been portraying a loss during the previous fiscal years,

why the information regarding the loss of further 3% would directly indicate the revaluation condition of the organisation. According

to Brunswik Lens Model, the investors directly evaluated the announcement on different valuation models, which helped in detecting

the actual share value of the organisation. Therefore, the announcement was a major event which allowed the investors to make the

buying and selling of JB hi fi shares. According to the Brunswik Lens Model, investors seeing the decline in overall profit of JB hi fi

decided to reduce their exposure to the organisation. this drastic move was made due to the low returns that will be generated by the

company during the fiscal year. the anticipation of share value is a relatively based on valuation of company’s future growth and

prospects. Therefore, the changes in future growth rate of JB Hi-Fi directly nullified the current share valuation of the organisation and

instigated a massive selling of share (Kaminski & Sporer, 2018). This was mainly with this during the announcement by 10% of the

share value declined during a single day trade. Moreover, the continuation of the decline and share price was seen throughout the week

where the values of the company declined from 25.7 per share to 22.05 per share.

Hence, under the lens model it could be identified that investors are selling the shares of the organisation due to the low prospects.

Hamm & Yang (2017) stated that evaluation of investors decision regarding the share price valuation of the company is essential as the

organisation could detect the impact of the announcement on its overall valuation. On the contrary, Beckstead (2017) argued that

sometimes due to adverse situations investors panic and degrade the valuation of an organisation, which does not indicate the actual

decisions made by the investors regarding valuation of a particular company. According to Brunswik Lens Model, the investors am in

selling the shares of JB hi fi due to the low future prospects of the company. In addition, the situation and mood of the investor are

basically portraying then input for Brunswik Lens Model, where the reaction provided by the investors were adequate, as the massive

selling needs to be conducted due to the future drop in profit level.

to buy or sell shares in JB Hi-Fi following their downgrade “announcement”.

Answer: Under Brunswik Lens Model the decision made by the investors can be evaluated under different circumstances and cue,

which led to the decision of buying or selling the shares of JB hi fi. The evaluation directly indicates that under the Brunswik Lens

Model, all the relevant information that is provided by the organisation is a relatively evaluated by investors under scrutiny level

(Sahoo & Sahoo, 2017). This mainly helps in detecting the decisions that could be made by the investors regarding the selling or

buying of shares. the announcement conducted by JB hi fi regarding the decline in its profit during the fiscal year by 3% directly

indicated a massive production in profits of the organisation. the company has been portraying a loss during the previous fiscal years,

why the information regarding the loss of further 3% would directly indicate the revaluation condition of the organisation. According

to Brunswik Lens Model, the investors directly evaluated the announcement on different valuation models, which helped in detecting

the actual share value of the organisation. Therefore, the announcement was a major event which allowed the investors to make the

buying and selling of JB hi fi shares. According to the Brunswik Lens Model, investors seeing the decline in overall profit of JB hi fi

decided to reduce their exposure to the organisation. this drastic move was made due to the low returns that will be generated by the

company during the fiscal year. the anticipation of share value is a relatively based on valuation of company’s future growth and

prospects. Therefore, the changes in future growth rate of JB Hi-Fi directly nullified the current share valuation of the organisation and

instigated a massive selling of share (Kaminski & Sporer, 2018). This was mainly with this during the announcement by 10% of the

share value declined during a single day trade. Moreover, the continuation of the decline and share price was seen throughout the week

where the values of the company declined from 25.7 per share to 22.05 per share.

Hence, under the lens model it could be identified that investors are selling the shares of the organisation due to the low prospects.

Hamm & Yang (2017) stated that evaluation of investors decision regarding the share price valuation of the company is essential as the

organisation could detect the impact of the announcement on its overall valuation. On the contrary, Beckstead (2017) argued that

sometimes due to adverse situations investors panic and degrade the valuation of an organisation, which does not indicate the actual

decisions made by the investors regarding valuation of a particular company. According to Brunswik Lens Model, the investors am in

selling the shares of JB hi fi due to the low future prospects of the company. In addition, the situation and mood of the investor are

basically portraying then input for Brunswik Lens Model, where the reaction provided by the investors were adequate, as the massive

selling needs to be conducted due to the future drop in profit level.

References:

Insert your references here, for example:

Hamm, R. M., & Yang, H. (2017). Alternative lens model equations for dichotomous judgments about dichotomous criteria.

Journal of behavioral decision making, 30(2), 527-532.

Beckstead, J. W. (2017). The bifocal lens model and equation: Examining the linkage between clinical judgments and

decisions. Medical Decision Making, 37(1), 35-45.

Illingworth, D. A., Thomas, R. P., Rozga, A., & Smith, C. J. (2017, September). Cue Use in Distal Autism Spectrum

Assessment: A Lens Model Analysis of the Efficacy of Telehealth Technologies. In Proceedings of the Human Factors

and Ergonomics Society Annual Meeting (Vol. 61, No. 1, pp. 170-170). Sage CA: Los Angeles, CA: SAGE Publications.

Sahoo, F. M., & Sahoo, K. (2017). The perceived predictors of achievement in management students: An innovative use of

lens model. Journal of the Indian Academy of Applied Psychology, 43(1), 34.

Kaminski, K. S., & Sporer, S. L. (2018). Observer judgments of identification accuracy are affected by non‐valid cues: A

Brunswikian lens model analysis. European Journal of Social Psychology, 48(1), 47-61.

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high

standard. Paragraphs are

coherently connected to each

other. Correct grammar, spelling

and punctuation.

Quality of writing is of a high

standard. Paragraphs are mostly

well structured. Few grammar,

spelling and punctuation mistakes.

Quality of writing is of a good

standard. Few grammar, spelling

and punctuation mistakes.

Some problems with sentence

structure and presentation

Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

Quality of writing is at a very poor

standard so barely

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

Insert your references here, for example:

Hamm, R. M., & Yang, H. (2017). Alternative lens model equations for dichotomous judgments about dichotomous criteria.

Journal of behavioral decision making, 30(2), 527-532.

Beckstead, J. W. (2017). The bifocal lens model and equation: Examining the linkage between clinical judgments and

decisions. Medical Decision Making, 37(1), 35-45.

Illingworth, D. A., Thomas, R. P., Rozga, A., & Smith, C. J. (2017, September). Cue Use in Distal Autism Spectrum

Assessment: A Lens Model Analysis of the Efficacy of Telehealth Technologies. In Proceedings of the Human Factors

and Ergonomics Society Annual Meeting (Vol. 61, No. 1, pp. 170-170). Sage CA: Los Angeles, CA: SAGE Publications.

Sahoo, F. M., & Sahoo, K. (2017). The perceived predictors of achievement in management students: An innovative use of

lens model. Journal of the Indian Academy of Applied Psychology, 43(1), 34.

Kaminski, K. S., & Sporer, S. L. (2018). Observer judgments of identification accuracy are affected by non‐valid cues: A

Brunswikian lens model analysis. European Journal of Social Psychology, 48(1), 47-61.

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high

standard. Paragraphs are

coherently connected to each

other. Correct grammar, spelling

and punctuation.

Quality of writing is of a high

standard. Paragraphs are mostly

well structured. Few grammar,

spelling and punctuation mistakes.

Quality of writing is of a good

standard. Few grammar, spelling

and punctuation mistakes.

Some problems with sentence

structure and presentation

Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

Quality of writing is at a very poor

standard so barely

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 5: Some academics have criticised the accounting profession for acting to legitimise the capitalist

system (supposedly by supporting the “haves” against the “have nots”. Indicate whether the case study

supports the critical view of accounting, or whether it doesn’t. Use the case study to support your answer.

Answer: After conducting the adequate evaluation it could be identified that the case study effectively supports the critical view of

accounting, where it helps legitimise the capitalist system currently used by the organisation. The case study directly indicates the

relevant changes in accounting vegetables that is adopted by organisations to support its capitalist system. In the case study, the

evaluation used by JB hi fi for disclosing all the relevant information regarding its future growth in a relevant conference is directly

indicating the ways of capitalist system. The company directly indicated that relevant measures used by the accounting professionals

help in drafting the future profits of an organisation. Therefore. it could be understood that the case study directly supports the critical

view of accounting, where Accountants are conducting relevant legitimate action to accommodate the capitalist system within the

organisation. The disclosure that was made by the company was a relatively considered as a capital system which indicate future

growth rate of an organisation. Accounting professionals has effectively been using the accounting system to legitimacy capitalist

measures used by organisations. The critical view of accounting directly indicates that accounting is effectively made to support

operational capability of the company well discarding any kind of ethical measures for minimising the impact of capitalist system. The

system relatively uses different types of measures such as depreciation tax lineage impairment loss and other valuation methods to help

capital system to maximize their profits while minimising any kind of cash outflow. The accounting profession has helped the capitalist

system to flourish and maximize its profitability, by providing them with different types of loopholes for supporting their actions.

Therefore, the measures used by JB hi fi while disclosing the decline in its profits for the fiscal year is relatively indicating the

measures that was taken by accounting profession for legitimizing the capitalist system. Moreover, from the evaluation it could also be

identified that the case study supports all the relevant actions of capitalist system, which is entitled to improve their profits in future.

this relatively supports the haves against the have nots, as big corporations able to generate higher rate of returns while poor people are

deprived of the facilities. In this context, Matthews (2017) stated that the finical crisis can be identified as the relevant measure used by

accounting professional for legalising the actions of capitalist, where the unethical measure led to the financial crisis and liquidated

financial market of the world.

Thus, under the valuation it could be understood that the company will not provide high level of return during the fiscal year, which

will directly have the negative impact on share price of the company. Therefore, the intention of the company was to minimise the

negative impact of the profit downgrade on its hare price, as it was supported by Bruce one of the investment bankers. This relevantly

indicates that accounting professional directly help the organisation in their use to legitimate the capitalist ways. Consequently, the

actions of the organisation are considered capitalist, where it focuses on maximising their profits (Kamla & Haque, 2017).

system (supposedly by supporting the “haves” against the “have nots”. Indicate whether the case study

supports the critical view of accounting, or whether it doesn’t. Use the case study to support your answer.

Answer: After conducting the adequate evaluation it could be identified that the case study effectively supports the critical view of

accounting, where it helps legitimise the capitalist system currently used by the organisation. The case study directly indicates the

relevant changes in accounting vegetables that is adopted by organisations to support its capitalist system. In the case study, the

evaluation used by JB hi fi for disclosing all the relevant information regarding its future growth in a relevant conference is directly

indicating the ways of capitalist system. The company directly indicated that relevant measures used by the accounting professionals

help in drafting the future profits of an organisation. Therefore. it could be understood that the case study directly supports the critical

view of accounting, where Accountants are conducting relevant legitimate action to accommodate the capitalist system within the

organisation. The disclosure that was made by the company was a relatively considered as a capital system which indicate future

growth rate of an organisation. Accounting professionals has effectively been using the accounting system to legitimacy capitalist

measures used by organisations. The critical view of accounting directly indicates that accounting is effectively made to support

operational capability of the company well discarding any kind of ethical measures for minimising the impact of capitalist system. The

system relatively uses different types of measures such as depreciation tax lineage impairment loss and other valuation methods to help

capital system to maximize their profits while minimising any kind of cash outflow. The accounting profession has helped the capitalist

system to flourish and maximize its profitability, by providing them with different types of loopholes for supporting their actions.

Therefore, the measures used by JB hi fi while disclosing the decline in its profits for the fiscal year is relatively indicating the

measures that was taken by accounting profession for legitimizing the capitalist system. Moreover, from the evaluation it could also be

identified that the case study supports all the relevant actions of capitalist system, which is entitled to improve their profits in future.

this relatively supports the haves against the have nots, as big corporations able to generate higher rate of returns while poor people are

deprived of the facilities. In this context, Matthews (2017) stated that the finical crisis can be identified as the relevant measure used by

accounting professional for legalising the actions of capitalist, where the unethical measure led to the financial crisis and liquidated

financial market of the world.

Thus, under the valuation it could be understood that the company will not provide high level of return during the fiscal year, which

will directly have the negative impact on share price of the company. Therefore, the intention of the company was to minimise the

negative impact of the profit downgrade on its hare price, as it was supported by Bruce one of the investment bankers. This relevantly

indicates that accounting professional directly help the organisation in their use to legitimate the capitalist ways. Consequently, the

actions of the organisation are considered capitalist, where it focuses on maximising their profits (Kamla & Haque, 2017).

References:

Insert your references here, for example:

Alawattage, C., Wickramasinghe, D., & Uddin, S. (2017). Theorising management accounting practices in Less Developed

Countries. The Routledge Companion to Performance Management and Control.

Matthews, D. R. (2017). Accountants and the professional project. Accounting, Auditing & Accountability Journal, 30(2),

306-327.

Morales, J., & Sponem, S. (2017). You too can have a critical perspective! 25 years of Critical Perspectives on Accounting.

Critical Perspectives on Accounting, 43, 149-166.

Kamla, R., & Haque, F. (2017). Islamic accounting, neo-imperialism and identity staging: The Accounting and Auditing

Organization for Islamic Financial Institutions. Critical Perspectives on Accounting.

Lin, L. (2017). Institutional Problems for Chinese Environmental Accounting: Evidence from the Accounting Profession

(Doctoral dissertation, School of Management).

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high Quality of writing is of a high Quality of writing is of a good Some problems with sentence Quality of writing is at a very poor

Insert your references here, for example:

Alawattage, C., Wickramasinghe, D., & Uddin, S. (2017). Theorising management accounting practices in Less Developed

Countries. The Routledge Companion to Performance Management and Control.

Matthews, D. R. (2017). Accountants and the professional project. Accounting, Auditing & Accountability Journal, 30(2),

306-327.

Morales, J., & Sponem, S. (2017). You too can have a critical perspective! 25 years of Critical Perspectives on Accounting.

Critical Perspectives on Accounting, 43, 149-166.

Kamla, R., & Haque, F. (2017). Islamic accounting, neo-imperialism and identity staging: The Accounting and Auditing

Organization for Islamic Financial Institutions. Critical Perspectives on Accounting.

Lin, L. (2017). Institutional Problems for Chinese Environmental Accounting: Evidence from the Accounting Profession

(Doctoral dissertation, School of Management).

Marker’s Comments: The marker will provide feedback here. Mark (10):

0

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

Demonstrates a balanced and very

high level of detailed knowledge of

core concepts by providing a very

high level of analysis. Utilises

current, appropriate and credible

sources.

Demonstrates a balanced and high

level of knowledge of core

concepts by providing a high level

of analysis. Utilises mostly current,

appropriate and credible sources.

Demonstrates a good level of

knowledge of some of the core

concepts by providing some level

of analysis. Utilises some current,

appropriate and credible sources.

Demonstrates limited knowledge of

core concepts by providing a

limited level of analysis. Utilises

few current, appropriate and

credible sources.

Demonstrates little, if any,

knowledge of the core concepts

with extremely limited, if any,

analysis. Utilises little, if any,

current, appropriate and credible

sources.

Quality of writing at a very high Quality of writing is of a high Quality of writing is of a good Some problems with sentence Quality of writing is at a very poor

Exceeds Expectations

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

standard. Paragraphs are

coherently connected to each

other. Correct grammar, spelling

and punctuation.

standard. Paragraphs are mostly

well structured. Few grammar,

spelling and punctuation mistakes.

standard. Few grammar, spelling

and punctuation mistakes.

structure and presentation

Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

standard so barely

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

(High Distinction) 85-100%

Exceeds Expectations

(Distinction) 75 - 84%

Meets Expectations

(Credit) 65 – 74%

Meets Expectations

(Pass) 50 – 64%

Below Expectations

(Fail) below 50%

standard. Paragraphs are

coherently connected to each

other. Correct grammar, spelling

and punctuation.

standard. Paragraphs are mostly

well structured. Few grammar,

spelling and punctuation mistakes.

standard. Few grammar, spelling

and punctuation mistakes.

structure and presentation

Frequent grammar, punctuation

and spelling mistakes. Use of

inappropriate language.

standard so barely

understandable. Many spelling

mistakes. Little or no evidence of

proof reading.

The assessment presents a

detailed and focused summary of

the ideas presented; drawing clear

and well thought-out conclusions.

The assessment presents a fairly

detailed and focused summary of

the ideas presented; drawing fairly

clear and well thought-out

conclusions.

The assessment presents a

somewhat detailed and focused

summary of the ideas presented;

providing some evidence of

conclusions.

The assessment provides limited

detail with no clear summary of the

ideas presented; drawing limited

conclusions.

The assessment fails to provide

any clear evidence of the ideas

presented; drawing no clear

conclusions.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.